Auditing Standard ASA 701 and Lessons from ABC Learning Collapse

VerifiedAdded on 2019/11/29

|16

|3209

|344

Report

AI Summary

The provided content discusses the auditing standard ASA 701, which aims to ensure consistent representation of ISA 701. The standard is introduced in response to the recent enhancements to auditor reports by the International Auditing and Assurance Standards Board. The content also touches on the collapse of ABC Learning, a child care corporation that went bankrupt due to poor financial management and lack of accountability. The government subsequently established new regulations for child care centers, including the requirement for providers to demonstrate their plans and policies before starting operations. The collapse of ABC Learning led to lessons being learned and improvements made in auditing standards and corporate governance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Contents

1. Executive summary………………………………………………………… 2

History of ABC

Controversy

Accounting issues

Government response

2. ASA 701 auditor’s

report…………………………………………………………………….. 5

Introduction

Reason

Scope

Operative date

3. ASA 701 auditor’s report related With ABC learning

collapse……………………………………………................................... 7

4. Lesson learnt from ABC

collapse……………………………………………………………………… 9

5. Conclusion………………………………………………………………….. 9

6. References …………………………………………………………………. 10

1

1. Executive summary………………………………………………………… 2

History of ABC

Controversy

Accounting issues

Government response

2. ASA 701 auditor’s

report…………………………………………………………………….. 5

Introduction

Reason

Scope

Operative date

3. ASA 701 auditor’s report related With ABC learning

collapse……………………………………………................................... 7

4. Lesson learnt from ABC

collapse……………………………………………………………………… 9

5. Conclusion………………………………………………………………….. 9

6. References …………………………………………………………………. 10

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Executive summary

This study based on ABC learning collapse. Focusing on issues, crises, change in government

policy and the negligence issues face by ABC learning. This study further stated about ASA 701-

and appointing an independent auditor, and how ASA 701 regulates if it applied to time.

About ABC

It formed in 1988 by Edmund (Eddy) Groves and his wife Le Neve Groves in Ashgrove,

Brisbane, Queensland and now it operated all around the Australia, the New Zealand and the

United States (Teen, 2012). It is Australia's largest corporate child care provider. In 1996 it

managed 18 child care Centre's. In 1999 it owned 30 Centre's. After listing on the ASX in 2001,

it had experienced a fast growth; by the end of 2005, it has 660 Centre in Australia. After two

years it has 2,238 Centre’s in Australia, New Zealand and the United States.

In 2008 ABC was autocratically defrayed and purchased by Goodstart childcare in December

2009. Now it was known by “Goodstart Early Learning” this organisation is now registered

charity as owned by the Brotherhood of St Laurence, Mission Australia. The Benevolent Society

and Social venture Australia (Rush & Downie, 2006).

ABC learning was a highly profitable company in the financial year 2004-2005. Net profit after

tax recorded $52.3 million out of total revenue $292.7 million.

2

This study based on ABC learning collapse. Focusing on issues, crises, change in government

policy and the negligence issues face by ABC learning. This study further stated about ASA 701-

and appointing an independent auditor, and how ASA 701 regulates if it applied to time.

About ABC

It formed in 1988 by Edmund (Eddy) Groves and his wife Le Neve Groves in Ashgrove,

Brisbane, Queensland and now it operated all around the Australia, the New Zealand and the

United States (Teen, 2012). It is Australia's largest corporate child care provider. In 1996 it

managed 18 child care Centre's. In 1999 it owned 30 Centre's. After listing on the ASX in 2001,

it had experienced a fast growth; by the end of 2005, it has 660 Centre in Australia. After two

years it has 2,238 Centre’s in Australia, New Zealand and the United States.

In 2008 ABC was autocratically defrayed and purchased by Goodstart childcare in December

2009. Now it was known by “Goodstart Early Learning” this organisation is now registered

charity as owned by the Brotherhood of St Laurence, Mission Australia. The Benevolent Society

and Social venture Australia (Rush & Downie, 2006).

ABC learning was a highly profitable company in the financial year 2004-2005. Net profit after

tax recorded $52.3 million out of total revenue $292.7 million.

