BSBRSK401/FNSRSK502: Risk Management Assessment - Finance Industry

VerifiedAdded on 2023/04/22

|13

|3231

|397

Homework Assignment

AI Summary

This document presents a comprehensive risk management assessment completed for the AAMC Training Group. It encompasses various tasks, including written activities that define risk categories and the risk management process, and a project requiring the identification and explanation of risks in the finance industry, considering both internal and external stakeholders. The assessment also features a case study analyzing potential risks for a finance broking business and its clients, followed by the development of an action plan to address a specific risk. The document demonstrates an understanding of the Australian Standard AS/NZS ISO 31000:2009, providing principles and guidelines for risk management. The assessment covers critical aspects of risk management in the finance sector, such as credit risk, regulatory risk, and marketing risks, and explores how to mitigate and manage them effectively.

Risk Management Assessment

Assessment cover sheet

In order for your assessment to be marked you must complete and upload all tasks

and this cover sheet via the AAMC Training Group portal. Your assessment tasks must

be uploaded in an electronic format i.e. Word, Excel, PDF or Scan. A maximum of five (5)

attachments (maximum 20MB each) can be uploaded for this assessment. Please see the

step-by-step instructions in your Member Area on how to upload assessments.

Student details

Course name

Assessment name Risk Management Assessment

Surname Given name

Address Postcode

Email

Phone Phone (other)

Current occupation

Industry Years in industry

When you upload your assessment you will be asked to confirm that your assessment

submission to AAMC Training is your own work and NOT the result of plagiarism or excessive

collaboration, and that all material used from any third party has been identified and

referenced appropriately. AAMC Training may conduct independent evaluation checks and

contact your supervisor to discuss your assessment.

Checklist of attachments:

☐ Task 1 – Written activities

☐ Task 2 – Project

☐ Task 3 – Case study 1

☐ Task 4 – Report

☐ Task 5 – Case Study 2

Please indicate style of course undertaken:

☐ Face to face Trainer’s name:

☐ Correspondence ☐ Online

Once your assessment has been successfully uploaded it will be pending review with your

nominated course assessor. Your assessor will mark your assessment and you will receive an

email advising you if you have been assessed as satisfactory. If you are marked as not yet

satisfactory you will be contacted and asked to provide additional information or re-visit the

assessment and re-upload your amended case study or written tasks.

Please contact us if you need assistance with your assessment:

Office: +61 (03) 9391 3643 / +61 (0)8 9344 4088 Email: info@aamctraining.edu.au

Assessment V2.3 © AAMC Training Group A1

Assessment cover sheet

In order for your assessment to be marked you must complete and upload all tasks

and this cover sheet via the AAMC Training Group portal. Your assessment tasks must

be uploaded in an electronic format i.e. Word, Excel, PDF or Scan. A maximum of five (5)

attachments (maximum 20MB each) can be uploaded for this assessment. Please see the

step-by-step instructions in your Member Area on how to upload assessments.

Student details

Course name

Assessment name Risk Management Assessment

Surname Given name

Address Postcode

Phone Phone (other)

Current occupation

Industry Years in industry

When you upload your assessment you will be asked to confirm that your assessment

submission to AAMC Training is your own work and NOT the result of plagiarism or excessive

collaboration, and that all material used from any third party has been identified and

referenced appropriately. AAMC Training may conduct independent evaluation checks and

contact your supervisor to discuss your assessment.

Checklist of attachments:

☐ Task 1 – Written activities

☐ Task 2 – Project

☐ Task 3 – Case study 1

☐ Task 4 – Report

☐ Task 5 – Case Study 2

Please indicate style of course undertaken:

☐ Face to face Trainer’s name:

☐ Correspondence ☐ Online

Once your assessment has been successfully uploaded it will be pending review with your

nominated course assessor. Your assessor will mark your assessment and you will receive an

email advising you if you have been assessed as satisfactory. If you are marked as not yet

satisfactory you will be contacted and asked to provide additional information or re-visit the

assessment and re-upload your amended case study or written tasks.

Please contact us if you need assistance with your assessment:

Office: +61 (03) 9391 3643 / +61 (0)8 9344 4088 Email: info@aamctraining.edu.au

Assessment V2.3 © AAMC Training Group A1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Risk Management Assessment

RISK MANAGEMENT ASSESSMENT TASKS

CREDIT TRANSFER

You may be able to claim credit transfer for a unit/s of competency that you have previously

completed with AAMC Training or another RTO. If you have been awarded a record of result

or statement of attainment for any of the units detailed below then please go to the Credit

Transfer tab in your Learning Centre and follow the prompts.

This assessment relates to the following units of competency:

BSBRSK401 Identify risk and apply risk management processes

FNSRSK502 Assess risk

Please refer to AAMC Training’s full Recognition Policy for further details.

IMPORTANT INSTRUCTIONS

Your answers to each of the tasks are to be typed into this document or supplied

electronically and uploaded.

No assessment word count has been specified although you are expected to provide good

quality answers to each of the questions.

Although some general discussion between students covering the assessment is allowed

your responses to each of the questions must be an individual effort.

PLEASE NOTE: AAMC Training only wants to see your own work. Please do not upload

parts of the learning guide or instructions on how to complete. When this extra information

is uploaded it presents unnecessary work for the assessors and in turn delays our

assessment responses.

Task 1 – Written activities

1. Name the two categories of risk.

1

2

2. Pure risk or speculative risk—which one can usually be mitigated by transferring the risk

to another party i.e. insurance company?

Click here to enter text.

3. What are the four steps in the risk management process?

1.

2.

3.

4.

A2 © AAMC Training Group Assessment V2.3

RISK MANAGEMENT ASSESSMENT TASKS

CREDIT TRANSFER

You may be able to claim credit transfer for a unit/s of competency that you have previously

completed with AAMC Training or another RTO. If you have been awarded a record of result

or statement of attainment for any of the units detailed below then please go to the Credit

Transfer tab in your Learning Centre and follow the prompts.

This assessment relates to the following units of competency:

BSBRSK401 Identify risk and apply risk management processes

FNSRSK502 Assess risk

Please refer to AAMC Training’s full Recognition Policy for further details.

IMPORTANT INSTRUCTIONS

Your answers to each of the tasks are to be typed into this document or supplied

electronically and uploaded.

No assessment word count has been specified although you are expected to provide good

quality answers to each of the questions.

Although some general discussion between students covering the assessment is allowed

your responses to each of the questions must be an individual effort.

PLEASE NOTE: AAMC Training only wants to see your own work. Please do not upload

parts of the learning guide or instructions on how to complete. When this extra information

is uploaded it presents unnecessary work for the assessors and in turn delays our

assessment responses.

Task 1 – Written activities

1. Name the two categories of risk.

1

2

2. Pure risk or speculative risk—which one can usually be mitigated by transferring the risk

to another party i.e. insurance company?

