ACC210 Financial Accounting Task 2 Major Assignment Semester 2 - 2017

VerifiedAdded on 2020/04/01

|13

|2915

|23

Homework Assignment

AI Summary

This document presents a comprehensive solution to ACC210 Financial Accounting Task 2, covering key accounting concepts. The assignment addresses fair value measurement, including valuation techniques for land and factories. It analyzes the revaluation of assets, providing detailed journal entries and calculations for machinery. The solution also explores the accounting treatment of internally generated intangible assets, differentiating between research and development phases, comparing internally generated versus acquired assets, and explaining the reasons for managerial reluctance to recognize such assets. Finally, the assignment includes calculations related to a defined benefit superannuation plan, determining the deficit of the fund, net defined benefit liability, and net interest. This solution serves as a valuable resource for students studying financial accounting, offering insights into complex accounting principles and their practical application.

ACC210(ATMC) - Financial Accounting

Task 2 – Major Assignment

Semester 2 - 2017

Student Name:

Student ID #:

Campus:

Task 2 – Major Assignment

Semester 2 - 2017

Student Name:

Student ID #:

Campus:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1. Ex 3.1..................................................................................................................................3

Accounting Justification:................................................................................................................3

Relevant Issues:.............................................................................................................................3

1. Determine subject of measurement..........................................................................................3

2. Determine valuation premise/method......................................................................................3

3. Determine market.....................................................................................................................3

4. Determine Valuation technique.................................................................................................3

Question 2. Ex 5.18................................................................................................................................4

Accounting Justification:................................................................................................................4

Relevant Issues:.............................................................................................................................4

1. Calculations & General Journal Entries 1/7/16 to 30/6/17:.......................................................4

2. Calculations & General Journal Entries 1/8/18:.........................................................................4

3. Calculations & General Journal Entries 30/6/18:.......................................................................4

Question 3. Ex 6.11................................................................................................................................5

Accounting Justification:................................................................................................................5

Relevant Issues:.............................................................................................................................5

1. Explain accounting issues...........................................................................................................5

2. Differences Internally Generated vs Acquired...........................................................................5

3. Reasons for Reluctance..............................................................................................................5

Question 4. Ex 9.19................................................................................................................................6

Accounting Justification:................................................................................................................6

Relevant Issues:.............................................................................................................................6

1. Deficit of Fund...........................................................................................................................6

2. Net Defined Benefit Liability......................................................................................................6

3. Net Interest................................................................................................................................6

4. Reconciliation............................................................................................................................6

5. Summary Journal.......................................................................................................................6

Page 2 of 13

Question 1. Ex 3.1..................................................................................................................................3

Accounting Justification:................................................................................................................3

Relevant Issues:.............................................................................................................................3

1. Determine subject of measurement..........................................................................................3

2. Determine valuation premise/method......................................................................................3

3. Determine market.....................................................................................................................3

4. Determine Valuation technique.................................................................................................3

Question 2. Ex 5.18................................................................................................................................4

Accounting Justification:................................................................................................................4

Relevant Issues:.............................................................................................................................4

1. Calculations & General Journal Entries 1/7/16 to 30/6/17:.......................................................4

2. Calculations & General Journal Entries 1/8/18:.........................................................................4

3. Calculations & General Journal Entries 30/6/18:.......................................................................4

Question 3. Ex 6.11................................................................................................................................5

Accounting Justification:................................................................................................................5

Relevant Issues:.............................................................................................................................5

1. Explain accounting issues...........................................................................................................5

2. Differences Internally Generated vs Acquired...........................................................................5

3. Reasons for Reluctance..............................................................................................................5

Question 4. Ex 9.19................................................................................................................................6

Accounting Justification:................................................................................................................6

Relevant Issues:.............................................................................................................................6

1. Deficit of Fund...........................................................................................................................6

2. Net Defined Benefit Liability......................................................................................................6

3. Net Interest................................................................................................................................6

4. Reconciliation............................................................................................................................6

5. Summary Journal.......................................................................................................................6

