ACC510 Financial Reporting Task 2 - Major Assignment, Semester 2, 2017

VerifiedAdded on 2020/04/07

|12

|2710

|37

Homework Assignment

AI Summary

This document presents a comprehensive solution to ACC510 Financial Reporting Task 2, focusing on key financial reporting concepts. The assignment addresses the application of AASB 13 concerning fair value measurement, particularly within the context of aged care homes, exploring the implications of highest and best use. It also delves into impairment testing under AASB 136, analyzing impairment losses for both Time and Leisure divisions, including relevant journal entries. Furthermore, the assignment examines intangible assets according to AASB 138, differentiating between research and development phases and discussing the accounting treatment for internally generated assets. Finally, the solution covers employee benefits, specifically defined benefit plans, as per AASB 119, including the calculation of deficit, net defined benefit liability, and net interest, along with a reconciliation and summary journal entries.

ACC510 - Financial Reporting

Task 2 – Major Assignment

Semester 2 - 2017

Student Name:

Student ID #:

Campus:

Task 2 – Major Assignment

Semester 2 - 2017

Student Name:

Student ID #:

Campus:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1.Case Study 3.1.........................................................................................................3

Accounting Justification.........................................................................................................3

Relevant Issues.......................................................................................................................3

Highest & Best Use................................................................................................................3

Application to aged care home...............................................................................................3

Two possible uses...................................................................................................................3

Question- 2.................................................................................................................................4

Accounting Justification:........................................................................................................4

Relevant Issues:......................................................................................................................4

Leisure........................................................................................................................................5

General Journal Entries 31/12/16:..........................................................................................5

Impairment Test 31/12/17......................................................................................................6

Leisure........................................................................................................................................6

Question 3.Case Study 6.1.........................................................................................................7

Accounting Justification:........................................................................................................7

Relevant Issues:......................................................................................................................7

Difference between two phases:.............................................................................................7

Decision / Conclusion / Reasons and Justification:............................................................8

Question 4. Ex 9.19....................................................................................................................8

1. Deficit of Fund...................................................................................................................8

2. Net Defined Benefit Liability.............................................................................................8

3. Net Interest.........................................................................................................................8

4. Reconciliation.....................................................................................................................9

5. Summary Journal..............................................................................................................10

References................................................................................................................................11

Page 2 of 12

Question 1.Case Study 3.1.........................................................................................................3

Accounting Justification.........................................................................................................3

Relevant Issues.......................................................................................................................3

Highest & Best Use................................................................................................................3

Application to aged care home...............................................................................................3

Two possible uses...................................................................................................................3

Question- 2.................................................................................................................................4

Accounting Justification:........................................................................................................4

Relevant Issues:......................................................................................................................4

Leisure........................................................................................................................................5

General Journal Entries 31/12/16:..........................................................................................5

Impairment Test 31/12/17......................................................................................................6

Leisure........................................................................................................................................6

Question 3.Case Study 6.1.........................................................................................................7

Accounting Justification:........................................................................................................7

Relevant Issues:......................................................................................................................7

Difference between two phases:.............................................................................................7

Decision / Conclusion / Reasons and Justification:............................................................8

Question 4. Ex 9.19....................................................................................................................8

1. Deficit of Fund...................................................................................................................8

2. Net Defined Benefit Liability.............................................................................................8

3. Net Interest.........................................................................................................................8

4. Reconciliation.....................................................................................................................9

5. Summary Journal..............................................................................................................10

References................................................................................................................................11

Page 2 of 12

QUESTION 1.CASE STUDY 3.1

Accounting Justification

The main objective of AASB 13 is to specify the meaning of fair value and provide

single standard guidelines for determining fair value. Further, guidelines relating to

disclosures of fair value measurement have also been provided in AASB 13. In accordance

with provisions specified in this standard fair value is the amount which is received or

transferred to a liability in an ordered transaction between market participants (Liang and

Riedl, 2013).

Relevant Issues

For the purpose of valuing financial instruments, financial institutions use fair value

method as part of everyday business. However, in situations of valuation of property, plant

and equipment, the results are very confusing and have changing valuations. Apart this is also

some inconsistencies in the way business units use methods of fair value for an accounting of

tangible assets, which poses a problem of inconsistency.

1. Highest & Best Use

It is important to determine whether the highest and best use of a particular asset

varies from its current use at the date in which the asset is measured. The highest and the

best use of the non-financial asset is considered a market participant is able to generate better

economic benefits than the current uses; or by selling the asset to another participant that can

use the asset better, which is legal and physically possible and financially feasible. In

accordance with the study of Palea (2014), the physical possibility considers the tangible

characteristics of the asset which is to be taken into account for pricing.

2. Application to aged care home

AASB 13 directs the accountants to use asset’s market price considering the highest and

best use of an asset for determination of fair value. However, this poses a problem for not-

for-profit units. If any of the assets of aged care home sold to a participant for building flats

(which will be it's highest and best use), the figure from the valuation will be inflated as there

would be no buyer for the asset used for altruistic purposes. Thus, the fair value may not

reflect the actual value. Thus, the problem of inflated value makes valuation more complex

and requires a lot of judgement on the part of accountants (Hu, Percy and Yao, 2015).

3. Two possible uses

The application of AASB 13 to aged care homes assumes that the entity’s asset (For

Example Flats) is transferred to a market participant. This creates an outstanding liability on

Page 3 of 12

Accounting Justification

The main objective of AASB 13 is to specify the meaning of fair value and provide

single standard guidelines for determining fair value. Further, guidelines relating to

disclosures of fair value measurement have also been provided in AASB 13. In accordance

with provisions specified in this standard fair value is the amount which is received or

transferred to a liability in an ordered transaction between market participants (Liang and

Riedl, 2013).

Relevant Issues

For the purpose of valuing financial instruments, financial institutions use fair value

method as part of everyday business. However, in situations of valuation of property, plant

and equipment, the results are very confusing and have changing valuations. Apart this is also

some inconsistencies in the way business units use methods of fair value for an accounting of

tangible assets, which poses a problem of inconsistency.

1. Highest & Best Use

It is important to determine whether the highest and best use of a particular asset

varies from its current use at the date in which the asset is measured. The highest and the

best use of the non-financial asset is considered a market participant is able to generate better

economic benefits than the current uses; or by selling the asset to another participant that can

use the asset better, which is legal and physically possible and financially feasible. In

accordance with the study of Palea (2014), the physical possibility considers the tangible

characteristics of the asset which is to be taken into account for pricing.

