HI5017 - Activity-Based Costing Model Application in Ooh Media Ltd

VerifiedAdded on 2023/06/12

|13

|2992

|472

Report

AI Summary

This report provides an in-depth analysis of the activity-based costing (ABC) model and its potential application to Ooh Media Limited, a leading out-of-home advertising company in Australia and New Zealand. It details the characteristics of the ABC model, including its ability to divide costs into fixed and variable components and its use of cost drivers to trace overhead costs. The report aligns the ABC model with Ooh Media Limited's mission, objectives, and corporate strategies, highlighting how the model can aid in achieving business goals by classifying activities and developing cost objectives. Recommendations for implementing the ABC model within Ooh Media Limited are provided, emphasizing the importance of management support and cross-functional teams. Finally, the report suggests budgetary control as an alternative management accounting tool and discusses its benefits for planning and controlling business operations. This analysis aims to provide a comprehensive understanding of how the ABC model can enhance costing techniques and support strategic decision-making within Ooh Media Limited.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary:

In this report, sincere attempt is taken for providing a brief discussion of the variety

of aspects, which are inherent in the model of activity-based costing (ABC). The report is

prepared with the intent to shed light on the above-stated model with regards to one of the

entities listed in the “Australian Securities Exchange (ASX)”. To meet this intent, Ooh Media

Limited is considered in this paper. Ooh Media Limited is considered as a leading provider of

the rapidly growing out-of-home advertising sector in Australia and New Zealand.

It has been found that all the business organisations are adopting the ABC model for

enhancing their overall costing system. Moreover, with the help of this model, it is possible

to divide the total costs into fixed costs and variable costs. Furthermore, the management

of Ooh Media Limited could seek essential costing information by utilising the ABC model.

The reason is that such system would help the company in creating effective costing

techniques.

Executive Summary:

In this report, sincere attempt is taken for providing a brief discussion of the variety

of aspects, which are inherent in the model of activity-based costing (ABC). The report is

prepared with the intent to shed light on the above-stated model with regards to one of the

entities listed in the “Australian Securities Exchange (ASX)”. To meet this intent, Ooh Media

Limited is considered in this paper. Ooh Media Limited is considered as a leading provider of

the rapidly growing out-of-home advertising sector in Australia and New Zealand.

It has been found that all the business organisations are adopting the ABC model for

enhancing their overall costing system. Moreover, with the help of this model, it is possible

to divide the total costs into fixed costs and variable costs. Furthermore, the management

of Ooh Media Limited could seek essential costing information by utilising the ABC model.

The reason is that such system would help the company in creating effective costing

techniques.

2MANAGERIAL ACCOUNTING

Table of Contents

Introduction:..............................................................................................................................3

a) Activity-based costing (ABC) model and its characteristics:..................................................3

b) Alignment of ABC model with the present goals and strategies of Ooh Media Limited:.....5

i) Mission and objectives of Ooh Media Limited:..................................................................5

ii) Corporate strategies of Ooh Media Limited:.....................................................................6

iii) Role of ABC model in accomplishing the strategies of Ooh Media Limited:....................6

c) Recommendations regarding the implementation of ABC model for Ooh Media Limited:..8

d) Alternative management accounting tool for Ooh Media Limited:......................................9

Conclusion:...............................................................................................................................10

References:...............................................................................................................................11

Table of Contents

Introduction:..............................................................................................................................3

a) Activity-based costing (ABC) model and its characteristics:..................................................3

b) Alignment of ABC model with the present goals and strategies of Ooh Media Limited:.....5

i) Mission and objectives of Ooh Media Limited:..................................................................5

ii) Corporate strategies of Ooh Media Limited:.....................................................................6

iii) Role of ABC model in accomplishing the strategies of Ooh Media Limited:....................6

c) Recommendations regarding the implementation of ABC model for Ooh Media Limited:..8

d) Alternative management accounting tool for Ooh Media Limited:......................................9

Conclusion:...............................................................................................................................10

References:...............................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Introduction:

In this report, sincere attempt is taken for providing a brief discussion of the variety

of aspects, which are inherent in the model of activity-based costing (ABC). The report is

prepared with the intent to shed light on the above-stated model with regards to one of the

entities listed in the “Australian Securities Exchange (ASX)”. To meet this intent, Ooh Media

