Financial Accounting Principles and Practice

VerifiedAdded on 2020/03/04

|26

|1529

|41

AI Summary

This assignment delves into fundamental principles of financial accounting. It explores debit and credit balances, adjustment entries (including accrued revenues and deferred expenses), types of liabilities, current ratios, and the construction of financial statements. Students are guided through manual and spreadsheet solutions, showcasing their understanding of these concepts.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Question 1 Solution

Plagiarism is the act of taking someone else’s work or ideas and passing them of as your own,

without their consent or knowledge (Oxford Dictionary, 2017). Plagiarism and collusion is unfair

to honest students because they have put in the time and effort to produce this work yet plagiarist

just copy and paste. Plagiarism is therefore wrong. (Bishop, 2017).

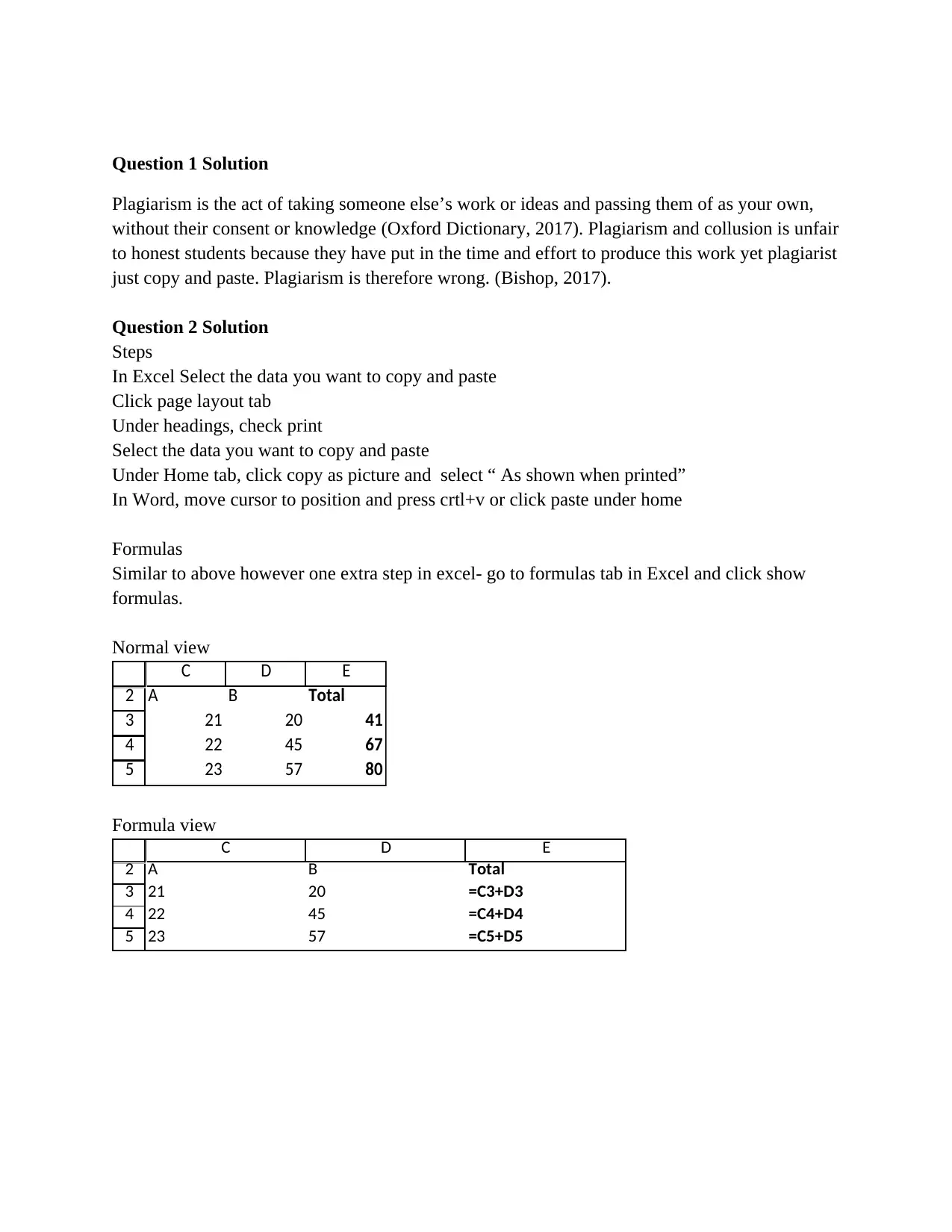

Question 2 Solution

Steps

In Excel Select the data you want to copy and paste

Click page layout tab

Under headings, check print

Select the data you want to copy and paste

Under Home tab, click copy as picture and select “ As shown when printed”

In Word, move cursor to position and press crtl+v or click paste under home

Formulas

Similar to above however one extra step in excel- go to formulas tab in Excel and click show

formulas.

Normal view

2

3

4

5

C D E

A B Total

21 20 41

22 45 67

23 57 80

Formula view

2

3

4

5

C D E

A B Total

21 20 =C3+D3

22 45 =C4+D4

23 57 =C5+D5

Plagiarism is the act of taking someone else’s work or ideas and passing them of as your own,

without their consent or knowledge (Oxford Dictionary, 2017). Plagiarism and collusion is unfair

to honest students because they have put in the time and effort to produce this work yet plagiarist

just copy and paste. Plagiarism is therefore wrong. (Bishop, 2017).

Question 2 Solution

Steps

In Excel Select the data you want to copy and paste

Click page layout tab

Under headings, check print

Select the data you want to copy and paste

Under Home tab, click copy as picture and select “ As shown when printed”

In Word, move cursor to position and press crtl+v or click paste under home

Formulas

Similar to above however one extra step in excel- go to formulas tab in Excel and click show

formulas.

Normal view

2

3

4

5

C D E

A B Total

21 20 41

22 45 67

23 57 80

Formula view

2

3

4

5

C D E

A B Total

21 20 =C3+D3

22 45 =C4+D4

23 57 =C5+D5

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Question 3 Solution: Websites relative to Accounting

https://www.accountingcoach.com/ This is a free learning website that is suited for students,

book keepers and businesses.

http://investopedia.com This website provides financial content, marketing news

and education

http:// www.aasb.gov.au This body sets the standards for Australian accounting

http://www.pwc.com/ This website offers financial services, however it can

also be used as a resourceful site for information on the

economy and trends.

http://www.cpaaustralia.com This website provides education, training and technical

support to accountants

Question 4 Solutions

CPA Accounting Australia Resource – Understanding Annual Reports

The website has provided guidelines on how to interpret Australian, Malaysia and New Zealand

financial reports to clients and their significance. (CPA Australia, 2017)

Question 5 Solutions

At my current work environment, my employer operates up to 100 workstations to enhance

communications, greater productivity, research, IT and administrative functions. They systems

accompanied by other work alone computers, are connected to the Info-set network, which is our

companies network, and then to the internet. Intel, Dell, Mac and Toshiba are amongst the

prominent vendors of the workstations. The systems are all connected together to the backbone

of the company network.

The administration network comprises of a number of virtual machines. The machines main

purpose is timesharing and mail servicing and provides database warehousing. The computing

environment differs from department to department. For example, the administration department

uses a blend of Macs and PCs. The programming department of the company uses access

platforms such as SGI, HP, IBM, DEC, Mac and Intel.

https://www.accountingcoach.com/ This is a free learning website that is suited for students,

book keepers and businesses.

http://investopedia.com This website provides financial content, marketing news

and education

http:// www.aasb.gov.au This body sets the standards for Australian accounting

http://www.pwc.com/ This website offers financial services, however it can

also be used as a resourceful site for information on the

economy and trends.

http://www.cpaaustralia.com This website provides education, training and technical

support to accountants

Question 4 Solutions

CPA Accounting Australia Resource – Understanding Annual Reports

The website has provided guidelines on how to interpret Australian, Malaysia and New Zealand

financial reports to clients and their significance. (CPA Australia, 2017)

Question 5 Solutions

At my current work environment, my employer operates up to 100 workstations to enhance

communications, greater productivity, research, IT and administrative functions. They systems

accompanied by other work alone computers, are connected to the Info-set network, which is our

companies network, and then to the internet. Intel, Dell, Mac and Toshiba are amongst the

prominent vendors of the workstations. The systems are all connected together to the backbone

of the company network.

The administration network comprises of a number of virtual machines. The machines main

purpose is timesharing and mail servicing and provides database warehousing. The computing

environment differs from department to department. For example, the administration department

uses a blend of Macs and PCs. The programming department of the company uses access

platforms such as SGI, HP, IBM, DEC, Mac and Intel.

The network is switched and consists of ten VLANs. It is comprised of HP and Juniper switches

and routers. The building therefore has gigabit networking and a connection to the computer

backbone.

The Company has a networked workstation for everyone within the office. The networked

workstations are for senior staff and selected junior staff with various workloads. Most of the

workstations run a version of Unix though some of the staff use Mac.

In case of breakdown or failure of the IT functions, there are additional two machines, Xenons,

which have the responsibility of handling office mail and reading newsgroups.

A feature of our working environment is that you get an email address that is potentially

permanent with a domain name. The email address can forward your mail to whichever

computer you are using to read your email.

In conclusion, my current computing environment appears complex, but it has ensured an

efficient work environment for all staff members, enabling them to work in the office and

remotely.

and routers. The building therefore has gigabit networking and a connection to the computer

backbone.

The Company has a networked workstation for everyone within the office. The networked

workstations are for senior staff and selected junior staff with various workloads. Most of the

workstations run a version of Unix though some of the staff use Mac.

In case of breakdown or failure of the IT functions, there are additional two machines, Xenons,

which have the responsibility of handling office mail and reading newsgroups.

A feature of our working environment is that you get an email address that is potentially

permanent with a domain name. The email address can forward your mail to whichever

computer you are using to read your email.

In conclusion, my current computing environment appears complex, but it has ensured an

efficient work environment for all staff members, enabling them to work in the office and

remotely.

Question 6 Solutions- Business Report

1. Introduction

1.1 Background

ABC Learning Company was founded in 1988 as a stable company. In 2001, the

Australian government introduced the Childcare Benefit Rebate System.

Following this directive, ABC acquired child care centers across the country and

went through a massive growth expansion with share prices reaching $8.60.

However, this growth did not last. By the end of 2007, the company went through

a drastic change of events. ABC’s assets and share prices fell to $0.54 causing it

to be placed under Administrators in November 2008 (Koch, 2009).

1.2 Purpose

The Purpose of this business report is to provide information on ABC’s Financial

Reports, and explore the key lessons from their downfall and 3 ethical issues.

2. Major Financial Reports

The major financial reports are-

Balance Sheet-The Balance Sheet is also known as the Statement of Financial

position. It displays the current financial position of a company at a specific date.

Cash Flow Statement- The Cash flow statement tells us how much money is

flowing in and out of the business from the 3 main activities i.e. investing,

operating and financing.

Profit and Loss- The Profit or Loss statement or Statement of Income shows us

how the company is using its assets to make profits over a defined period.

Furthermore, it explains the change in net assets a company owns between start

and end of reporting period (Koch, 2009).

3. Key Lessons from ABC Learning

The rise and fall of ABC Learning Childcare Center can be blamed on aggressive

expansion backed by lack of discipline. As a result, some of the key lessons we can

learn from the ABC story include the following:

Always Recognize Revenue Properly

ABC cooked revenue figures for its leases and employee contracts, making it

appear as if it was experiencing growth.

Focus on Core Activities

1. Introduction

1.1 Background

ABC Learning Company was founded in 1988 as a stable company. In 2001, the

Australian government introduced the Childcare Benefit Rebate System.

Following this directive, ABC acquired child care centers across the country and

went through a massive growth expansion with share prices reaching $8.60.

However, this growth did not last. By the end of 2007, the company went through

a drastic change of events. ABC’s assets and share prices fell to $0.54 causing it

to be placed under Administrators in November 2008 (Koch, 2009).

1.2 Purpose

The Purpose of this business report is to provide information on ABC’s Financial

Reports, and explore the key lessons from their downfall and 3 ethical issues.

2. Major Financial Reports

The major financial reports are-

Balance Sheet-The Balance Sheet is also known as the Statement of Financial

position. It displays the current financial position of a company at a specific date.

Cash Flow Statement- The Cash flow statement tells us how much money is

flowing in and out of the business from the 3 main activities i.e. investing,

operating and financing.

Profit and Loss- The Profit or Loss statement or Statement of Income shows us

how the company is using its assets to make profits over a defined period.

Furthermore, it explains the change in net assets a company owns between start

and end of reporting period (Koch, 2009).

3. Key Lessons from ABC Learning

The rise and fall of ABC Learning Childcare Center can be blamed on aggressive

expansion backed by lack of discipline. As a result, some of the key lessons we can

learn from the ABC story include the following:

Always Recognize Revenue Properly

ABC cooked revenue figures for its leases and employee contracts, making it

appear as if it was experiencing growth.

