ACC566 - Accounting Systems: Assessment 2 Solution, June 2019

VerifiedAdded on 2022/10/15

|24

|4517

|407

Homework Assignment

AI Summary

This document provides a comprehensive solution to ACC566 Assessment 2, focusing on accounting systems and processes. The solution covers multiple aspects of financial accounting, including the application of the FIFO (First-In, First-Out) method for inventory valuation with detailed calculations for small and large bicycles. It includes journal entries, ledger postings (Purchase A/c, Bank A/c, Capital A/c, Red bike rock ltd A/c, Fast freight ltd A/c, Delivery cost A/c, Stall fees A/c, Discount received A/c, Local childcare center A/c, Sales A/c), and an adjusted trial balance. Furthermore, the solution addresses bank reconciliation, providing a detailed bank reconciliation statement, adjusting entries, and a bank account ledger. The document aims to assist students in understanding and solving complex accounting problems related to inventory, journal entries, ledger accounts, trial balance, and bank reconciliation, offering a complete and practical guide to enhance their learning experience in financial accounting.

ACC 566

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Assessment 2..............................................................................................................................3

Question 1..................................................................................................................................3

i).............................................................................................................................................3

ii)............................................................................................................................................5

iii)...........................................................................................................................................7

iv).........................................................................................................................................11

v)..........................................................................................................................................12

Question 2................................................................................................................................13

i)...........................................................................................................................................13

ii)..........................................................................................................................................13

iii).........................................................................................................................................15

iv).........................................................................................................................................15

Question 3................................................................................................................................17

Introduction..........................................................................................................................17

Internal control and its importance......................................................................................17

Risk of employee theft.........................................................................................................18

Ways by which bicycles would have stolen.........................................................................19

Procedure to prevent employee theft....................................................................................19

Conclusion............................................................................................................................20

Question 4................................................................................................................................21

References................................................................................................................................23

Assessment 2..............................................................................................................................3

Question 1..................................................................................................................................3

i).............................................................................................................................................3

ii)............................................................................................................................................5

iii)...........................................................................................................................................7

iv).........................................................................................................................................11

v)..........................................................................................................................................12

Question 2................................................................................................................................13

i)...........................................................................................................................................13

ii)..........................................................................................................................................13

iii).........................................................................................................................................15

iv).........................................................................................................................................15

Question 3................................................................................................................................17

Introduction..........................................................................................................................17

Internal control and its importance......................................................................................17

Risk of employee theft.........................................................................................................18

Ways by which bicycles would have stolen.........................................................................19

Procedure to prevent employee theft....................................................................................19

Conclusion............................................................................................................................20

Question 4................................................................................................................................21

References................................................................................................................................23

Assessment 2

Question 1

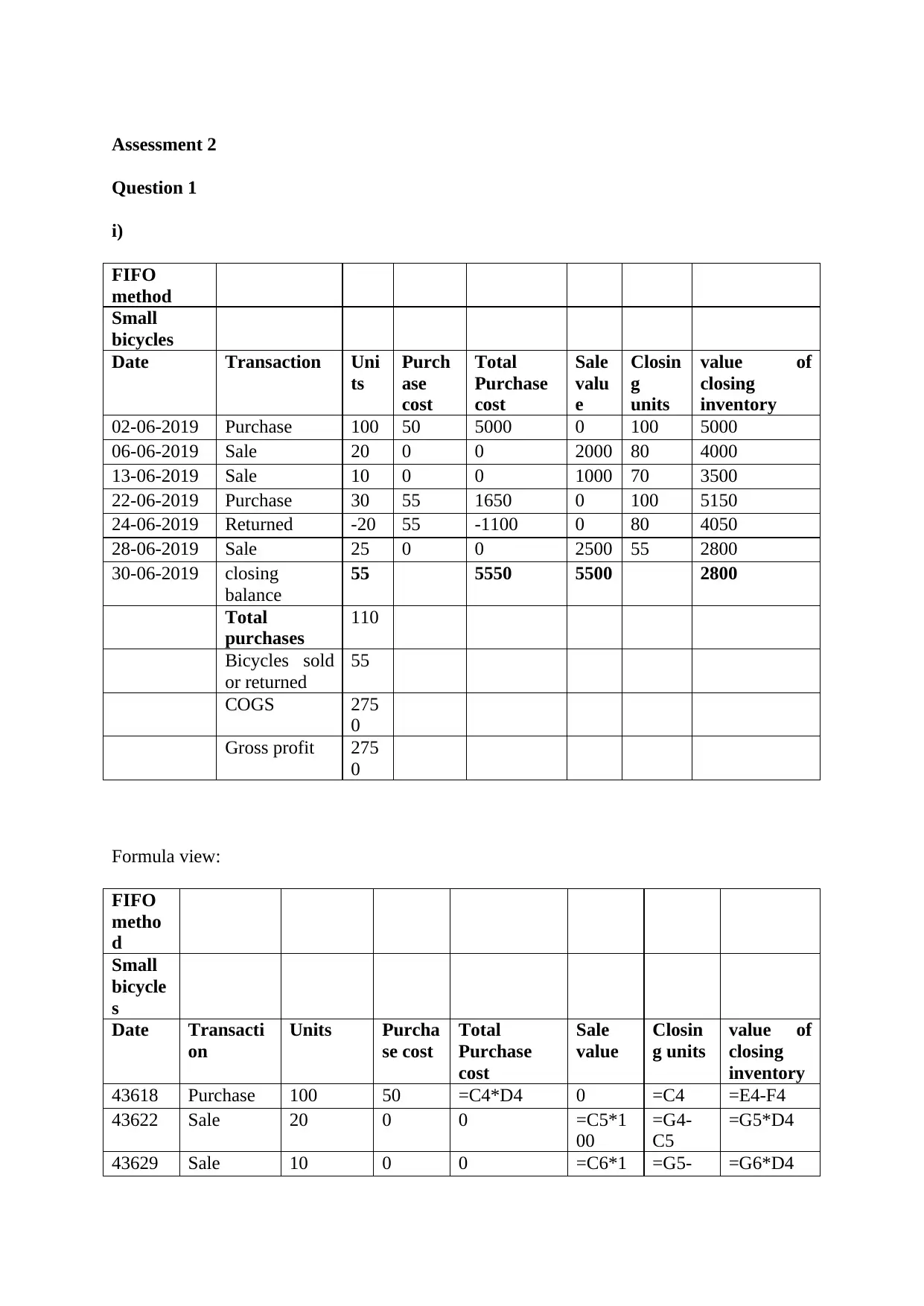

i)

