ABC Learning Centre Collapse & Auditing Standards

VerifiedAdded on 2020/02/24

|12

|3126

|72

AI Summary

This assignment analyzes the auditing failures that contributed to the collapse of ABC Learning Centres. It investigates the specific issues that auditors missed, their impact on the company's financial stability, and the subsequent development of the new auditing standard ASA701 as a response to these failings. Students will need to research case studies, reports, and regulatory documents related to the ABC Learning Centres collapse and the evolution of auditing standards.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

AUDITING ISSUES

RESPONSIBLE FOR

COLLAPSE OF ABC

LEARNING CENTRE AND

THE DEVELOPMENT OF

NEW AUDITING

STANDARD ASA701

RESPONSIBLE FOR

COLLAPSE OF ABC

LEARNING CENTRE AND

THE DEVELOPMENT OF

NEW AUDITING

STANDARD ASA701

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

EXECUTIVE SUMMARY

The reason behind presenting this report is to identify the auditing problems that led to the

subside of ABC Learning Centre and problems that ensured the development of new auditing

standard ASA701 Communicating Key Audit Matters in the Independent Auditor’s report.

Additionally, we also discuss the key audit matters which were essential to be unveiled in the

audit report of ABC Learning Centre during the period of its collapse. The report provides us

with an insight of the usefulness of Auditing Standard ASA701 (ISA701) and gives details of

the objective and scope of the said auditing standard. It also clearly provides what key audit

matters are and why is it important to communicate the same in the auditor’s independent

report and how by doing so shareholders are benefitted as they get an insight of the

company’s financial position.

2

The reason behind presenting this report is to identify the auditing problems that led to the

subside of ABC Learning Centre and problems that ensured the development of new auditing

standard ASA701 Communicating Key Audit Matters in the Independent Auditor’s report.

Additionally, we also discuss the key audit matters which were essential to be unveiled in the

audit report of ABC Learning Centre during the period of its collapse. The report provides us

with an insight of the usefulness of Auditing Standard ASA701 (ISA701) and gives details of

the objective and scope of the said auditing standard. It also clearly provides what key audit

matters are and why is it important to communicate the same in the auditor’s independent

report and how by doing so shareholders are benefitted as they get an insight of the

company’s financial position.

2

Table of Contents

INTRODUCTION.....................................................................................................................................4

ABC LEARNING CENTRE-AUDITING ISSUES RESPOSIBLE FOR COLLAPSE OF THE COMPANY..................4

AUDITING STANDARD ASA701 Communicating Key Audit Matters in the Independent Auditor’s

Report and ITS USEFULLNESS………………………………………………………………………………………………...............6

KEY AUDIT MATTERS TO BE DISCLOSED IN THE AUDIT REPORT OF ABC LEARNING CENTRE……………….7

RECOMMENDATION………………………………………………………………………………………………………………………….9

REFERENCES……………………………………………………………………………………………………………………………………11

3

INTRODUCTION.....................................................................................................................................4

ABC LEARNING CENTRE-AUDITING ISSUES RESPOSIBLE FOR COLLAPSE OF THE COMPANY..................4

AUDITING STANDARD ASA701 Communicating Key Audit Matters in the Independent Auditor’s