Focus on Core Activities

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Due to lack of attention, the overseas locations in US, New Zealand and

Singapore ended up not performing well. This resulted in the company selling of

these subsidiaries and a fall in share price.

Importance of a Company’s financial accounts in indicating its health

Investor’s did not pay close attention to the published accounts which showed red

flags.

Importance of Sound Corporate Governance

ABC did not disclose its related party transactions with Queensland Maintenance

and .Furthermore, Eddie Grove did not disclose margin loans

Complex financial structure and transaction

ABC Learning’s transactions were too complex for financial investors and

regulators to understand.

4. Identify three Ethical Issues

Compliance and Governance

The company did not comply with accounting rules such as disclosure and Board

scrutiny

Individual Power

Eddy Groves was a sole decision maker and he made decisions that eventually led

to the collapse.

Transparency

ABC was not transparent in its financial transactions. Furthermore, they inflated

revenues and were not disclosing related third party transaction.

Summary

The story of ABC teaches us the risk of improper valuations coupled with bad

financial decisions can lead to the collapse of an organization. Therefore, it is prudent

for a business to go with the best estimate and ensure proper accounting practices.

References

Koch, D. (2009, November). The ABC of a Corporate Collapse. CPA Australia. Retrieved from

https://www.youtube.com/watch?v=YYF6JW9vJKo&list=PL12C0ADD577F6B741Jjj

Singapore ended up not performing well. This resulted in the company selling of

these subsidiaries and a fall in share price.

Importance of a Company’s financial accounts in indicating its health

Investor’s did not pay close attention to the published accounts which showed red

flags.

Importance of Sound Corporate Governance

ABC did not disclose its related party transactions with Queensland Maintenance

and .Furthermore, Eddie Grove did not disclose margin loans

Complex financial structure and transaction

ABC Learning’s transactions were too complex for financial investors and

regulators to understand.

4. Identify three Ethical Issues

Compliance and Governance

The company did not comply with accounting rules such as disclosure and Board

scrutiny

Individual Power

Eddy Groves was a sole decision maker and he made decisions that eventually led

to the collapse.

Transparency

ABC was not transparent in its financial transactions. Furthermore, they inflated

revenues and were not disclosing related third party transaction.

Summary

The story of ABC teaches us the risk of improper valuations coupled with bad

financial decisions can lead to the collapse of an organization. Therefore, it is prudent

for a business to go with the best estimate and ensure proper accounting practices.

References

Koch, D. (2009, November). The ABC of a Corporate Collapse. CPA Australia. Retrieved from

