Dissertation: Examining the Link Between Cash Holdings & Audit Fees

VerifiedAdded on 2023/06/08

|17

|4938

|468

Dissertation

AI Summary

This dissertation investigates the relationship between abnormal cash holdings and audit fees for 50 companies listed on the FTSE 100 index, utilizing correlation and regression analysis. Descriptive statistics reveal that, on average, these companies hold lower cash reserves than optimal, with a negative median indicating that over half the companies have less cash than required. Correlation analysis indicates a weak negative relationship between abnormal cash holdings and both firm size and audit fees. Regression analysis suggests that firms with lower-than-optimal cash holdings tend to pay higher audit fees, possibly due to increased auditor scrutiny of their liquidity. Furthermore, the study confirms a positive correlation between firm size and audit fees, indicating that larger companies are charged higher audit fees. The findings support the alternative hypothesis that abnormal cash holdings influence audit fees, and that larger firm size leads to increased audit costs.

DISSERTATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

CHAPTER 4: DATA ANALYSIS AND FINDINGS.....................................................................3

Descriptive Statistics...................................................................................................................3

Correlation...................................................................................................................................5

Regression....................................................................................................................................6

DISCUSSION................................................................................................................................11

REFERENCES..............................................................................................................................15

Books and Journals....................................................................................................................15

APPENDIX....................................................................................................................................16

Frequency table..........................................................................................................................16

CHAPTER 4: DATA ANALYSIS AND FINDINGS.....................................................................3

Descriptive Statistics...................................................................................................................3

Correlation...................................................................................................................................5

Regression....................................................................................................................................6

DISCUSSION................................................................................................................................11

REFERENCES..............................................................................................................................15

Books and Journals....................................................................................................................15

APPENDIX....................................................................................................................................16

Frequency table..........................................................................................................................16

CHAPTER 4: DATA ANALYSIS AND FINDINGS

This section of the dissertation will analyze the data collected regarding abnormal cash

holdings and audit fees of 50 companies listed on the FTSE 100 index using correlation and

regression tools. Further, the interpretation of the outcome will also be covered in this section to

assess whether the null hypothesis is accepted or an alternative hypothesis.

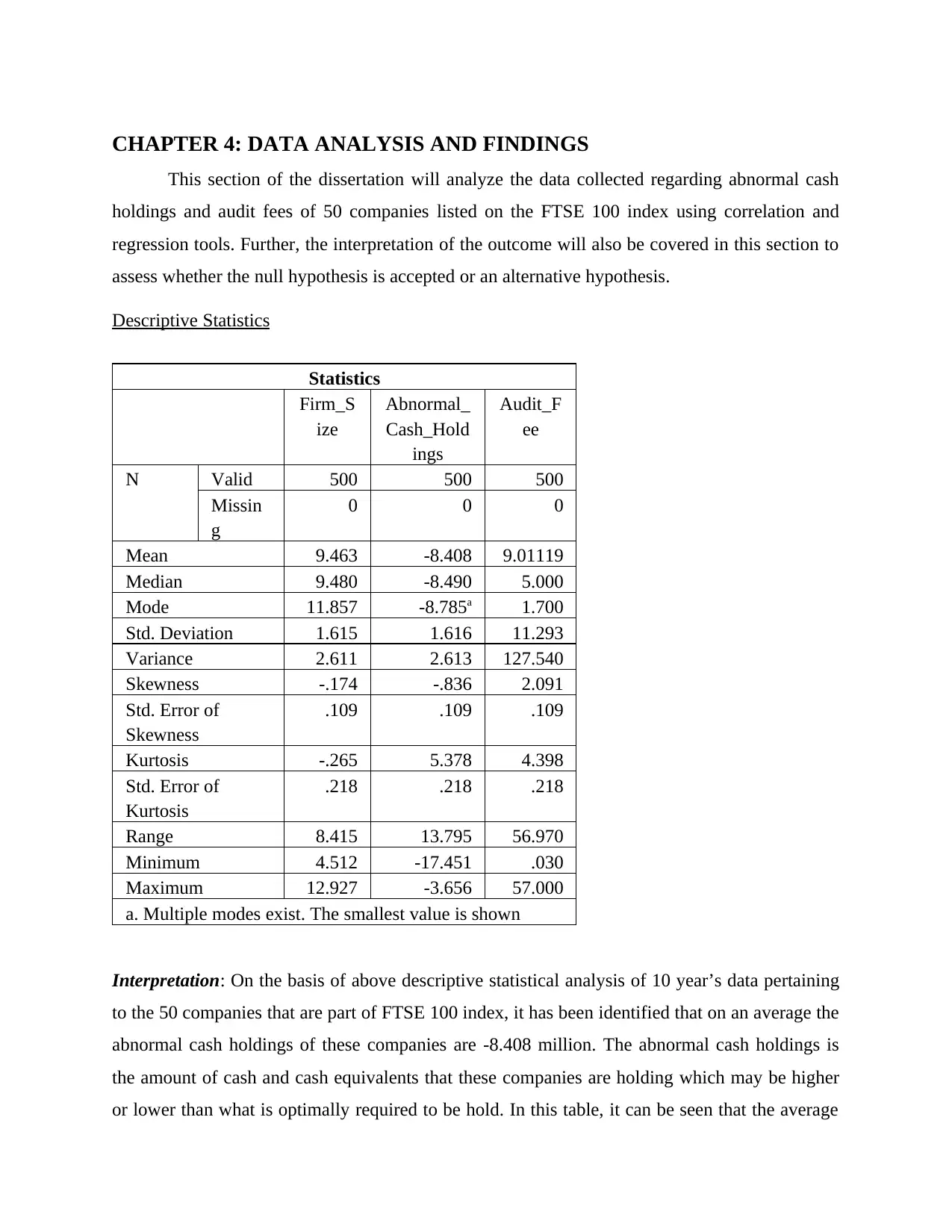

Descriptive Statistics

Statistics

Firm_S

ize

Abnormal_

Cash_Hold

ings

Audit_F

ee

N Valid 500 500 500

Missin

g

0 0 0

Mean 9.463 -8.408 9.01119

Median 9.480 -8.490 5.000

Mode 11.857 -8.785a 1.700

Std. Deviation 1.615 1.616 11.293

Variance 2.611 2.613 127.540

Skewness -.174 -.836 2.091

Std. Error of

Skewness

.109 .109 .109

Kurtosis -.265 5.378 4.398

Std. Error of

Kurtosis

.218 .218 .218

Range 8.415 13.795 56.970

Minimum 4.512 -17.451 .030

Maximum 12.927 -3.656 57.000

a. Multiple modes exist. The smallest value is shown

Interpretation: On the basis of above descriptive statistical analysis of 10 year’s data pertaining

to the 50 companies that are part of FTSE 100 index, it has been identified that on an average the

abnormal cash holdings of these companies are -8.408 million. The abnormal cash holdings is

the amount of cash and cash equivalents that these companies are holding which may be higher

or lower than what is optimally required to be hold. In this table, it can be seen that the average

This section of the dissertation will analyze the data collected regarding abnormal cash

holdings and audit fees of 50 companies listed on the FTSE 100 index using correlation and

regression tools. Further, the interpretation of the outcome will also be covered in this section to

assess whether the null hypothesis is accepted or an alternative hypothesis.