2. Application to aged care home

AASB 13 directs the accountants to use asset’s market price considering the highest and

best use of an asset for determination of fair value. However, this poses a problem for not-

for-profit units. If any of the assets of aged care home sold to a participant for building flats

(which will be it's highest and best use), the figure from the valuation will be inflated as there

would be no buyer for the asset used for altruistic purposes. Thus, the fair value may not

reflect the actual value. Thus, the problem of inflated value makes valuation more complex

and requires a lot of judgement on the part of accountants (Hu, Percy and Yao, 2015).

3. Two possible uses

The application of AASB 13 to aged care homes assumes that the entity’s asset (For

Example Flats) is transferred to a market participant. This creates an outstanding liability on

Page 3 of 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

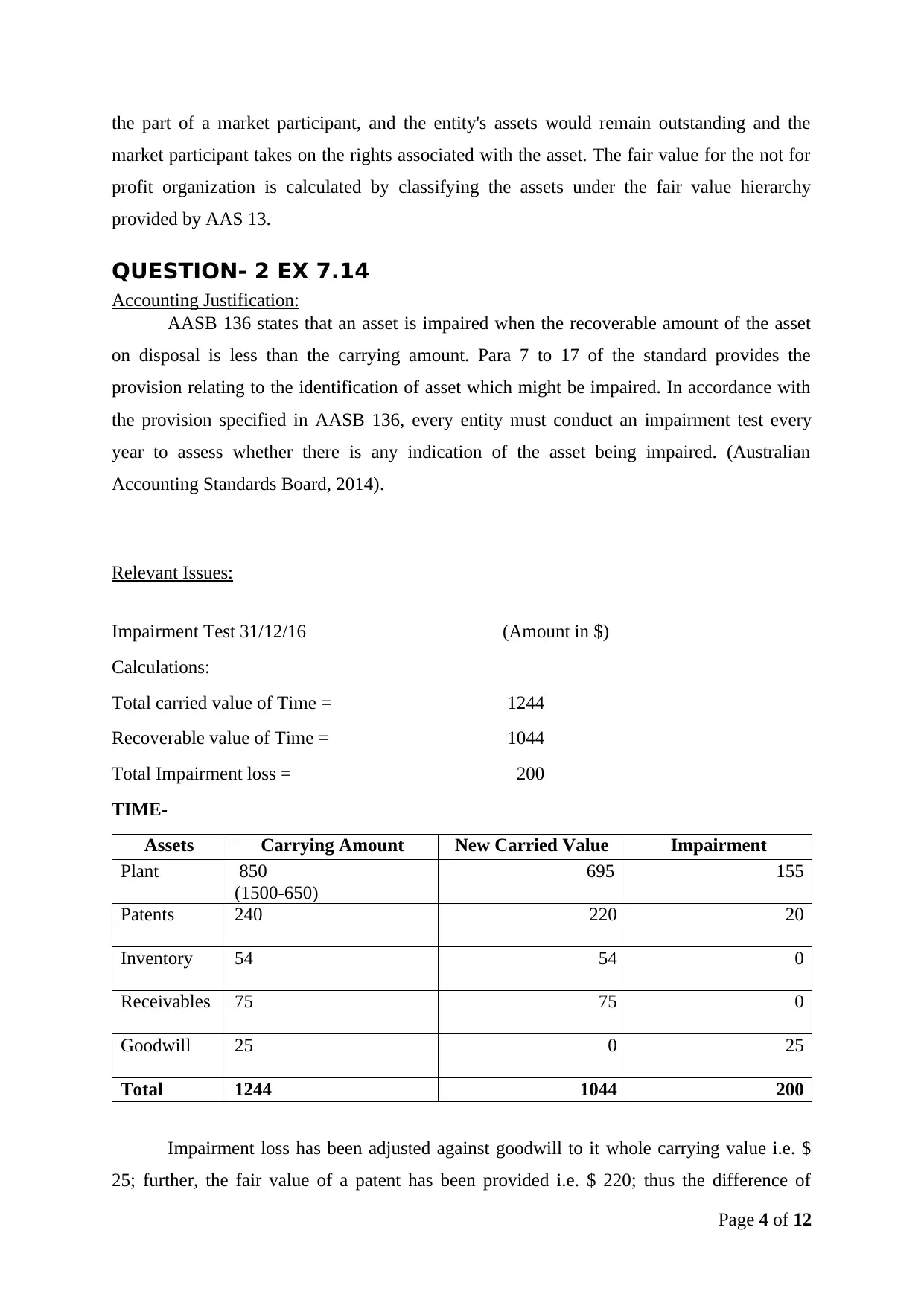

the part of a market participant, and the entity's assets would remain outstanding and the

market participant takes on the rights associated with the asset. The fair value for the not for

profit organization is calculated by classifying the assets under the fair value hierarchy

provided by AAS 13.

QUESTION- 2 EX 7.14

Accounting Justification:

AASB 136 states that an asset is impaired when the recoverable amount of the asset

on disposal is less than the carrying amount. Para 7 to 17 of the standard provides the

provision relating to the identification of asset which might be impaired. In accordance with

the provision specified in AASB 136, every entity must conduct an impairment test every

year to assess whether there is any indication of the asset being impaired. (Australian

Accounting Standards Board, 2014).

Relevant Issues:

Impairment Test 31/12/16 (Amount in $)

Calculations:

Total carried value of Time = 1244

Recoverable value of Time = 1044

Total Impairment loss = 200

TIME-

Assets Carrying Amount New Carried Value Impairment

Plant 850

(1500-650)

695 155

Patents 240 220 20

Inventory 54 54 0

Receivables 75 75 0

Goodwill 25 0 25

Total 1244 1044 200

Impairment loss has been adjusted against goodwill to it whole carrying value i.e. $

25; further, the fair value of a patent has been provided i.e. $ 220; thus the difference of

Page 4 of 12

market participant takes on the rights associated with the asset. The fair value for the not for

profit organization is calculated by classifying the assets under the fair value hierarchy

provided by AAS 13.

QUESTION- 2 EX 7.14

Accounting Justification:

AASB 136 states that an asset is impaired when the recoverable amount of the asset

on disposal is less than the carrying amount. Para 7 to 17 of the standard provides the

provision relating to the identification of asset which might be impaired. In accordance with

the provision specified in AASB 136, every entity must conduct an impairment test every

year to assess whether there is any indication of the asset being impaired. (Australian

Accounting Standards Board, 2014).

