ACC510 Financial Reporting Task 2 - Major Assignment Semester 2 ATMC

VerifiedAdded on 2020/04/07

|9

|2041

|86

Homework Assignment

AI Summary

This document presents a comprehensive solution to ACC510 Financial Reporting Task 2, a major assignment for Semester 2. The assignment addresses key accounting concepts through case studies and exercises. Question 1 explores fair value accounting, emphasizing its subjective nature and application in contexts like aged care homes. Question 2 delves into impairment testing, specifically analyzing impairment losses for cash-generating units and the associated journal entries. Question 3 focuses on accounting for research and development costs, distinguishing between the research and development phases and their respective treatments in financial statements. Finally, Question 4 examines defined benefit obligations, including deficit calculations, net liabilities, interest, reconciliation, and journal entries related to pension plans. The solution provides detailed accounting justifications, relevant issues, and calculations to support the answers.

ACC510 (ATMC) - Financial Reporting

Task 2 – Major Assignment

Semester 2 - 2017

Student Name:

Student ID #:

Campus:

Task 2 – Major Assignment

Semester 2 - 2017

Student Name:

Student ID #:

Campus:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1. Case Study 3.1....................................................................................................................3

Accounting Justification:................................................................................................................3

Relevant Issues:.............................................................................................................................3

1. Highest & Best Use................................................................................................................3

2. Application to aged care home..............................................................................................3

3. Two possible uses..................................................................................................................3

Question 2. Ex 7.14................................................................................................................................4

Accounting Justification:................................................................................................................4

Relevant Issues:.............................................................................................................................4

1. Impairment Test 31/12/16....................................................................................................4

a. Calculations:.......................................................................................................................4

b. General Journal Entries 31/12/16:.....................................................................................4

2. Impairment Test 31/12/17....................................................................................................4

a. Calculations........................................................................................................................4

b. General Journal Entries 31/12/17:.....................................................................................4

Question 3. Case Study 6.1....................................................................................................................5

Accounting Justification:................................................................................................................5

Relevant Issues:.............................................................................................................................5

1. Difference between two phases:...........................................................................................5

2. Accounting for Research & Development:.............................................................................5

3. Decision / Conclusion / Reasons and Justification:................................................................5

Question 4. Ex 9.19................................................................................................................................6

Accounting Justification:................................................................................................................6

Relevant Issues:.............................................................................................................................6

1. Deficit of Fund...........................................................................................................................6

2. Net Defined Benefit Liability......................................................................................................6

3. Net Interest................................................................................................................................6

4. Reconciliation............................................................................................................................6

5. Summary Journal.......................................................................................................................6

Page 2 of 9

Question 1. Case Study 3.1....................................................................................................................3

Accounting Justification:................................................................................................................3

Relevant Issues:.............................................................................................................................3

1. Highest & Best Use................................................................................................................3

2. Application to aged care home..............................................................................................3

3. Two possible uses..................................................................................................................3

Question 2. Ex 7.14................................................................................................................................4

Accounting Justification:................................................................................................................4

Relevant Issues:.............................................................................................................................4

1. Impairment Test 31/12/16....................................................................................................4

a. Calculations:.......................................................................................................................4

b. General Journal Entries 31/12/16:.....................................................................................4

2. Impairment Test 31/12/17....................................................................................................4

a. Calculations........................................................................................................................4

b. General Journal Entries 31/12/17:.....................................................................................4

Question 3. Case Study 6.1....................................................................................................................5

Accounting Justification:................................................................................................................5

Relevant Issues:.............................................................................................................................5

1. Difference between two phases:...........................................................................................5

2. Accounting for Research & Development:.............................................................................5

3. Decision / Conclusion / Reasons and Justification:................................................................5

Question 4. Ex 9.19................................................................................................................................6

Accounting Justification:................................................................................................................6

Relevant Issues:.............................................................................................................................6

1. Deficit of Fund...........................................................................................................................6

2. Net Defined Benefit Liability......................................................................................................6

3. Net Interest................................................................................................................................6

4. Reconciliation............................................................................................................................6

5. Summary Journal.......................................................................................................................6

Page 2 of 9

Question 1. Case Study 3.1

Accounting Justification:

Fair value of the asset is the amount that can be procured when the asset is sold between

the willing and the knowledgeable parties at the arm’s length transaction and when they

enter the transaction freely. Paragraph B2 defines the entire concept of the fair value

measurement. Whereas Para 36 & Para 11 of the conceptual framework of general purpose

financial statements deals with the fair value accounting. The topic of fair value is subjective

and depends on the judgement being taken in the circumstances of the case. There may be

huge fluctuations in the fair value being computed by different individuals as it all depends

on the assumptions and judgements being used and hence depends on the circumstances of

the case. The transaction costs of selling an asset and that of transferring a liability in the

most advantageous transaction i.e., in the principal market should be directly attributable to

the asset and should meet the following criteria:

1. They should directly arise to the entity

2. They would not have taken place to entity had it not decided to dell asset or transfer

the liability.

Relevant Issues:

The most relevant issue here is the determination of the fair value being different in

different cases and being a subject which depends purely on judgemental decisions, the

value of property, plant and equipment as per fair value may vary hugely everyday. It is

generally used for the financial assets and further, it may be difficult for a non-profit entity

to use the fair value based on the highest and best use as the same property may be used

for varying purposes and market value may change depending on use.

1. Highest & Best Use

The principle of highest and best use comes for the non-financial assets where it is seen that

how the asset can be best utilised by the market participant to generate the highest

economic benefits out of the assets or to sell it to another market participant who can best

utilize the same. It considers 3 factors namely it should be physically possible, financially

feasible and legally acceptable.