Descriptive Statistics

Statistics

Firm_S

ize

Abnormal_

Cash_Hold

ings

Audit_F

ee

N Valid 500 500 500

Missin

g

0 0 0

Mean 9.463 -8.408 9.01119

Median 9.480 -8.490 5.000

Mode 11.857 -8.785a 1.700

Std. Deviation 1.615 1.616 11.293

Variance 2.611 2.613 127.540

Skewness -.174 -.836 2.091

Std. Error of

Skewness

.109 .109 .109

Kurtosis -.265 5.378 4.398

Std. Error of

Kurtosis

.218 .218 .218

Range 8.415 13.795 56.970

Minimum 4.512 -17.451 .030

Maximum 12.927 -3.656 57.000

a. Multiple modes exist. The smallest value is shown

Interpretation: On the basis of above descriptive statistical analysis of 10 year’s data pertaining

to the 50 companies that are part of FTSE 100 index, it has been identified that on an average the

abnormal cash holdings of these companies are -8.408 million. The abnormal cash holdings is

the amount of cash and cash equivalents that these companies are holding which may be higher

or lower than what is optimally required to be hold. In this table, it can be seen that the average

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

abnormal cash holdings are of 50 companies in the period of past ten years have come out to be

negative 8.408 which indicates that these companies are holding lower cash and cash equivalents

with them than what is their optimal requirements. Further, negative median of 8.490 indicates

that more than 50% companies are having lower actual cash than optimal cash to the extent of

8.490 million approximately and accordingly, their abnormal cash holdings are deviating from

average just by 1.616%. Further, the maximum abnormal cash holdings identified from the 10

year’s data of 50 companies is -17.451 and the minimum abnormal cash holdings of the same is

identified as -3.656 and accordingly, giving the range of 13.795.

Moreover, to have a distribution of data normal, the Kurtosis value must lie in the range

of -1 and +1 and if the identified value is lower or higher, then the distributions are said to be

abnormal. The Kurtosis value determined for the abnormal cash holdings of 50 companies for

the past 10 years is 5.378. So, due to this value being greater than 1, the distribution would

definitely be too peaked. On looking at the skewness of the distribution, the value identified for

abnormal cash holdings is -0.836 which is falling in the range of -0.5 and -1 and thus indicating

the data concerning the past 10 year’s abnormal cash holdings of 50 companies are moderately

skewed.

Moving on to the descriptive statistics of firm size, the average firm size of 50 companies

for the past 10 years is identified as 9.463 and through median, it has been determined that more

than 50% companies are having their firm size as 9.480 approximately and the standard

deviation shows that the firm size of these companies are deviating from average by 1.615%.

The maximum firm size of 12.927 is being reported by Shell plc in the year 2016 while the

minimum firm size of 4.512 is being reported by Entain plc in the year 2012. This in turn gives

the range of 8.415. The Kurtosis value for the firm size data of 50 companies for past 10 years is

identified as -0.265 which is neither greater than +1 nor less than -1 and on this basis, it can be

said that the distribution is neither peaked or flatter too much and thus, is normal. The skewness

for the data of firm size comes out as -0.174 and due to falling in the range of -0.5 and 0.5, it can

be said that the data are symmetrical in a fair manner.

The third variable of interest concerning this study is the audit fees charged from the 50

companies of FTSE 100 index for the last ten years. The above descriptive statistics table shows

that the average fee paid by 50 companies in the last ten years is 9.0 million and more than 50%

negative 8.408 which indicates that these companies are holding lower cash and cash equivalents

with them than what is their optimal requirements. Further, negative median of 8.490 indicates

that more than 50% companies are having lower actual cash than optimal cash to the extent of

8.490 million approximately and accordingly, their abnormal cash holdings are deviating from

average just by 1.616%. Further, the maximum abnormal cash holdings identified from the 10

year’s data of 50 companies is -17.451 and the minimum abnormal cash holdings of the same is

identified as -3.656 and accordingly, giving the range of 13.795.

Moreover, to have a distribution of data normal, the Kurtosis value must lie in the range

of -1 and +1 and if the identified value is lower or higher, then the distributions are said to be

abnormal. The Kurtosis value determined for the abnormal cash holdings of 50 companies for

the past 10 years is 5.378. So, due to this value being greater than 1, the distribution would

definitely be too peaked. On looking at the skewness of the distribution, the value identified for

abnormal cash holdings is -0.836 which is falling in the range of -0.5 and -1 and thus indicating

the data concerning the past 10 year’s abnormal cash holdings of 50 companies are moderately

skewed.

Moving on to the descriptive statistics of firm size, the average firm size of 50 companies

for the past 10 years is identified as 9.463 and through median, it has been determined that more

than 50% companies are having their firm size as 9.480 approximately and the standard

deviation shows that the firm size of these companies are deviating from average by 1.615%.

The maximum firm size of 12.927 is being reported by Shell plc in the year 2016 while the

minimum firm size of 4.512 is being reported by Entain plc in the year 2012. This in turn gives

the range of 8.415. The Kurtosis value for the firm size data of 50 companies for past 10 years is

identified as -0.265 which is neither greater than +1 nor less than -1 and on this basis, it can be

said that the distribution is neither peaked or flatter too much and thus, is normal. The skewness

for the data of firm size comes out as -0.174 and due to falling in the range of -0.5 and 0.5, it can

be said that the data are symmetrical in a fair manner.