Report and ITS USEFULLNESS………………………………………………………………………………………………...............6

KEY AUDIT MATTERS TO BE DISCLOSED IN THE AUDIT REPORT OF ABC LEARNING CENTRE……………….7

RECOMMENDATION………………………………………………………………………………………………………………………….9

REFERENCES……………………………………………………………………………………………………………………………………11

3

INTRODUCTION

ABC LEARNING CENTRE –AUDITING ISSUES RESPONSIBLE FOR

COLLAPSE OF THE COMPANY

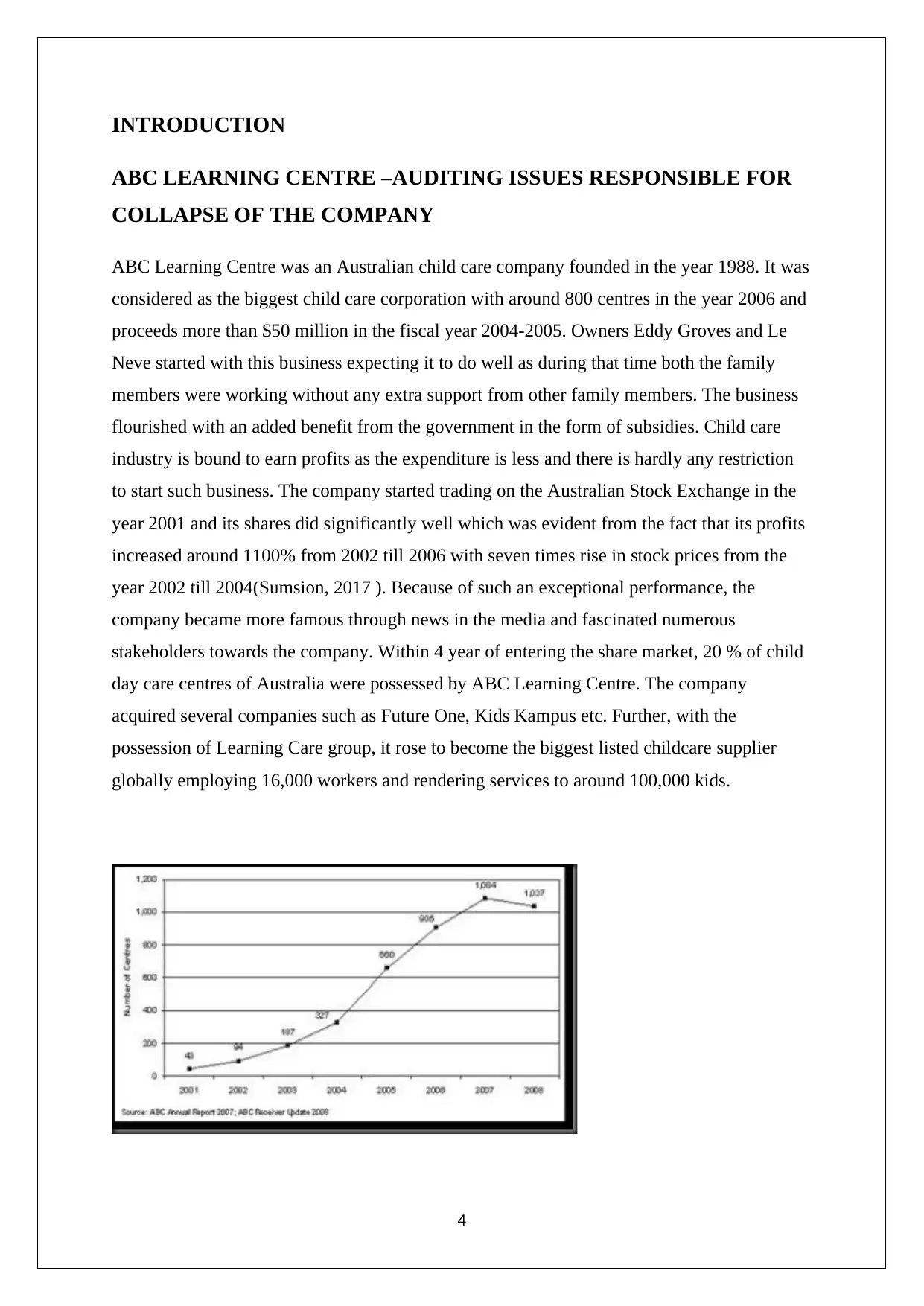

ABC Learning Centre was an Australian child care company founded in the year 1988. It was

considered as the biggest child care corporation with around 800 centres in the year 2006 and

proceeds more than $50 million in the fiscal year 2004-2005. Owners Eddy Groves and Le

Neve started with this business expecting it to do well as during that time both the family

members were working without any extra support from other family members. The business

flourished with an added benefit from the government in the form of subsidies. Child care

industry is bound to earn profits as the expenditure is less and there is hardly any restriction

to start such business. The company started trading on the Australian Stock Exchange in the

year 2001 and its shares did significantly well which was evident from the fact that its profits

increased around 1100% from 2002 till 2006 with seven times rise in stock prices from the

year 2002 till 2004(Sumsion, 2017 ). Because of such an exceptional performance, the

company became more famous through news in the media and fascinated numerous

stakeholders towards the company. Within 4 year of entering the share market, 20 % of child

day care centres of Australia were possessed by ABC Learning Centre. The company

acquired several companies such as Future One, Kids Kampus etc. Further, with the

possession of Learning Care group, it rose to become the biggest listed childcare supplier

globally employing 16,000 workers and rendering services to around 100,000 kids.

