Financial Statement Analysis: Company vs. Partnership

VerifiedAdded on 2020/03/16

|15

|2630

|35

AI Summary

This assignment delves into the comparison of financial statements between companies and partnerships. It examines the structure and content of balance sheets, income statements, and cash flow statements, highlighting the distinct features and requirements for each business entity. The analysis explores concepts such as equity, capital contributions, and mandatory reporting obligations, providing insights into how these factors shape financial reporting practices.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACC102 ACCOUNTING 1B

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Introduction......................................................................................................................................3

Part A: Analysis of the consolidated financial statements of JB Hi-Fi Limited..............................3

Analysis of increase or decrease in its current liabilities.................................................................3

Major liabilities of JB Hi-Fi Limited...............................................................................................4

Items included under ‘Provisions’ in the ‘Current Liabilities’........................................................5

Cash raised by interest-bearing loans..............................................................................................6

Secured Non-Current Liabilities......................................................................................................7

Amount of the non-current borrowings due to be repaid................................................................8

Non-Current Provisions...................................................................................................................9

Part B:..............................................................................................................................................9

Income Tax Expense......................................................................................................................10

Distribution of Profits....................................................................................................................11

Issued capital.................................................................................................................................12

Cash Flow Statements....................................................................................................................13

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

2

Introduction......................................................................................................................................3

Part A: Analysis of the consolidated financial statements of JB Hi-Fi Limited..............................3

Analysis of increase or decrease in its current liabilities.................................................................3

Major liabilities of JB Hi-Fi Limited...............................................................................................4

Items included under ‘Provisions’ in the ‘Current Liabilities’........................................................5

Cash raised by interest-bearing loans..............................................................................................6

Secured Non-Current Liabilities......................................................................................................7

Amount of the non-current borrowings due to be repaid................................................................8

Non-Current Provisions...................................................................................................................9

Part B:..............................................................................................................................................9

Income Tax Expense......................................................................................................................10

Distribution of Profits....................................................................................................................11

Issued capital.................................................................................................................................12

Cash Flow Statements....................................................................................................................13

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

2

Introduction

The present report aims to present an analysis of the various financial elements present in

the consolidated financial statements of two ASX listed company. The business companies

selected for the purpose are JB Hi-Fi Limited and Country Road Limited.

Part A: Analysis of the consolidated financial statements of JB Hi-Fi Limited

Analysis of increase or decrease in its current liabilities

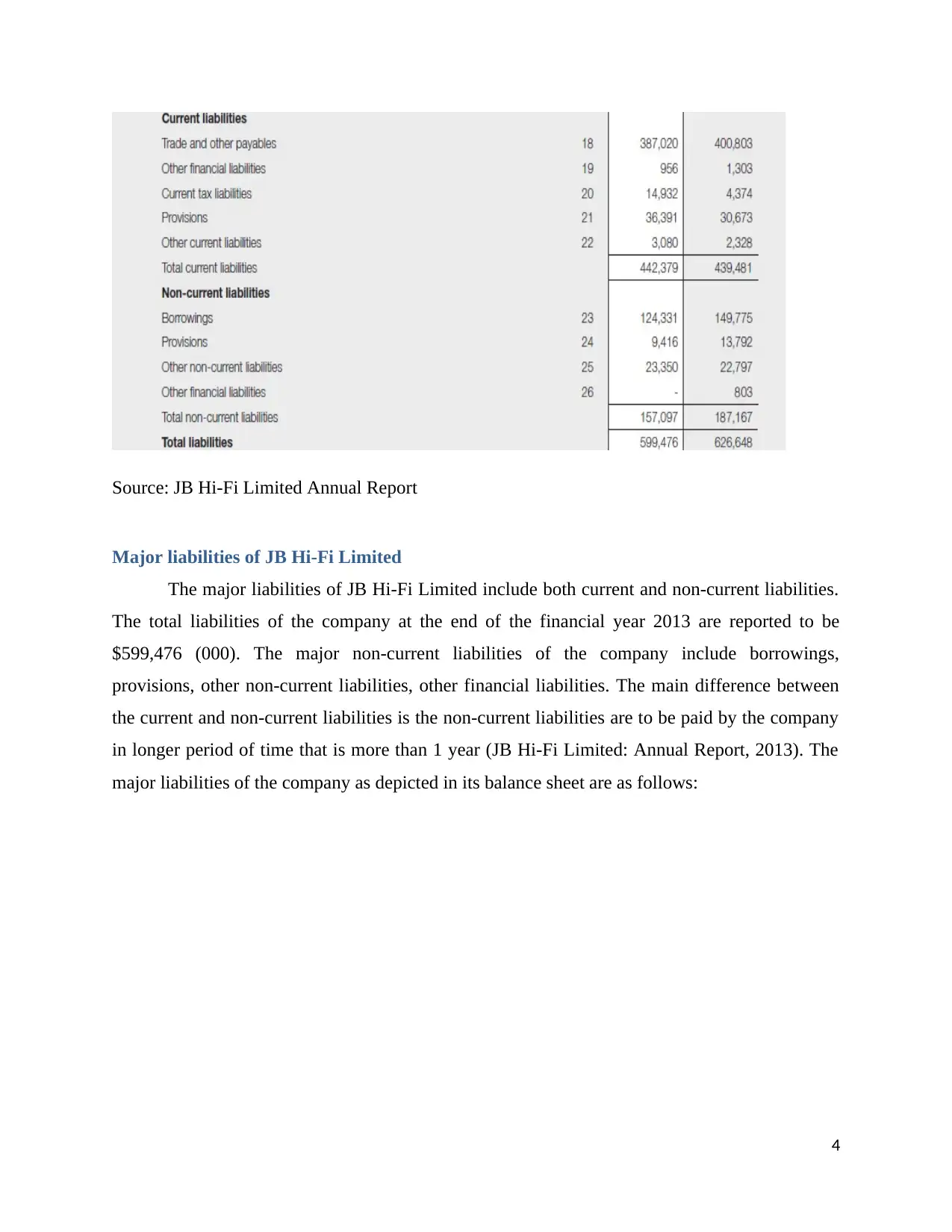

The current liabilities refer to the debt obligations of a business entity that is liable to be

paid within a year and is stated in the balance sheet. The current liabilities of the company are

short-term debt, accounts payable, accrued liabilities and other financial obligations that must be

paid within short-period of time (Epstein and Jermakowicz, 2010). The JB Hi-Fi Limited is a

recognized retailer of Australia involved in providing variety of products to the people of the

country such as consumer goods, video games, DVDs, CDs, home appliances and others. The

current liabilities as reported in the balance sheet of the company are trade and other payable,

other financial liabilities, current tax liabilities, provisions and other current liabilities. The

current tax liabilities include income tax and provision includes employee benefits and lease

provision. The other financial liabilities includes interest rate swap while the other current

liabilities include lease accrual and incentives. The current liabilities of the company have

increased significantly in the year 2013 of amount $442,379 as compared to year 2012 of

$439,481 (JB Hi-Fi Limited: Annual Report, 2013).