https://www.youtube.com/watch?v=YYF6JW9vJKo&list=PL12C0ADD577F6B741Jjj

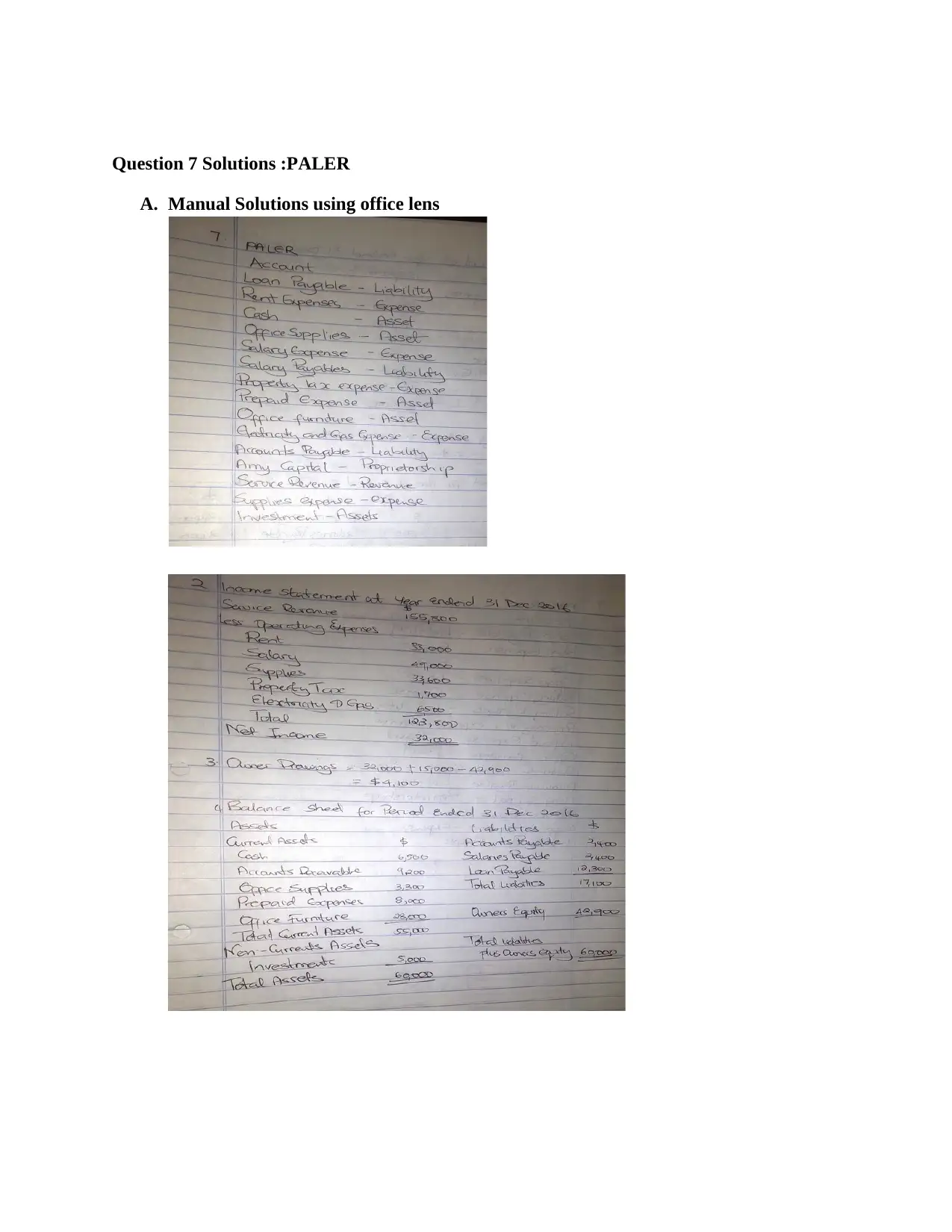

Question 7 Solutions :PALER

A. Manual Solutions using office lens

A. Manual Solutions using office lens

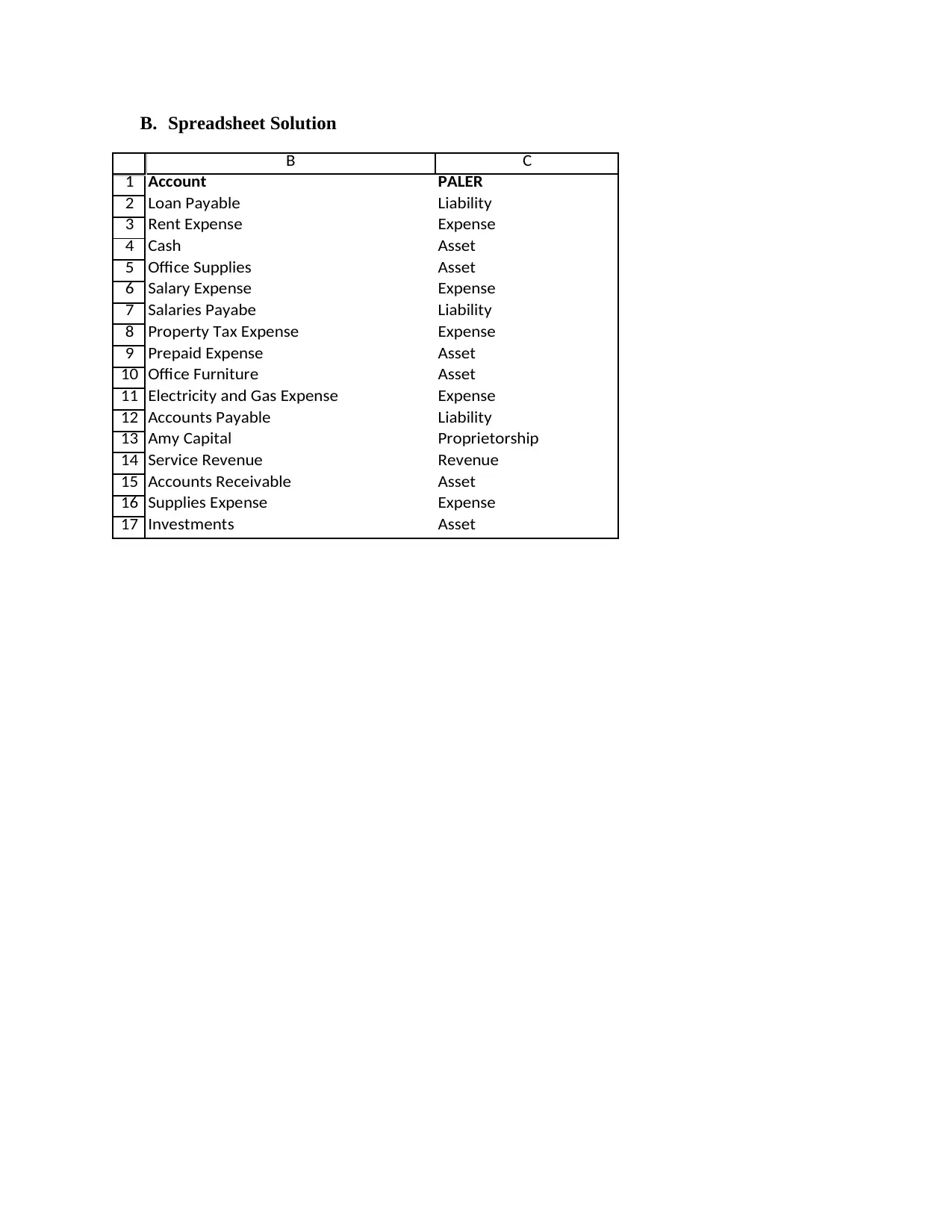

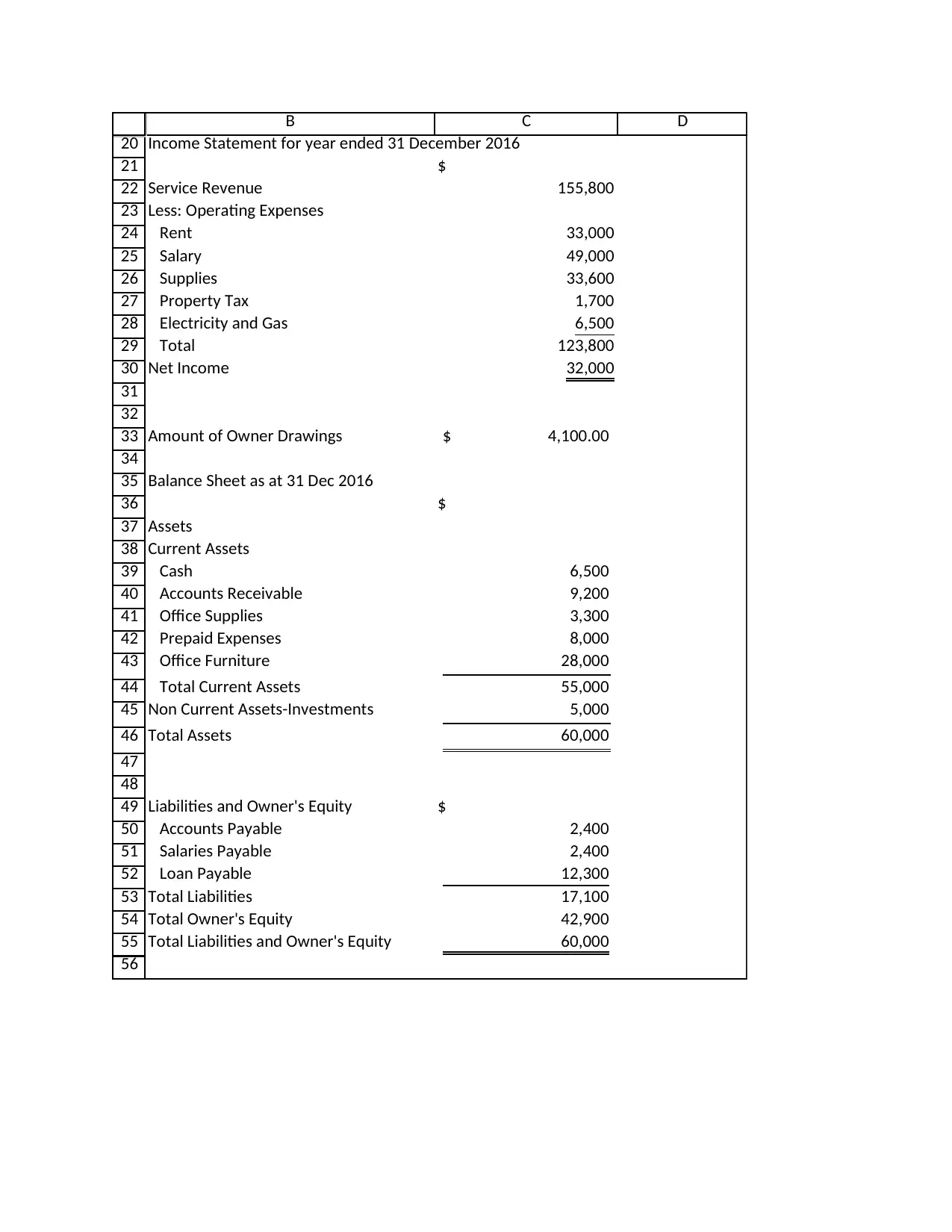

B. Spreadsheet Solution

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

B C

Account PALER

Loan Payable Liability

Rent Expense Expense

Cash Asset

Office Supplies Asset

Salary Expense Expense

Salaries Payabe Liability

Property Tax Expense Expense

Prepaid Expense Asset

Office Furniture Asset

Electricity and Gas Expense Expense

Accounts Payable Liability

Amy Capital Proprietorship

Service Revenue Revenue

Accounts Receivable Asset

Supplies Expense Expense

Investments Asset

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

B C

Account PALER

Loan Payable Liability

Rent Expense Expense

Cash Asset

Office Supplies Asset

Salary Expense Expense

Salaries Payabe Liability

Property Tax Expense Expense

Prepaid Expense Asset

Office Furniture Asset

Electricity and Gas Expense Expense

Accounts Payable Liability

Amy Capital Proprietorship

Service Revenue Revenue

Accounts Receivable Asset

Supplies Expense Expense

Investments Asset

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

B C D

$

Service Revenue 155,800

Less: Operating Expenses

Rent 33,000

Salary 49,000

Supplies 33,600

Property Tax 1,700

Electricity and Gas 6,500

Total 123,800

Net Income 32,000

Amount of Owner Drawings 4,100.00$

Balance Sheet as at 31 Dec 2016

$

Assets

Current Assets

Cash 6,500

Accounts Receivable 9,200

Office Supplies 3,300

Prepaid Expenses 8,000

Office Furniture 28,000

Total Current Assets 55,000

Non Current Assets-Investments 5,000

Total Assets 60,000

Liabilities and Owner's Equity $

Accounts Payable 2,400

Salaries Payable 2,400

Loan Payable 12,300

Total Liabilities 17,100

Total Owner's Equity 42,900

Total Liabilities and Owner's Equity 60,000

Income Statement for year ended 31 December 2016

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

B C D

$

Service Revenue 155,800

Less: Operating Expenses

Rent 33,000

Salary 49,000

Supplies 33,600

Property Tax 1,700

Electricity and Gas 6,500

Total 123,800

Net Income 32,000

Amount of Owner Drawings 4,100.00$

Balance Sheet as at 31 Dec 2016

$

Assets

Current Assets

Cash 6,500

Accounts Receivable 9,200

Office Supplies 3,300

Prepaid Expenses 8,000

Office Furniture 28,000

Total Current Assets 55,000

Non Current Assets-Investments 5,000

Total Assets 60,000

Liabilities and Owner's Equity $

Accounts Payable 2,400

Salaries Payable 2,400

Loan Payable 12,300

Total Liabilities 17,100

Total Owner's Equity 42,900

Total Liabilities and Owner's Equity 60,000

Income Statement for year ended 31 December 2016

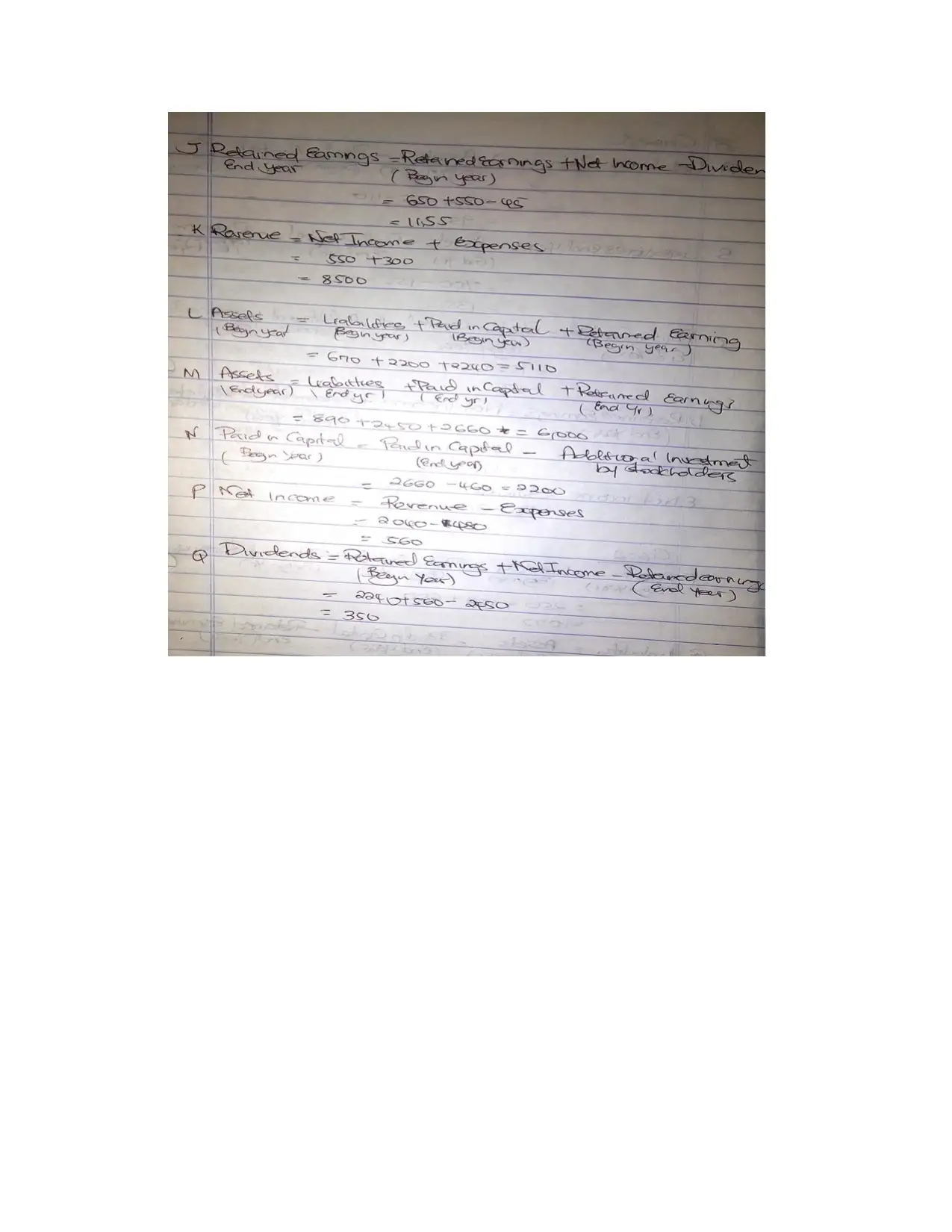

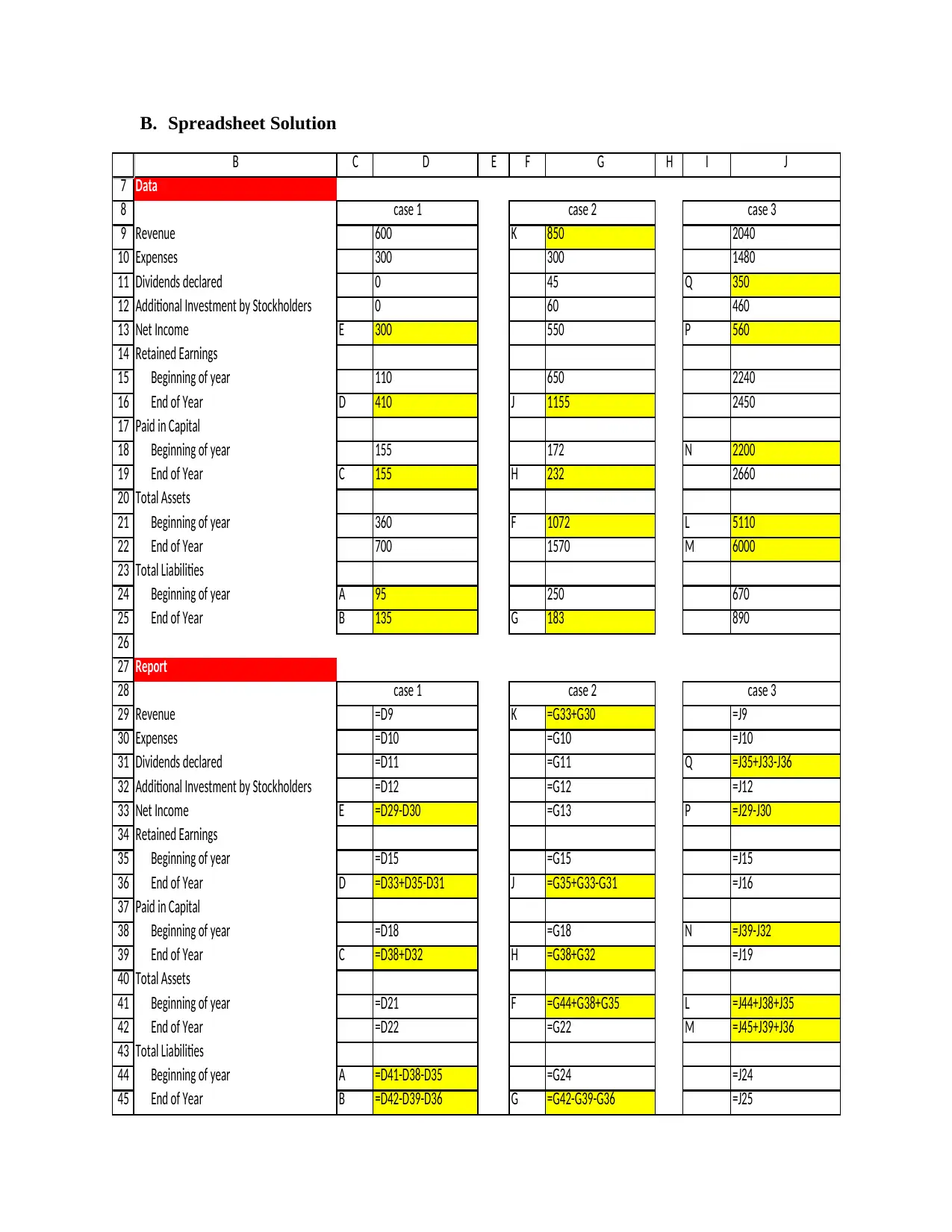

Question 8 Solutions: Balance Sheet Equation

A. Manual solutions using Office Lens

A. Manual solutions using Office Lens

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

B. Spreadsheet Solution

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

B C D E F G H I J

Data

Revenue 600 K 850 2040

Expenses 300 300 1480

Dividends declared 0 45 Q 350

Additional Investment by Stockholders 0 60 460

Net Income E 300 550 P 560

Retained Earnings

Beginning of year 110 650 2240

End of Year D 410 J 1155 2450

Paid in Capital

Beginning of year 155 172 N 2200

End of Year C 155 H 232 2660

Total Assets

Beginning of year 360 F 1072 L 5110

End of Year 700 1570 M 6000

Total Liabilities

Beginning of year A 95 250 670

End of Year B 135 G 183 890

Report

Revenue =D9 K =G33+G30 =J9

Expenses =D10 =G10 =J10

Dividends declared =D11 =G11 Q =J35+J33-J36

Additional Investment by Stockholders =D12 =G12 =J12

Net Income E =D29-D30 =G13 P =J29-J30

Retained Earnings

Beginning of year =D15 =G15 =J15

End of Year D =D33+D35-D31 J =G35+G33-G31 =J16

Paid in Capital