2

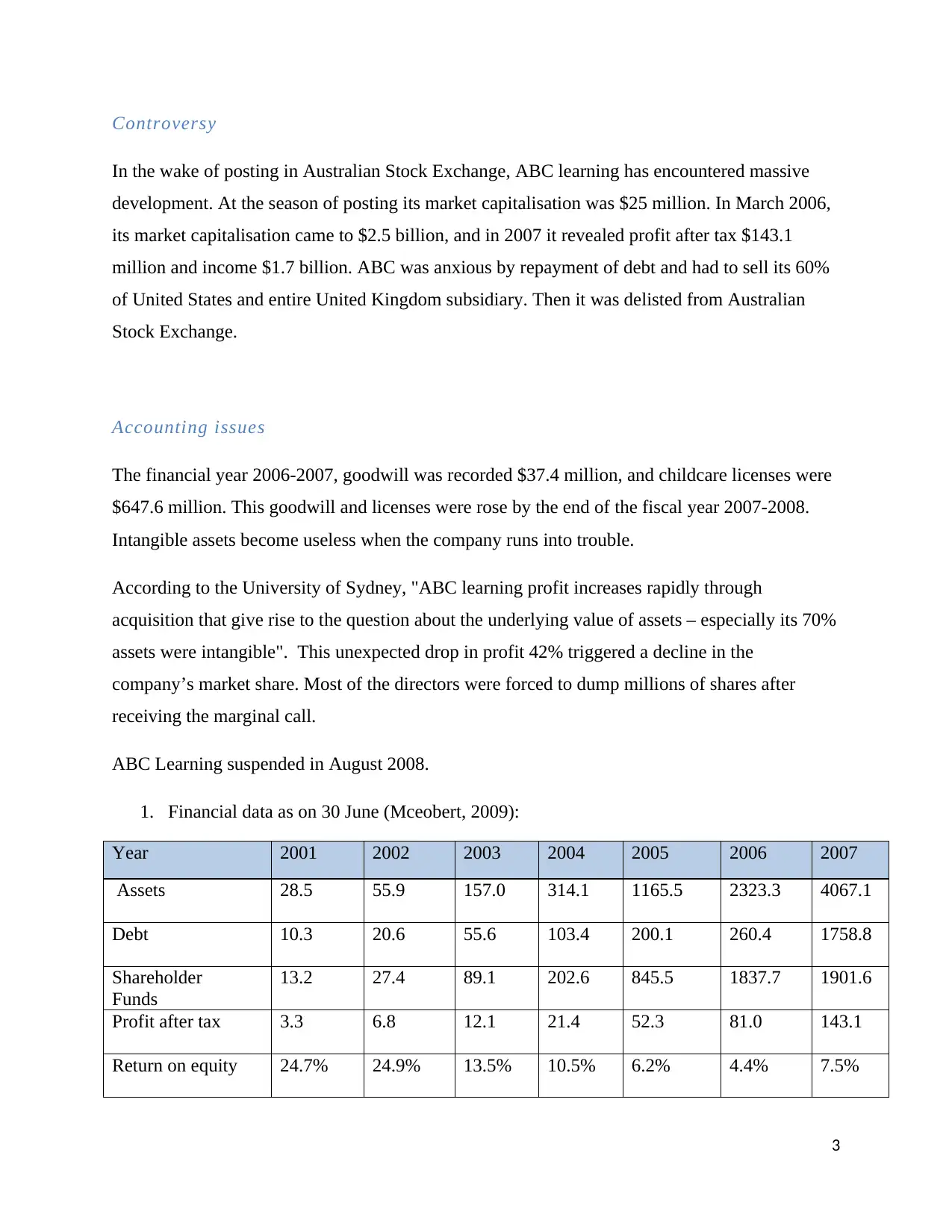

Controversy

In the wake of posting in Australian Stock Exchange, ABC learning has encountered massive

development. At the season of posting its market capitalisation was $25 million. In March 2006,

its market capitalisation came to $2.5 billion, and in 2007 it revealed profit after tax $143.1

million and income $1.7 billion. ABC was anxious by repayment of debt and had to sell its 60%

of United States and entire United Kingdom subsidiary. Then it was delisted from Australian

Stock Exchange.

Accounting issues

The financial year 2006-2007, goodwill was recorded $37.4 million, and childcare licenses were

$647.6 million. This goodwill and licenses were rose by the end of the fiscal year 2007-2008.

Intangible assets become useless when the company runs into trouble.

According to the University of Sydney, "ABC learning profit increases rapidly through

acquisition that give rise to the question about the underlying value of assets – especially its 70%

assets were intangible". This unexpected drop in profit 42% triggered a decline in the

company’s market share. Most of the directors were forced to dump millions of shares after

receiving the marginal call.

ABC Learning suspended in August 2008.

1. Financial data as on 30 June (Mceobert, 2009):

Year 2001 2002 2003 2004 2005 2006 2007

Assets 28.5 55.9 157.0 314.1 1165.5 2323.3 4067.1

Debt 10.3 20.6 55.6 103.4 200.1 260.4 1758.8

Shareholder

Funds

13.2 27.4 89.1 202.6 845.5 1837.7 1901.6

Profit after tax 3.3 6.8 12.1 21.4 52.3 81.0 143.1

Return on equity 24.7% 24.9% 13.5% 10.5% 6.2% 4.4% 7.5%

3

In the wake of posting in Australian Stock Exchange, ABC learning has encountered massive

development. At the season of posting its market capitalisation was $25 million. In March 2006,

its market capitalisation came to $2.5 billion, and in 2007 it revealed profit after tax $143.1

million and income $1.7 billion. ABC was anxious by repayment of debt and had to sell its 60%

of United States and entire United Kingdom subsidiary. Then it was delisted from Australian

Stock Exchange.

Accounting issues

The financial year 2006-2007, goodwill was recorded $37.4 million, and childcare licenses were

$647.6 million. This goodwill and licenses were rose by the end of the fiscal year 2007-2008.

Intangible assets become useless when the company runs into trouble.

According to the University of Sydney, "ABC learning profit increases rapidly through

acquisition that give rise to the question about the underlying value of assets – especially its 70%

assets were intangible". This unexpected drop in profit 42% triggered a decline in the

company’s market share. Most of the directors were forced to dump millions of shares after

receiving the marginal call.

ABC Learning suspended in August 2008.

