Analysis of Acquisitions and Financial Statement Preparation

VerifiedAdded on 2020/03/02

|6

|974

|329

Project

AI Summary

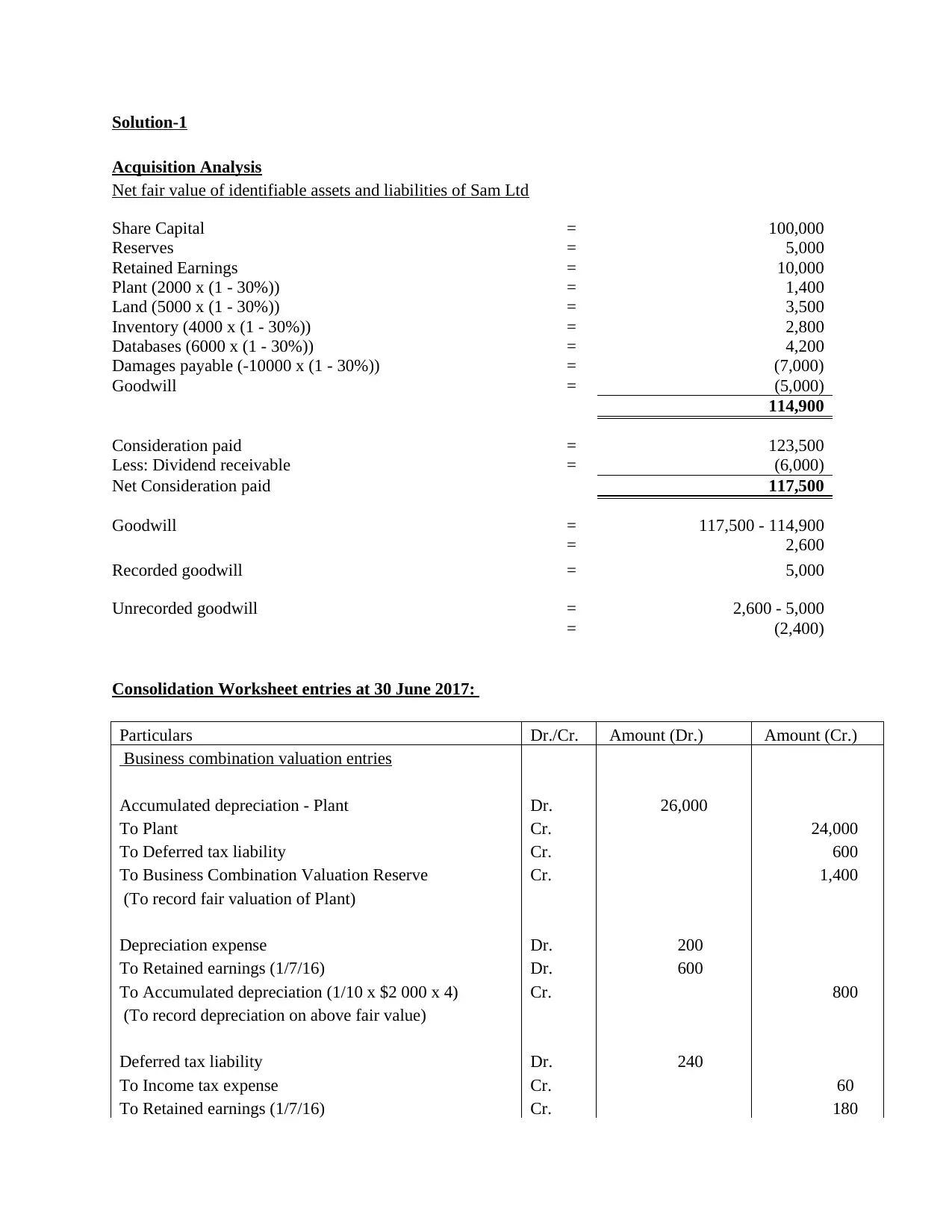

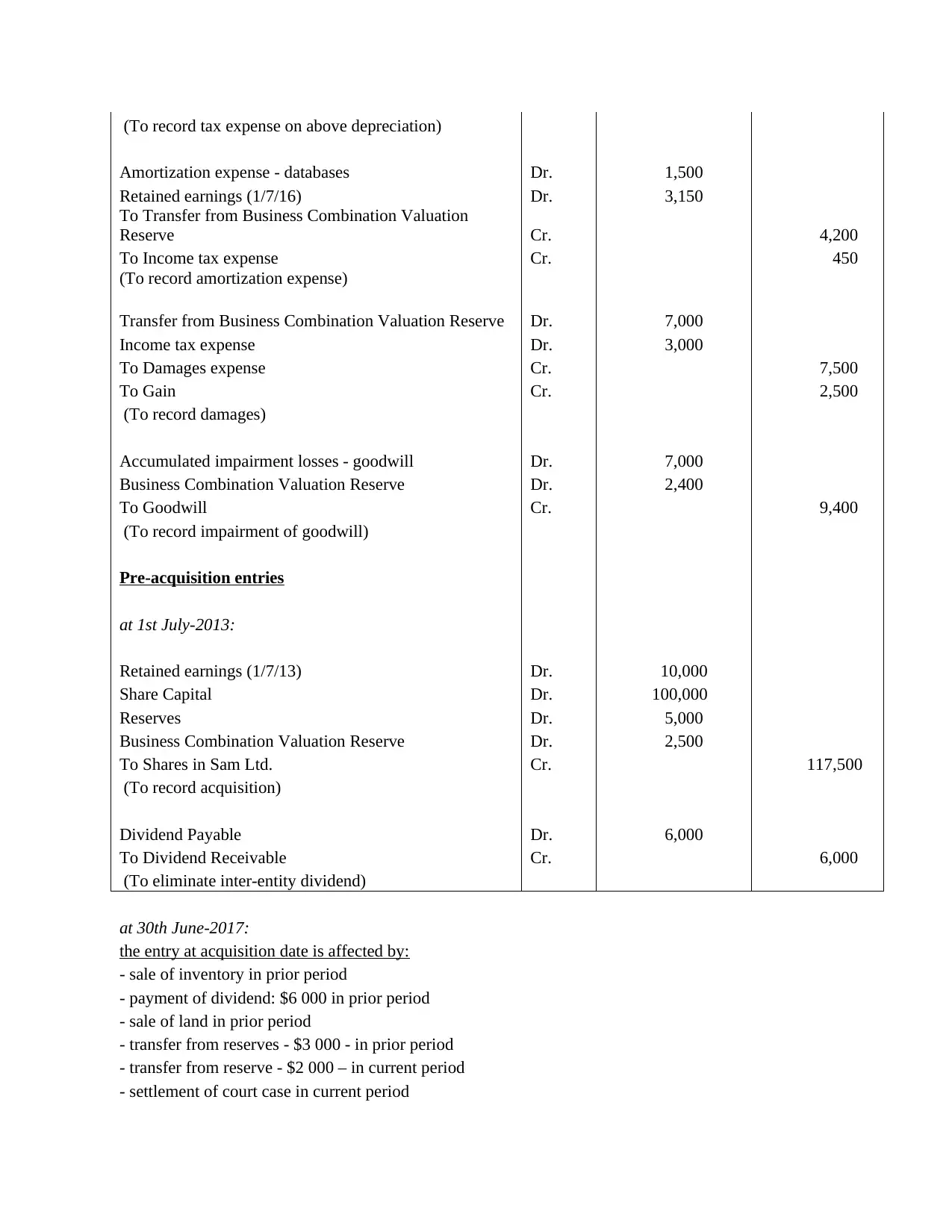