4

ABC LEARNING CENTRE –AUDITING ISSUES RESPONSIBLE FOR

COLLAPSE OF THE COMPANY

ABC Learning Centre was an Australian child care company founded in the year 1988. It was

considered as the biggest child care corporation with around 800 centres in the year 2006 and

proceeds more than $50 million in the fiscal year 2004-2005. Owners Eddy Groves and Le

Neve started with this business expecting it to do well as during that time both the family

members were working without any extra support from other family members. The business

flourished with an added benefit from the government in the form of subsidies. Child care

industry is bound to earn profits as the expenditure is less and there is hardly any restriction

to start such business. The company started trading on the Australian Stock Exchange in the

year 2001 and its shares did significantly well which was evident from the fact that its profits

increased around 1100% from 2002 till 2006 with seven times rise in stock prices from the

year 2002 till 2004(Sumsion, 2017 ). Because of such an exceptional performance, the

company became more famous through news in the media and fascinated numerous

stakeholders towards the company. Within 4 year of entering the share market, 20 % of child

day care centres of Australia were possessed by ABC Learning Centre. The company

acquired several companies such as Future One, Kids Kampus etc. Further, with the

possession of Learning Care group, it rose to become the biggest listed childcare supplier

globally employing 16,000 workers and rendering services to around 100,000 kids.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Source: (http://rayanbaaqeel.blogspot.in/2011/06/case-study-of-abc-learning-centers.html)

The above figure clearly shows rise in the number of ABC Learning centre from the year

2001 till 2007. Not only had the centres grown but also its share price from $2 to $13.94.This

expansion was supported by the government with the help of child care benefit schemes as

well as fee subsidies. The said industry was considered as downfall resistant.

However, in the year 2008, in the wake of international economic catastrophe, dreadful

reports were out, of the company’s profit being dropped from over 40% from the last year.

Market assumption increased concerning ABC Learning’s monetary conditions. There was a

dramatic decrease in the price of company’s shares; it fell by over 65 % in a month. Soon, the

company’s securities were no longer trading. Lawful intimidation against the company

intensified and both the owners Eddy Groves and Le Neve resigned from the company in the

month of September, 2008. The collapse of the company is anticipated to have started way

before the organization was aware of it. Controversy arose over the dubious practices

embraced by then accounting firm Pitcher Partners related with auditing of corporation’s

financial records. The company opted for deliberate receivership revealing it’s doubtful

accounting practices in the month of November, 2008. There were several reasons that led to

the collapse of ABC Learning including the growth in the competition, monetary disparities

owing to huge acquisitions and debts. However, the major reason for its failure was

disparities in the fiscal facts given by the management. The financial statement of the

company gave misleading information wherein 72% to 81% of intangible assets majorly

included numerous operating licences comprised the assets in the balance sheet (Baaqeel,

2008). These licences were insignificant but the company professed huge price on them. The

appraisal of these licences fascinated shareholders and increased its value. However, in a

statement by the Australian Securities and Investment Commission it is assured that the

licences were of almost no value to the company. Goodwill of around $37.4 million and

licences of around $647.6 were accounted in the commencement of the fiscal year 2006-07

(Teen, 2012). However, by the fiscal year ending 2007-08, goodwill increased to $271

million and licenses of around $2.4 billion whereas in these 2 years $2 million and $8.4

million were the impairment charges for goodwill and licences .Also, a complaint was

registered that the revaluation of licenses was the basis of profits of $390 million that the

5

The above figure clearly shows rise in the number of ABC Learning centre from the year

2001 till 2007. Not only had the centres grown but also its share price from $2 to $13.94.This

expansion was supported by the government with the help of child care benefit schemes as

well as fee subsidies. The said industry was considered as downfall resistant.

However, in the year 2008, in the wake of international economic catastrophe, dreadful

reports were out, of the company’s profit being dropped from over 40% from the last year.