1. Financial data as on 30 June (Mceobert, 2009):

Year 2001 2002 2003 2004 2005 2006 2007

Assets 28.5 55.9 157.0 314.1 1165.5 2323.3 4067.1

Debt 10.3 20.6 55.6 103.4 200.1 260.4 1758.8

Shareholder

Funds

13.2 27.4 89.1 202.6 845.5 1837.7 1901.6

Profit after tax 3.3 6.8 12.1 21.4 52.3 81.0 143.1

Return on equity 24.7% 24.9% 13.5% 10.5% 6.2% 4.4% 7.5%

3

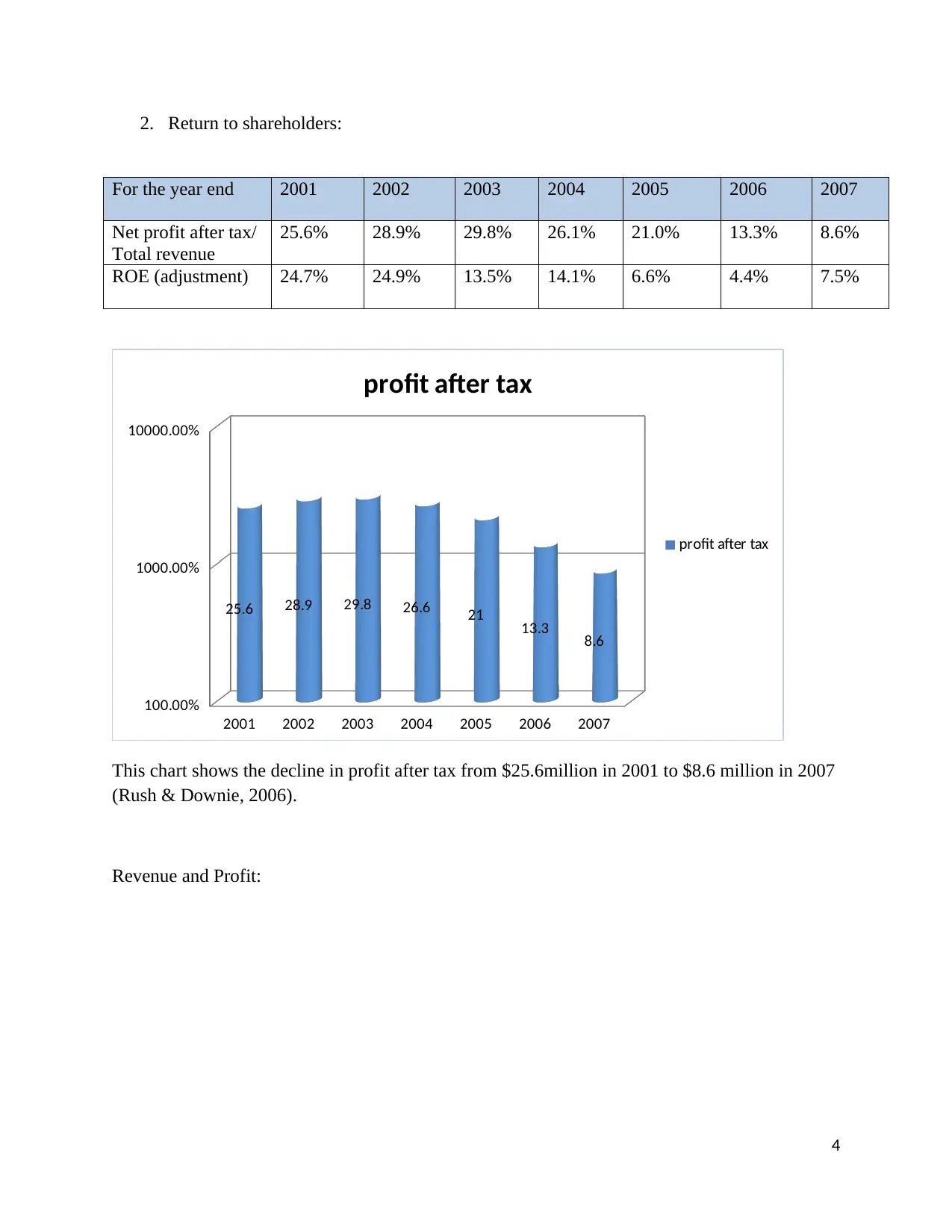

2. Return to shareholders:

For the year end 2001 2002 2003 2004 2005 2006 2007

Net profit after tax/

Total revenue

25.6% 28.9% 29.8% 26.1% 21.0% 13.3% 8.6%

ROE (adjustment) 24.7% 24.9% 13.5% 14.1% 6.6% 4.4% 7.5%

2001 2002 2003 2004 2005 2006 2007

100.00%

1000.00%

10000.00%

25.6 28.9 29.8 26.6 21 13.3 8.6

profit after tax

profit after tax

This chart shows the decline in profit after tax from $25.6million in 2001 to $8.6 million in 2007

(Rush & Downie, 2006).

Revenue and Profit:

4

For the year end 2001 2002 2003 2004 2005 2006 2007

Net profit after tax/

Total revenue

25.6% 28.9% 29.8% 26.1% 21.0% 13.3% 8.6%

ROE (adjustment) 24.7% 24.9% 13.5% 14.1% 6.6% 4.4% 7.5%

2001 2002 2003 2004 2005 2006 2007

100.00%

1000.00%

10000.00%

25.6 28.9 29.8 26.6 21 13.3 8.6

profit after tax

profit after tax

This chart shows the decline in profit after tax from $25.6million in 2001 to $8.6 million in 2007

(Rush & Downie, 2006).

