Activity-Based Costing vs Traditional Costing: A Comprehensive Report

VerifiedAdded on 2023/06/03

|9

|1563

|324

Report

AI Summary

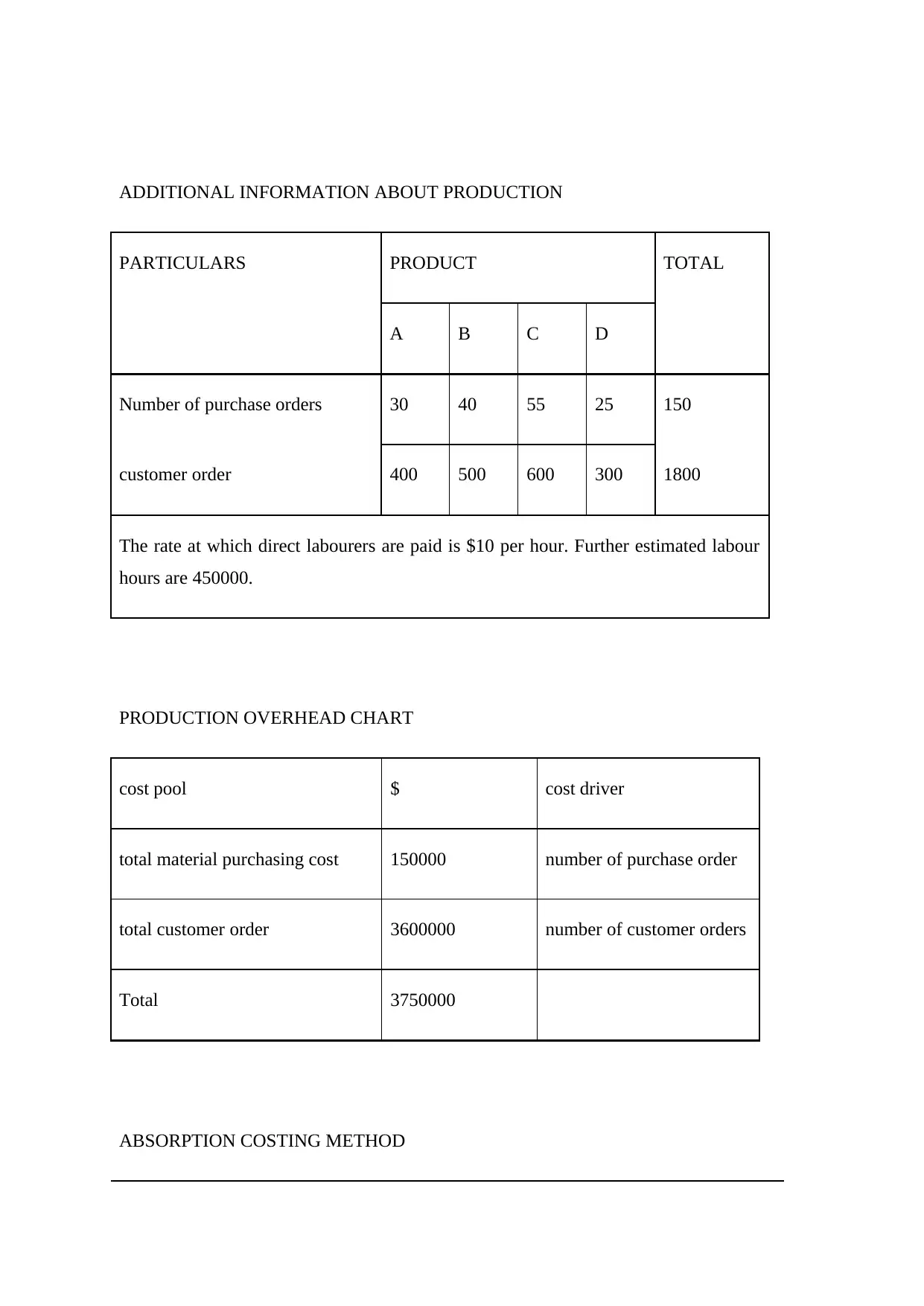

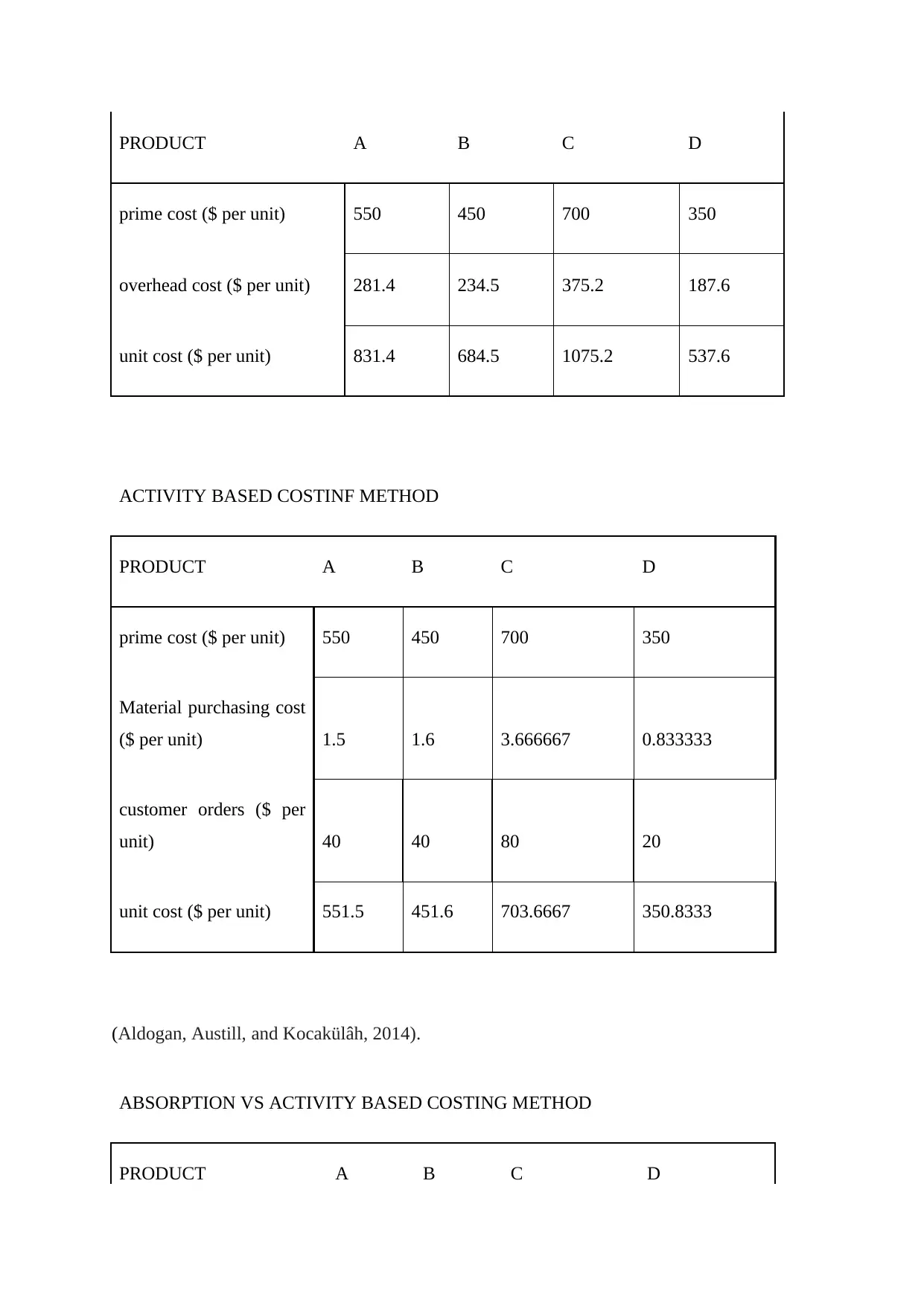

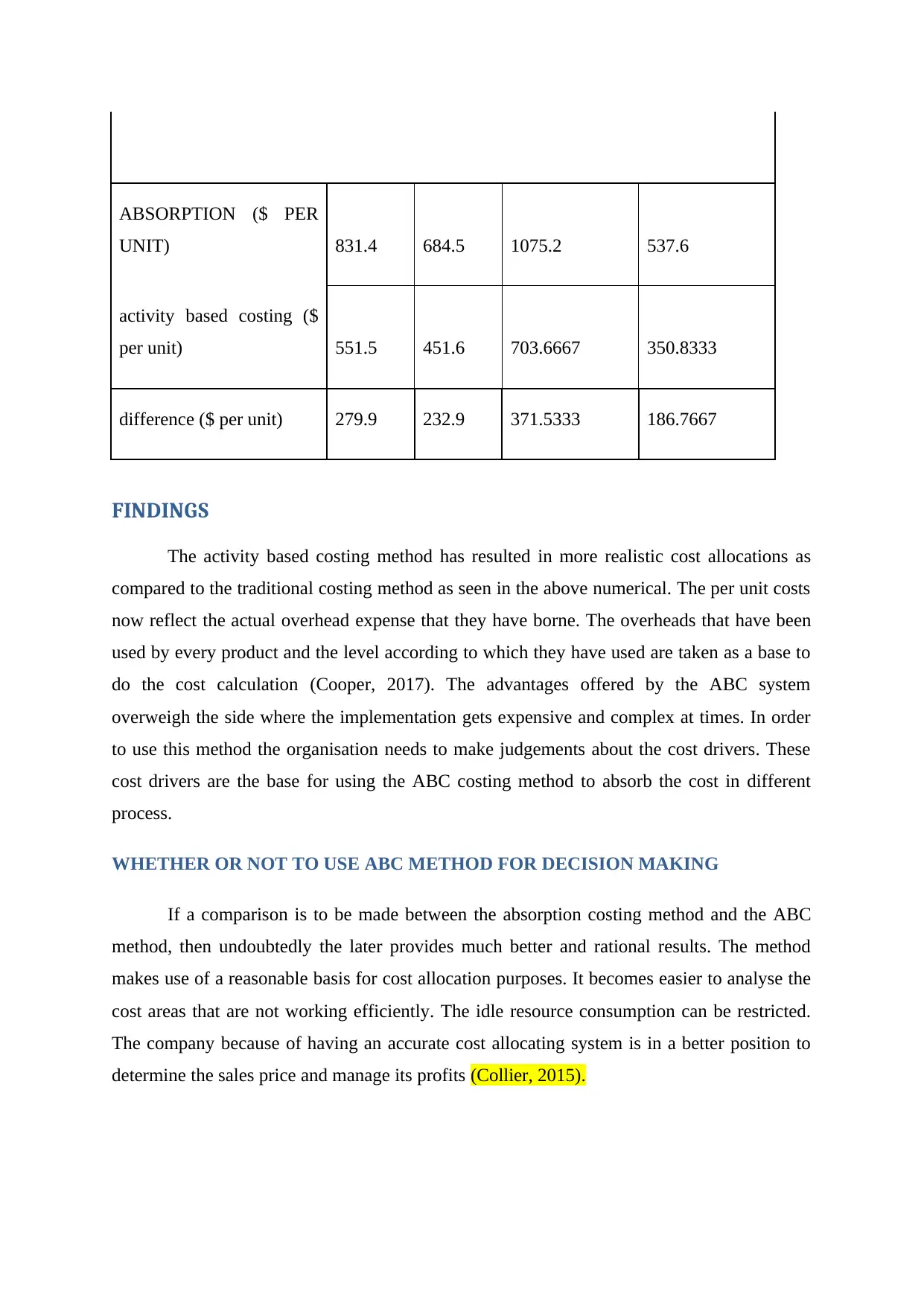

This report provides a comparative analysis of traditional absorption costing and activity-based costing (ABC) methods, highlighting their differences in cost allocation. Traditional methods use estimated overhead rates based on budgeted production hours, often ignoring the specific resource consumption of different products. In contrast, ABC uses cost drivers to allocate costs more precisely, focusing on the activities that cause overhead expenses, such as machine setups or quality checks. A numerical example illustrates the application of both methods, revealing that ABC leads to more realistic cost allocations by reflecting the actual overhead borne by each product. While ABC implementation can be expensive and complex, its advantages, including better cost analysis and improved pricing decisions, often outweigh the costs. The report concludes that ABC provides a more rational basis for cost allocation, enabling better management of resources and profits, but its adoption should be based on a cost-benefit analysis.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.