FIFO

method

Small

bicycles

Date Transaction Uni

ts

Purch

ase

cost

Total

Purchase

cost

Sale

valu

e

Closin

g

units

value of

closing

inventory

02-06-2019 Purchase 100 50 5000 0 100 5000

06-06-2019 Sale 20 0 0 2000 80 4000

13-06-2019 Sale 10 0 0 1000 70 3500

22-06-2019 Purchase 30 55 1650 0 100 5150

24-06-2019 Returned -20 55 -1100 0 80 4050

28-06-2019 Sale 25 0 0 2500 55 2800

30-06-2019 closing

balance

55 5550 5500 2800

Total

purchases

110

Bicycles sold

or returned

55

COGS 275

0

Gross profit 275

0

Formula view:

FIFO

metho

d

Small

bicycle

s

Date Transacti

on

Units Purcha

se cost

Total

Purchase

cost

Sale

value

Closin

g units

value of

closing

inventory

43618 Purchase 100 50 =C4*D4 0 =C4 =E4-F4

43622 Sale 20 0 0 =C5*1

00

=G4-

C5

=G5*D4

43629 Sale 10 0 0 =C6*1 =G5- =G6*D4

Question 1

i)

FIFO

method

Small

bicycles

Date Transaction Uni

ts

Purch

ase

cost

Total

Purchase

cost

Sale

valu

e

Closin

g

units

value of

closing

inventory

02-06-2019 Purchase 100 50 5000 0 100 5000

06-06-2019 Sale 20 0 0 2000 80 4000

13-06-2019 Sale 10 0 0 1000 70 3500

22-06-2019 Purchase 30 55 1650 0 100 5150

24-06-2019 Returned -20 55 -1100 0 80 4050

28-06-2019 Sale 25 0 0 2500 55 2800

30-06-2019 closing

balance

55 5550 5500 2800

Total

purchases

110

Bicycles sold

or returned

55

COGS 275

0

Gross profit 275

0

Formula view:

FIFO

metho

d

Small

bicycle

s

Date Transacti

on

Units Purcha

se cost

Total

Purchase

cost

Sale

value

Closin

g units

value of

closing

inventory

43618 Purchase 100 50 =C4*D4 0 =C4 =E4-F4

43622 Sale 20 0 0 =C5*1

00

=G4-

C5

=G5*D4

43629 Sale 10 0 0 =C6*1 =G5- =G6*D4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

00 C6

43638 Purchase 30 55 =C7*D7 0 =G6+C

7

=H6+E7

43640 Returned -20 55 =C8*D8 =0 =G7+C

8

=H7+E8

43644 Sale 25 0 0 =C9*1

00

=G8-

C9

=(45*50)+

(10*55)

43646 closing

balance

=C4-C5-

C6+C7+

C8-C9

=E4+E7+E8 =SUM(

F4:F10

)

=H9

Total

purchases

=C4+C7+

C8

Bicycles

sold or

returned

=C5+C6+

C9

COGS =0+E10-

H10

Gross

profit

=5500-

C13

large bicycles

Date Transaction Unit

s

Purchas

e cost

Total

Purchase

cost

Sale

valu

e

Closin

g units

value of closing

inventory

02-

06-

2019

Purchase 100 50 5000 0 100 5000

06-

06-

2019

Sale 10 0 0 1000 90 4500

22-

06-

2019

Purchase 10 55 550 0 100 5050

28-

06-

2019

Sale 15 0 0 1500 85 4300

30-

06-

2019

closing balance 85 5550 2500 4300

Total

purchases

110

Bicycles sold

or returned

25

COGS 1250

Gross profit 1250

43638 Purchase 30 55 =C7*D7 0 =G6+C

7

=H6+E7

43640 Returned -20 55 =C8*D8 =0 =G7+C

8

=H7+E8

43644 Sale 25 0 0 =C9*1

00

=G8-

C9

=(45*50)+

(10*55)

43646 closing

balance

=C4-C5-

C6+C7+

C8-C9

=E4+E7+E8 =SUM(

F4:F10

)