3

The present report aims to present an analysis of the various financial elements present in

the consolidated financial statements of two ASX listed company. The business companies

selected for the purpose are JB Hi-Fi Limited and Country Road Limited.

Part A: Analysis of the consolidated financial statements of JB Hi-Fi Limited

Analysis of increase or decrease in its current liabilities

The current liabilities refer to the debt obligations of a business entity that is liable to be

paid within a year and is stated in the balance sheet. The current liabilities of the company are

short-term debt, accounts payable, accrued liabilities and other financial obligations that must be

paid within short-period of time (Epstein and Jermakowicz, 2010). The JB Hi-Fi Limited is a

recognized retailer of Australia involved in providing variety of products to the people of the

country such as consumer goods, video games, DVDs, CDs, home appliances and others. The

current liabilities as reported in the balance sheet of the company are trade and other payable,

other financial liabilities, current tax liabilities, provisions and other current liabilities. The

current tax liabilities include income tax and provision includes employee benefits and lease

provision. The other financial liabilities includes interest rate swap while the other current

liabilities include lease accrual and incentives. The current liabilities of the company have

increased significantly in the year 2013 of amount $442,379 as compared to year 2012 of

$439,481 (JB Hi-Fi Limited: Annual Report, 2013).

3

Source: JB Hi-Fi Limited Annual Report

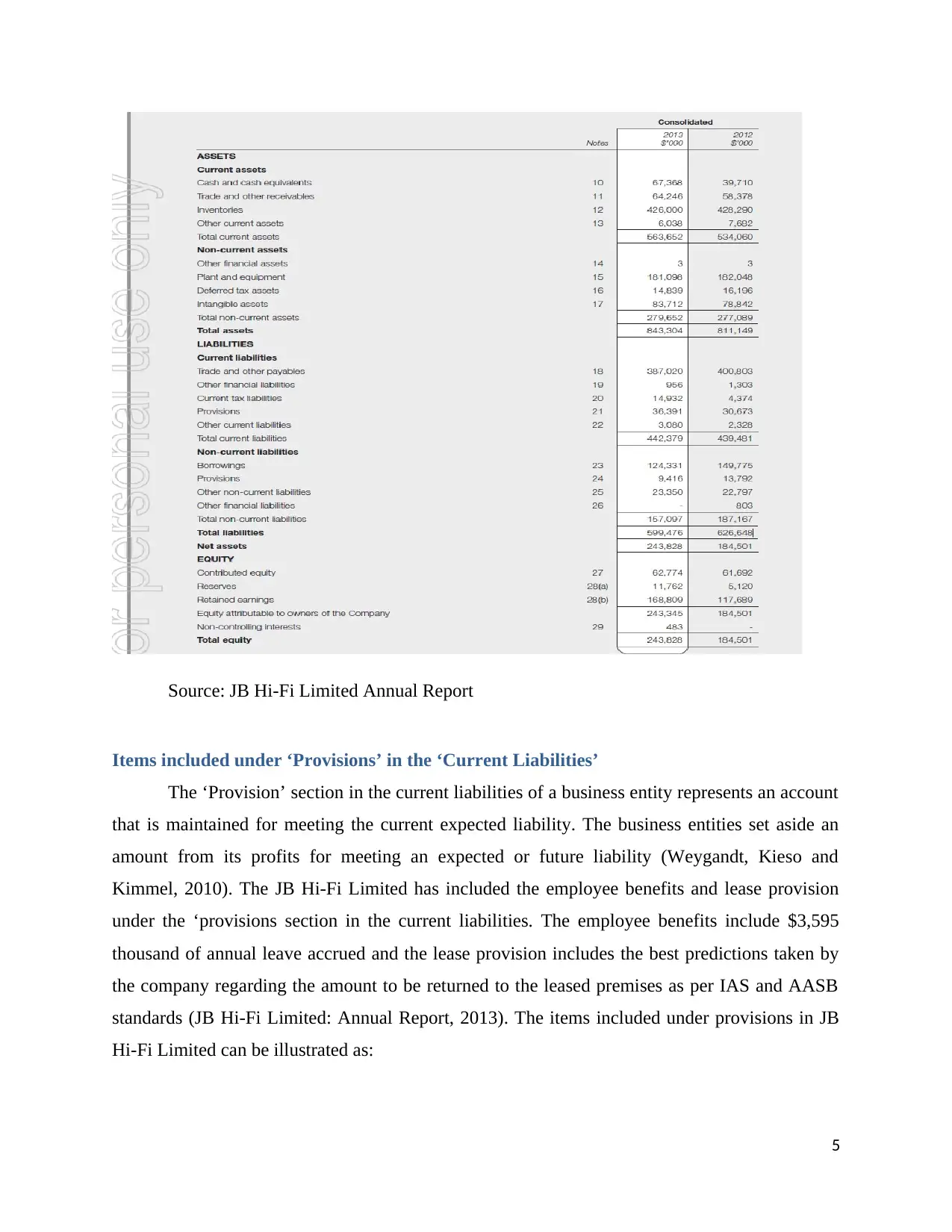

Major liabilities of JB Hi-Fi Limited

The major liabilities of JB Hi-Fi Limited include both current and non-current liabilities.

The total liabilities of the company at the end of the financial year 2013 are reported to be

$599,476 (000). The major non-current liabilities of the company include borrowings,

provisions, other non-current liabilities, other financial liabilities. The main difference between

the current and non-current liabilities is the non-current liabilities are to be paid by the company

in longer period of time that is more than 1 year (JB Hi-Fi Limited: Annual Report, 2013). The

major liabilities of the company as depicted in its balance sheet are as follows:

4

Major liabilities of JB Hi-Fi Limited

The major liabilities of JB Hi-Fi Limited include both current and non-current liabilities.

