ACC 200: Evaluation of Job Costing System for Connectta Limited

VerifiedAdded on 2022/11/13

|14

|2693

|249

Report

AI Summary

This report provides a detailed analysis of the costing system employed by Connectta Limited, a furniture manufacturing company. It begins with an executive summary and introduction to job costing, the system used to ascertain the cost of manufacturing. The report then delves into a discussion and analysis section, divided into six parts. Part 1 examines the suitability of job costing for Connectta Limited, given its manufacturing processes. Part 2 calculates the work in process for the period ending December 31, 2018. Part 3 calculates the cost of chairs in finished goods inventory. Part 4 analyzes the over or under-applied overhead. Part 5 discusses the accounting treatments for overhead application. Finally, Part 6 highlights the deficiencies of traditional costing methods and advocates for Activity Based Costing (ABC) to improve overhead allocation and product costing accuracy. The report concludes with a summary of findings and references.

Running head: ACC 200

ACC 200

Name of the Student:

Name of the University:

Authors Note:

ACC 200

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACC 200

Executive summary:

Costing system helps business entities especially manufacturing entities to ascertain the

cost of manufacturing. Ascertainment of proper cost of products manufactured helps the

management of such entity to impose suitable profit margin on such products to maximize the

amount of revenue and subsequent profit. Job costing is an integral branch of costing system that

is used to ascertain the cost of specific job orders performed and completed by an organization.

A detailed analysis of the costing system used in Connectta Limited along with necessary

calculation below shows the importance of a consisting system to the decision making process of

the organization. It is important to note though that the use of costing system by an organization

will be effective only when the system chosen is appropriate to the nature of business and the

business itself.

ACC 200

Executive summary:

Costing system helps business entities especially manufacturing entities to ascertain the

cost of manufacturing. Ascertainment of proper cost of products manufactured helps the

management of such entity to impose suitable profit margin on such products to maximize the

amount of revenue and subsequent profit. Job costing is an integral branch of costing system that

is used to ascertain the cost of specific job orders performed and completed by an organization.

A detailed analysis of the costing system used in Connectta Limited along with necessary

calculation below shows the importance of a consisting system to the decision making process of

the organization. It is important to note though that the use of costing system by an organization

will be effective only when the system chosen is appropriate to the nature of business and the

business itself.

2

ACC 200

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Discussion and analysis:..................................................................................................................3

Part 1:...........................................................................................................................................3

Part 2:...........................................................................................................................................3

Part 3:...........................................................................................................................................5

Part 4:...........................................................................................................................................7

Part 5:...........................................................................................................................................8

Part 6:...........................................................................................................................................9

Conclusion:....................................................................................................................................11

References:....................................................................................................................................12

ACC 200

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Discussion and analysis:..................................................................................................................3

Part 1:...........................................................................................................................................3

Part 2:...........................................................................................................................................3

Part 3:...........................................................................................................................................5

Part 4:...........................................................................................................................................7

Part 5:...........................................................................................................................................8

Part 6:...........................................................................................................................................9

Conclusion:....................................................................................................................................11

References:....................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACC 200

Introduction:

Connectta Limited is involved in manufacturing of furniture. In order to ascertain the cost of

manufacturing the company uses job costing system. All the information provided about the

manufacturing activities of the company shall be used to ascertain whether the job costing

system is appropriate for the company and disclosing the actual cost of production. On the basis

of available information necessary calculation shall also be made to ascertain the cost of

furniture manufactured by the company (Askarany, 2011).

Discussion and analysis:

Part 1:

Manufacturing entities such as cloth manufacturing entities, food manufacturing entities, air craft

manufacturing entities are examples of entities which use job costing system to ascertain the cost

of cloths, foods and aircrafts. Thus, entities with manufacturing settings that enable them to track

jobs with different types of direct expenses including direct materials and direct labor will use

job costing. Thus, an organization that manufactures such products that enable them to track

different jobs used to manufacture these products will use job costing system. Hence, when a

company manufactures products which are not identical and requires different specifications for

different products use of job costing system shall be appropriate (Esmalifalak, Albin and

Behzadpoor, 2015).

