Financial Accounting and Analysis: A Comprehensive Assignment

VerifiedAdded on 2023/01/04

|25

|3439

|68

Homework Assignment

AI Summary

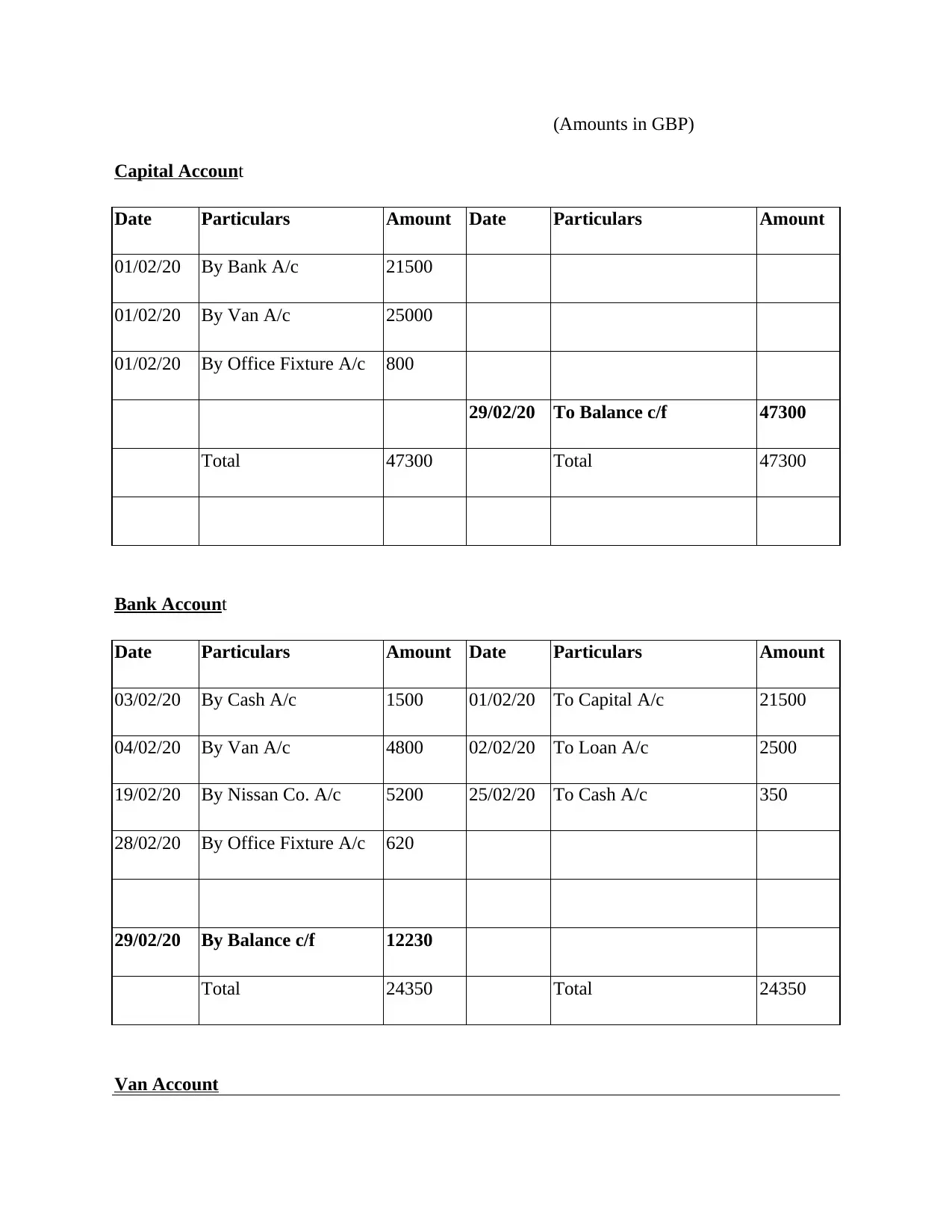

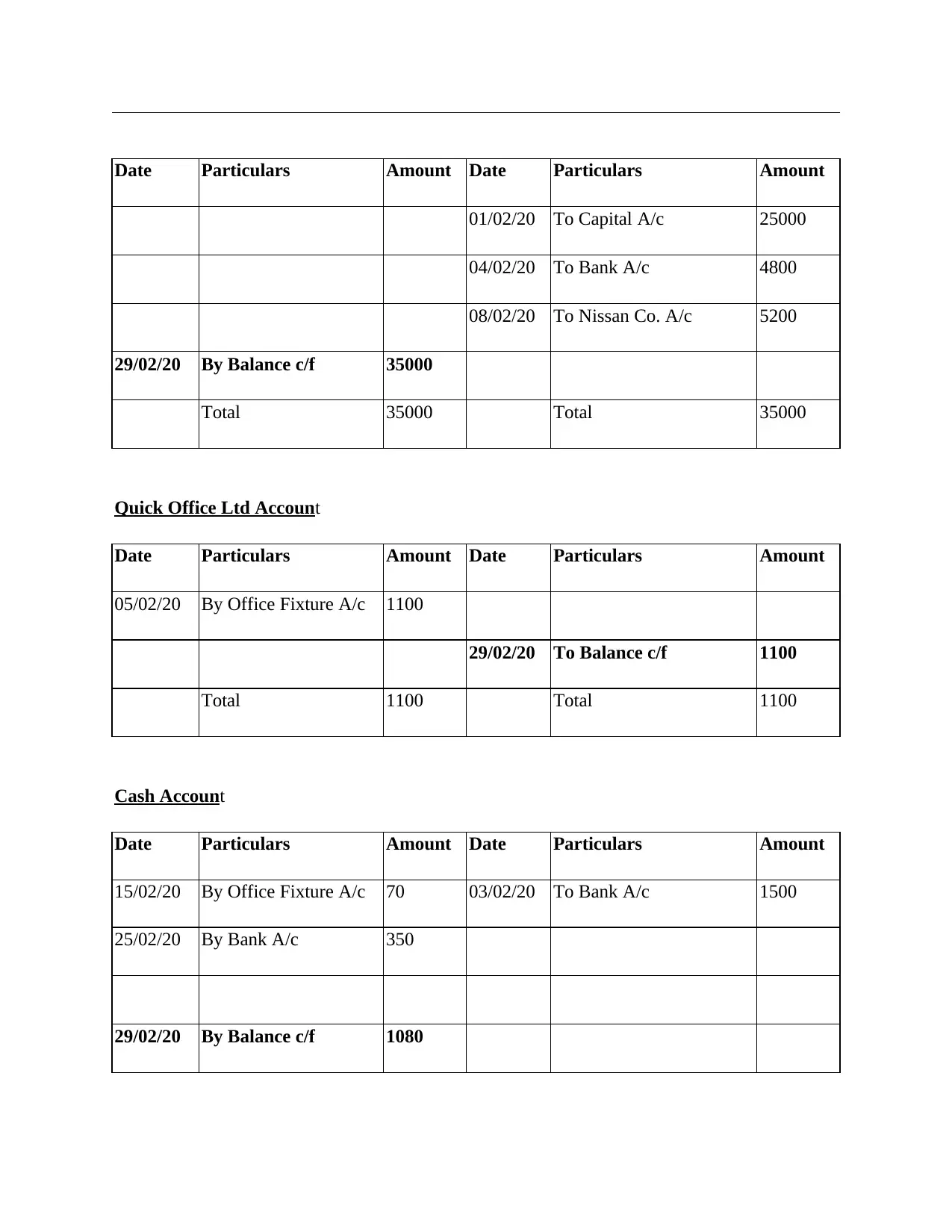