Revenue and Profit:

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2001 2002 2003 2004 2005

0

50

100

150

200

250

300

Revenue

profit

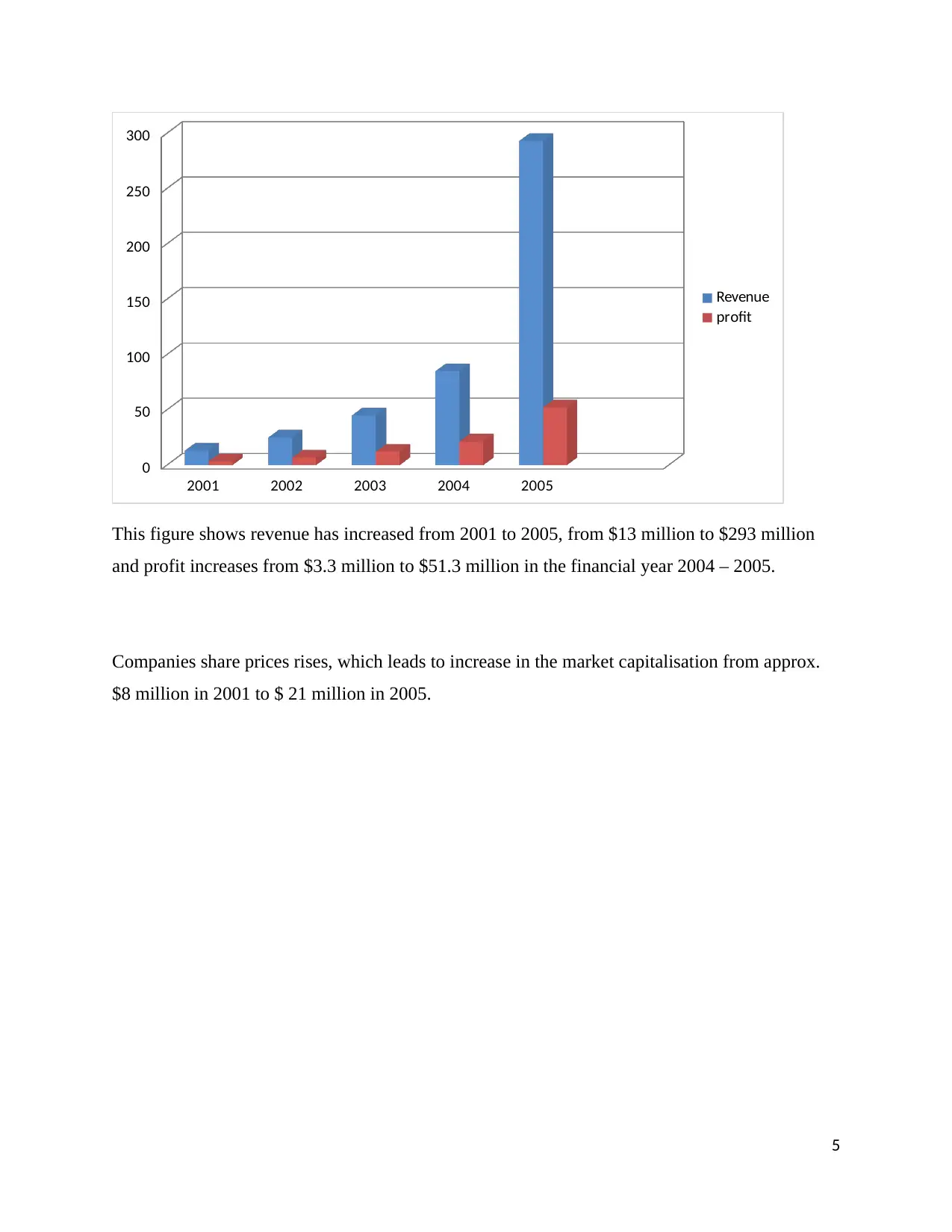

This figure shows revenue has increased from 2001 to 2005, from $13 million to $293 million

and profit increases from $3.3 million to $51.3 million in the financial year 2004 – 2005.

Companies share prices rises, which leads to increase in the market capitalisation from approx.

$8 million in 2001 to $ 21 million in 2005.

5

0

50

100

150

200

250

300

Revenue

profit

This figure shows revenue has increased from 2001 to 2005, from $13 million to $293 million

and profit increases from $3.3 million to $51.3 million in the financial year 2004 – 2005.

Companies share prices rises, which leads to increase in the market capitalisation from approx.

$8 million in 2001 to $ 21 million in 2005.

5

2001 2002 2003 2004 2005

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

Series 1

Series 1

Demand about offering off company's assets, done November 2008, the organisation drop under

receivership following builds the debt of the company; its auditors would unabated on disguise

their accounts. Legislature visits $22 million with ABC agency for keeping their core open until

the end from claiming 2008.

The ABC taking in delisted from the ASX 200.

In 2010, lenders of the organisation voted should shut the agency also its 570 Centre's were made

by "Goodstart initial Learning".

Government response (2014):

Committee Recommendation 1:

The Australian government announced that productivity commission would undertake an Inquiry

into Child Care Centre. Government asked Productivity Commission to make a recommendation

6

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

Series 1

Series 1

Demand about offering off company's assets, done November 2008, the organisation drop under

receivership following builds the debt of the company; its auditors would unabated on disguise

their accounts. Legislature visits $22 million with ABC agency for keeping their core open until

the end from claiming 2008.