Market assumption increased concerning ABC Learning’s monetary conditions. There was a

dramatic decrease in the price of company’s shares; it fell by over 65 % in a month. Soon, the

company’s securities were no longer trading. Lawful intimidation against the company

intensified and both the owners Eddy Groves and Le Neve resigned from the company in the

month of September, 2008. The collapse of the company is anticipated to have started way

before the organization was aware of it. Controversy arose over the dubious practices

embraced by then accounting firm Pitcher Partners related with auditing of corporation’s

financial records. The company opted for deliberate receivership revealing it’s doubtful

accounting practices in the month of November, 2008. There were several reasons that led to

the collapse of ABC Learning including the growth in the competition, monetary disparities

owing to huge acquisitions and debts. However, the major reason for its failure was

disparities in the fiscal facts given by the management. The financial statement of the

company gave misleading information wherein 72% to 81% of intangible assets majorly

included numerous operating licences comprised the assets in the balance sheet (Baaqeel,

2008). These licences were insignificant but the company professed huge price on them. The

appraisal of these licences fascinated shareholders and increased its value. However, in a

statement by the Australian Securities and Investment Commission it is assured that the

licences were of almost no value to the company. Goodwill of around $37.4 million and

licences of around $647.6 were accounted in the commencement of the fiscal year 2006-07

(Teen, 2012). However, by the fiscal year ending 2007-08, goodwill increased to $271

million and licenses of around $2.4 billion whereas in these 2 years $2 million and $8.4

million were the impairment charges for goodwill and licences .Also, a complaint was

registered that the revaluation of licenses was the basis of profits of $390 million that the

5

company made between the years 2001 and 2005. Also, potential cash flows of the company,

of which the company was unsure of was the cause of its increased value.

There were different views by different auditors on the practice adopted for auditing.

Incompetent judgment was given by the company’s auditors, Pitcher Partners from the time

of their engagement with the company in the year 2003. The accounting practise followed

showed exaggerated picture of the growth of the company. As a result, it was forecasted the

company to make $200 million of profits in the month of January 2008. This profitable

business ensnared shareholders which helped it to expand globally. However, the major

auditing issue accounting for the downfall of the company were incompetence on the part of

the auditors of the company. The company intended to disburse $70 million as per the

proclamation from a share market in the year 2008. (Walsh, 2015). Another major issue with

ABC Learning Centre was the existence of related party transactions. There was failure on

the part of company in adhering to corporate governance measures. The auditors failed to

provide substantial facts related to exact accounting of a number of fees and subsidies,

categorization of items that generate revenue and for its judgement on the company for being

a going concern. The auditor failed miserably in predicting threat and this all resulted in

overvaluation of company’s revenue which led to its collapse.

AUDITING STANDARD ASA701 Communicating Key Audit Matters in the

Independent Auditor’s Report and ITS USEFULLNESS

The Auditing Standard ASA701 Communicating Key Audit Matters in the Independent

Auditor’s Report was issued by The Auditing and Assurance Standards Board (AUASB) in

the month of December, 2015. It provides information to auditors in relation to new Key

Audit Matters (KAMs) that are obligatory to be incorporated in their reports (Bullock, 2017).

All the listed Australian corporations for fiscal year ending as of 15th December, 2016 are

bound to adhere to the said accounting standard. The main intend for the development of the

standard is to provide better understanding of the accounts of a company to its shareholders

and to augment auditors reporting. It is pertinent in agreement with the Corporations

Act 2001; an audit of a financial report for a financial year, or an audit of a financial report

for a half year and also an audit of a financial report, or a whole of financial statements, for

any other purpose. For a better understanding of the said standard, it is important to be

acquainted with the meaning of Key Audit Matters (KAMs). All substantial matters as per

auditors qualified perception, which is to be included in the audit of the fiscal report of the

6

of which the company was unsure of was the cause of its increased value.

There were different views by different auditors on the practice adopted for auditing.

Incompetent judgment was given by the company’s auditors, Pitcher Partners from the time

of their engagement with the company in the year 2003. The accounting practise followed

showed exaggerated picture of the growth of the company. As a result, it was forecasted the

company to make $200 million of profits in the month of January 2008. This profitable

business ensnared shareholders which helped it to expand globally. However, the major

auditing issue accounting for the downfall of the company were incompetence on the part of

the auditors of the company. The company intended to disburse $70 million as per the

proclamation from a share market in the year 2008. (Walsh, 2015). Another major issue with

ABC Learning Centre was the existence of related party transactions. There was failure on

the part of company in adhering to corporate governance measures. The auditors failed to

provide substantial facts related to exact accounting of a number of fees and subsidies,

categorization of items that generate revenue and for its judgement on the company for being

a going concern. The auditor failed miserably in predicting threat and this all resulted in

overvaluation of company’s revenue which led to its collapse.