Click here to enter text.

3. What are the four steps in the risk management process?

1.

2.

3.

4.

A2 © AAMC Training Group Assessment V2.3

Risk Management Assessment

4. In assessing credit risk from a single borrower, a lender must consider what three issues?

1.

2.

3.

5. The seven Cs analysis frame work is the most common of all expert systems. It involves

examining the borrower using the seven key principles in lending; list them.

1.

2.

3.

4.

5.

6.

7.

6. What are the more common types of security?

Click here to enter text.

7. What does the PARSER analysis method consider?

Click here to enter text.

Assessment V2.3 © AAMC Training Group A3

4. In assessing credit risk from a single borrower, a lender must consider what three issues?

1.

2.

3.

5. The seven Cs analysis frame work is the most common of all expert systems. It involves

examining the borrower using the seven key principles in lending; list them.

1.

2.

3.

4.

5.

6.

7.

6. What are the more common types of security?

Click here to enter text.

7. What does the PARSER analysis method consider?

Click here to enter text.

Assessment V2.3 © AAMC Training Group A3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Risk Management Assessment

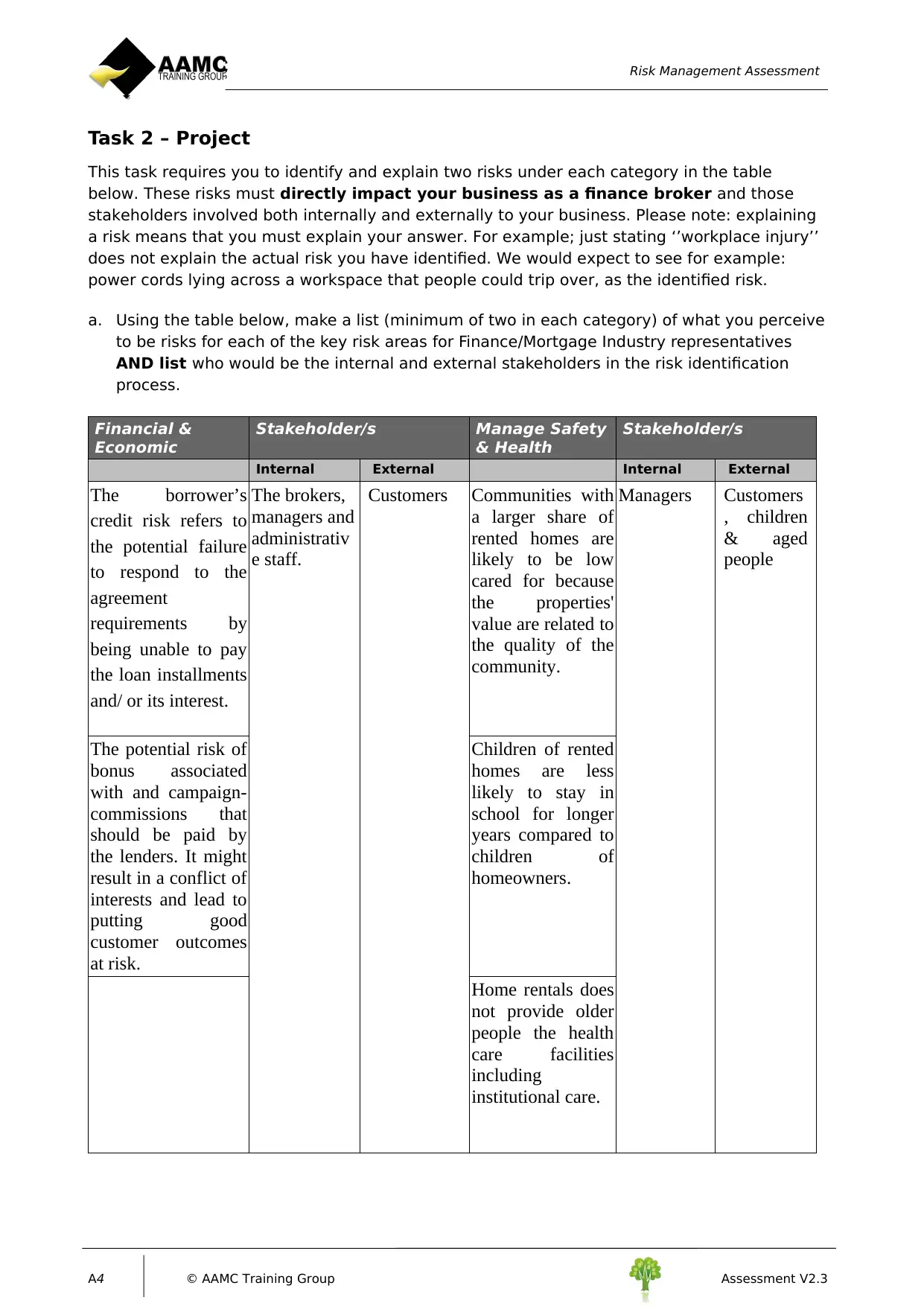

Task 2 – Project

This task requires you to identify and explain two risks under each category in the table

below. These risks must directly impact your business as a finance broker and those

stakeholders involved both internally and externally to your business. Please note: explaining

a risk means that you must explain your answer. For example; just stating ‘’workplace injury’’

does not explain the actual risk you have identified. We would expect to see for example:

power cords lying across a workspace that people could trip over, as the identified risk.

a. Using the table below, make a list (minimum of two in each category) of what you perceive

to be risks for each of the key risk areas for Finance/Mortgage Industry representatives

AND list who would be the internal and external stakeholders in the risk identification

process.

Financial &

Economic

Stakeholder/s Manage Safety

& Health

Stakeholder/s

Internal External Internal External

The borrower’s

credit risk refers to

the potential failure

to respond to the

agreement

requirements by

being unable to pay

the loan installments

and/ or its interest.

The brokers,

managers and

administrativ

e staff.

Customers Communities with

a larger share of

rented homes are

likely to be low

cared for because

the properties'

value are related to

the quality of the

community.

Managers Customers

, children

& aged

people

The potential risk of

bonus associated

with and campaign-

commissions that

should be paid by

the lenders. It might

result in a conflict of

interests and lead to

putting good

customer outcomes

at risk.

Children of rented

homes are less

likely to stay in

school for longer

years compared to

children of

homeowners.

Home rentals does

not provide older

people the health

care facilities

including

institutional care.

A4 © AAMC Training Group Assessment V2.3

Task 2 – Project

This task requires you to identify and explain two risks under each category in the table

below. These risks must directly impact your business as a finance broker and those

stakeholders involved both internally and externally to your business. Please note: explaining

a risk means that you must explain your answer. For example; just stating ‘’workplace injury’’

does not explain the actual risk you have identified. We would expect to see for example:

power cords lying across a workspace that people could trip over, as the identified risk.

a. Using the table below, make a list (minimum of two in each category) of what you perceive

to be risks for each of the key risk areas for Finance/Mortgage Industry representatives

AND list who would be the internal and external stakeholders in the risk identification

process.