=H9

Total

purchases

=C4+C7+

C8

Bicycles

sold or

returned

=C5+C6+

C9

COGS =0+E10-

H10

Gross

profit

=5500-

C13

large bicycles

Date Transaction Unit

s

Purchas

e cost

Total

Purchase

cost

Sale

valu

e

Closin

g units

value of closing

inventory

02-

06-

2019

Purchase 100 50 5000 0 100 5000

06-

06-

2019

Sale 10 0 0 1000 90 4500

22-

06-

2019

Purchase 10 55 550 0 100 5050

28-

06-

2019

Sale 15 0 0 1500 85 4300

30-

06-

2019

closing balance 85 5550 2500 4300

Total

purchases

110

Bicycles sold

or returned

25

COGS 1250

Gross profit 1250

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

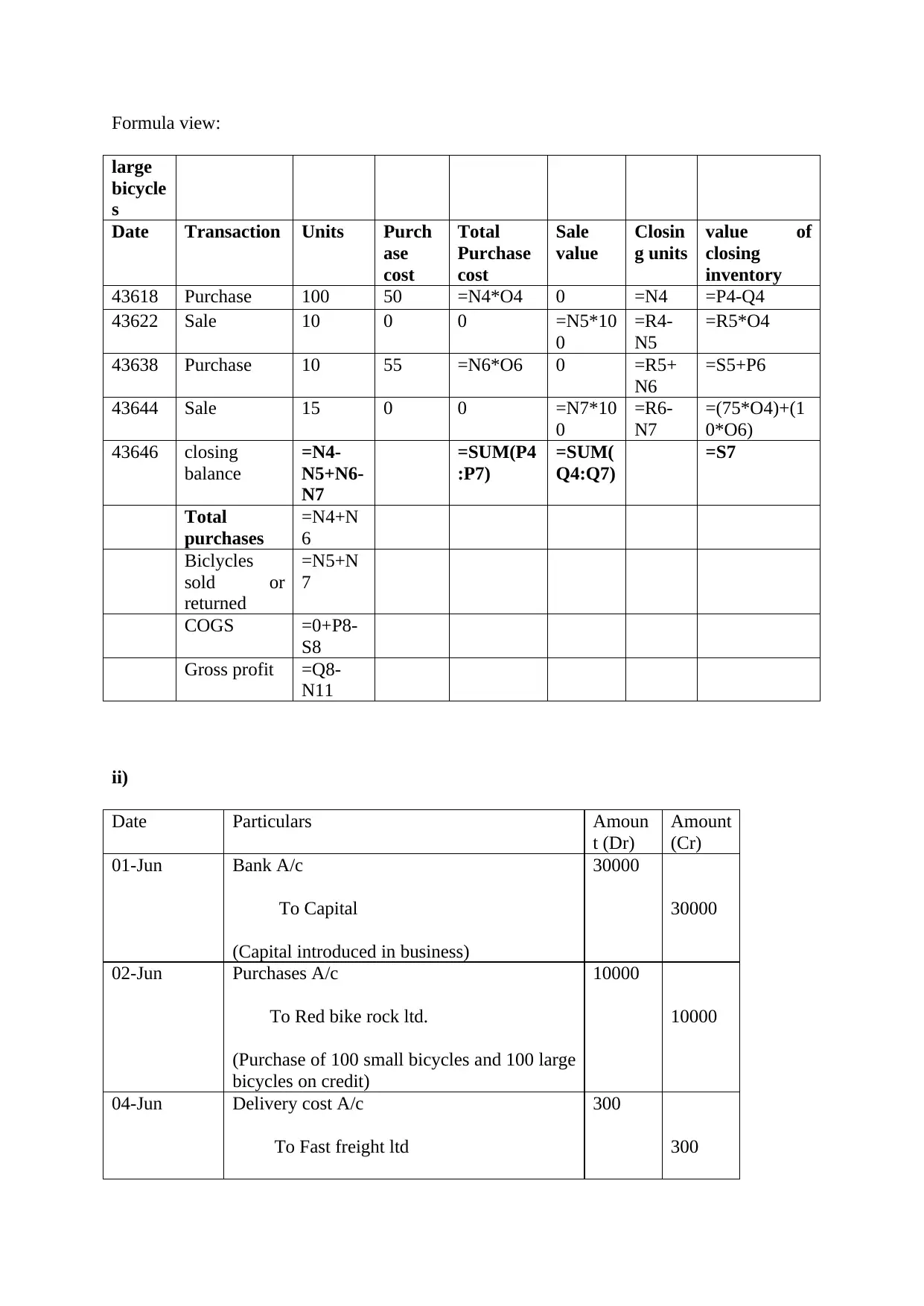

Formula view:

large

bicycle

s

Date Transaction Units Purch

ase

cost

Total

Purchase

cost

Sale

value

Closin

g units

value of

closing

inventory

43618 Purchase 100 50 =N4*O4 0 =N4 =P4-Q4

43622 Sale 10 0 0 =N5*10

0

=R4-

N5

=R5*O4

43638 Purchase 10 55 =N6*O6 0 =R5+

N6

=S5+P6

43644 Sale 15 0 0 =N7*10

0

=R6-

N7

=(75*O4)+(1

0*O6)

43646 closing

balance

=N4-

N5+N6-

N7

=SUM(P4

:P7)

=SUM(

Q4:Q7)