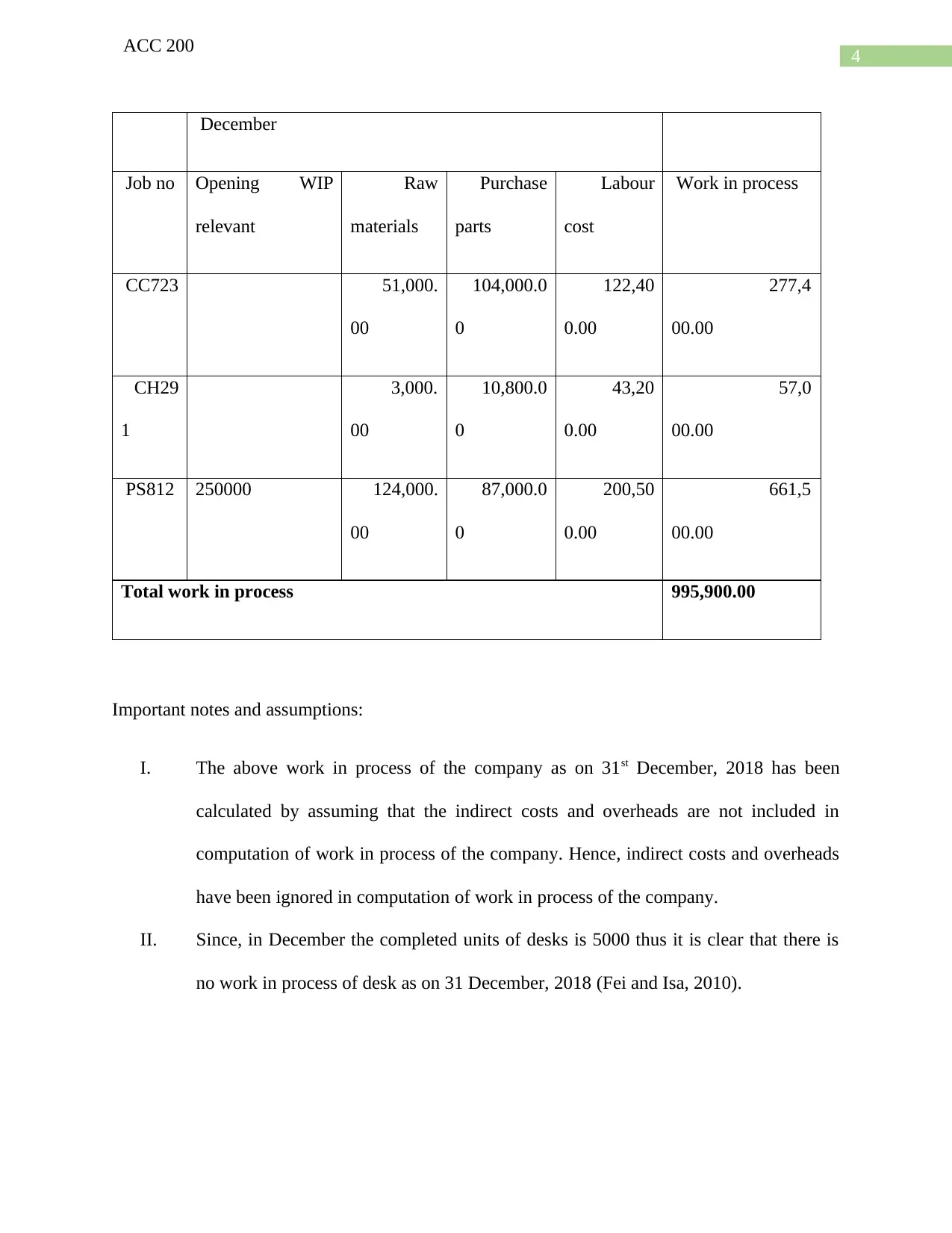

Part 2:

As per the information the work in process of the company for the period ending on November

30 has been provided. Taking into consideration the requisition of raw materials, use of labor and

other direct costs incurred in the month of December the work in process of the company as on

December 31 is calculated below:

ACC 200

Introduction:

Connectta Limited is involved in manufacturing of furniture. In order to ascertain the cost of

manufacturing the company uses job costing system. All the information provided about the

manufacturing activities of the company shall be used to ascertain whether the job costing

system is appropriate for the company and disclosing the actual cost of production. On the basis

of available information necessary calculation shall also be made to ascertain the cost of

furniture manufactured by the company (Askarany, 2011).

Discussion and analysis:

Part 1:

Manufacturing entities such as cloth manufacturing entities, food manufacturing entities, air craft

manufacturing entities are examples of entities which use job costing system to ascertain the cost

of cloths, foods and aircrafts. Thus, entities with manufacturing settings that enable them to track

jobs with different types of direct expenses including direct materials and direct labor will use

job costing. Thus, an organization that manufactures such products that enable them to track

different jobs used to manufacture these products will use job costing system. Hence, when a

company manufactures products which are not identical and requires different specifications for

different products use of job costing system shall be appropriate (Esmalifalak, Albin and

Behzadpoor, 2015).

Part 2:

As per the information the work in process of the company for the period ending on November

30 has been provided. Taking into consideration the requisition of raw materials, use of labor and

other direct costs incurred in the month of December the work in process of the company as on

December 31 is calculated below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACC 200

December

Job no Opening WIP

relevant

Raw

materials

Purchase

parts

Labour

cost

Work in process

CC723 51,000.

