Products and Services Offered by Abu Dhabi Islamic Bank

VerifiedAdded on 2023/06/15

|8

|2164

|155

AI Summary

This article discusses the various products and services offered by Abu Dhabi Islamic Bank, including corporate banking solutions, wealth management, and personal finance options. It also highlights the differences between Islamic banking processes and conventional bank processes, using examples such as automobile loans and home financing.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL MARKETS AND INSTITUTES

Financial Markets and Institutes

Name of Student:

Name of University:

Author’s Note:

Financial Markets and Institutes

Name of Student:

Name of University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1FINANCIAL MARKETS AND INSTITUTES

Table of Contents

Introduction......................................................................................................................................2

Products and services offered by ADIB..........................................................................................2

Differentiated banking mechanism than the conventional banks....................................................2

Conclusion.......................................................................................................................................4

References........................................................................................................................................5

Table of Contents

Introduction......................................................................................................................................2

Products and services offered by ADIB..........................................................................................2

Differentiated banking mechanism than the conventional banks....................................................2

Conclusion.......................................................................................................................................4

References........................................................................................................................................5

2FINANCIAL MARKETS AND INSTITUTES

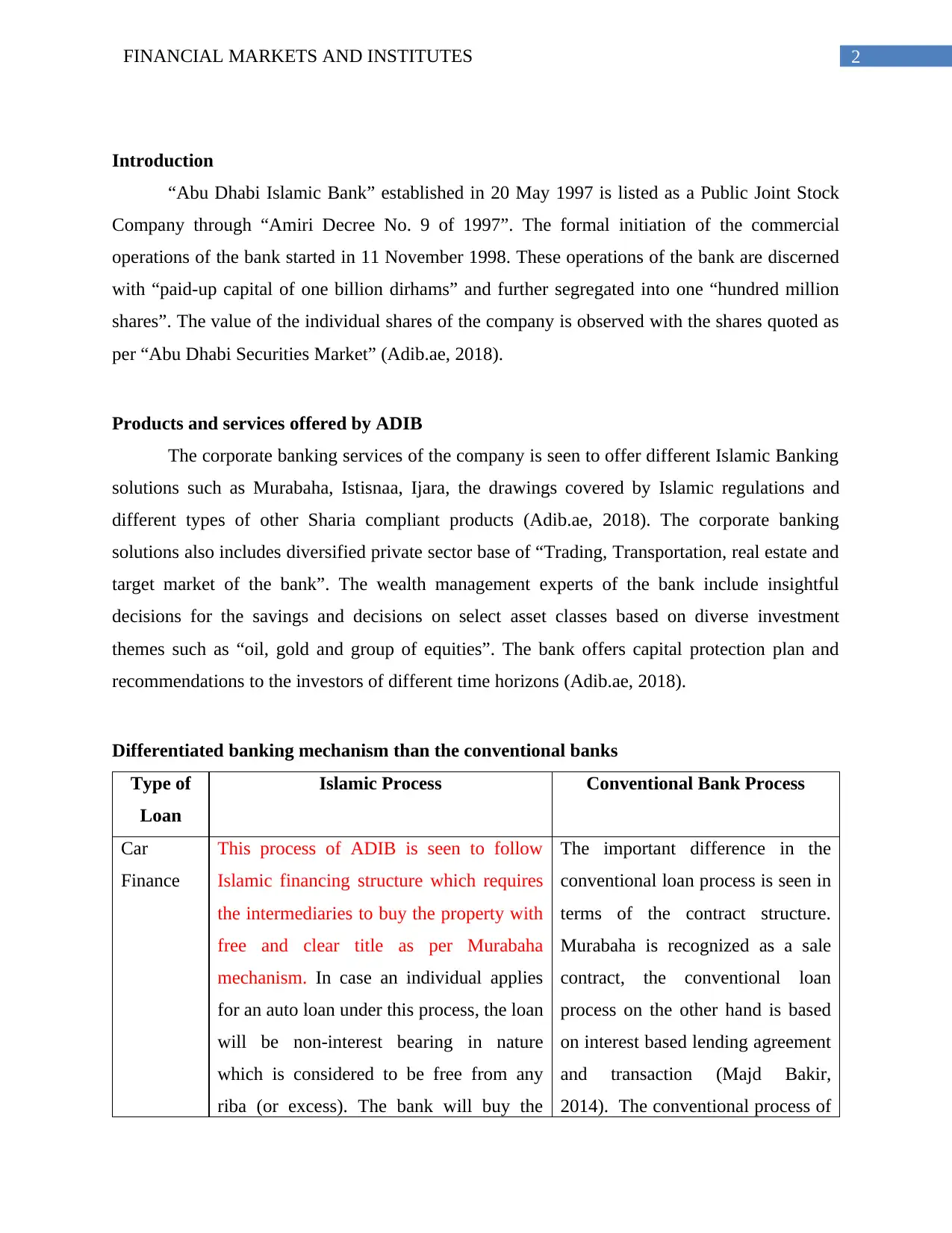

Introduction

“Abu Dhabi Islamic Bank” established in 20 May 1997 is listed as a Public Joint Stock

Company through “Amiri Decree No. 9 of 1997”. The formal initiation of the commercial

operations of the bank started in 11 November 1998. These operations of the bank are discerned

with “paid-up capital of one billion dirhams” and further segregated into one “hundred million

shares”. The value of the individual shares of the company is observed with the shares quoted as

per “Abu Dhabi Securities Market” (Adib.ae, 2018).

Products and services offered by ADIB

The corporate banking services of the company is seen to offer different Islamic Banking

solutions such as Murabaha, Istisnaa, Ijara, the drawings covered by Islamic regulations and

different types of other Sharia compliant products (Adib.ae, 2018). The corporate banking