Page 2 of 13

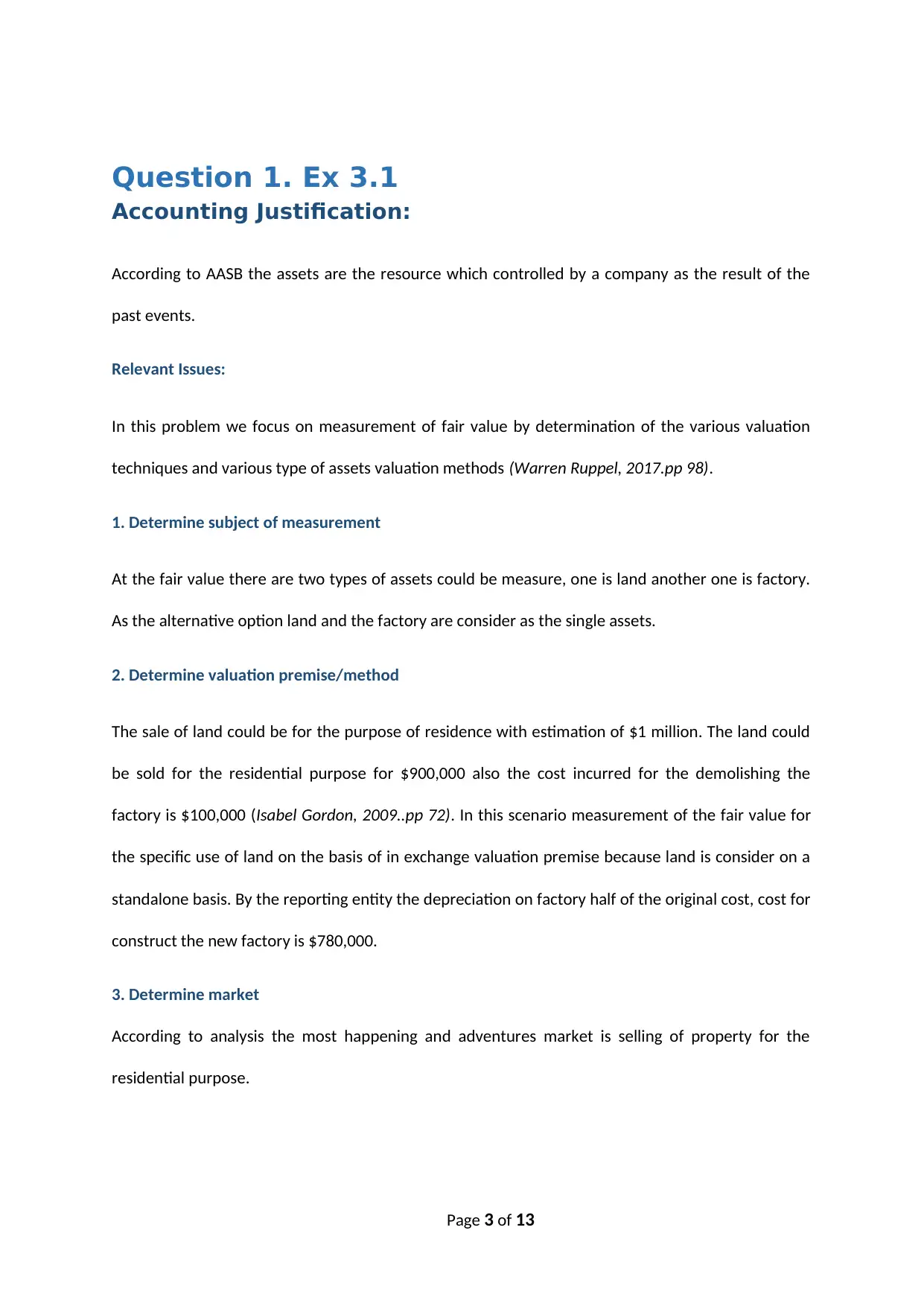

Question 1. Ex 3.1

Accounting Justification:

According to AASB the assets are the resource which controlled by a company as the result of the

past events.

Relevant Issues:

In this problem we focus on measurement of fair value by determination of the various valuation

techniques and various type of assets valuation methods (Warren Ruppel, 2017.pp 98).

1. Determine subject of measurement

At the fair value there are two types of assets could be measure, one is land another one is factory.

As the alternative option land and the factory are consider as the single assets.

2. Determine valuation premise/method

The sale of land could be for the purpose of residence with estimation of $1 million. The land could

be sold for the residential purpose for $900,000 also the cost incurred for the demolishing the

factory is $100,000 (Isabel Gordon, 2009..pp 72). In this scenario measurement of the fair value for

the specific use of land on the basis of in exchange valuation premise because land is consider on a

standalone basis. By the reporting entity the depreciation on factory half of the original cost, cost for

construct the new factory is $780,000.

3. Determine market

According to analysis the most happening and adventures market is selling of property for the

residential purpose.

Page 3 of 13

Accounting Justification:

According to AASB the assets are the resource which controlled by a company as the result of the

past events.

Relevant Issues:

In this problem we focus on measurement of fair value by determination of the various valuation

techniques and various type of assets valuation methods (Warren Ruppel, 2017.pp 98).

1. Determine subject of measurement

At the fair value there are two types of assets could be measure, one is land another one is factory.

As the alternative option land and the factory are consider as the single assets.

2. Determine valuation premise/method

The sale of land could be for the purpose of residence with estimation of $1 million. The land could

be sold for the residential purpose for $900,000 also the cost incurred for the demolishing the

factory is $100,000 (Isabel Gordon, 2009..pp 72). In this scenario measurement of the fair value for

the specific use of land on the basis of in exchange valuation premise because land is consider on a

standalone basis. By the reporting entity the depreciation on factory half of the original cost, cost for

construct the new factory is $780,000.

3. Determine market

According to analysis the most happening and adventures market is selling of property for the

residential purpose.

Page 3 of 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Determine Valuation technique

The best approach for the proper valuation technique is market approach because there are many

observable inputs in terms of property market selling prices (Warren Ruppel, 2017..pp 37).

On the separate assets factory has o fair value and the fair value of land is based on the market price

of the similar property of $900,000.

The high and best use of the land with the calculation comparison:

As the vacant block the value of the land for the purpose of resident, which includes the factory at

the 0 fair value and,

1. If the factory is develop for the industrial used which also includes the factory as an ongoing

asset.

High and best use is the higher of below mentioned two values. If

1. Is chosen, then the fair value of the factory is zero and no depreciation will be calculated.

2. Is chosen, then it will be required to calculate the fair value of the factory separate from the

fair value of the land for depreciation on the factory (Abbas Ali Mirza, 2015..pp 102). If

should be argue with the below mentioned formula-

Fair value of the factory = Difference between the fair value of the land for residential

purposes - Fair value of the combined assets

Page 4 of 13

The best approach for the proper valuation technique is market approach because there are many

observable inputs in terms of property market selling prices (Warren Ruppel, 2017..pp 37).

On the separate assets factory has o fair value and the fair value of land is based on the market price

of the similar property of $900,000.

The high and best use of the land with the calculation comparison:

As the vacant block the value of the land for the purpose of resident, which includes the factory at

the 0 fair value and,

1. If the factory is develop for the industrial used which also includes the factory as an ongoing

asset.

High and best use is the higher of below mentioned two values. If

1. Is chosen, then the fair value of the factory is zero and no depreciation will be calculated.

2. Is chosen, then it will be required to calculate the fair value of the factory separate from the

fair value of the land for depreciation on the factory (Abbas Ali Mirza, 2015..pp 102). If

should be argue with the below mentioned formula-

Fair value of the factory = Difference between the fair value of the land for residential