00

104,000.0

0

122,40

0.00

277,4

00.00

CH29

1

3,000.

00

10,800.0

0

43,20

0.00

57,0

00.00

PS812 250000 124,000.

00

87,000.0

0

200,50

0.00

661,5

00.00

Total work in process 995,900.00

Important notes and assumptions:

I. The above work in process of the company as on 31st December, 2018 has been

calculated by assuming that the indirect costs and overheads are not included in

computation of work in process of the company. Hence, indirect costs and overheads

have been ignored in computation of work in process of the company.

II. Since, in December the completed units of desks is 5000 thus it is clear that there is

no work in process of desk as on 31 December, 2018 (Fei and Isa, 2010).

ACC 200

December

Job no Opening WIP

relevant

Raw

materials

Purchase

parts

Labour

cost

Work in process

CC723 51,000.

00

104,000.0

0

122,40

0.00

277,4

00.00

CH29

1

3,000.

00

10,800.0

0

43,20

0.00

57,0

00.00

PS812 250000 124,000.

00

87,000.0

0

200,50

0.00

661,5

00.00

Total work in process 995,900.00

Important notes and assumptions:

I. The above work in process of the company as on 31st December, 2018 has been

calculated by assuming that the indirect costs and overheads are not included in

computation of work in process of the company. Hence, indirect costs and overheads

have been ignored in computation of work in process of the company.

II. Since, in December the completed units of desks is 5000 thus it is clear that there is

no work in process of desk as on 31 December, 2018 (Fei and Isa, 2010).

5

ACC 200

III. No printer stand has been completed as on 31st December, 2018 thus, it is clear that

the work in process as on 30th November, 2018 is still included in the working process

of the company as on 31st December 2018.

Taking into consideration the above notes the work in process of the company as on 31st

December, 2018 is $995900.00.