Limited is considered in this paper. Ooh Media Limited is considered as a leading provider of

the rapidly growing out-of-home advertising sector in Australia and New Zealand. It has

unparalleled portfolio of digital and classic signs throughout roadside, airport, retail and

place-based media offering in cafes, office towers, bars, universities and fitness venues

(oOh!media AU 2018). Hence, this paper would provide a detailed account of the

characteristics of the ABC model and its implementation process by offering apt suggestions.

a) Activity-based costing (ABC) model and its characteristics:

One of the popular costing tools is the ABC model helping the enterprises to identify

activities carried out forming a part of the business operations. It assigns the products with

indirect costs and importance is laid on the relation among products, activities and costs so

that the goods produced could be assigned with indirect costs with much efficacy, which is

not possible under the conventional costing model (Brooks 2015). Exceptions could be

found where the managers of the enterprises find it extremely hard to assign the products

with some indirect costs in accordance with this model. For instance, it becomes

complicated for the managers and as a result, it might minimise their ability in assign the

same with indirect cost. However, all the necessary cost information are provided under the

ABC model due to which popularity is gained in almost all global industries and companies

Introduction:

In this report, sincere attempt is taken for providing a brief discussion of the variety

of aspects, which are inherent in the model of activity-based costing (ABC). The report is

prepared with the intent to shed light on the above-stated model with regards to one of the

entities listed in the “Australian Securities Exchange (ASX)”. To meet this intent, Ooh Media

Limited is considered in this paper. Ooh Media Limited is considered as a leading provider of

the rapidly growing out-of-home advertising sector in Australia and New Zealand. It has

unparalleled portfolio of digital and classic signs throughout roadside, airport, retail and

place-based media offering in cafes, office towers, bars, universities and fitness venues

(oOh!media AU 2018). Hence, this paper would provide a detailed account of the

characteristics of the ABC model and its implementation process by offering apt suggestions.

a) Activity-based costing (ABC) model and its characteristics:

One of the popular costing tools is the ABC model helping the enterprises to identify

activities carried out forming a part of the business operations. It assigns the products with

indirect costs and importance is laid on the relation among products, activities and costs so

that the goods produced could be assigned with indirect costs with much efficacy, which is

not possible under the conventional costing model (Brooks 2015). Exceptions could be

found where the managers of the enterprises find it extremely hard to assign the products

with some indirect costs in accordance with this model. For instance, it becomes

complicated for the managers and as a result, it might minimise their ability in assign the

same with indirect cost. However, all the necessary cost information are provided under the

ABC model due to which popularity is gained in almost all global industries and companies

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

irrespective of their nature and size (Benson et al. 2015). The role of ABC model is significant

in some major business areas that include product line profitability analysis, analysis of

customer profitability, target costing and others. Hence, the applicability of the ABC model

is widely popular in all types of business organisations. This model has a certain set of

characteristics, which are described as follows:

It is possible to distribute the overall costs as variable costs and fixed costs with the

help of ABC model application. As a result, this division of cost eases the process of

the organisations in enforcing effective pricing strategies based on their industry

movements and cost operations (Edmonds et al. 2016).

The patterns in cost behaviour could be compared easily in the costing operations of

the organisations.

Adequate benefits could be obtained by using this model, as the patterns of cost

behaviour could be associated with different aspects like volume, time, diversity and

other events related to cost.