=S7

Total

purchases

=N4+N

6

Biclycles

sold or

returned

=N5+N

7

COGS =0+P8-

S8

Gross profit =Q8-

N11

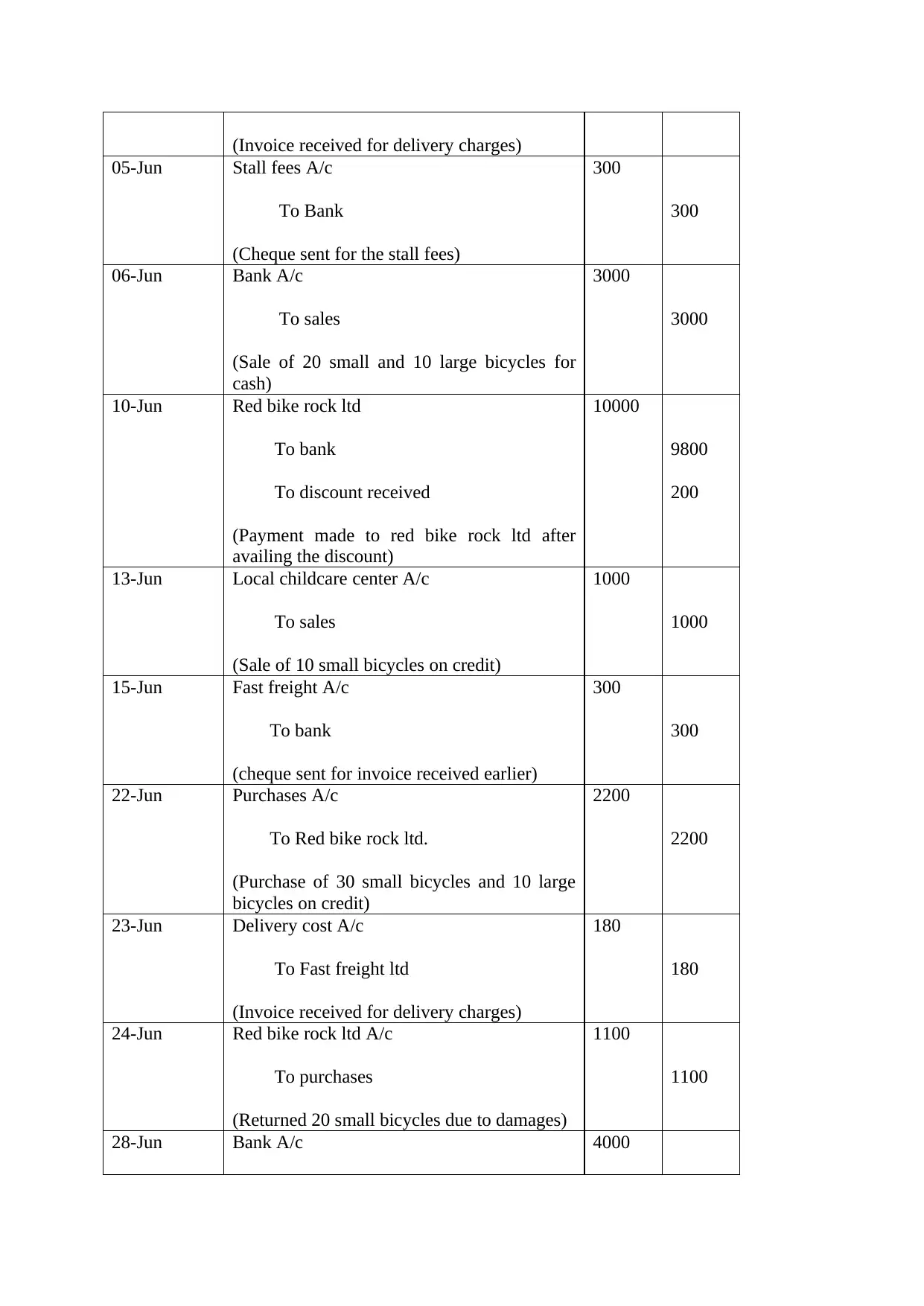

ii)

Date Particulars Amoun

t (Dr)

Amount

(Cr)

01-Jun Bank A/c

To Capital

(Capital introduced in business)

30000

30000

02-Jun Purchases A/c

To Red bike rock ltd.

(Purchase of 100 small bicycles and 100 large

bicycles on credit)

10000

10000

04-Jun Delivery cost A/c

To Fast freight ltd

300

300

large

bicycle

s

Date Transaction Units Purch

ase

cost

Total

Purchase

cost

Sale

value

Closin

g units

value of

closing

inventory

43618 Purchase 100 50 =N4*O4 0 =N4 =P4-Q4

43622 Sale 10 0 0 =N5*10

0

=R4-

N5

=R5*O4

43638 Purchase 10 55 =N6*O6 0 =R5+

N6

=S5+P6

43644 Sale 15 0 0 =N7*10

0

=R6-

N7

=(75*O4)+(1

0*O6)

43646 closing

balance

=N4-

N5+N6-

N7

=SUM(P4

:P7)

=SUM(

Q4:Q7)

=S7

Total

purchases

=N4+N

6

Biclycles

sold or

returned

=N5+N

7

COGS =0+P8-

S8

Gross profit =Q8-

N11

ii)

Date Particulars Amoun

t (Dr)

Amount

(Cr)

01-Jun Bank A/c

To Capital

(Capital introduced in business)

30000

30000

02-Jun Purchases A/c

To Red bike rock ltd.

(Purchase of 100 small bicycles and 100 large

bicycles on credit)

10000

10000

04-Jun Delivery cost A/c

To Fast freight ltd

300

300

(Invoice received for delivery charges)

05-Jun Stall fees A/c

To Bank

(Cheque sent for the stall fees)

300

300

06-Jun Bank A/c

To sales

(Sale of 20 small and 10 large bicycles for

cash)

3000

3000

10-Jun Red bike rock ltd

To bank

To discount received

(Payment made to red bike rock ltd after

availing the discount)

10000

9800

200

13-Jun Local childcare center A/c

To sales

(Sale of 10 small bicycles on credit)

1000

1000

15-Jun Fast freight A/c

To bank

(cheque sent for invoice received earlier)

300

300

22-Jun Purchases A/c

To Red bike rock ltd.

(Purchase of 30 small bicycles and 10 large

bicycles on credit)

2200

2200

23-Jun Delivery cost A/c

To Fast freight ltd

(Invoice received for delivery charges)

180

180

24-Jun Red bike rock ltd A/c

To purchases

(Returned 20 small bicycles due to damages)

1100

1100

28-Jun Bank A/c 4000

05-Jun Stall fees A/c

To Bank

(Cheque sent for the stall fees)

300

300

06-Jun Bank A/c

To sales

(Sale of 20 small and 10 large bicycles for

cash)

3000

3000

10-Jun Red bike rock ltd

To bank

To discount received

(Payment made to red bike rock ltd after

availing the discount)

10000

9800

200

13-Jun Local childcare center A/c

To sales

(Sale of 10 small bicycles on credit)

1000

1000

15-Jun Fast freight A/c

To bank

(cheque sent for invoice received earlier)

300

300

22-Jun Purchases A/c

To Red bike rock ltd.

(Purchase of 30 small bicycles and 10 large

bicycles on credit)

2200

2200

23-Jun Delivery cost A/c

To Fast freight ltd

(Invoice received for delivery charges)

180

180

24-Jun Red bike rock ltd A/c

To purchases

(Returned 20 small bicycles due to damages)

1100

1100

28-Jun Bank A/c 4000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To sales

(Sale of 25 small and 15 large bicycles for

cash)

4000

iii)