Beginning of year =D18 =G18 N =J39-J32

End of Year C =D38+D32 H =G38+G32 =J19

Total Assets

Beginning of year =D21 F =G44+G38+G35 L =J44+J38+J35

End of Year =D22 =G22 M =J45+J39+J36

Total Liabilities

Beginning of year A =D41-D38-D35 =G24 =J24

End of Year B =D42-D39-D36 G =G42-G39-G36 =J25

case 1 case 2 case 3

case 1 case 2 case 3

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

B C D E F G H I J

Data

Revenue 600 K 850 2040

Expenses 300 300 1480

Dividends declared 0 45 Q 350

Additional Investment by Stockholders 0 60 460

Net Income E 300 550 P 560

Retained Earnings

Beginning of year 110 650 2240

End of Year D 410 J 1155 2450

Paid in Capital

Beginning of year 155 172 N 2200

End of Year C 155 H 232 2660

Total Assets

Beginning of year 360 F 1072 L 5110

End of Year 700 1570 M 6000

Total Liabilities

Beginning of year A 95 250 670

End of Year B 135 G 183 890

Report

Revenue =D9 K =G33+G30 =J9

Expenses =D10 =G10 =J10

Dividends declared =D11 =G11 Q =J35+J33-J36

Additional Investment by Stockholders =D12 =G12 =J12

Net Income E =D29-D30 =G13 P =J29-J30

Retained Earnings

Beginning of year =D15 =G15 =J15

End of Year D =D33+D35-D31 J =G35+G33-G31 =J16

Paid in Capital

Beginning of year =D18 =G18 N =J39-J32

End of Year C =D38+D32 H =G38+G32 =J19

Total Assets

Beginning of year =D21 F =G44+G38+G35 L =J44+J38+J35

End of Year =D22 =G22 M =J45+J39+J36

Total Liabilities

Beginning of year A =D41-D38-D35 =G24 =J24

End of Year B =D42-D39-D36 G =G42-G39-G36 =J25

case 1 case 2 case 3

case 1 case 2 case 3

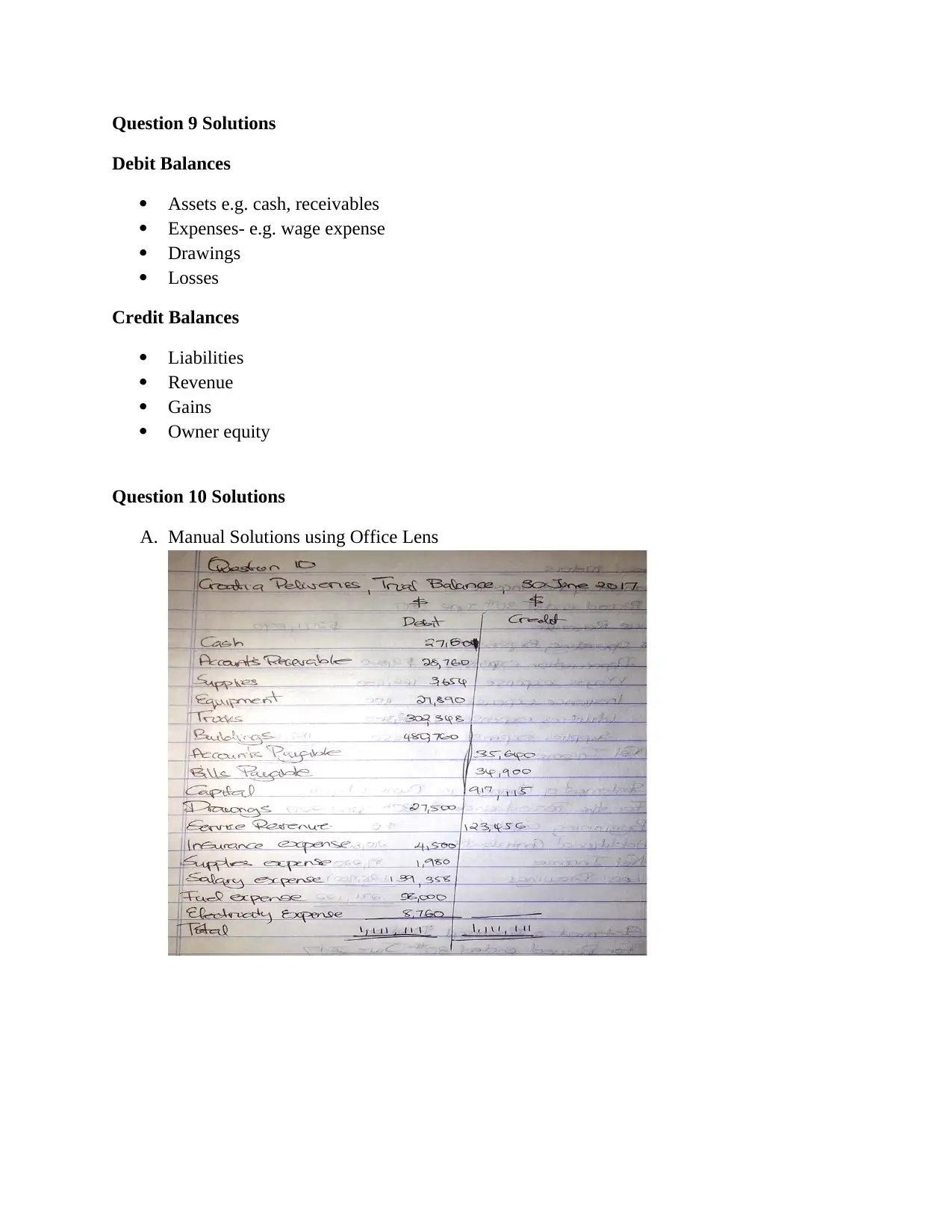

Question 9 Solutions

Debit Balances

Assets e.g. cash, receivables

Expenses- e.g. wage expense

Drawings

Losses

Credit Balances

Liabilities

Revenue

Gains

Owner equity

Question 10 Solutions

A. Manual Solutions using Office Lens

Debit Balances

Assets e.g. cash, receivables

Expenses- e.g. wage expense

Drawings

Losses

Credit Balances

Liabilities

Revenue

Gains

Owner equity

Question 10 Solutions

A. Manual Solutions using Office Lens

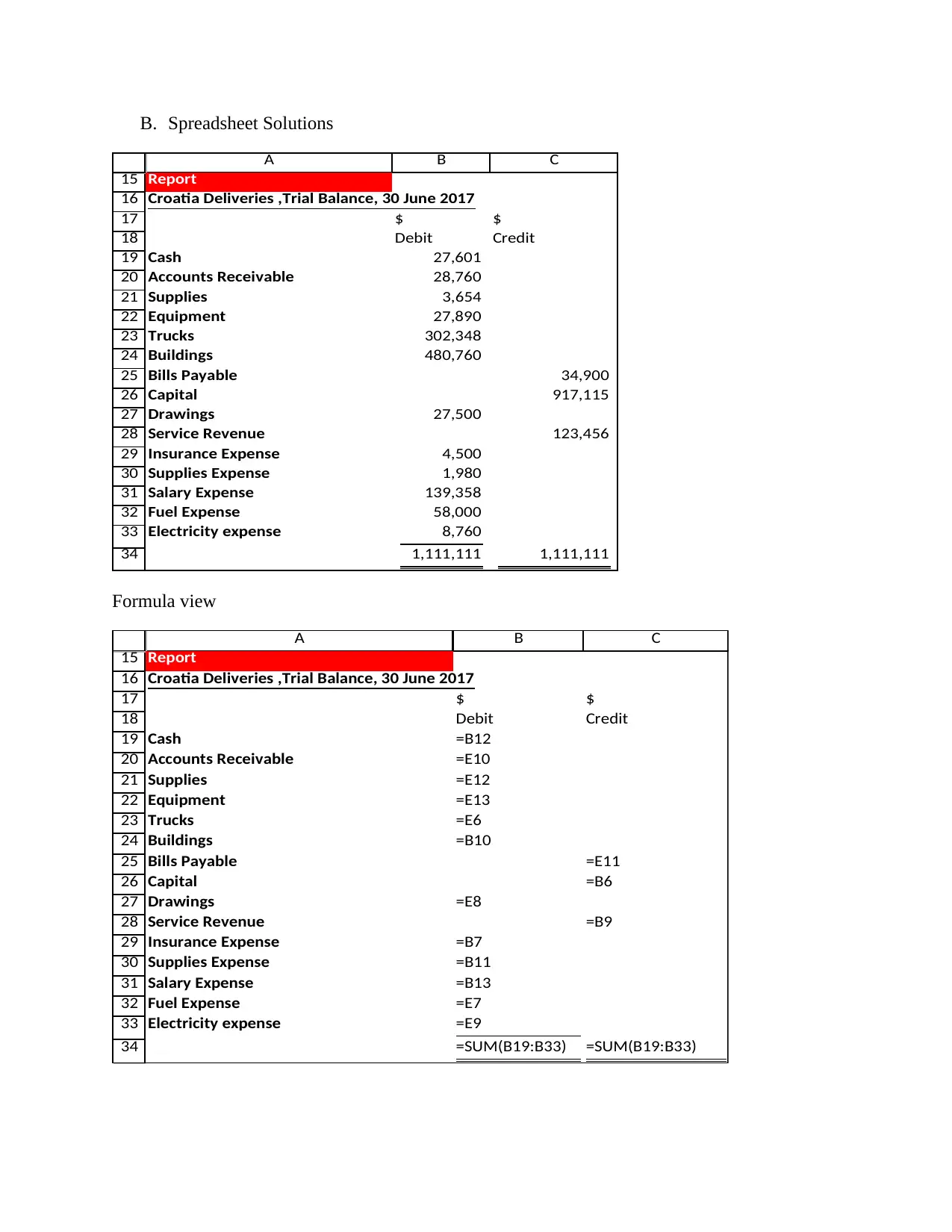

B. Spreadsheet Solutions

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

A B C

Report

Croatia Deliveries ,Trial Balance, 30 June 2017

$ $

Debit Credit

Cash 27,601

Accounts Receivable 28,760

Supplies 3,654

Equipment 27,890

Trucks 302,348

Buildings 480,760

Bills Payable 34,900

Capital 917,115

Drawings 27,500

Service Revenue 123,456

Insurance Expense 4,500

Supplies Expense 1,980

Salary Expense 139,358

Fuel Expense 58,000

Electricity expense 8,760

1,111,111 1,111,111

Formula view

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

A B C

Report

$ $

Debit Credit

Cash =B12

Accounts Receivable =E10

Supplies =E12

Equipment =E13

Trucks =E6

Buildings =B10

Bills Payable =E11

Capital =B6

Drawings =E8

Service Revenue =B9

Insurance Expense =B7

Supplies Expense =B11

Salary Expense =B13

Fuel Expense =E7

Electricity expense =E9

=SUM(B19:B33) =SUM(B19:B33)

Croatia Deliveries ,Trial Balance, 30 June 2017

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

A B C

Report

Croatia Deliveries ,Trial Balance, 30 June 2017

$ $

Debit Credit

Cash 27,601

Accounts Receivable 28,760

Supplies 3,654

Equipment 27,890

Trucks 302,348

Buildings 480,760

Bills Payable 34,900

Capital 917,115

Drawings 27,500

Service Revenue 123,456

Insurance Expense 4,500

Supplies Expense 1,980

Salary Expense 139,358

Fuel Expense 58,000

Electricity expense 8,760

1,111,111 1,111,111

Formula view

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

A B C

Report

$ $

Debit Credit

Cash =B12

Accounts Receivable =E10

Supplies =E12

Equipment =E13

Trucks =E6

Buildings =B10

Bills Payable =E11

Capital =B6

Drawings =E8

Service Revenue =B9

Insurance Expense =B7

Supplies Expense =B11

Salary Expense =B13

Fuel Expense =E7

Electricity expense =E9

=SUM(B19:B33) =SUM(B19:B33)

Croatia Deliveries ,Trial Balance, 30 June 2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