The ABC taking in delisted from the ASX 200.

In 2010, lenders of the organisation voted should shut the agency also its 570 Centre's were made

by "Goodstart initial Learning".

Government response (2014):

Committee Recommendation 1:

The Australian government announced that productivity commission would undertake an Inquiry

into Child Care Centre. Government asked Productivity Commission to make a recommendation

6

about the contribution that the Child Care Centre make to children development. Final report

presented to the Productivity Commission by the end of the Oct 2014.

Committee Recommendation 2:

The Government makes detailed information to the use of commonwealth funding by the State

And territory government, to provide access to 15 hours per week of personal services for all

four- year-olds in Australia.

Australian Government gives $655.6 million to state and territory government.

Committee Recommendation 3,4,5,6 and 7:

In Productivity Commission enquiry will include: focusing on parents’ choices, work and study

needs, needs of rural, remote and regional families, and the needs of weak children. The

Australian Government asked Productivity Commission whether they do it within existing

funding.

Productivity Commission chooses possible scenario for examines: Australia’s economy,

community and parents and how to be funded and by whom.

The Final report was given by Productivity Commission to Government by the end of Oct 2014.

Committee Recommendation 8, 9 and 10:

In this Committee Recommends to the Govt. establishment of a new statutory body the National

Quality Framework for Early Childhood Education and Care (NQF) (Mena, 2016) for the

purpose to advising the minister on Childcare policy and its implementation.

It is consistent national implementation. To assist it, the Australian and State and territory

government fund the Australian Children’s Education and Care Quality Authority (ACECQA).

Council of Australian Government established it.

7

presented to the Productivity Commission by the end of the Oct 2014.

Committee Recommendation 2:

The Government makes detailed information to the use of commonwealth funding by the State

And territory government, to provide access to 15 hours per week of personal services for all

four- year-olds in Australia.

Australian Government gives $655.6 million to state and territory government.

Committee Recommendation 3,4,5,6 and 7:

In Productivity Commission enquiry will include: focusing on parents’ choices, work and study

needs, needs of rural, remote and regional families, and the needs of weak children. The

Australian Government asked Productivity Commission whether they do it within existing

funding.

Productivity Commission chooses possible scenario for examines: Australia’s economy,

community and parents and how to be funded and by whom.

The Final report was given by Productivity Commission to Government by the end of Oct 2014.

Committee Recommendation 8, 9 and 10:

In this Committee Recommends to the Govt. establishment of a new statutory body the National

Quality Framework for Early Childhood Education and Care (NQF) (Mena, 2016) for the

purpose to advising the minister on Childcare policy and its implementation.

It is consistent national implementation. To assist it, the Australian and State and territory

government fund the Australian Children’s Education and Care Quality Authority (ACECQA).

Council of Australian Government established it.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Functions of ACECQA’s:

- Promote national consistency

- Maintaining registers of Childcare and Early learning services

- Promote quality improvement by Childcare and Early learning

- Educating and informing about NQF.

The Report should be transparent and accountable:

- Published annual reports of its achievement and activities of the last financial year

- Provide report at a regional and state level on Government expenditure.

- Published data of each quarter.

Introduction of ASA701

Introduction

Accounting standard ASA 701 established by Auditing and Assurance Standard Board

(AUASB). AUASB has an independent agency, which is responsible for developing standards

and guidelines for Auditors and provide another assurance service. AUASB established under

section 227A of Australian Security and Investment Act 2001 (federal register of legislation,

2015).

8

- Promote national consistency

- Maintaining registers of Childcare and Early learning services

- Promote quality improvement by Childcare and Early learning

- Educating and informing about NQF.

The Report should be transparent and accountable:

- Published annual reports of its achievement and activities of the last financial year

- Provide report at a regional and state level on Government expenditure.

- Published data of each quarter.

Introduction of ASA701

Introduction

Accounting standard ASA 701 established by Auditing and Assurance Standard Board

(AUASB). AUASB has an independent agency, which is responsible for developing standards

and guidelines for Auditors and provide another assurance service. AUASB established under

section 227A of Australian Security and Investment Act 2001 (federal register of legislation,

2015).

8

Its primary Aim to develop an Accounting Standard ASA701 is to appoint an independent

auditor for an auditing a company’s wrong doing, to save public interest.

Main Reason:

Auditing standard ASA701 has different from ISA 701. ISA 701 maintains the audit quality, but

ASA 701 considered a right to do so. Key features of ASA 701 are:

Command the auditor’s report of listed companies.

Let the auditor decide whether to use Key Audit Matters in their reports.

How auditor’s decided:

a) Those things that need significant auditor attention

b) Related to the accounts where the chances of risk are higher than earlier.

c) Identify critical issues in the auditor report.

Documents of audit required

How account present individual critical audit matters,

Which matters is not stated in the report.

ASA 701 Applies:

I. Audit financial report and financial statement

II. Review a report for fiscal year or half- year

Scope:

The evaluator's obligation to convey enter review matters in the examiner's report. It is

expected to address both the reviewer's choice as:

1. What to send in the auditor's report

2. Shape

9

auditor for an auditing a company’s wrong doing, to save public interest.