Financial &

Economic

Stakeholder/s Manage Safety

& Health

Stakeholder/s

Internal External Internal External

The borrower’s

credit risk refers to

the potential failure

to respond to the

agreement

requirements by

being unable to pay

the loan installments

and/ or its interest.

The brokers,

managers and

administrativ

e staff.

Customers Communities with

a larger share of

rented homes are

likely to be low

cared for because

the properties'

value are related to

the quality of the

community.

Managers Customers

, children

& aged

people

The potential risk of

bonus associated

with and campaign-

commissions that

should be paid by

the lenders. It might

result in a conflict of

interests and lead to

putting good

customer outcomes

at risk.

Children of rented

homes are less

likely to stay in

school for longer

years compared to

children of

homeowners.

Home rentals does

not provide older

people the health

care facilities

including

institutional care.

A4 © AAMC Training Group Assessment V2.3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Risk Management Assessment

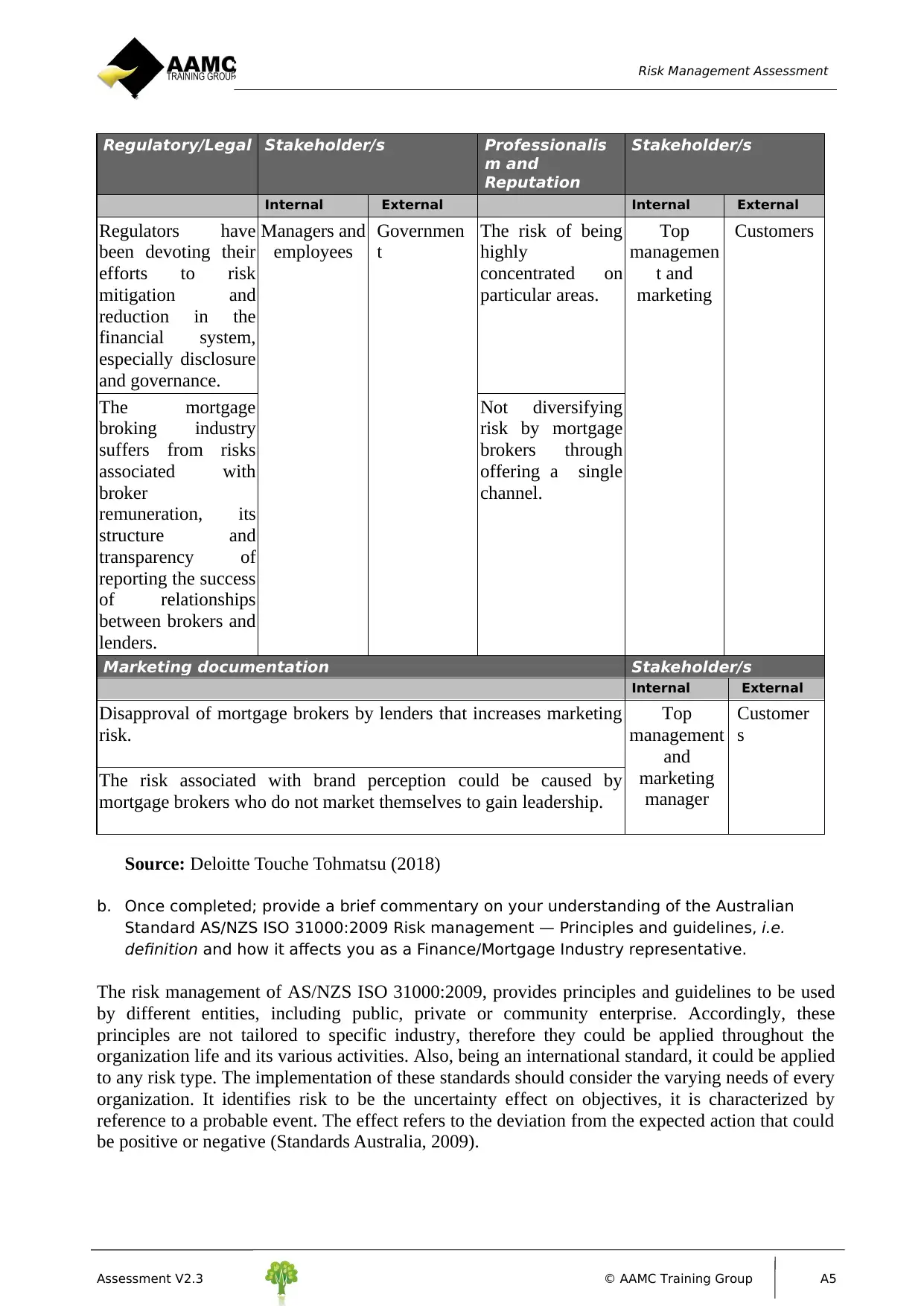

Regulatory/Legal Stakeholder/s Professionalis

m and

Reputation

Stakeholder/s

Internal External Internal External

Regulators have

been devoting their

efforts to risk

mitigation and

reduction in the

financial system,

especially disclosure

and governance.

Managers and

employees

Governmen

t

The risk of being

highly

concentrated on

particular areas.

Top

managemen

t and

marketing

Customers

The mortgage

broking industry

suffers from risks

associated with

broker

remuneration, its

structure and

transparency of

reporting the success

of relationships

between brokers and

lenders.

Not diversifying

risk by mortgage

brokers through

offering a single

channel.

Marketing documentation Stakeholder/s

Internal External

Disapproval of mortgage brokers by lenders that increases marketing

risk.

Top

management

and

marketing

manager

Customer

s

The risk associated with brand perception could be caused by

mortgage brokers who do not market themselves to gain leadership.

Source: Deloitte Touche Tohmatsu (2018)

b. Once completed; provide a brief commentary on your understanding of the Australian

Standard AS/NZS ISO 31000:2009 Risk management — Principles and guidelines, i.e.

definition and how it affects you as a Finance/Mortgage Industry representative.

The risk management of AS/NZS ISO 31000:2009, provides principles and guidelines to be used

by different entities, including public, private or community enterprise. Accordingly, these

principles are not tailored to specific industry, therefore they could be applied throughout the

organization life and its various activities. Also, being an international standard, it could be applied

to any risk type. The implementation of these standards should consider the varying needs of every

organization. It identifies risk to be the uncertainty effect on objectives, it is characterized by

reference to a probable event. The effect refers to the deviation from the expected action that could

be positive or negative (Standards Australia, 2009).