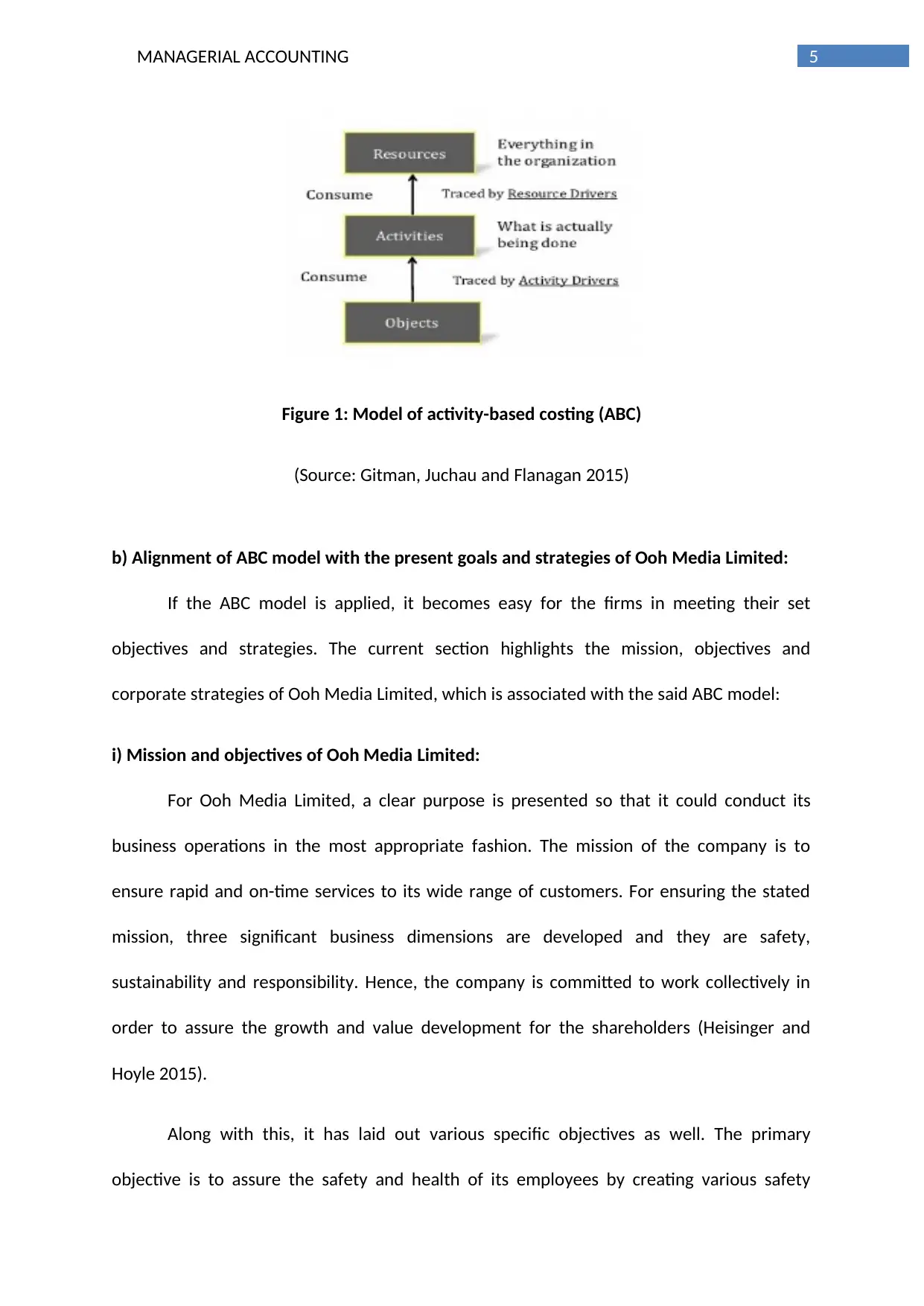

In order to trace the overhead costs to the products or services, the cost drivers are

identified under the ABC model (Gitman 2014).

The managers of the business firms find it relatively easy to state the cost behaviour

patterns with the help of the identified cost drivers.

irrespective of their nature and size (Benson et al. 2015). The role of ABC model is significant

in some major business areas that include product line profitability analysis, analysis of

customer profitability, target costing and others. Hence, the applicability of the ABC model

is widely popular in all types of business organisations. This model has a certain set of

characteristics, which are described as follows:

It is possible to distribute the overall costs as variable costs and fixed costs with the

help of ABC model application. As a result, this division of cost eases the process of

the organisations in enforcing effective pricing strategies based on their industry

movements and cost operations (Edmonds et al. 2016).

The patterns in cost behaviour could be compared easily in the costing operations of

the organisations.

Adequate benefits could be obtained by using this model, as the patterns of cost

behaviour could be associated with different aspects like volume, time, diversity and

other events related to cost.

In order to trace the overhead costs to the products or services, the cost drivers are

identified under the ABC model (Gitman 2014).

The managers of the business firms find it relatively easy to state the cost behaviour

patterns with the help of the identified cost drivers.