solutions also includes diversified private sector base of “Trading, Transportation, real estate and

target market of the bank”. The wealth management experts of the bank include insightful

decisions for the savings and decisions on select asset classes based on diverse investment

themes such as “oil, gold and group of equities”. The bank offers capital protection plan and

recommendations to the investors of different time horizons (Adib.ae, 2018).

Differentiated banking mechanism than the conventional banks

Type of

Loan

Islamic Process Conventional Bank Process

Car

Finance

This process of ADIB is seen to follow

Islamic financing structure which requires

the intermediaries to buy the property with

free and clear title as per Murabaha

mechanism. In case an individual applies

for an auto loan under this process, the loan

will be non-interest bearing in nature

which is considered to be free from any

riba (or excess). The bank will buy the

The important difference in the

conventional loan process is seen in

terms of the contract structure.

Murabaha is recognized as a sale

contract, the conventional loan

process on the other hand is based

on interest based lending agreement

and transaction (Majd Bakir,

2014). The conventional process of

Introduction

“Abu Dhabi Islamic Bank” established in 20 May 1997 is listed as a Public Joint Stock

Company through “Amiri Decree No. 9 of 1997”. The formal initiation of the commercial

operations of the bank started in 11 November 1998. These operations of the bank are discerned

with “paid-up capital of one billion dirhams” and further segregated into one “hundred million

shares”. The value of the individual shares of the company is observed with the shares quoted as

per “Abu Dhabi Securities Market” (Adib.ae, 2018).

Products and services offered by ADIB

The corporate banking services of the company is seen to offer different Islamic Banking

solutions such as Murabaha, Istisnaa, Ijara, the drawings covered by Islamic regulations and

different types of other Sharia compliant products (Adib.ae, 2018). The corporate banking

solutions also includes diversified private sector base of “Trading, Transportation, real estate and

target market of the bank”. The wealth management experts of the bank include insightful

decisions for the savings and decisions on select asset classes based on diverse investment

themes such as “oil, gold and group of equities”. The bank offers capital protection plan and

recommendations to the investors of different time horizons (Adib.ae, 2018).

Differentiated banking mechanism than the conventional banks

Type of

Loan

Islamic Process Conventional Bank Process

Car

Finance

This process of ADIB is seen to follow

Islamic financing structure which requires

the intermediaries to buy the property with

free and clear title as per Murabaha

mechanism. In case an individual applies

for an auto loan under this process, the loan

will be non-interest bearing in nature

which is considered to be free from any

riba (or excess). The bank will buy the

The important difference in the

conventional loan process is seen in

terms of the contract structure.