Assessment V2.3 © AAMC Training Group A5

Regulatory/Legal Stakeholder/s Professionalis

m and

Reputation

Stakeholder/s

Internal External Internal External

Regulators have

been devoting their

efforts to risk

mitigation and

reduction in the

financial system,

especially disclosure

and governance.

Managers and

employees

Governmen

t

The risk of being

highly

concentrated on

particular areas.

Top

managemen

t and

marketing

Customers

The mortgage

broking industry

suffers from risks

associated with

broker

remuneration, its

structure and

transparency of

reporting the success

of relationships

between brokers and

lenders.

Not diversifying

risk by mortgage

brokers through

offering a single

channel.

Marketing documentation Stakeholder/s

Internal External

Disapproval of mortgage brokers by lenders that increases marketing

risk.

Top

management

and

marketing

manager

Customer

s

The risk associated with brand perception could be caused by

mortgage brokers who do not market themselves to gain leadership.

Source: Deloitte Touche Tohmatsu (2018)

b. Once completed; provide a brief commentary on your understanding of the Australian

Standard AS/NZS ISO 31000:2009 Risk management — Principles and guidelines, i.e.

definition and how it affects you as a Finance/Mortgage Industry representative.

The risk management of AS/NZS ISO 31000:2009, provides principles and guidelines to be used

by different entities, including public, private or community enterprise. Accordingly, these

principles are not tailored to specific industry, therefore they could be applied throughout the

organization life and its various activities. Also, being an international standard, it could be applied

to any risk type. The implementation of these standards should consider the varying needs of every

organization. It identifies risk to be the uncertainty effect on objectives, it is characterized by

reference to a probable event. The effect refers to the deviation from the expected action that could

be positive or negative (Standards Australia, 2009).

Assessment V2.3 © AAMC Training Group A5

Risk Management Assessment

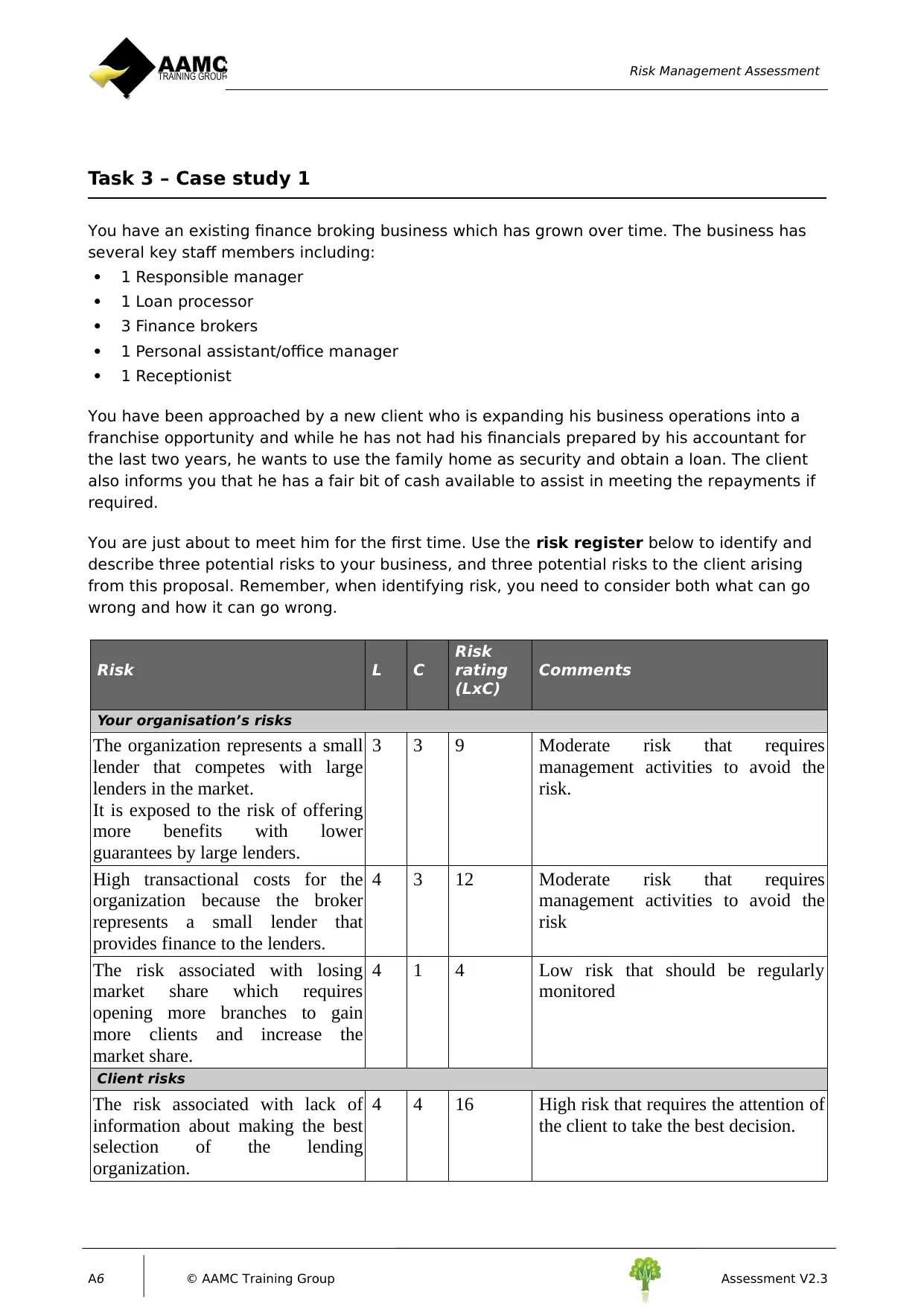

Task 3 – Case study 1

You have an existing finance broking business which has grown over time. The business has

several key staff members including:

1 Responsible manager

1 Loan processor

3 Finance brokers

1 Personal assistant/office manager

1 Receptionist

You have been approached by a new client who is expanding his business operations into a

franchise opportunity and while he has not had his financials prepared by his accountant for

the last two years, he wants to use the family home as security and obtain a loan. The client

also informs you that he has a fair bit of cash available to assist in meeting the repayments if

required.

You are just about to meet him for the first time. Use the risk register below to identify and

describe three potential risks to your business, and three potential risks to the client arising

from this proposal. Remember, when identifying risk, you need to consider both what can go

wrong and how it can go wrong.

Risk L C

Risk

rating

(LxC)

Comments

Your organisation’s risks

The organization represents a small

lender that competes with large

lenders in the market.

It is exposed to the risk of offering

more benefits with lower

guarantees by large lenders.

3 3 9 Moderate risk that requires

management activities to avoid the

risk.

High transactional costs for the

organization because the broker

represents a small lender that

provides finance to the lenders.