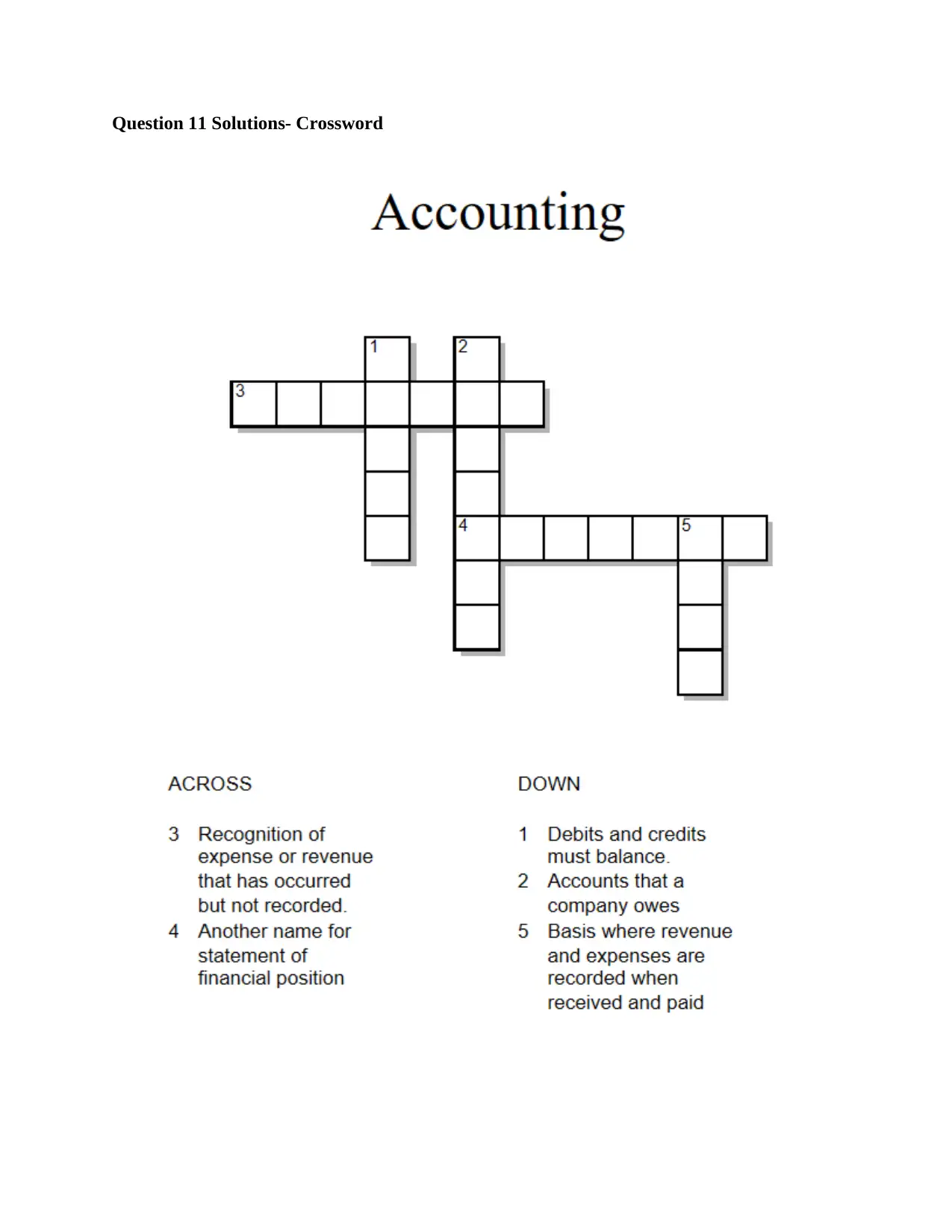

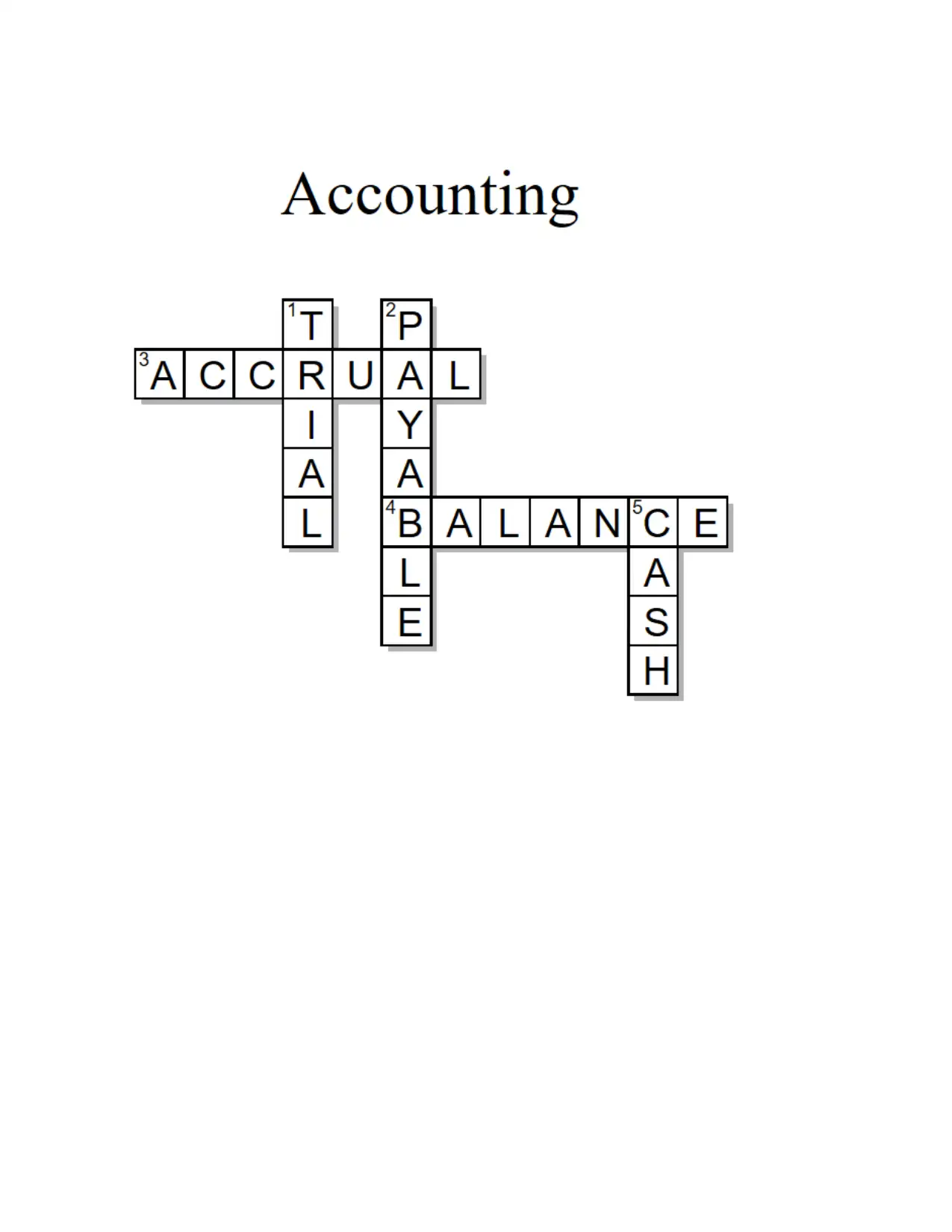

Question 11 Solutions- Crossword

Question 12 Solutions- Adjusting Entries plus examples

o Accrued Revenues

Debit Credit

Accrued Receivables XXX

Service Revenue XXX

o Deferred expenses

Debit Credit

Expense XXX

Prepaid expense XXX

Question 13 Solutions- Liabilities

o Current liabilities are financial obligations due by company within the current year e.g.

accounts payable and salary payable.

o Non-current liabilities are long term financial obligations e.g. long term lease, loan

payables

Question 14 Solutions- Current Ratios

This ratio is an indicator of liquidity and shows the proportion of current assets to current

liabilities (Accounting Coach, 2017).

o Accrued Revenues

Debit Credit

Accrued Receivables XXX

Service Revenue XXX

o Deferred expenses

Debit Credit

Expense XXX

Prepaid expense XXX

Question 13 Solutions- Liabilities

o Current liabilities are financial obligations due by company within the current year e.g.

accounts payable and salary payable.

o Non-current liabilities are long term financial obligations e.g. long term lease, loan

payables

Question 14 Solutions- Current Ratios

This ratio is an indicator of liquidity and shows the proportion of current assets to current

liabilities (Accounting Coach, 2017).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