Murabaha is recognized as a sale

contract, the conventional loan

process on the other hand is based

on interest based lending agreement

and transaction (Majd Bakir,

2014). The conventional process of

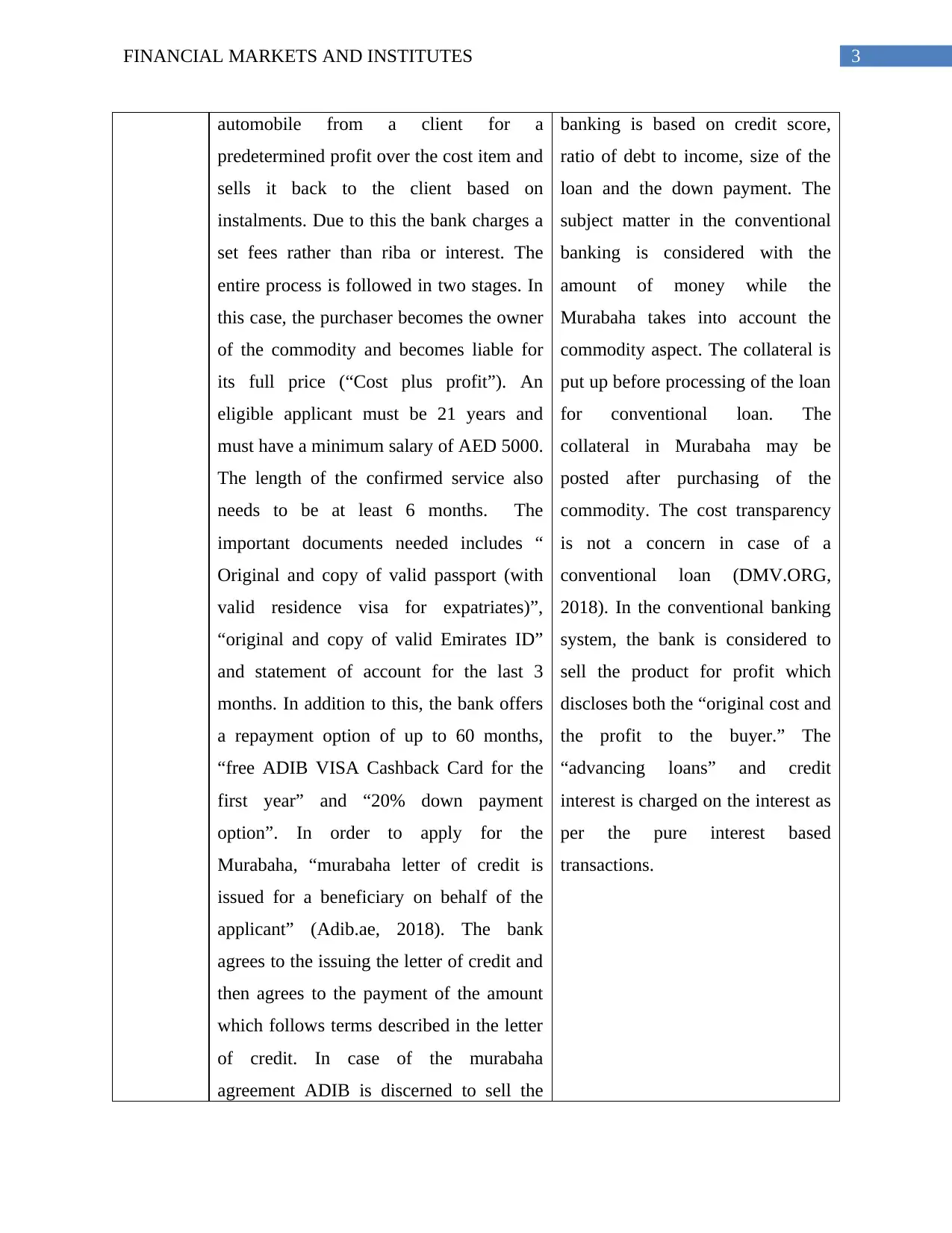

3FINANCIAL MARKETS AND INSTITUTES

automobile from a client for a

predetermined profit over the cost item and

sells it back to the client based on

instalments. Due to this the bank charges a

set fees rather than riba or interest. The

entire process is followed in two stages. In

this case, the purchaser becomes the owner

of the commodity and becomes liable for

its full price (“Cost plus profit”). An

eligible applicant must be 21 years and

must have a minimum salary of AED 5000.