5MANAGERIAL ACCOUNTING

Figure 1: Model of activity-based costing (ABC)

(Source: Gitman, Juchau and Flanagan 2015)

b) Alignment of ABC model with the present goals and strategies of Ooh Media Limited:

If the ABC model is applied, it becomes easy for the firms in meeting their set

objectives and strategies. The current section highlights the mission, objectives and

corporate strategies of Ooh Media Limited, which is associated with the said ABC model:

i) Mission and objectives of Ooh Media Limited:

For Ooh Media Limited, a clear purpose is presented so that it could conduct its

business operations in the most appropriate fashion. The mission of the company is to

ensure rapid and on-time services to its wide range of customers. For ensuring the stated

mission, three significant business dimensions are developed and they are safety,

sustainability and responsibility. Hence, the company is committed to work collectively in

order to assure the growth and value development for the shareholders (Heisinger and

Hoyle 2015).

Along with this, it has laid out various specific objectives as well. The primary

objective is to assure the safety and health of its employees by creating various safety

Figure 1: Model of activity-based costing (ABC)

(Source: Gitman, Juchau and Flanagan 2015)

b) Alignment of ABC model with the present goals and strategies of Ooh Media Limited:

If the ABC model is applied, it becomes easy for the firms in meeting their set

objectives and strategies. The current section highlights the mission, objectives and

corporate strategies of Ooh Media Limited, which is associated with the said ABC model:

i) Mission and objectives of Ooh Media Limited:

For Ooh Media Limited, a clear purpose is presented so that it could conduct its

business operations in the most appropriate fashion. The mission of the company is to

ensure rapid and on-time services to its wide range of customers. For ensuring the stated

mission, three significant business dimensions are developed and they are safety,

sustainability and responsibility. Hence, the company is committed to work collectively in

order to assure the growth and value development for the shareholders (Heisinger and

Hoyle 2015).

Along with this, it has laid out various specific objectives as well. The primary

objective is to assure the safety and health of its employees by creating various safety

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

principles and standards. The second objective takes into account the achievement of the

business targets and objectives by working in combination. Finally, it intends to assure

business integrity and mutual respect with the associated stakeholders.

ii) Corporate strategies of Ooh Media Limited:

Ooh Media Limited has a range of activities that help in driving the business

operations. Based on the significant strategies, the organisation intends to become the

leading advertising provider by providing effective out-of-home advertising services. Hence,

the company is needed to raise its level of productivity by gaining adequate knowledge of

the critical risks. Hence, the company is involved in working with combination so that the

overall objectives could be achieved. When these strategies are applied, Ooh Media Limited

could ensure competitive advantage in the out-of-home advertising sector.

iii) Role of ABC model in accomplishing the strategies of Ooh Media Limited:

It has already been dissected that the popularity of ABC model has increased over

the years widely, especially in manufacturing sector, mining sector, service sector and

others. In this respect, it is to be mentioned that Ooh Media Limited is considered as a

leading provider of the rapidly growing out-of-home advertising sector in Australia and New

Zealand. This helps in developing an organisational strategy through which certain

advantages are bound to be sought by implementing the ABC model and ultimately, this

would result in accomplishment of business objectives and goals (Lawrence 2016).

The adoption of the ABC system in Ooh Media Limited would classify the out-of-

home advertising industry into certain significant categories. The main categories are the

following:

principles and standards. The second objective takes into account the achievement of the

business targets and objectives by working in combination. Finally, it intends to assure

business integrity and mutual respect with the associated stakeholders.

ii) Corporate strategies of Ooh Media Limited:

Ooh Media Limited has a range of activities that help in driving the business

operations. Based on the significant strategies, the organisation intends to become the

leading advertising provider by providing effective out-of-home advertising services. Hence,

the company is needed to raise its level of productivity by gaining adequate knowledge of

the critical risks. Hence, the company is involved in working with combination so that the

overall objectives could be achieved. When these strategies are applied, Ooh Media Limited

could ensure competitive advantage in the out-of-home advertising sector.

iii) Role of ABC model in accomplishing the strategies of Ooh Media Limited:

It has already been dissected that the popularity of ABC model has increased over

the years widely, especially in manufacturing sector, mining sector, service sector and

others. In this respect, it is to be mentioned that Ooh Media Limited is considered as a

leading provider of the rapidly growing out-of-home advertising sector in Australia and New

Zealand. This helps in developing an organisational strategy through which certain

advantages are bound to be sought by implementing the ABC model and ultimately, this

would result in accomplishment of business objectives and goals (Lawrence 2016).

