Analysis of Revenue Recognition, Trial Balances and Accounting Methods

VerifiedAdded on 2023/01/09

|7

|1090

|26

Report

AI Summary

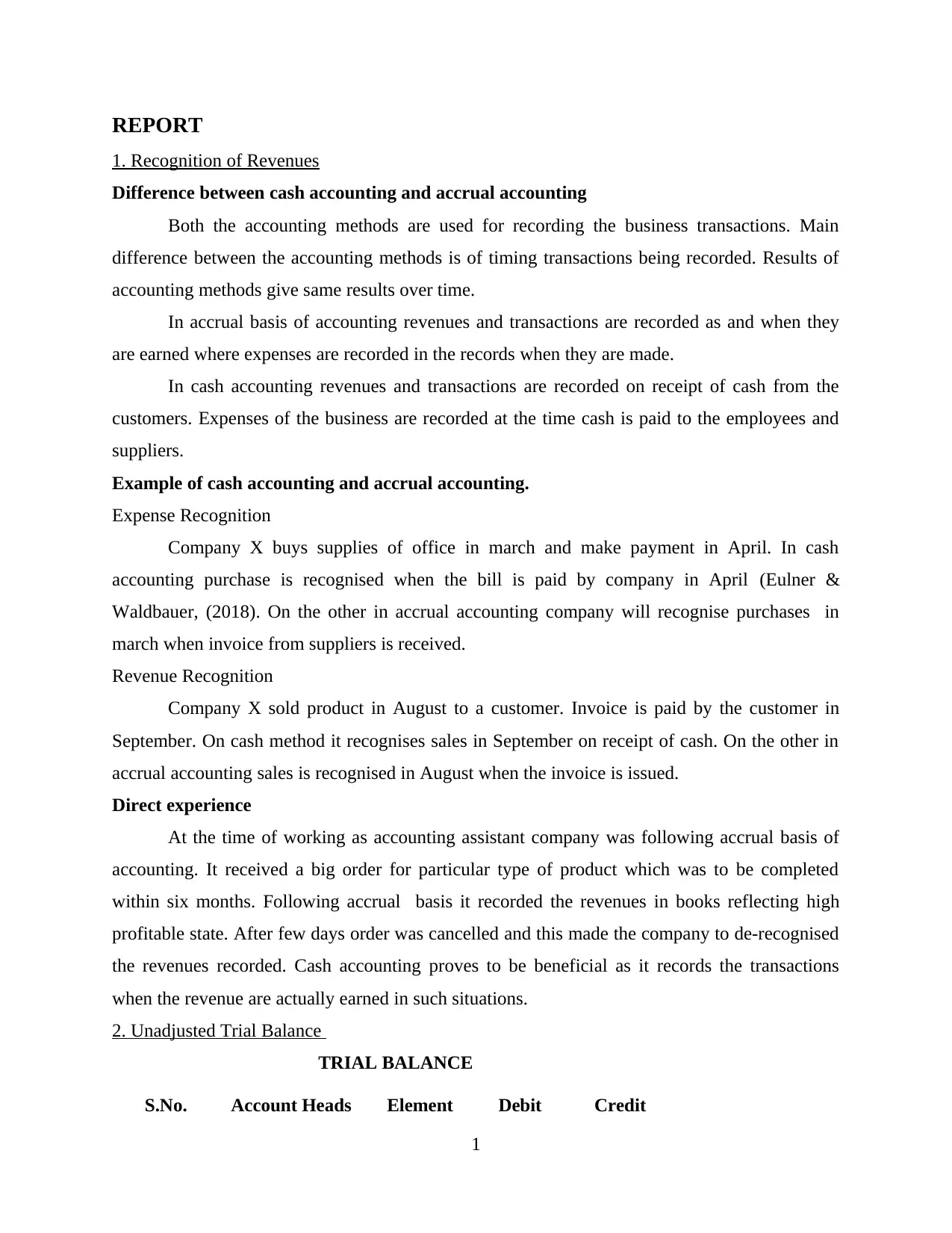

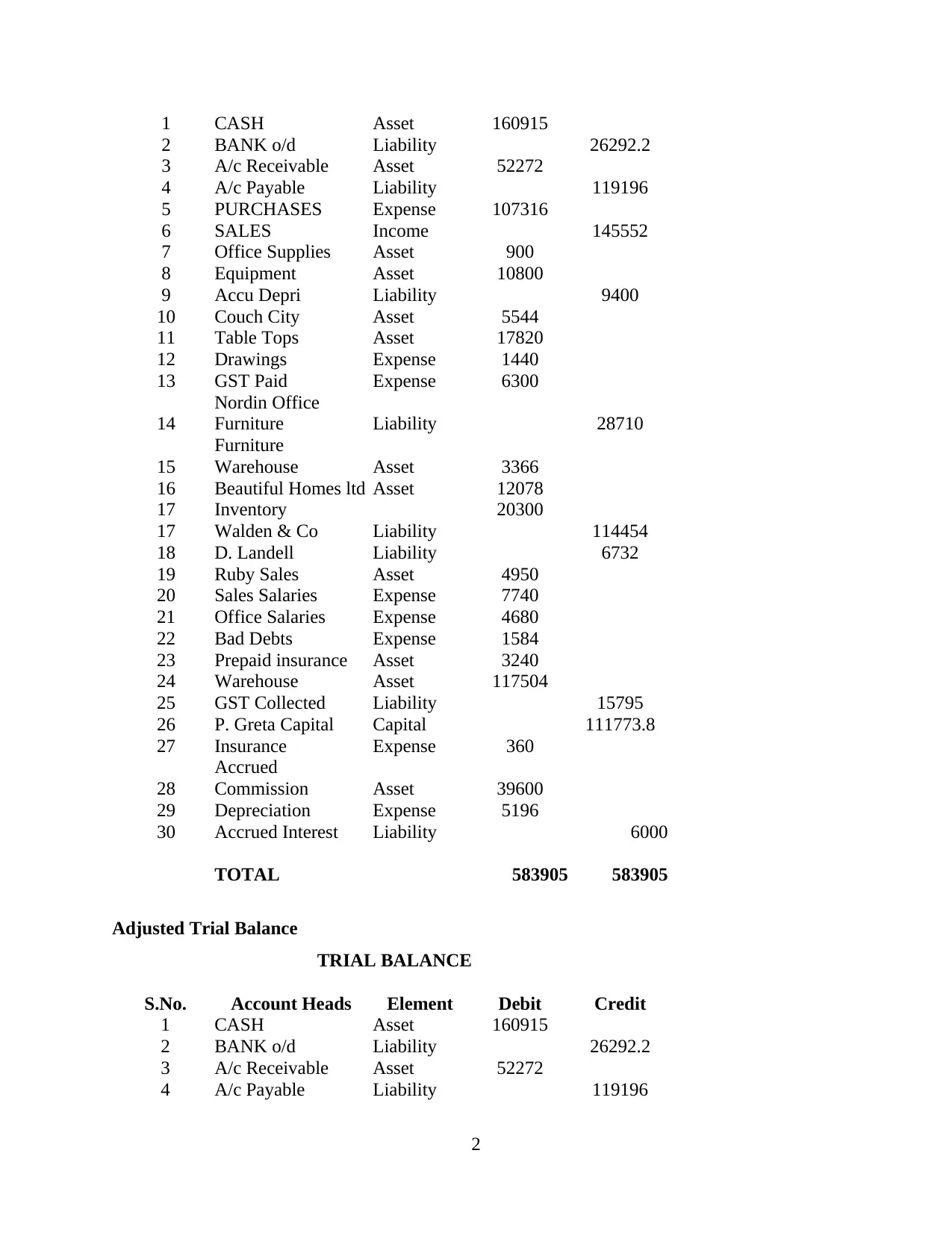

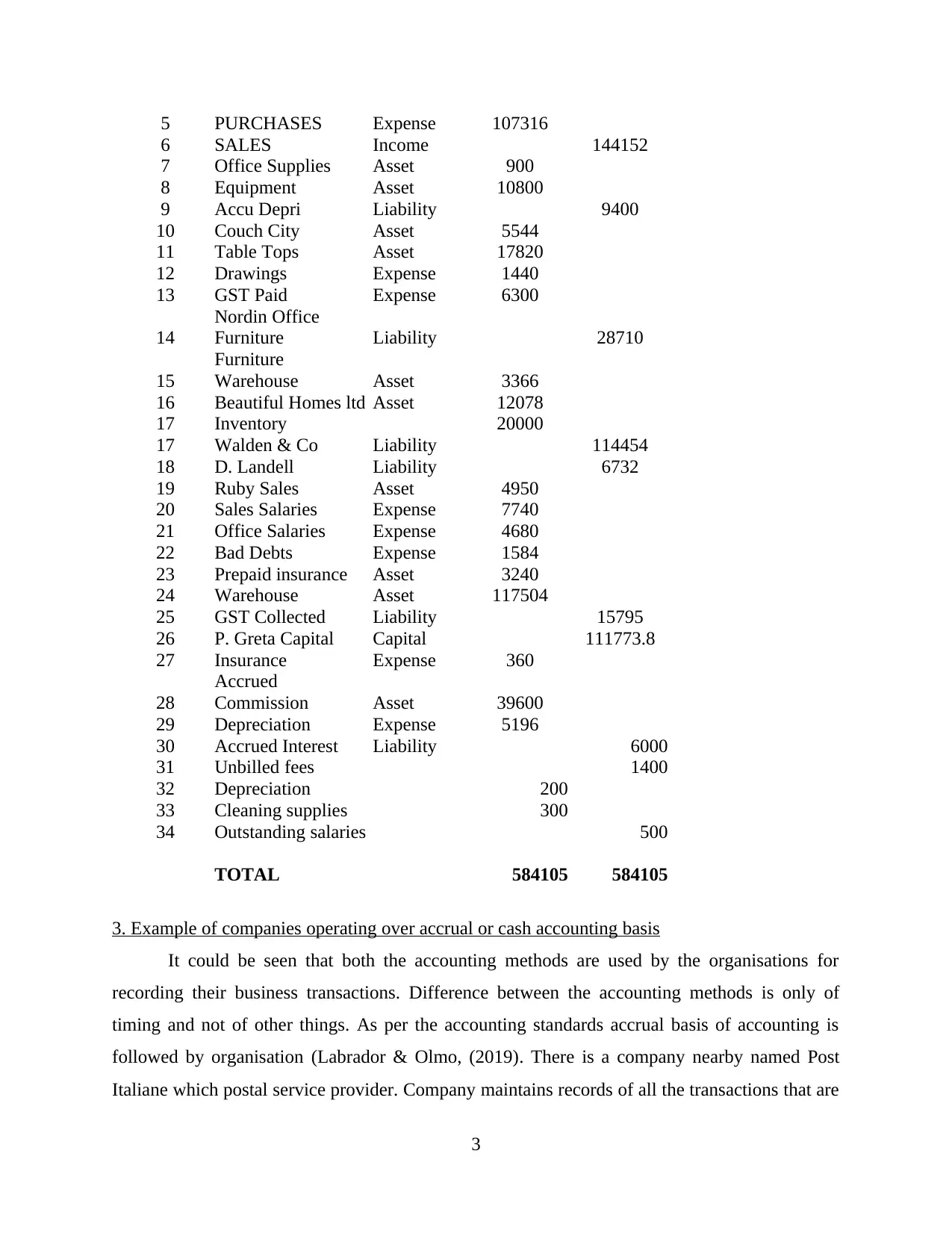

This report delves into the crucial aspects of revenue recognition and its impact on financial reporting. It differentiates between accrual and cash accounting methods, highlighting their distinct approaches to recording revenues and expenses, and provides real-world examples to illustrate their practical applications. The report includes the preparation of an unadjusted and adjusted trial balance, incorporating specific adjustments such as unbilled fees, depreciation, expired insurance, remaining cleaning supplies, and accrued salaries. Furthermore, the report analyzes a business operating in the student's local area to determine whether it utilizes accrual or cash-based accounting, providing insights into the practical application of these accounting methods. Finally, the report includes references to academic sources to support the analysis.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.