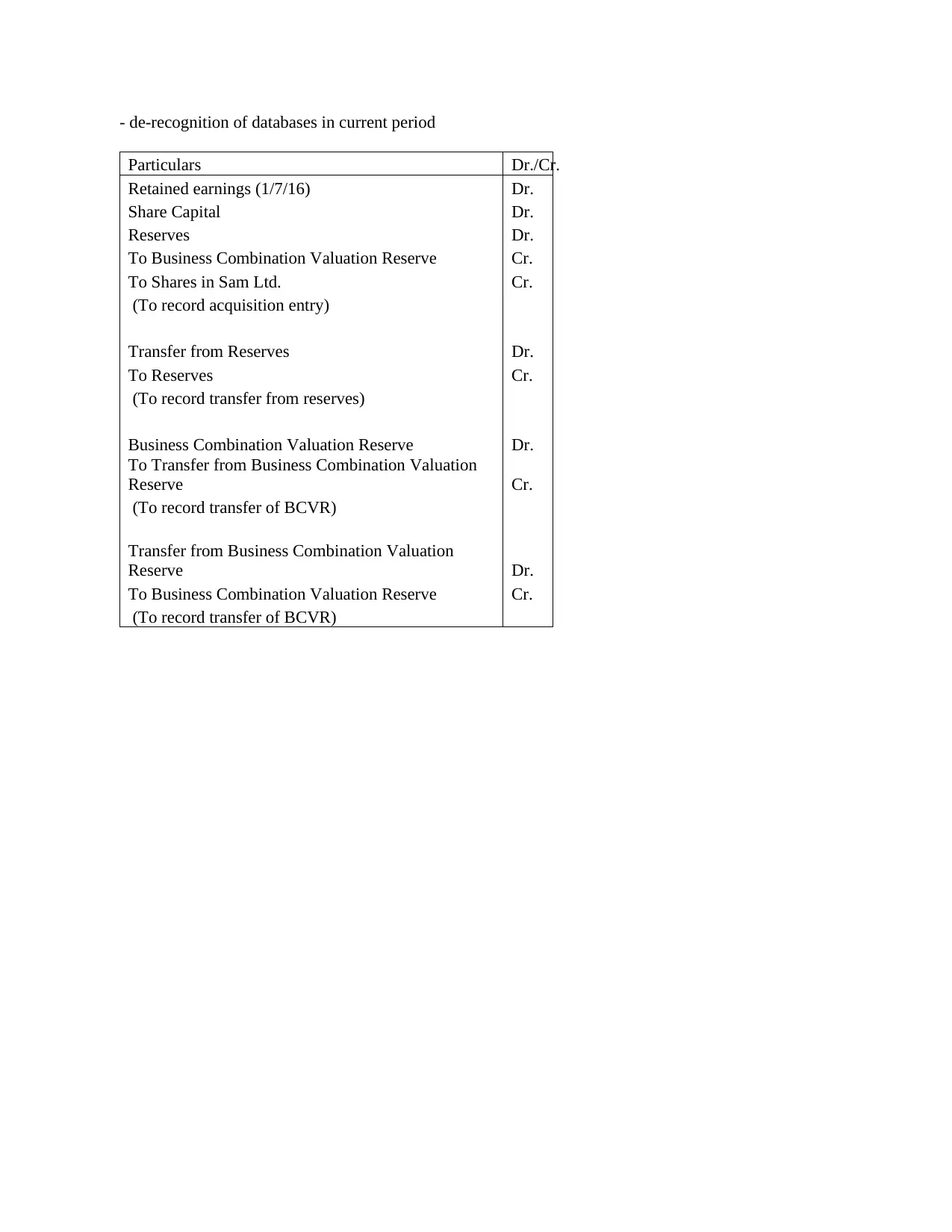

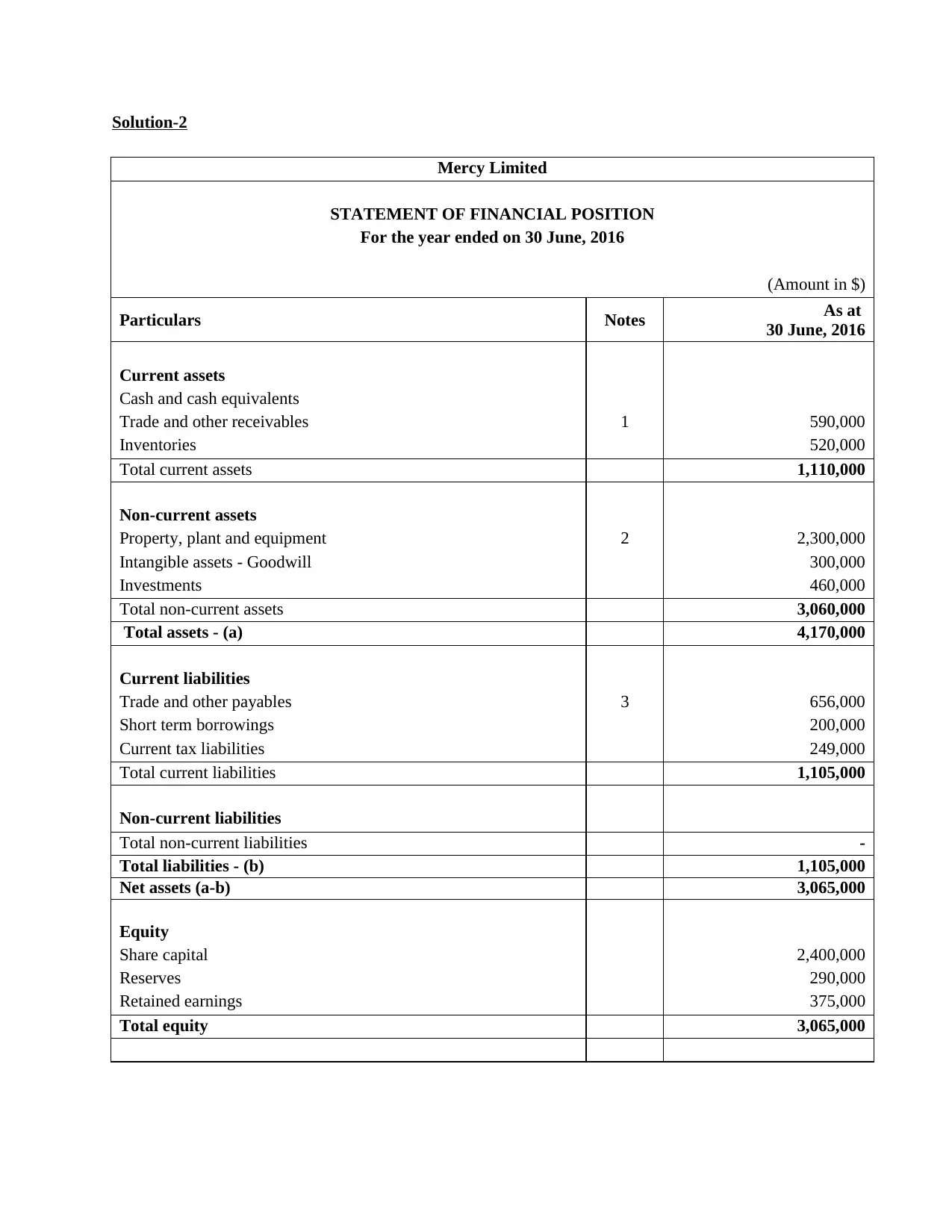

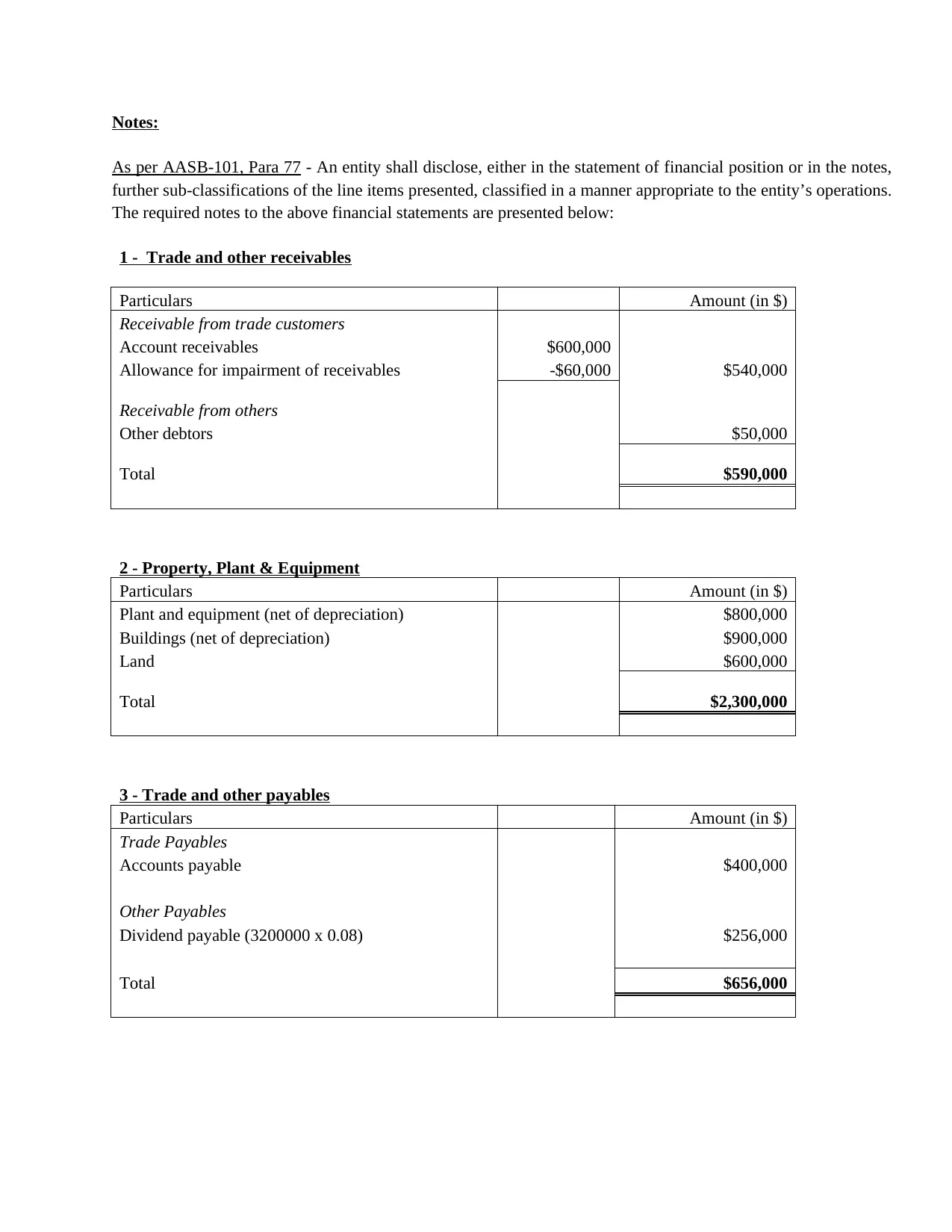

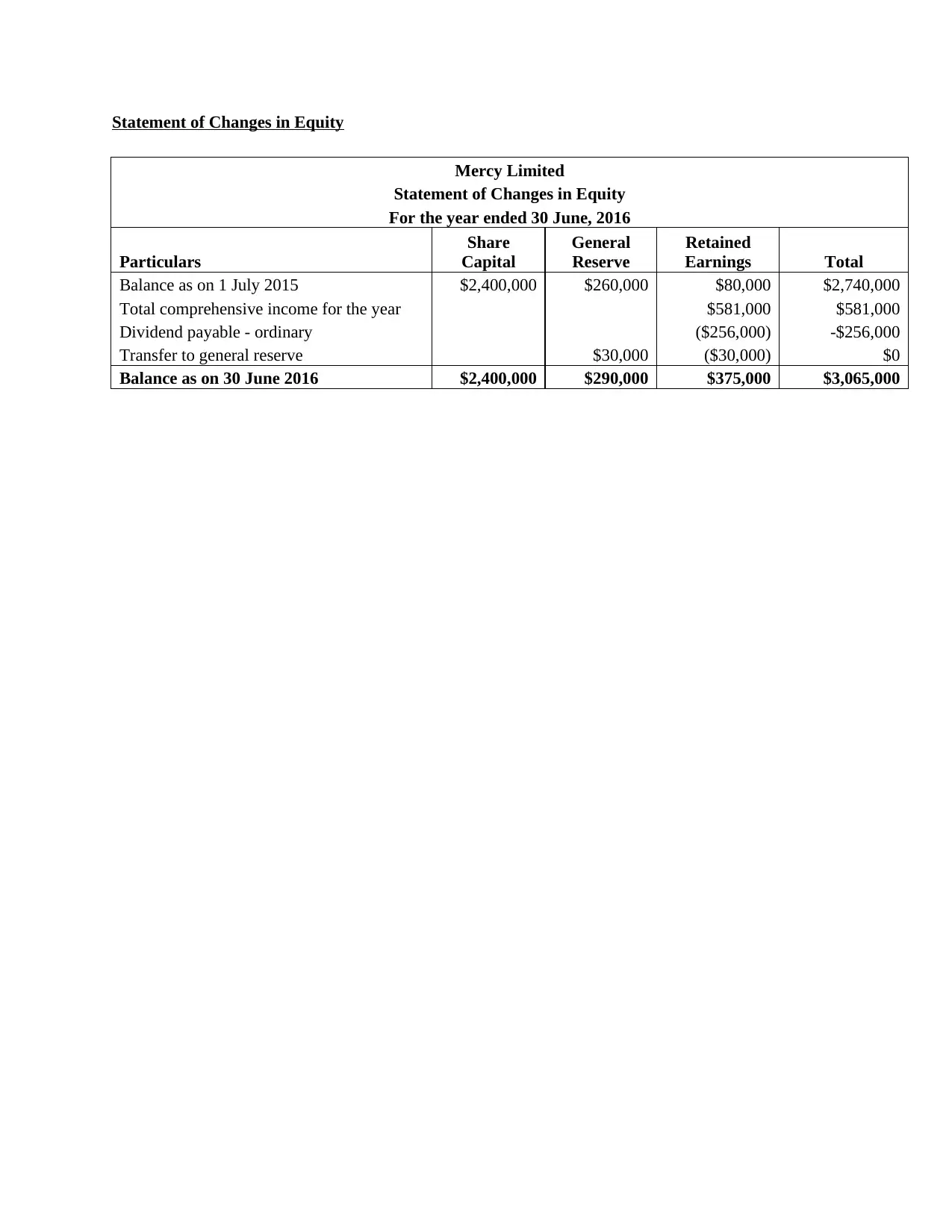

This project presents a detailed analysis of an acquisition, including the calculation of net fair value of identifiable assets and liabilities, goodwill, and the preparation of consolidation worksheet entries. It covers business combination valuation entries, pre-acquisition entries, and adjustments for various transactions. The second part of the project involves the preparation of financial statements for Mercy Limited, including a statement of financial position and a statement of changes in equity. The financial position includes detailed notes on receivables, property, plant, and equipment, and payables. The statement of changes in equity outlines the movements in share capital, reserves, and retained earnings. The project adheres to AASB-101 guidelines and provides a comprehensive overview of financial reporting and consolidation principles.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.