purposes - Fair value of the combined assets

Page 4 of 13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

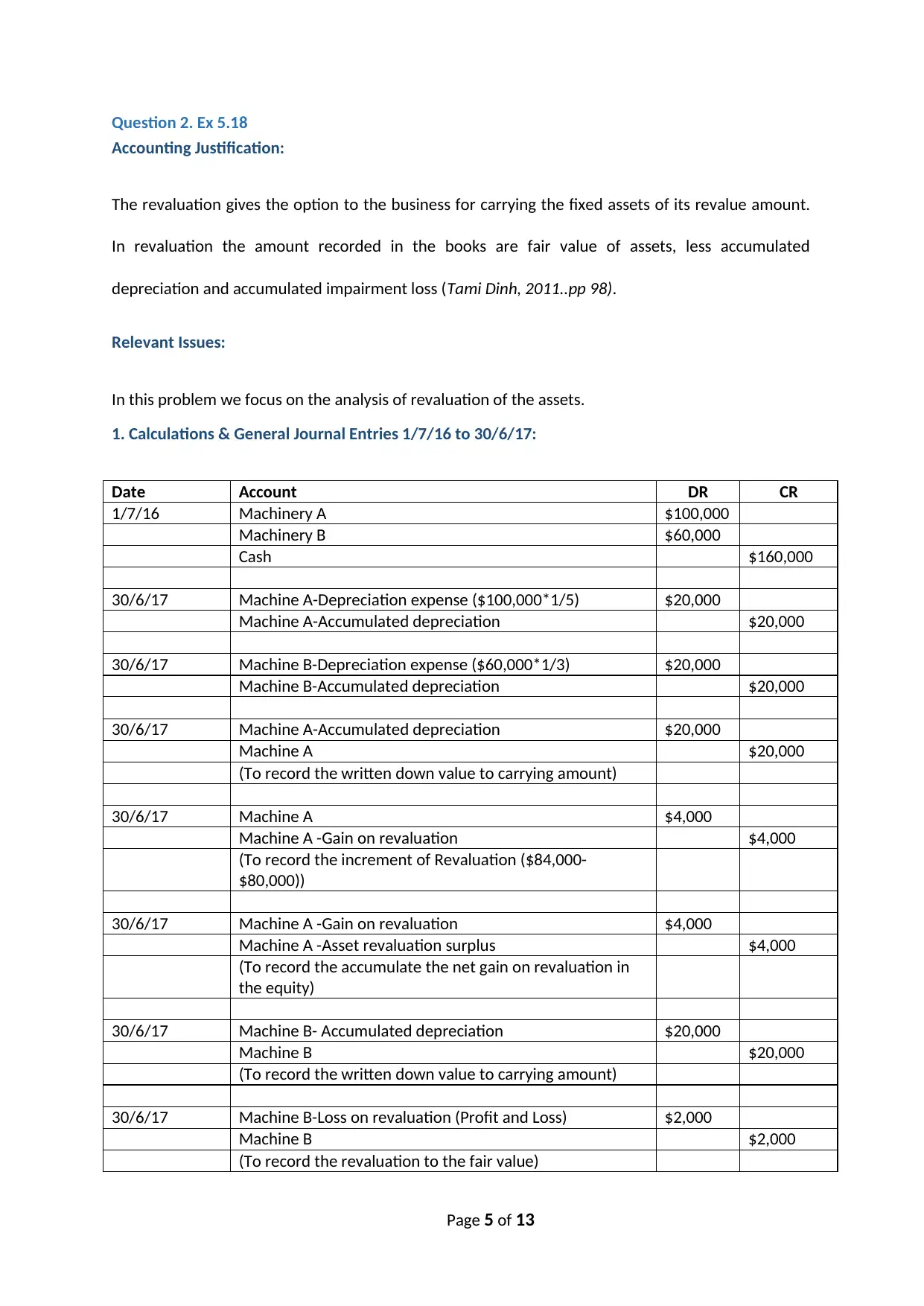

Question 2. Ex 5.18

Accounting Justification:

The revaluation gives the option to the business for carrying the fixed assets of its revalue amount.

In revaluation the amount recorded in the books are fair value of assets, less accumulated

depreciation and accumulated impairment loss (Tami Dinh, 2011..pp 98).

Relevant Issues:

In this problem we focus on the analysis of revaluation of the assets.

1. Calculations & General Journal Entries 1/7/16 to 30/6/17:

Date Account DR CR

1/7/16 Machinery A $100,000

Machinery B $60,000

Cash $160,000

30/6/17 Machine A-Depreciation expense ($100,000*1/5) $20,000

Machine A-Accumulated depreciation $20,000

30/6/17 Machine B-Depreciation expense ($60,000*1/3) $20,000

Machine B-Accumulated depreciation $20,000

30/6/17 Machine A-Accumulated depreciation $20,000

Machine A $20,000

(To record the written down value to carrying amount)

30/6/17 Machine A $4,000

Machine A -Gain on revaluation $4,000

(To record the increment of Revaluation ($84,000-

$80,000))

30/6/17 Machine A -Gain on revaluation $4,000

Machine A -Asset revaluation surplus $4,000

(To record the accumulate the net gain on revaluation in

the equity)

30/6/17 Machine B- Accumulated depreciation $20,000

Machine B $20,000

(To record the written down value to carrying amount)

30/6/17 Machine B-Loss on revaluation (Profit and Loss) $2,000

Machine B $2,000

(To record the revaluation to the fair value)

Page 5 of 13

Accounting Justification:

The revaluation gives the option to the business for carrying the fixed assets of its revalue amount.

In revaluation the amount recorded in the books are fair value of assets, less accumulated

depreciation and accumulated impairment loss (Tami Dinh, 2011..pp 98).

Relevant Issues:

In this problem we focus on the analysis of revaluation of the assets.

1. Calculations & General Journal Entries 1/7/16 to 30/6/17:

Date Account DR CR

1/7/16 Machinery A $100,000

Machinery B $60,000

Cash $160,000

30/6/17 Machine A-Depreciation expense ($100,000*1/5) $20,000

Machine A-Accumulated depreciation $20,000

30/6/17 Machine B-Depreciation expense ($60,000*1/3) $20,000

Machine B-Accumulated depreciation $20,000

30/6/17 Machine A-Accumulated depreciation $20,000

Machine A $20,000

(To record the written down value to carrying amount)

30/6/17 Machine A $4,000

Machine A -Gain on revaluation $4,000

(To record the increment of Revaluation ($84,000-

$80,000))

30/6/17 Machine A -Gain on revaluation $4,000

Machine A -Asset revaluation surplus $4,000

(To record the accumulate the net gain on revaluation in

the equity)

30/6/17 Machine B- Accumulated depreciation $20,000

Machine B $20,000

(To record the written down value to carrying amount)

30/6/17 Machine B-Loss on revaluation (Profit and Loss) $2,000

Machine B $2,000

(To record the revaluation to the fair value)