Ledger posting

Purchase A/c

Date Particulars Amount Date Particulars Amount

02-Jun To Red bike rock ltd 10000 24-Jun by Red bike rock

ltd

1100

22-Jun To Red bike rock ltd 2200

30-Jun By closing balance 11100

12200 12200

Bank A/c

Date Particulars Amount Date Particulars Amount

01-Jun To capital 30000 05-Jun By stall fees 300

06-Jun To sales 3000 10-Jun By red bike rock ltd 9800

28-Jun To sales 4000 15-Jun By fast freight ltd 300

30-Jun By closing balance 26600

37000 37000

Capital

A/c

Date Particulars Amount Date Particulars Amount

01-Jun By bank 30000

30-Jun To closing balance 30000

30000 30000

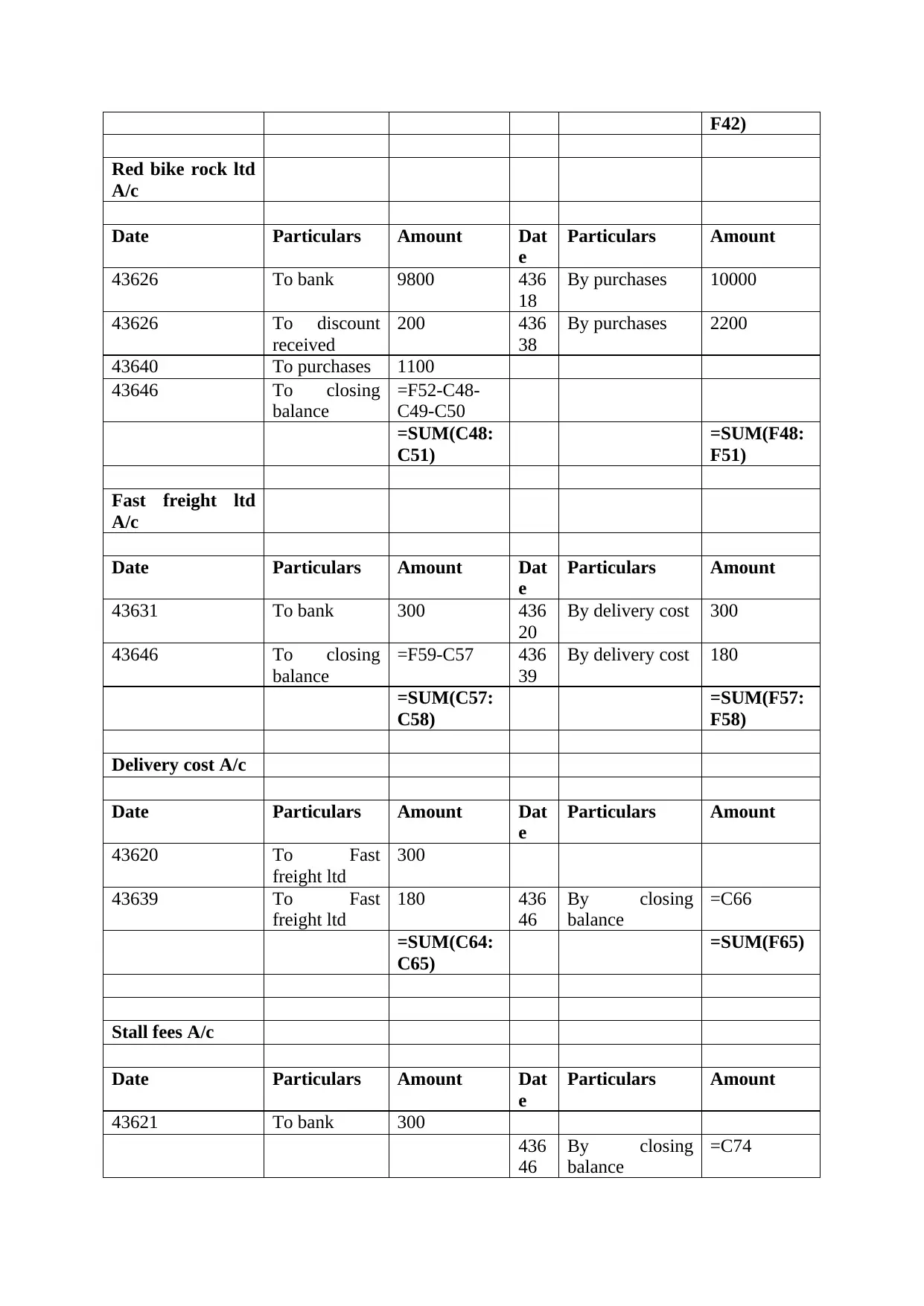

Red bike rock ltd A/c

Date Particulars Amount Date Particulars Amount

10-Jun To bank 9800 02-Jun By purchases 10000

10-Jun To discount received 200 22-Jun By purchases 2200

24-Jun To purchases 1100

30-Jun To closing balance 1100

(Sale of 25 small and 15 large bicycles for

cash)

4000

iii)