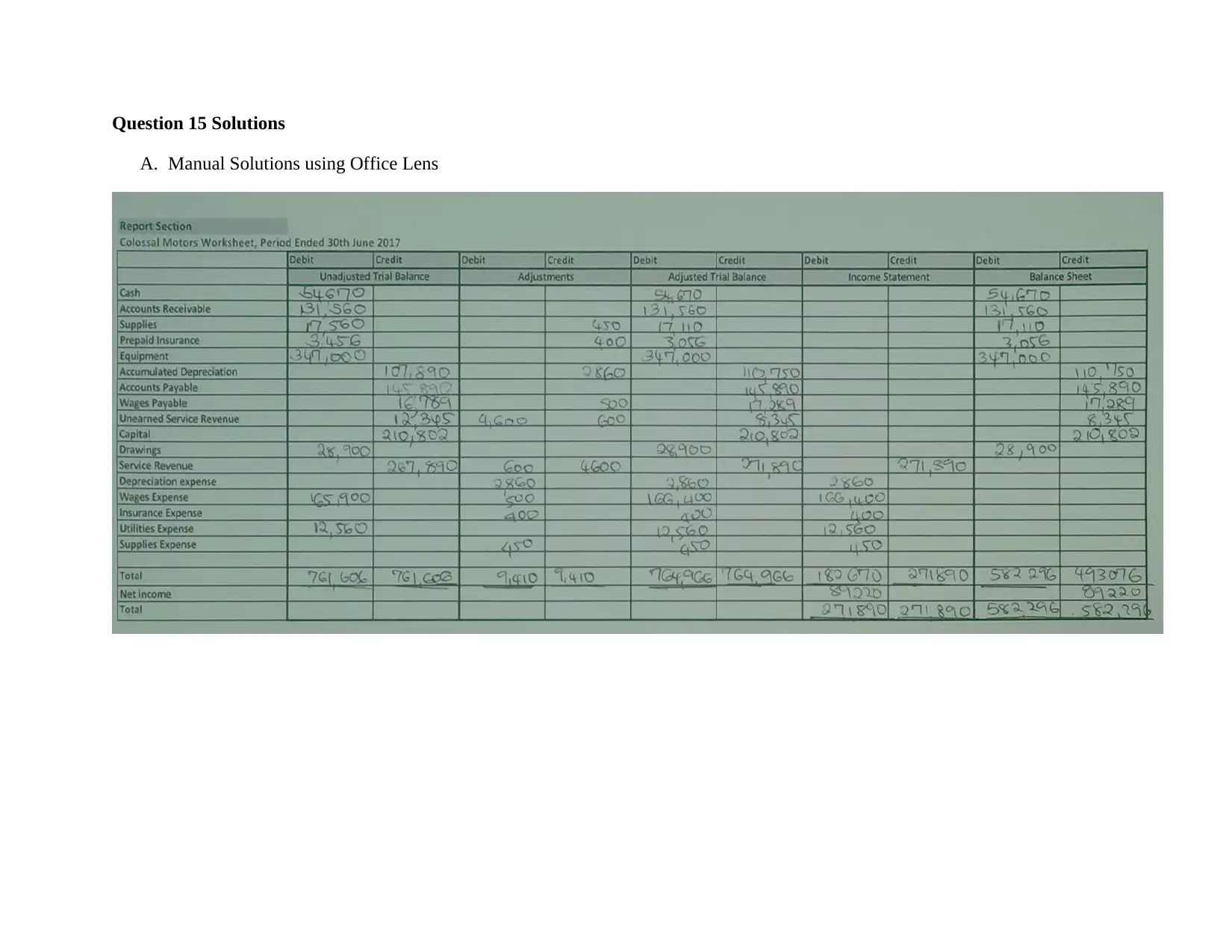

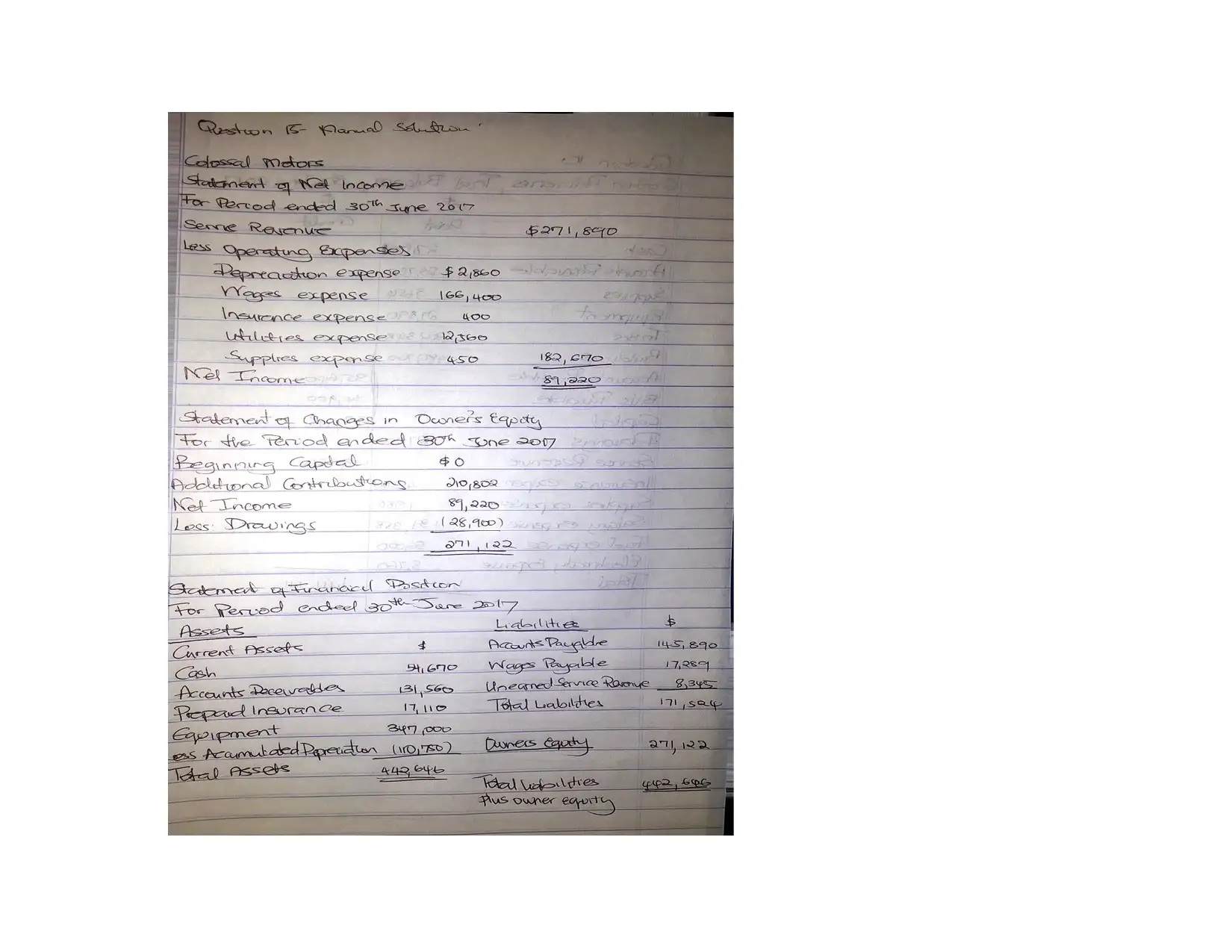

Question 15 Solutions

A. Manual Solutions using Office Lens

A. Manual Solutions using Office Lens

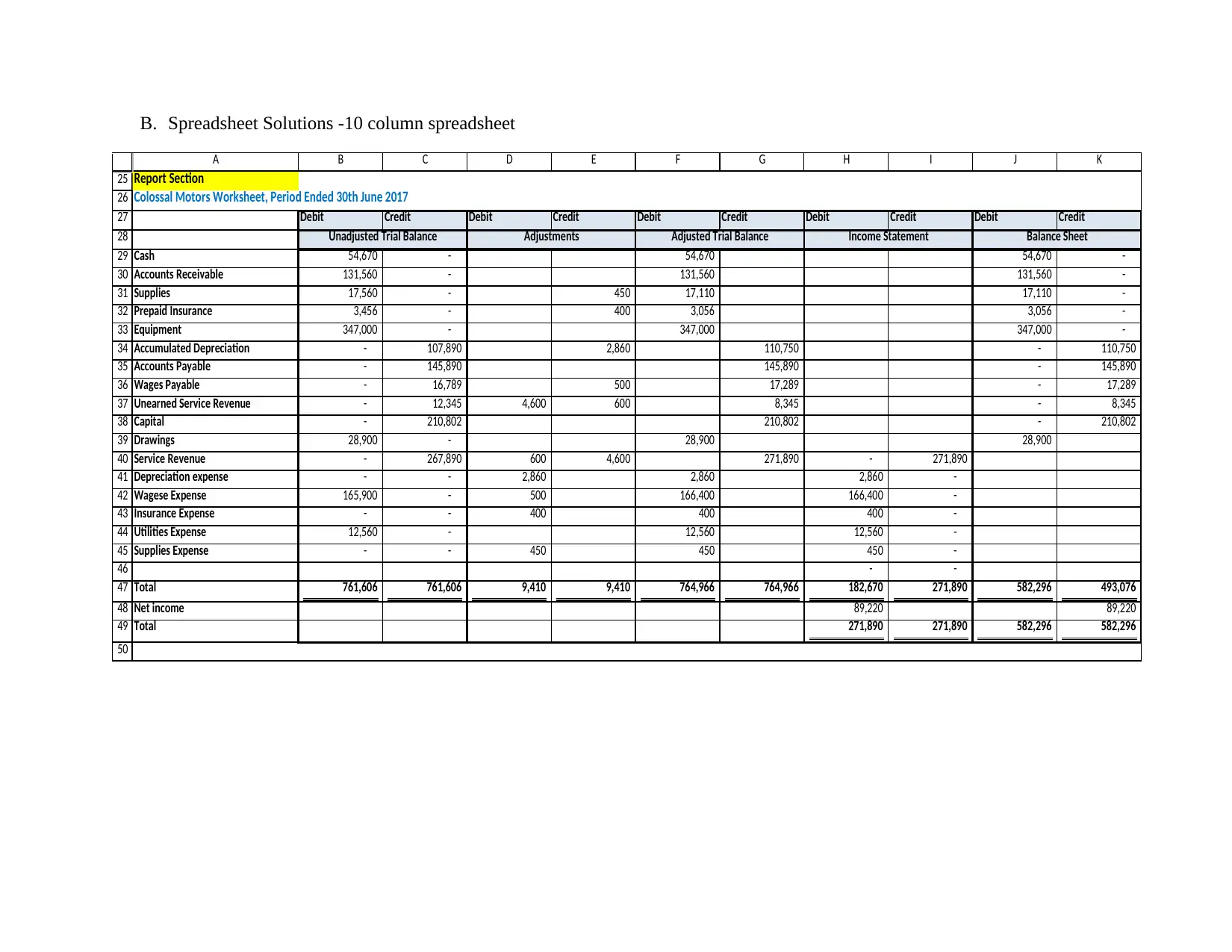

B. Spreadsheet Solutions -10 column spreadsheet

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

A B C D E F G H I J K

Report Section

Colossal Motors Worksheet, Period Ended 30th June 2017

Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit

Cash 54,670 - 54,670 54,670 -

Accounts Receivable 131,560 - 131,560 131,560 -

Supplies 17,560 - 450 17,110 17,110 -

Prepaid Insurance 3,456 - 400 3,056 3,056 -

Equipment 347,000 - 347,000 347,000 -

Accumulated Depreciation - 107,890 2,860 110,750 - 110,750

Accounts Payable - 145,890 145,890 - 145,890

Wages Payable - 16,789 500 17,289 - 17,289

Unearned Service Revenue - 12,345 4,600 600 8,345 - 8,345

Capital - 210,802 210,802 - 210,802

Drawings 28,900 - 28,900 28,900

Service Revenue - 267,890 600 4,600 271,890 - 271,890

Depreciation expense - - 2,860 2,860 2,860 -

Wagese Expense 165,900 - 500 166,400 166,400 -

Insurance Expense - - 400 400 400 -

Utilities Expense 12,560 - 12,560 12,560 -

Supplies Expense - - 450 450 450 -

- -

Total 761,606 761,606 9,410 9,410 764,966 764,966 182,670 271,890 582,296 493,076

Net income 89,220 89,220

Total 271,890 271,890 582,296 582,296

Unadjusted Trial Balance Adjustments Adjusted Trial Balance Income Statement Balance Sheet

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

A B C D E F G H I J K

Report Section

Colossal Motors Worksheet, Period Ended 30th June 2017

Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit

Cash 54,670 - 54,670 54,670 -

Accounts Receivable 131,560 - 131,560 131,560 -

Supplies 17,560 - 450 17,110 17,110 -

Prepaid Insurance 3,456 - 400 3,056 3,056 -

Equipment 347,000 - 347,000 347,000 -

Accumulated Depreciation - 107,890 2,860 110,750 - 110,750

Accounts Payable - 145,890 145,890 - 145,890

Wages Payable - 16,789 500 17,289 - 17,289

Unearned Service Revenue - 12,345 4,600 600 8,345 - 8,345

Capital - 210,802 210,802 - 210,802

Drawings 28,900 - 28,900 28,900

Service Revenue - 267,890 600 4,600 271,890 - 271,890

Depreciation expense - - 2,860 2,860 2,860 -

Wagese Expense 165,900 - 500 166,400 166,400 -

Insurance Expense - - 400 400 400 -

Utilities Expense 12,560 - 12,560 12,560 -

Supplies Expense - - 450 450 450 -

- -

Total 761,606 761,606 9,410 9,410 764,966 764,966 182,670 271,890 582,296 493,076

Net income 89,220 89,220

Total 271,890 271,890 582,296 582,296

Unadjusted Trial Balance Adjustments Adjusted Trial Balance Income Statement Balance Sheet

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

A B C D E F G H I J K

Report Section

Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit

Cash =B5 =C5 =B29+D29-E29 =F29 =G29

Accounts Receivable =B6 =C6 =B30+D30-E30 =F30 =G30

Supplies =B7 =C7 450 =B31+D31-E31 =F31 =G31

Prepaid Insurance =B8 =C8 400 =B32+D32-E32 =F32 =G32

Equipment =B9 =C9 =B33+D33-E33 =F33 =G33

Accumulated Depreciation =B10 =C10 2860 =C34-D34+E34 =F34 =G34

Accounts Payable =B11 =C11 =C35-D35+E35 =F35 =G35

Wages Payable =B12 =C12 500 =C36-D36+E36 =F36 =G36

Unearned Service Revenue =B13 =C13 4600 600 =C37-D37+E37 =F37 =G37

Capital =B14 =C14 =C38-D38+E38 =F38 =G38

Drawings =B15 =C15 =B39+D39-E39 =F39

Service Revenue =B16 =C16 600 4600 =C40-D40+E40 =F40 =G40

Depreciation expense =B17 =C17 2860 =B41+D41-E41 =F41 =G41

Wagese Expense =B18 =C18 500 =B42+D42-E42 =F42 =G42

Insurance Expense =B19 =C19 400 =B43+D43-E43 =F43 =G43

Utilities Expense =B20 =C20 =B44+D44-E44 =F44 =G44

Supplies Expense =B21 =C21 450 =B45+D45-E45 =F45 =G45

=F46 =G46

Total =SUM(B29:B45) =SUM(C29:C45) =SUM(D29:D45) =SUM(E29:E45) =SUM(F29:F45) =SUM(G29:G45) =SUM(H29:H45) =SUM(I29:I45) =SUM(J29:J45) =SUM(K29:K45)

Net income =I40-H47 =H48

Total =H47+H48 =I47+I48 =J47+J48 =K47+K48

Colossal Motors Worksheet, Period Ended 30th June 2017

Unadjusted Trial Balance Adjustments Adjusted Trial Balance Income Statement Balance Sheet

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

A B C D E F G H I J K

Report Section

Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit

Cash =B5 =C5 =B29+D29-E29 =F29 =G29

Accounts Receivable =B6 =C6 =B30+D30-E30 =F30 =G30

Supplies =B7 =C7 450 =B31+D31-E31 =F31 =G31

Prepaid Insurance =B8 =C8 400 =B32+D32-E32 =F32 =G32

Equipment =B9 =C9 =B33+D33-E33 =F33 =G33

Accumulated Depreciation =B10 =C10 2860 =C34-D34+E34 =F34 =G34

Accounts Payable =B11 =C11 =C35-D35+E35 =F35 =G35

Wages Payable =B12 =C12 500 =C36-D36+E36 =F36 =G36

Unearned Service Revenue =B13 =C13 4600 600 =C37-D37+E37 =F37 =G37

Capital =B14 =C14 =C38-D38+E38 =F38 =G38

Drawings =B15 =C15 =B39+D39-E39 =F39

Service Revenue =B16 =C16 600 4600 =C40-D40+E40 =F40 =G40

Depreciation expense =B17 =C17 2860 =B41+D41-E41 =F41 =G41

Wagese Expense =B18 =C18 500 =B42+D42-E42 =F42 =G42

Insurance Expense =B19 =C19 400 =B43+D43-E43 =F43 =G43

Utilities Expense =B20 =C20 =B44+D44-E44 =F44 =G44

Supplies Expense =B21 =C21 450 =B45+D45-E45 =F45 =G45

=F46 =G46

Total =SUM(B29:B45) =SUM(C29:C45) =SUM(D29:D45) =SUM(E29:E45) =SUM(F29:F45) =SUM(G29:G45) =SUM(H29:H45) =SUM(I29:I45) =SUM(J29:J45) =SUM(K29:K45)

Net income =I40-H47 =H48

Total =H47+H48 =I47+I48 =J47+J48 =K47+K48

Colossal Motors Worksheet, Period Ended 30th June 2017

Unadjusted Trial Balance Adjustments Adjusted Trial Balance Income Statement Balance Sheet

2a. Financial Reports

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

A B C

Colossal Motors

Statement of Net Income

For the period ended 30th June

$

Service Revenue 271,890

Less: Operating Expenses

Depreciation expense 2,860

Wagese Expense 166,400

Insurance Expense 400

Utilities Expense 12,560

Supplies Expense 450 182,670

Net Income 89,220

Colossal Motors

Statement of Changes in Owner's Equity

For the period ended 30th June

$

Capital beginning -

Additional Contributions 210,802

Net Income 89,220

Less: Drawings 28,900

271,122

Colossal Motors

Statement of Financial position For Period Ending 30 June

Assets

Cash 54,670

Accounts Receivable 131,560

Supplies 17,110

Prepaid Insurance 3,056

Equipment 347,000

Less Accumulated Depreciation (110,750)

