Financial Accounting: Standard Violations and Journal Entries

VerifiedAdded on 2020/02/24

|4

|1245

|115

Homework Assignment

AI Summary

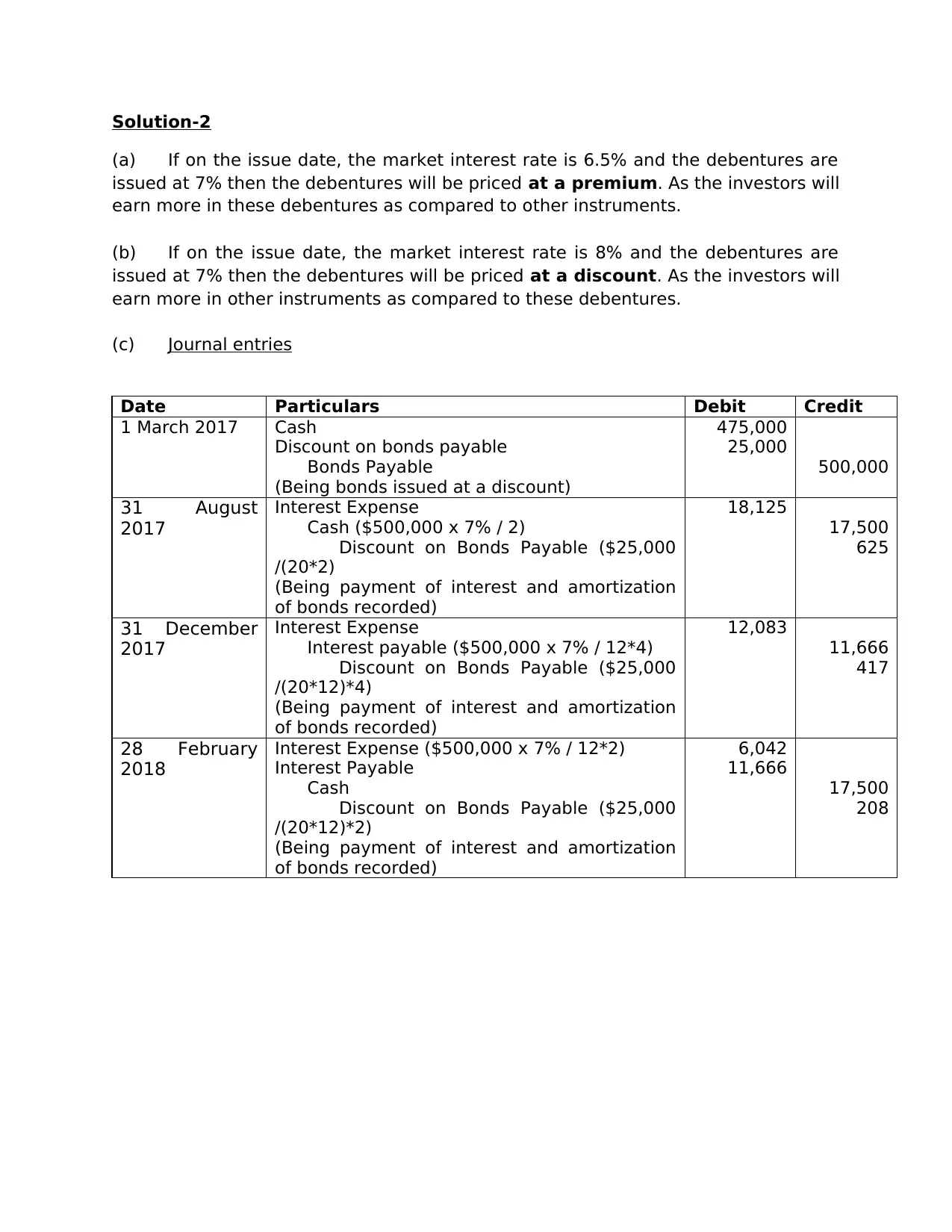

This assignment addresses several financial accounting issues. The first part analyzes violations of accounting standards AASB 116 and AASB 138, focusing on the improper treatment of repairs and maintenance, the incorrect capitalization of plant and equipment, and the valuation of intangible assets. It explains why debiting ordinary repairs to plant and equipment and debiting plant and equipment purchases to repairs expense are violations of AASB 116, and why valuing intangible assets at $1 or $0 is incorrect. The second part provides journal entries related to debentures issued at a discount, including calculations for interest expense and the amortization of the discount. The assignment explains the pricing of debentures based on market interest rates and provides journal entries for the issuance, interest payments, and discount amortization.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.