Relevant Issues:

Impairment Test 31/12/16 (Amount in $)

Calculations:

Total carried value of Time = 1244

Recoverable value of Time = 1044

Total Impairment loss = 200

TIME-

Assets Carrying Amount New Carried Value Impairment

Plant 850

(1500-650)

695 155

Patents 240 220 20

Inventory 54 54 0

Receivables 75 75 0

Goodwill 25 0 25

Total 1244 1044 200

Impairment loss has been adjusted against goodwill to it whole carrying value i.e. $

25; further, the fair value of a patent has been provided i.e. $ 220; thus the difference of

Page 4 of 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

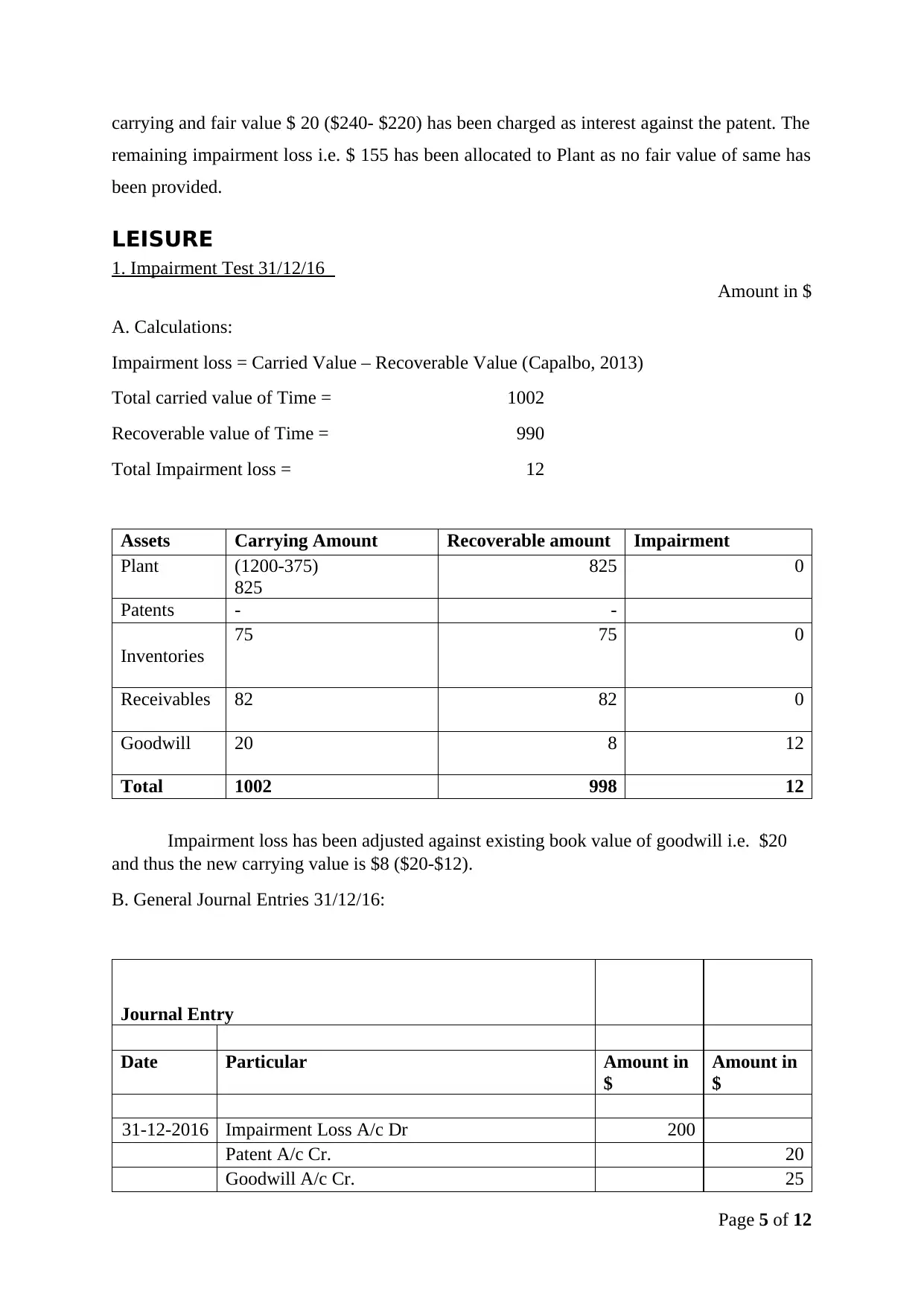

carrying and fair value $ 20 ($240- $220) has been charged as interest against the patent. The

remaining impairment loss i.e. $ 155 has been allocated to Plant as no fair value of same has

been provided.

LEISURE

1. Impairment Test 31/12/16

Amount in $

A. Calculations:

Impairment loss = Carried Value – Recoverable Value (Capalbo, 2013)

Total carried value of Time = 1002

Recoverable value of Time = 990

Total Impairment loss = 12

Assets Carrying Amount Recoverable amount Impairment

Plant (1200-375)

825

825 0

Patents - -

Inventories

75 75 0

Receivables 82 82 0

Goodwill 20 8 12

Total 1002 998 12

Impairment loss has been adjusted against existing book value of goodwill i.e. $20

and thus the new carrying value is $8 ($20-$12).

B. General Journal Entries 31/12/16:

Journal Entry

Date Particular Amount in

$

Amount in

$

31-12-2016 Impairment Loss A/c Dr 200

Patent A/c Cr. 20

Goodwill A/c Cr. 25

Page 5 of 12

remaining impairment loss i.e. $ 155 has been allocated to Plant as no fair value of same has

been provided.

LEISURE

1. Impairment Test 31/12/16

Amount in $

A. Calculations:

Impairment loss = Carried Value – Recoverable Value (Capalbo, 2013)

Total carried value of Time = 1002

Recoverable value of Time = 990

Total Impairment loss = 12

Assets Carrying Amount Recoverable amount Impairment

Plant (1200-375)

825

825 0

Patents - -

Inventories

75 75 0

Receivables 82 82 0

Goodwill 20 8 12

Total 1002 998 12

Impairment loss has been adjusted against existing book value of goodwill i.e. $20

and thus the new carrying value is $8 ($20-$12).

