Accounting Assignment: AASB 13 Objectives and Impairment Loss Analysis

VerifiedAdded on 2023/04/25

|7

|1457

|324

Homework Assignment

AI Summary

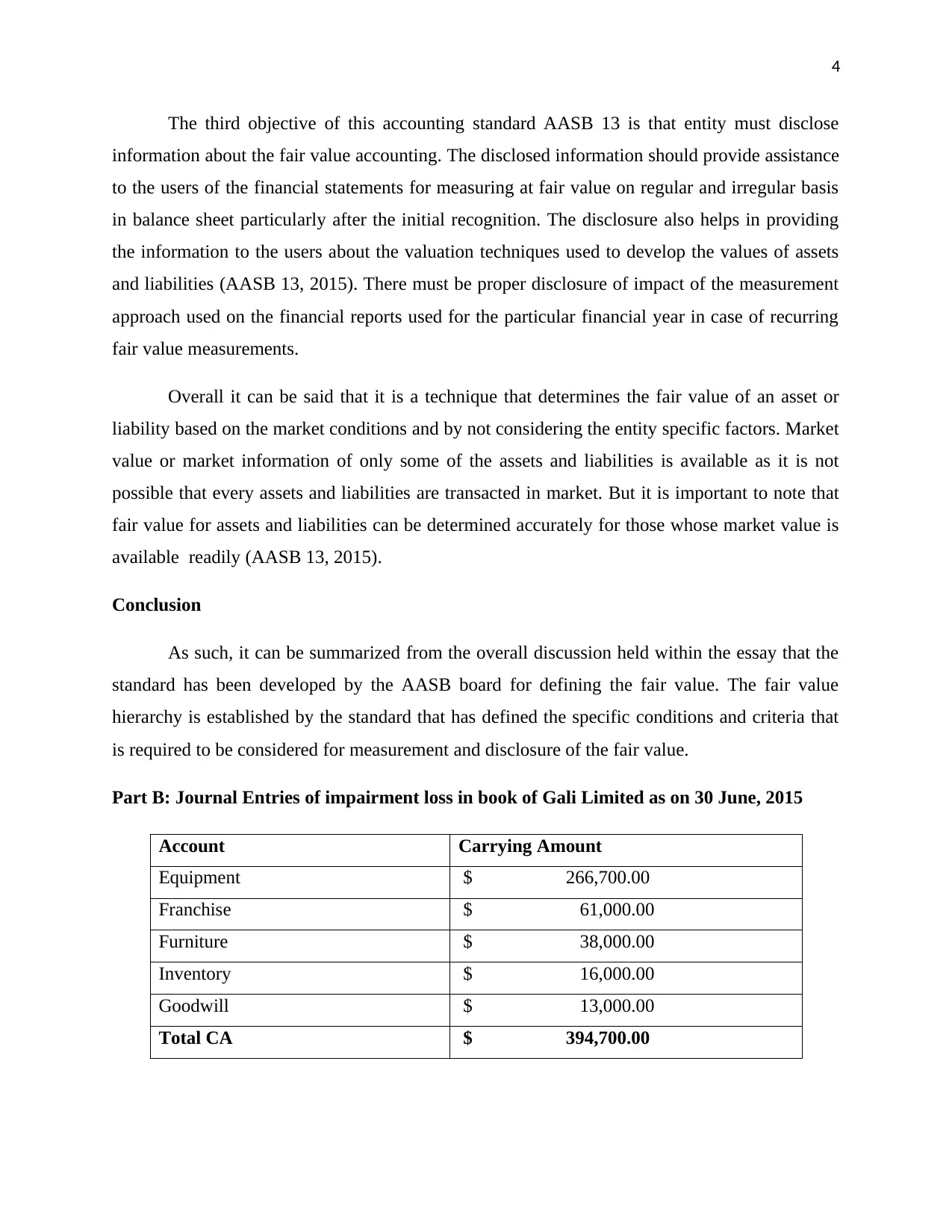

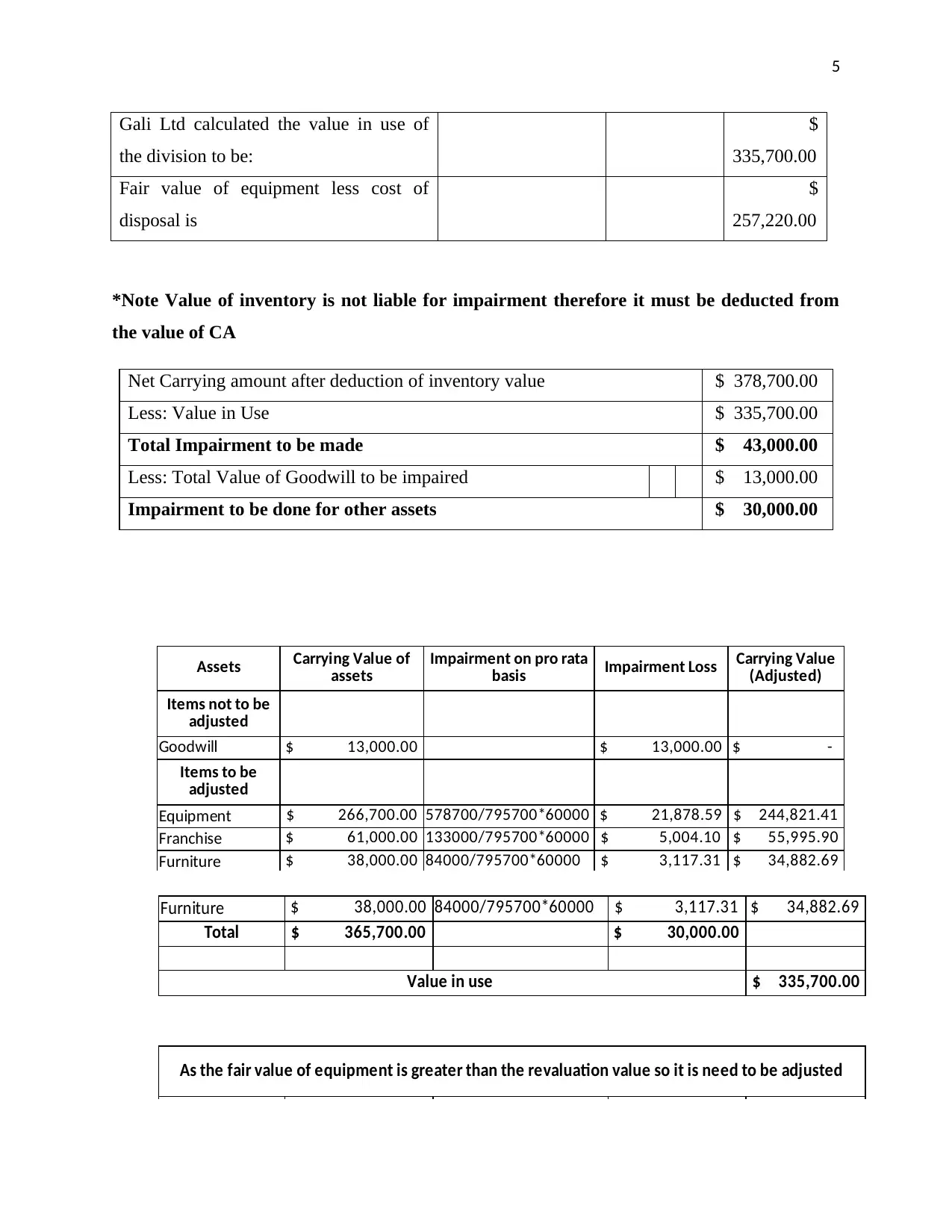

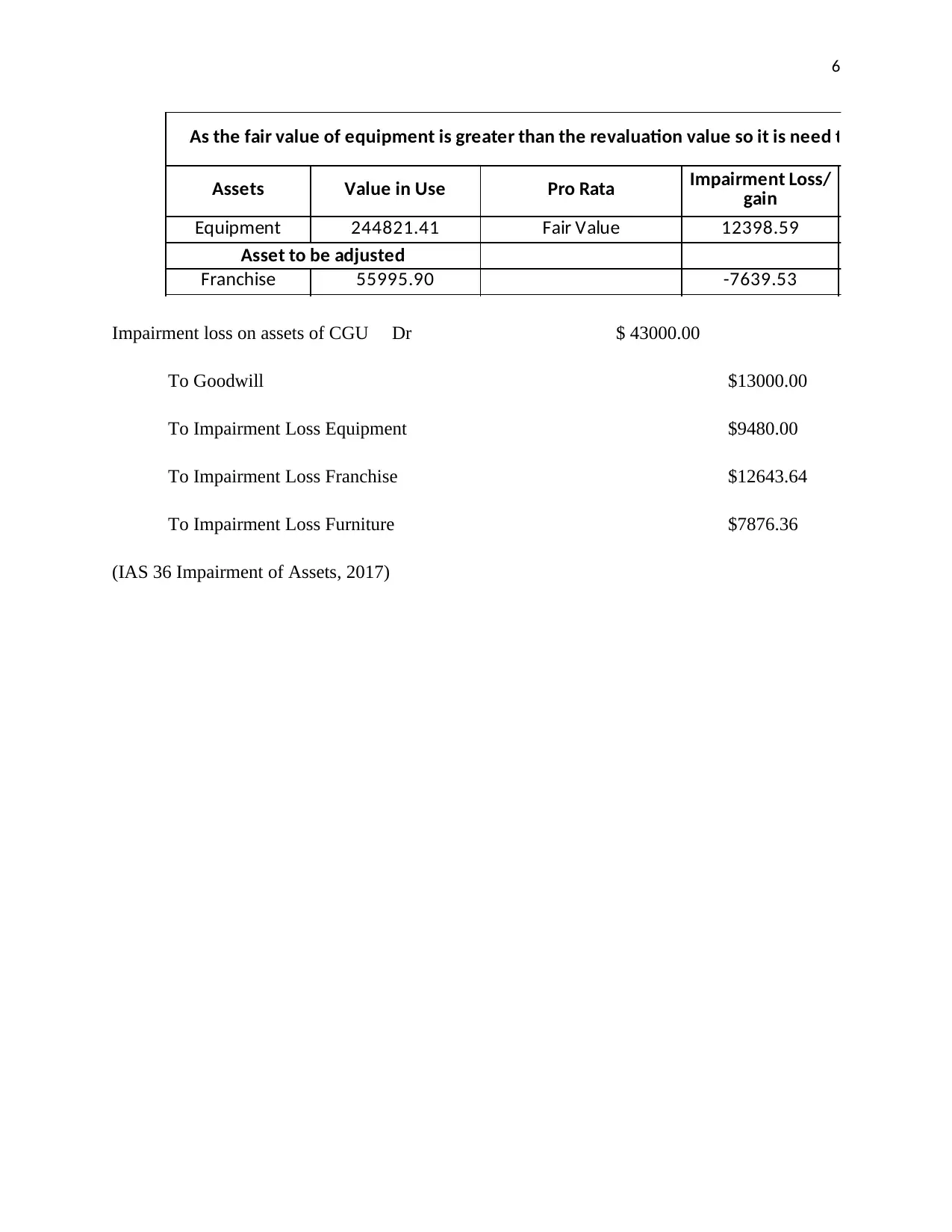

This assignment delves into the core principles of AASB 13, focusing on the objectives of fair value measurement as defined by the Australian Accounting Standards Board (AASB). The essay component explains the meaning of fair value, the measurement of an entity's fair value, and the importance of disclosing fair value measurements, emphasizing the standard's role in improving consistency and comparability in financial reporting. The second part of the assignment involves a practical application, where the student calculates and presents journal entries for an impairment loss scenario for Gali Ltd. This includes determining the impairment loss, allocating the loss across various assets (equipment, franchise, and furniture), and preparing the necessary journal entries to reflect the impairment in the company's financial records. The assignment demonstrates the student's understanding of accounting standards and their ability to apply them to real-world scenarios.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.