The adoption of the ABC system in Ooh Media Limited would classify the out-of-

home advertising industry into certain significant categories. The main categories are the

following:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

Processing activities

Input activities

Administrative activities

Support activities

The enforcement of the ABC model in the organisation would recognise five various

activity levels that constitute of batch-level activities, unit-level activities, factory-level

activities, service-level activities and consumer-level activities. The unit-level activities take

place when each service is formulated within the organisation. The batch-level activities are

inherent when the organisation carries out the production process in unit groups. The

service-level activities are those that support the service formulation design for specific

services. For seeking advantages from the service formulation process, the use of facility-

level activities is made (Narayanaswamy 2017). Hence, it could be cited that the ABC system

would help Ooh Media Limited for assisting the classification of repetitive and non-

repetitive production activities.

In addition, ABC model helps the organisation in developing relationship between cost

activities and cost drivers. The development of cause and effect relation could be made

through the cost drivers and from this relationship; it would be possible to develop the cost

objectives. After seeking help from the resource drivers, the management of Ooh Media

Limited finds it easy to measure the services that each activity has consumed. On the other

hand, these activities would assist Ooh Media Limited to measure the demand intensity and

frequency developed on the basis of the ABC model (Osadchy and Akhmetshin 2015).

However, the adoption of the ABC system might place the cost accountants of Ooh

Media Limited in a position where certain problems are bound to be inherent while

Processing activities

Input activities

Administrative activities

Support activities

The enforcement of the ABC model in the organisation would recognise five various

activity levels that constitute of batch-level activities, unit-level activities, factory-level

activities, service-level activities and consumer-level activities. The unit-level activities take

place when each service is formulated within the organisation. The batch-level activities are

inherent when the organisation carries out the production process in unit groups. The

service-level activities are those that support the service formulation design for specific

services. For seeking advantages from the service formulation process, the use of facility-

level activities is made (Narayanaswamy 2017). Hence, it could be cited that the ABC system

would help Ooh Media Limited for assisting the classification of repetitive and non-

repetitive production activities.

In addition, ABC model helps the organisation in developing relationship between cost

activities and cost drivers. The development of cause and effect relation could be made

through the cost drivers and from this relationship; it would be possible to develop the cost

objectives. After seeking help from the resource drivers, the management of Ooh Media

Limited finds it easy to measure the services that each activity has consumed. On the other

hand, these activities would assist Ooh Media Limited to measure the demand intensity and

frequency developed on the basis of the ABC model (Osadchy and Akhmetshin 2015).

However, the adoption of the ABC system might place the cost accountants of Ooh

Media Limited in a position where certain problems are bound to be inherent while

8MANAGERIAL ACCOUNTING

selecting the cost drivers. This mandates the need for trade-off accuracy in contrast to the

issues inherent in the ABC model. As a result, all the similar cost drivers are to be grouped in

a single pool of cost. When the process is complete, the management of Ooh Media Limited

is needed to apply the cost pools in the service line by making application of the rates of

cost driver based on the number of transactions (Titman and Martin 2014).

When the ABC system is applied in the context of the above-depicted processes, the

managers of Ooh Media Limited would possess all the essential cost information about the

total manufacturing system. At the time there is presence of required costing information,

the managers of the organisation might find it easy in optimising the costs of the products

so as to ensure its business objectives and goals.

c) Recommendations regarding the implementation of ABC model for Ooh Media Limited:

Several techniques are present through which it is possible to implement the ABC

model for Ooh Media Limited. Out of them, two most feasible recommendations are

provided in the context of the organisation, which are enumerated briefly as follows:

Initially, it is recommended to the higher-level management of Ooh Media Limited to

support the implementation of this model within the organisation. Therefore, it is

crucial for the organisation to consider the role of the cross-functional team to

handle the aspects associated with the adoption of the ABC system. Hence, the top

management of the organisation is needed to deliver all the required resources to

the formulated team so as to ensure suitable implementation of the ABC system

within the organisation (Warren and Jones 2018).

selecting the cost drivers. This mandates the need for trade-off accuracy in contrast to the

issues inherent in the ABC model. As a result, all the similar cost drivers are to be grouped in

a single pool of cost. When the process is complete, the management of Ooh Media Limited

is needed to apply the cost pools in the service line by making application of the rates of

cost driver based on the number of transactions (Titman and Martin 2014).