Total Asset 442,646

Liabilities and Owner's Equity

Accounts Payable 145,890

Wages Payable 17,289

Unearned Service Revenue 8,345

Total Liabilities 171,524

Total Owner's Equity 271,122

Total Liabilities and Owner's Equity 442,646

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

A B C

Colossal Motors

Statement of Net Income

For the period ended 30th June

$

Service Revenue 271,890

Less: Operating Expenses

Depreciation expense 2,860

Wagese Expense 166,400

Insurance Expense 400

Utilities Expense 12,560

Supplies Expense 450 182,670

Net Income 89,220

Colossal Motors

Statement of Changes in Owner's Equity

For the period ended 30th June

$

Capital beginning -

Additional Contributions 210,802

Net Income 89,220

Less: Drawings 28,900

271,122

Colossal Motors

Statement of Financial position For Period Ending 30 June

Assets

Cash 54,670

Accounts Receivable 131,560

Supplies 17,110

Prepaid Insurance 3,056

Equipment 347,000

Less Accumulated Depreciation (110,750)

Total Asset 442,646

Liabilities and Owner's Equity

Accounts Payable 145,890

Wages Payable 17,289

Unearned Service Revenue 8,345

Total Liabilities 171,524

Total Owner's Equity 271,122

Total Liabilities and Owner's Equity 442,646

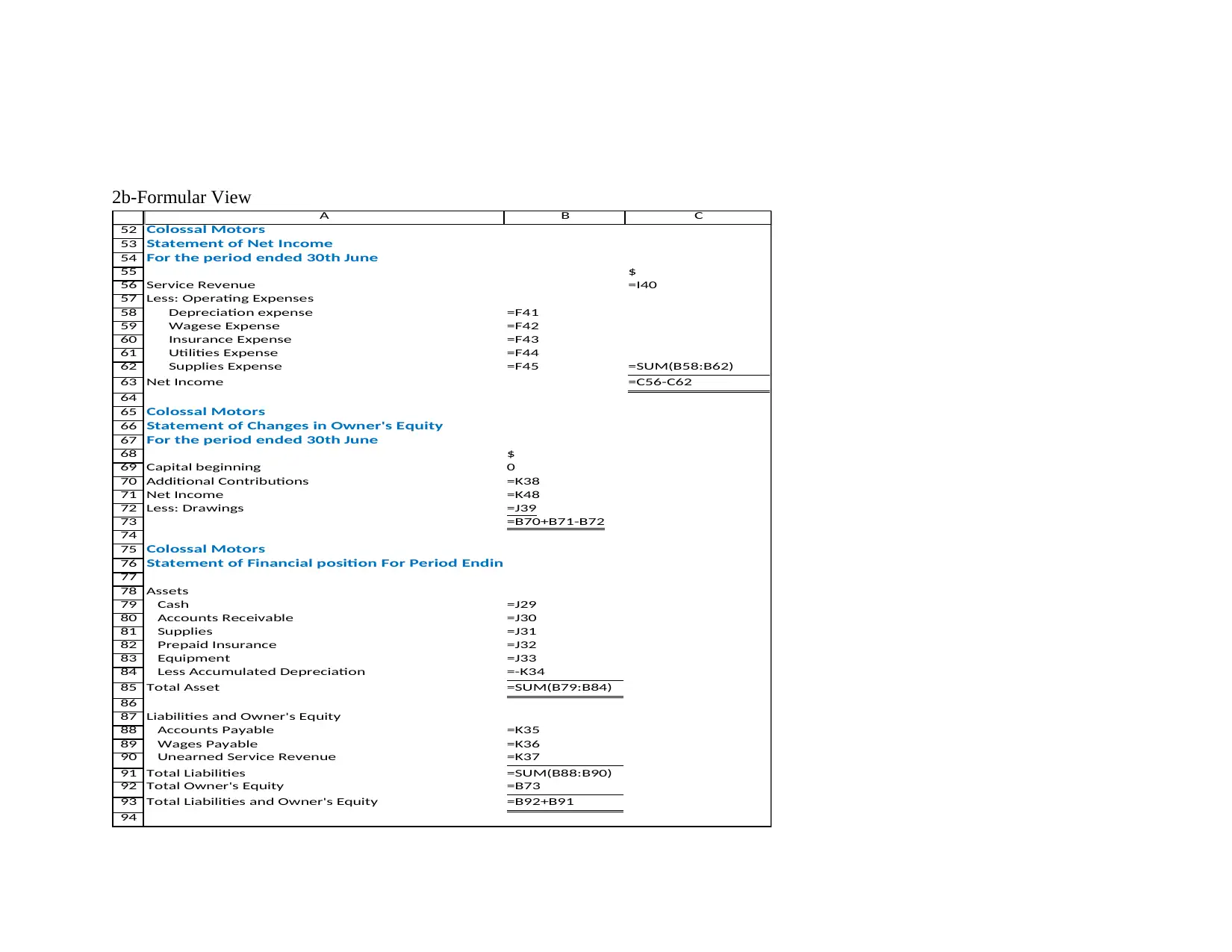

2b-Formular View

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

A B C

Colossal Motors

Statement of Net Income

For the period ended 30th June

$

Service Revenue =I40

Less: Operating Expenses

Depreciation expense =F41

Wagese Expense =F42

Insurance Expense =F43

Utilities Expense =F44

Supplies Expense =F45 =SUM(B58:B62)

Net Income =C56-C62

Colossal Motors

Statement of Changes in Owner's Equity

For the period ended 30th June

$

Capital beginning 0

Additional Contributions =K38

Net Income =K48

Less: Drawings =J39

=B70+B71-B72

Colossal Motors

Statement of Financial position For Period Ending 30 June

Assets

Cash =J29

Accounts Receivable =J30

Supplies =J31

Prepaid Insurance =J32

Equipment =J33

Less Accumulated Depreciation =-K34

Total Asset =SUM(B79:B84)

Liabilities and Owner's Equity

Accounts Payable =K35

Wages Payable =K36

Unearned Service Revenue =K37

Total Liabilities =SUM(B88:B90)

Total Owner's Equity =B73

Total Liabilities and Owner's Equity =B92+B91

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

A B C

Colossal Motors

Statement of Net Income

For the period ended 30th June

$

Service Revenue =I40

Less: Operating Expenses

Depreciation expense =F41

Wagese Expense =F42

Insurance Expense =F43

Utilities Expense =F44

Supplies Expense =F45 =SUM(B58:B62)

Net Income =C56-C62

Colossal Motors

Statement of Changes in Owner's Equity

For the period ended 30th June

$

Capital beginning 0

Additional Contributions =K38

Net Income =K48

Less: Drawings =J39

=B70+B71-B72

Colossal Motors

Statement of Financial position For Period Ending 30 June

Assets

Cash =J29

Accounts Receivable =J30

Supplies =J31

Prepaid Insurance =J32

Equipment =J33

Less Accumulated Depreciation =-K34

Total Asset =SUM(B79:B84)

Liabilities and Owner's Equity

Accounts Payable =K35

Wages Payable =K36

Unearned Service Revenue =K37

Total Liabilities =SUM(B88:B90)