Main Reason:

Auditing standard ASA701 has different from ISA 701. ISA 701 maintains the audit quality, but

ASA 701 considered a right to do so. Key features of ASA 701 are:

Command the auditor’s report of listed companies.

Let the auditor decide whether to use Key Audit Matters in their reports.

How auditor’s decided:

a) Those things that need significant auditor attention

b) Related to the accounts where the chances of risk are higher than earlier.

c) Identify critical issues in the auditor report.

Documents of audit required

How account present individual critical audit matters,

Which matters is not stated in the report.

ASA 701 Applies:

I. Audit financial report and financial statement

II. Review a report for fiscal year or half- year

Scope:

The evaluator's obligation to convey enter review matters in the examiner's report. It is

expected to address both the reviewer's choice as:

1. What to send in the auditor's report

2. Shape

9

3. Contents.

The reason for imparting key review is to improve the informative estimation of the

evaluator's report by giving more prominent straightforwardness about the study that

performed. Providing critical review matters provides extra data to clients of the

budgetary answer to help them in understanding those issues. Imparting critical review

issues may likewise assist proposed customers in understanding the substance and

territories of massive administration choice in the inspected budgetary report

Auditor report may likewise give implying clients a premise to additionally draw in with

administration and those accused of policy about specific issues identifying with the

substance, and the examined money related report or the review that performed

Auditors have framed a supposition on the money related story all in all aside from :

a) Substitute for revelation in the budgetary report expects the administration to make,

or generally to accomplish impartial introduction.

b) Substitute for the reviewer, adjusted its sentiment when conditions required.

c) Make a different assessment on single issues.

Auditor was to recognised review matters, shaped a conclusion on the financial report

and discusses them with reviewer's report.

Critical examination cases in the analyst's report were the most centrality money related

story of the present time frame.

Operative date of ASA 701 communicating critical matters in the independent Auditor's report:-

“Ending or after 15 December 2016”

10

The reason for imparting key review is to improve the informative estimation of the

evaluator's report by giving more prominent straightforwardness about the study that

performed. Providing critical review matters provides extra data to clients of the

budgetary answer to help them in understanding those issues. Imparting critical review

issues may likewise assist proposed customers in understanding the substance and

territories of massive administration choice in the inspected budgetary report

Auditor report may likewise give implying clients a premise to additionally draw in with

administration and those accused of policy about specific issues identifying with the

substance, and the examined money related report or the review that performed

Auditors have framed a supposition on the money related story all in all aside from :

a) Substitute for revelation in the budgetary report expects the administration to make,

or generally to accomplish impartial introduction.

b) Substitute for the reviewer, adjusted its sentiment when conditions required.

c) Make a different assessment on single issues.

Auditor was to recognised review matters, shaped a conclusion on the financial report

and discusses them with reviewer's report.

Critical examination cases in the analyst's report were the most centrality money related

story of the present time frame.

Operative date of ASA 701 communicating critical matters in the independent Auditor's report:-

“Ending or after 15 December 2016”

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

The auditor shall determine critical audit matters:

Higher risk of material, misstatement or risk accordance with ASA 315

The decision regarding the areas of a financial report including management judgment,

accounting estimate which having high uncertainty.

The audit

Or should identify those matters which need significant attention. They focus on the nature of the

concerns those charged with governance that linked with the issues disclosed in the financial

report.

ISA 570 Going Concern:

ISA 570 stated that (2006): it is the auditor’s responsibility to use going concern in the

preparation of financial statement.

OBJECTIVES:

Auditor has to obtain sufficient evidence while preparing financial statement

Auditors have to know, the implication of report

Auditor review prove got, regardless of whether a material vulnerability exists identified

with occasions or conditions that may provide the reason to feel ambiguous about

massive the substance's

11

Higher risk of material, misstatement or risk accordance with ASA 315

The decision regarding the areas of a financial report including management judgment,

accounting estimate which having high uncertainty.

The audit

Or should identify those matters which need significant attention. They focus on the nature of the

concerns those charged with governance that linked with the issues disclosed in the financial

report.

ISA 570 Going Concern:

ISA 570 stated that (2006): it is the auditor’s responsibility to use going concern in the

preparation of financial statement.

OBJECTIVES:

Auditor has to obtain sufficient evidence while preparing financial statement

Auditors have to know, the implication of report

Auditor review prove got, regardless of whether a material vulnerability exists identified

with occasions or conditions that may provide the reason to feel ambiguous about

massive the substance's

11

ASA 570:

The AUASB issue ASA 570 under section 227A of Australian Securities and Investment

Commission Act 2000. Auditing standard has replaced ISA 570 going concern with ASA 570,

which is published by AUASB in October 2009.

The main feature of ASA 570:

Examining Standard ASA 570 has a few contracts from the ISA 570 with the intention of to keep

up review quality. It was working date of money related announcing is finishing on or after 15

December 2016.

Authority Statement (Anon., 2017)

Issues that lead to improvement of Auditing Standard ASA 501:

The main purpose of introducing ASA 701 is to ensure consistent representation of ISA 701. The

introduction of ASA 701 reflects the AUASB’s commitment with the recent enhancements to

auditor report which developed by the International Auditing and Assurance Standards Board.