The third variable of interest concerning this study is the audit fees charged from the 50

companies of FTSE 100 index for the last ten years. The above descriptive statistics table shows

that the average fee paid by 50 companies in the last ten years is 9.0 million and more than 50%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

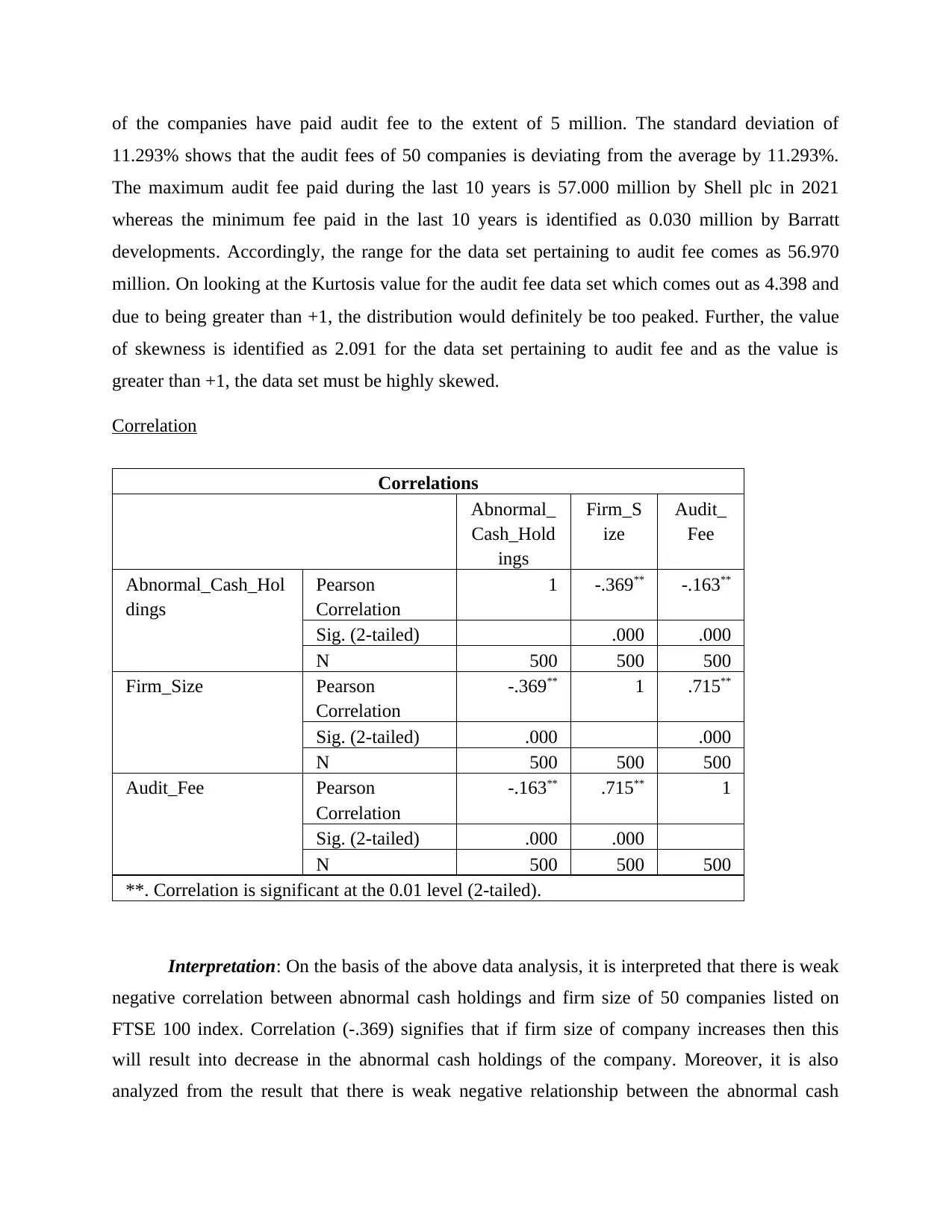

of the companies have paid audit fee to the extent of 5 million. The standard deviation of

11.293% shows that the audit fees of 50 companies is deviating from the average by 11.293%.

The maximum audit fee paid during the last 10 years is 57.000 million by Shell plc in 2021

whereas the minimum fee paid in the last 10 years is identified as 0.030 million by Barratt

developments. Accordingly, the range for the data set pertaining to audit fee comes as 56.970

million. On looking at the Kurtosis value for the audit fee data set which comes out as 4.398 and

due to being greater than +1, the distribution would definitely be too peaked. Further, the value

of skewness is identified as 2.091 for the data set pertaining to audit fee and as the value is

greater than +1, the data set must be highly skewed.

Correlation

Correlations

Abnormal_

Cash_Hold

ings

Firm_S

ize

Audit_

Fee

Abnormal_Cash_Hol

dings

Pearson

Correlation

1 -.369** -.163**

Sig. (2-tailed) .000 .000

N 500 500 500

Firm_Size Pearson

Correlation

-.369** 1 .715**

Sig. (2-tailed) .000 .000

N 500 500 500

Audit_Fee Pearson

Correlation

-.163** .715** 1

Sig. (2-tailed) .000 .000

N 500 500 500

**. Correlation is significant at the 0.01 level (2-tailed).

Interpretation: On the basis of the above data analysis, it is interpreted that there is weak

negative correlation between abnormal cash holdings and firm size of 50 companies listed on

FTSE 100 index. Correlation (-.369) signifies that if firm size of company increases then this

will result into decrease in the abnormal cash holdings of the company. Moreover, it is also

analyzed from the result that there is weak negative relationship between the abnormal cash

11.293% shows that the audit fees of 50 companies is deviating from the average by 11.293%.

The maximum audit fee paid during the last 10 years is 57.000 million by Shell plc in 2021

whereas the minimum fee paid in the last 10 years is identified as 0.030 million by Barratt

developments. Accordingly, the range for the data set pertaining to audit fee comes as 56.970

million. On looking at the Kurtosis value for the audit fee data set which comes out as 4.398 and

due to being greater than +1, the distribution would definitely be too peaked. Further, the value

of skewness is identified as 2.091 for the data set pertaining to audit fee and as the value is

greater than +1, the data set must be highly skewed.