AUDITING STANDARD ASA701 Communicating Key Audit Matters in the

Independent Auditor’s Report and ITS USEFULLNESS

The Auditing Standard ASA701 Communicating Key Audit Matters in the Independent

Auditor’s Report was issued by The Auditing and Assurance Standards Board (AUASB) in

the month of December, 2015. It provides information to auditors in relation to new Key

Audit Matters (KAMs) that are obligatory to be incorporated in their reports (Bullock, 2017).

All the listed Australian corporations for fiscal year ending as of 15th December, 2016 are

bound to adhere to the said accounting standard. The main intend for the development of the

standard is to provide better understanding of the accounts of a company to its shareholders

and to augment auditors reporting. It is pertinent in agreement with the Corporations

Act 2001; an audit of a financial report for a financial year, or an audit of a financial report

for a half year and also an audit of a financial report, or a whole of financial statements, for

any other purpose. For a better understanding of the said standard, it is important to be

acquainted with the meaning of Key Audit Matters (KAMs). All substantial matters as per

auditors qualified perception, which is to be included in the audit of the fiscal report of the

6

present year accounts for key audit matters. They are chosen from matters interfaced with

those entrusted with authority. As per the said standard, the major purpose of the auditor is

identification of such key audit matters, drawing judgment on the financial statement and

conveying the detailed analysis in his report.

Auditing Standard ASA701 explains auditor’s accountability in relation to key audit matters.

It is the duty of the auditor to convey key audit matters in his report which will not only

clearly explain auditor’s judgement for the matters he conveys but also the substance and

structure of the statement. Disclosure of key audit matters provides better clarity and will

further augment the significance of auditor’s report. Anticipated users will be benefited as

they will gain extra knowledge of the fiscal report from key audit matters which will help in

better understanding of those important matters. Further, it will help them in getting

considerable perception of the entity and also in identifying major fields of administration

prudence. Moving forward, such conveyance might offer projected users a foundation for

getting involved with the administration and with those who are in authority in relation to the

organization, the assessment and the assessed financial statement. These key audit matters are

in agreement with the auditor’s viewpoint on the complete financial statement and not an

alternative for revelations in the fiscal report that the relevant financial reporting structure

requires administration to make, or that are otherwise essential to attain reasonable

arrangement; an alternative for the auditor articulating a customized view when necessary by

the situation of a definite audit appointment in accordance with ASA 705; an alternative for

reporting in agreement with ASA 570 when a material uncertainty exists relating to events or

conditions that may cast noteworthy reservation on an entity’s ability to continue as a going

concern; or a detach view on individual matters. Assessment of general purpose fiscal

statements of listed companies requires adherence to this said auditing standard. It is

applicable in conditions wherein auditor determines to convey such matters in auditing report

of the company. It is also pertinent when auditor is lawfully enforced to convey such matters

in the report.

However, it is very important to ascertain key audit matters. Auditor should take into

consideration greater projected risk area, considerable auditor discernment in areas which

requires important administration prudence and the consequence of important dealings on the

audit while deciding key audit matters (Pratt, 2014)

7

those entrusted with authority. As per the said standard, the major purpose of the auditor is

identification of such key audit matters, drawing judgment on the financial statement and

conveying the detailed analysis in his report.

Auditing Standard ASA701 explains auditor’s accountability in relation to key audit matters.

It is the duty of the auditor to convey key audit matters in his report which will not only

clearly explain auditor’s judgement for the matters he conveys but also the substance and

structure of the statement. Disclosure of key audit matters provides better clarity and will

further augment the significance of auditor’s report. Anticipated users will be benefited as

they will gain extra knowledge of the fiscal report from key audit matters which will help in

better understanding of those important matters. Further, it will help them in getting

considerable perception of the entity and also in identifying major fields of administration

prudence. Moving forward, such conveyance might offer projected users a foundation for

getting involved with the administration and with those who are in authority in relation to the

organization, the assessment and the assessed financial statement. These key audit matters are

in agreement with the auditor’s viewpoint on the complete financial statement and not an

alternative for revelations in the fiscal report that the relevant financial reporting structure

requires administration to make, or that are otherwise essential to attain reasonable

arrangement; an alternative for the auditor articulating a customized view when necessary by

the situation of a definite audit appointment in accordance with ASA 705; an alternative for

reporting in agreement with ASA 570 when a material uncertainty exists relating to events or

conditions that may cast noteworthy reservation on an entity’s ability to continue as a going

concern; or a detach view on individual matters. Assessment of general purpose fiscal

statements of listed companies requires adherence to this said auditing standard. It is

applicable in conditions wherein auditor determines to convey such matters in auditing report

of the company. It is also pertinent when auditor is lawfully enforced to convey such matters

in the report.