B. General Journal Entries 31/12/16:

Journal Entry

Date Particular Amount in

$

Amount in

$

31-12-2016 Impairment Loss A/c Dr 200

Patent A/c Cr. 20

Goodwill A/c Cr. 25

Page 5 of 12

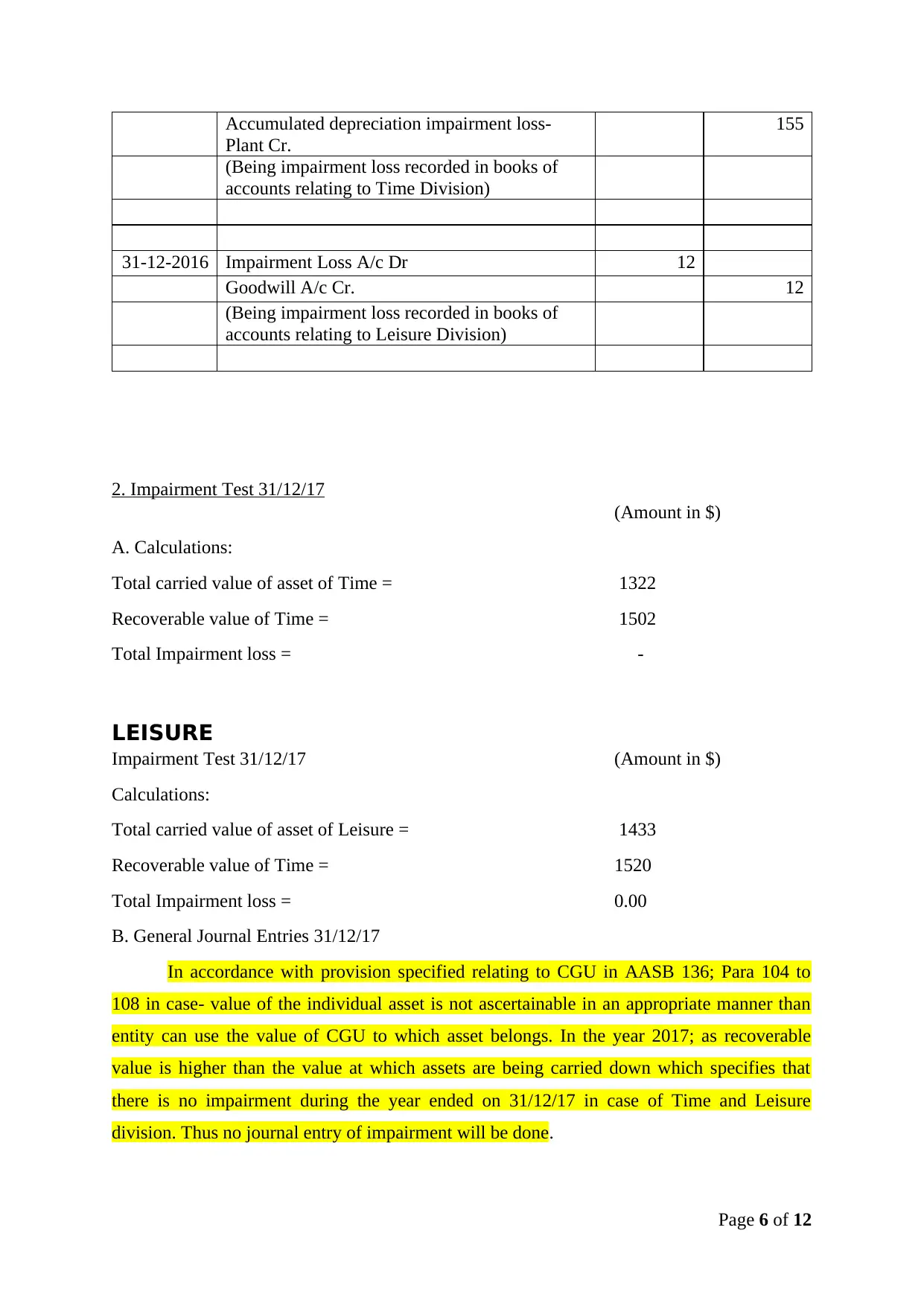

Accumulated depreciation impairment loss-

Plant Cr.

155

(Being impairment loss recorded in books of

accounts relating to Time Division)

31-12-2016 Impairment Loss A/c Dr 12

Goodwill A/c Cr. 12

(Being impairment loss recorded in books of

accounts relating to Leisure Division)

2. Impairment Test 31/12/17

(Amount in $)

A. Calculations:

Total carried value of asset of Time = 1322

Recoverable value of Time = 1502

Total Impairment loss = -

LEISURE

Impairment Test 31/12/17 (Amount in $)

Calculations:

Total carried value of asset of Leisure = 1433

Recoverable value of Time = 1520

Total Impairment loss = 0.00

B. General Journal Entries 31/12/17

In accordance with provision specified relating to CGU in AASB 136; Para 104 to

108 in case- value of the individual asset is not ascertainable in an appropriate manner than

entity can use the value of CGU to which asset belongs. In the year 2017; as recoverable

value is higher than the value at which assets are being carried down which specifies that

there is no impairment during the year ended on 31/12/17 in case of Time and Leisure

division. Thus no journal entry of impairment will be done.

Page 6 of 12

Plant Cr.

155

(Being impairment loss recorded in books of

accounts relating to Time Division)

31-12-2016 Impairment Loss A/c Dr 12

Goodwill A/c Cr. 12

(Being impairment loss recorded in books of

accounts relating to Leisure Division)

2. Impairment Test 31/12/17

(Amount in $)

A. Calculations:

Total carried value of asset of Time = 1322

Recoverable value of Time = 1502

Total Impairment loss = -

LEISURE

Impairment Test 31/12/17 (Amount in $)

Calculations:

Total carried value of asset of Leisure = 1433

Recoverable value of Time = 1520

Total Impairment loss = 0.00

B. General Journal Entries 31/12/17

In accordance with provision specified relating to CGU in AASB 136; Para 104 to

108 in case- value of the individual asset is not ascertainable in an appropriate manner than

entity can use the value of CGU to which asset belongs. In the year 2017; as recoverable

value is higher than the value at which assets are being carried down which specifies that

there is no impairment during the year ended on 31/12/17 in case of Time and Leisure

division. Thus no journal entry of impairment will be done.

Page 6 of 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 3.CASE STUDY 6.1

Accounting Justification:

AASB 138 (Intangible Assets) specifies the provision relating to accounting and

recognizing of an intangible asset. Para 48 to 67 specifies provision regarding internally

generated goodwill and the expense done during research phase and development phase. It

has been provided in the standard that the development phase of an internal project must be

recognized only if the following conditions are fulfilled:

The development of the intangible asset must be technically feasible so that it

is available for further use or sale.

There must be a complete intention of completing the intangible asset and

using or selling it (Hitz, 2013).

The intangible asset is capable of being used.

The intangible asset generates economic benefits in future.