4 3 12 Moderate risk that requires

management activities to avoid the

risk

The risk associated with losing

market share which requires

opening more branches to gain

more clients and increase the

market share.

4 1 4 Low risk that should be regularly

monitored

Client risks

The risk associated with lack of

information about making the best

selection of the lending

organization.

4 4 16 High risk that requires the attention of

the client to take the best decision.

A6 © AAMC Training Group Assessment V2.3

Task 3 – Case study 1

You have an existing finance broking business which has grown over time. The business has

several key staff members including:

1 Responsible manager

1 Loan processor

3 Finance brokers

1 Personal assistant/office manager

1 Receptionist

You have been approached by a new client who is expanding his business operations into a

franchise opportunity and while he has not had his financials prepared by his accountant for

the last two years, he wants to use the family home as security and obtain a loan. The client

also informs you that he has a fair bit of cash available to assist in meeting the repayments if

required.

You are just about to meet him for the first time. Use the risk register below to identify and

describe three potential risks to your business, and three potential risks to the client arising

from this proposal. Remember, when identifying risk, you need to consider both what can go

wrong and how it can go wrong.

Risk L C

Risk

rating

(LxC)

Comments

Your organisation’s risks

The organization represents a small

lender that competes with large

lenders in the market.

It is exposed to the risk of offering

more benefits with lower

guarantees by large lenders.

3 3 9 Moderate risk that requires

management activities to avoid the

risk.

High transactional costs for the

organization because the broker

represents a small lender that

provides finance to the lenders.

4 3 12 Moderate risk that requires

management activities to avoid the

risk

The risk associated with losing

market share which requires

opening more branches to gain

more clients and increase the

market share.

4 1 4 Low risk that should be regularly

monitored

Client risks

The risk associated with lack of

information about making the best

selection of the lending

organization.

4 4 16 High risk that requires the attention of

the client to take the best decision.

A6 © AAMC Training Group Assessment V2.3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Risk Management Assessment

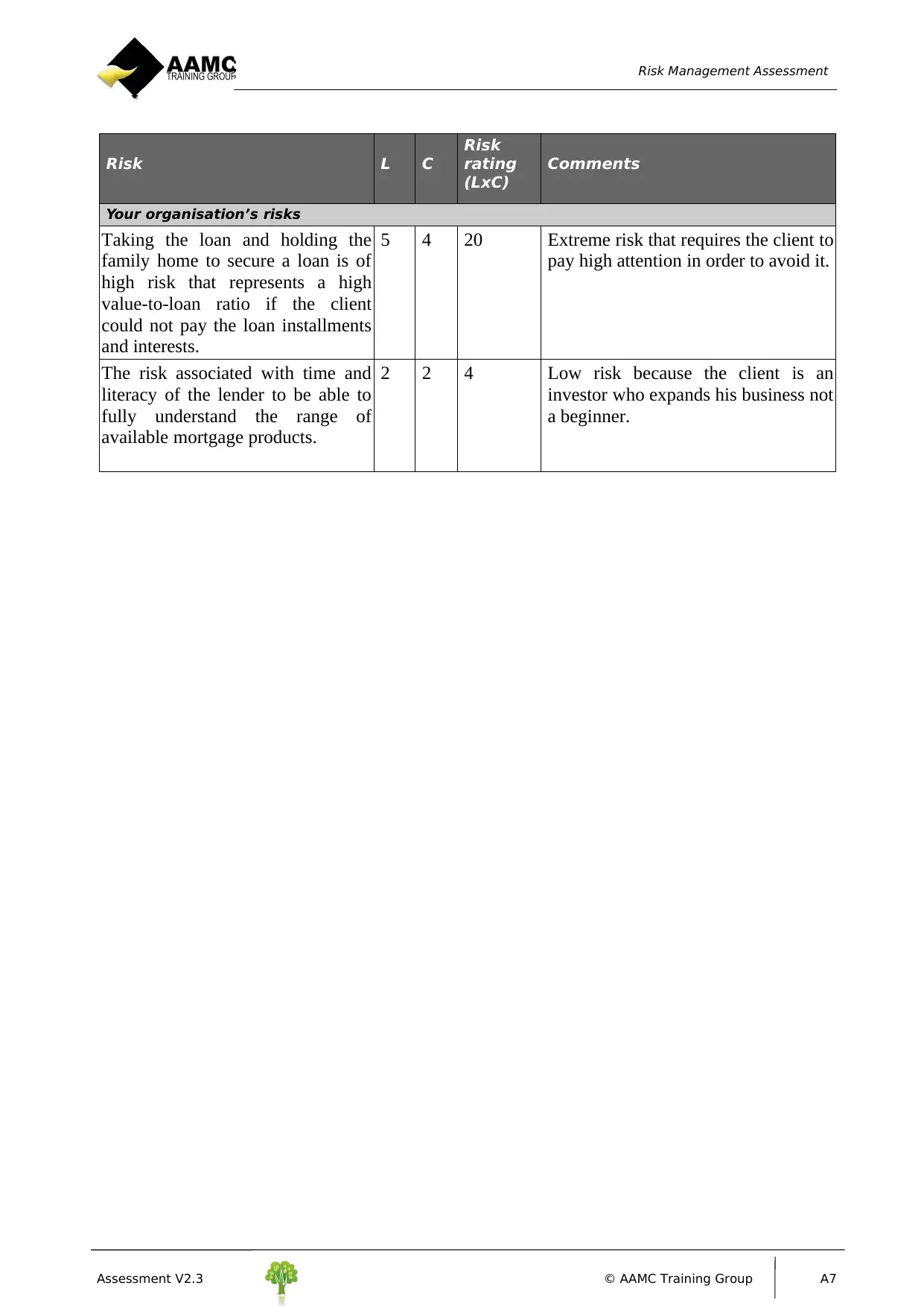

Risk L C

Risk

rating

(LxC)

Comments

Your organisation’s risks

Taking the loan and holding the

family home to secure a loan is of

high risk that represents a high

value-to-loan ratio if the client

could not pay the loan installments

and interests.

5 4 20 Extreme risk that requires the client to

pay high attention in order to avoid it.

The risk associated with time and

literacy of the lender to be able to

fully understand the range of

available mortgage products.

2 2 4 Low risk because the client is an

investor who expands his business not

a beginner.

Assessment V2.3 © AAMC Training Group A7

Risk L C

Risk

rating

(LxC)

Comments

Your organisation’s risks

Taking the loan and holding the

family home to secure a loan is of

high risk that represents a high

value-to-loan ratio if the client

could not pay the loan installments

and interests.

5 4 20 Extreme risk that requires the client to

pay high attention in order to avoid it.

The risk associated with time and

literacy of the lender to be able to

fully understand the range of

available mortgage products.

2 2 4 Low risk because the client is an

investor who expands his business not

a beginner.