However, it is very important to ascertain key audit matters. Auditor should take into

consideration greater projected risk area, considerable auditor discernment in areas which

requires important administration prudence and the consequence of important dealings on the

audit while deciding key audit matters (Pratt, 2014)

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

KEY AUDIT MATTERS TO BE DISCLOSED IN THE AUDIT

REPORT OF ABC LEARNING CENTRE

The ABC Learning collapse has been considered a major one in the history of company

failure. Since the purpose of accounting standard 701 is to provide more liberty in revealing

vigorous and significant details on key audit matters to the intended users of the financial

report, audit report of ABC Learning was lacking such information, its value was inflated and

most of its intangible assets in the asset side of financial statement were goodwill and

licences which are estimated to have no value. The said standard comprises of not much

changes in the auditors judgement but the statistics and data which is revealed to its users.

Now, the significant matters which were a part of the internal audit report will be affixed

with the available fiscal reports. However, in the case of ABC Learning, its liabilities were

almost invariable in between the months starting from June till December. Owing to

financing again with new loans at a lower rate of interest, liabilities of around $1.1 billion

were re-categorised as long term financial obligations. This matter accounts for significant

importance and users were not aware of what was happening within the organization as

auditing report had shown positive future prospects of the company.

Australian Securities and Investments Commission suspended the ex- auditor of ABC

Learning, Simon Andrew Peter Green for five years from performing his duties (Kruger,

2012). It is clear from the reports that former Pitching Partner was unsuccessful in

performing his services as an auditor. He could not gather satisfactory audit substantiation

associated with precise accounting handling for a variety of fees that lead to over valuation of

the company’s revenue. This particular matter was one of the major key auditing matters that

were not revealed to its intended users. Hence, had ASA701 been released before the collapse

of ABC Learning Centre, it could have been avoided. In the case of the said company, auditor

did not perform efficiently and ignored the area of high projected risk which led to

misstatement of financial report (ASIC, 2012). Further, he could not gain substantial proof to

categorize the revenue items which once more resulted in misstatement of the financial

reports as there were items which were inaccurately categorised as returns and these were

mostly not a part of child care services offered by the company. Miscommunication of this

particular key audit matter resulted in overvaluation of its income.

8

REPORT OF ABC LEARNING CENTRE

The ABC Learning collapse has been considered a major one in the history of company

failure. Since the purpose of accounting standard 701 is to provide more liberty in revealing

vigorous and significant details on key audit matters to the intended users of the financial

report, audit report of ABC Learning was lacking such information, its value was inflated and

most of its intangible assets in the asset side of financial statement were goodwill and

licences which are estimated to have no value. The said standard comprises of not much

changes in the auditors judgement but the statistics and data which is revealed to its users.

Now, the significant matters which were a part of the internal audit report will be affixed

with the available fiscal reports. However, in the case of ABC Learning, its liabilities were

almost invariable in between the months starting from June till December. Owing to

financing again with new loans at a lower rate of interest, liabilities of around $1.1 billion

were re-categorised as long term financial obligations. This matter accounts for significant

importance and users were not aware of what was happening within the organization as

auditing report had shown positive future prospects of the company.

Australian Securities and Investments Commission suspended the ex- auditor of ABC

Learning, Simon Andrew Peter Green for five years from performing his duties (Kruger,

2012). It is clear from the reports that former Pitching Partner was unsuccessful in

performing his services as an auditor. He could not gather satisfactory audit substantiation

associated with precise accounting handling for a variety of fees that lead to over valuation of

the company’s revenue. This particular matter was one of the major key auditing matters that

were not revealed to its intended users. Hence, had ASA701 been released before the collapse

of ABC Learning Centre, it could have been avoided. In the case of the said company, auditor

did not perform efficiently and ignored the area of high projected risk which led to

misstatement of financial report (ASIC, 2012). Further, he could not gain substantial proof to

categorize the revenue items which once more resulted in misstatement of the financial

reports as there were items which were inaccurately categorised as returns and these were

mostly not a part of child care services offered by the company. Miscommunication of this

particular key audit matter resulted in overvaluation of its income.