Adequate technical, financial and other resources are available to complete the

development of intangible asset.

The expenditure attributable to intangible of being assets is capable of being

measured during its development phase (Ahmed and Duellman, 2013).

Relevant Issues:

Any expenditure made on the asset before the above criteria are satisfied or the asset

is fully developed, it cannot be recognised as the cost of the asset and remains expensed in

the period in which they were incurred. Thus, the expenditures recognised for an intangible

asset which is internally generated does not comprise of the entire cost. In addition to this

problem, IAS 38 also forbids costs capitalisation of some intangible assets that are internally

generated, in spite of them meeting the criteria of development mentioned above.

1. Difference between two phases:

The research phase is the planned investigation undertaken with the intention of gaining

scientific or technical knowledge and understanding. The research phase relates to an in-

process development attained separately by an entity or in a business combination which is

recognised as an intangible asset and the asset is incurred only after the completion of that

project(André, Dionysiou and Tsalavoutas, 2016). The development phase is the application

of the findings of the research or other knowledge planned or designed for the creation of an

asset.

Page 7 of 12

Accounting Justification:

AASB 138 (Intangible Assets) specifies the provision relating to accounting and

recognizing of an intangible asset. Para 48 to 67 specifies provision regarding internally

generated goodwill and the expense done during research phase and development phase. It

has been provided in the standard that the development phase of an internal project must be

recognized only if the following conditions are fulfilled:

The development of the intangible asset must be technically feasible so that it

is available for further use or sale.

There must be a complete intention of completing the intangible asset and

using or selling it (Hitz, 2013).

The intangible asset is capable of being used.

The intangible asset generates economic benefits in future.

Adequate technical, financial and other resources are available to complete the

development of intangible asset.

The expenditure attributable to intangible of being assets is capable of being

measured during its development phase (Ahmed and Duellman, 2013).

Relevant Issues:

Any expenditure made on the asset before the above criteria are satisfied or the asset

is fully developed, it cannot be recognised as the cost of the asset and remains expensed in

the period in which they were incurred. Thus, the expenditures recognised for an intangible

asset which is internally generated does not comprise of the entire cost. In addition to this

problem, IAS 38 also forbids costs capitalisation of some intangible assets that are internally

generated, in spite of them meeting the criteria of development mentioned above.

1. Difference between two phases:

The research phase is the planned investigation undertaken with the intention of gaining

scientific or technical knowledge and understanding. The research phase relates to an in-

process development attained separately by an entity or in a business combination which is

recognised as an intangible asset and the asset is incurred only after the completion of that

project(André, Dionysiou and Tsalavoutas, 2016). The development phase is the application

of the findings of the research or other knowledge planned or designed for the creation of an

asset.

Page 7 of 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Accounting for Research & Development:

The requirement to capitalize costs associated with development phase after specified

criteria are met under the accounting provisions of internally generated assets could

considerably affect profit and have long-term effects for the organization. As per AASB 138,

an entity is required to assess the useful life of its intangible assets (R&D). If the assets have

definite life amortisation applies on the estimated useful life of the asset. 20 years is

rebuttable assumption of the maximum amortisation period. Those assets which have an

indefinite life are not amortised but are assessed annually for adjustments of impairment

(Dinh and et.al. 2015).

3. Decision / Conclusion / Reasons and Justification:

AAAB 138 is applicable on those companies which have medium to long-term contracts of

research and development and also to those companies that operate in the technology sector.

Such companies may need to consider that the provisions are followed with a view to

upgrading the level of data in order to give the information required by AASB.

QUESTION 4. EX 9.19

Accounting Justification

AASB 119 deals with the provision relating to employee benefits. Para 57 of the specified

standard provides steps to be involved in defined benefit plans by an organization. The steps

comprise ascertainment of deficit or surplus; ascertaining the amount of net defined benefit

liability. Further, the amount relating to current service cost, net interest on defined benefit

liability and past service gain is to be recognized in profit and loss account. Lastly, net

defined benefit liability is ascertained which comprises actuarial gain or losses, return on plan

asset (as per Para 130) and change in asset ceiling (as per Para 64).

1. Deficit of Fund

Particular Amount In $

000

Value of defined benefit obligation as on 31-12-16 23000

Fair value of defined benefit obligation as on 31-12-16 (20130)

Deficit 2870

2. Net Defined Benefit Liability

Page 8 of 12

The requirement to capitalize costs associated with development phase after specified

criteria are met under the accounting provisions of internally generated assets could

considerably affect profit and have long-term effects for the organization. As per AASB 138,

an entity is required to assess the useful life of its intangible assets (R&D). If the assets have

definite life amortisation applies on the estimated useful life of the asset. 20 years is

rebuttable assumption of the maximum amortisation period. Those assets which have an

indefinite life are not amortised but are assessed annually for adjustments of impairment

(Dinh and et.al. 2015).

3. Decision / Conclusion / Reasons and Justification:

AAAB 138 is applicable on those companies which have medium to long-term contracts of

research and development and also to those companies that operate in the technology sector.

Such companies may need to consider that the provisions are followed with a view to

upgrading the level of data in order to give the information required by AASB.

QUESTION 4. EX 9.19

Accounting Justification

AASB 119 deals with the provision relating to employee benefits. Para 57 of the specified

standard provides steps to be involved in defined benefit plans by an organization. The steps

comprise ascertainment of deficit or surplus; ascertaining the amount of net defined benefit

liability. Further, the amount relating to current service cost, net interest on defined benefit

liability and past service gain is to be recognized in profit and loss account. Lastly, net

defined benefit liability is ascertained which comprises actuarial gain or losses, return on plan

asset (as per Para 130) and change in asset ceiling (as per Para 64).