Page 5 of 13

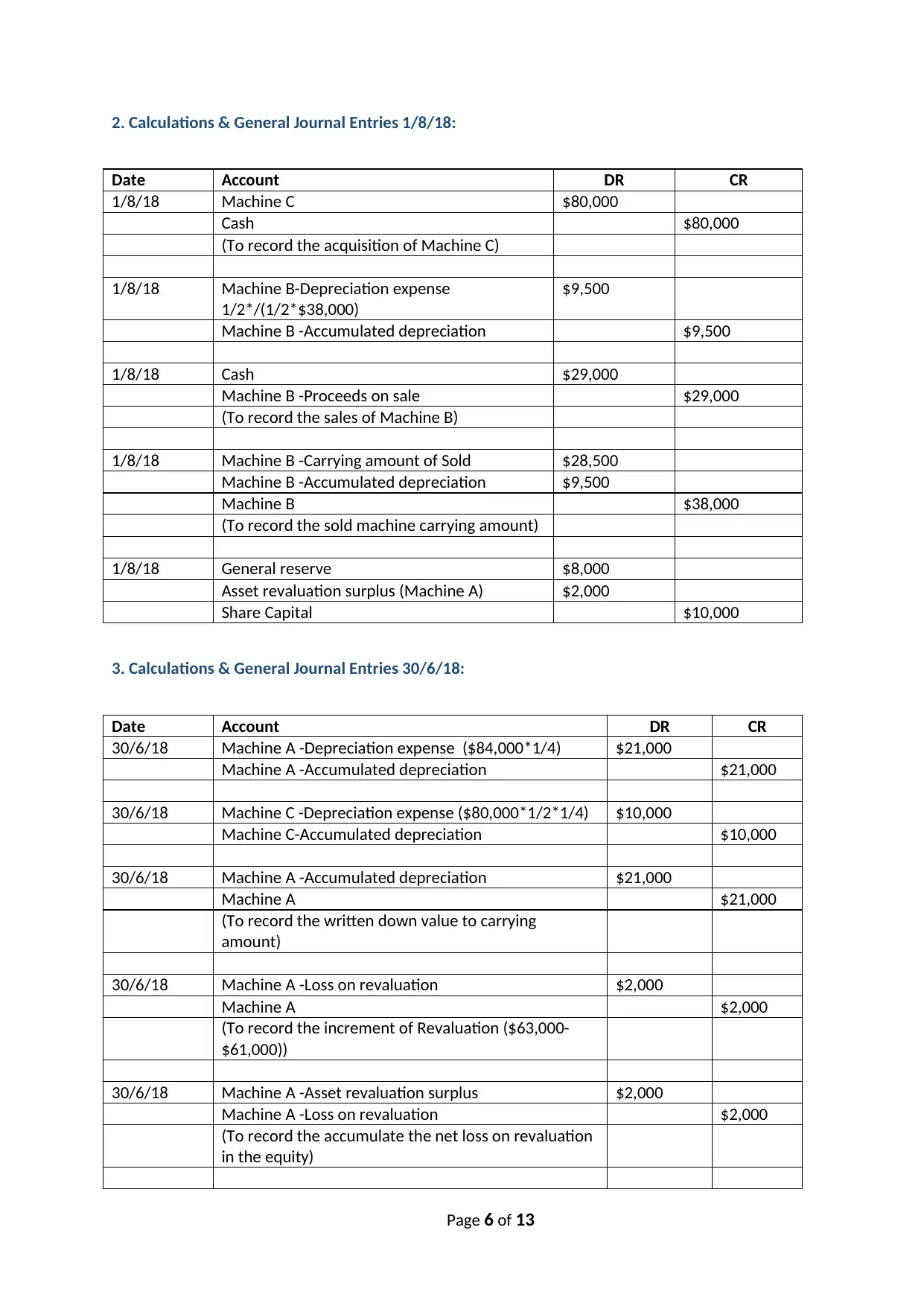

2. Calculations & General Journal Entries 1/8/18:

Date Account DR CR

1/8/18 Machine C $80,000

Cash $80,000

(To record the acquisition of Machine C)

1/8/18 Machine B-Depreciation expense

1/2*/(1/2*$38,000)

$9,500

Machine B -Accumulated depreciation $9,500

1/8/18 Cash $29,000

Machine B -Proceeds on sale $29,000

(To record the sales of Machine B)

1/8/18 Machine B -Carrying amount of Sold $28,500

Machine B -Accumulated depreciation $9,500

Machine B $38,000

(To record the sold machine carrying amount)

1/8/18 General reserve $8,000

Asset revaluation surplus (Machine A) $2,000

Share Capital $10,000

3. Calculations & General Journal Entries 30/6/18:

Date Account DR CR

30/6/18 Machine A -Depreciation expense ($84,000*1/4) $21,000

Machine A -Accumulated depreciation $21,000

30/6/18 Machine C -Depreciation expense ($80,000*1/2*1/4) $10,000

Machine C-Accumulated depreciation $10,000

30/6/18 Machine A -Accumulated depreciation $21,000

Machine A $21,000

(To record the written down value to carrying

amount)

30/6/18 Machine A -Loss on revaluation $2,000

Machine A $2,000

(To record the increment of Revaluation ($63,000-

$61,000))

30/6/18 Machine A -Asset revaluation surplus $2,000

Machine A -Loss on revaluation $2,000

(To record the accumulate the net loss on revaluation

in the equity)

Page 6 of 13

Date Account DR CR

1/8/18 Machine C $80,000

Cash $80,000

(To record the acquisition of Machine C)

1/8/18 Machine B-Depreciation expense

1/2*/(1/2*$38,000)

$9,500

Machine B -Accumulated depreciation $9,500

1/8/18 Cash $29,000

Machine B -Proceeds on sale $29,000

(To record the sales of Machine B)

1/8/18 Machine B -Carrying amount of Sold $28,500

Machine B -Accumulated depreciation $9,500

Machine B $38,000

(To record the sold machine carrying amount)

1/8/18 General reserve $8,000

Asset revaluation surplus (Machine A) $2,000

Share Capital $10,000

3. Calculations & General Journal Entries 30/6/18:

Date Account DR CR

30/6/18 Machine A -Depreciation expense ($84,000*1/4) $21,000

Machine A -Accumulated depreciation $21,000

30/6/18 Machine C -Depreciation expense ($80,000*1/2*1/4) $10,000

Machine C-Accumulated depreciation $10,000

30/6/18 Machine A -Accumulated depreciation $21,000

Machine A $21,000

(To record the written down value to carrying

amount)

30/6/18 Machine A -Loss on revaluation $2,000

Machine A $2,000

(To record the increment of Revaluation ($63,000-

$61,000))

30/6/18 Machine A -Asset revaluation surplus $2,000

Machine A -Loss on revaluation $2,000

(To record the accumulate the net loss on revaluation

in the equity)