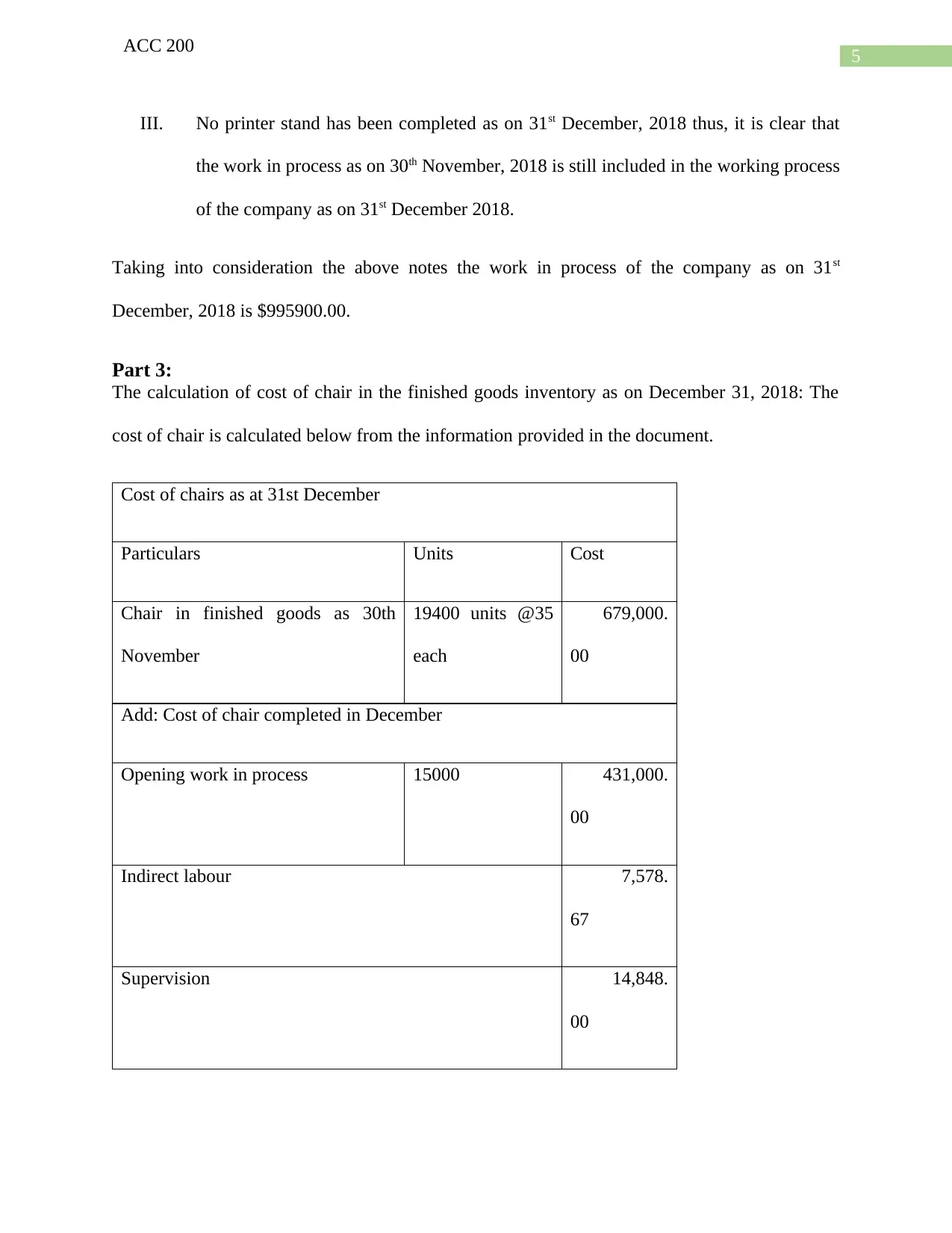

Part 3:

The calculation of cost of chair in the finished goods inventory as on December 31, 2018: The

cost of chair is calculated below from the information provided in the document.

Cost of chairs as at 31st December

Particulars Units Cost

Chair in finished goods as 30th

November

19400 units @35

each

679,000.

00

Add: Cost of chair completed in December

Opening work in process 15000 431,000.

00

Indirect labour 7,578.

67

Supervision 14,848.

00

ACC 200

III. No printer stand has been completed as on 31st December, 2018 thus, it is clear that

the work in process as on 30th November, 2018 is still included in the working process

of the company as on 31st December 2018.

Taking into consideration the above notes the work in process of the company as on 31st

December, 2018 is $995900.00.

Part 3:

The calculation of cost of chair in the finished goods inventory as on December 31, 2018: The

cost of chair is calculated below from the information provided in the document.

Cost of chairs as at 31st December

Particulars Units Cost

Chair in finished goods as 30th

November

19400 units @35

each

679,000.

00

Add: Cost of chair completed in December

Opening work in process 15000 431,000.

00

Indirect labour 7,578.

67

Supervision 14,848.

