Corporate Accounting and Financial Reporting (ACC204) Impairment Loss

VerifiedAdded on 2020/05/28

|8

|1534

|85

Report

AI Summary

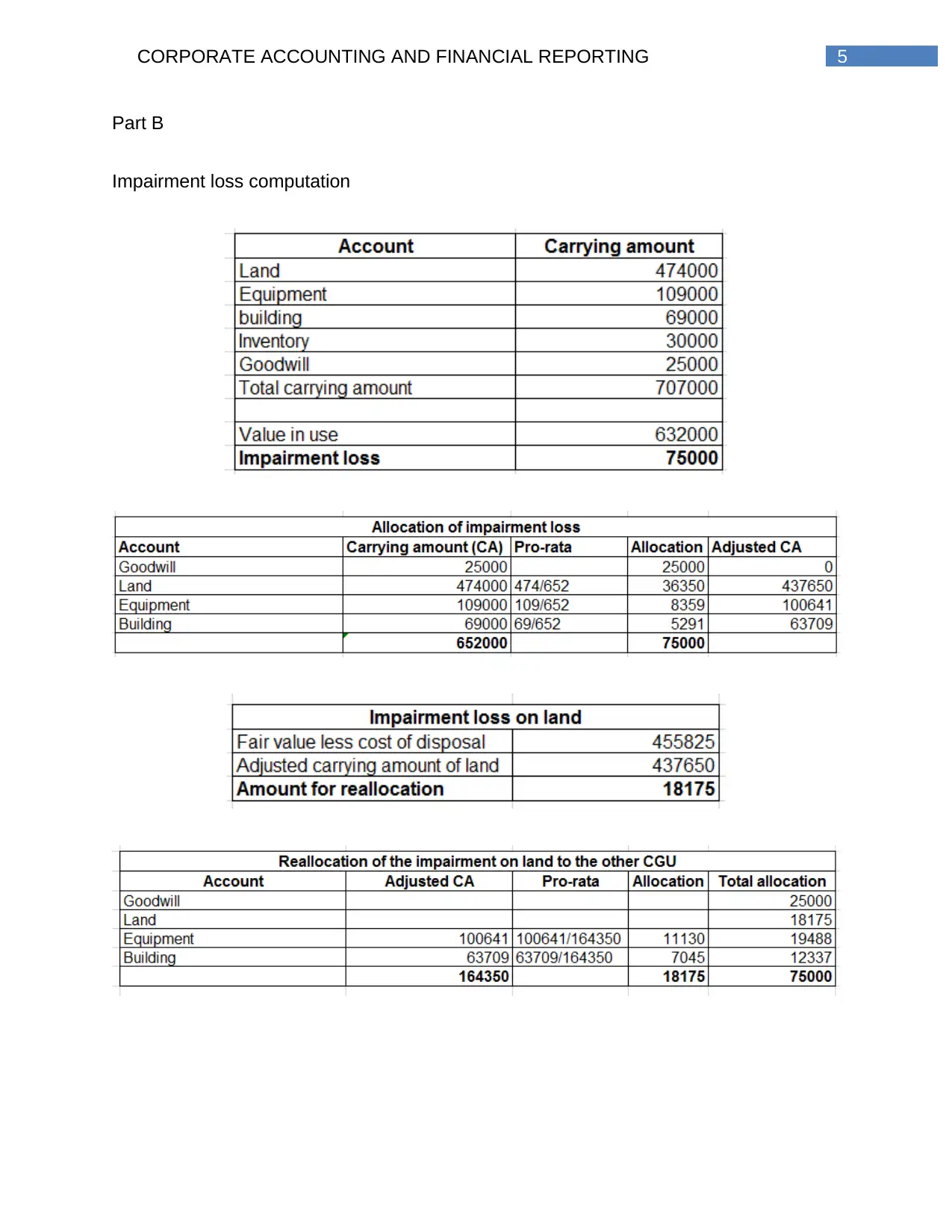

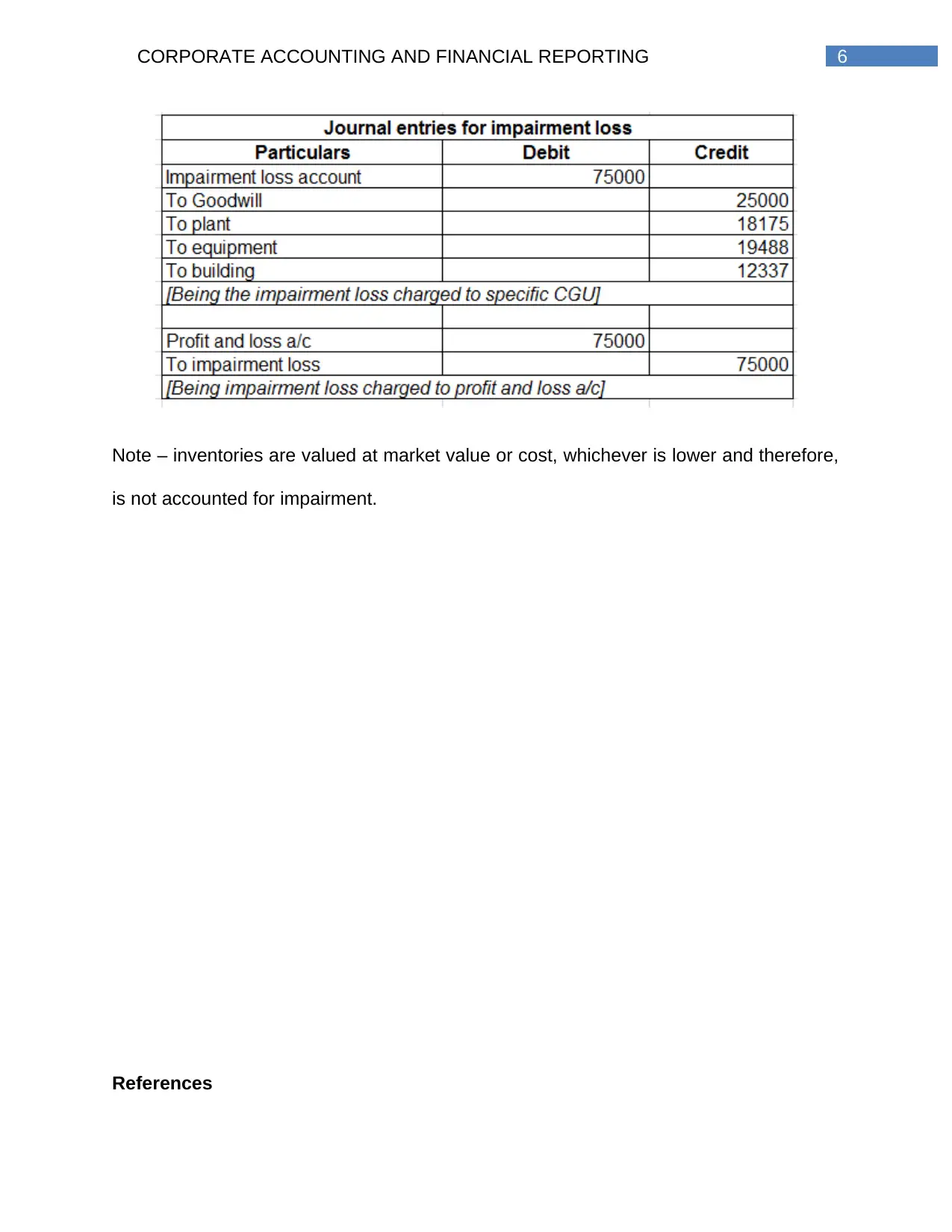

This report provides an in-depth analysis of impairment losses in corporate accounting, focusing on the guidelines outlined in AASB 136. It defines impairment, explaining when an asset's recorded value exceeds its market price, and details the process of assessing recoverable amounts for both individual assets and cash-generating units (CGUs). The report emphasizes the importance of identifying impairment indicators, both internal and external, and outlines how to calculate recoverable amounts using fair value less costs of disposal and value in use. It further discusses the allocation of impairment losses to CGUs, including goodwill, and explains the process of impairment testing. The report references relevant literature and provides a comprehensive understanding of impairment accounting practices.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.