2. Application to aged care home

The market value does not depends on the type of the entity or the valuation method being

used. So it should be applied uniformly whether its aged care homes or any profit making

entity based on the market based exit price as on the date of measurement.

3. Two possible uses

Fair valuation is of significant use in many cases like the impairment value assessment of

both the tangible and intangible assets. Secondly, International financial reporting standards

(IFRS) governs the reporting of the financial assets and liabilities in the financials in at fair

value. This is one another major use.

Page 3 of 9

Accounting Justification:

Fair value of the asset is the amount that can be procured when the asset is sold between

the willing and the knowledgeable parties at the arm’s length transaction and when they

enter the transaction freely. Paragraph B2 defines the entire concept of the fair value

measurement. Whereas Para 36 & Para 11 of the conceptual framework of general purpose

financial statements deals with the fair value accounting. The topic of fair value is subjective

and depends on the judgement being taken in the circumstances of the case. There may be

huge fluctuations in the fair value being computed by different individuals as it all depends

on the assumptions and judgements being used and hence depends on the circumstances of

the case. The transaction costs of selling an asset and that of transferring a liability in the

most advantageous transaction i.e., in the principal market should be directly attributable to

the asset and should meet the following criteria:

1. They should directly arise to the entity

2. They would not have taken place to entity had it not decided to dell asset or transfer

the liability.

Relevant Issues:

The most relevant issue here is the determination of the fair value being different in

different cases and being a subject which depends purely on judgemental decisions, the

value of property, plant and equipment as per fair value may vary hugely everyday. It is

generally used for the financial assets and further, it may be difficult for a non-profit entity

to use the fair value based on the highest and best use as the same property may be used

for varying purposes and market value may change depending on use.

1. Highest & Best Use

The principle of highest and best use comes for the non-financial assets where it is seen that

how the asset can be best utilised by the market participant to generate the highest

economic benefits out of the assets or to sell it to another market participant who can best

utilize the same. It considers 3 factors namely it should be physically possible, financially

feasible and legally acceptable.

2. Application to aged care home

The market value does not depends on the type of the entity or the valuation method being

used. So it should be applied uniformly whether its aged care homes or any profit making

entity based on the market based exit price as on the date of measurement.

3. Two possible uses

Fair valuation is of significant use in many cases like the impairment value assessment of

both the tangible and intangible assets. Secondly, International financial reporting standards

(IFRS) governs the reporting of the financial assets and liabilities in the financials in at fair

value. This is one another major use.