The total liabilities of the company at the end of the financial year 2013 are reported to be

$599,476 (000). The major non-current liabilities of the company include borrowings,

provisions, other non-current liabilities, other financial liabilities. The main difference between

the current and non-current liabilities is the non-current liabilities are to be paid by the company

in longer period of time that is more than 1 year (JB Hi-Fi Limited: Annual Report, 2013). The

major liabilities of the company as depicted in its balance sheet are as follows:

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Source: JB Hi-Fi Limited Annual Report

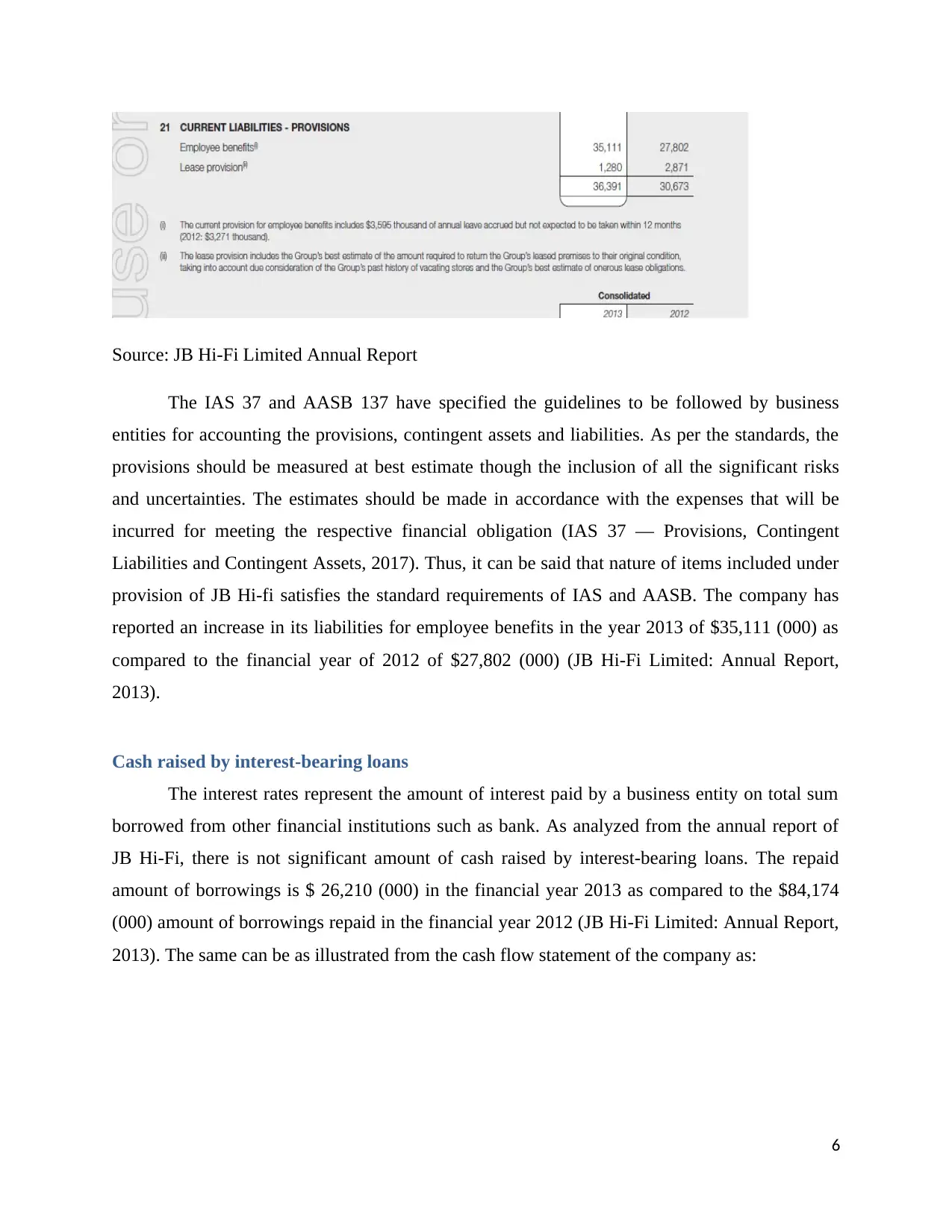

Items included under ‘Provisions’ in the ‘Current Liabilities’

The ‘Provision’ section in the current liabilities of a business entity represents an account

that is maintained for meeting the current expected liability. The business entities set aside an

amount from its profits for meeting an expected or future liability (Weygandt, Kieso and

Kimmel, 2010). The JB Hi-Fi Limited has included the employee benefits and lease provision

under the ‘provisions section in the current liabilities. The employee benefits include $3,595

thousand of annual leave accrued and the lease provision includes the best predictions taken by

the company regarding the amount to be returned to the leased premises as per IAS and AASB

standards (JB Hi-Fi Limited: Annual Report, 2013). The items included under provisions in JB

Hi-Fi Limited can be illustrated as:

5

Items included under ‘Provisions’ in the ‘Current Liabilities’

The ‘Provision’ section in the current liabilities of a business entity represents an account

that is maintained for meeting the current expected liability. The business entities set aside an

amount from its profits for meeting an expected or future liability (Weygandt, Kieso and

Kimmel, 2010). The JB Hi-Fi Limited has included the employee benefits and lease provision

under the ‘provisions section in the current liabilities. The employee benefits include $3,595

thousand of annual leave accrued and the lease provision includes the best predictions taken by

the company regarding the amount to be returned to the leased premises as per IAS and AASB

standards (JB Hi-Fi Limited: Annual Report, 2013). The items included under provisions in JB

Hi-Fi Limited can be illustrated as:

5

Source: JB Hi-Fi Limited Annual Report

The IAS 37 and AASB 137 have specified the guidelines to be followed by business

entities for accounting the provisions, contingent assets and liabilities. As per the standards, the

provisions should be measured at best estimate though the inclusion of all the significant risks

and uncertainties. The estimates should be made in accordance with the expenses that will be

incurred for meeting the respective financial obligation (IAS 37 — Provisions, Contingent

Liabilities and Contingent Assets, 2017). Thus, it can be said that nature of items included under

provision of JB Hi-fi satisfies the standard requirements of IAS and AASB. The company has

reported an increase in its liabilities for employee benefits in the year 2013 of $35,111 (000) as

compared to the financial year of 2012 of $27,802 (000) (JB Hi-Fi Limited: Annual Report,

2013).