1. Deficit of Fund

Particular Amount In $

000

Value of defined benefit obligation as on 31-12-16 23000

Fair value of defined benefit obligation as on 31-12-16 (20130)

Deficit 2870

2. Net Defined Benefit Liability

Page 8 of 12

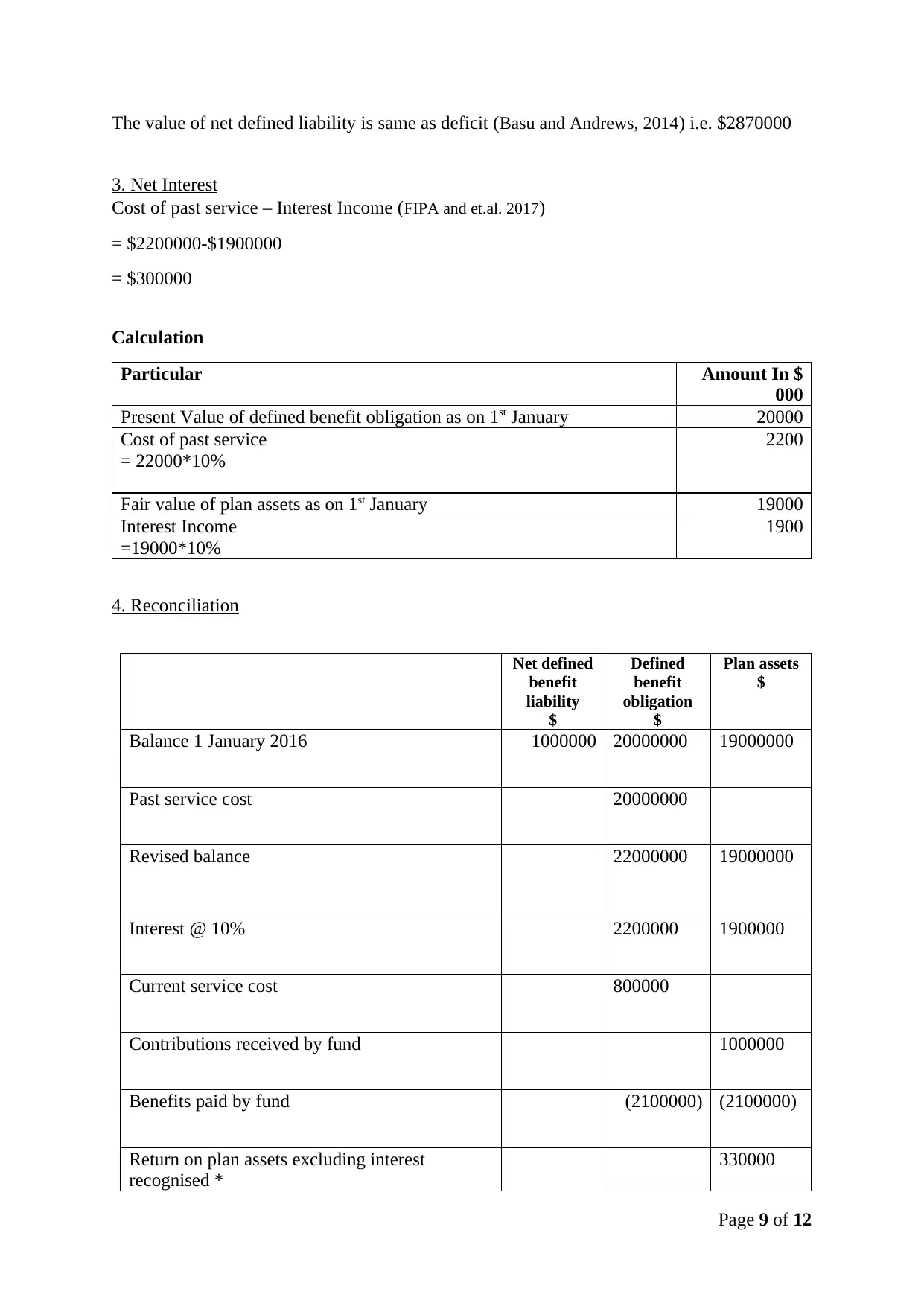

The value of net defined liability is same as deficit (Basu and Andrews, 2014) i.e. $2870000

3. Net Interest

Cost of past service – Interest Income (FIPA and et.al. 2017)

= $2200000-$1900000

= $300000

Calculation

Particular Amount In $

000

Present Value of defined benefit obligation as on 1st January 20000

Cost of past service

= 22000*10%

2200

Fair value of plan assets as on 1st January 19000

Interest Income

=19000*10%

1900

4. Reconciliation

Net defined

benefit

liability

$

Defined

benefit

obligation

$

Plan assets

$

Balance 1 January 2016 1000000 20000000 19000000

Past service cost 20000000

Revised balance 22000000 19000000

Interest @ 10% 2200000 1900000

Current service cost 800000

Contributions received by fund 1000000

Benefits paid by fund (2100000) (2100000)

Return on plan assets excluding interest

recognised *

330000

Page 9 of 12

3. Net Interest

Cost of past service – Interest Income (FIPA and et.al. 2017)

= $2200000-$1900000

= $300000

Calculation

Particular Amount In $

000

Present Value of defined benefit obligation as on 1st January 20000

Cost of past service

= 22000*10%

2200

Fair value of plan assets as on 1st January 19000

Interest Income

=19000*10%

1900

4. Reconciliation

Net defined

benefit

liability

$

Defined

benefit

obligation

$

Plan assets

$

Balance 1 January 2016 1000000 20000000 19000000

Past service cost 20000000

Revised balance 22000000 19000000

Interest @ 10% 2200000 1900000

Current service cost 800000

Contributions received by fund 1000000

Benefits paid by fund (2100000) (2100000)

