ACC91210 Finance for Managers: Capital Budgeting and Policy Analysis

VerifiedAdded on 2023/01/20

|26

|3100

|50

Report

AI Summary

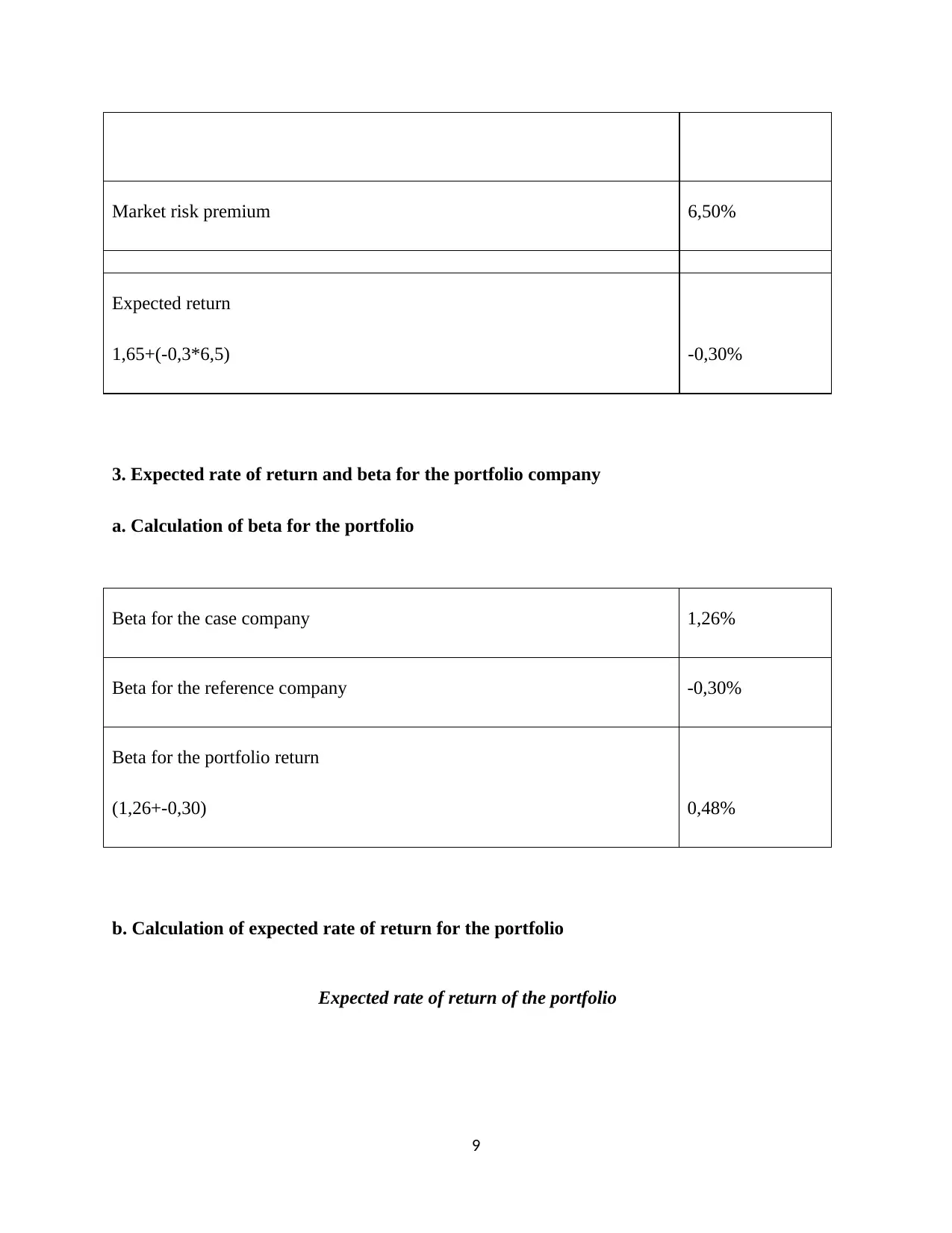

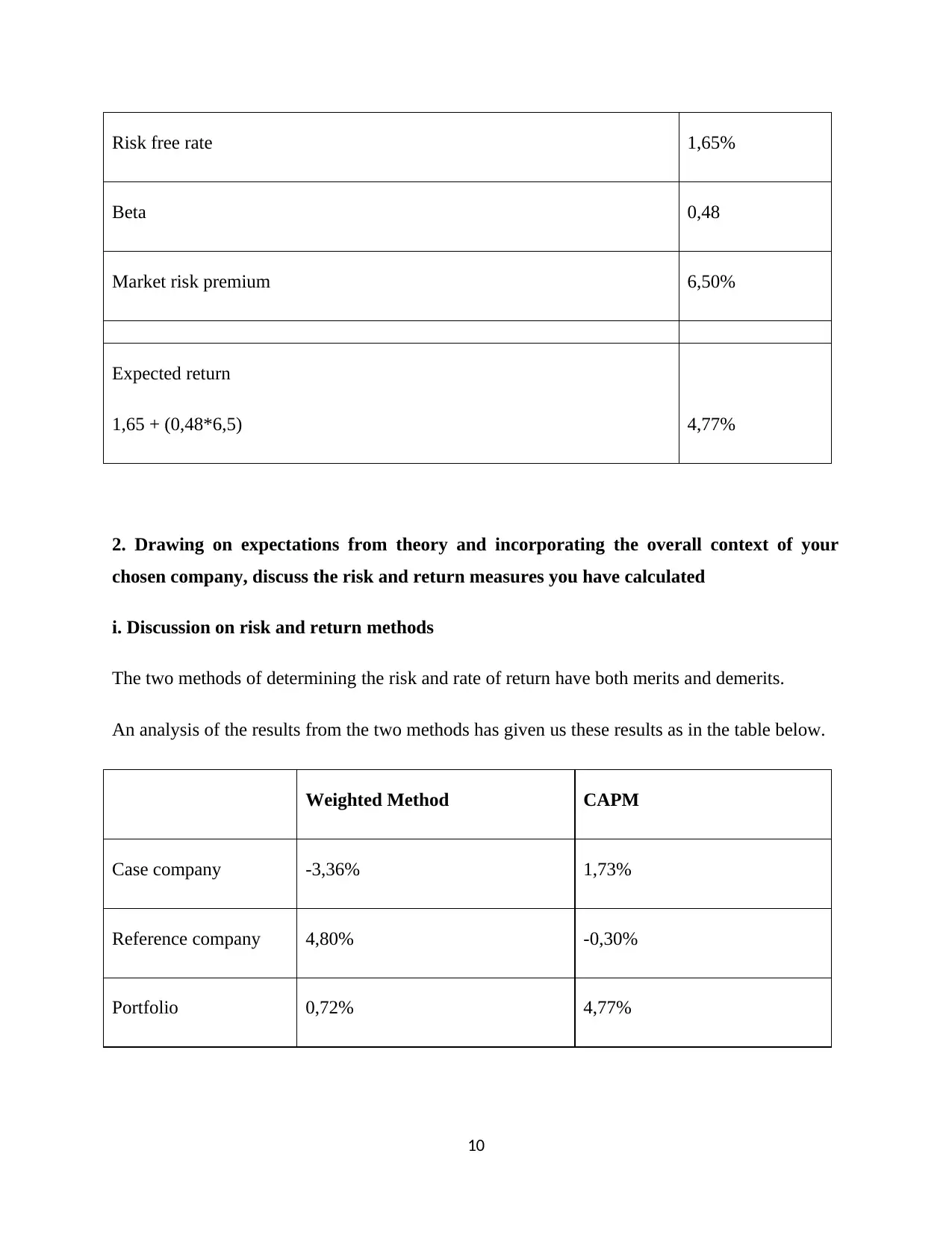

This report provides a comprehensive analysis of capital structure, payout policies, and capital budgeting, as applied to a case study company within the context of ACC91210 Finance for Managers. The report begins with an examination of capital structure and payout policies, including an evaluation of risk and return measures using the Capital Asset Pricing Model (CAPM) and weighted average methods. It then transitions to capital budgeting, focusing on a financial analysis of a proposed project involving recycling sachet waste, using techniques such as payback period and net present value (NPV). The analysis includes detailed financial projections and cash flow calculations, aiming to determine the project's feasibility and its potential impact on the company's financial performance, addressing the importance of capital investment decisions and strategic financial planning.

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.