When the ABC system is applied in the context of the above-depicted processes, the

managers of Ooh Media Limited would possess all the essential cost information about the

total manufacturing system. At the time there is presence of required costing information,

the managers of the organisation might find it easy in optimising the costs of the products

so as to ensure its business objectives and goals.

c) Recommendations regarding the implementation of ABC model for Ooh Media Limited:

Several techniques are present through which it is possible to implement the ABC

model for Ooh Media Limited. Out of them, two most feasible recommendations are

provided in the context of the organisation, which are enumerated briefly as follows:

Initially, it is recommended to the higher-level management of Ooh Media Limited to

support the implementation of this model within the organisation. Therefore, it is

crucial for the organisation to consider the role of the cross-functional team to

handle the aspects associated with the adoption of the ABC system. Hence, the top

management of the organisation is needed to deliver all the required resources to

the formulated team so as to ensure suitable implementation of the ABC system

within the organisation (Warren and Jones 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

There is presence of two important factors because of which the top management of

Ooh Media Limited is advised to support the implementation of this system. At the

time the management fails to provide considerable support, the employees of the

organisation might not be willing to accept the change. Moreover, they would

perceive that the system is not important, if the management does not provide

considerable importance to the ABC model (Weygandt, Kimmel and Kieso 2015).

d) Alternative management accounting tool for Ooh Media Limited:

Except the ABC model, there is availability of certain management accounting tools

available for use of the global business organisations. Among them, budgetary control is

deemed to be the most suitable for Ooh Media Limited. The adoption of this technique

would help the organisation in planning and controlling various business operations by

utilising the tool of management accounting. By implementing the tool of budgetary control,

the management of the organisation finds it easy in terms of planning, controlling and

follow-up of the different business operations of the organisation (Weygandt, Kimmel and

Kieso 2015). The budgetary control is observed to have certain benefits, which are

demonstrated briefly as follows:

The corporate firms are able to increase the overall staff performance so that their

business objectives and strategies could be accomplished (White 2014).

In case, the actual expenses exceed the overall expense budgeted for each

department, it would be possible for the management of Ooh Media Limited in

undertaking remedial actions for ensuring better performance and expense control.

When budgetary control is enforced in the business activities of Ooh Media Limited,

adequate amount of information could be obtained about the past events, since it is

There is presence of two important factors because of which the top management of

Ooh Media Limited is advised to support the implementation of this system. At the

time the management fails to provide considerable support, the employees of the

organisation might not be willing to accept the change. Moreover, they would

perceive that the system is not important, if the management does not provide

considerable importance to the ABC model (Weygandt, Kimmel and Kieso 2015).

d) Alternative management accounting tool for Ooh Media Limited:

Except the ABC model, there is availability of certain management accounting tools

available for use of the global business organisations. Among them, budgetary control is

deemed to be the most suitable for Ooh Media Limited. The adoption of this technique

would help the organisation in planning and controlling various business operations by

utilising the tool of management accounting. By implementing the tool of budgetary control,

the management of the organisation finds it easy in terms of planning, controlling and

follow-up of the different business operations of the organisation (Weygandt, Kimmel and

Kieso 2015). The budgetary control is observed to have certain benefits, which are

demonstrated briefly as follows:

The corporate firms are able to increase the overall staff performance so that their

business objectives and strategies could be accomplished (White 2014).

In case, the actual expenses exceed the overall expense budgeted for each

department, it would be possible for the management of Ooh Media Limited in

undertaking remedial actions for ensuring better performance and expense control.

When budgetary control is enforced in the business activities of Ooh Media Limited,

adequate amount of information could be obtained about the past events, since it is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

possible to develop effective strategies by utilising the information in order to assure

the non-repeat of such mistakes (Zhang, Hoque and Isa 2015).

Conclusion:

Based on the above discussion, it could be stated that all the business organisations

are adopting the ABC model for enhancing their overall costing system. Moreover, with the

help of this model, it is possible to divide the total costs into fixed costs and variable costs.