8

Another flaw of the former auditor was that he could not gather considerable information to

facilitate any rational auditor to establish that the said company was a going concern and will

continue to operate in future. Hence, it proves that the auditing of the company’s financial

statement was not done efficiently and it lacked auditor’s competence. Hence, assessment of

a company as a going concern again accounts for another key accounting matter. He did not

work proficiently as he couldn’t draw facts to sustain his stand in relation to wages and

salaries, party transaction etc. However, an auditor is considered as the caretaker who is

expected to guarantee efficiency when it comes to the value of financial statements. Moving

forward, another fault on the part of the ex-auditor was that it couldn’t provide substantiation

in maintaining his judgement that there was no inaccuracy in the financial statement of the

company. However, as per Accounting Standard 701, conveyance of key audit matter

provides precision of the audit and auditor forms judgement on the complete financial report.

The auditor could not effectively file trial that was taken to access the possibility of scam. He

lacked the competence to gauge the possible financial threat. Lastly, there was a major fault

that led to the fall of ABC Learning Centre as the auditor was inadequate in qualified

perception and cynicism while conducting audit of the company’s financial report for the

year 2007.Hence, it is proven from the above issues faced by the company relating to the

audit were majorly responsible for its collapse. Hence, if the company adhered to the

provisions of ASA701, the scenario would have been entirely different and stakeholders

would have got clear picture of the entity.

RECOMMENDATION

At the end, we recommend that the auditing standard ASA701 Communicating Key Audit

Matters in the Independent Auditor’s Report was developed to provide its intended users to

understand the company they are investing their money in. The said standard will be useful to

get an insight of the profits of the company. By following ASA701, all the significant

information that was a part of internal audit report will be affixed with financial statement

which will in turn help the projected shareholders to get a better view of the company. Clear

understanding of key audit matters and communication of the same in independent auditors

report will surely involve greater participation amongst auditors, audit and managing

committees. Further, it is also clear from the above report that the collapse of ABC Learning

9

facilitate any rational auditor to establish that the said company was a going concern and will

continue to operate in future. Hence, it proves that the auditing of the company’s financial

statement was not done efficiently and it lacked auditor’s competence. Hence, assessment of

a company as a going concern again accounts for another key accounting matter. He did not

work proficiently as he couldn’t draw facts to sustain his stand in relation to wages and

salaries, party transaction etc. However, an auditor is considered as the caretaker who is

expected to guarantee efficiency when it comes to the value of financial statements. Moving

forward, another fault on the part of the ex-auditor was that it couldn’t provide substantiation

in maintaining his judgement that there was no inaccuracy in the financial statement of the

company. However, as per Accounting Standard 701, conveyance of key audit matter

provides precision of the audit and auditor forms judgement on the complete financial report.

The auditor could not effectively file trial that was taken to access the possibility of scam. He

lacked the competence to gauge the possible financial threat. Lastly, there was a major fault

that led to the fall of ABC Learning Centre as the auditor was inadequate in qualified

perception and cynicism while conducting audit of the company’s financial report for the

year 2007.Hence, it is proven from the above issues faced by the company relating to the

audit were majorly responsible for its collapse. Hence, if the company adhered to the

provisions of ASA701, the scenario would have been entirely different and stakeholders

would have got clear picture of the entity.

RECOMMENDATION

At the end, we recommend that the auditing standard ASA701 Communicating Key Audit

Matters in the Independent Auditor’s Report was developed to provide its intended users to

understand the company they are investing their money in. The said standard will be useful to

get an insight of the profits of the company. By following ASA701, all the significant

information that was a part of internal audit report will be affixed with financial statement

which will in turn help the projected shareholders to get a better view of the company. Clear

understanding of key audit matters and communication of the same in independent auditors

report will surely involve greater participation amongst auditors, audit and managing

committees. Further, it is also clear from the above report that the collapse of ABC Learning

9

Centre is the correct example of auditing failure in the history. One of the major reasons for

its collapse is to be blamed on the auditors.