Page 6 of 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

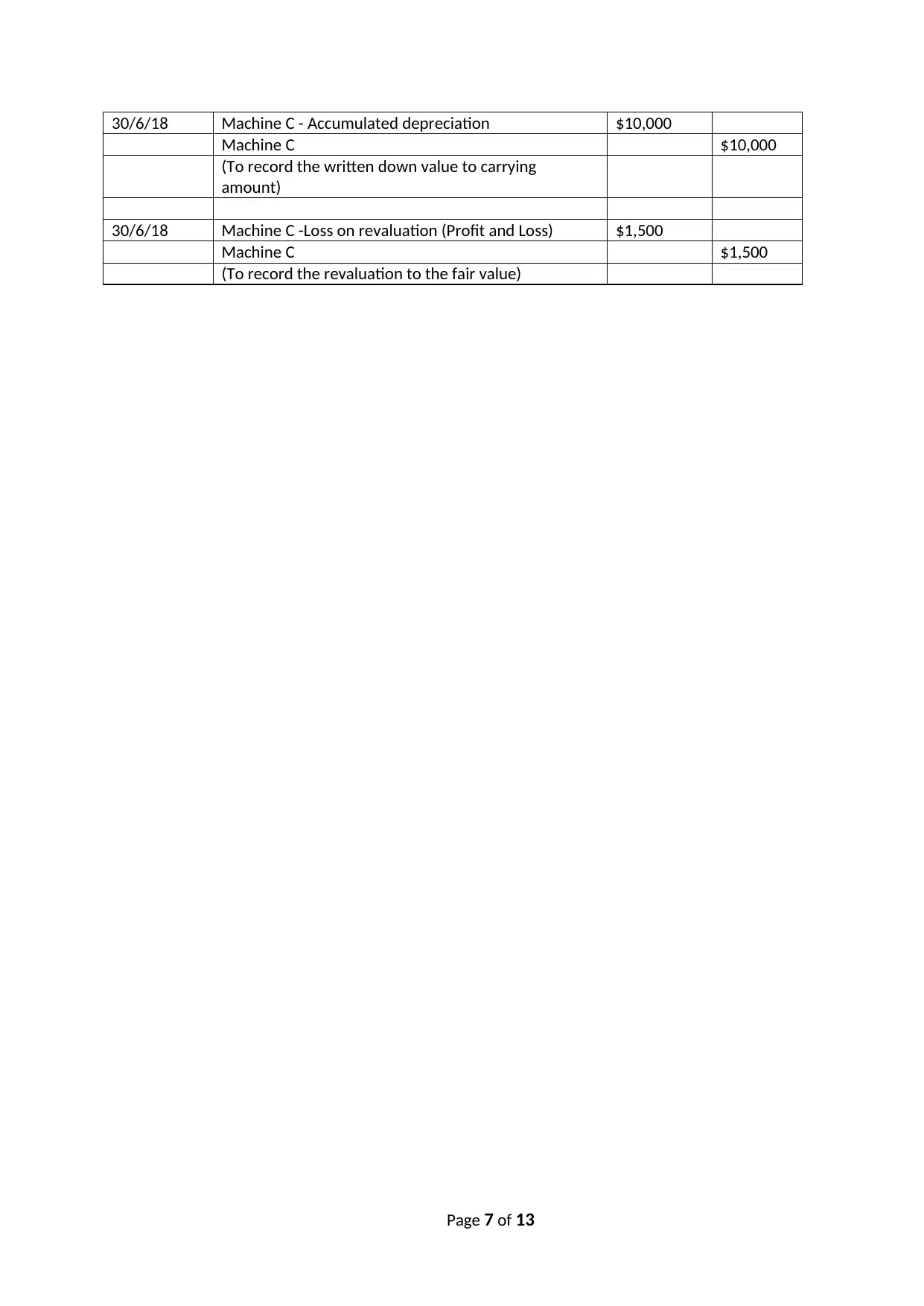

30/6/18 Machine C - Accumulated depreciation $10,000

Machine C $10,000

(To record the written down value to carrying

amount)

30/6/18 Machine C -Loss on revaluation (Profit and Loss) $1,500

Machine C $1,500

(To record the revaluation to the fair value)

Page 7 of 13

Machine C $10,000

(To record the written down value to carrying

amount)

30/6/18 Machine C -Loss on revaluation (Profit and Loss) $1,500

Machine C $1,500

(To record the revaluation to the fair value)

Page 7 of 13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 3. Ex 6.11

Accounting Justification:

The internally generated intangibles assets focus on the criteria of the recognition also the

generation of the assets to be classify as the-

1. Development Phase

2. Research Phase

Relevant Issues:

In this problem we focus on the analysis of AASB 138/IAS 38 in terms of internally generated

intangibles assets.

1. Explain accounting issues

The expense on the development of internally generated intangibles may be dependent on whether

the expenditure is classified as R&D. Research always plan for investigation of new knowledge and

development is the important application of the research findings (Warren Ruppel, 2017..pp44).

Research expense consider as the expense as incurred and development expense capitalized if all

the 6 criteria in para 57 of AASB 138 are met (Abbas Ali Mirza, 2015...pp37).

The AASB 138 explains that the internally generated intangibles like mastheads or brands not be

recognize also this list not focused on the patents.

2. Differences Internally Generated vs Acquired

It is very easy to recognize the intangibles when they are acquire in the comparison of when they are

internally generated. For acquiring of the intangibles there is a market of transaction and all

acquired assets measure at cost for the business measure at the fair value for business

combinations.

Page 8 of 13

Accounting Justification:

The internally generated intangibles assets focus on the criteria of the recognition also the

generation of the assets to be classify as the-

1. Development Phase

2. Research Phase

Relevant Issues:

In this problem we focus on the analysis of AASB 138/IAS 38 in terms of internally generated

intangibles assets.

1. Explain accounting issues

The expense on the development of internally generated intangibles may be dependent on whether

the expenditure is classified as R&D. Research always plan for investigation of new knowledge and

development is the important application of the research findings (Warren Ruppel, 2017..pp44).

Research expense consider as the expense as incurred and development expense capitalized if all

the 6 criteria in para 57 of AASB 138 are met (Abbas Ali Mirza, 2015...pp37).

The AASB 138 explains that the internally generated intangibles like mastheads or brands not be

recognize also this list not focused on the patents.

2. Differences Internally Generated vs Acquired

It is very easy to recognize the intangibles when they are acquire in the comparison of when they are

internally generated. For acquiring of the intangibles there is a market of transaction and all

acquired assets measure at cost for the business measure at the fair value for business

combinations.

Page 8 of 13

The assets which are acquire for the business combination fair values may be used compared with

having to calculate a cost. With the acquire assets the assets not allowed according to Para 63 for

recognize as internally generated intangibles (Tami Dinh, 2011...pp29).

On the assets are recognised then all the assets are subsequently treated the same.