Page 3 of 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

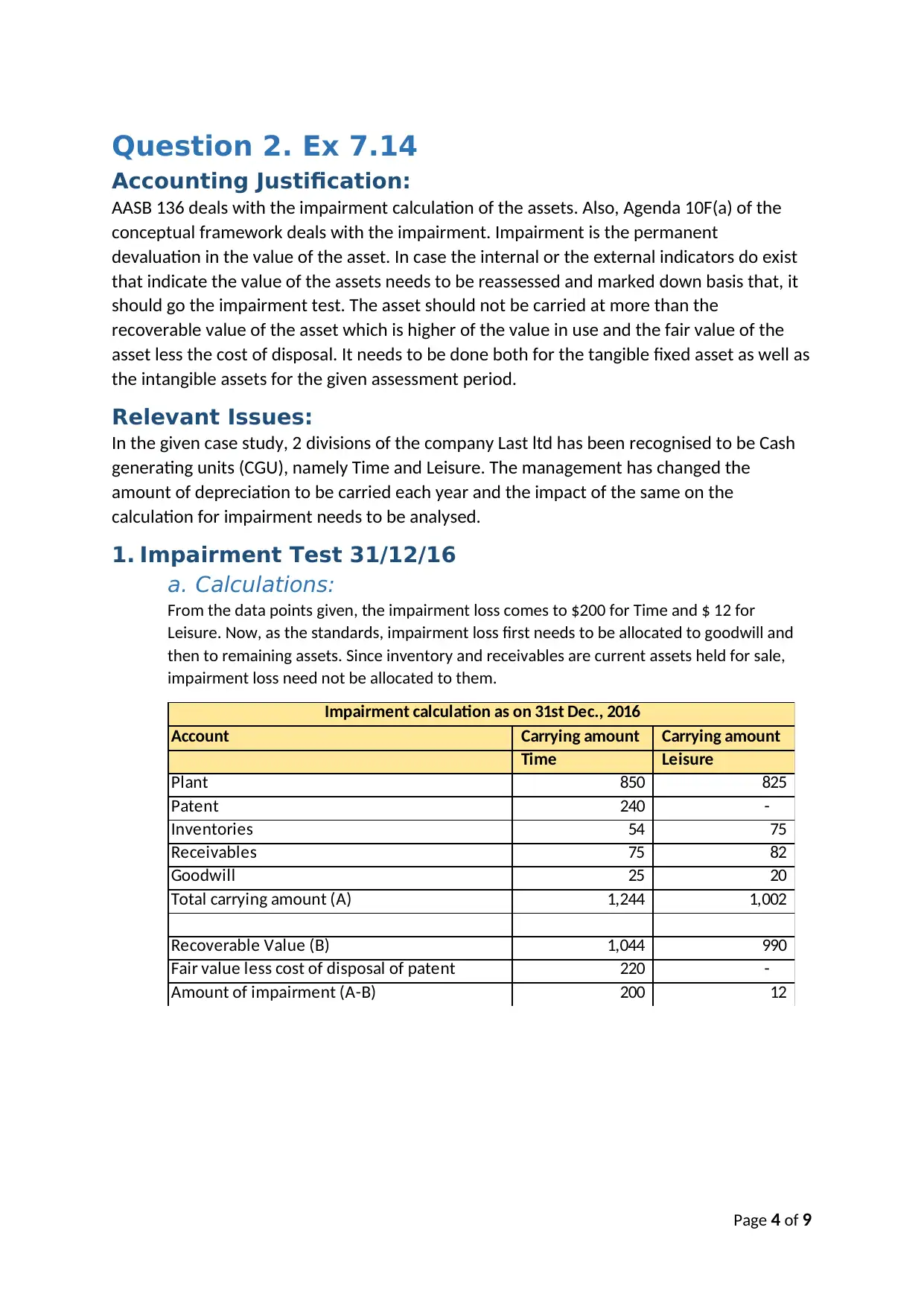

Question 2. Ex 7.14

Accounting Justification:

AASB 136 deals with the impairment calculation of the assets. Also, Agenda 10F(a) of the

conceptual framework deals with the impairment. Impairment is the permanent

devaluation in the value of the asset. In case the internal or the external indicators do exist

that indicate the value of the assets needs to be reassessed and marked down basis that, it

should go the impairment test. The asset should not be carried at more than the

recoverable value of the asset which is higher of the value in use and the fair value of the

asset less the cost of disposal. It needs to be done both for the tangible fixed asset as well as

the intangible assets for the given assessment period.

Relevant Issues:

In the given case study, 2 divisions of the company Last ltd has been recognised to be Cash

generating units (CGU), namely Time and Leisure. The management has changed the

amount of depreciation to be carried each year and the impact of the same on the

calculation for impairment needs to be analysed.

1. Impairment Test 31/12/16

a. Calculations:

From the data points given, the impairment loss comes to $200 for Time and $ 12 for

Leisure. Now, as the standards, impairment loss first needs to be allocated to goodwill and

then to remaining assets. Since inventory and receivables are current assets held for sale,

impairment loss need not be allocated to them.

Account Carrying amount Carrying amount

Time Leisure

Plant 850 825

Patent 240 -

Inventories 54 75

Receivables 75 82

Goodwill 25 20

Total carrying amount (A) 1,244 1,002

Recoverable Value (B) 1,044 990

Fair value less cost of disposal of patent 220 -

Amount of impairment (A-B) 200 12

Impairment calculation as on 31st Dec., 2016

Page 4 of 9

Accounting Justification:

AASB 136 deals with the impairment calculation of the assets. Also, Agenda 10F(a) of the

conceptual framework deals with the impairment. Impairment is the permanent

devaluation in the value of the asset. In case the internal or the external indicators do exist

that indicate the value of the assets needs to be reassessed and marked down basis that, it

should go the impairment test. The asset should not be carried at more than the

recoverable value of the asset which is higher of the value in use and the fair value of the

asset less the cost of disposal. It needs to be done both for the tangible fixed asset as well as

the intangible assets for the given assessment period.

Relevant Issues:

In the given case study, 2 divisions of the company Last ltd has been recognised to be Cash

generating units (CGU), namely Time and Leisure. The management has changed the

amount of depreciation to be carried each year and the impact of the same on the

calculation for impairment needs to be analysed.

1. Impairment Test 31/12/16

a. Calculations:

From the data points given, the impairment loss comes to $200 for Time and $ 12 for

Leisure. Now, as the standards, impairment loss first needs to be allocated to goodwill and

then to remaining assets. Since inventory and receivables are current assets held for sale,

impairment loss need not be allocated to them.

