Project Evaluation: Pinto Limited Business Case Study - ACC00716

VerifiedAdded on 2023/04/23

|7

|1513

|465

Case Study

AI Summary

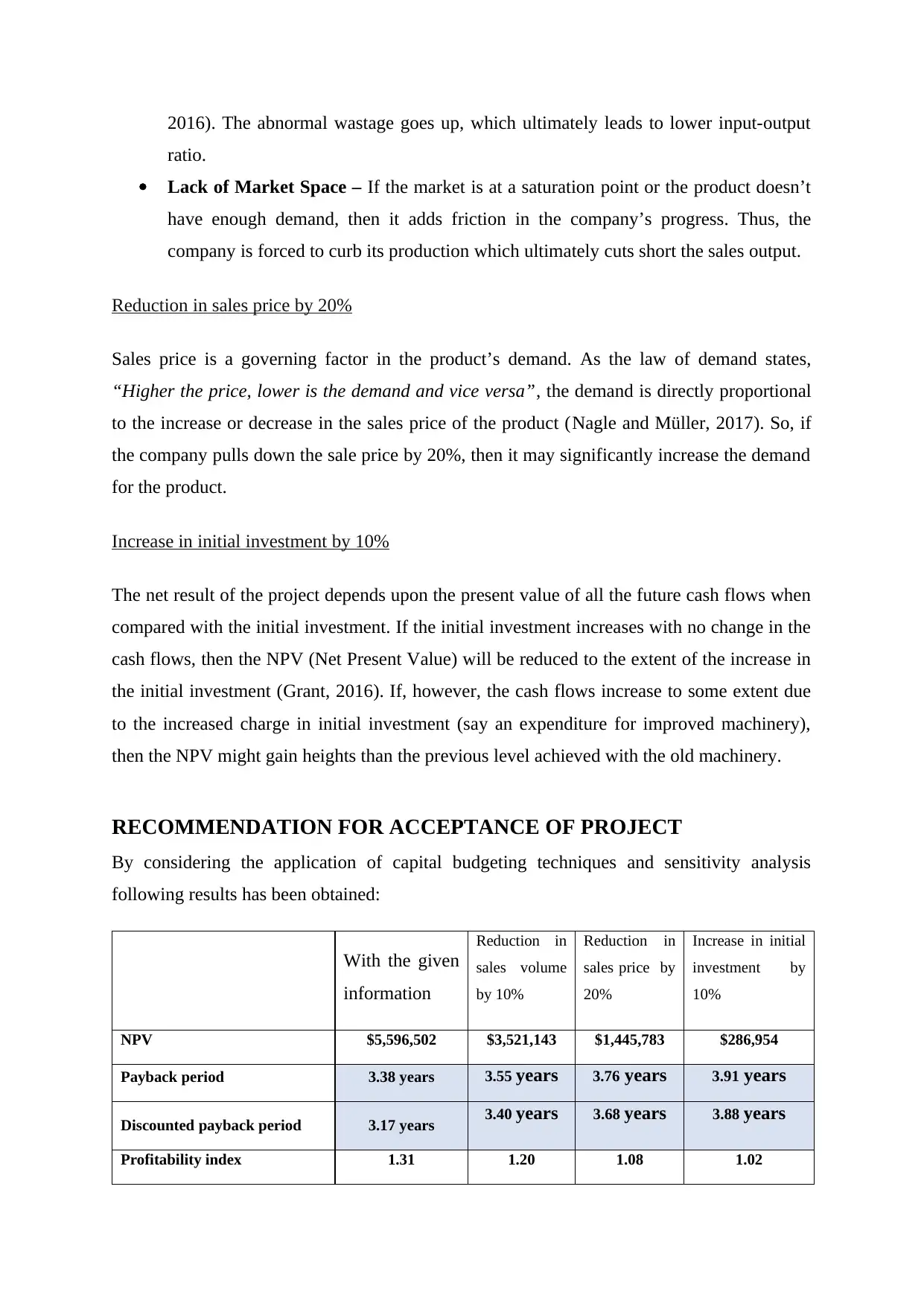

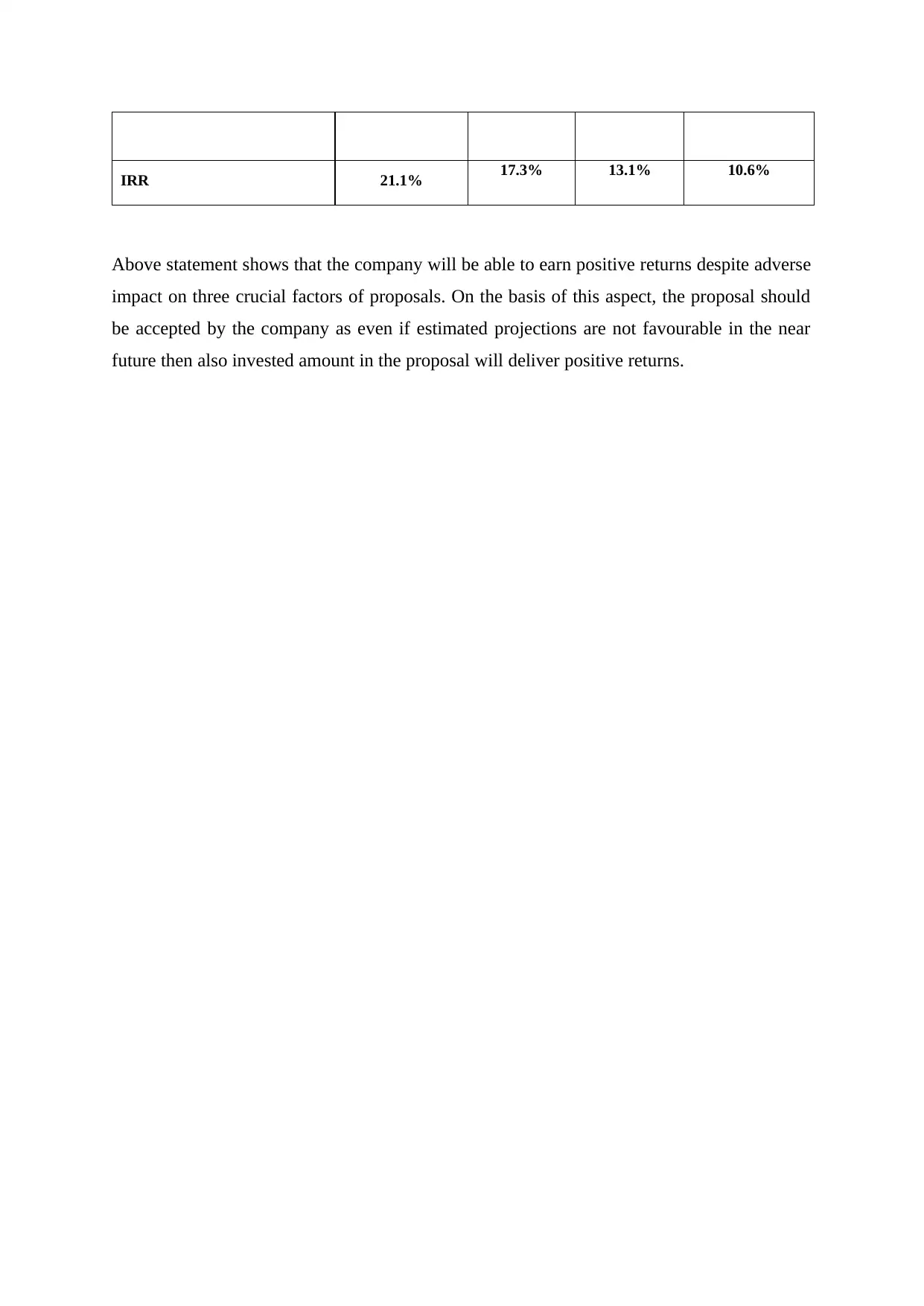

This assignment provides a comprehensive analysis of Pinto Limited's project using various project evaluation methods, including Net Present Value (NPV), Internal Rate of Return (IRR), Payback Period, Discounted Payback Period, and Profitability Index. The report assesses the project's risk by modeling three sensitivities: a reduction in sales volume by 10%, a reduction in sales price by 20%, and an increase in initial investment by 10%. Based on the analysis, the report recommends whether Pinto Limited should accept the project, considering the potential impact of these sensitivities on the project's financial viability. The document is contributed by a student and available on Desklib, a platform offering study tools and resources for students.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.