Analyzing Financial Statements & Ratios

VerifiedAdded on 2020/03/04

|5

|1619

|106

AI Summary

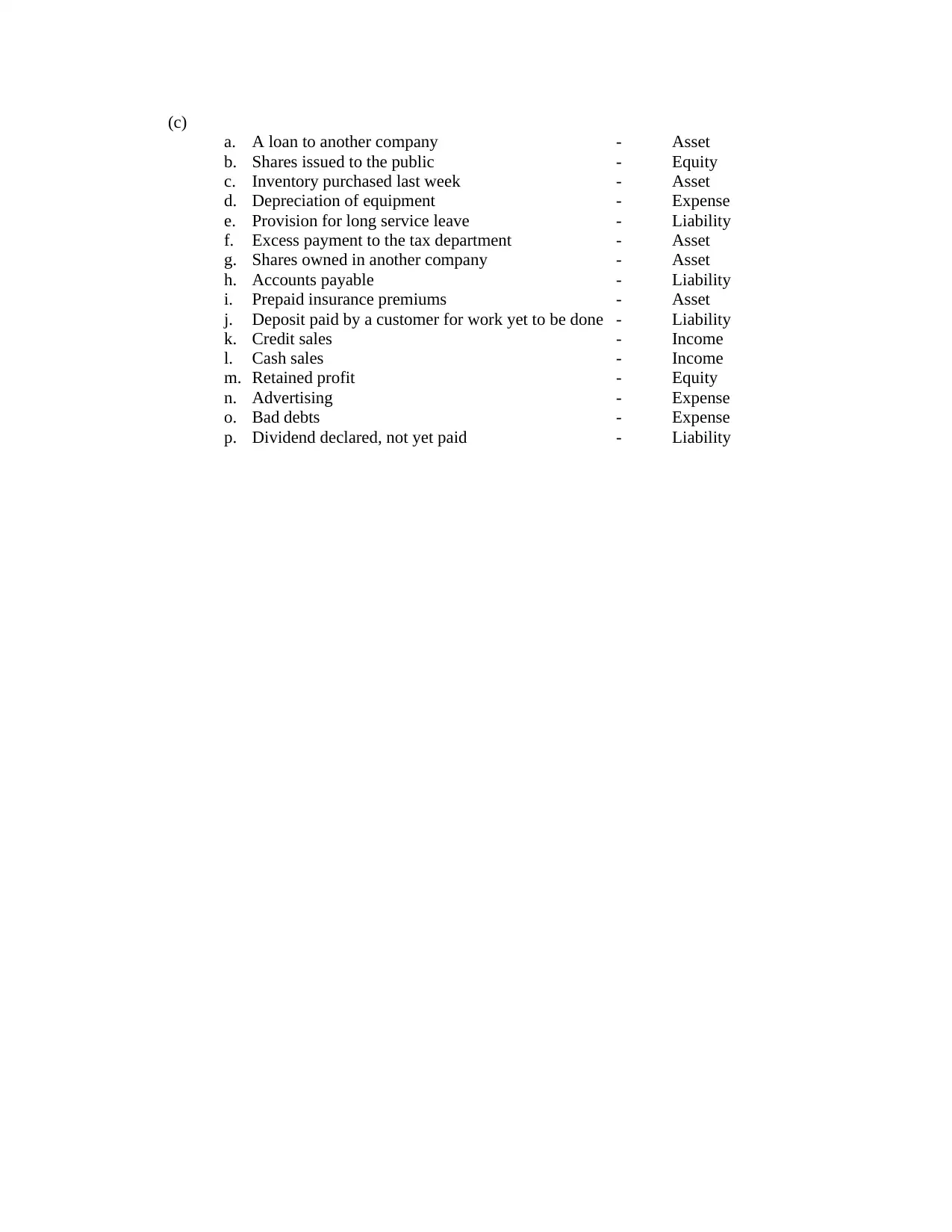

This assignment explores the concept of financial statement analysis by examining a company's performance through its dividend yield ratio and comparing it to industry averages. It also delves into the various users of financial statements, such as shareholders, lenders, and investors, highlighting their specific needs and information requirements. Furthermore, the assignment classifies different business transactions according to their impact on various accounting elements like assets, liabilities, equity, income, and expenses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.