Account Carrying amount Carrying amount

Time Leisure

Plant 850 825

Patent 240 -

Inventories 54 75

Receivables 75 82

Goodwill 25 20

Total carrying amount (A) 1,244 1,002

Recoverable Value (B) 1,044 990

Fair value less cost of disposal of patent 220 -

Amount of impairment (A-B) 200 12

Impairment calculation as on 31st Dec., 2016

Page 4 of 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

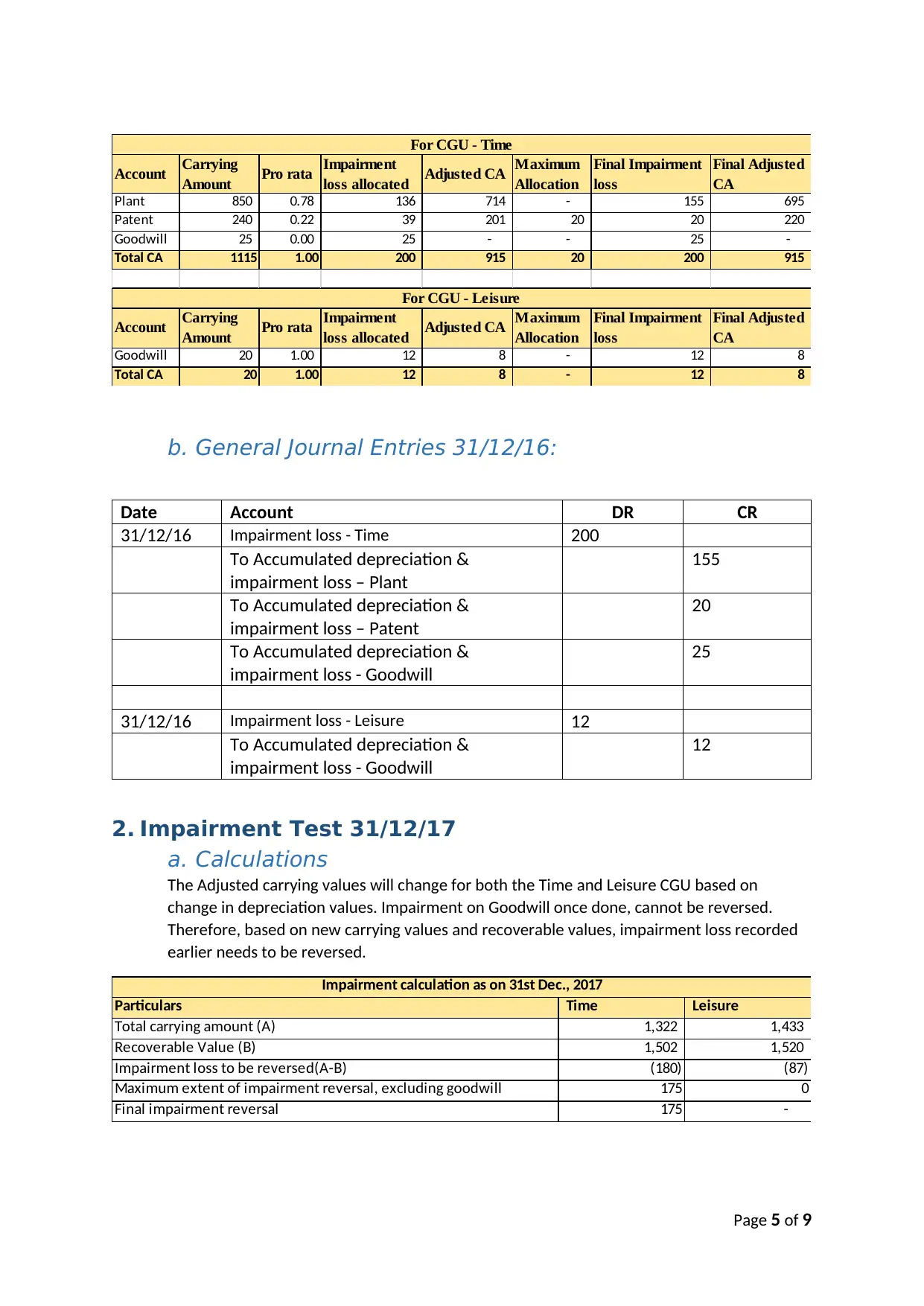

Account Carrying

Amount Pro rata Impairment

loss allocated Adjusted CA Maximum

Allocation

Final Impairment

loss

Final Adjusted

CA

Plant 850 0.78 136 714 - 155 695

Patent 240 0.22 39 201 20 20 220

Goodwill 25 0.00 25 - - 25 -

Total CA 1115 1.00 200 915 20 200 915

Account Carrying

Amount Pro rata Impairment

loss allocated Adjusted CA Maximum

Allocation

Final Impairment

loss

Final Adjusted

CA

Goodwill 20 1.00 12 8 - 12 8

Total CA 20 1.00 12 8 - 12 8

For CGU - Time

For CGU - Leisure

b. General Journal Entries 31/12/16:

Date Account DR CR

31/12/16 Impairment loss - Time 200

To Accumulated depreciation &

impairment loss – Plant

155

To Accumulated depreciation &

impairment loss – Patent

20

To Accumulated depreciation &

impairment loss - Goodwill

25

31/12/16 Impairment loss - Leisure 12

To Accumulated depreciation &

impairment loss - Goodwill

12

2. Impairment Test 31/12/17

a. Calculations

The Adjusted carrying values will change for both the Time and Leisure CGU based on

change in depreciation values. Impairment on Goodwill once done, cannot be reversed.

Therefore, based on new carrying values and recoverable values, impairment loss recorded

earlier needs to be reversed.

Particulars Time Leisure

Total carrying amount (A) 1,322 1,433

Recoverable Value (B) 1,502 1,520

Impairment loss to be reversed(A-B) (180) (87)

Maximum extent of impairment reversal, excluding goodwill 175 0

Final impairment reversal 175 -

Impairment calculation as on 31st Dec., 2017

Page 5 of 9

Amount Pro rata Impairment

loss allocated Adjusted CA Maximum

Allocation

Final Impairment

loss

Final Adjusted

CA

Plant 850 0.78 136 714 - 155 695

Patent 240 0.22 39 201 20 20 220

Goodwill 25 0.00 25 - - 25 -

Total CA 1115 1.00 200 915 20 200 915

Account Carrying

Amount Pro rata Impairment

loss allocated Adjusted CA Maximum

Allocation

Final Impairment

loss

Final Adjusted

CA

Goodwill 20 1.00 12 8 - 12 8

Total CA 20 1.00 12 8 - 12 8

For CGU - Time

For CGU - Leisure

b. General Journal Entries 31/12/16:

Date Account DR CR

31/12/16 Impairment loss - Time 200

To Accumulated depreciation &

impairment loss – Plant

155

To Accumulated depreciation &

impairment loss – Patent

20

To Accumulated depreciation &

impairment loss - Goodwill

25

31/12/16 Impairment loss - Leisure 12

To Accumulated depreciation &

impairment loss - Goodwill

12

2. Impairment Test 31/12/17

a. Calculations

The Adjusted carrying values will change for both the Time and Leisure CGU based on

change in depreciation values. Impairment on Goodwill once done, cannot be reversed.

Therefore, based on new carrying values and recoverable values, impairment loss recorded

earlier needs to be reversed.