10

its collapse is to be blamed on the auditors.

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES:

Sumsion, J., (2017), ABC Learning and Australian early education and care: a retrospective

ethical audit of a radical experiment Available at

https://www.cela.org.au/wp-content/uploads/2017/06/AttachmentChildcareMarkets.pdf

(Accessed 17th September 2017)

Baaqeel, R., (2008), Case Study Of Learning Centres CollapseAvailable at

http://rayanbaaqeel.blogspot.in/2011/06/case-study-of-abc-learning-centers.html / (Accessed

18th September 2017 )

Teen, Y.M., (2012), The ABC of a corporate collapse Available at

http://governanceforstakeholders.com/2012/12/28/the-abc-of-a-corporate-collapse/ (Accessed

18th September 2017)

Walsh, L., (2015), Key corporate governance systems ‘missing’ from ABC Available at

http://www.couriermail.com.au/news/key-corporate-governance-systems-missing-from-abc/

news-story/f601d3e4242f16efbc70610f9707de05?sv=96f188f44e8845619b7d48fa7cf73f91

(Accessed 17th September 2017)

Bullock, L., (2017), Auditors reminded on crucial 2017 changes Available at

https://www.accountantsdaily.com.au/tax-compliance/10014-auditors-reminded-on-crucial-

2017-changes (Accessed 18th September 2017)

Pratt, H., (2014), New auditing reporting requirements are imminent Available at

file:///C:/Users/hp/Downloads/Dec14%20-%20AuditorReporting%20(2).pdf. (Accessed 18th

September 2017)

Kruger, C., (2012), Five –year suspension for former ABC Learning Auditor Available at

http://www.smh.com.au/business/fiveyear-suspension-for-former-abc-learning-auditor-

20120808-23uj8.html (Accessed 18th September 2017)

ASIC., (2012), 12-186MR Former ABC Learning Centres auditor prevented from auditing

companies for five years Available at http://asic.gov.au/about-asic/media-centre/find-a-

media-release/2012-releases/12-186mr-former-abc-learning-centres-auditor-prevented-from-

auditing-companies-for-five-years/ (Accessed 18th September 2017)

11

Sumsion, J., (2017), ABC Learning and Australian early education and care: a retrospective

ethical audit of a radical experiment Available at

https://www.cela.org.au/wp-content/uploads/2017/06/AttachmentChildcareMarkets.pdf

(Accessed 17th September 2017)

Baaqeel, R., (2008), Case Study Of Learning Centres CollapseAvailable at

http://rayanbaaqeel.blogspot.in/2011/06/case-study-of-abc-learning-centers.html / (Accessed

18th September 2017 )

Teen, Y.M., (2012), The ABC of a corporate collapse Available at

http://governanceforstakeholders.com/2012/12/28/the-abc-of-a-corporate-collapse/ (Accessed

18th September 2017)

Walsh, L., (2015), Key corporate governance systems ‘missing’ from ABC Available at

http://www.couriermail.com.au/news/key-corporate-governance-systems-missing-from-abc/

news-story/f601d3e4242f16efbc70610f9707de05?sv=96f188f44e8845619b7d48fa7cf73f91

(Accessed 17th September 2017)

Bullock, L., (2017), Auditors reminded on crucial 2017 changes Available at

https://www.accountantsdaily.com.au/tax-compliance/10014-auditors-reminded-on-crucial-

2017-changes (Accessed 18th September 2017)

Pratt, H., (2014), New auditing reporting requirements are imminent Available at

file:///C:/Users/hp/Downloads/Dec14%20-%20AuditorReporting%20(2).pdf. (Accessed 18th

September 2017)

Kruger, C., (2012), Five –year suspension for former ABC Learning Auditor Available at

http://www.smh.com.au/business/fiveyear-suspension-for-former-abc-learning-auditor-

20120808-23uj8.html (Accessed 18th September 2017)

ASIC., (2012), 12-186MR Former ABC Learning Centres auditor prevented from auditing

companies for five years Available at http://asic.gov.au/about-asic/media-centre/find-a-

media-release/2012-releases/12-186mr-former-abc-learning-centres-auditor-prevented-from-

auditing-companies-for-five-years/ (Accessed 18th September 2017)

11

12

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.