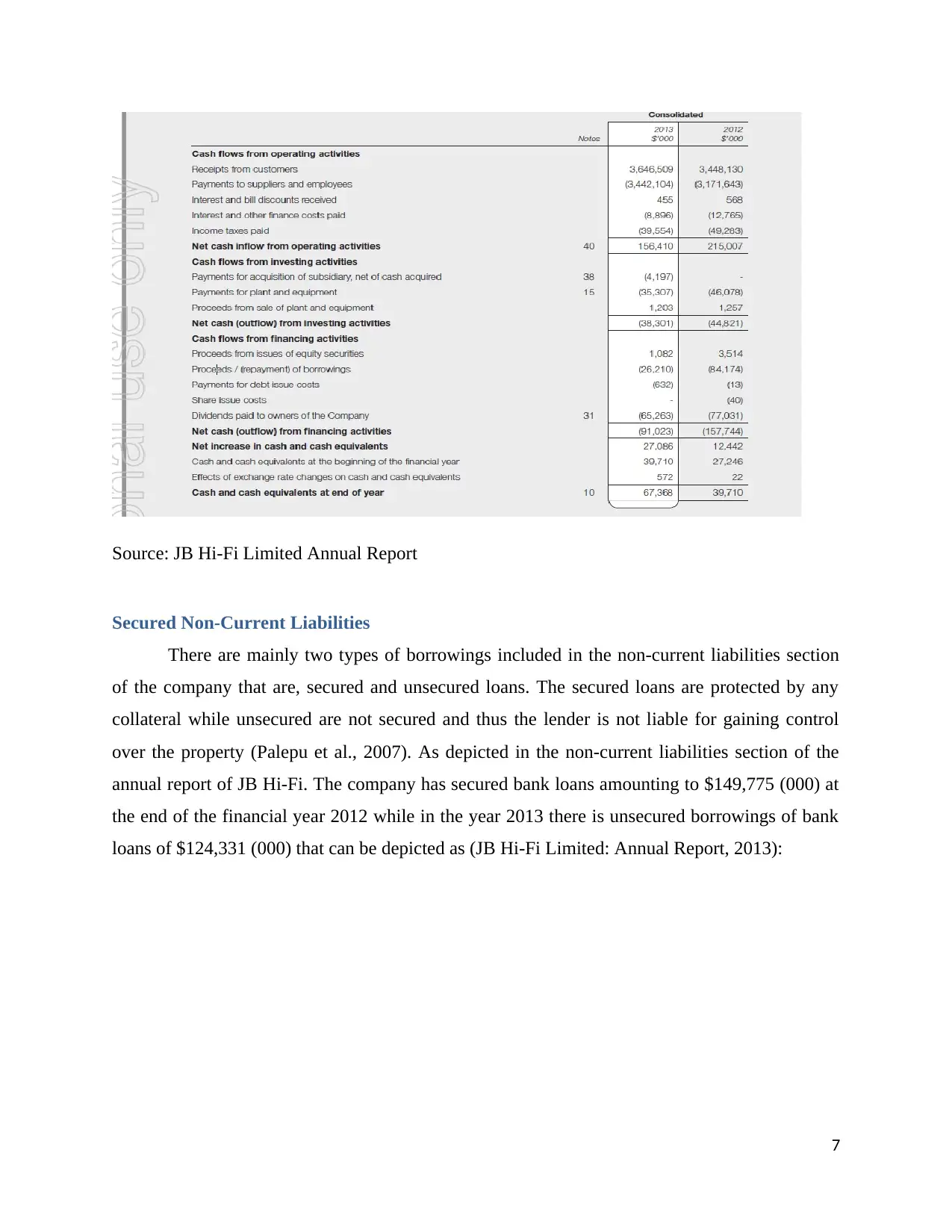

Cash raised by interest-bearing loans

The interest rates represent the amount of interest paid by a business entity on total sum

borrowed from other financial institutions such as bank. As analyzed from the annual report of

JB Hi-Fi, there is not significant amount of cash raised by interest-bearing loans. The repaid

amount of borrowings is $ 26,210 (000) in the financial year 2013 as compared to the $84,174

(000) amount of borrowings repaid in the financial year 2012 (JB Hi-Fi Limited: Annual Report,

2013). The same can be as illustrated from the cash flow statement of the company as:

6

The IAS 37 and AASB 137 have specified the guidelines to be followed by business

entities for accounting the provisions, contingent assets and liabilities. As per the standards, the

provisions should be measured at best estimate though the inclusion of all the significant risks

and uncertainties. The estimates should be made in accordance with the expenses that will be

incurred for meeting the respective financial obligation (IAS 37 — Provisions, Contingent

Liabilities and Contingent Assets, 2017). Thus, it can be said that nature of items included under

provision of JB Hi-fi satisfies the standard requirements of IAS and AASB. The company has

reported an increase in its liabilities for employee benefits in the year 2013 of $35,111 (000) as

compared to the financial year of 2012 of $27,802 (000) (JB Hi-Fi Limited: Annual Report,

2013).

Cash raised by interest-bearing loans

The interest rates represent the amount of interest paid by a business entity on total sum

borrowed from other financial institutions such as bank. As analyzed from the annual report of

JB Hi-Fi, there is not significant amount of cash raised by interest-bearing loans. The repaid

amount of borrowings is $ 26,210 (000) in the financial year 2013 as compared to the $84,174

(000) amount of borrowings repaid in the financial year 2012 (JB Hi-Fi Limited: Annual Report,

2013). The same can be as illustrated from the cash flow statement of the company as:

6

Source: JB Hi-Fi Limited Annual Report

Secured Non-Current Liabilities

There are mainly two types of borrowings included in the non-current liabilities section

of the company that are, secured and unsecured loans. The secured loans are protected by any

collateral while unsecured are not secured and thus the lender is not liable for gaining control

over the property (Palepu et al., 2007). As depicted in the non-current liabilities section of the

annual report of JB Hi-Fi. The company has secured bank loans amounting to $149,775 (000) at

the end of the financial year 2012 while in the year 2013 there is unsecured borrowings of bank

loans of $124,331 (000) that can be depicted as (JB Hi-Fi Limited: Annual Report, 2013):

7

Secured Non-Current Liabilities

There are mainly two types of borrowings included in the non-current liabilities section

of the company that are, secured and unsecured loans. The secured loans are protected by any

collateral while unsecured are not secured and thus the lender is not liable for gaining control

over the property (Palepu et al., 2007). As depicted in the non-current liabilities section of the

annual report of JB Hi-Fi. The company has secured bank loans amounting to $149,775 (000) at

the end of the financial year 2012 while in the year 2013 there is unsecured borrowings of bank

loans of $124,331 (000) that can be depicted as (JB Hi-Fi Limited: Annual Report, 2013):

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Source: JB Hi-Fi Limited Annual Report