Ledger posting

Purchase A/c

Date Particulars Amount Date Particulars Amount

02-Jun To Red bike rock ltd 10000 24-Jun by Red bike rock

ltd

1100

22-Jun To Red bike rock ltd 2200

30-Jun By closing balance 11100

12200 12200

Bank A/c

Date Particulars Amount Date Particulars Amount

01-Jun To capital 30000 05-Jun By stall fees 300

06-Jun To sales 3000 10-Jun By red bike rock ltd 9800

28-Jun To sales 4000 15-Jun By fast freight ltd 300

30-Jun By closing balance 26600

37000 37000

Capital

A/c

Date Particulars Amount Date Particulars Amount

01-Jun By bank 30000

30-Jun To closing balance 30000

30000 30000

Red bike rock ltd A/c

Date Particulars Amount Date Particulars Amount

10-Jun To bank 9800 02-Jun By purchases 10000

10-Jun To discount received 200 22-Jun By purchases 2200

24-Jun To purchases 1100

30-Jun To closing balance 1100

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

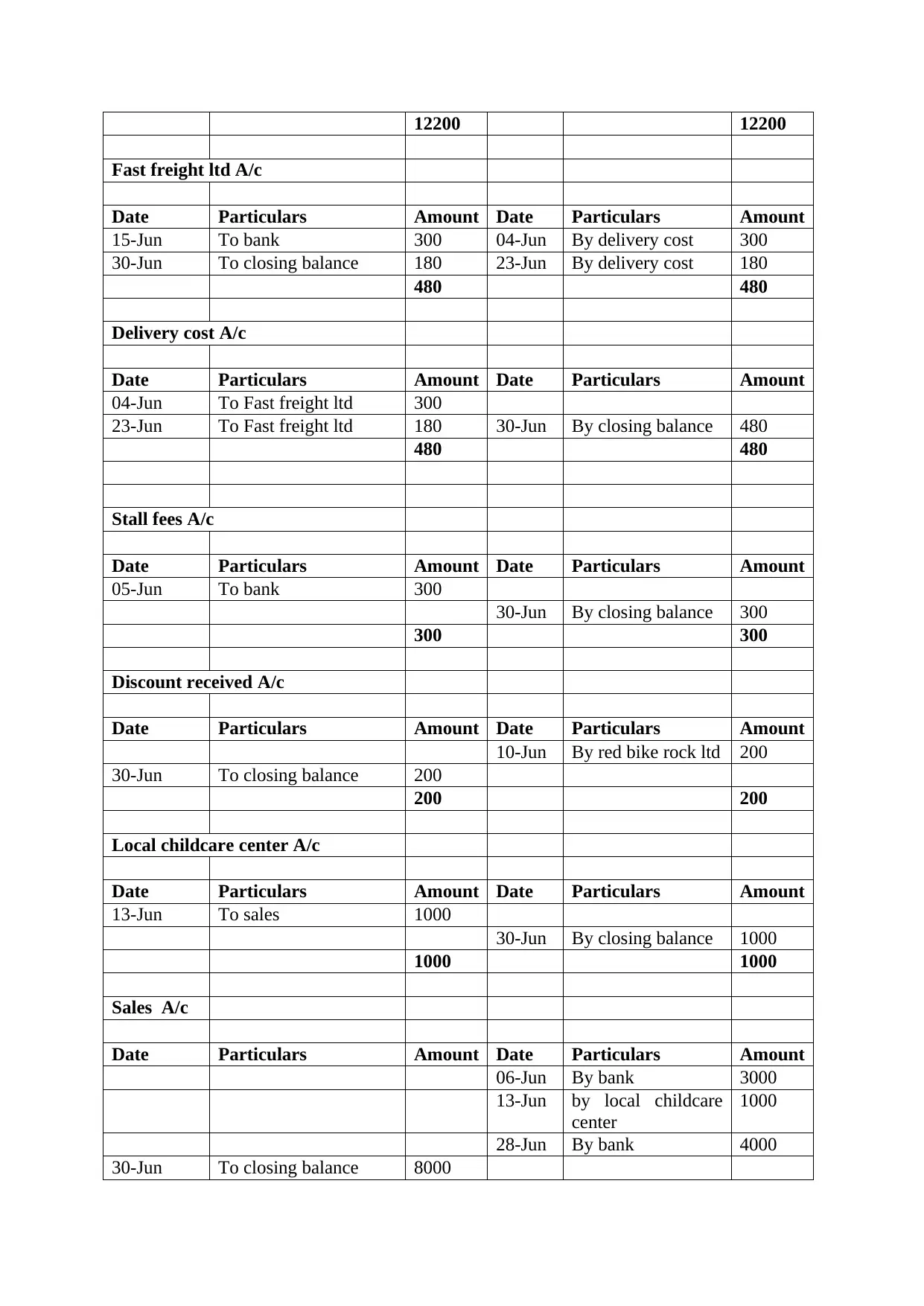

12200 12200

Fast freight ltd A/c

Date Particulars Amount Date Particulars Amount

15-Jun To bank 300 04-Jun By delivery cost 300

30-Jun To closing balance 180 23-Jun By delivery cost 180

480 480

Delivery cost A/c

Date Particulars Amount Date Particulars Amount

04-Jun To Fast freight ltd 300

23-Jun To Fast freight ltd 180 30-Jun By closing balance 480

480 480

Stall fees A/c

Date Particulars Amount Date Particulars Amount

05-Jun To bank 300

30-Jun By closing balance 300

300 300

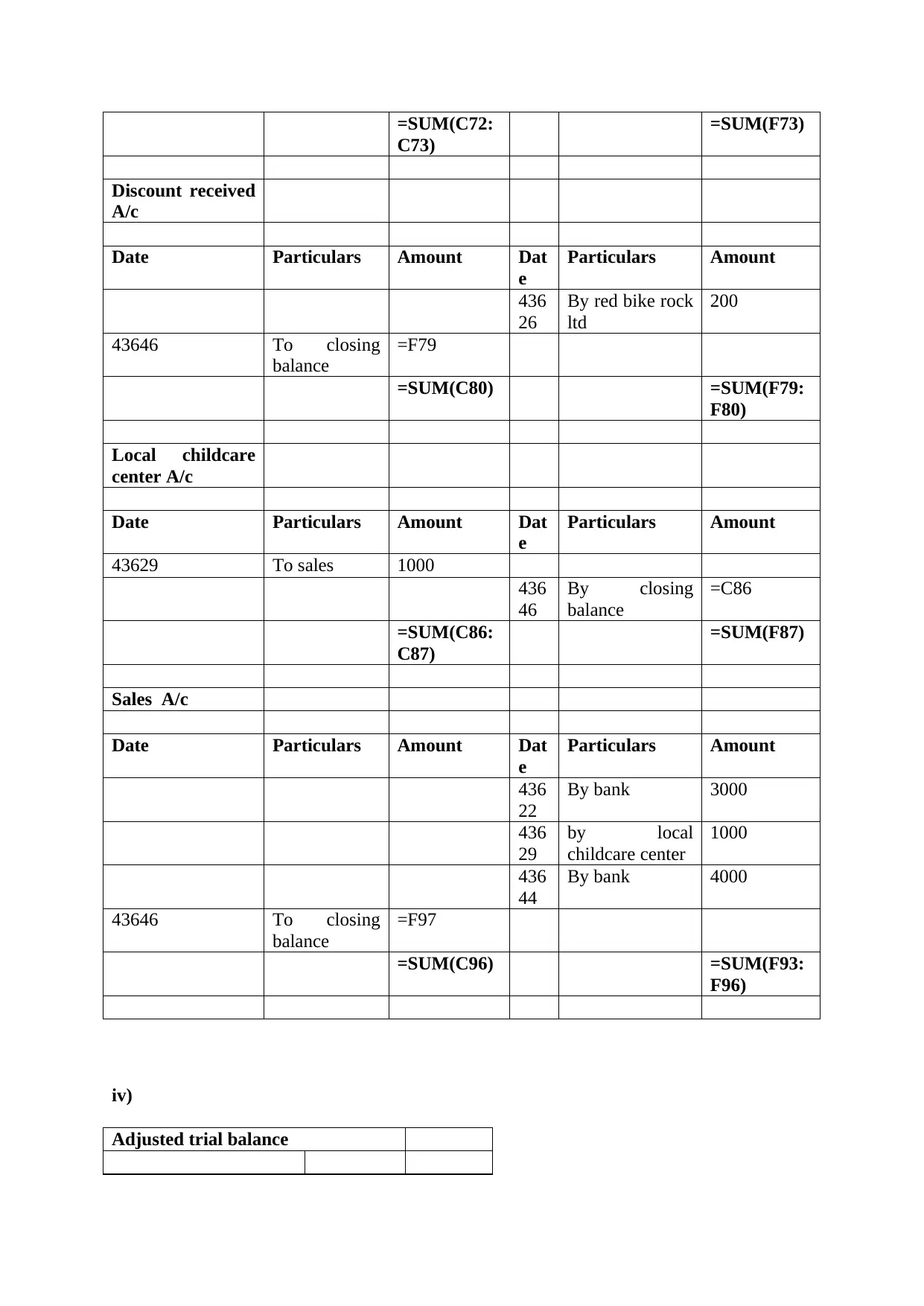

Discount received A/c

Date Particulars Amount Date Particulars Amount

10-Jun By red bike rock ltd 200

30-Jun To closing balance 200

200 200

Local childcare center A/c

Date Particulars Amount Date Particulars Amount

13-Jun To sales 1000

30-Jun By closing balance 1000

1000 1000

Sales A/c

Date Particulars Amount Date Particulars Amount