The length of the confirmed service also

needs to be at least 6 months. The

important documents needed includes “

Original and copy of valid passport (with

valid residence visa for expatriates)”,

“original and copy of valid Emirates ID”

and statement of account for the last 3

months. In addition to this, the bank offers

a repayment option of up to 60 months,

“free ADIB VISA Cashback Card for the

first year” and “20% down payment

option”. In order to apply for the

Murabaha, “murabaha letter of credit is

issued for a beneficiary on behalf of the

applicant” (Adib.ae, 2018). The bank

agrees to the issuing the letter of credit and

then agrees to the payment of the amount

which follows terms described in the letter

of credit. In case of the murabaha

agreement ADIB is discerned to sell the

banking is based on credit score,

ratio of debt to income, size of the

loan and the down payment. The

subject matter in the conventional

banking is considered with the

amount of money while the

Murabaha takes into account the

commodity aspect. The collateral is

put up before processing of the loan

for conventional loan. The

collateral in Murabaha may be

posted after purchasing of the

commodity. The cost transparency

is not a concern in case of a

conventional loan (DMV.ORG,

2018). In the conventional banking

system, the bank is considered to

sell the product for profit which

discloses both the “original cost and

the profit to the buyer.” The

“advancing loans” and credit

interest is charged on the interest as

per the pure interest based

transactions.

automobile from a client for a

predetermined profit over the cost item and

sells it back to the client based on

instalments. Due to this the bank charges a

set fees rather than riba or interest. The

entire process is followed in two stages. In

this case, the purchaser becomes the owner

of the commodity and becomes liable for

its full price (“Cost plus profit”). An

eligible applicant must be 21 years and

must have a minimum salary of AED 5000.

The length of the confirmed service also

needs to be at least 6 months. The

important documents needed includes “

Original and copy of valid passport (with

valid residence visa for expatriates)”,

“original and copy of valid Emirates ID”

and statement of account for the last 3

months. In addition to this, the bank offers

a repayment option of up to 60 months,

“free ADIB VISA Cashback Card for the

first year” and “20% down payment

option”. In order to apply for the

Murabaha, “murabaha letter of credit is

issued for a beneficiary on behalf of the

applicant” (Adib.ae, 2018). The bank

agrees to the issuing the letter of credit and

then agrees to the payment of the amount

which follows terms described in the letter

of credit. In case of the murabaha

agreement ADIB is discerned to sell the

banking is based on credit score,

ratio of debt to income, size of the

loan and the down payment. The

subject matter in the conventional

banking is considered with the

amount of money while the

Murabaha takes into account the

commodity aspect. The collateral is

put up before processing of the loan

for conventional loan. The

collateral in Murabaha may be

posted after purchasing of the

commodity. The cost transparency

is not a concern in case of a

conventional loan (DMV.ORG,

2018). In the conventional banking

system, the bank is considered to

sell the product for profit which

discloses both the “original cost and

the profit to the buyer.” The

“advancing loans” and credit

interest is charged on the interest as

per the pure interest based

transactions.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4FINANCIAL MARKETS AND INSTITUTES

contract (Chelhi et al., 2017).

Home

Finance

This process has discussed on benefit of

home financing through Istisna. Based on

this contract the client will ask the bank for

construction of the unit. This will be able

to meet the different types of the

specifications given by the bank to meet

the desire of the client. The client will then

pay the price in instalments. In this case the

borrower needs to provide a “Valid salary

certificate”, income verification, “Passport

copy along with valid resident visa for

expats”, Khulaset Al Kaid and Bank

Statement. The minimum salary

requirement for the applicant is identified

with AED 10,000 for UAE Nationals and

AED 15,000 for Expats. The age criteria

requirement is discerned to be 21 years.