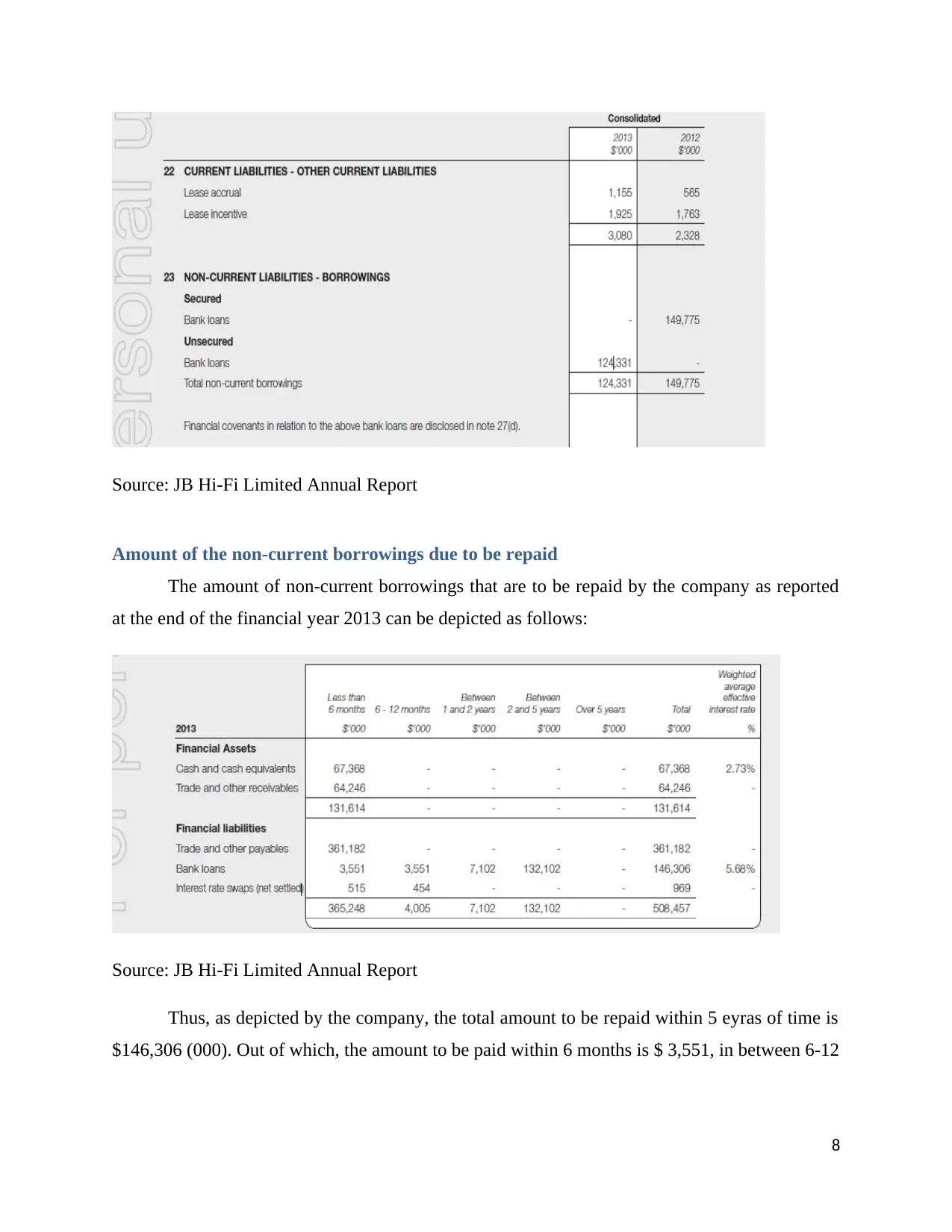

Amount of the non-current borrowings due to be repaid

The amount of non-current borrowings that are to be repaid by the company as reported

at the end of the financial year 2013 can be depicted as follows:

Source: JB Hi-Fi Limited Annual Report

Thus, as depicted by the company, the total amount to be repaid within 5 eyras of time is

$146,306 (000). Out of which, the amount to be paid within 6 months is $ 3,551, in between 6-12

8

Amount of the non-current borrowings due to be repaid

The amount of non-current borrowings that are to be repaid by the company as reported

at the end of the financial year 2013 can be depicted as follows:

Source: JB Hi-Fi Limited Annual Report

Thus, as depicted by the company, the total amount to be repaid within 5 eyras of time is

$146,306 (000). Out of which, the amount to be paid within 6 months is $ 3,551, in between 6-12

8

months is $3,551 and that to be given under 1-2 years is $7,102. The amount that is repaid

between 2-5 years is $132,102 (JB Hi-Fi Limited: Annual Report, 2013).

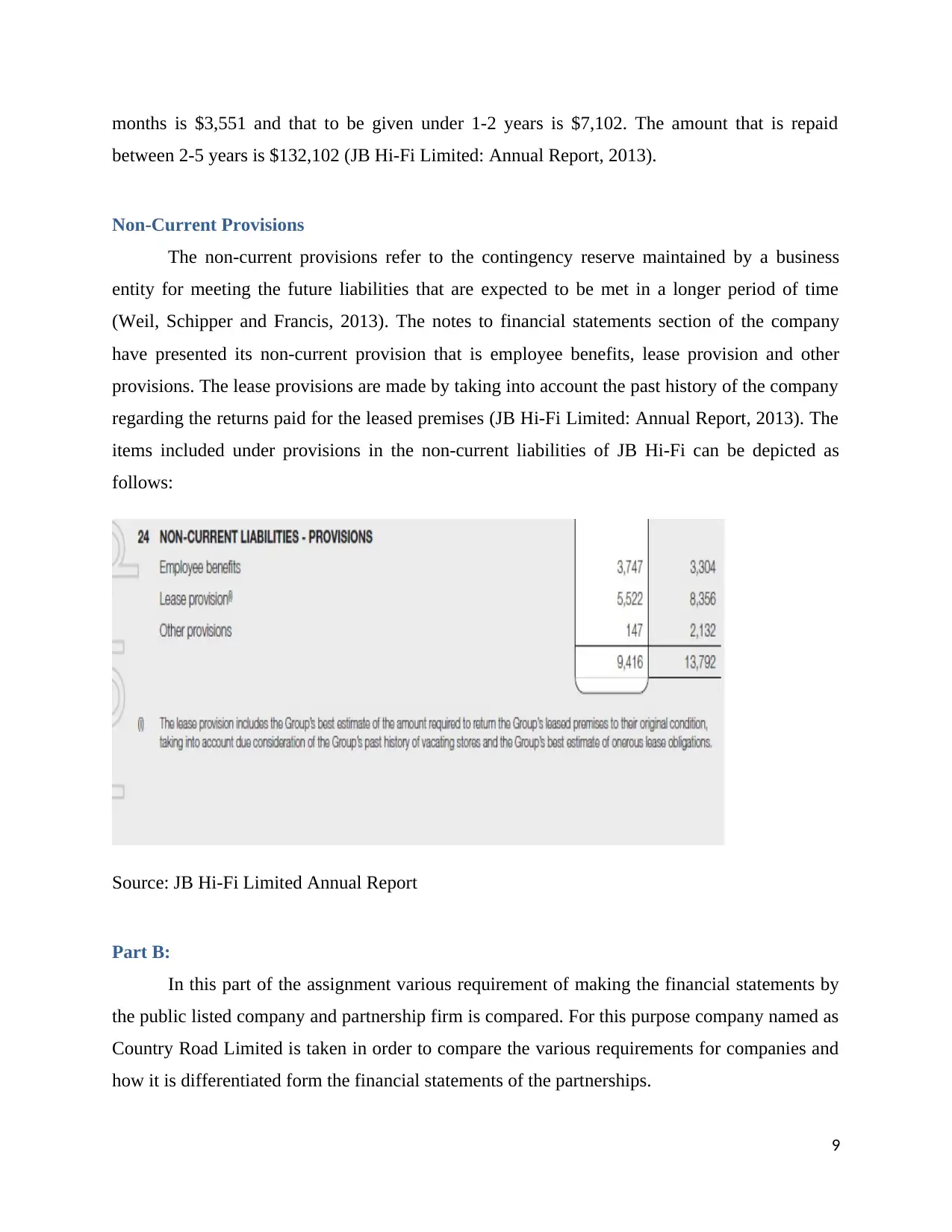

Non-Current Provisions

The non-current provisions refer to the contingency reserve maintained by a business

entity for meeting the future liabilities that are expected to be met in a longer period of time

