Financial Analysis Report: ABC Retail Company (2016-2018)

VerifiedAdded on 2023/06/08

|11

|1823

|456

Report

AI Summary

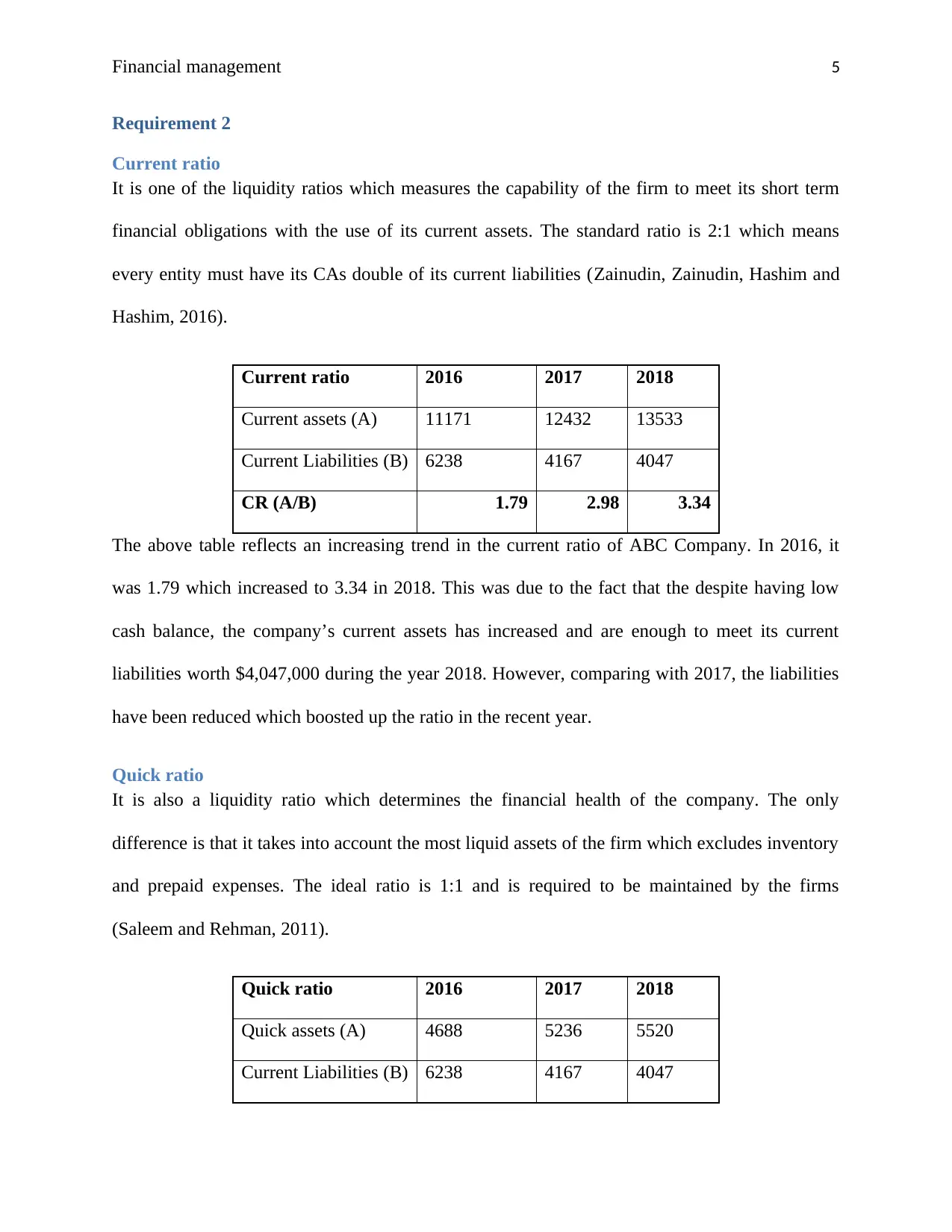

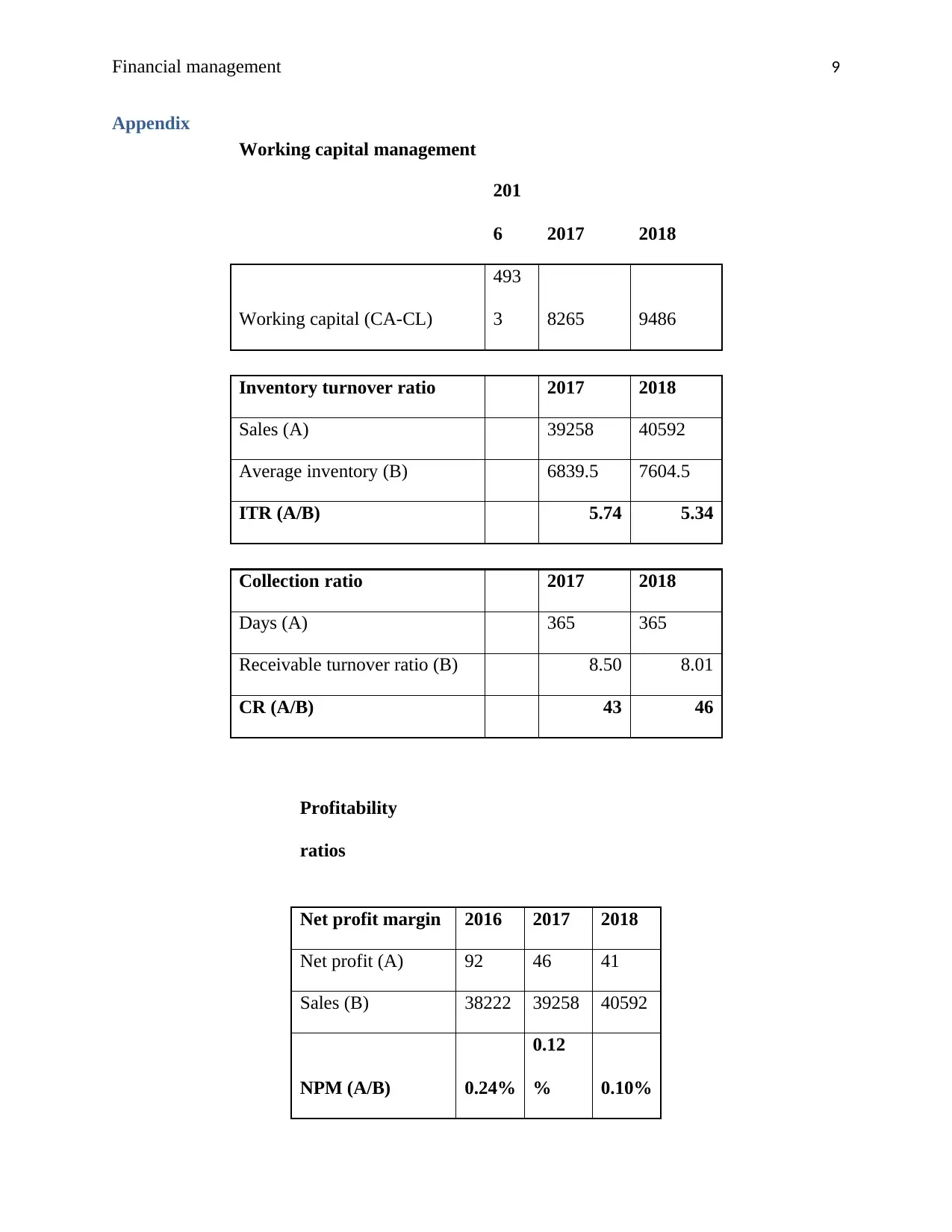

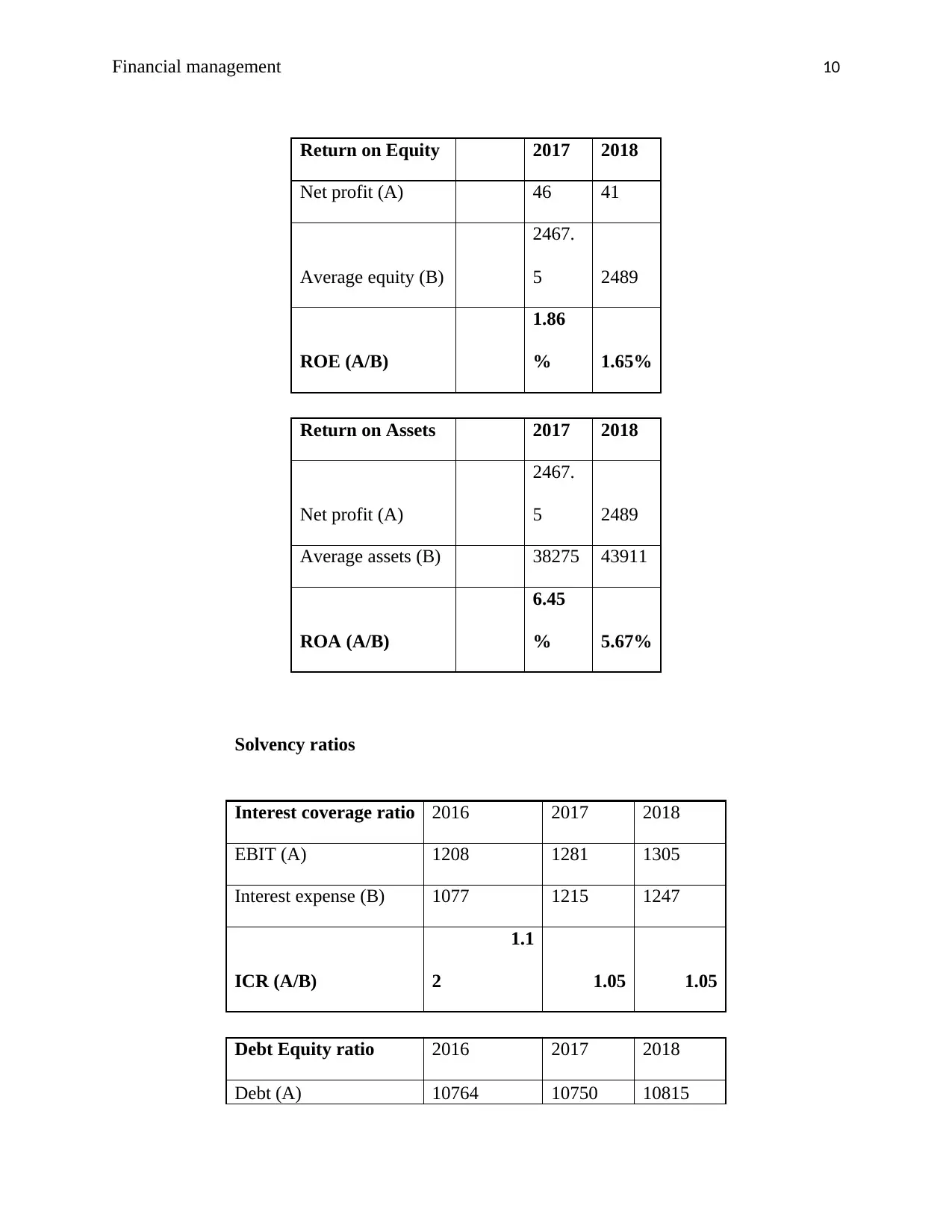

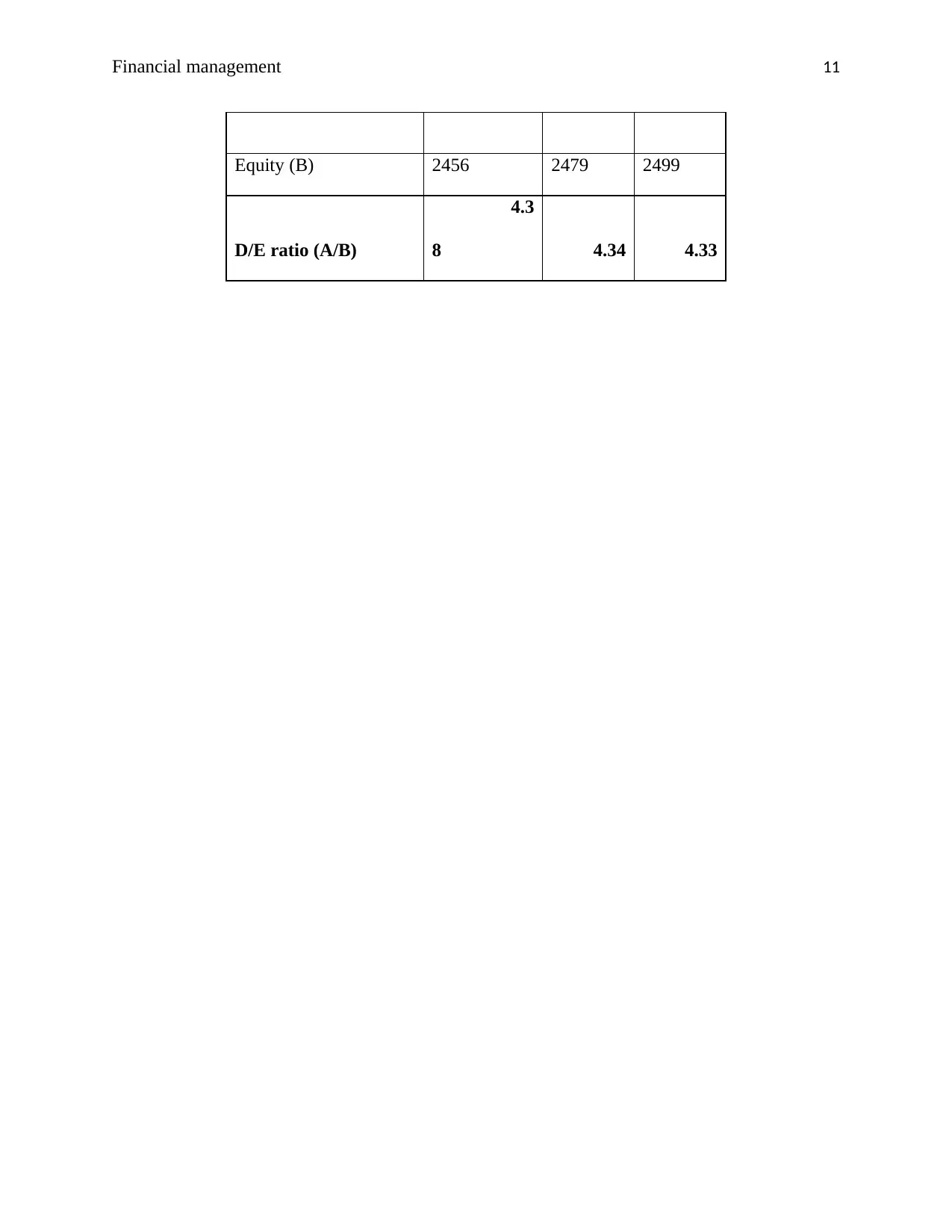

This report provides a comprehensive financial analysis of ABC Retail Company for the period of 2016-2018. The analysis includes the calculation of share price and market capitalization as of June 30, 2018, along with a comparison of the company's P/E ratio to the industry average. The report assesses the company's liquidity through current and quick ratios, evaluating its working capital management using inventory turnover and collection ratios. Profitability is examined through profit margins, ROE, and ROA, while solvency is evaluated using the interest coverage ratio and debt-to-equity ratio. The analysis highlights trends in these ratios, providing insights into the company's financial health, performance, and potential for investment or lending, concluding with an assessment of the company's overall financial position and recommendations for improvement.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.