Case Study: Comparing ABC and Traditional Costing at Danbake Ltd

VerifiedAdded on 2023/06/10

|5

|790

|357

Case Study

AI Summary

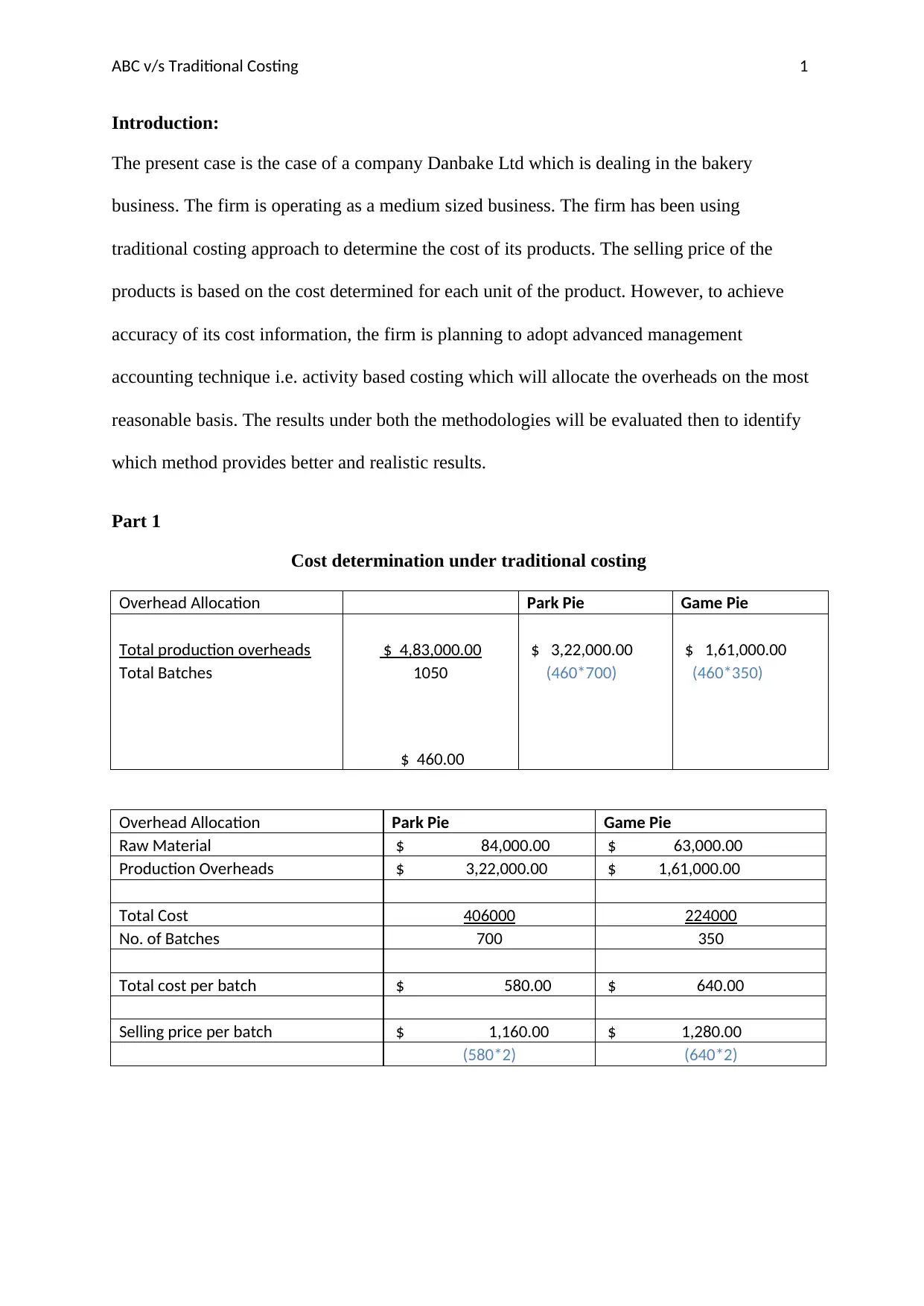

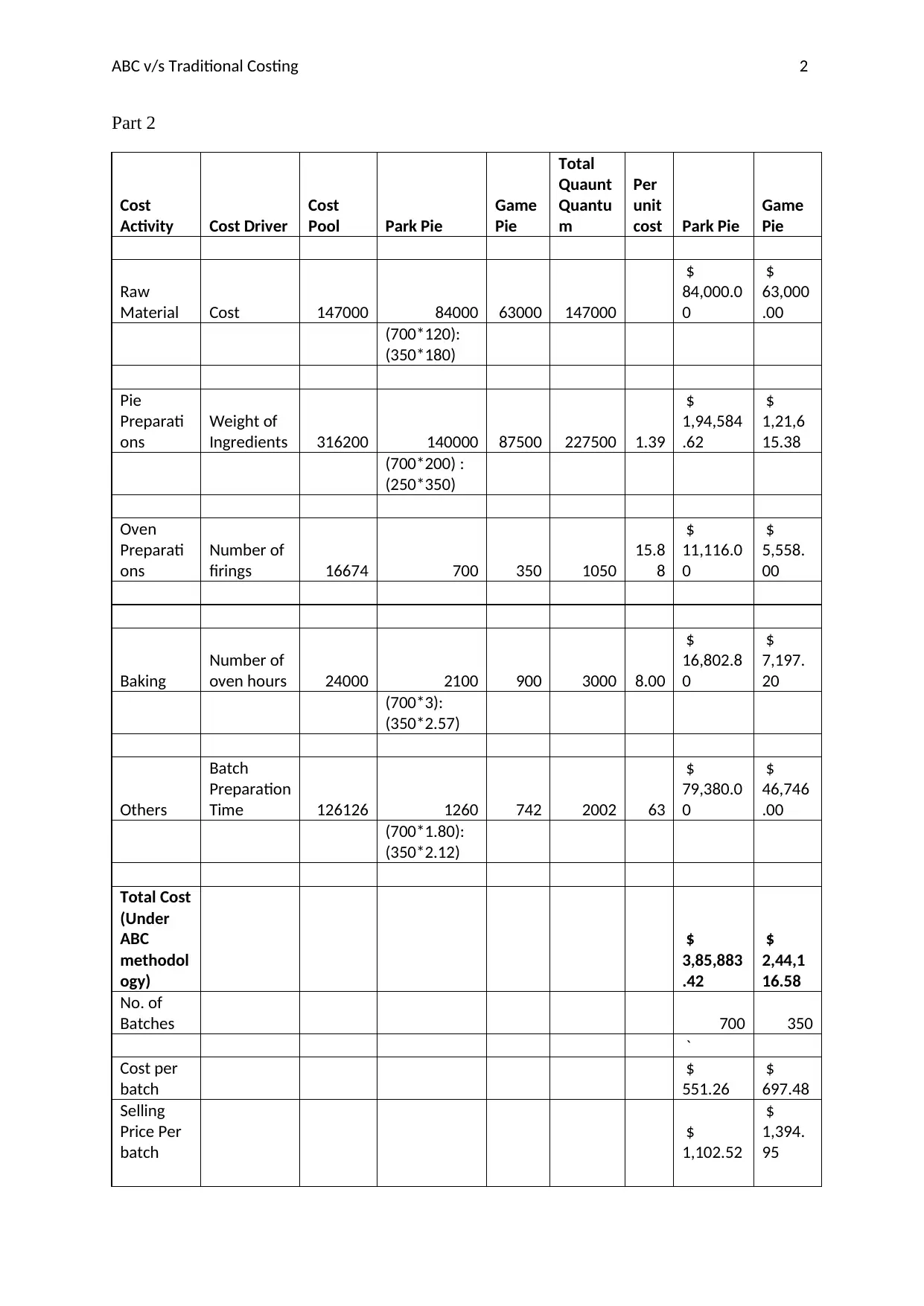

This case study analyzes Danbake Ltd., a bakery company, and its transition from traditional costing to Activity Based Costing (ABC). The assignment details the traditional costing approach, including overhead allocation and cost determination for Park Pie and Game Pie. It then presents the ABC method, identifying cost drivers for various activities like raw material, preparation, and baking. A comparison of the results highlights that traditional costing overvalues Park Pie and undervalues Game Pie compared to ABC. The study concludes that ABC provides more accurate product costing by allocating overhead costs based on actual resource consumption, recommending that Danbake Ltd. adopt ABC for improved cost management and decision-making. The assignment references key cost accounting texts and provides detailed calculations under both methodologies.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.