(Weil, Schipper and Francis, 2013). The notes to financial statements section of the company

have presented its non-current provision that is employee benefits, lease provision and other

provisions. The lease provisions are made by taking into account the past history of the company

regarding the returns paid for the leased premises (JB Hi-Fi Limited: Annual Report, 2013). The

items included under provisions in the non-current liabilities of JB Hi-Fi can be depicted as

follows:

Source: JB Hi-Fi Limited Annual Report

Part B:

In this part of the assignment various requirement of making the financial statements by

the public listed company and partnership firm is compared. For this purpose company named as

Country Road Limited is taken in order to compare the various requirements for companies and

how it is differentiated form the financial statements of the partnerships.

9

between 2-5 years is $132,102 (JB Hi-Fi Limited: Annual Report, 2013).

Non-Current Provisions

The non-current provisions refer to the contingency reserve maintained by a business

entity for meeting the future liabilities that are expected to be met in a longer period of time

(Weil, Schipper and Francis, 2013). The notes to financial statements section of the company

have presented its non-current provision that is employee benefits, lease provision and other

provisions. The lease provisions are made by taking into account the past history of the company

regarding the returns paid for the leased premises (JB Hi-Fi Limited: Annual Report, 2013). The

items included under provisions in the non-current liabilities of JB Hi-Fi can be depicted as

follows:

Source: JB Hi-Fi Limited Annual Report

Part B:

In this part of the assignment various requirement of making the financial statements by

the public listed company and partnership firm is compared. For this purpose company named as

Country Road Limited is taken in order to compare the various requirements for companies and

how it is differentiated form the financial statements of the partnerships.

9

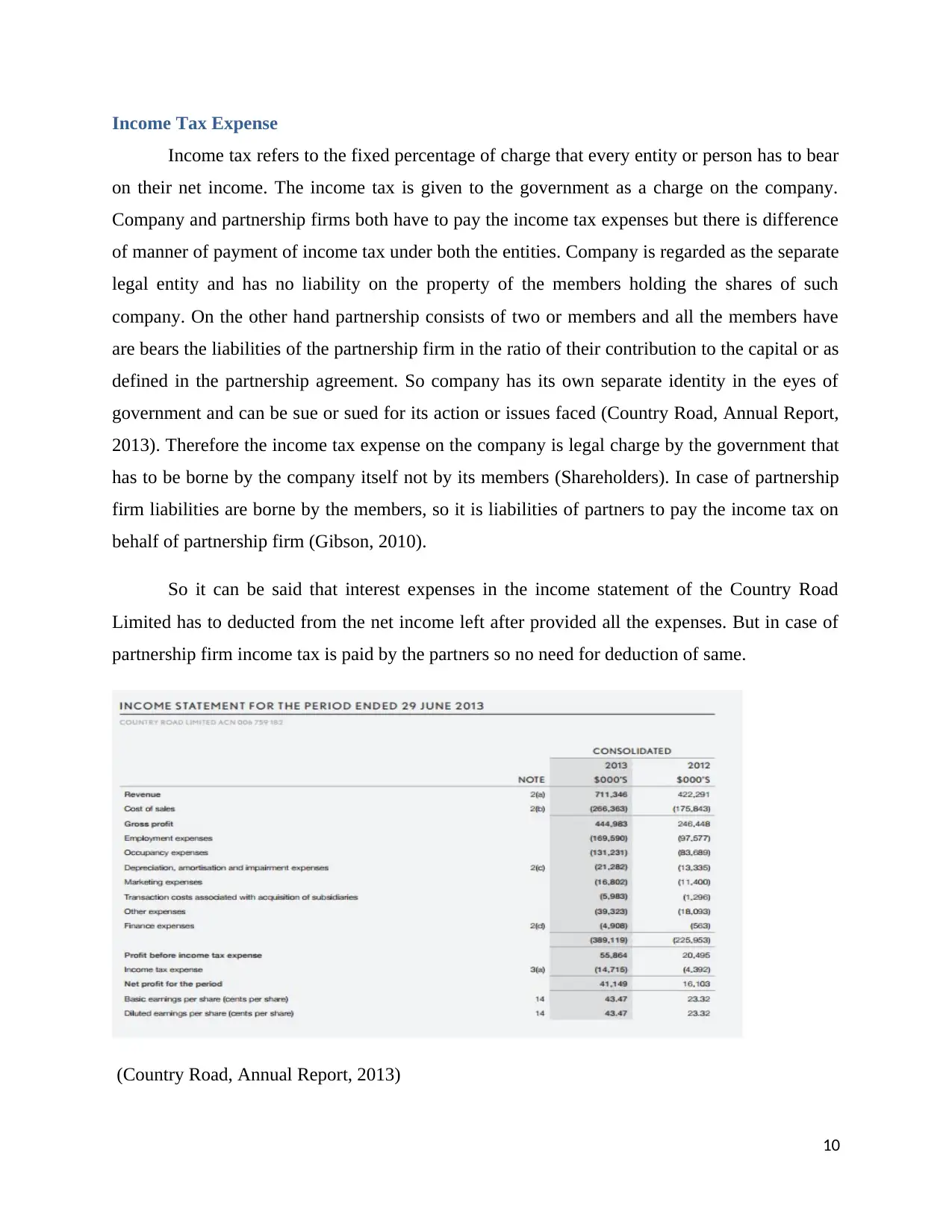

Income Tax Expense

Income tax refers to the fixed percentage of charge that every entity or person has to bear

on their net income. The income tax is given to the government as a charge on the company.

Company and partnership firms both have to pay the income tax expenses but there is difference

of manner of payment of income tax under both the entities. Company is regarded as the separate

legal entity and has no liability on the property of the members holding the shares of such

company. On the other hand partnership consists of two or members and all the members have

are bears the liabilities of the partnership firm in the ratio of their contribution to the capital or as

defined in the partnership agreement. So company has its own separate identity in the eyes of

government and can be sue or sued for its action or issues faced (Country Road, Annual Report,

2013). Therefore the income tax expense on the company is legal charge by the government that

has to be borne by the company itself not by its members (Shareholders). In case of partnership

firm liabilities are borne by the members, so it is liabilities of partners to pay the income tax on

behalf of partnership firm (Gibson, 2010).