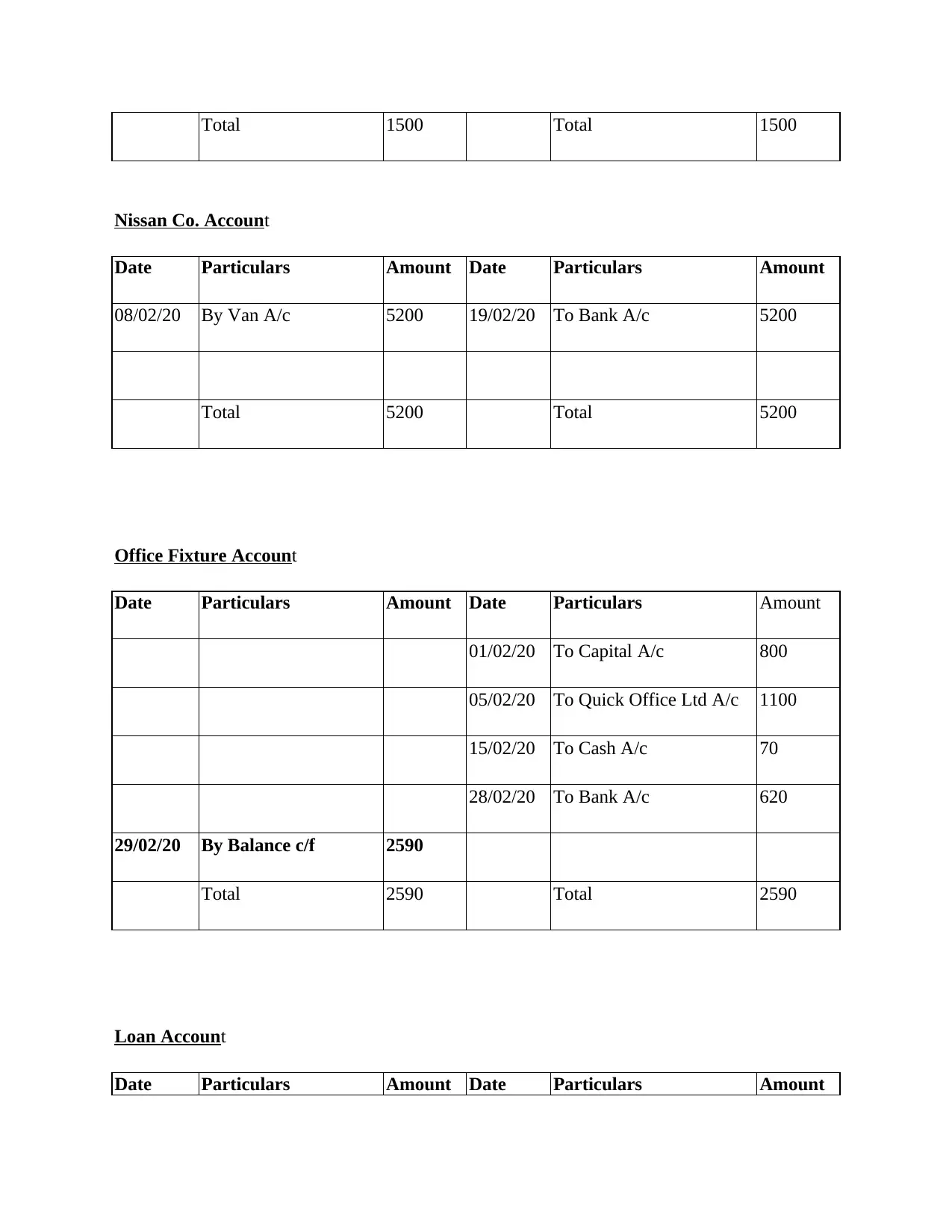

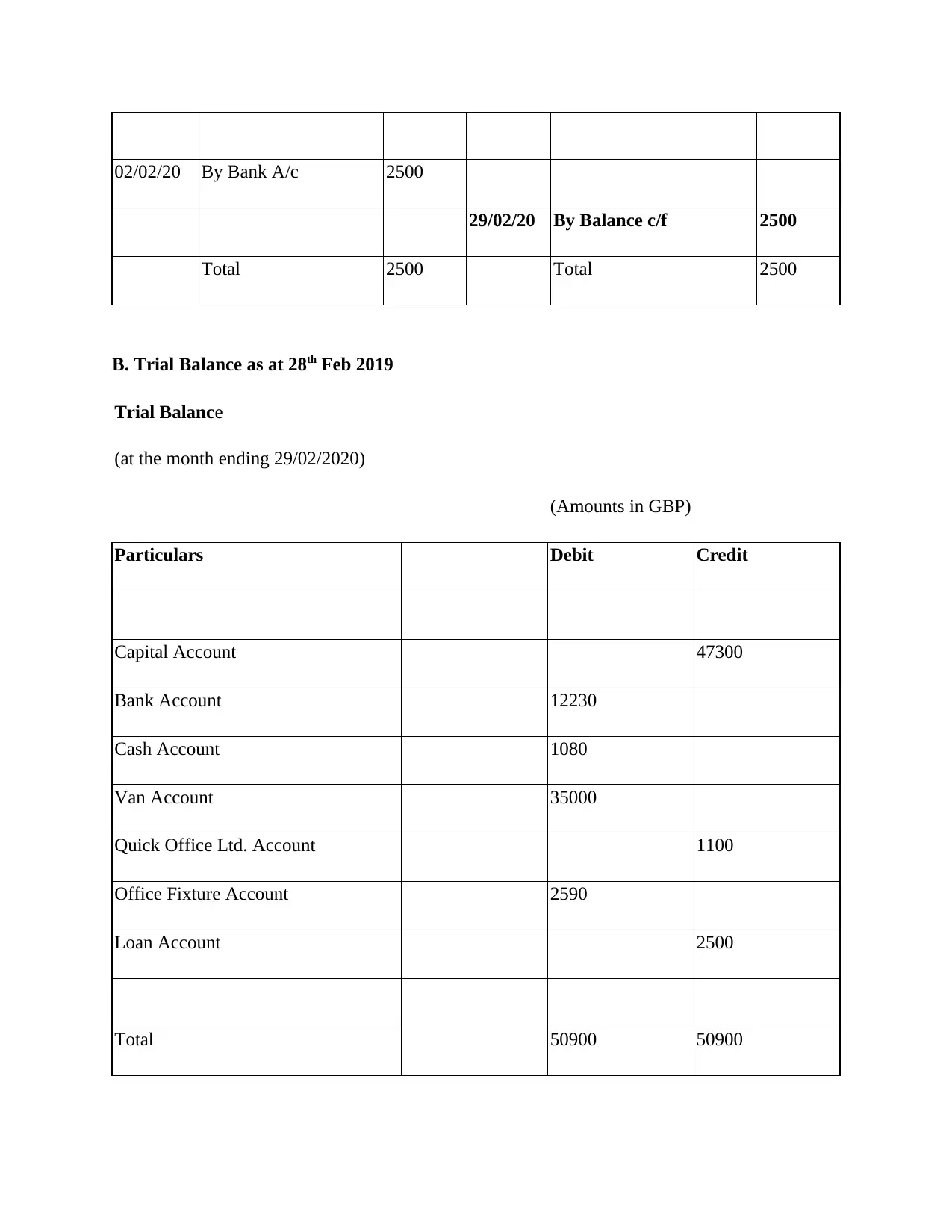

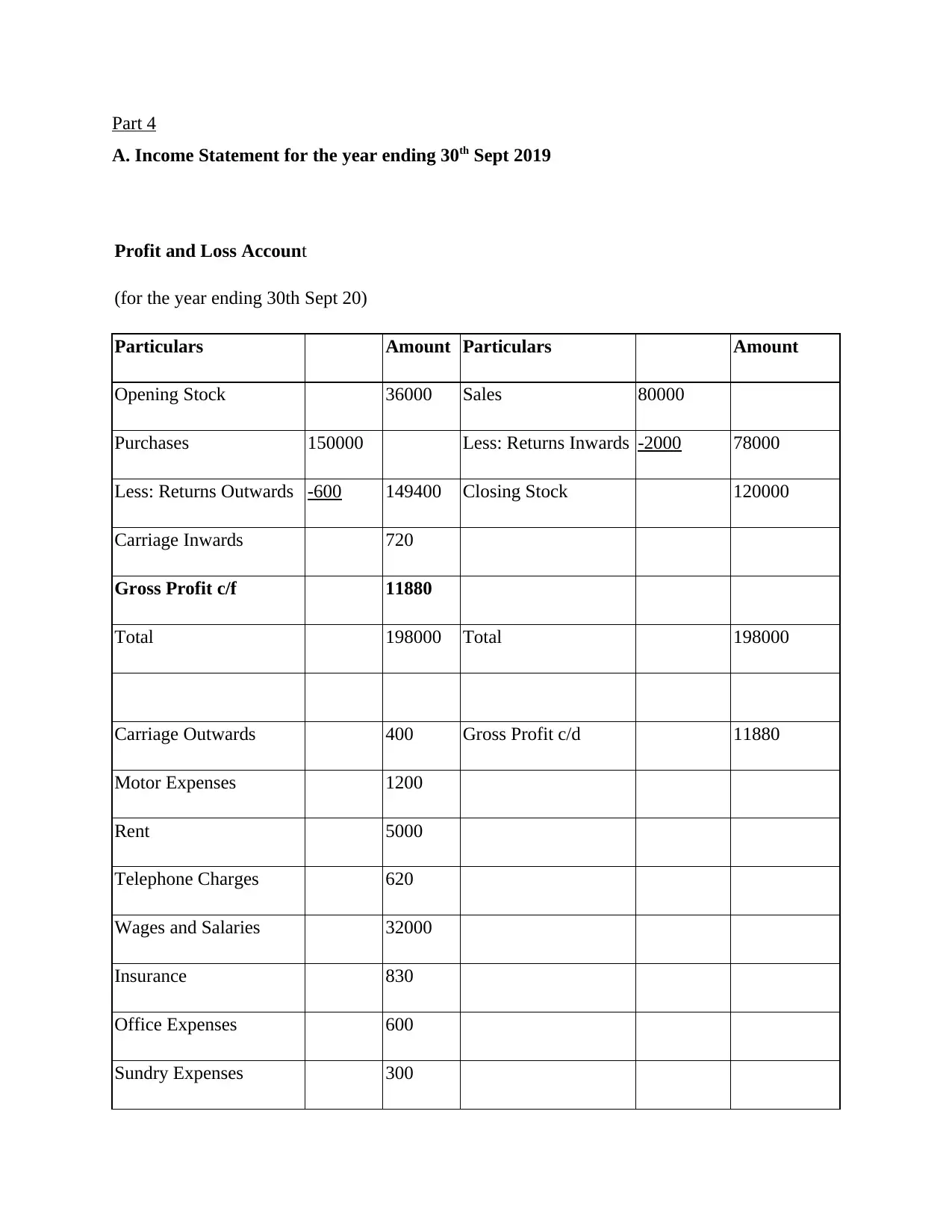

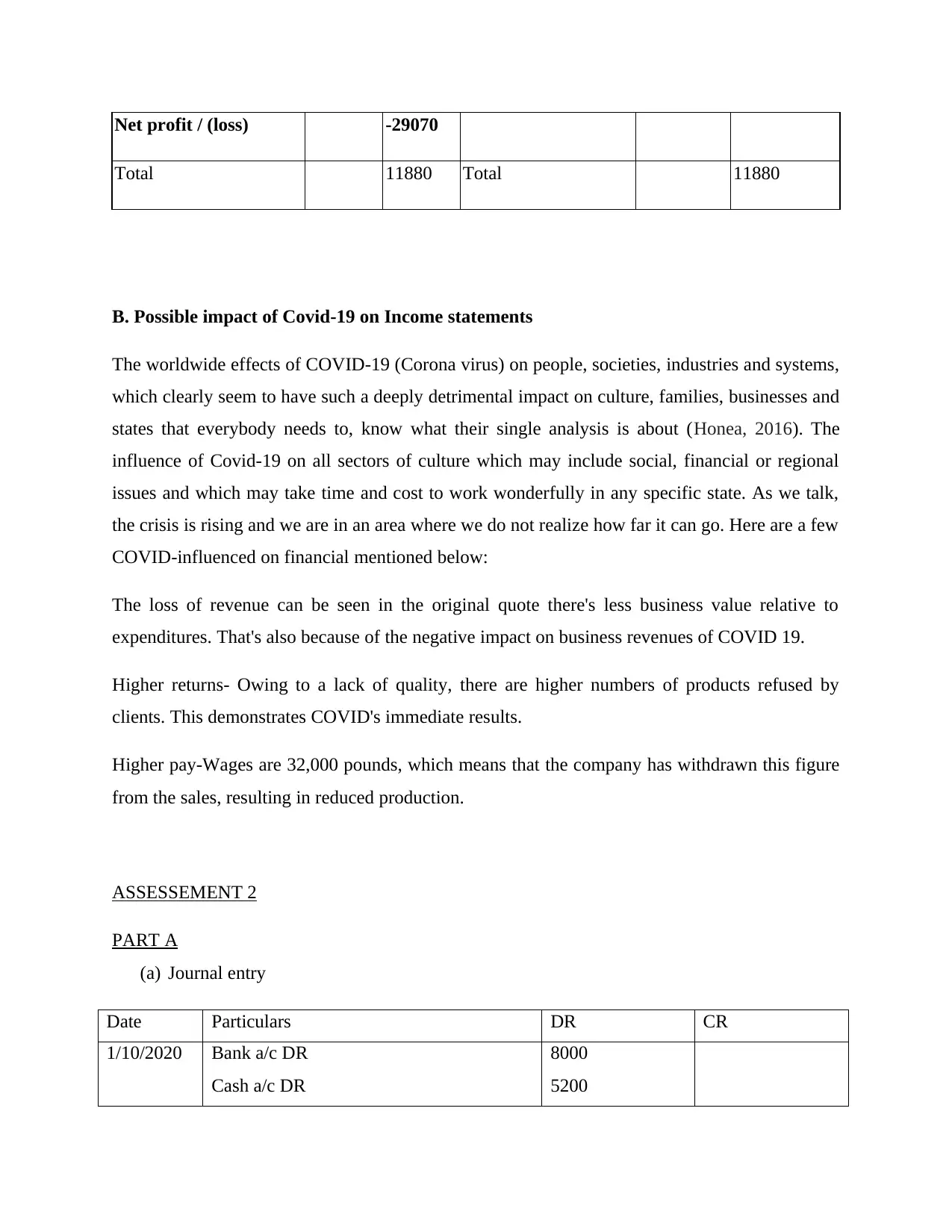

This document presents a detailed solution to an accounting assignment, encompassing two assessments. The first assessment involves various calculations, including journal entries, and the creation of ledger accounts, trial balance, and income statement. The second assessment focuses on analyzing a business's financial performance through ratio analysis. The assignment covers topics such as different types of business structures, advantages and disadvantages of accounting for profit businesses, and the potential impact of COVID-19 on income statements. The solution includes detailed journal entries, general ledger accounts, a trial balance, and an income statement, providing a comprehensive understanding of financial accounting principles and their practical application. The document also includes an analysis of the impact of COVID-19 on financial statements.

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.