Some of the other document required is

considered with “Verified employment,

Valid for UAE nationals & residents and

Joint applications accepted”. The bank

provides financing of up to “AED 20

million for UAE Nationals & AED 15

Million for expatriates” this process is

based on Istisna. In addition to this it

provides “Financing of up to 80% of

property value” and partial settlement of

30% outstanding annually (Adib.ae, 2018).

A conventional home loan applicant

needs to present proof of income,

identity and residence. The

borrowing limit will be based on

the individual’s income and interest

rate will be charged as per the total

amount loan borrowed. The

conventional borrowing will

include tax concessions based on IT

returns. The conventional loan will

also include the option for

instalment payment however, the

borrower does not need to produce

“Istisna letter of credit is issued for

a beneficiary on behalf of the

applicant” and Khulaset Al Kaid

(Majd Bakir, 2014).

Boat

Finance

The financing of boat is considered to be

most ideal with the application of Ijara

The boat loan needs to be approved

and signed with necessary

contract (Chelhi et al., 2017).

Home

Finance

This process has discussed on benefit of

home financing through Istisna. Based on

this contract the client will ask the bank for

construction of the unit. This will be able

to meet the different types of the

specifications given by the bank to meet

the desire of the client. The client will then

pay the price in instalments. In this case the

borrower needs to provide a “Valid salary

certificate”, income verification, “Passport

copy along with valid resident visa for

expats”, Khulaset Al Kaid and Bank

Statement. The minimum salary

requirement for the applicant is identified

with AED 10,000 for UAE Nationals and

AED 15,000 for Expats. The age criteria

requirement is discerned to be 21 years.

Some of the other document required is

considered with “Verified employment,

Valid for UAE nationals & residents and

Joint applications accepted”. The bank

provides financing of up to “AED 20

million for UAE Nationals & AED 15

Million for expatriates” this process is

based on Istisna. In addition to this it

provides “Financing of up to 80% of

property value” and partial settlement of

30% outstanding annually (Adib.ae, 2018).

A conventional home loan applicant

needs to present proof of income,

identity and residence. The

borrowing limit will be based on

the individual’s income and interest

rate will be charged as per the total

amount loan borrowed. The

conventional borrowing will

include tax concessions based on IT

returns. The conventional loan will

also include the option for

instalment payment however, the

borrower does not need to produce

“Istisna letter of credit is issued for

a beneficiary on behalf of the

applicant” and Khulaset Al Kaid

(Majd Bakir, 2014).