So it can be said that interest expenses in the income statement of the Country Road

Limited has to deducted from the net income left after provided all the expenses. But in case of

partnership firm income tax is paid by the partners so no need for deduction of same.

(Country Road, Annual Report, 2013)

10

Income tax refers to the fixed percentage of charge that every entity or person has to bear

on their net income. The income tax is given to the government as a charge on the company.

Company and partnership firms both have to pay the income tax expenses but there is difference

of manner of payment of income tax under both the entities. Company is regarded as the separate

legal entity and has no liability on the property of the members holding the shares of such

company. On the other hand partnership consists of two or members and all the members have

are bears the liabilities of the partnership firm in the ratio of their contribution to the capital or as

defined in the partnership agreement. So company has its own separate identity in the eyes of

government and can be sue or sued for its action or issues faced (Country Road, Annual Report,

2013). Therefore the income tax expense on the company is legal charge by the government that

has to be borne by the company itself not by its members (Shareholders). In case of partnership

firm liabilities are borne by the members, so it is liabilities of partners to pay the income tax on

behalf of partnership firm (Gibson, 2010).

So it can be said that interest expenses in the income statement of the Country Road

Limited has to deducted from the net income left after provided all the expenses. But in case of

partnership firm income tax is paid by the partners so no need for deduction of same.

(Country Road, Annual Report, 2013)

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Distribution of Profits

Profits remained after deducting all the expenses and tax liability has to either transferred

to the retained earnings or has to be distributed to the members (Shareholders) of the respective

entity. In case of companies profits are derived after deducting the expenses are transferred to the

equity capital in form of retained earnings and it is subject to distribution in case dividends are

declared by the company. Dividend refers to distribution of profits earned by the company to

their respective shareholders as per the number of shares hold by them. In statement of change in

equity various balance such as retained earnings, equity share capital, etc are recorded and any

change to them is also provided so to make the changes in amount of leftover retained earnings

with the company. The total profit available is appropriated in total number of shares subscribed

by the shareholders of the company. Profits are divided into two main parts one is retained

earnings and current year dividends (Country Road, Annual Report, 2013). Retained earnings is

leftover of profits remained after distribution of dividends. In case of partnership firms profits of

company are distributed to the respective partners in ratio of their capital contribution or any

manner specified in the partnership agreement. So it can be said that there is difference of

distribution of profit among company and partnership firm in various ways. Firstly their no

liability on company to distribute the profits but in case of partnership partners have right to

receive the profits. There is no fixed percentage of profits to be distributed to the shareholders of

the company whereas a partnership firm has to pay fixed profits to their partners (Stickney,

2009).

11

Profits remained after deducting all the expenses and tax liability has to either transferred

to the retained earnings or has to be distributed to the members (Shareholders) of the respective

entity. In case of companies profits are derived after deducting the expenses are transferred to the

equity capital in form of retained earnings and it is subject to distribution in case dividends are

declared by the company. Dividend refers to distribution of profits earned by the company to

their respective shareholders as per the number of shares hold by them. In statement of change in

equity various balance such as retained earnings, equity share capital, etc are recorded and any

change to them is also provided so to make the changes in amount of leftover retained earnings

with the company. The total profit available is appropriated in total number of shares subscribed

by the shareholders of the company. Profits are divided into two main parts one is retained

earnings and current year dividends (Country Road, Annual Report, 2013). Retained earnings is

leftover of profits remained after distribution of dividends. In case of partnership firms profits of

company are distributed to the respective partners in ratio of their capital contribution or any

manner specified in the partnership agreement. So it can be said that there is difference of

distribution of profit among company and partnership firm in various ways. Firstly their no

liability on company to distribute the profits but in case of partnership partners have right to

receive the profits. There is no fixed percentage of profits to be distributed to the shareholders of

the company whereas a partnership firm has to pay fixed profits to their partners (Stickney,

2009).

11

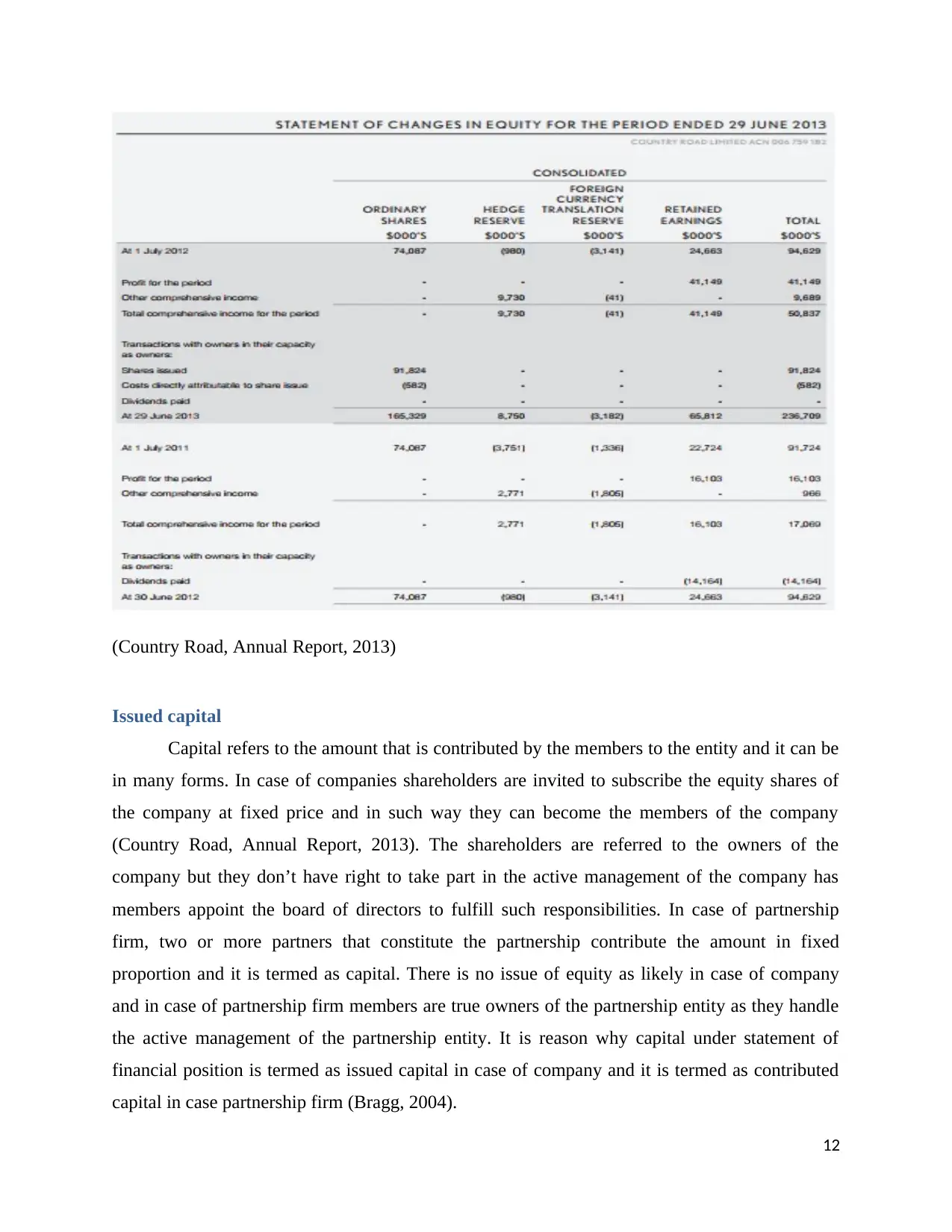

(Country Road, Annual Report, 2013)