Particulars Time Leisure

Total carrying amount (A) 1,322 1,433

Recoverable Value (B) 1,502 1,520

Impairment loss to be reversed(A-B) (180) (87)

Maximum extent of impairment reversal, excluding goodwill 175 0

Final impairment reversal 175 -

Impairment calculation as on 31st Dec., 2017

Page 5 of 9

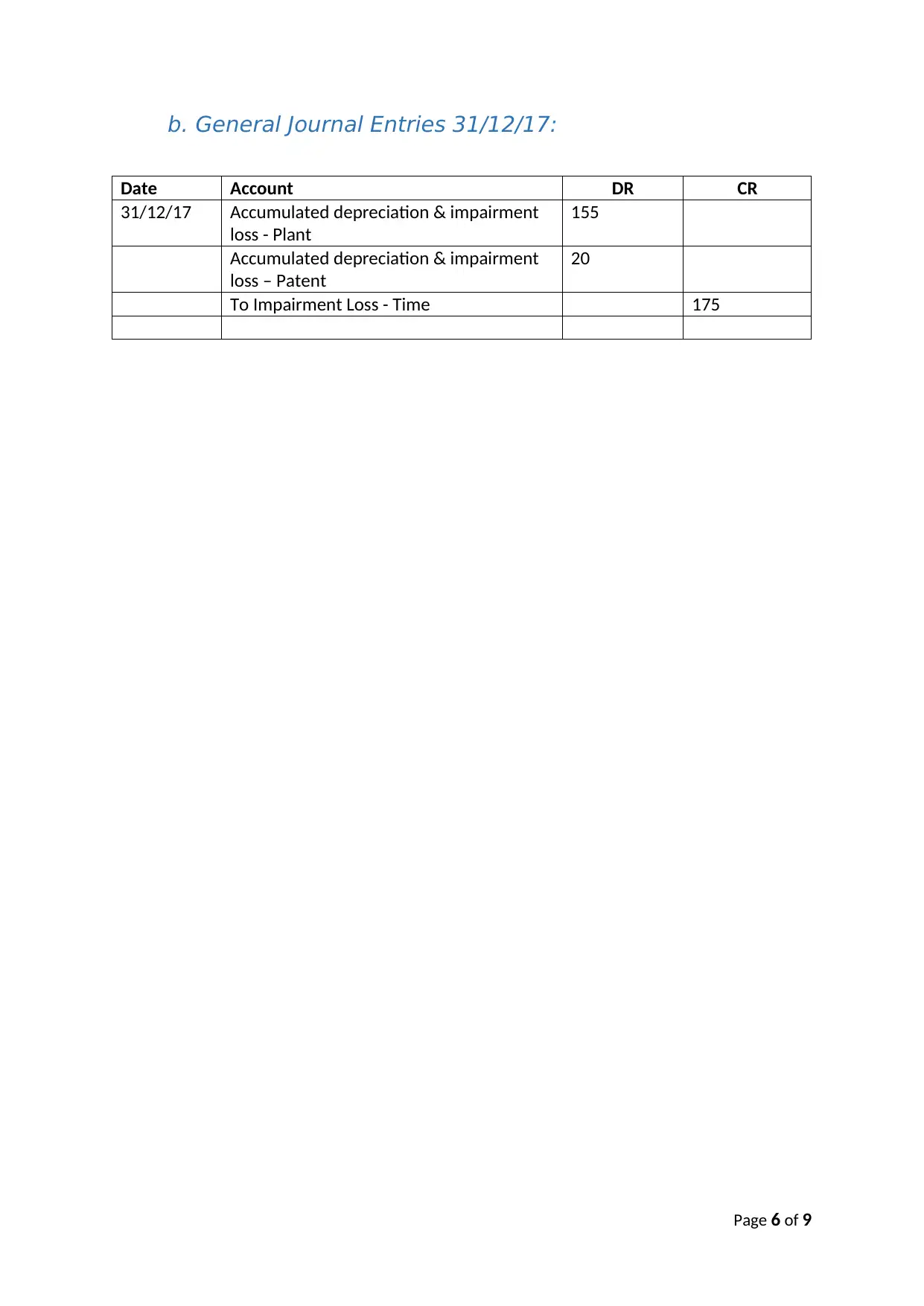

b. General Journal Entries 31/12/17:

Date Account DR CR

31/12/17 Accumulated depreciation & impairment

loss - Plant

155

Accumulated depreciation & impairment

loss – Patent

20

To Impairment Loss - Time 175

Page 6 of 9

Date Account DR CR

31/12/17 Accumulated depreciation & impairment

loss - Plant

155

Accumulated depreciation & impairment

loss – Patent

20

To Impairment Loss - Time 175

Page 6 of 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 3. Case Study 6.1

Accounting Justification:

Accounting for research and development costs is being dealt by the paragraph 8 of the

AASB standard 138 on the intangible assets. The same is being addressed by SSAP 13

accounting for research and development in case of the conceptual framework. This

generally arises in case of the internally generated intangible assets. Research is pre

requisite to the development and is the first original and planned cost that the company

may incur in order to gain the technical knowledge or scientific understanding of the

subject. In research phase, it is seen whether the same will be viable or not and whether it

will have future economic benefits or not. Whereas, development of anything is a post facto

activity coming as a result of due analysis or knowledge or plan or understanding at the time

of the research to in order to produce substantially improved products or come with the

better version of the old process before the production starts. In case the entity is unable to

find the split between the research and development cost in an internally generated

intangible asset, it will simple assume everything to be a part of the research costs only.

Relevant Issues:

The relevant issue here is to distinguish between the research and the development costs

being incurred and then how the same should be treated in the financial books, whether it is

bound by period or by the stages of R&D.