06-Jun By bank 3000

13-Jun by local childcare

center

1000

28-Jun By bank 4000

30-Jun To closing balance 8000

Fast freight ltd A/c

Date Particulars Amount Date Particulars Amount

15-Jun To bank 300 04-Jun By delivery cost 300

30-Jun To closing balance 180 23-Jun By delivery cost 180

480 480

Delivery cost A/c

Date Particulars Amount Date Particulars Amount

04-Jun To Fast freight ltd 300

23-Jun To Fast freight ltd 180 30-Jun By closing balance 480

480 480

Stall fees A/c

Date Particulars Amount Date Particulars Amount

05-Jun To bank 300

30-Jun By closing balance 300

300 300

Discount received A/c

Date Particulars Amount Date Particulars Amount

10-Jun By red bike rock ltd 200

30-Jun To closing balance 200

200 200

Local childcare center A/c

Date Particulars Amount Date Particulars Amount

13-Jun To sales 1000

30-Jun By closing balance 1000

1000 1000

Sales A/c

Date Particulars Amount Date Particulars Amount

06-Jun By bank 3000

13-Jun by local childcare

center

1000

28-Jun By bank 4000

30-Jun To closing balance 8000

8000 8000

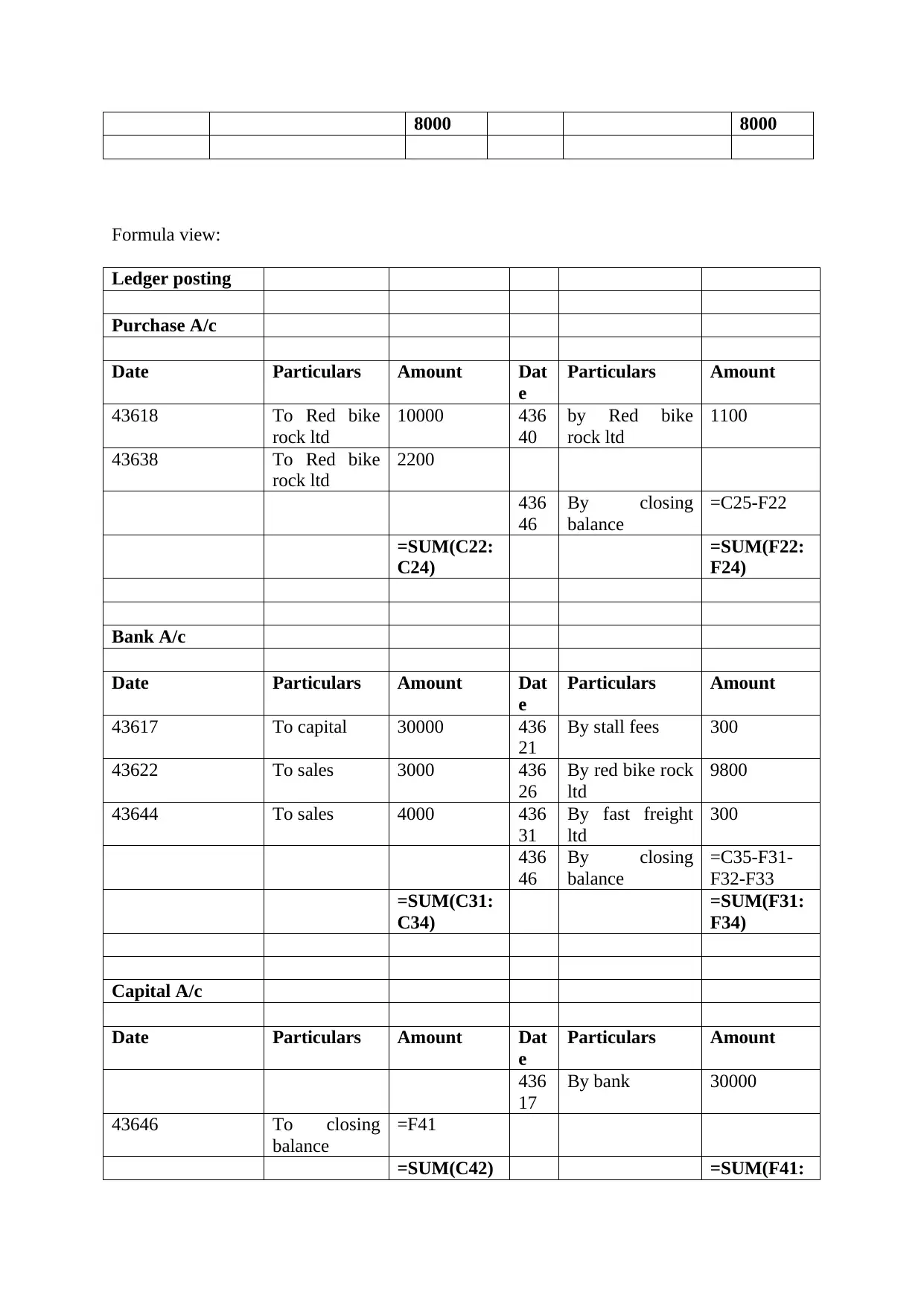

Formula view:

Ledger posting

Purchase A/c

Date Particulars Amount Dat

e

Particulars Amount

43618 To Red bike

rock ltd

10000 436

40

by Red bike

rock ltd

1100

43638 To Red bike

rock ltd

2200

436

46

By closing

balance

=C25-F22

=SUM(C22:

C24)

=SUM(F22:

F24)

Bank A/c

Date Particulars Amount Dat

e

Particulars Amount

43617 To capital 30000 436

21

By stall fees 300

43622 To sales 3000 436

26

By red bike rock

ltd

9800

43644 To sales 4000 436

31

By fast freight

ltd

300

436

46

By closing

balance

=C35-F31-

F32-F33

=SUM(C31:

C34)

=SUM(F31:

F34)

Capital A/c

Date Particulars Amount Dat

e

Particulars Amount

436

17

By bank 30000

43646 To closing

balance

=F41

=SUM(C42) =SUM(F41:

Formula view:

Ledger posting

Purchase A/c

Date Particulars Amount Dat

e

Particulars Amount

43618 To Red bike

rock ltd

10000 436

40

by Red bike

rock ltd

1100

43638 To Red bike

rock ltd

2200

436

46

By closing

balance

=C25-F22

=SUM(C22:

C24)

=SUM(F22:

F24)

Bank A/c

Date Particulars Amount Dat

e

Particulars Amount

43617 To capital 30000 436

21

By stall fees 300

43622 To sales 3000 436

26

By red bike rock

ltd

9800

43644 To sales 4000 436

31

By fast freight

ltd

300

436

46

By closing

balance

=C35-F31-

F32-F33

=SUM(C31:

C34)

=SUM(F31:

F34)

Capital A/c

Date Particulars Amount Dat

e

Particulars Amount

436

17

By bank 30000

43646 To closing

balance

=F41

=SUM(C42) =SUM(F41:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

F42)

Red bike rock ltd

A/c

Date Particulars Amount Dat

e

Particulars Amount

43626 To bank 9800 436

18

By purchases 10000

43626 To discount

received

200 436

38

By purchases 2200

43640 To purchases 1100

43646 To closing

balance

=F52-C48-

C49-C50

=SUM(C48:

C51)

=SUM(F48:

F51)

Fast freight ltd

A/c

Date Particulars Amount Dat

e

Particulars Amount

43631 To bank 300 436

20

By delivery cost 300

43646 To closing

balance

=F59-C57 436

39

By delivery cost 180

=SUM(C57:

C58)

=SUM(F57:

F58)

Delivery cost A/c

Date Particulars Amount Dat

e

Particulars Amount

43620 To Fast

freight ltd

300

43639 To Fast

freight ltd

180 436

46

By closing

balance

=C66

=SUM(C64:

C65)

=SUM(F65)

Stall fees A/c

Date Particulars Amount Dat

e

Particulars Amount

43621 To bank 300

436

46

By closing

balance

=C74

Red bike rock ltd

A/c

Date Particulars Amount Dat

e

Particulars Amount

43626 To bank 9800 436

18

By purchases 10000

43626 To discount

received

200 436

38

By purchases 2200

43640 To purchases 1100

43646 To closing

balance

=F52-C48-

C49-C50

=SUM(C48:

C51)

=SUM(F48:

F51)

Fast freight ltd

A/c

Date Particulars Amount Dat

e

Particulars Amount

43631 To bank 300 436

20

By delivery cost 300

43646 To closing

balance

=F59-C57 436

39

By delivery cost 180

=SUM(C57:

C58)

=SUM(F57:

F58)

Delivery cost A/c

Date Particulars Amount Dat

e

Particulars Amount

43620 To Fast

freight ltd

300

43639 To Fast

freight ltd

180 436

46

By closing

balance

=C66

=SUM(C64:

C65)

=SUM(F65)

Stall fees A/c

Date Particulars Amount Dat

e

Particulars Amount

43621 To bank 300

436

46

By closing

balance

=C74

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

=SUM(C72:

C73)

=SUM(F73)

Discount received

A/c

Date Particulars Amount Dat

e

Particulars Amount

436

26

By red bike rock

ltd

200

43646 To closing

balance

=F79

=SUM(C80) =SUM(F79:

F80)

Local childcare

center A/c

Date Particulars Amount Dat

e

Particulars Amount

43629 To sales 1000

436

46

By closing

balance

=C86

=SUM(C86:

C87)

=SUM(F87)

Sales A/c

Date Particulars Amount Dat

e

Particulars Amount

436

22

By bank 3000

436

29

by local

childcare center

1000

436

44

By bank 4000

43646 To closing

balance

=F97

=SUM(C96) =SUM(F93:

F96)

iv)

Adjusted trial balance

C73)

=SUM(F73)

Discount received

A/c

Date Particulars Amount Dat

e

Particulars Amount

436

26

By red bike rock

ltd

200

43646 To closing

balance

=F79

=SUM(C80) =SUM(F79:

F80)

Local childcare

center A/c

Date Particulars Amount Dat

e

Particulars Amount

43629 To sales 1000

436

46

By closing

balance

=C86

=SUM(C86:

C87)

=SUM(F87)

Sales A/c

Date Particulars Amount Dat

e

Particulars Amount

436

22

By bank 3000

436

29

by local

childcare center

1000

436

44

By bank 4000

43646 To closing

balance

=F97

=SUM(C96) =SUM(F93:

F96)

iv)

Adjusted trial balance

Particulars Amount

(Dr)

Amount

(Cr)

Purchase A/c 11100

Bank A/c 26600

Capital A/c 30000

Red bike rock ltd A/c 1100

Fast freight ltd A/c 180

Delivery cost A/c 480

Stall fees A/c 300

Discount received A/c 200

Local childcare centre

A/c

1000

Sales A/c 8000

Total 39480 39480

Formula view:

Adjusted trial balance

Particulars Amount (Dr) Amount (Cr)

Purchase A/c =F24

Bank A/c =F34

Capital A/c =C42

Red bike rock ltd A/c =C51

Fast freight ltd A/c =C58

Delivery cost A/c =F65

Stall fees A/c =F73

Discount received A/c =C80

Local childcare centre A/c =F87

Sales A/c =C96

Total =SUM(B103:B112

)

=SUM(C103:C112)

v)

Adjustment entry:

Closing stock A/c Dr. 7100

To Trading A/c 7100

(Dr)

Amount

(Cr)

Purchase A/c 11100

Bank A/c 26600

Capital A/c 30000

Red bike rock ltd A/c 1100

Fast freight ltd A/c 180

Delivery cost A/c 480

Stall fees A/c 300

Discount received A/c 200

Local childcare centre

A/c

1000

Sales A/c 8000

Total 39480 39480

Formula view:

Adjusted trial balance

Particulars Amount (Dr) Amount (Cr)

Purchase A/c =F24

Bank A/c =F34

Capital A/c =C42

Red bike rock ltd A/c =C51

Fast freight ltd A/c =C58

Delivery cost A/c =F65

Stall fees A/c =F73

Discount received A/c =C80

Local childcare centre A/c =F87

Sales A/c =C96

Total =SUM(B103:B112

)

=SUM(C103:C112)

v)

Adjustment entry:

Closing stock A/c Dr. 7100

To Trading A/c 7100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.