Assessment V2.3 © AAMC Training Group A7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Risk Management Assessment

Task 4 – Report

Using the activity in Task 3 – Case Study 1, complete the following template. Select one of

the risks from the risk register and develop an action plan for dealing with this risk. Consider

all of the members in your business and how they may play a role in the various areas listed

in the plan. Remember a preventative action is one that should stop the risk from occurring

and corrective actions need to be considered after the risk has occurred to stop it from

happening again. Monitoring and review actions are important to ensure that the business is

regularly checking their processes to prevent reoccurrences of the risk.

Risk Item no 1 Describe risk item The organization represents a small lender

that competes with large lenders in the

market. It is exposed to the risk of offering

more benefits with lower guarantees by large

lenders.

Responsible area The organization

Initial assessment Likelihood Consequence Rating

3 3 9= Moderate risk

A8 © AAMC Training Group Assessment V2.3

Task 4 – Report

Using the activity in Task 3 – Case Study 1, complete the following template. Select one of

the risks from the risk register and develop an action plan for dealing with this risk. Consider

all of the members in your business and how they may play a role in the various areas listed

in the plan. Remember a preventative action is one that should stop the risk from occurring

and corrective actions need to be considered after the risk has occurred to stop it from

happening again. Monitoring and review actions are important to ensure that the business is

regularly checking their processes to prevent reoccurrences of the risk.

Risk Item no 1 Describe risk item The organization represents a small lender

that competes with large lenders in the

market. It is exposed to the risk of offering

more benefits with lower guarantees by large

lenders.

Responsible area The organization

Initial assessment Likelihood Consequence Rating

3 3 9= Moderate risk

A8 © AAMC Training Group Assessment V2.3

Risk Management Assessment

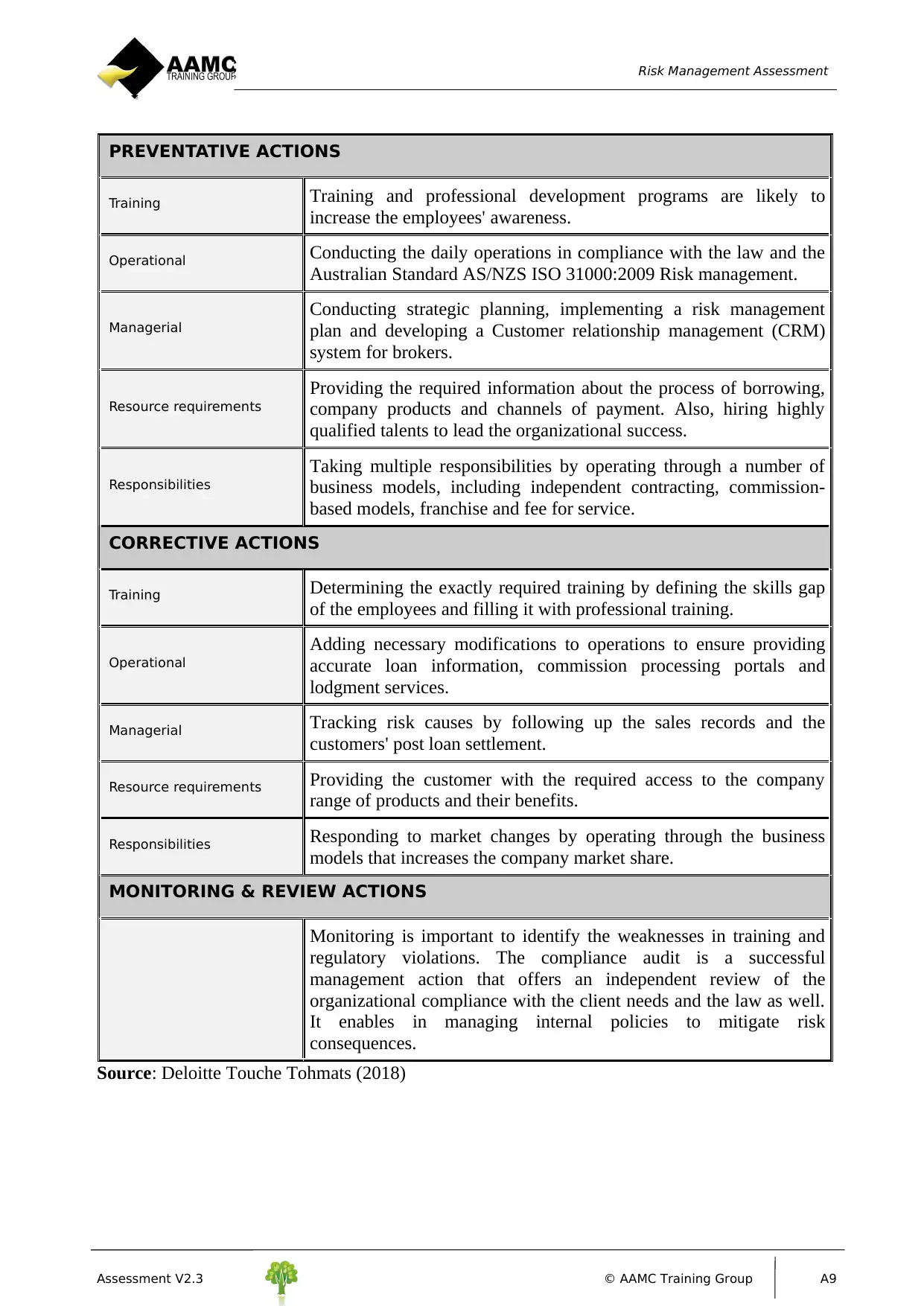

PREVENTATIVE ACTIONS

Training Training and professional development programs are likely to

increase the employees' awareness.

Operational Conducting the daily operations in compliance with the law and the

Australian Standard AS/NZS ISO 31000:2009 Risk management.

Managerial

Conducting strategic planning, implementing a risk management

plan and developing a Customer relationship management (CRM)

system for brokers.

Resource requirements

Providing the required information about the process of borrowing,

company products and channels of payment. Also, hiring highly

qualified talents to lead the organizational success.

Responsibilities

Taking multiple responsibilities by operating through a number of

business models, including independent contracting, commission-

based models, franchise and fee for service.

CORRECTIVE ACTIONS

Training Determining the exactly required training by defining the skills gap

of the employees and filling it with professional training.

Operational

Adding necessary modifications to operations to ensure providing

accurate loan information, commission processing portals and

lodgment services.

Managerial Tracking risk causes by following up the sales records and the

customers' post loan settlement.

Resource requirements Providing the customer with the required access to the company

range of products and their benefits.

Responsibilities Responding to market changes by operating through the business

models that increases the company market share.

MONITORING & REVIEW ACTIONS

Monitoring is important to identify the weaknesses in training and

regulatory violations. The compliance audit is a successful

management action that offers an independent review of the

organizational compliance with the client needs and the law as well.