00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

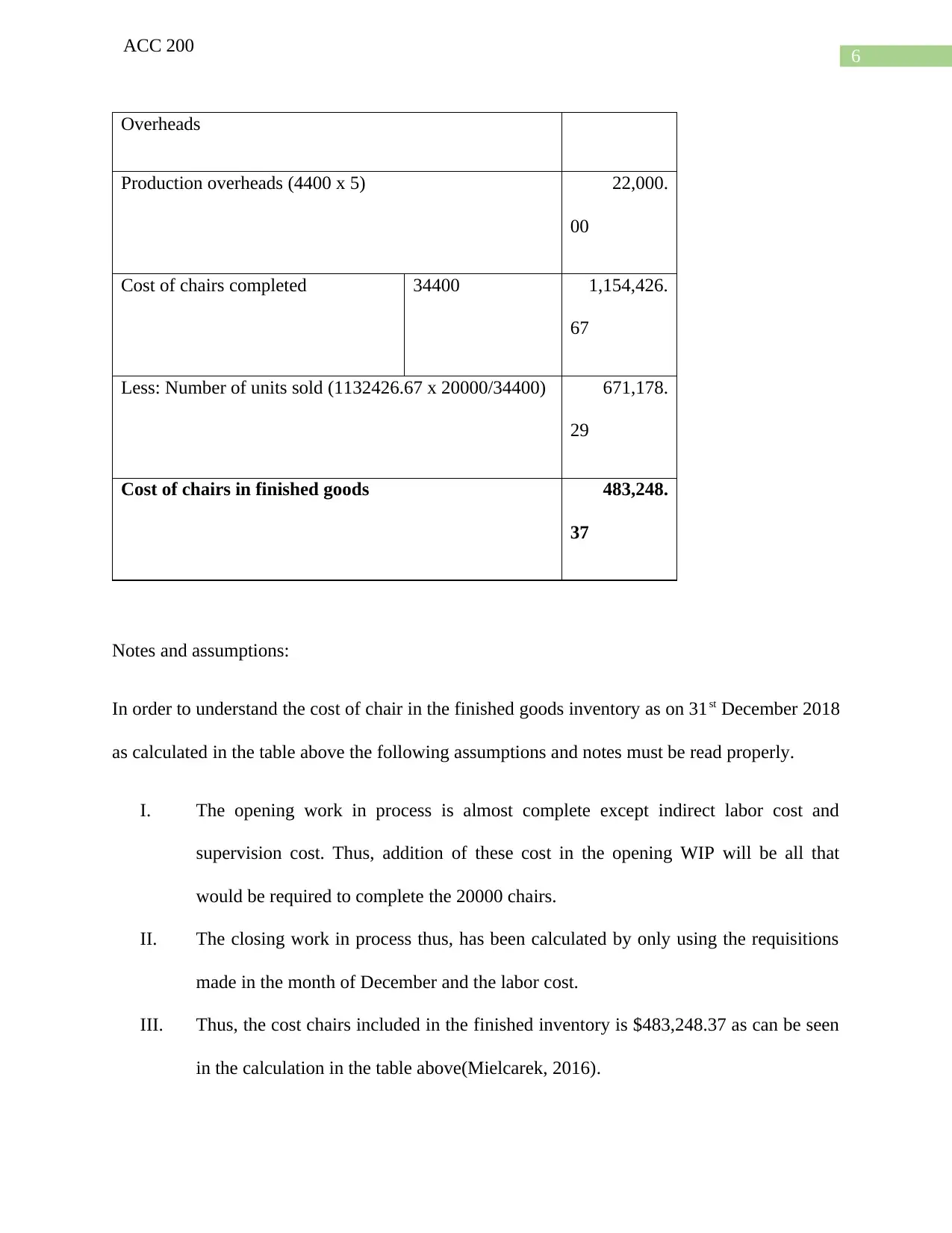

ACC 200

Overheads

Production overheads (4400 x 5) 22,000.

00

Cost of chairs completed 34400 1,154,426.

67

Less: Number of units sold (1132426.67 x 20000/34400) 671,178.

29

Cost of chairs in finished goods 483,248.

37

Notes and assumptions:

In order to understand the cost of chair in the finished goods inventory as on 31st December 2018

as calculated in the table above the following assumptions and notes must be read properly.

I. The opening work in process is almost complete except indirect labor cost and

supervision cost. Thus, addition of these cost in the opening WIP will be all that

would be required to complete the 20000 chairs.

II. The closing work in process thus, has been calculated by only using the requisitions

made in the month of December and the labor cost.

III. Thus, the cost chairs included in the finished inventory is $483,248.37 as can be seen

in the calculation in the table above(Mielcarek, 2016).

ACC 200

Overheads

Production overheads (4400 x 5) 22,000.

00

Cost of chairs completed 34400 1,154,426.

67

Less: Number of units sold (1132426.67 x 20000/34400) 671,178.

29

Cost of chairs in finished goods 483,248.

37

Notes and assumptions:

In order to understand the cost of chair in the finished goods inventory as on 31st December 2018

as calculated in the table above the following assumptions and notes must be read properly.

I. The opening work in process is almost complete except indirect labor cost and

supervision cost. Thus, addition of these cost in the opening WIP will be all that

would be required to complete the 20000 chairs.

II. The closing work in process thus, has been calculated by only using the requisitions

made in the month of December and the labor cost.

III. Thus, the cost chairs included in the finished inventory is $483,248.37 as can be seen

in the calculation in the table above(Mielcarek, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACC 200