Correlation

Correlations

Abnormal_

Cash_Hold

ings

Firm_S

ize

Audit_

Fee

Abnormal_Cash_Hol

dings

Pearson

Correlation

1 -.369** -.163**

Sig. (2-tailed) .000 .000

N 500 500 500

Firm_Size Pearson

Correlation

-.369** 1 .715**

Sig. (2-tailed) .000 .000

N 500 500 500

Audit_Fee Pearson

Correlation

-.163** .715** 1

Sig. (2-tailed) .000 .000

N 500 500 500

**. Correlation is significant at the 0.01 level (2-tailed).

Interpretation: On the basis of the above data analysis, it is interpreted that there is weak

negative correlation between abnormal cash holdings and firm size of 50 companies listed on

FTSE 100 index. Correlation (-.369) signifies that if firm size of company increases then this

will result into decrease in the abnormal cash holdings of the company. Moreover, it is also

analyzed from the result that there is weak negative relationship between the abnormal cash

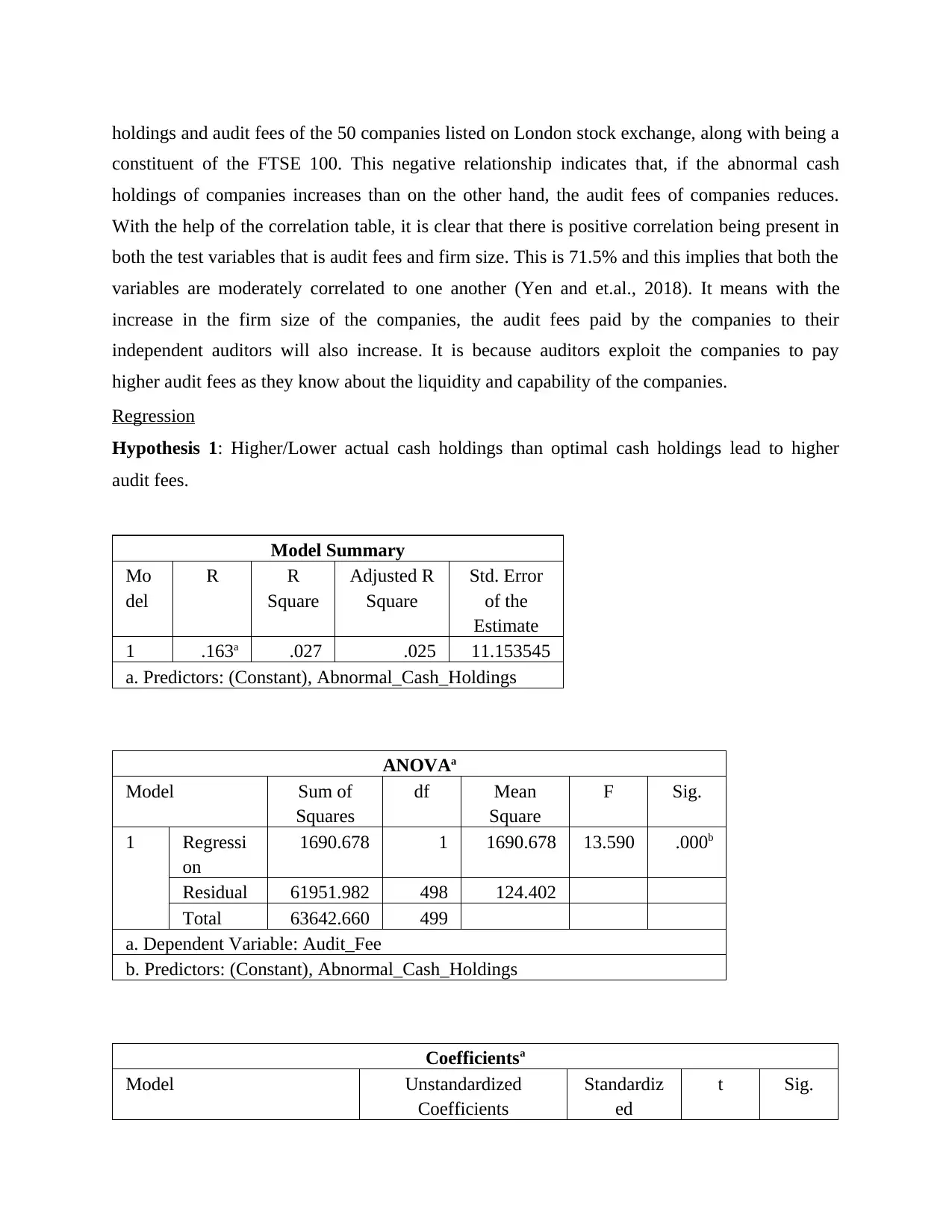

holdings and audit fees of the 50 companies listed on London stock exchange, along with being a

constituent of the FTSE 100. This negative relationship indicates that, if the abnormal cash

holdings of companies increases than on the other hand, the audit fees of companies reduces.

With the help of the correlation table, it is clear that there is positive correlation being present in

both the test variables that is audit fees and firm size. This is 71.5% and this implies that both the

variables are moderately correlated to one another (Yen and et.al., 2018). It means with the

increase in the firm size of the companies, the audit fees paid by the companies to their

independent auditors will also increase. It is because auditors exploit the companies to pay

higher audit fees as they know about the liquidity and capability of the companies.

Regression

Hypothesis 1: Higher/Lower actual cash holdings than optimal cash holdings lead to higher

audit fees.

Model Summary

Mo

del

R R

Square

Adjusted R

Square

Std. Error

of the

Estimate

1 .163a .027 .025 11.153545

a. Predictors: (Constant), Abnormal_Cash_Holdings

ANOVAa

Model Sum of

Squares

df Mean

Square

F Sig.