It enables in managing internal policies to mitigate risk

consequences.

Source: Deloitte Touche Tohmats (2018)

Assessment V2.3 © AAMC Training Group A9

PREVENTATIVE ACTIONS

Training Training and professional development programs are likely to

increase the employees' awareness.

Operational Conducting the daily operations in compliance with the law and the

Australian Standard AS/NZS ISO 31000:2009 Risk management.

Managerial

Conducting strategic planning, implementing a risk management

plan and developing a Customer relationship management (CRM)

system for brokers.

Resource requirements

Providing the required information about the process of borrowing,

company products and channels of payment. Also, hiring highly

qualified talents to lead the organizational success.

Responsibilities

Taking multiple responsibilities by operating through a number of

business models, including independent contracting, commission-

based models, franchise and fee for service.

CORRECTIVE ACTIONS

Training Determining the exactly required training by defining the skills gap

of the employees and filling it with professional training.

Operational

Adding necessary modifications to operations to ensure providing

accurate loan information, commission processing portals and

lodgment services.

Managerial Tracking risk causes by following up the sales records and the

customers' post loan settlement.

Resource requirements Providing the customer with the required access to the company

range of products and their benefits.

Responsibilities Responding to market changes by operating through the business

models that increases the company market share.

MONITORING & REVIEW ACTIONS

Monitoring is important to identify the weaknesses in training and

regulatory violations. The compliance audit is a successful

management action that offers an independent review of the

organizational compliance with the client needs and the law as well.

It enables in managing internal policies to mitigate risk

consequences.

Source: Deloitte Touche Tohmats (2018)

Assessment V2.3 © AAMC Training Group A9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Risk Management Assessment

Task 5 – Case study 2

In this Case Study you are the credit assessor for ABank. In your role as the credit assessor

you are required to determine the risks associated with the scenario below. The following

information is from a loan application submitted to ABank by an authorised credit

representative:

Applicant Single male applicant (29 years of age).

Loan Details and

Purpose

Applicant wants to buy an investment property for $450,000 and

borrow $405,000 plus LMI. A loan term of 15 years is requested with an

Interest Only product.

The Loan to Value Ratio (LVR is 90.00%);

Credit History Applicant has 3 Consumer Payments Defaults listed in his Credit Report

Residence Is currently living at home with parents and is paying no rent. He does

not have his own home.

Employment/

Income

Applicant is a sub-contractor working in the mining industry for 2

years. The applicant's income is $100,000 per annum.

The likely rental return for the property is in the vicinity of $420.00 per

week.

Credit Card Limit of $8,000 with a current balance of $5,000.

Other Loan

Debts

$30,000 car loan with repayments of $609.00 per month.

Assets Savings with a bank $50,000

Small assets with a total value of $60,000

Household Living

Expenses

$1,200.00 per month

Costs Stamp duty and purchase costs to be paid from savings.

Recommendatio

n

The Loan Application is recommended for pre-approval by the

authorised credit representative.

1. Complete a Risk Assessment using the Risk Register template below, noting all points

listed:

List and highlight 3 Risks you consider to be important and which you have identified

from the above Loan Application scenario and list the risks you have identified in the

relevant column.

Rate each of the 3 Risks according to their Likelihood (L) and Consequence (C) of

a negative event occurring and insert the ratings in the relevant columns.

Calculate the Risk Rating (LxC) value for each of the 3 Risks and insert the Risk

Rating values in the relevant column.

Refer to the Ranking Key table below and record the required action

Add your own comments on how the risk will be treated.

A10 © AAMC Training Group Assessment V2.3

Task 5 – Case study 2

In this Case Study you are the credit assessor for ABank. In your role as the credit assessor

you are required to determine the risks associated with the scenario below. The following

information is from a loan application submitted to ABank by an authorised credit

representative:

Applicant Single male applicant (29 years of age).

Loan Details and

Purpose

Applicant wants to buy an investment property for $450,000 and

borrow $405,000 plus LMI. A loan term of 15 years is requested with an

Interest Only product.

The Loan to Value Ratio (LVR is 90.00%);

Credit History Applicant has 3 Consumer Payments Defaults listed in his Credit Report

Residence Is currently living at home with parents and is paying no rent. He does

not have his own home.

Employment/

Income

Applicant is a sub-contractor working in the mining industry for 2

years. The applicant's income is $100,000 per annum.

The likely rental return for the property is in the vicinity of $420.00 per

week.

Credit Card Limit of $8,000 with a current balance of $5,000.

Other Loan

Debts

$30,000 car loan with repayments of $609.00 per month.

Assets Savings with a bank $50,000

Small assets with a total value of $60,000

Household Living

Expenses

$1,200.00 per month

Costs Stamp duty and purchase costs to be paid from savings.

Recommendatio

n

The Loan Application is recommended for pre-approval by the

authorised credit representative.

1. Complete a Risk Assessment using the Risk Register template below, noting all points

listed:

List and highlight 3 Risks you consider to be important and which you have identified

from the above Loan Application scenario and list the risks you have identified in the

relevant column.

Rate each of the 3 Risks according to their Likelihood (L) and Consequence (C) of

a negative event occurring and insert the ratings in the relevant columns.

Calculate the Risk Rating (LxC) value for each of the 3 Risks and insert the Risk

Rating values in the relevant column.

Refer to the Ranking Key table below and record the required action

Add your own comments on how the risk will be treated.

A10 © AAMC Training Group Assessment V2.3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Risk Management Assessment