Return on plan assets excluding interest

recognised *

330000

Page 9 of 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

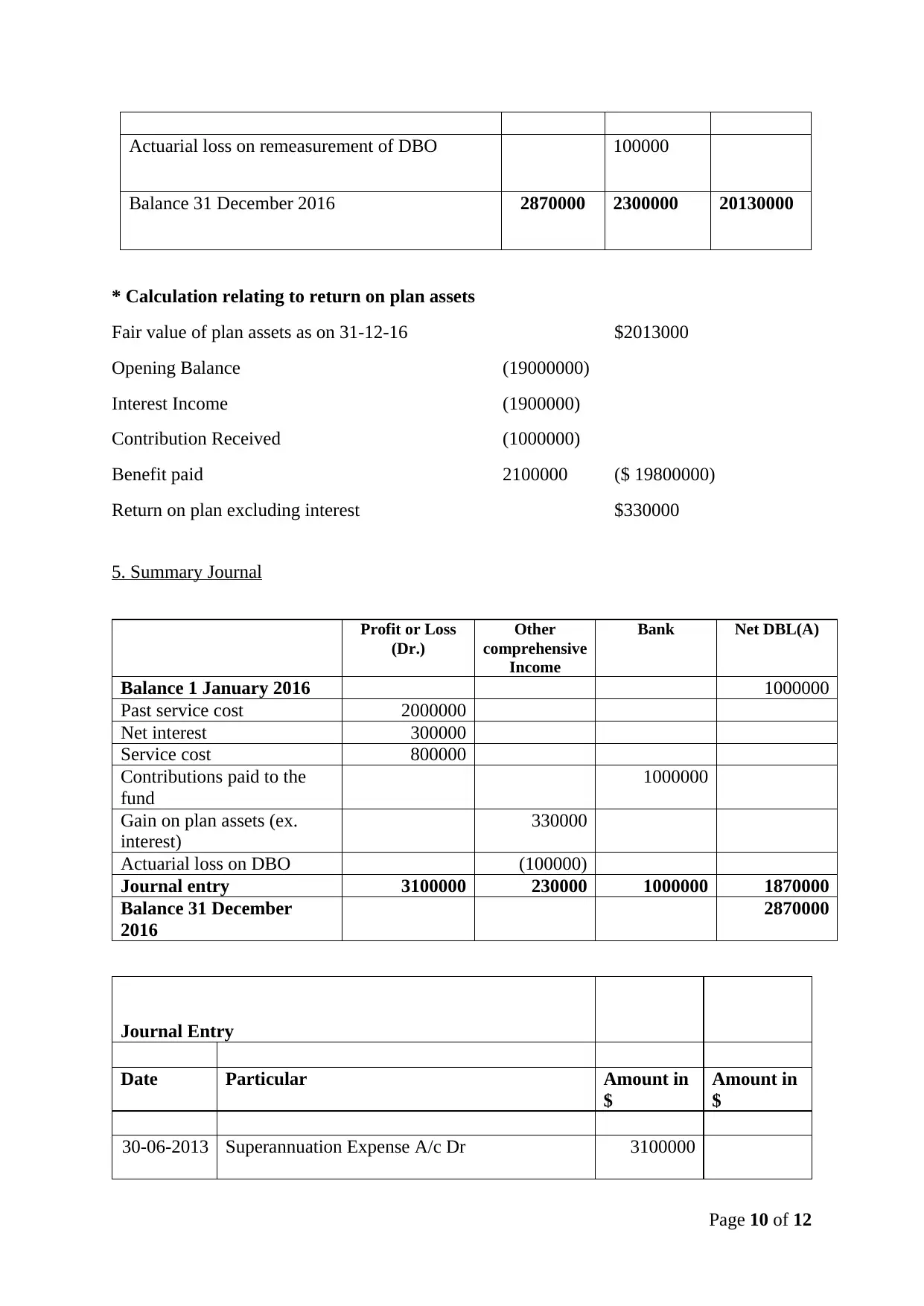

Actuarial loss on remeasurement of DBO 100000

Balance 31 December 2016 2870000 2300000 20130000

* Calculation relating to return on plan assets

Fair value of plan assets as on 31-12-16 $2013000

Opening Balance (19000000)

Interest Income (1900000)

Contribution Received (1000000)

Benefit paid 2100000 ($ 19800000)

Return on plan excluding interest $330000

5. Summary Journal

Profit or Loss

(Dr.)

Other

comprehensive

Income

Bank Net DBL(A)

Balance 1 January 2016 1000000

Past service cost 2000000

Net interest 300000

Service cost 800000

Contributions paid to the

fund

1000000

Gain on plan assets (ex.

interest)

330000

Actuarial loss on DBO (100000)

Journal entry 3100000 230000 1000000 1870000

Balance 31 December

2016

2870000

Journal Entry

Date Particular Amount in

$

Amount in

$

30-06-2013 Superannuation Expense A/c Dr 3100000

Page 10 of 12

Balance 31 December 2016 2870000 2300000 20130000

* Calculation relating to return on plan assets

Fair value of plan assets as on 31-12-16 $2013000

Opening Balance (19000000)

Interest Income (1900000)

Contribution Received (1000000)

Benefit paid 2100000 ($ 19800000)

Return on plan excluding interest $330000

5. Summary Journal

Profit or Loss

(Dr.)

Other

comprehensive

Income

Bank Net DBL(A)

Balance 1 January 2016 1000000

Past service cost 2000000

Net interest 300000

Service cost 800000

Contributions paid to the

fund

1000000

Gain on plan assets (ex.

interest)

330000

Actuarial loss on DBO (100000)