1. Difference between two phases:

The major difference between the research and the development phase is that research

is not certain to give an expected outcome whereas development is. Development of an

asset is only proceeded with by the company when its certain to give the future

economic benefits whereas research may or may not give so.

2. Accounting for Research & Development:

During a research phase the company won’t be able to prove or demonstrate that the

company would be having the future economic benefits from the internally generated

assets and therefore the same should be recognised as a part of the expense as and

when it is incurred. Whereas in the development phase which is further advanced than

the research phase the company would be able to demonstrate that the same has got

future economic benefits and hence the same should be capitalized in the value of the

intangible assets. In case any cost has been incurred by the company during the

development phase, the same needs to be capitalised in value of asset.

3. Decision / Conclusion / Reasons and Justification:

The conclusion or decision based on above is that the research cost should be charged

off to the P&L account whereas the development cost should be capitalized in the

books. The decision to capitalize is backed by whether it is saleable in the open market,

whether the technical feasibility exists, whether the intention was there to create it and

whether or not it can be accurately measured. The entity should be able to demonstrate

that the asset would be able to give probable future economic benefits.

Page 7 of 9

Accounting Justification:

Accounting for research and development costs is being dealt by the paragraph 8 of the

AASB standard 138 on the intangible assets. The same is being addressed by SSAP 13

accounting for research and development in case of the conceptual framework. This

generally arises in case of the internally generated intangible assets. Research is pre

requisite to the development and is the first original and planned cost that the company

may incur in order to gain the technical knowledge or scientific understanding of the

subject. In research phase, it is seen whether the same will be viable or not and whether it

will have future economic benefits or not. Whereas, development of anything is a post facto

activity coming as a result of due analysis or knowledge or plan or understanding at the time

of the research to in order to produce substantially improved products or come with the

better version of the old process before the production starts. In case the entity is unable to

find the split between the research and development cost in an internally generated

intangible asset, it will simple assume everything to be a part of the research costs only.

Relevant Issues:

The relevant issue here is to distinguish between the research and the development costs

being incurred and then how the same should be treated in the financial books, whether it is

bound by period or by the stages of R&D.

1. Difference between two phases:

The major difference between the research and the development phase is that research

is not certain to give an expected outcome whereas development is. Development of an

asset is only proceeded with by the company when its certain to give the future

economic benefits whereas research may or may not give so.

2. Accounting for Research & Development:

During a research phase the company won’t be able to prove or demonstrate that the

company would be having the future economic benefits from the internally generated

assets and therefore the same should be recognised as a part of the expense as and

when it is incurred. Whereas in the development phase which is further advanced than

the research phase the company would be able to demonstrate that the same has got

future economic benefits and hence the same should be capitalized in the value of the

intangible assets. In case any cost has been incurred by the company during the

development phase, the same needs to be capitalised in value of asset.

3. Decision / Conclusion / Reasons and Justification:

The conclusion or decision based on above is that the research cost should be charged

off to the P&L account whereas the development cost should be capitalized in the

books. The decision to capitalize is backed by whether it is saleable in the open market,

whether the technical feasibility exists, whether the intention was there to create it and

whether or not it can be accurately measured. The entity should be able to demonstrate

that the asset would be able to give probable future economic benefits.

Page 7 of 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 4. Ex 9.19

Accounting Justification:

AASB 1056 deals with the defined benefit obligations and superannuation benefits for the

employees. This is a kind of pension benefit being given to the employees in lieu of the

services being rendered by them to the company. The option is given to the employee to

opt for it and this is given as a post retirement benefit to the employees. Furthermore, the

company in the given case has stopped giving such benefit to the new employees though it

continues to do so for the old employees who availed of such a benefit. In case of a defined

contribution plan both the employee as well as the employee contribute to the common

fund and the future benefits is dependent on the investment earnings which keeps on

fluctuating based on the interest rates available in the market.

Relevant Issues:

The relevant issue in the given case has already been mentioned above in the justification.

The related calculations are shown below:

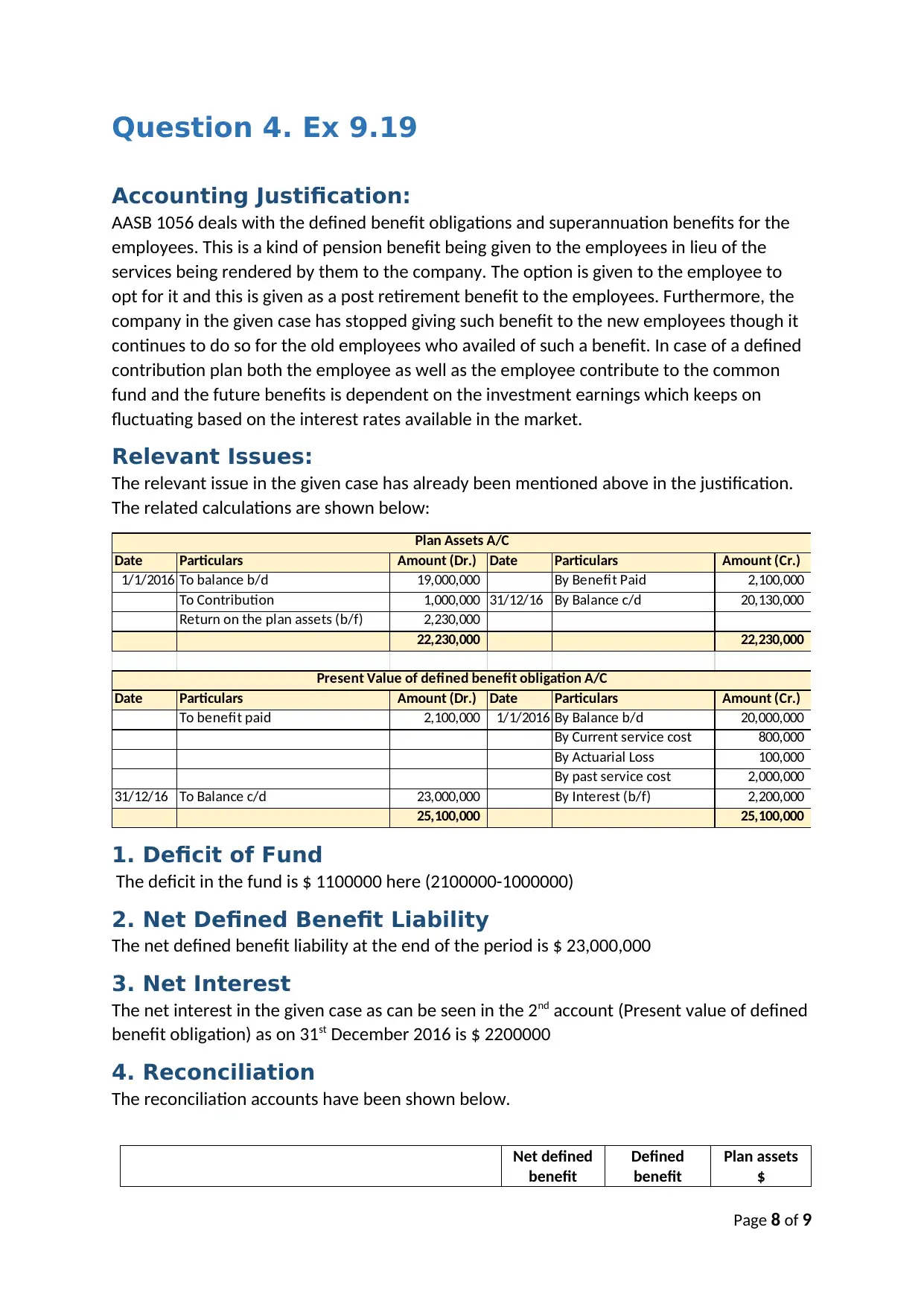

Date Particulars Amount (Dr.) Date Particulars Amount (Cr.)

1/1/2016 To balance b/d 19,000,000 By Benefit Paid 2,100,000

To Contribution 1,000,000 31/12/16 By Balance c/d 20,130,000

Return on the plan assets (b/f) 2,230,000

22,230,000 22,230,000

Date Particulars Amount (Dr.) Date Particulars Amount (Cr.)

To benefit paid 2,100,000 1/1/2016 By Balance b/d 20,000,000

By Current service cost 800,000

By Actuarial Loss 100,000

By past service cost 2,000,000

31/12/16 To Balance c/d 23,000,000 By Interest (b/f) 2,200,000

25,100,000 25,100,000

Plan Assets A/C

Present Value of defined benefit obligation A/C

1. Deficit of Fund

The deficit in the fund is $ 1100000 here (2100000-1000000)

2. Net Defined Benefit Liability

The net defined benefit liability at the end of the period is $ 23,000,000

3. Net Interest

The net interest in the given case as can be seen in the 2nd account (Present value of defined