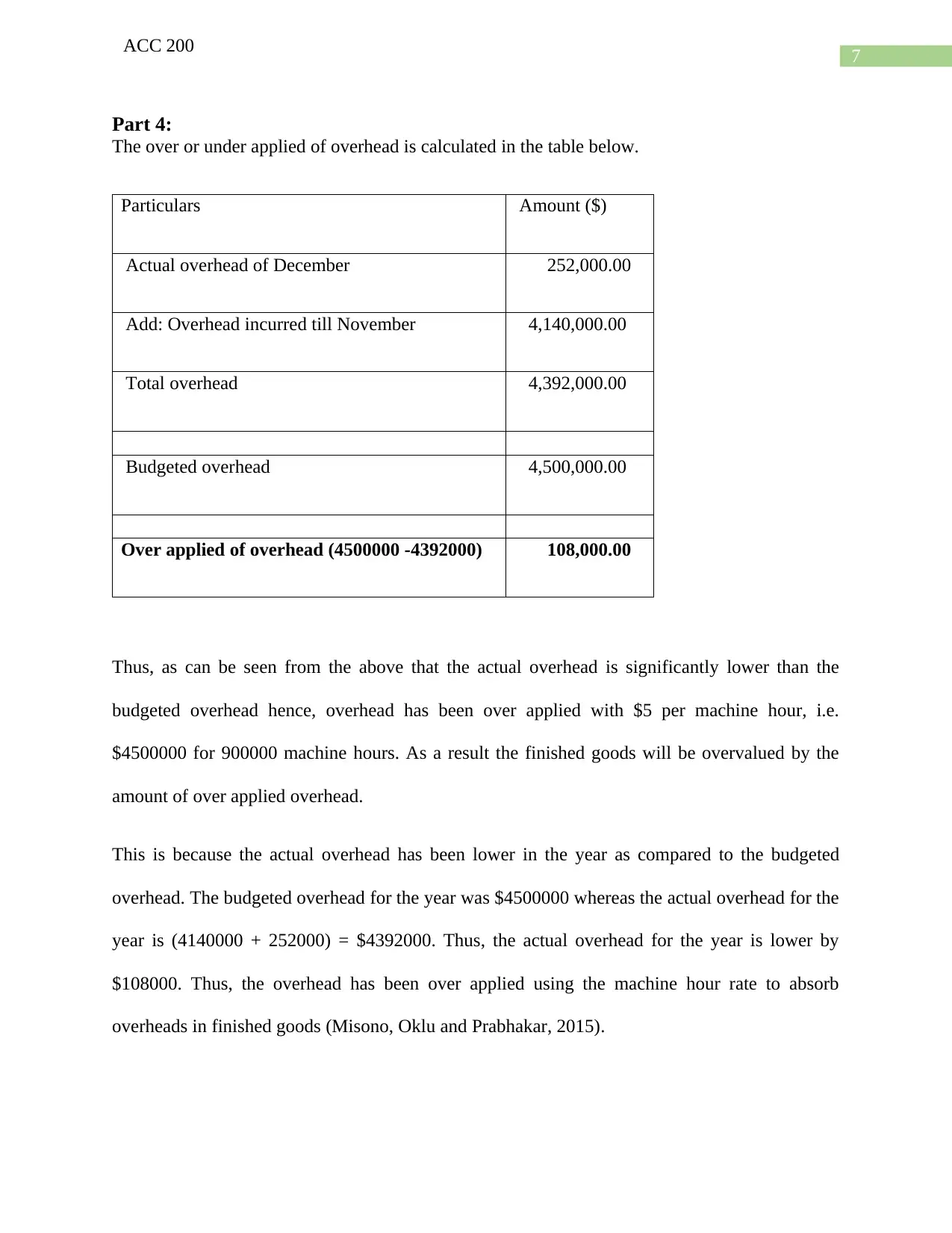

Part 4:

The over or under applied of overhead is calculated in the table below.

Particulars Amount ($)

Actual overhead of December 252,000.00

Add: Overhead incurred till November 4,140,000.00

Total overhead 4,392,000.00

Budgeted overhead 4,500,000.00

Over applied of overhead (4500000 -4392000) 108,000.00

Thus, as can be seen from the above that the actual overhead is significantly lower than the

budgeted overhead hence, overhead has been over applied with $5 per machine hour, i.e.

$4500000 for 900000 machine hours. As a result the finished goods will be overvalued by the

amount of over applied overhead.

This is because the actual overhead has been lower in the year as compared to the budgeted

overhead. The budgeted overhead for the year was $4500000 whereas the actual overhead for the

year is (4140000 + 252000) = $4392000. Thus, the actual overhead for the year is lower by

$108000. Thus, the overhead has been over applied using the machine hour rate to absorb

overheads in finished goods (Misono, Oklu and Prabhakar, 2015).

ACC 200

Part 4:

The over or under applied of overhead is calculated in the table below.

Particulars Amount ($)

Actual overhead of December 252,000.00

Add: Overhead incurred till November 4,140,000.00

Total overhead 4,392,000.00

Budgeted overhead 4,500,000.00

Over applied of overhead (4500000 -4392000) 108,000.00

Thus, as can be seen from the above that the actual overhead is significantly lower than the

budgeted overhead hence, overhead has been over applied with $5 per machine hour, i.e.

$4500000 for 900000 machine hours. As a result the finished goods will be overvalued by the

amount of over applied overhead.

This is because the actual overhead has been lower in the year as compared to the budgeted

overhead. The budgeted overhead for the year was $4500000 whereas the actual overhead for the

year is (4140000 + 252000) = $4392000. Thus, the actual overhead for the year is lower by

$108000. Thus, the overhead has been over applied using the machine hour rate to absorb

overheads in finished goods (Misono, Oklu and Prabhakar, 2015).

8

ACC 200

Part 5:

The accounting treatment of overhead applied on products to ascertain the cost of production is

quite complex especially when the overhead is over or under applied. In general the overhead

absorbed is directly debited to the cost of production in accounting when the overhead is neither

under nor over applied. However, in case of under or over application of overhead then there are

alternative accounting treatment to account for the over applied or under applied overhead as the

case may be (RUAN and ZHOU, 2017).

Firstly, in accounting the overheads are directly transferred to the cost of production thus, the

cost of production is debited with proportionate credit to the production overhead. In case the

actual overhead is lower than the budgeted overhead then the actual overhead is considered in

accounting to ensure that the goods are not overvalued. For example the budgeted overhead is $5

per hour however, the actual production is lower at $4.50 per hour then the accounting treatment

will record the production overhead at $4.50 per hour to make sure that the finished goods are

not overvalued.