Boat

Finance

The financing of boat is considered to be

most ideal with the application of Ijara

The boat loan needs to be approved

and signed with necessary

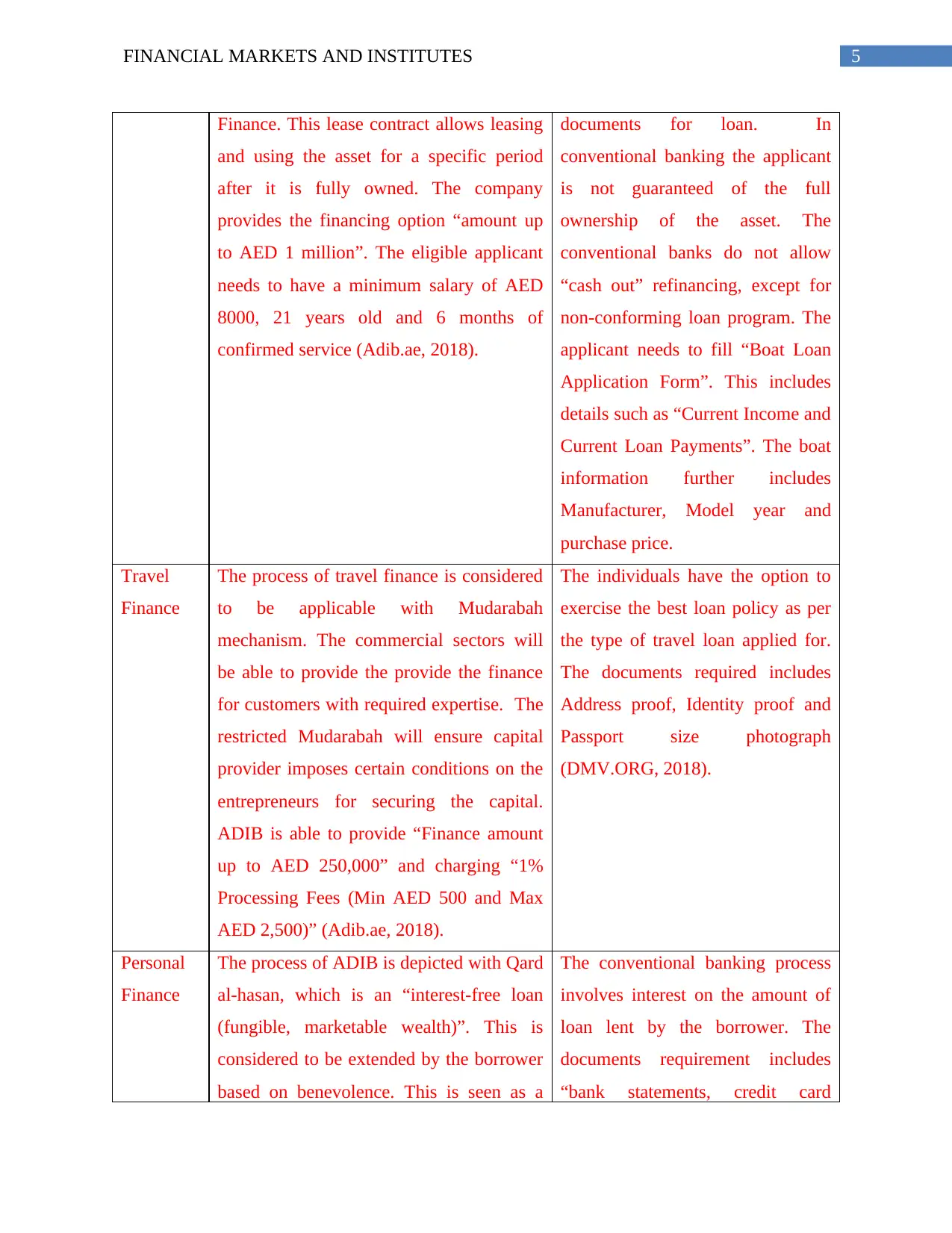

5FINANCIAL MARKETS AND INSTITUTES

Finance. This lease contract allows leasing

and using the asset for a specific period

after it is fully owned. The company

provides the financing option “amount up

to AED 1 million”. The eligible applicant

needs to have a minimum salary of AED

8000, 21 years old and 6 months of

confirmed service (Adib.ae, 2018).

documents for loan. In

conventional banking the applicant

is not guaranteed of the full

ownership of the asset. The

conventional banks do not allow

“cash out” refinancing, except for

non-conforming loan program. The

applicant needs to fill “Boat Loan

Application Form”. This includes

details such as “Current Income and

Current Loan Payments”. The boat

information further includes

Manufacturer, Model year and

purchase price.

Travel

Finance

The process of travel finance is considered

to be applicable with Mudarabah

mechanism. The commercial sectors will

be able to provide the provide the finance

for customers with required expertise. The

restricted Mudarabah will ensure capital

provider imposes certain conditions on the

entrepreneurs for securing the capital.

ADIB is able to provide “Finance amount

up to AED 250,000” and charging “1%

Processing Fees (Min AED 500 and Max

AED 2,500)” (Adib.ae, 2018).

The individuals have the option to

exercise the best loan policy as per

the type of travel loan applied for.

The documents required includes

Address proof, Identity proof and

Passport size photograph

(DMV.ORG, 2018).

Personal

Finance

The process of ADIB is depicted with Qard

al-hasan, which is an “interest-free loan

(fungible, marketable wealth)”. This is

considered to be extended by the borrower

based on benevolence. This is seen as a

The conventional banking process

involves interest on the amount of

loan lent by the borrower. The

documents requirement includes

“bank statements, credit card

Finance. This lease contract allows leasing

and using the asset for a specific period

after it is fully owned. The company

provides the financing option “amount up

to AED 1 million”. The eligible applicant

needs to have a minimum salary of AED

8000, 21 years old and 6 months of

confirmed service (Adib.ae, 2018).

documents for loan. In

conventional banking the applicant

is not guaranteed of the full

ownership of the asset. The

conventional banks do not allow

“cash out” refinancing, except for

non-conforming loan program. The

applicant needs to fill “Boat Loan

Application Form”. This includes

details such as “Current Income and

Current Loan Payments”. The boat

information further includes

Manufacturer, Model year and

purchase price.