Total Owner's Equity =B73

Total Liabilities and Owner's Equity =B92+B91

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

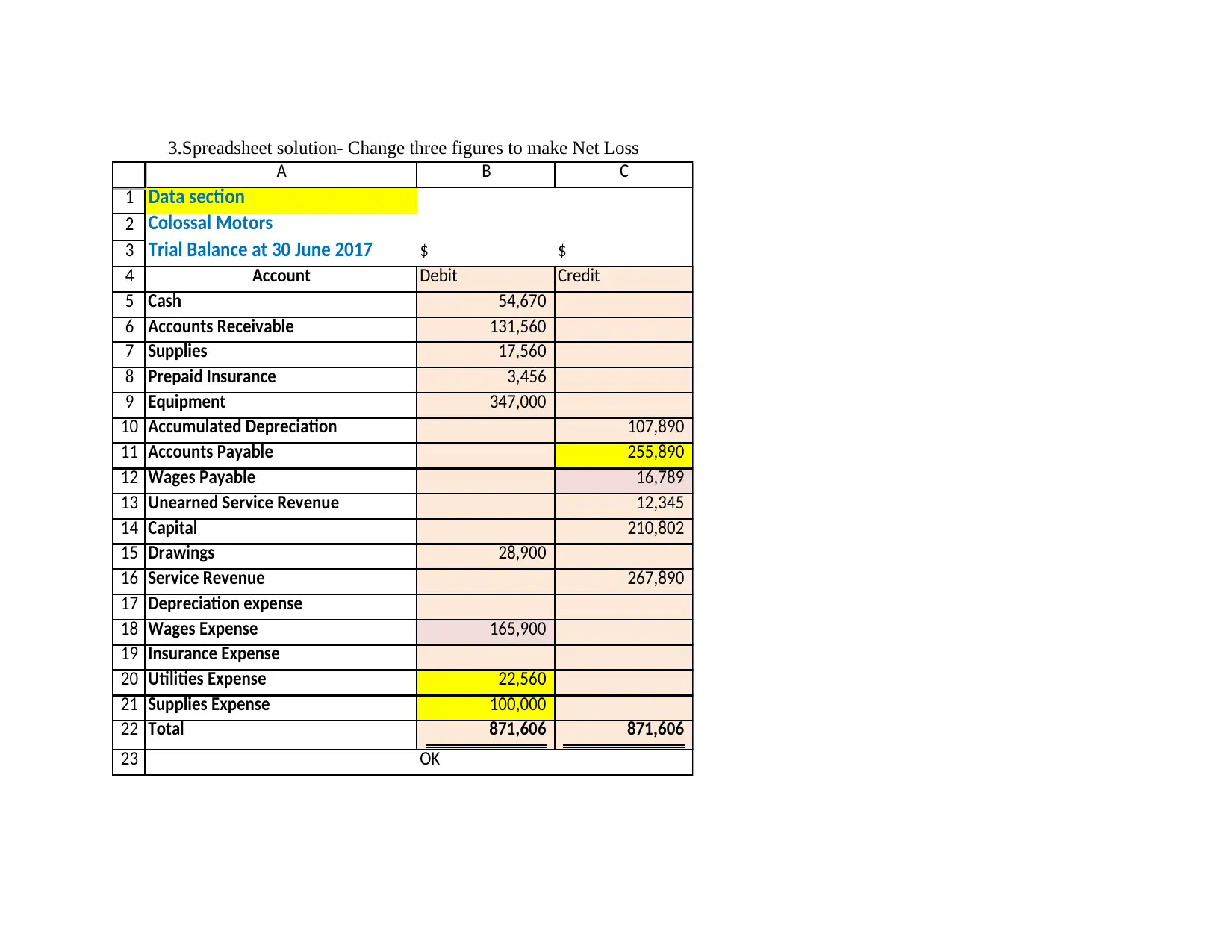

3.Spreadsheet solution- Change three figures to make Net Loss

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

A B C

Data section

Colossal Motors

Trial Balance at 30 June 2017 $ $

Account Debit Credit

Cash 54,670

Accounts Receivable 131,560

Supplies 17,560

Prepaid Insurance 3,456

Equipment 347,000

Accumulated Depreciation 107,890

Accounts Payable 255,890

Wages Payable 16,789

Unearned Service Revenue 12,345

Capital 210,802

Drawings 28,900

Service Revenue 267,890

Depreciation expense

Wages Expense 165,900

Insurance Expense

Utilities Expense 22,560

Supplies Expense 100,000

Total 871,606 871,606

OK

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

A B C

Data section

Colossal Motors

Trial Balance at 30 June 2017 $ $

Account Debit Credit

Cash 54,670

Accounts Receivable 131,560

Supplies 17,560

Prepaid Insurance 3,456

Equipment 347,000

Accumulated Depreciation 107,890

Accounts Payable 255,890

Wages Payable 16,789

Unearned Service Revenue 12,345

Capital 210,802

Drawings 28,900

Service Revenue 267,890

Depreciation expense

Wages Expense 165,900

Insurance Expense

Utilities Expense 22,560

Supplies Expense 100,000

Total 871,606 871,606

OK

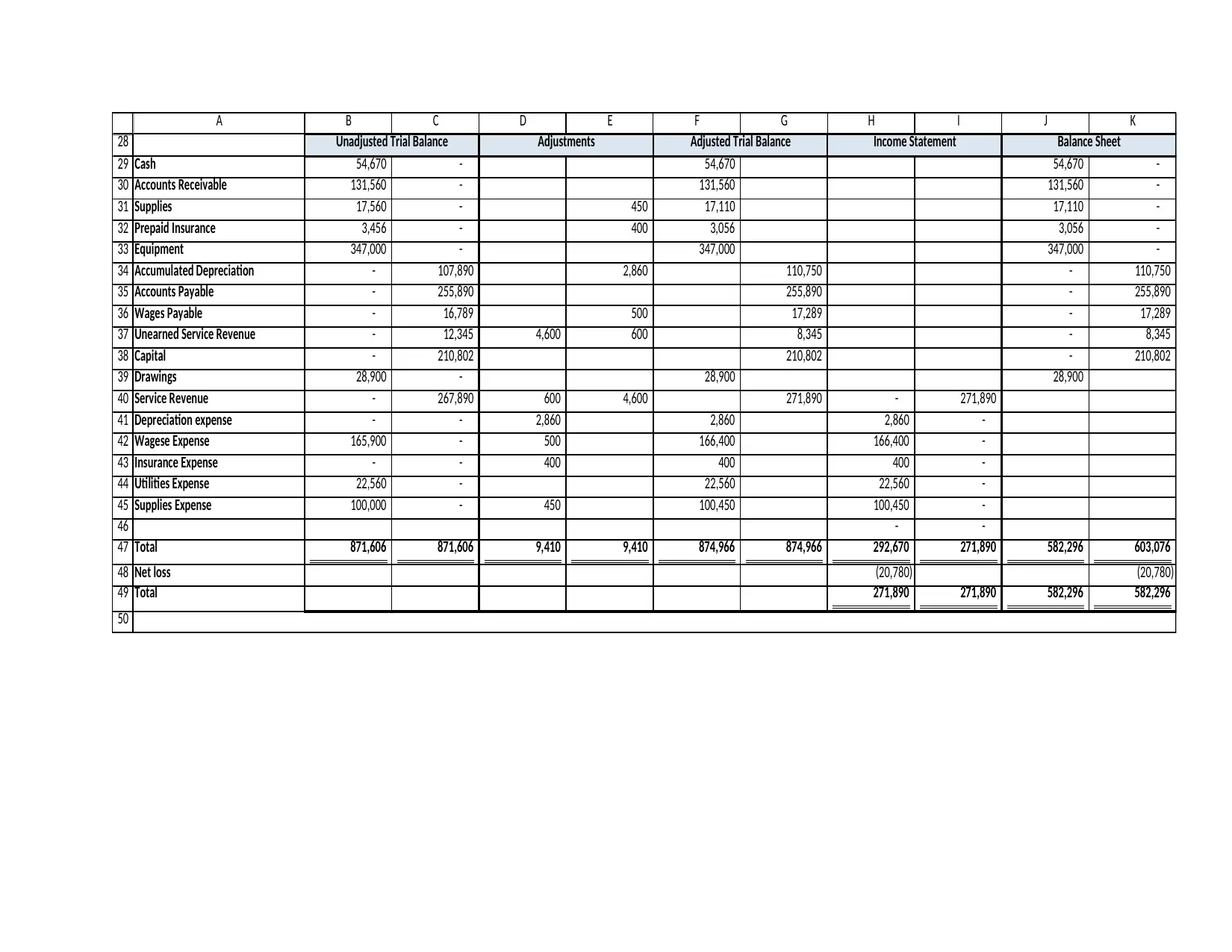

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

A B C D E F G H I J K

Cash 54,670 - 54,670 54,670 -

Accounts Receivable 131,560 - 131,560 131,560 -

Supplies 17,560 - 450 17,110 17,110 -

Prepaid Insurance 3,456 - 400 3,056 3,056 -

Equipment 347,000 - 347,000 347,000 -

Accumulated Depreciation - 107,890 2,860 110,750 - 110,750

Accounts Payable - 255,890 255,890 - 255,890

Wages Payable - 16,789 500 17,289 - 17,289

Unearned Service Revenue - 12,345 4,600 600 8,345 - 8,345

Capital - 210,802 210,802 - 210,802

Drawings 28,900 - 28,900 28,900

Service Revenue - 267,890 600 4,600 271,890 - 271,890

Depreciation expense - - 2,860 2,860 2,860 -

Wagese Expense 165,900 - 500 166,400 166,400 -

Insurance Expense - - 400 400 400 -

Utilities Expense 22,560 - 22,560 22,560 -

Supplies Expense 100,000 - 450 100,450 100,450 -

- -

Total 871,606 871,606 9,410 9,410 874,966 874,966 292,670 271,890 582,296 603,076

Net loss (20,780) (20,780)

Total 271,890 271,890 582,296 582,296

Unadjusted Trial Balance Adjustments Adjusted Trial Balance Income Statement Balance Sheet

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

A B C D E F G H I J K

Cash 54,670 - 54,670 54,670 -

Accounts Receivable 131,560 - 131,560 131,560 -

Supplies 17,560 - 450 17,110 17,110 -

Prepaid Insurance 3,456 - 400 3,056 3,056 -

Equipment 347,000 - 347,000 347,000 -

Accumulated Depreciation - 107,890 2,860 110,750 - 110,750

Accounts Payable - 255,890 255,890 - 255,890

Wages Payable - 16,789 500 17,289 - 17,289

Unearned Service Revenue - 12,345 4,600 600 8,345 - 8,345

Capital - 210,802 210,802 - 210,802

Drawings 28,900 - 28,900 28,900

Service Revenue - 267,890 600 4,600 271,890 - 271,890

Depreciation expense - - 2,860 2,860 2,860 -

Wagese Expense 165,900 - 500 166,400 166,400 -

Insurance Expense - - 400 400 400 -

Utilities Expense 22,560 - 22,560 22,560 -

Supplies Expense 100,000 - 450 100,450 100,450 -

- -

Total 871,606 871,606 9,410 9,410 874,966 874,966 292,670 271,890 582,296 603,076

Net loss (20,780) (20,780)

Total 271,890 271,890 582,296 582,296

Unadjusted Trial Balance Adjustments Adjusted Trial Balance Income Statement Balance Sheet

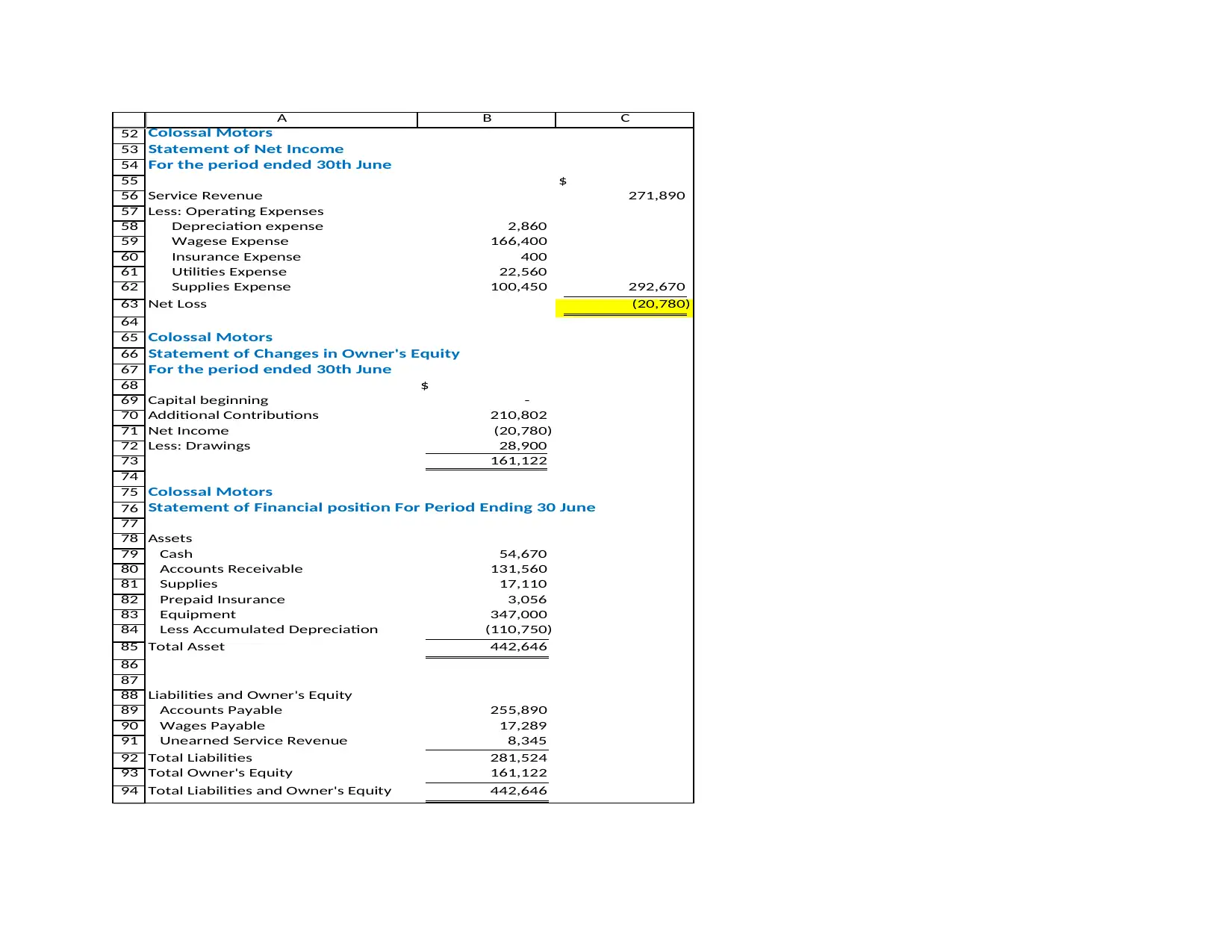

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

A B C

Colossal Motors

Statement of Net Income

For the period ended 30th June

$

Service Revenue 271,890

Less: Operating Expenses

Depreciation expense 2,860

Wagese Expense 166,400

Insurance Expense 400

Utilities Expense 22,560

Supplies Expense 100,450 292,670

Net Loss (20,780)

Colossal Motors

Statement of Changes in Owner's Equity

For the period ended 30th June

$

Capital beginning -

Additional Contributions 210,802

Net Income (20,780)

Less: Drawings 28,900

161,122

Colossal Motors

Statement of Financial position For Period Ending 30 June

Assets

Cash 54,670

Accounts Receivable 131,560

Supplies 17,110

Prepaid Insurance 3,056

Equipment 347,000

Less Accumulated Depreciation (110,750)

Total Asset 442,646

Liabilities and Owner's Equity

Accounts Payable 255,890

Wages Payable 17,289

Unearned Service Revenue 8,345

Total Liabilities 281,524

Total Owner's Equity 161,122

Total Liabilities and Owner's Equity 442,646

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

A B C

Colossal Motors

Statement of Net Income

For the period ended 30th June

$

Service Revenue 271,890

Less: Operating Expenses

Depreciation expense 2,860

Wagese Expense 166,400

Insurance Expense 400

Utilities Expense 22,560

Supplies Expense 100,450 292,670

Net Loss (20,780)

Colossal Motors

Statement of Changes in Owner's Equity

For the period ended 30th June

$

Capital beginning -

Additional Contributions 210,802

Net Income (20,780)

Less: Drawings 28,900

161,122

Colossal Motors

Statement of Financial position For Period Ending 30 June

Assets

Cash 54,670

Accounts Receivable 131,560

Supplies 17,110

Prepaid Insurance 3,056

Equipment 347,000

Less Accumulated Depreciation (110,750)

Total Asset 442,646

Liabilities and Owner's Equity

Accounts Payable 255,890

Wages Payable 17,289

Unearned Service Revenue 8,345

Total Liabilities 281,524

Total Owner's Equity 161,122

Total Liabilities and Owner's Equity 442,646

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Accounting Coach. (2017). What is the current ratio? Retrieved from Accounting Coach: https://www.accountingcoach.com/blog/current-ratio-2

Bishop, M. (2017). What's Wrong with Cheating? Retrieved from CSUSM: http://www.csusm.edu/dos/studres/wwc.html

CPA Australia. (2017). Understanding Annual Reports. Retrieved from CPA Australia:

https://www.cpaaustralia.com.au/professional-resources/reporting/understanding-annual-reports

Koch, D. (2009, November). The ABC of a Corporate Collapse. CPA Australia. Retrieved from https://www.youtube.com/watch?

v=YYF6JW9vJKo&list=PL12C0ADD577F6B741Jjj

Oxford Dictionary. (2017). Definition of Plagiarism. Retrieved from Oxford Dictionary: https://en.oxforddictionaries.com/definition/plagiarism

Accounting Coach. (2017). What is the current ratio? Retrieved from Accounting Coach: https://www.accountingcoach.com/blog/current-ratio-2

Bishop, M. (2017). What's Wrong with Cheating? Retrieved from CSUSM: http://www.csusm.edu/dos/studres/wwc.html

CPA Australia. (2017). Understanding Annual Reports. Retrieved from CPA Australia:

https://www.cpaaustralia.com.au/professional-resources/reporting/understanding-annual-reports

Koch, D. (2009, November). The ABC of a Corporate Collapse. CPA Australia. Retrieved from https://www.youtube.com/watch?

v=YYF6JW9vJKo&list=PL12C0ADD577F6B741Jjj

Oxford Dictionary. (2017). Definition of Plagiarism. Retrieved from Oxford Dictionary: https://en.oxforddictionaries.com/definition/plagiarism

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.