3. Reasons for Reluctance

1. Managers preferred to inflate the future profits – Managers always focus on the inflate the

future profits because major investment of the company in R & D are written off, this shows

or guarantee that the future earnings derive from these acquiring will be reported as the

unencumbered by the major expense, or the amortization of the intangible asset, (Abbas Ali

Mirza, 2015..pp112). The impact of the ratios like return on equity and return on assets are

better in the future if written off occurred now rather than periodic amortization later

(Isabel Gordon, 2009..pp73).

2. Investors generally consider write-offs as one-time items – The number of big hits is

considering better than the amortization periodically. The discount of investor effect one

time writes off and cheers the improved profitability in next upcoming years. (Warren

Ruppel, 2017..pp121)

3. In case of failure the immediate expensing obviates the need to provide explanations – If

the company people written off their assets then this is the complete failure and manager

always preferred to avoid the lawsuits and questions. Also failure always gives more

attention than success.

4. Cost and benefit –The rules of accounting focus on the company in incurring the costs, such

as measuring fair values, running analytical models and payment of auditor for reviewing the

measures.

Page 9 of 13

having to calculate a cost. With the acquire assets the assets not allowed according to Para 63 for

recognize as internally generated intangibles (Tami Dinh, 2011...pp29).

On the assets are recognised then all the assets are subsequently treated the same.

3. Reasons for Reluctance

1. Managers preferred to inflate the future profits – Managers always focus on the inflate the

future profits because major investment of the company in R & D are written off, this shows

or guarantee that the future earnings derive from these acquiring will be reported as the

unencumbered by the major expense, or the amortization of the intangible asset, (Abbas Ali

Mirza, 2015..pp112). The impact of the ratios like return on equity and return on assets are

better in the future if written off occurred now rather than periodic amortization later

(Isabel Gordon, 2009..pp73).

2. Investors generally consider write-offs as one-time items – The number of big hits is

considering better than the amortization periodically. The discount of investor effect one

time writes off and cheers the improved profitability in next upcoming years. (Warren

Ruppel, 2017..pp121)

3. In case of failure the immediate expensing obviates the need to provide explanations – If

the company people written off their assets then this is the complete failure and manager

always preferred to avoid the lawsuits and questions. Also failure always gives more

attention than success.

4. Cost and benefit –The rules of accounting focus on the company in incurring the costs, such

as measuring fair values, running analytical models and payment of auditor for reviewing the

measures.

Page 9 of 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5. Lack of relevance of capitalized numbers – The relevance of the capitalized number is less

because there is no sufficient link between the expected future benefits and capitalized

costs.

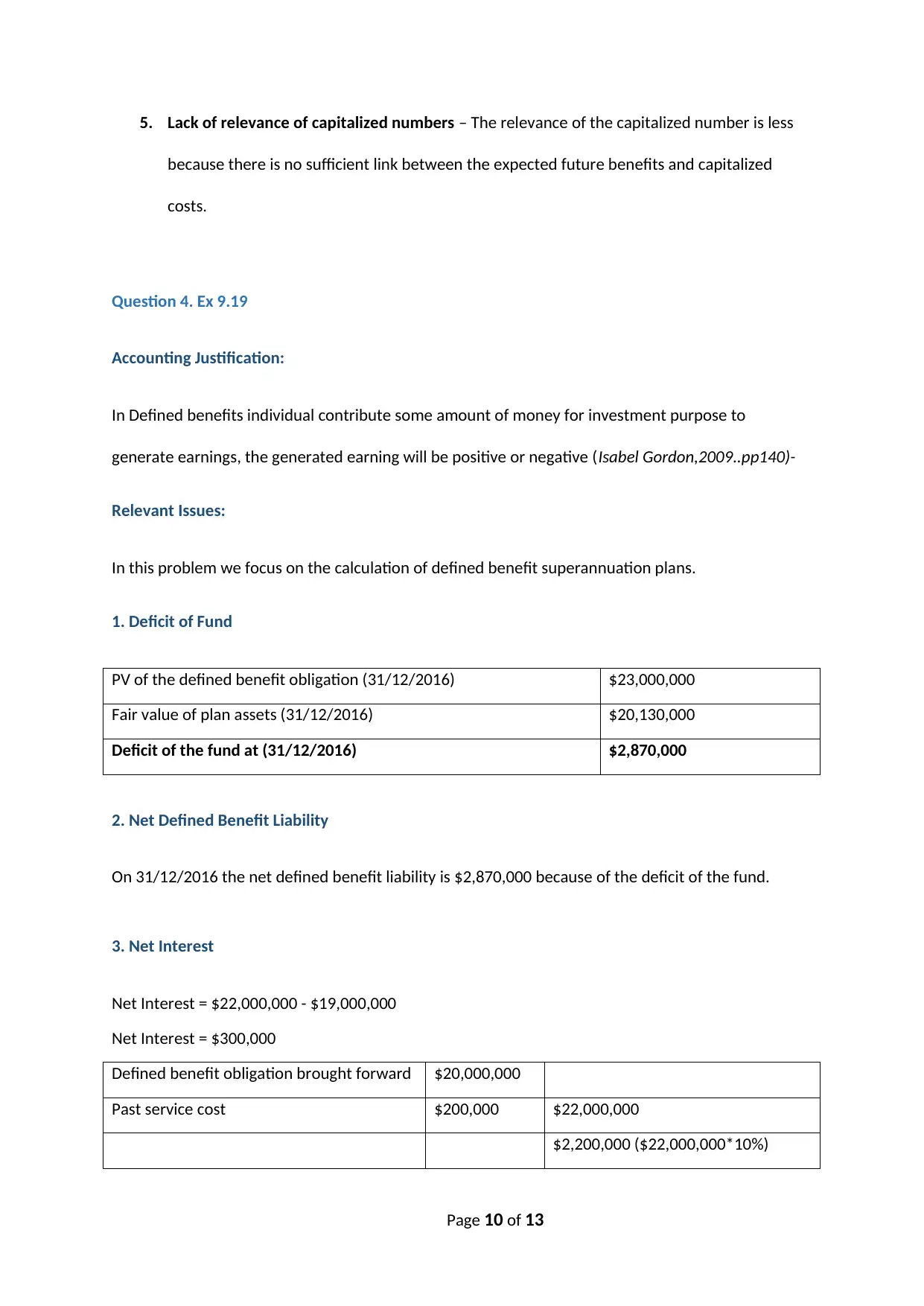

Question 4. Ex 9.19

Accounting Justification:

In Defined benefits individual contribute some amount of money for investment purpose to

generate earnings, the generated earning will be positive or negative (Isabel Gordon,2009..pp140)-

Relevant Issues:

In this problem we focus on the calculation of defined benefit superannuation plans.