Travel

Finance

The process of travel finance is considered

to be applicable with Mudarabah

mechanism. The commercial sectors will

be able to provide the provide the finance

for customers with required expertise. The

restricted Mudarabah will ensure capital

provider imposes certain conditions on the

entrepreneurs for securing the capital.

ADIB is able to provide “Finance amount

up to AED 250,000” and charging “1%

Processing Fees (Min AED 500 and Max

AED 2,500)” (Adib.ae, 2018).

The individuals have the option to

exercise the best loan policy as per

the type of travel loan applied for.

The documents required includes

Address proof, Identity proof and

Passport size photograph

(DMV.ORG, 2018).

Personal

Finance

The process of ADIB is depicted with Qard

al-hasan, which is an “interest-free loan

(fungible, marketable wealth)”. This is

considered to be extended by the borrower

based on benevolence. This is seen as a

The conventional banking process

involves interest on the amount of

loan lent by the borrower. The

documents requirement includes

“bank statements, credit card

6FINANCIAL MARKETS AND INSTITUTES

“gratuitous loan extension to needy people

for a specified period of time”. The bank

provides “First instalment payment grace

period up to 90 days”, “Two free

instalments postponements every year” and

“Takaful cover protection with competitive

rates”. The individual must have a

minimum salary of AED 8000 per month

and UAE or expatriate with a minimum

age of 21 years (Adib.ae, 2018). .

information and loans records”

(Majd Bakir, 2014).

Debt

Settlemen

t

The "Musharkah Financing" ideal as the

client will be able to request for finance by

anticipating the bank’s shares anticipated

with profits and losses of the project as per

the client. The borrower needs to present

liability certificate, bank account statement

for the last 3 months and original valid

emirates ID (Adib.ae, 2018).

Conventional banks offer debt

consolidation loans which requires

the borrower to pay the applicable

rate of interest based on amount of

loan borrowed. The document

requirement includes bank

statements, credit card information

and loans records (DMV.ORG,

2018).

Conclusion

The significant discussion of the study is able to identify the different types the products

and services offered by ADIB offered in general. In addition to this, the learnings of the

discourse have taken into consideration the import differences pertaining to the Islamic Banking

Process and Conventional Bank Process. The important characteristics in the Islamic Banking

Process has discussed on the Islamic financing structure followed by ADIB which requires the

intermediaries to buy the property with free and clear title. The entire process is explained with

the intention of borrowing a loan for automobile. The bank will buy the automobile from a client

for a predetermined profit over the cost item and sells it back to the client based on instalments.

Due to this the bank charges a set fees rather than riba or interest. The entire process is followed

“gratuitous loan extension to needy people

for a specified period of time”. The bank

provides “First instalment payment grace

period up to 90 days”, “Two free

instalments postponements every year” and

“Takaful cover protection with competitive

rates”. The individual must have a

minimum salary of AED 8000 per month

and UAE or expatriate with a minimum

age of 21 years (Adib.ae, 2018). .

information and loans records”

(Majd Bakir, 2014).

Debt

Settlemen

t

The "Musharkah Financing" ideal as the

client will be able to request for finance by

anticipating the bank’s shares anticipated

with profits and losses of the project as per

the client. The borrower needs to present

liability certificate, bank account statement

for the last 3 months and original valid

emirates ID (Adib.ae, 2018).

Conventional banks offer debt

consolidation loans which requires

the borrower to pay the applicable

rate of interest based on amount of

loan borrowed. The document

requirement includes bank

statements, credit card information

and loans records (DMV.ORG,

2018).

Conclusion

The significant discussion of the study is able to identify the different types the products

and services offered by ADIB offered in general. In addition to this, the learnings of the

discourse have taken into consideration the import differences pertaining to the Islamic Banking

Process and Conventional Bank Process. The important characteristics in the Islamic Banking

Process has discussed on the Islamic financing structure followed by ADIB which requires the

intermediaries to buy the property with free and clear title. The entire process is explained with

the intention of borrowing a loan for automobile. The bank will buy the automobile from a client

for a predetermined profit over the cost item and sells it back to the client based on instalments.