Issued capital

Capital refers to the amount that is contributed by the members to the entity and it can be

in many forms. In case of companies shareholders are invited to subscribe the equity shares of

the company at fixed price and in such way they can become the members of the company

(Country Road, Annual Report, 2013). The shareholders are referred to the owners of the

company but they don’t have right to take part in the active management of the company has

members appoint the board of directors to fulfill such responsibilities. In case of partnership

firm, two or more partners that constitute the partnership contribute the amount in fixed

proportion and it is termed as capital. There is no issue of equity as likely in case of company

and in case of partnership firm members are true owners of the partnership entity as they handle

the active management of the partnership entity. It is reason why capital under statement of

financial position is termed as issued capital in case of company and it is termed as contributed

capital in case partnership firm (Bragg, 2004).

12

Issued capital

Capital refers to the amount that is contributed by the members to the entity and it can be

in many forms. In case of companies shareholders are invited to subscribe the equity shares of

the company at fixed price and in such way they can become the members of the company

(Country Road, Annual Report, 2013). The shareholders are referred to the owners of the

company but they don’t have right to take part in the active management of the company has

members appoint the board of directors to fulfill such responsibilities. In case of partnership

firm, two or more partners that constitute the partnership contribute the amount in fixed

proportion and it is termed as capital. There is no issue of equity as likely in case of company

and in case of partnership firm members are true owners of the partnership entity as they handle

the active management of the partnership entity. It is reason why capital under statement of

financial position is termed as issued capital in case of company and it is termed as contributed

capital in case partnership firm (Bragg, 2004).

12

Cash Flow Statements

Cash flow statements refer to the financial statements that provide the flow of cash from

various activities such as operating activity, investment activity and financial activity (Country

Road, Annual Report, 2013). It is mandatory for the companies to prepare the cash flow

statement whereas there is no such requirement in case of partnership firms. As per the

companies act and IFRS there is requirement to include the statement of cash flow together with

other statement in case of companies. Cash flow statement is detailed overview of cash flows and

it can also be seen from the bank and cash account of the entity. In order to make it simple to

understand for the users of financial statement of company, cash flow statement is prepared and

no such requirement is posed in partnership firms (Ernst and Häcker, 2012).

Conclusion

Understanding the financial statement of the company is not easy and it involves

inclusion of various topics and sub topics. There are many items in the complex financial

statements of any company.

13

Cash flow statements refer to the financial statements that provide the flow of cash from

various activities such as operating activity, investment activity and financial activity (Country

Road, Annual Report, 2013). It is mandatory for the companies to prepare the cash flow

statement whereas there is no such requirement in case of partnership firms. As per the

companies act and IFRS there is requirement to include the statement of cash flow together with

other statement in case of companies. Cash flow statement is detailed overview of cash flows and

it can also be seen from the bank and cash account of the entity. In order to make it simple to

understand for the users of financial statement of company, cash flow statement is prepared and

no such requirement is posed in partnership firms (Ernst and Häcker, 2012).

Conclusion

Understanding the financial statement of the company is not easy and it involves

inclusion of various topics and sub topics. There are many items in the complex financial

statements of any company.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Bragg, S. 2004. GAAP Implementation Guide. John Wiley & Sons.

Country Road. 2013. Annual Report. [Online]. Available at:

https://www.countryroad.com.au/images/assetimages/ASX/CRG_Annual_Report_2013.pdf

[Accessed on: 6 October, 2017].

Epstein, B and Jermakowicz, E. 2010. WILEY Interpretation and Application of International

Financial Reporting Standards. John Wiley & Sons.

Ernst, D. and Häcker, J. 2012. Applied International Corporate Finance. Vahlen.

Gibson, C. 2010. Financial Reporting and Analysis: Using Financial Accounting Information.

Cengage Learning.

IAS 37 — Provisions, Contingent Liabilities and Contingent Assets. 2017. [Online]. Available

at: https://www.iasplus.com/en/standards/ias/ias37 [Accessed on: 6 September 2017].

JB Hi-Fi Limited. 2013. Annual Report.

Palepu, K. et al. 2007. Business Analysis and Valuation: Text and Cases. Cengage Learning

EMEA.

Stickney, C.P. et al. 2009. Financial Accounting: An Introduction to Concepts, Methods and

Uses. Cengage Learning.

Weil, R., Schipper, K. and Francis, J. 2013. Financial Accounting: An Introduction to Concepts,

Methods and Uses. Cengage Learning.

Weygandt, J., Kieso, D.E. and Kimmel, P.D. 2010. Financial Accounting: IFRS. John Wiley &

Sons.

14

Bragg, S. 2004. GAAP Implementation Guide. John Wiley & Sons.

Country Road. 2013. Annual Report. [Online]. Available at:

https://www.countryroad.com.au/images/assetimages/ASX/CRG_Annual_Report_2013.pdf

[Accessed on: 6 October, 2017].

Epstein, B and Jermakowicz, E. 2010. WILEY Interpretation and Application of International

Financial Reporting Standards. John Wiley & Sons.

Ernst, D. and Häcker, J. 2012. Applied International Corporate Finance. Vahlen.

Gibson, C. 2010. Financial Reporting and Analysis: Using Financial Accounting Information.

Cengage Learning.

IAS 37 — Provisions, Contingent Liabilities and Contingent Assets. 2017. [Online]. Available

at: https://www.iasplus.com/en/standards/ias/ias37 [Accessed on: 6 September 2017].

JB Hi-Fi Limited. 2013. Annual Report.

Palepu, K. et al. 2007. Business Analysis and Valuation: Text and Cases. Cengage Learning

EMEA.

Stickney, C.P. et al. 2009. Financial Accounting: An Introduction to Concepts, Methods and

Uses. Cengage Learning.

Weil, R., Schipper, K. and Francis, J. 2013. Financial Accounting: An Introduction to Concepts,

Methods and Uses. Cengage Learning.

Weygandt, J., Kieso, D.E. and Kimmel, P.D. 2010. Financial Accounting: IFRS. John Wiley &

Sons.

14

15

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.