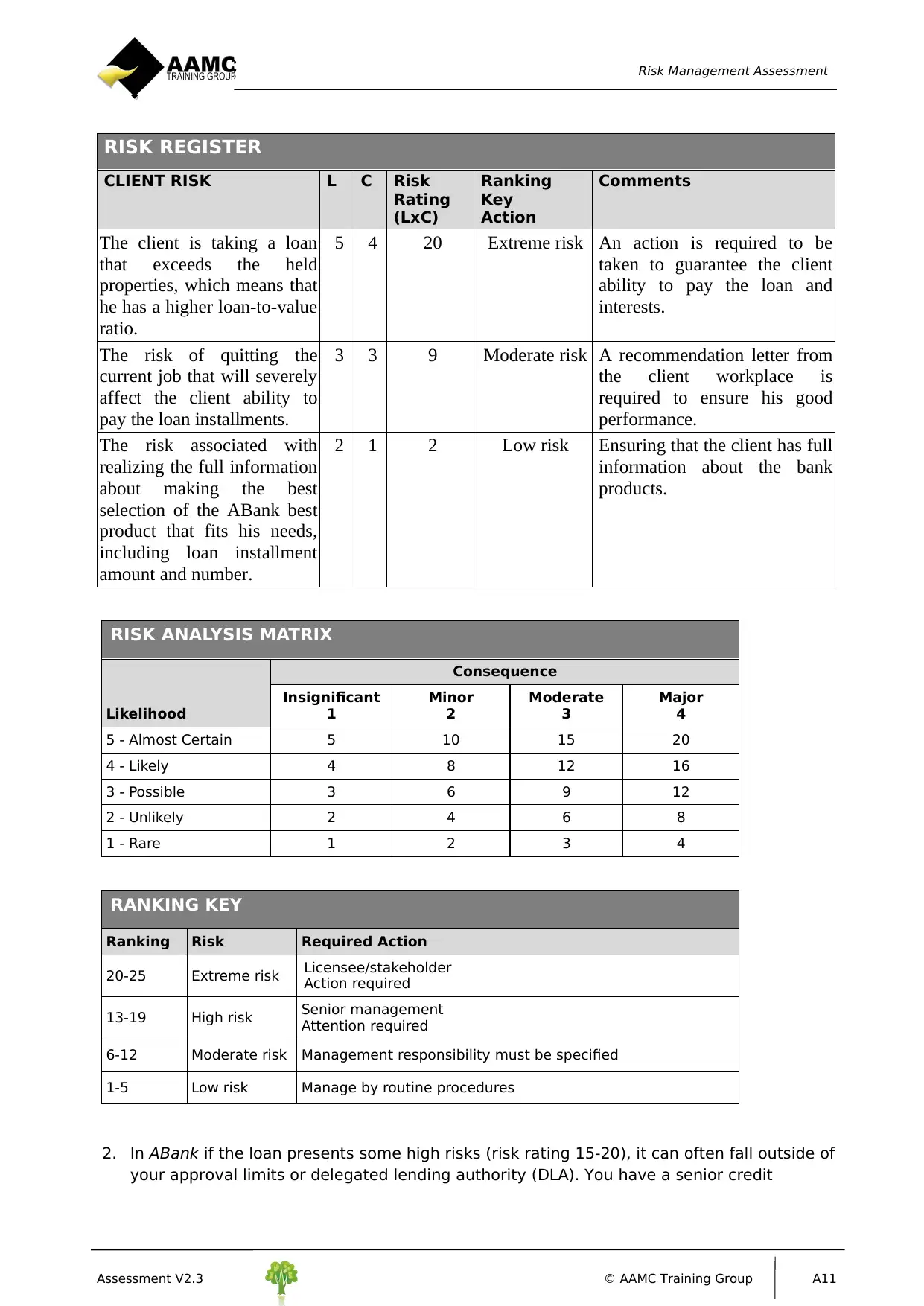

RISK REGISTER

CLIENT RISK L C Risk

Rating

(LxC)

Ranking

Key

Action

Comments

The client is taking a loan

that exceeds the held

properties, which means that

he has a higher loan-to-value

ratio.

5 4 20 Extreme risk An action is required to be

taken to guarantee the client

ability to pay the loan and

interests.

The risk of quitting the

current job that will severely

affect the client ability to

pay the loan installments.

3 3 9 Moderate risk A recommendation letter from

the client workplace is

required to ensure his good

performance.

The risk associated with

realizing the full information

about making the best

selection of the ABank best

product that fits his needs,

including loan installment

amount and number.

2 1 2 Low risk Ensuring that the client has full

information about the bank

products.

RISK ANALYSIS MATRIX

Likelihood

Consequence

Insignificant

1

Minor

2

Moderate

3

Major

4

5 - Almost Certain 5 10 15 20

4 - Likely 4 8 12 16

3 - Possible 3 6 9 12

2 - Unlikely 2 4 6 8

1 - Rare 1 2 3 4

RANKING KEY

Ranking Risk Required Action

20-25 Extreme risk Licensee/stakeholder

Action required

13-19 High risk Senior management

Attention required

6-12 Moderate risk Management responsibility must be specified

1-5 Low risk Manage by routine procedures

2. In ABank if the loan presents some high risks (risk rating 15-20), it can often fall outside of

your approval limits or delegated lending authority (DLA). You have a senior credit

Assessment V2.3 © AAMC Training Group A11

RISK REGISTER

CLIENT RISK L C Risk

Rating

(LxC)

Ranking

Key

Action

Comments

The client is taking a loan

that exceeds the held

properties, which means that

he has a higher loan-to-value

ratio.

5 4 20 Extreme risk An action is required to be

taken to guarantee the client

ability to pay the loan and

interests.

The risk of quitting the

current job that will severely

affect the client ability to

pay the loan installments.

3 3 9 Moderate risk A recommendation letter from

the client workplace is

required to ensure his good

performance.

The risk associated with

realizing the full information

about making the best

selection of the ABank best

product that fits his needs,

including loan installment

amount and number.

2 1 2 Low risk Ensuring that the client has full

information about the bank

products.

RISK ANALYSIS MATRIX

Likelihood

Consequence

Insignificant

1

Minor

2

Moderate

3

Major

4

5 - Almost Certain 5 10 15 20

4 - Likely 4 8 12 16

3 - Possible 3 6 9 12

2 - Unlikely 2 4 6 8

1 - Rare 1 2 3 4

RANKING KEY

Ranking Risk Required Action

20-25 Extreme risk Licensee/stakeholder

Action required

13-19 High risk Senior management

Attention required

6-12 Moderate risk Management responsibility must be specified

1-5 Low risk Manage by routine procedures

2. In ABank if the loan presents some high risks (risk rating 15-20), it can often fall outside of

your approval limits or delegated lending authority (DLA). You have a senior credit

Assessment V2.3 © AAMC Training Group A11

Risk Management Assessment

assessor that you refer loans for approval that present higher risks. Based on your risk

ratings determine if the Loan Application is outside your Delegated Lending Authority

(DLA). Briefly explain why you may need to escalate the loan application to a higher DLA

holder, for approval sign-off.

The client should provide sufficient guarantees to secure his position and proof his ability to pay

the loan and the interests. The examination of the client case revealed that there is a high potential

of his inability to pay the loan installments because the loan value highly exceeds his bank

financial statement, assets and salary. It is the role of the lender to address the weak compliance of

the poor client.

A12 © AAMC Training Group Assessment V2.3

assessor that you refer loans for approval that present higher risks. Based on your risk

ratings determine if the Loan Application is outside your Delegated Lending Authority

(DLA). Briefly explain why you may need to escalate the loan application to a higher DLA

holder, for approval sign-off.

The client should provide sufficient guarantees to secure his position and proof his ability to pay

the loan and the interests. The examination of the client case revealed that there is a high potential

of his inability to pay the loan installments because the loan value highly exceeds his bank

financial statement, assets and salary. It is the role of the lender to address the weak compliance of

the poor client.

A12 © AAMC Training Group Assessment V2.3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.