1. Deficit of Fund

PV of the defined benefit obligation (31/12/2016) $23,000,000

Fair value of plan assets (31/12/2016) $20,130,000

Deficit of the fund at (31/12/2016) $2,870,000

2. Net Defined Benefit Liability

On 31/12/2016 the net defined benefit liability is $2,870,000 because of the deficit of the fund.

3. Net Interest

Net Interest = $22,000,000 - $19,000,000

Net Interest = $300,000

Defined benefit obligation brought forward $20,000,000

Past service cost $200,000 $22,000,000

$2,200,000 ($22,000,000*10%)

Page 10 of 13

because there is no sufficient link between the expected future benefits and capitalized

costs.

Question 4. Ex 9.19

Accounting Justification:

In Defined benefits individual contribute some amount of money for investment purpose to

generate earnings, the generated earning will be positive or negative (Isabel Gordon,2009..pp140)-

Relevant Issues:

In this problem we focus on the calculation of defined benefit superannuation plans.

1. Deficit of Fund

PV of the defined benefit obligation (31/12/2016) $23,000,000

Fair value of plan assets (31/12/2016) $20,130,000

Deficit of the fund at (31/12/2016) $2,870,000

2. Net Defined Benefit Liability

On 31/12/2016 the net defined benefit liability is $2,870,000 because of the deficit of the fund.

3. Net Interest

Net Interest = $22,000,000 - $19,000,000

Net Interest = $300,000

Defined benefit obligation brought forward $20,000,000

Past service cost $200,000 $22,000,000

$2,200,000 ($22,000,000*10%)

Page 10 of 13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

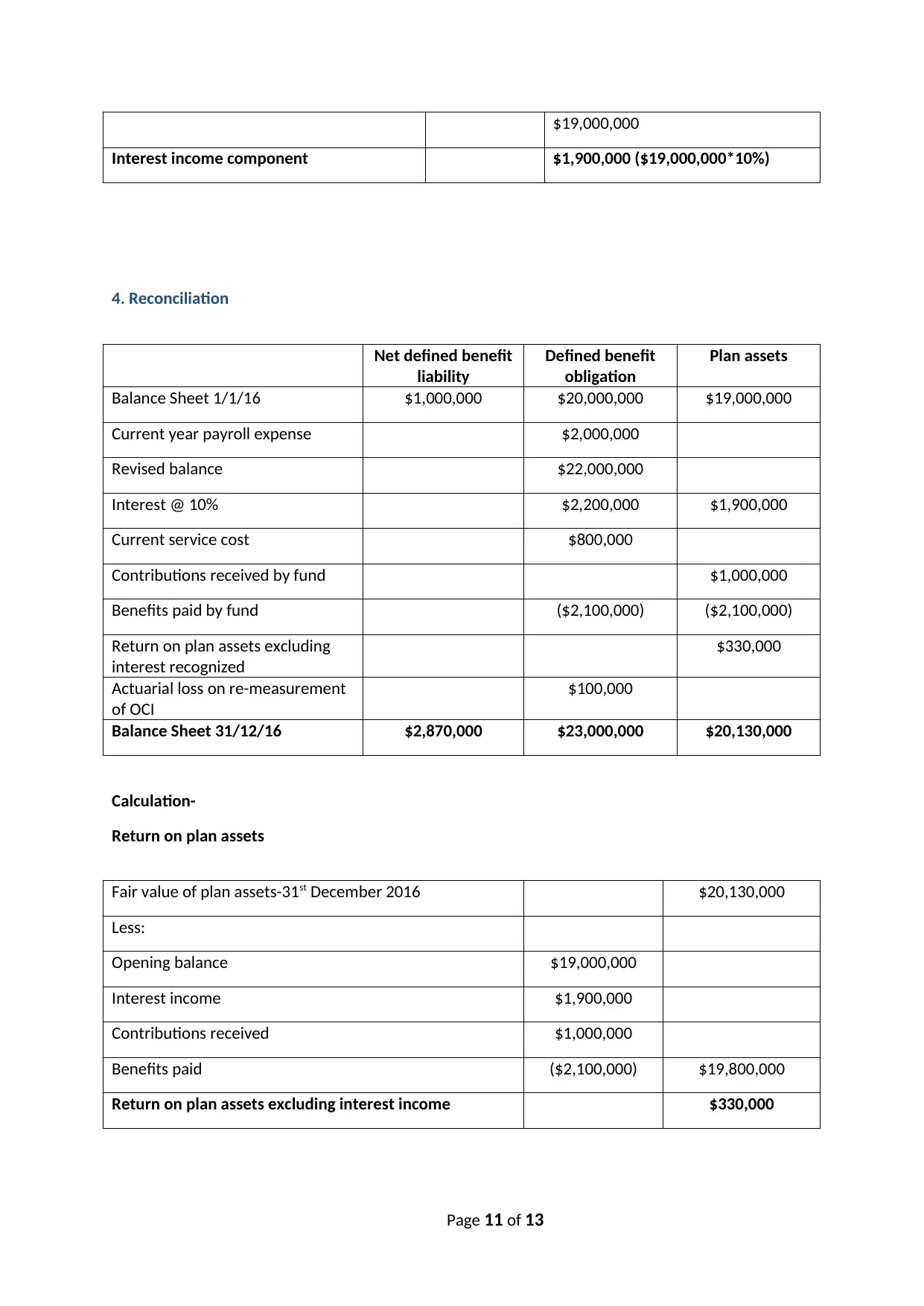

$19,000,000

Interest income component $1,900,000 ($19,000,000*10%)

4. Reconciliation

Net defined benefit

liability

Defined benefit

obligation

Plan assets

Balance Sheet 1/1/16 $1,000,000 $20,000,000 $19,000,000

Current year payroll expense $2,000,000

Revised balance $22,000,000

Interest @ 10% $2,200,000 $1,900,000

Current service cost $800,000

Contributions received by fund $1,000,000

Benefits paid by fund ($2,100,000) ($2,100,000)

Return on plan assets excluding

interest recognized

$330,000

Actuarial loss on re-measurement

of OCI

$100,000

Balance Sheet 31/12/16 $2,870,000 $23,000,000 $20,130,000

Calculation-

Return on plan assets

Fair value of plan assets-31st December 2016 $20,130,000

Less:

Opening balance $19,000,000

Interest income $1,900,000

Contributions received $1,000,000

Benefits paid ($2,100,000) $19,800,000

Return on plan assets excluding interest income $330,000

Page 11 of 13

Interest income component $1,900,000 ($19,000,000*10%)