1 Regressi

on

1690.678 1 1690.678 13.590 .000b

Residual 61951.982 498 124.402

Total 63642.660 499

a. Dependent Variable: Audit_Fee

b. Predictors: (Constant), Abnormal_Cash_Holdings

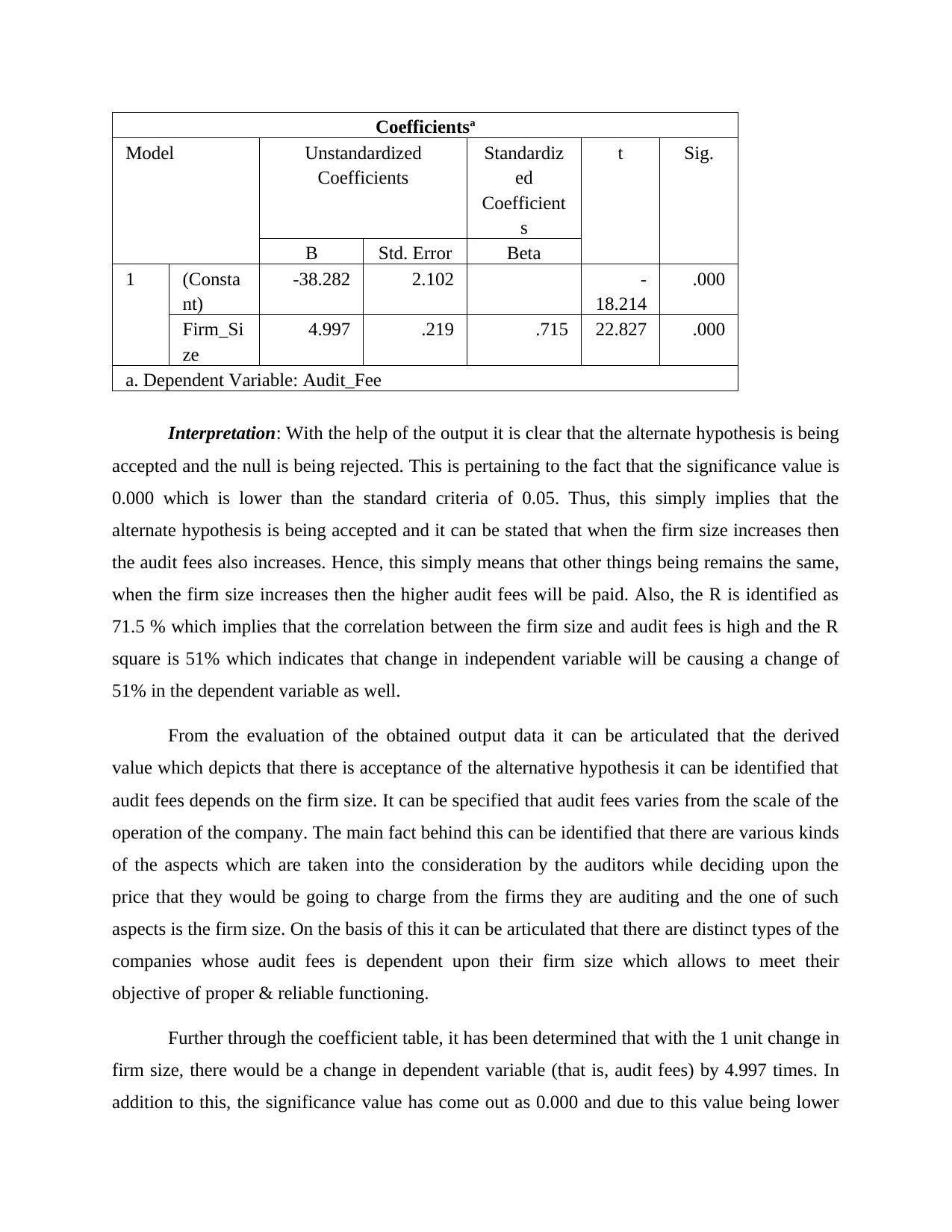

Coefficientsa

Model Unstandardized

Coefficients

Standardiz

ed

t Sig.

constituent of the FTSE 100. This negative relationship indicates that, if the abnormal cash

holdings of companies increases than on the other hand, the audit fees of companies reduces.

With the help of the correlation table, it is clear that there is positive correlation being present in

both the test variables that is audit fees and firm size. This is 71.5% and this implies that both the

variables are moderately correlated to one another (Yen and et.al., 2018). It means with the

increase in the firm size of the companies, the audit fees paid by the companies to their

independent auditors will also increase. It is because auditors exploit the companies to pay

higher audit fees as they know about the liquidity and capability of the companies.

Regression

Hypothesis 1: Higher/Lower actual cash holdings than optimal cash holdings lead to higher

audit fees.

Model Summary

Mo

del

R R

Square

Adjusted R

Square

Std. Error

of the

Estimate

1 .163a .027 .025 11.153545

a. Predictors: (Constant), Abnormal_Cash_Holdings

ANOVAa

Model Sum of

Squares

df Mean

Square

F Sig.