12

Authority Statement

The Auditing and Assurance Standards Board (AUASB) makes this Auditing Standard (2017)

(Auditing Standard ASA 2017-1 Amendments to Australian Auditing Standards, 2017) ASA

570 Going Concern under section 227B of the Australian Securities and Investments

Commission Act 2001 and section 336 of the Corporations Act 2001. This Auditing Standard

is to read in conjunction with ASA 101 Preamble to Australian Auditing Standards, which sets

out the intentions of the AUASB on how the Australian Auditing Standards, operative for

financial reporting periods commencing on or after 1 January 2010, are to be understood,

interpreted and applied. This Auditing Standard is to also read in conjunction with ASA 200

Overall Objectives of the Independent Auditor and the Conduct of an Audit by Australian

Auditing Standards.

Date: 1 Dec 2015 M H Kelsall

Chairman- AUASB

The AUASB issue ASA 570 under section 227A of Australian Securities and Investment

Commission Act 2000. Auditing standard has replaced ISA 570 going concern with ASA 570,

which is published by AUASB in October 2009.

The main feature of ASA 570:

Examining Standard ASA 570 has a few contracts from the ISA 570 with the intention of to keep

up review quality. It was working date of money related announcing is finishing on or after 15

December 2016.

Authority Statement (Anon., 2017)

Issues that lead to improvement of Auditing Standard ASA 501:

The main purpose of introducing ASA 701 is to ensure consistent representation of ISA 701. The

introduction of ASA 701 reflects the AUASB’s commitment with the recent enhancements to

auditor report which developed by the International Auditing and Assurance Standards Board.

12

Authority Statement

The Auditing and Assurance Standards Board (AUASB) makes this Auditing Standard (2017)

(Auditing Standard ASA 2017-1 Amendments to Australian Auditing Standards, 2017) ASA

570 Going Concern under section 227B of the Australian Securities and Investments

Commission Act 2001 and section 336 of the Corporations Act 2001. This Auditing Standard

is to read in conjunction with ASA 101 Preamble to Australian Auditing Standards, which sets

out the intentions of the AUASB on how the Australian Auditing Standards, operative for

financial reporting periods commencing on or after 1 January 2010, are to be understood,

interpreted and applied. This Auditing Standard is to also read in conjunction with ASA 200

Overall Objectives of the Independent Auditor and the Conduct of an Audit by Australian

Auditing Standards.

Date: 1 Dec 2015 M H Kelsall

Chairman- AUASB

How ASA 701 Communicating Key Matters in Independent Auditor’s Report

(Government, 2015):

Why financial auditing is needed:

When the business grows large, there is a need to keep the record of all account. It is mandatory

when accountability is highly needed. Sometimes managers are supposed to be providing more

accurate report.

A Financial institution, tax office and the management always get a great benefit while

conducting an audit. When they made self - governing audit, financial firms get accurate data

from auditing report.

In case of ABC learning; earlier warning that may exist with respect to going concern, auditing

issue surrounding collapse of ABC learning leads to the development of new auditing standard

ASA 701.

Lessons learned from ABC learning Collapse (kruger, 2009):

From the failure of ABC learning, new regulations established for new operators:

Before starting the business, new operators have to demonstrate their plans and policies

that they are suitable to operate child care Centre.

13

(Government, 2015):

Why financial auditing is needed:

When the business grows large, there is a need to keep the record of all account. It is mandatory

when accountability is highly needed. Sometimes managers are supposed to be providing more

accurate report.

A Financial institution, tax office and the management always get a great benefit while

conducting an audit. When they made self - governing audit, financial firms get accurate data

from auditing report.

In case of ABC learning; earlier warning that may exist with respect to going concern, auditing

issue surrounding collapse of ABC learning leads to the development of new auditing standard

ASA 701.

Lessons learned from ABC learning Collapse (kruger, 2009):

From the failure of ABC learning, new regulations established for new operators:

Before starting the business, new operators have to demonstrate their plans and policies

that they are suitable to operate child care Centre.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

They have to give notice 42 days before to close the child care Centre.

Active control over the child care Centre.

Introduce a new civil penalty regime.

The government in their Budget 2009 – 2010 proposed new plans regarding child care Centre's:

Provider of Long Day Care had estimated before they approved for Child Care Benefit

and this estimation has done every year.

The New powers give to the Minister For education to an independent audit or

investigation.

Conclusion

It has been the huge turnaround in the Child Care Business in Australia. ABC brought

supernatural occurrence up in most recent 20 years in the field of Child Care and obtained 20%

of the Child Care Business of Australia. This fall happened because the administration of the

ABC learning organisation was wasteful in controlling the fate of the organization. The

organisation was concentrate on using the business as opposed to reinforcing its base. False

bookkeeping data and changes in government properties are a reason for the sudden destruction

of the firm.

14

Active control over the child care Centre.

Introduce a new civil penalty regime.

The government in their Budget 2009 – 2010 proposed new plans regarding child care Centre's:

Provider of Long Day Care had estimated before they approved for Child Care Benefit

and this estimation has done every year.

The New powers give to the Minister For education to an independent audit or

investigation.

Conclusion

It has been the huge turnaround in the Child Care Business in Australia. ABC brought

supernatural occurrence up in most recent 20 years in the field of Child Care and obtained 20%

of the Child Care Business of Australia. This fall happened because the administration of the

ABC learning organisation was wasteful in controlling the fate of the organization. The

organisation was concentrate on using the business as opposed to reinforcing its base. False

bookkeeping data and changes in government properties are a reason for the sudden destruction

of the firm.