4. Reconciliation

Net defined benefit

liability

Defined benefit

obligation

Plan assets

Balance Sheet 1/1/16 $1,000,000 $20,000,000 $19,000,000

Current year payroll expense $2,000,000

Revised balance $22,000,000

Interest @ 10% $2,200,000 $1,900,000

Current service cost $800,000

Contributions received by fund $1,000,000

Benefits paid by fund ($2,100,000) ($2,100,000)

Return on plan assets excluding

interest recognized

$330,000

Actuarial loss on re-measurement

of OCI

$100,000

Balance Sheet 31/12/16 $2,870,000 $23,000,000 $20,130,000

Calculation-

Return on plan assets

Fair value of plan assets-31st December 2016 $20,130,000

Less:

Opening balance $19,000,000

Interest income $1,900,000

Contributions received $1,000,000

Benefits paid ($2,100,000) $19,800,000

Return on plan assets excluding interest income $330,000

Page 11 of 13

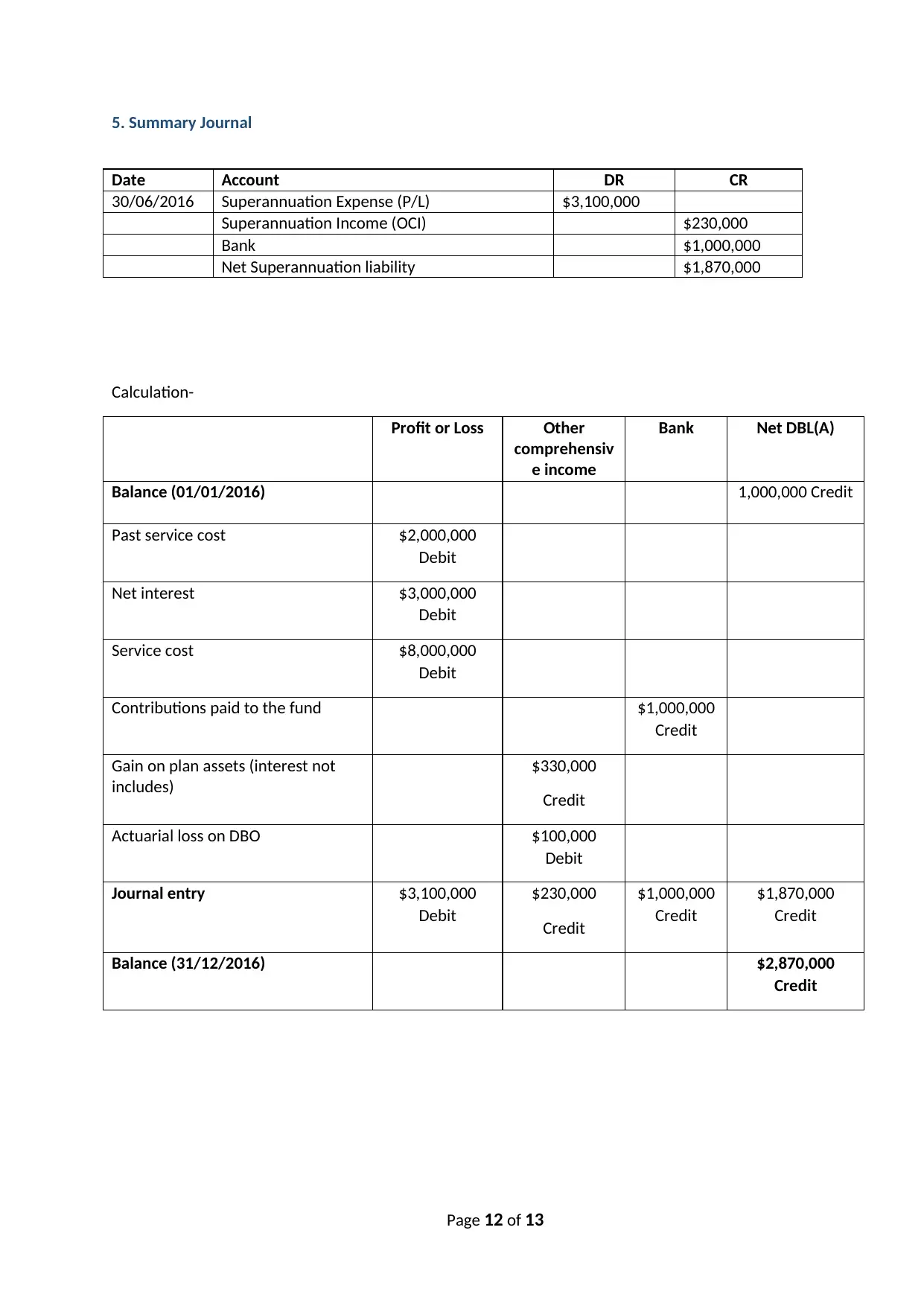

5. Summary Journal

Date Account DR CR

30/06/2016 Superannuation Expense (P/L) $3,100,000

Superannuation Income (OCI) $230,000

Bank $1,000,000

Net Superannuation liability $1,870,000

Calculation-

Profit or Loss Other

comprehensiv

e income

Bank Net DBL(A)

Balance (01/01/2016) 1,000,000 Credit

Past service cost $2,000,000

Debit

Net interest $3,000,000

Debit

Service cost $8,000,000

Debit

Contributions paid to the fund $1,000,000

Credit

Gain on plan assets (interest not

includes)

$330,000

Credit

Actuarial loss on DBO $100,000

Debit

Journal entry $3,100,000

Debit

$230,000

Credit

$1,000,000

Credit

$1,870,000

Credit

Balance (31/12/2016) $2,870,000

Credit

Page 12 of 13

Date Account DR CR

30/06/2016 Superannuation Expense (P/L) $3,100,000

Superannuation Income (OCI) $230,000

Bank $1,000,000

Net Superannuation liability $1,870,000

Calculation-

Profit or Loss Other

comprehensiv

e income

Bank Net DBL(A)

Balance (01/01/2016) 1,000,000 Credit

Past service cost $2,000,000

Debit

Net interest $3,000,000

Debit

Service cost $8,000,000

Debit

Contributions paid to the fund $1,000,000

Credit

Gain on plan assets (interest not

includes)

$330,000

Credit

Actuarial loss on DBO $100,000

Debit

Journal entry $3,100,000

Debit

$230,000

Credit

$1,000,000

Credit

$1,870,000

Credit

Balance (31/12/2016) $2,870,000

Credit

Page 12 of 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.