1 Regressi

on

1690.678 1 1690.678 13.590 .000b

Residual 61951.982 498 124.402

Total 63642.660 499

a. Dependent Variable: Audit_Fee

b. Predictors: (Constant), Abnormal_Cash_Holdings

Coefficientsa

Model Unstandardized

Coefficients

Standardiz

ed

t Sig.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

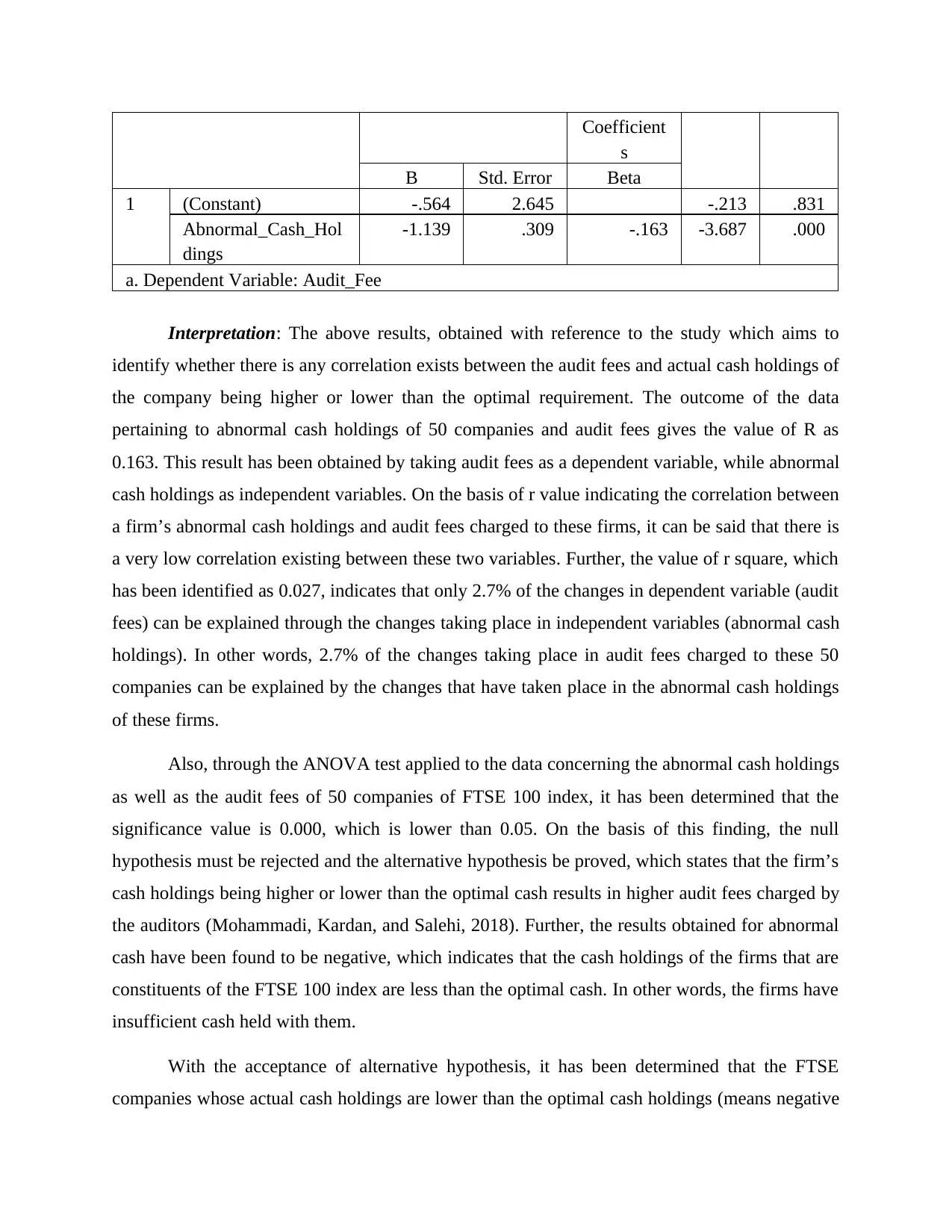

Coefficient

s

B Std. Error Beta

1 (Constant) -.564 2.645 -.213 .831

Abnormal_Cash_Hol

dings

-1.139 .309 -.163 -3.687 .000

a. Dependent Variable: Audit_Fee

Interpretation: The above results, obtained with reference to the study which aims to

identify whether there is any correlation exists between the audit fees and actual cash holdings of

the company being higher or lower than the optimal requirement. The outcome of the data

pertaining to abnormal cash holdings of 50 companies and audit fees gives the value of R as

0.163. This result has been obtained by taking audit fees as a dependent variable, while abnormal

cash holdings as independent variables. On the basis of r value indicating the correlation between

a firm’s abnormal cash holdings and audit fees charged to these firms, it can be said that there is

a very low correlation existing between these two variables. Further, the value of r square, which

has been identified as 0.027, indicates that only 2.7% of the changes in dependent variable (audit

fees) can be explained through the changes taking place in independent variables (abnormal cash

holdings). In other words, 2.7% of the changes taking place in audit fees charged to these 50

companies can be explained by the changes that have taken place in the abnormal cash holdings

of these firms.

Also, through the ANOVA test applied to the data concerning the abnormal cash holdings

as well as the audit fees of 50 companies of FTSE 100 index, it has been determined that the

significance value is 0.000, which is lower than 0.05. On the basis of this finding, the null

hypothesis must be rejected and the alternative hypothesis be proved, which states that the firm’s

cash holdings being higher or lower than the optimal cash results in higher audit fees charged by

the auditors (Mohammadi, Kardan, and Salehi, 2018). Further, the results obtained for abnormal

cash have been found to be negative, which indicates that the cash holdings of the firms that are

constituents of the FTSE 100 index are less than the optimal cash. In other words, the firms have

insufficient cash held with them.

With the acceptance of alternative hypothesis, it has been determined that the FTSE

companies whose actual cash holdings are lower than the optimal cash holdings (means negative

s

B Std. Error Beta

1 (Constant) -.564 2.645 -.213 .831

Abnormal_Cash_Hol

dings

-1.139 .309 -.163 -3.687 .000

a. Dependent Variable: Audit_Fee

Interpretation: The above results, obtained with reference to the study which aims to

identify whether there is any correlation exists between the audit fees and actual cash holdings of

the company being higher or lower than the optimal requirement. The outcome of the data

pertaining to abnormal cash holdings of 50 companies and audit fees gives the value of R as

0.163. This result has been obtained by taking audit fees as a dependent variable, while abnormal

cash holdings as independent variables. On the basis of r value indicating the correlation between

a firm’s abnormal cash holdings and audit fees charged to these firms, it can be said that there is

a very low correlation existing between these two variables. Further, the value of r square, which

has been identified as 0.027, indicates that only 2.7% of the changes in dependent variable (audit

fees) can be explained through the changes taking place in independent variables (abnormal cash

holdings). In other words, 2.7% of the changes taking place in audit fees charged to these 50

companies can be explained by the changes that have taken place in the abnormal cash holdings

of these firms.

Also, through the ANOVA test applied to the data concerning the abnormal cash holdings

as well as the audit fees of 50 companies of FTSE 100 index, it has been determined that the

significance value is 0.000, which is lower than 0.05. On the basis of this finding, the null

hypothesis must be rejected and the alternative hypothesis be proved, which states that the firm’s

cash holdings being higher or lower than the optimal cash results in higher audit fees charged by

the auditors (Mohammadi, Kardan, and Salehi, 2018). Further, the results obtained for abnormal

cash have been found to be negative, which indicates that the cash holdings of the firms that are

constituents of the FTSE 100 index are less than the optimal cash. In other words, the firms have

insufficient cash held with them.

With the acceptance of alternative hypothesis, it has been determined that the FTSE

companies whose actual cash holdings are lower than the optimal cash holdings (means negative

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

abnormal cash holdings) pay higher audit fees to their auditors. It is because the actual cash

position is lower than optimal cash positions within the companies which may be due to poor

cash management and accordingly, auditors need to do more work with more effort to provide an

opinion on the liquidity of the company. Thus, they demand higher audit fees from companies

for taking the risk pertaining to liquidity position.

Further through the coefficient table, it has been identified that with the 1 unit change in

abnormal cash holdings of the firm, there would be a change in audit fees by -1.139. This means

if the actual cash holdings would decrease by 1 unit than optimal cash leading to higher negative

abnormal cash holding, then the audit will increase by 1.139. In addition to this, the significance

value in the coefficient table shows that with the higher or lower actual cash held than the

optimal cash, the audit fees charged to these firms would be higher. This is because the

significance value corresponding to abnormal cash holdings comes out as 0.000.

Hypothesis 2: Ceteris paribus, Higher client firm size leads to higher audit fees.

Model Summary

Mo

del

R R

Square

Adjusted R

Square

Std. Error

of the

Estimate

1 .715a .511 .510 7.902696

a. Predictors: (Constant), Firm_Size

ANOVAa

Model Sum of

Squares

df Mean

Square

F Sig.