benefit obligation) as on 31st December 2016 is $ 2200000

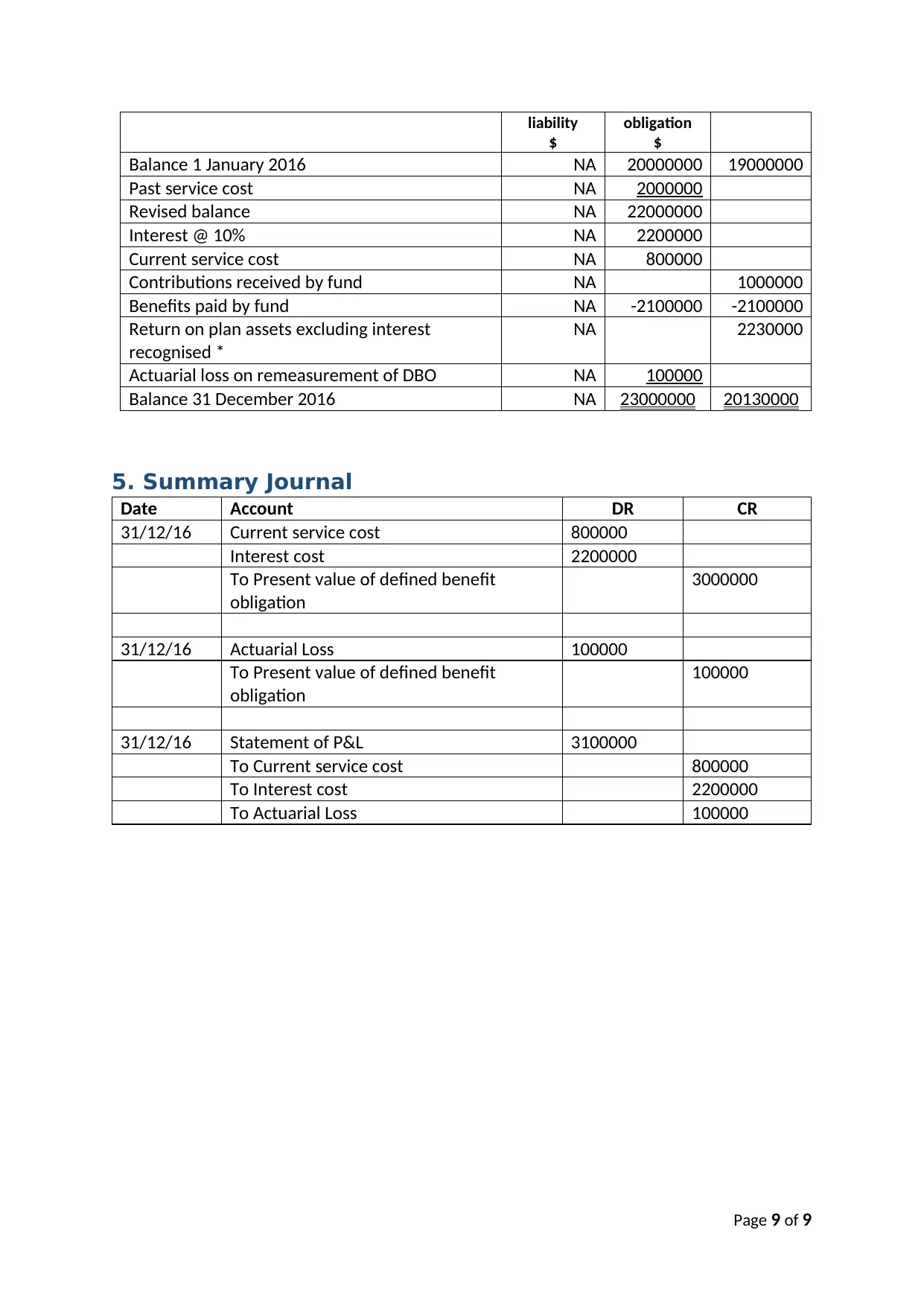

4. Reconciliation

The reconciliation accounts have been shown below.

Net defined

benefit

Defined

benefit

Plan assets

$

Page 8 of 9

Accounting Justification:

AASB 1056 deals with the defined benefit obligations and superannuation benefits for the

employees. This is a kind of pension benefit being given to the employees in lieu of the

services being rendered by them to the company. The option is given to the employee to

opt for it and this is given as a post retirement benefit to the employees. Furthermore, the

company in the given case has stopped giving such benefit to the new employees though it

continues to do so for the old employees who availed of such a benefit. In case of a defined

contribution plan both the employee as well as the employee contribute to the common

fund and the future benefits is dependent on the investment earnings which keeps on

fluctuating based on the interest rates available in the market.

Relevant Issues:

The relevant issue in the given case has already been mentioned above in the justification.

The related calculations are shown below:

Date Particulars Amount (Dr.) Date Particulars Amount (Cr.)

1/1/2016 To balance b/d 19,000,000 By Benefit Paid 2,100,000

To Contribution 1,000,000 31/12/16 By Balance c/d 20,130,000

Return on the plan assets (b/f) 2,230,000

22,230,000 22,230,000

Date Particulars Amount (Dr.) Date Particulars Amount (Cr.)

To benefit paid 2,100,000 1/1/2016 By Balance b/d 20,000,000

By Current service cost 800,000

By Actuarial Loss 100,000

By past service cost 2,000,000

31/12/16 To Balance c/d 23,000,000 By Interest (b/f) 2,200,000

25,100,000 25,100,000

Plan Assets A/C

Present Value of defined benefit obligation A/C

1. Deficit of Fund

The deficit in the fund is $ 1100000 here (2100000-1000000)

2. Net Defined Benefit Liability

The net defined benefit liability at the end of the period is $ 23,000,000

3. Net Interest

The net interest in the given case as can be seen in the 2nd account (Present value of defined

benefit obligation) as on 31st December 2016 is $ 2200000

4. Reconciliation

The reconciliation accounts have been shown below.

Net defined

benefit

Defined

benefit

Plan assets

$

Page 8 of 9

liability

$

obligation

$

Balance 1 January 2016 NA 20000000 19000000

Past service cost NA 2000000

Revised balance NA 22000000

Interest @ 10% NA 2200000

Current service cost NA 800000

Contributions received by fund NA 1000000

Benefits paid by fund NA -2100000 -2100000

Return on plan assets excluding interest

recognised *

NA 2230000

Actuarial loss on remeasurement of DBO NA 100000

Balance 31 December 2016 NA 23000000 20130000

5. Summary Journal

Date Account DR CR

31/12/16 Current service cost 800000

Interest cost 2200000

To Present value of defined benefit

obligation

3000000

31/12/16 Actuarial Loss 100000

To Present value of defined benefit

obligation

100000

31/12/16 Statement of P&L 3100000

To Current service cost 800000

To Interest cost 2200000

To Actuarial Loss 100000

Page 9 of 9

$

obligation

$

Balance 1 January 2016 NA 20000000 19000000

Past service cost NA 2000000

Revised balance NA 22000000

Interest @ 10% NA 2200000

Current service cost NA 800000

Contributions received by fund NA 1000000

Benefits paid by fund NA -2100000 -2100000

Return on plan assets excluding interest

recognised *

NA 2230000

Actuarial loss on remeasurement of DBO NA 100000

Balance 31 December 2016 NA 23000000 20130000

5. Summary Journal

Date Account DR CR

31/12/16 Current service cost 800000

Interest cost 2200000

To Present value of defined benefit

obligation

3000000

31/12/16 Actuarial Loss 100000

To Present value of defined benefit

obligation

100000

31/12/16 Statement of P&L 3100000

To Current service cost 800000

To Interest cost 2200000

To Actuarial Loss 100000

Page 9 of 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.