In case the actual production overhead is higher than the budgeted production overhead then

contrastingly the actual production overhead is not considered to value the inventory. Instead the

budgeted production overheads is used to ascertain the cost of goods sold and accordingly,

accounting treatment is made. The excess production overhead over and above the budgeted

production overhead is directly debited in the profit and loss account. This is again done to

ensure that the inefficiency of a firm should not be reflected in finished inventory as this will

inflate the profit also (Sheu and Pan, 2009).

ACC 200

Part 5:

The accounting treatment of overhead applied on products to ascertain the cost of production is

quite complex especially when the overhead is over or under applied. In general the overhead

absorbed is directly debited to the cost of production in accounting when the overhead is neither

under nor over applied. However, in case of under or over application of overhead then there are

alternative accounting treatment to account for the over applied or under applied overhead as the

case may be (RUAN and ZHOU, 2017).

Firstly, in accounting the overheads are directly transferred to the cost of production thus, the

cost of production is debited with proportionate credit to the production overhead. In case the

actual overhead is lower than the budgeted overhead then the actual overhead is considered in

accounting to ensure that the goods are not overvalued. For example the budgeted overhead is $5

per hour however, the actual production is lower at $4.50 per hour then the accounting treatment

will record the production overhead at $4.50 per hour to make sure that the finished goods are

not overvalued.

In case the actual production overhead is higher than the budgeted production overhead then

contrastingly the actual production overhead is not considered to value the inventory. Instead the

budgeted production overheads is used to ascertain the cost of goods sold and accordingly,

accounting treatment is made. The excess production overhead over and above the budgeted

production overhead is directly debited in the profit and loss account. This is again done to

ensure that the inefficiency of a firm should not be reflected in finished inventory as this will

inflate the profit also (Sheu and Pan, 2009).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACC 200

Completely separate from the above accounting treatments an alternative accounting treatment is

to only consider the direct cost of production while calculating cost of goods sold. In such case

the production overheads are directly debited in the profit and loss account. In this case the

concept of over applied and under applied of overheads are not relevant any more. However, the

accounting treatment has a major fault line and it lies with the fact that assessing the efficiency

of an organization will be difficult as the indirect costs will be directly debited in the profit and

loss account (Vazakidis and Karagiannis, 2009).

Part 6:

There are number of deficiencies in traditional costing method in which a predetermined

overhead rate is calculated by using either direct labor hour or machine hour. The deficiencies of

the traditional costing system firstly need to be discussed before analyzing the merit behind using

an alternative costing method to apply production overheads. The deficiencies are discussed

below:

I. The production overheads are an indirect cost pool where number of indirect costs are

accumulated. Using a single pre-determined overhead rate by using direct material or

direct labor or machine hour cannot properly allocate the production overheads to

different products.

II. There are number of components of production overheads such as ordering cost,

machine set up cost, inspection cost, power electricity and other such cost. Different

products require different quantum of these elements thus using a single

predetermined overhead rate based on a pre-determined yardstick will not correctly

ascertain the cost of different products (Wegmann, 2011).

ACC 200

Completely separate from the above accounting treatments an alternative accounting treatment is

to only consider the direct cost of production while calculating cost of goods sold. In such case

the production overheads are directly debited in the profit and loss account. In this case the

concept of over applied and under applied of overheads are not relevant any more. However, the

accounting treatment has a major fault line and it lies with the fact that assessing the efficiency

of an organization will be difficult as the indirect costs will be directly debited in the profit and

loss account (Vazakidis and Karagiannis, 2009).

Part 6:

There are number of deficiencies in traditional costing method in which a predetermined

overhead rate is calculated by using either direct labor hour or machine hour. The deficiencies of

the traditional costing system firstly need to be discussed before analyzing the merit behind using

an alternative costing method to apply production overheads. The deficiencies are discussed

below:

I. The production overheads are an indirect cost pool where number of indirect costs are

accumulated. Using a single pre-determined overhead rate by using direct material or

direct labor or machine hour cannot properly allocate the production overheads to

different products.

II. There are number of components of production overheads such as ordering cost,

machine set up cost, inspection cost, power electricity and other such cost. Different

products require different quantum of these elements thus using a single

predetermined overhead rate based on a pre-determined yardstick will not correctly

ascertain the cost of different products (Wegmann, 2011).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACC 200

Thus, with passage of time of traditional costing system has lose its popularity and organizations

now use activity based costing and other costing methods to allocate the production overheads

properly. A brief introduction about the Activity Based Costing shall be helpful to the readers

before proceeding to dissect the benefits using the method to overcome the deficiencies of

traditional costing system.

Activity based costing (ABC): In ABC method the indirect costs are divided into different cost

pools. The cost drivers are identified which are contributing to the cost pools. Based on the cost

drivers the costs of different cost pools are allocated to different products. Identification of cost

drivers is the most crucial element in ABC system to correctly allocate the production overheads.