14

The disappointment of ABC is not just as a result of ABC business strategy; it is likewise a

disappointment of government policies and their directions. The purpose behind the fall is the

false report exhibited by the organisation's chefs and CEO. It came into the light when securities

exchange of ABC learning goes down.

That is the blame of association as well as the fault of Government Child Care Policy.

Australia has moved its public Child Care Center to private child care Center. At the point when

kid cares Center end up plainly private then government had less control over youngster mind

Center. There is nothing incorrect in private Child Care Center; they have their guidelines and

unmistakable quality.

Government changes its strategy and presents the new arrangement of Child Care which one of

the greatest reason for ABC crumple.

Government action begin developing, and ABC learning starts concentrating on buying Child

Care Center demand of running them appropriately.

The disappointment of ABC learning offers to ascend to the "Goodstart early learning". New

Association gets lessons from ABC disappointment.

REFERENCES:

Anon., 2006. Auditing Standard ASA 501. pdf. Australia: Auditing and Assurance Standards Board.

Anon., 2014. Provision of ChildCare. Doc. Australia: Australian Government.

Anon., 2017. [Online] Federal Register of Legislation Available at:

https://www.legislation.gov.au/Details/F2017L00693.

15

disappointment of government policies and their directions. The purpose behind the fall is the

false report exhibited by the organisation's chefs and CEO. It came into the light when securities

exchange of ABC learning goes down.

That is the blame of association as well as the fault of Government Child Care Policy.

Australia has moved its public Child Care Center to private child care Center. At the point when

kid cares Center end up plainly private then government had less control over youngster mind

Center. There is nothing incorrect in private Child Care Center; they have their guidelines and

unmistakable quality.

Government changes its strategy and presents the new arrangement of Child Care which one of

the greatest reason for ABC crumple.

Government action begin developing, and ABC learning starts concentrating on buying Child

Care Center demand of running them appropriately.

The disappointment of ABC learning offers to ascend to the "Goodstart early learning". New

Association gets lessons from ABC disappointment.

REFERENCES:

Anon., 2006. Auditing Standard ASA 501. pdf. Australia: Auditing and Assurance Standards Board.

Anon., 2014. Provision of ChildCare. Doc. Australia: Australian Government.

Anon., 2017. [Online] Federal Register of Legislation Available at:

https://www.legislation.gov.au/Details/F2017L00693.

15

Anon., 2017. Auditing Standard ASA 2017-1 Amendments to Australian Auditing Standards. May.

Anon., 2017. FAMILY ASSISTANCE LEGISLATION AMENDMENT (CHILD CARE ). [Online] Available at:

https://www.legislation.gov.au/Details/C2011B00095/ab901baa-0503-4964-9456-b5e7c1e07d06.

ARMEDIA, t., 2002. The selling out of children’s services. 1 Dec. 0.

Auditing Standard ASA 2017-1 Amendments to Australian Auditing Standards, 2017. Australian

Government. [Online] Available at: https://www.legislation.gov.au/Details/F2017L00693 [Accessed 15

September 2017].

federal register of legislation, 2015. Auditing Standard ASA 570 Going Concern. [Online] Australia

Available at: www.legislation.gov.au.

Government, A., 2015. Federal Register of Legislation. [Online] Auditing and Assurance Standards Board

Available at: www.legislation.gov.au.

kruger, c., 2009. Lessons to be learnt from ABC Learning's collapse. pdf. Australia: The Sunday Morning

Herald.

Mceobert, A., 2009. ABC Learning Centres Limited –did the annual reports give enough warning?

january. p.17.

Mena, 2016. Developing our education workforce Early Childhood Specialists. (2016).. pdf. Australia.

Rush, E. & Downie, C., 2006. ABC Learning Centres: A case study of Australia’s largest child care

corporation. The Australia Institute, June. p.87.

Teen, M.Y., 2012. The ABC of a corporate collapse. Governance for Stakeholders.

16

Anon., 2017. FAMILY ASSISTANCE LEGISLATION AMENDMENT (CHILD CARE ). [Online] Available at:

https://www.legislation.gov.au/Details/C2011B00095/ab901baa-0503-4964-9456-b5e7c1e07d06.

ARMEDIA, t., 2002. The selling out of children’s services. 1 Dec. 0.

Auditing Standard ASA 2017-1 Amendments to Australian Auditing Standards, 2017. Australian

Government. [Online] Available at: https://www.legislation.gov.au/Details/F2017L00693 [Accessed 15

September 2017].

federal register of legislation, 2015. Auditing Standard ASA 570 Going Concern. [Online] Australia

Available at: www.legislation.gov.au.

Government, A., 2015. Federal Register of Legislation. [Online] Auditing and Assurance Standards Board

Available at: www.legislation.gov.au.

kruger, c., 2009. Lessons to be learnt from ABC Learning's collapse. pdf. Australia: The Sunday Morning

Herald.

Mceobert, A., 2009. ABC Learning Centres Limited –did the annual reports give enough warning?

january. p.17.

Mena, 2016. Developing our education workforce Early Childhood Specialists. (2016).. pdf. Australia.

Rush, E. & Downie, C., 2006. ABC Learning Centres: A case study of Australia’s largest child care

corporation. The Australia Institute, June. p.87.

Teen, M.Y., 2012. The ABC of a corporate collapse. Governance for Stakeholders.

16

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.