Due to this the bank charges a set fees rather than riba or interest. The entire process is followed

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MARKETS AND INSTITUTES

in two stages. In the first stage the bank purchases the commodity which the client is willing to

sell. This stage is followed by client agreeing to the payment schedule for the repurchasing of the

goods.

References

Abu Dhabi Islamic Bank Corporate Banking . (2018). Adib.ae. Retrieved 5 February 2018, from

http://www.adib.ae/en/m/Pages/corporate_banking.aspx

ADIB | ADIB Car Finance in UAE | Abu Dhabi Islamic Bank . (2018). Adib.ae. Retrieved 5

February 2018, from http://www.adib.ae/en/personal/financing/car-finance

ADIB | Telephone Banking | ADIB Services | Personal Banking . (2018). Adib.ae. Retrieved 5

February 2018, from

http://www.adib.ae/en/pages/personal_services_telephone_banking.aspx

ADIB | Wealth Management | ADIB Structured Products . (2018). Adib.ae. Retrieved 5 February

2018, from

http://www.adib.ae/en/Pages/personal_wealth_management_structured_product.aspx

Chelhi, K., El Hachloufi, M., Aboulethar, M., Eddaoui, A. and Marzak, A., 2017. Estimation of

Murabaha Margin. Journal of Applied Finance and Banking, 7(5), p.49.

DMV.ORG. (2018). Understanding Car Financing | DMV.ORG. [online] Available at:

https://www.dmv.org/how-to-guides/auto-financing.php [Accessed 5 Feb. 2018].

Majd Bakir, m. (2014). Islamic Finance | What Is the Difference Between Murabaha and

Conventional Loan?. Financialencyclopedia.net. Retrieved 5 February 2018, from

http://www.financialencyclopedia.net/islamic-finance/questions/what-is-the-difference-

between-murabaha-and-conventional-loan.html

Understanding Car Financing | DMV.ORG. (2018). DMV.ORG. Retrieved 5 February 2018,

from https://www.dmv.org/how-to-guides/auto-financing.php

in two stages. In the first stage the bank purchases the commodity which the client is willing to

sell. This stage is followed by client agreeing to the payment schedule for the repurchasing of the

goods.

References

Abu Dhabi Islamic Bank Corporate Banking . (2018). Adib.ae. Retrieved 5 February 2018, from

http://www.adib.ae/en/m/Pages/corporate_banking.aspx

ADIB | ADIB Car Finance in UAE | Abu Dhabi Islamic Bank . (2018). Adib.ae. Retrieved 5

February 2018, from http://www.adib.ae/en/personal/financing/car-finance

ADIB | Telephone Banking | ADIB Services | Personal Banking . (2018). Adib.ae. Retrieved 5

February 2018, from

http://www.adib.ae/en/pages/personal_services_telephone_banking.aspx

ADIB | Wealth Management | ADIB Structured Products . (2018). Adib.ae. Retrieved 5 February

2018, from

http://www.adib.ae/en/Pages/personal_wealth_management_structured_product.aspx

Chelhi, K., El Hachloufi, M., Aboulethar, M., Eddaoui, A. and Marzak, A., 2017. Estimation of

Murabaha Margin. Journal of Applied Finance and Banking, 7(5), p.49.

DMV.ORG. (2018). Understanding Car Financing | DMV.ORG. [online] Available at:

https://www.dmv.org/how-to-guides/auto-financing.php [Accessed 5 Feb. 2018].

Majd Bakir, m. (2014). Islamic Finance | What Is the Difference Between Murabaha and

Conventional Loan?. Financialencyclopedia.net. Retrieved 5 February 2018, from

http://www.financialencyclopedia.net/islamic-finance/questions/what-is-the-difference-

between-murabaha-and-conventional-loan.html

Understanding Car Financing | DMV.ORG. (2018). DMV.ORG. Retrieved 5 February 2018,

from https://www.dmv.org/how-to-guides/auto-financing.php

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.