Journal entry 3100000 230000 1000000 1870000

Balance 31 December

2016

2870000

Journal Entry

Date Particular Amount in

$

Amount in

$

30-06-2013 Superannuation Expense A/c Dr 3100000

Page 10 of 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

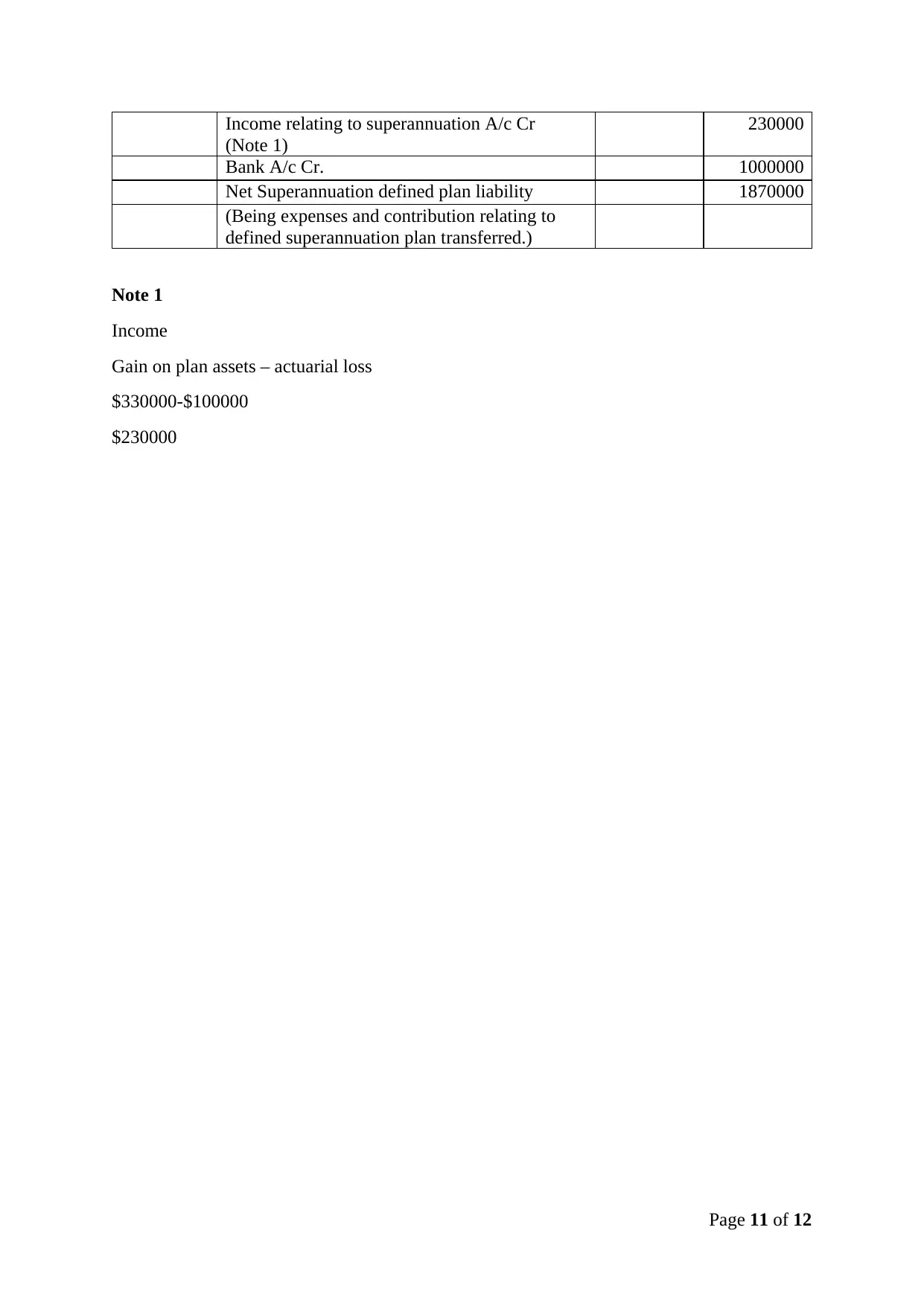

Income relating to superannuation A/c Cr

(Note 1)

230000

Bank A/c Cr. 1000000

Net Superannuation defined plan liability 1870000

(Being expenses and contribution relating to

defined superannuation plan transferred.)

Note 1

Income

Gain on plan assets – actuarial loss

$330000-$100000

$230000

Page 11 of 12

(Note 1)

230000

Bank A/c Cr. 1000000

Net Superannuation defined plan liability 1870000

(Being expenses and contribution relating to

defined superannuation plan transferred.)

Note 1

Income

Gain on plan assets – actuarial loss

$330000-$100000

$230000

Page 11 of 12

REFERENCES

Books and Journal

Ahmed, A.S. &Duellman, S., 2013. Managerial overconfidence and accounting

conservatism. Journal of Accounting Research, 51(1), Pp.1-30.

André, P., Dionysiou, D. &Tsalavoutas, I., 2016. Mandated disclosures of IAS 36 and IAS

38: value relevance and analysts’ forecasts. Working paper. HEC, Lausanne.

Basu, A. &Andrews, S. 2014. Asset allocation policy, returns and expenses of superannuation

funds: recent evidence based on default options. Australian Economic Review, 47(1), Pp.63-77.

Capalbo, F., 2013. Impairment of Assets.

Collings, S., Impairment of Assets. Interpretation and Application of UK GAAP: For Accounting Periods

Commencing On or After 1 January 2015, Pp.241-259.

Dinh, T., Eierle, B., Schultze, W. &Steeger, L., 2015. Research and development,

uncertainty, and analysts’ forecasts: The case of IAS 38. Journal of International Financial

Management & Accounting, 26(3). Pp.257-293.

FIPA, M.T.G., Stylianou, M.V., Carey, P., Cooper, B., Tanewski, G. &Mroczkowski, N.,

2017. Accounting of Defined benefit plan. IPA-Deakin SME Research Centre.

Hitz, J.M., 2013. Capitalize or expense? Recent evidence on the accounting for intangible

assets under IAS 38 by STOXX 200

firms. ZeitschriftfürInternationaleRechnungslegungIRZ, 5, Pp.319-324.

Hu, F., Percy, M. &Yao, D., 2015. Asset revaluations and earnings management: Evidence

from Australian companies. Corporate Ownership and Control, 13(1), Pp.930-939.

International Accounting Standards Board, 2014. International accounting standards IAS 36,

Impairment of assets, and IAS 38, Intangible assets. IASCF Publications Dept.

Liang, L. &Riedl, E.J., 2013. The effect of fair value versus historical cost reporting model

on analyst forecast accuracy. The Accounting Review, 89(3), Pp.1151-1177.

Palea, V., 2014. Fair value accounting and its usefulness to financial statement users. Journal

of Financial Reporting and Accounting, 12(2), Pp.102-116.

Page 12 of 12

Books and Journal

Ahmed, A.S. &Duellman, S., 2013. Managerial overconfidence and accounting

conservatism. Journal of Accounting Research, 51(1), Pp.1-30.

André, P., Dionysiou, D. &Tsalavoutas, I., 2016. Mandated disclosures of IAS 36 and IAS

38: value relevance and analysts’ forecasts. Working paper. HEC, Lausanne.

Basu, A. &Andrews, S. 2014. Asset allocation policy, returns and expenses of superannuation

funds: recent evidence based on default options. Australian Economic Review, 47(1), Pp.63-77.

Capalbo, F., 2013. Impairment of Assets.

Collings, S., Impairment of Assets. Interpretation and Application of UK GAAP: For Accounting Periods

Commencing On or After 1 January 2015, Pp.241-259.

Dinh, T., Eierle, B., Schultze, W. &Steeger, L., 2015. Research and development,

uncertainty, and analysts’ forecasts: The case of IAS 38. Journal of International Financial

Management & Accounting, 26(3). Pp.257-293.

FIPA, M.T.G., Stylianou, M.V., Carey, P., Cooper, B., Tanewski, G. &Mroczkowski, N.,

2017. Accounting of Defined benefit plan. IPA-Deakin SME Research Centre.

Hitz, J.M., 2013. Capitalize or expense? Recent evidence on the accounting for intangible

assets under IAS 38 by STOXX 200

firms. ZeitschriftfürInternationaleRechnungslegungIRZ, 5, Pp.319-324.

Hu, F., Percy, M. &Yao, D., 2015. Asset revaluations and earnings management: Evidence

from Australian companies. Corporate Ownership and Control, 13(1), Pp.930-939.

International Accounting Standards Board, 2014. International accounting standards IAS 36,

Impairment of assets, and IAS 38, Intangible assets. IASCF Publications Dept.

Liang, L. &Riedl, E.J., 2013. The effect of fair value versus historical cost reporting model

on analyst forecast accuracy. The Accounting Review, 89(3), Pp.1151-1177.

Palea, V., 2014. Fair value accounting and its usefulness to financial statement users. Journal

of Financial Reporting and Accounting, 12(2), Pp.102-116.

Page 12 of 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.