Thus, it is clear that there is significant difference between the traditional costing method and

activity based costing method. Unlike traditional costing method in ABC method the production

overheads are segregated into different cost pools depending on the cost drivers. The cost pools

then allocated to different products on the basis of cost drivers. Thus, the following deficiencies

of traditional costing system can be overcame with the use of ABC system to allocate production

overheads.

The overheads will not be allocated on the basis of a pre-determined overhead rate:

The production overheads will be allocated on the basis of cost drivers after identifying the

drivers and allocating the costs to different costs pools. Thus, no single pre-determined overhead

arte will be used to allocate the production overheads.

Unscientific method of traditional costing system will not be followed: The traditional costing

system is quite unscientific when it comes to allocation of production overheads in different

products. Use of cost drivers and cost pools is a scientific way to allocate production overheads.

ACC 200

Thus, with passage of time of traditional costing system has lose its popularity and organizations

now use activity based costing and other costing methods to allocate the production overheads

properly. A brief introduction about the Activity Based Costing shall be helpful to the readers

before proceeding to dissect the benefits using the method to overcome the deficiencies of

traditional costing system.

Activity based costing (ABC): In ABC method the indirect costs are divided into different cost

pools. The cost drivers are identified which are contributing to the cost pools. Based on the cost

drivers the costs of different cost pools are allocated to different products. Identification of cost

drivers is the most crucial element in ABC system to correctly allocate the production overheads.

Thus, it is clear that there is significant difference between the traditional costing method and

activity based costing method. Unlike traditional costing method in ABC method the production

overheads are segregated into different cost pools depending on the cost drivers. The cost pools

then allocated to different products on the basis of cost drivers. Thus, the following deficiencies

of traditional costing system can be overcame with the use of ABC system to allocate production

overheads.

The overheads will not be allocated on the basis of a pre-determined overhead rate:

The production overheads will be allocated on the basis of cost drivers after identifying the

drivers and allocating the costs to different costs pools. Thus, no single pre-determined overhead

arte will be used to allocate the production overheads.

Unscientific method of traditional costing system will not be followed: The traditional costing

system is quite unscientific when it comes to allocation of production overheads in different

products. Use of cost drivers and cost pools is a scientific way to allocate production overheads.

11

ACC 200

Ascertainment of product cost correctly: With the use of ABC method it would be possible to

correctly ascertain the cost of product properly. With Traditional costing method it is not

possible to correctly ascertain the cost of different products as the overhead allocation in most of

the times is improper and incorrect (Woodward, 2005).

Dealing with ineffective management: With the use of ABC method it would be possible to

correctly ascertain the cost of different products which will help the management to correctly

price these products. This will help the management to efficiently manage an organization as

correct product pricing often end up increasing the amount of revenue of an organization.

Increase amount of profitability with proper management: The ABC system as already

mentioned will help the management to correctly ascertain the cost of products. Once the cost of

products is correctly determined it would be possible for the management to impose appropriate

percentage as the margin tom determine the selling price with the objective of maximizing the

amount of revenue and resultant profit. Thus, achieving higher profitability and revenue would

be possible with the use of ABC method to allocate production overheads.

Conclusion:

Discussion in the above document shows the importance of allocation of production

overheads correctly. There are primarily two methods to allocate production overheads in

different products these are Traditional and Activity Based Costing (ABC). Using ABC method

will help the management of an organization to allocate the production overheads in different

products correctly. Thus, it is important to use ABC method to correctly ascertain the cost of

products.

ACC 200

Ascertainment of product cost correctly: With the use of ABC method it would be possible to

correctly ascertain the cost of product properly. With Traditional costing method it is not

possible to correctly ascertain the cost of different products as the overhead allocation in most of

the times is improper and incorrect (Woodward, 2005).

Dealing with ineffective management: With the use of ABC method it would be possible to

correctly ascertain the cost of different products which will help the management to correctly

price these products. This will help the management to efficiently manage an organization as

correct product pricing often end up increasing the amount of revenue of an organization.

Increase amount of profitability with proper management: The ABC system as already

mentioned will help the management to correctly ascertain the cost of products. Once the cost of

products is correctly determined it would be possible for the management to impose appropriate

percentage as the margin tom determine the selling price with the objective of maximizing the

amount of revenue and resultant profit. Thus, achieving higher profitability and revenue would

be possible with the use of ABC method to allocate production overheads.

Conclusion:

Discussion in the above document shows the importance of allocation of production

overheads correctly. There are primarily two methods to allocate production overheads in

different products these are Traditional and Activity Based Costing (ABC). Using ABC method

will help the management of an organization to allocate the production overheads in different

products correctly. Thus, it is important to use ABC method to correctly ascertain the cost of

products.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.