1 Regressi

on

32541.261 1 32541.261 521.05

5

.000b

Residual 31101.399 498 62.453

Total 63642.660 499

a. Dependent Variable: Audit_Fee

b. Predictors: (Constant), Firm_Size

position is lower than optimal cash positions within the companies which may be due to poor

cash management and accordingly, auditors need to do more work with more effort to provide an

opinion on the liquidity of the company. Thus, they demand higher audit fees from companies

for taking the risk pertaining to liquidity position.

Further through the coefficient table, it has been identified that with the 1 unit change in

abnormal cash holdings of the firm, there would be a change in audit fees by -1.139. This means

if the actual cash holdings would decrease by 1 unit than optimal cash leading to higher negative

abnormal cash holding, then the audit will increase by 1.139. In addition to this, the significance

value in the coefficient table shows that with the higher or lower actual cash held than the

optimal cash, the audit fees charged to these firms would be higher. This is because the

significance value corresponding to abnormal cash holdings comes out as 0.000.

Hypothesis 2: Ceteris paribus, Higher client firm size leads to higher audit fees.

Model Summary

Mo

del

R R

Square

Adjusted R

Square

Std. Error

of the

Estimate

1 .715a .511 .510 7.902696

a. Predictors: (Constant), Firm_Size

ANOVAa

Model Sum of

Squares

df Mean

Square

F Sig.

1 Regressi

on

32541.261 1 32541.261 521.05

5

.000b

Residual 31101.399 498 62.453

Total 63642.660 499

a. Dependent Variable: Audit_Fee

b. Predictors: (Constant), Firm_Size

Coefficientsa

Model Unstandardized

Coefficients

Standardiz

ed

Coefficient

s

t Sig.

B Std. Error Beta

1 (Consta

nt)

-38.282 2.102 -

18.214

.000

Firm_Si

ze

4.997 .219 .715 22.827 .000

a. Dependent Variable: Audit_Fee

Interpretation: With the help of the output it is clear that the alternate hypothesis is being

accepted and the null is being rejected. This is pertaining to the fact that the significance value is

0.000 which is lower than the standard criteria of 0.05. Thus, this simply implies that the

alternate hypothesis is being accepted and it can be stated that when the firm size increases then

the audit fees also increases. Hence, this simply means that other things being remains the same,

when the firm size increases then the higher audit fees will be paid. Also, the R is identified as

71.5 % which implies that the correlation between the firm size and audit fees is high and the R

square is 51% which indicates that change in independent variable will be causing a change of

51% in the dependent variable as well.

From the evaluation of the obtained output data it can be articulated that the derived

value which depicts that there is acceptance of the alternative hypothesis it can be identified that

audit fees depends on the firm size. It can be specified that audit fees varies from the scale of the

operation of the company. The main fact behind this can be identified that there are various kinds

of the aspects which are taken into the consideration by the auditors while deciding upon the

price that they would be going to charge from the firms they are auditing and the one of such

aspects is the firm size. On the basis of this it can be articulated that there are distinct types of the

companies whose audit fees is dependent upon their firm size which allows to meet their

objective of proper & reliable functioning.

Further through the coefficient table, it has been determined that with the 1 unit change in

firm size, there would be a change in dependent variable (that is, audit fees) by 4.997 times. In

addition to this, the significance value has come out as 0.000 and due to this value being lower

Model Unstandardized

Coefficients

Standardiz

ed

Coefficient

s

t Sig.

B Std. Error Beta

1 (Consta

nt)

-38.282 2.102 -

18.214

.000

Firm_Si

ze

4.997 .219 .715 22.827 .000

a. Dependent Variable: Audit_Fee

Interpretation: With the help of the output it is clear that the alternate hypothesis is being

accepted and the null is being rejected. This is pertaining to the fact that the significance value is

0.000 which is lower than the standard criteria of 0.05. Thus, this simply implies that the

alternate hypothesis is being accepted and it can be stated that when the firm size increases then

the audit fees also increases. Hence, this simply means that other things being remains the same,

when the firm size increases then the higher audit fees will be paid. Also, the R is identified as

71.5 % which implies that the correlation between the firm size and audit fees is high and the R

square is 51% which indicates that change in independent variable will be causing a change of

51% in the dependent variable as well.

From the evaluation of the obtained output data it can be articulated that the derived

value which depicts that there is acceptance of the alternative hypothesis it can be identified that

audit fees depends on the firm size. It can be specified that audit fees varies from the scale of the

operation of the company. The main fact behind this can be identified that there are various kinds

of the aspects which are taken into the consideration by the auditors while deciding upon the

price that they would be going to charge from the firms they are auditing and the one of such

aspects is the firm size. On the basis of this it can be articulated that there are distinct types of the

companies whose audit fees is dependent upon their firm size which allows to meet their

objective of proper & reliable functioning.

Further through the coefficient table, it has been determined that with the 1 unit change in

firm size, there would be a change in dependent variable (that is, audit fees) by 4.997 times. In

addition to this, the significance value has come out as 0.000 and due to this value being lower

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

than 0.05, it can be said that there is a statistical significance lies between the firm size and audit

fees and accordingly, higher or lower firm size led to higher or lower audit fees.

fees and accordingly, higher or lower firm size led to higher or lower audit fees.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DISCUSSION

The discussion in this section of the data analysis chapter will be done to support the

findings of the study. The study has found that the higher audit fees are charged to firms by the

auditors that have their actual cash holdings lower than the optimal cash required to be

maintained with companies.

The audit fees to be charged by the auditor, according to Vaez, Montazer Hojat and

Khosravi, (2018), are the dependent factor over the cash that a firm hold, which has been taken

as an independent variable. The amount of audit fees to be payable by large companies is usually

insignificant compared to the other financial results of the company. However, the same amount

could be hefty as well as significant for small commercial companies that are experiencing poor

or low financial performance. This becomes the case because of the auditor’s risk in auditing the

financial statements of these firms with lower cash holdings than the optimal requirements.

Accordingly, to take a higher risk in auditing financially weak companies, the auditors attempt to

charge higher audit fees from these firms. Another reason for charging higher fees by the

auditors of companies that are facing financial constraints in some or other ways is that they have

less access to the funds provided by the capital market and for the future contingencies they must

have an optimal level of cash balances with them. However, in the case of having fewer cash

holdings as compared to what is required at an optimal level, the auditors of such companies

found a risk of failure and, accordingly, they backed up their risks by charging higher audit fees.