Furthermore, the management of Ooh Media Limited could seek essential costing

information by utilising the ABC model. The reason is that such system would help the

company in creating effective costing techniques. Thus, in order to ensure the appropriate

enforcement and adoption of the ABC model, the top management of the company is

required to support the entire process.

However, the adoption of the ABC system might place the cost accountants of Ooh

Media Limited in a position where certain problems are bound to be inherent while

selecting the cost drivers. This mandates the need for trade-off accuracy in contrast to the

issues inherent in the ABC model. As a result, all the similar cost drivers are to be grouped in

a single pool of cost. When the process is complete, the management of Ooh Media Limited

is needed to apply the cost pools in the service line by making application of the rates of

cost driver based on the number of transactions.

possible to develop effective strategies by utilising the information in order to assure

the non-repeat of such mistakes (Zhang, Hoque and Isa 2015).

Conclusion:

Based on the above discussion, it could be stated that all the business organisations

are adopting the ABC model for enhancing their overall costing system. Moreover, with the

help of this model, it is possible to divide the total costs into fixed costs and variable costs.

Furthermore, the management of Ooh Media Limited could seek essential costing

information by utilising the ABC model. The reason is that such system would help the

company in creating effective costing techniques. Thus, in order to ensure the appropriate

enforcement and adoption of the ABC model, the top management of the company is

required to support the entire process.

However, the adoption of the ABC system might place the cost accountants of Ooh

Media Limited in a position where certain problems are bound to be inherent while

selecting the cost drivers. This mandates the need for trade-off accuracy in contrast to the

issues inherent in the ABC model. As a result, all the similar cost drivers are to be grouped in

a single pool of cost. When the process is complete, the management of Ooh Media Limited

is needed to apply the cost pools in the service line by making application of the rates of

cost driver based on the number of transactions.

11MANAGERIAL ACCOUNTING

References:

Benson, K., Clarkson, P.M., Smith, T. and Tutticci, I., 2015. A review of accounting research in

the Asia Pacific region. Australian Journal of Management, 40(1), pp.36-88.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Edmonds, T.P., Edmonds, C.D., Tsay, B.Y. and Olds, P.R., 2016. Fundamental managerial

accounting concepts. McGraw-Hill Education.

Gitman, L.J., 2014. Principles of Managerial Finance, Student Value Edition+ New

Myfinancelab with Pearson Etext... Prentice Hall.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Heisinger, K. and Hoyle, J., 2015. Managerial Accounting.

Lawrence, J.G., 2016. Principles of managerial finance.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd.

oOh!media AU., 2018. Billboards Australia | oOh!media. [online] Available at:

https://www.oohmedia.com.au/about-ooh/ [Accessed 28 May 2018].

Osadchy, E.A. and Akhmetshin, E.M., 2015. Accounting and control of indirect costs of

organization as a condition of optimizing its financial and economic activities. International

Business Management, 9(7), pp.1705-1709.

Titman, S. and Martin, J.D., 2014. Valuation. Pearson Higher Ed.

References:

Benson, K., Clarkson, P.M., Smith, T. and Tutticci, I., 2015. A review of accounting research in

the Asia Pacific region. Australian Journal of Management, 40(1), pp.36-88.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Edmonds, T.P., Edmonds, C.D., Tsay, B.Y. and Olds, P.R., 2016. Fundamental managerial

accounting concepts. McGraw-Hill Education.

Gitman, L.J., 2014. Principles of Managerial Finance, Student Value Edition+ New

Myfinancelab with Pearson Etext... Prentice Hall.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Heisinger, K. and Hoyle, J., 2015. Managerial Accounting.

Lawrence, J.G., 2016. Principles of managerial finance.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd.

oOh!media AU., 2018. Billboards Australia | oOh!media. [online] Available at:

https://www.oohmedia.com.au/about-ooh/ [Accessed 28 May 2018].

Osadchy, E.A. and Akhmetshin, E.M., 2015. Accounting and control of indirect costs of

organization as a condition of optimizing its financial and economic activities. International

Business Management, 9(7), pp.1705-1709.

Titman, S. and Martin, J.D., 2014. Valuation. Pearson Higher Ed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.