Moreover, it was analyzed from the correlation findings that there was a negative

correlation between the abnormal cash holdings and audit fees of the company. These findings

are also supported by author which stated that when companies failed to maintain the optimal

cash within the organization and their actual cash is lower than optimal cash than auditors charge

higher audit fees from such companies. The abnormal cash holdings of the company are

difference between actual cash holding and optimal cash holdings (Mitra, Jaggi and Al-Hayale,

2019). The findings of mean state that the abnormal cash holding is negative because actual cash

holdings is lower than the optimal cash holdings. On the same side, the audit fees of companies

are higher which indicate negative relation between two variables that is abnormal cash holdings

and audit fees.

The discussion in this section of the data analysis chapter will be done to support the

findings of the study. The study has found that the higher audit fees are charged to firms by the

auditors that have their actual cash holdings lower than the optimal cash required to be

maintained with companies.

The audit fees to be charged by the auditor, according to Vaez, Montazer Hojat and

Khosravi, (2018), are the dependent factor over the cash that a firm hold, which has been taken

as an independent variable. The amount of audit fees to be payable by large companies is usually

insignificant compared to the other financial results of the company. However, the same amount

could be hefty as well as significant for small commercial companies that are experiencing poor

or low financial performance. This becomes the case because of the auditor’s risk in auditing the

financial statements of these firms with lower cash holdings than the optimal requirements.

Accordingly, to take a higher risk in auditing financially weak companies, the auditors attempt to

charge higher audit fees from these firms. Another reason for charging higher fees by the

auditors of companies that are facing financial constraints in some or other ways is that they have

less access to the funds provided by the capital market and for the future contingencies they must

have an optimal level of cash balances with them. However, in the case of having fewer cash

holdings as compared to what is required at an optimal level, the auditors of such companies

found a risk of failure and, accordingly, they backed up their risks by charging higher audit fees.

Moreover, it was analyzed from the correlation findings that there was a negative

correlation between the abnormal cash holdings and audit fees of the company. These findings

are also supported by author which stated that when companies failed to maintain the optimal

cash within the organization and their actual cash is lower than optimal cash than auditors charge

higher audit fees from such companies. The abnormal cash holdings of the company are

difference between actual cash holding and optimal cash holdings (Mitra, Jaggi and Al-Hayale,

2019). The findings of mean state that the abnormal cash holding is negative because actual cash

holdings is lower than the optimal cash holdings. On the same side, the audit fees of companies

are higher which indicate negative relation between two variables that is abnormal cash holdings

and audit fees.

However, on the other hand, Choi and et.al., (2020) in their research paper indicated that

for the insufficient cash holdings within the organizations, the auditors of the company charge

high audit fees. It is because the auditor considers that there is a higher risk of potential losses in

the company because of low liquidity in cash reserves. The independent auditors of the company

are highly responsible for providing reasonable assurance and an opinion on the truthfulness and

fairness of the financial statements of the company. Hence, it is stated that it is important for the

auditors to look out and analyze whether the actual cash holdings of the firms are meeting the

optimal cash holding criteria or not.

It is further analyzed from the data analysis and findings that FTSE companies whose

actual cash holdings are less than the optimal cash holdings pay higher audit fees to their auditor.

The comparison between the excess and insufficient cash reserves of the company with its target

cash reserves helps the auditors to know whether the company is able to manage its cash flow

appropriately or not. It is evident from the findings that if the actual cash holding is less than

optimal cash holdings, the companies need to pay higher audit fees. It is because the work and

effort of the auditors increase as the auditors need to do extra work to analyze the performance of

companies and provide a fair opinion. As a result of the extra work, auditors of company’s

demand higher pay from their companies, causing audit fees to rise (Musah, Anokye and

Gakpetor, 2018). This statement is also proved by the hypothesis testing done in this research

with the use of a regression model.

As per the opinion of Tran and et al. (2019), there are various levels of factors that

influence the audit fees paid by the company to its auditors. It is shown by scholars in their

research paper that actual audit characteristics are a significant factor that influences the audit

fees. The audit fees are an independent variable in the research paper which is highly influenced

by the dependent variable such as cash holdings of the company. It is stated by the authors in

their research paper that every year companies prepare a budget to forecast the target and optimal

cash holdings of the company. Not only that, companies, after forecasting, compare the budget

with their actual cash holdings to analyse and assess the cash management within the

organizations.

It is also stated by the author that an audit of every UK company listed under the FTSE

100 index is compulsory as per the Companies Act, 2006. The auditors should be objective and

for the insufficient cash holdings within the organizations, the auditors of the company charge

high audit fees. It is because the auditor considers that there is a higher risk of potential losses in

the company because of low liquidity in cash reserves. The independent auditors of the company

are highly responsible for providing reasonable assurance and an opinion on the truthfulness and

fairness of the financial statements of the company. Hence, it is stated that it is important for the

auditors to look out and analyze whether the actual cash holdings of the firms are meeting the

optimal cash holding criteria or not.

It is further analyzed from the data analysis and findings that FTSE companies whose

actual cash holdings are less than the optimal cash holdings pay higher audit fees to their auditor.

The comparison between the excess and insufficient cash reserves of the company with its target

cash reserves helps the auditors to know whether the company is able to manage its cash flow

appropriately or not. It is evident from the findings that if the actual cash holding is less than

optimal cash holdings, the companies need to pay higher audit fees. It is because the work and

effort of the auditors increase as the auditors need to do extra work to analyze the performance of

companies and provide a fair opinion. As a result of the extra work, auditors of company’s

demand higher pay from their companies, causing audit fees to rise (Musah, Anokye and

Gakpetor, 2018). This statement is also proved by the hypothesis testing done in this research

with the use of a regression model.

As per the opinion of Tran and et al. (2019), there are various levels of factors that

influence the audit fees paid by the company to its auditors. It is shown by scholars in their

research paper that actual audit characteristics are a significant factor that influences the audit

fees. The audit fees are an independent variable in the research paper which is highly influenced

by the dependent variable such as cash holdings of the company. It is stated by the authors in

their research paper that every year companies prepare a budget to forecast the target and optimal

cash holdings of the company. Not only that, companies, after forecasting, compare the budget

with their actual cash holdings to analyse and assess the cash management within the

organizations.

It is also stated by the author that an audit of every UK company listed under the FTSE

100 index is compulsory as per the Companies Act, 2006. The auditors should be objective and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.