Accountancy Homework: Investment Appraisal & Financial Ratios Analysis

VerifiedAdded on 2023/06/10

|11

|2066

|184

Homework Assignment

AI Summary

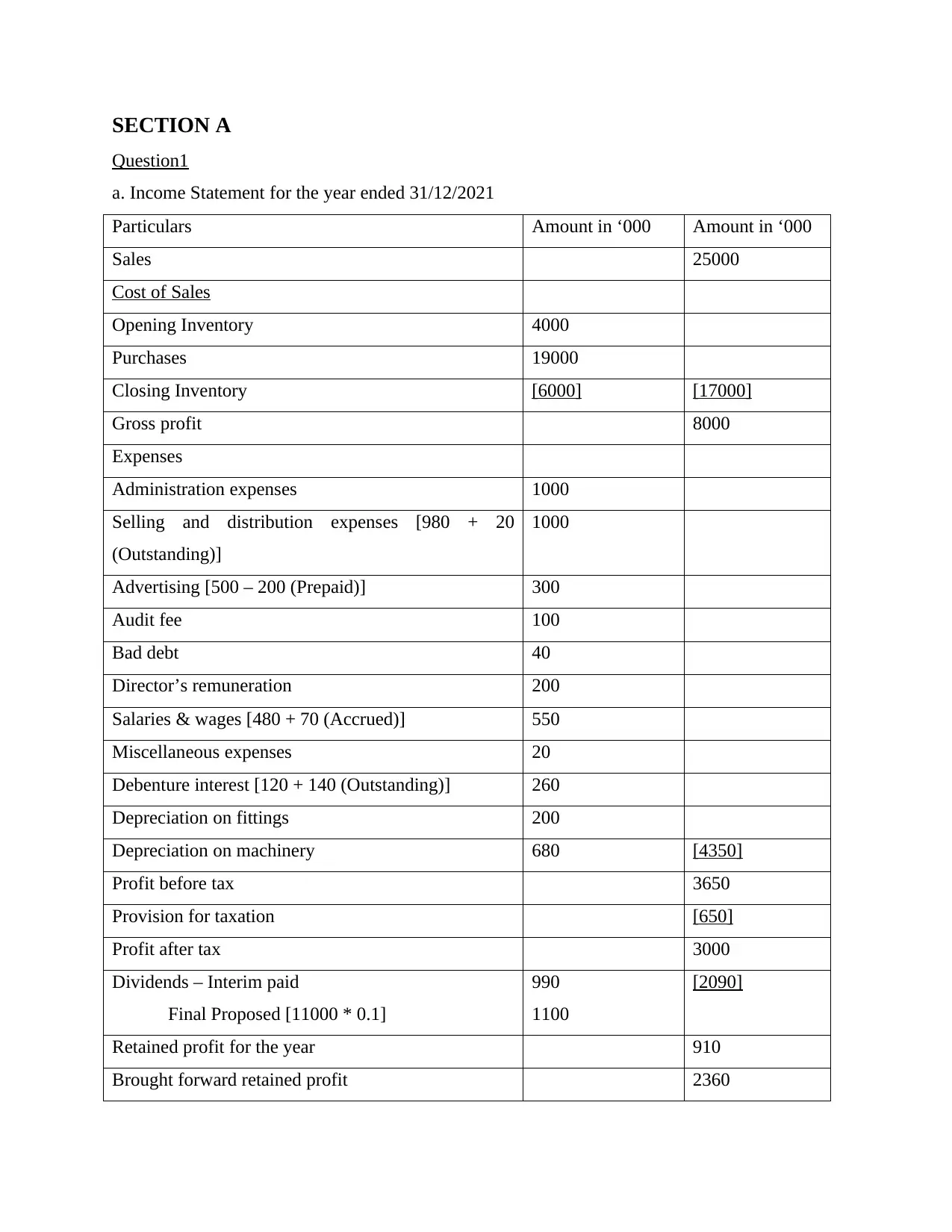

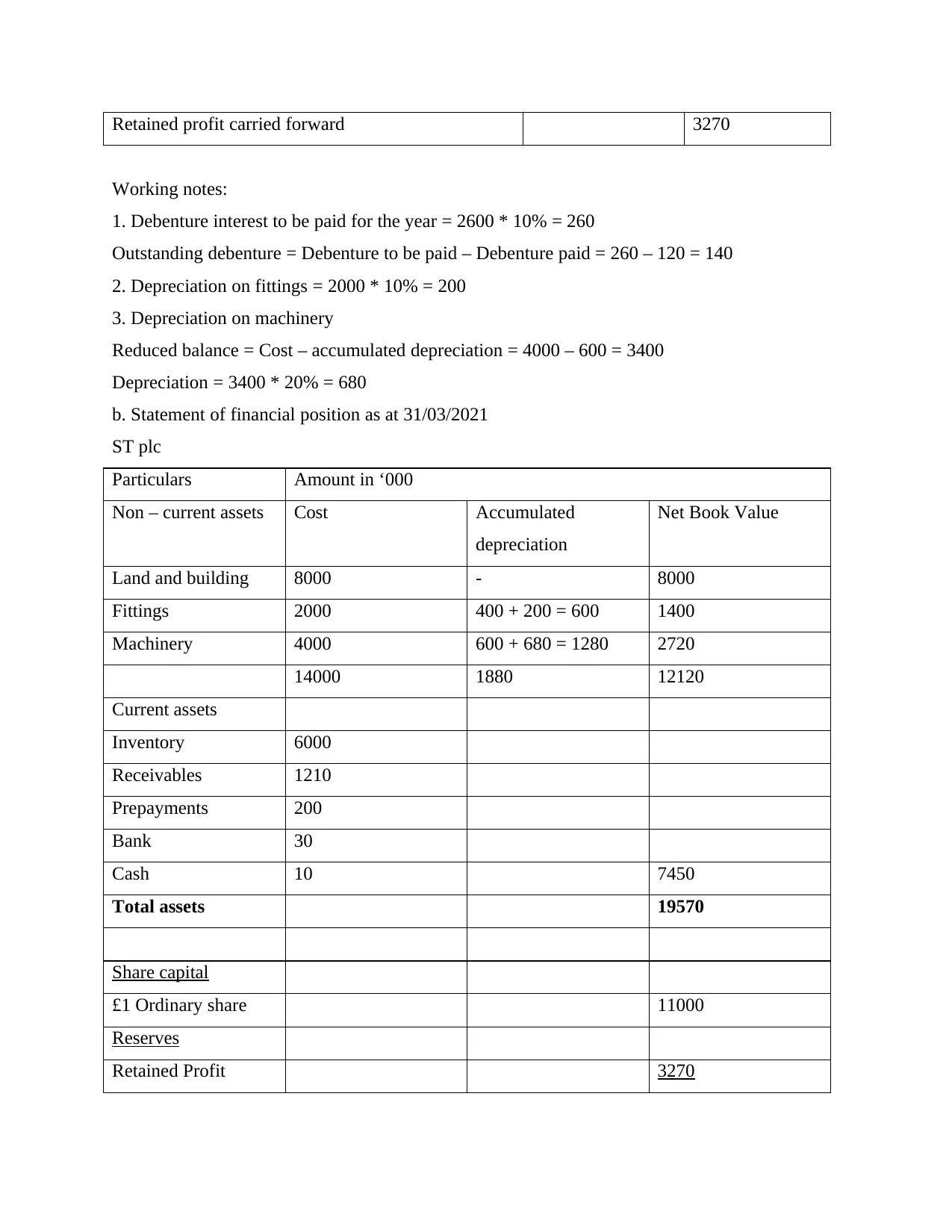

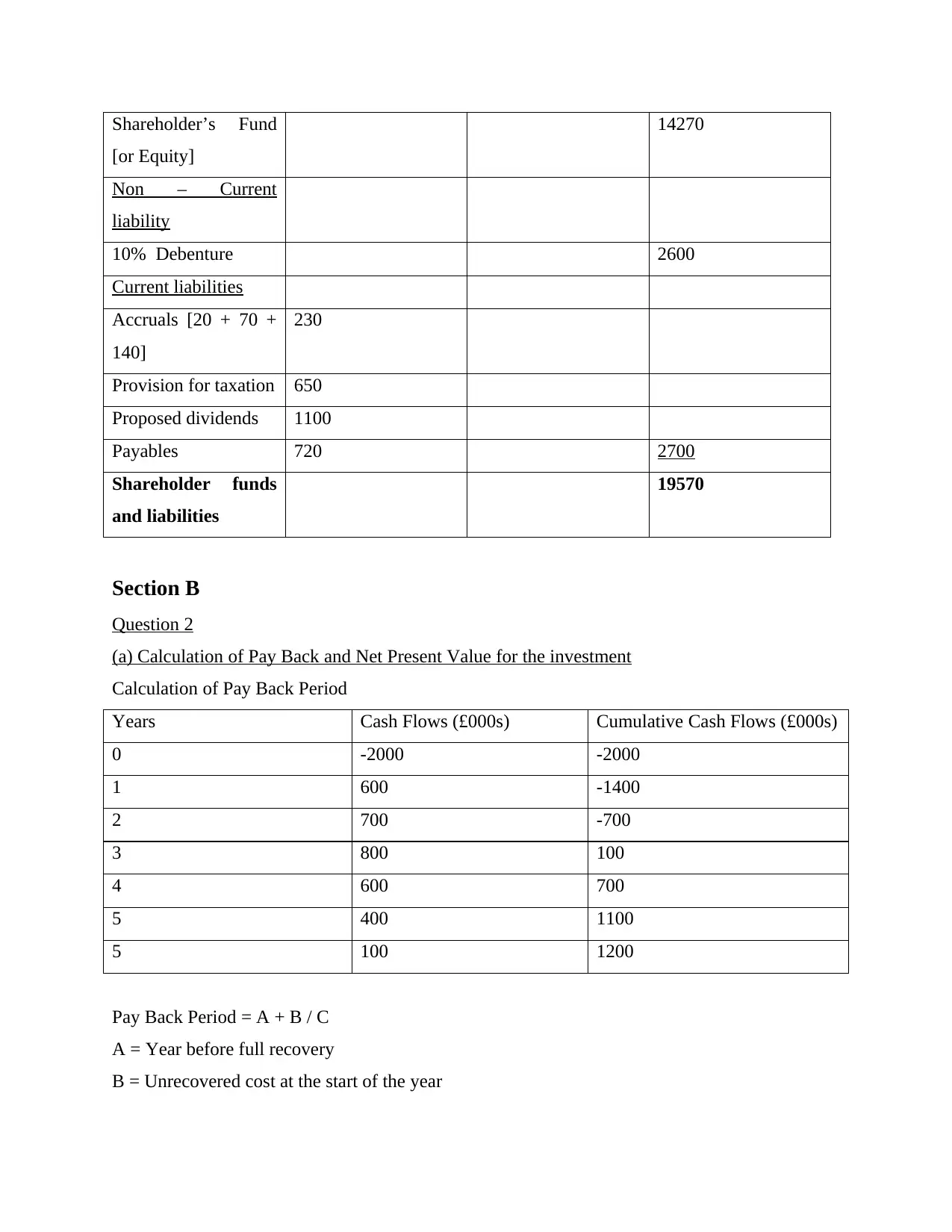

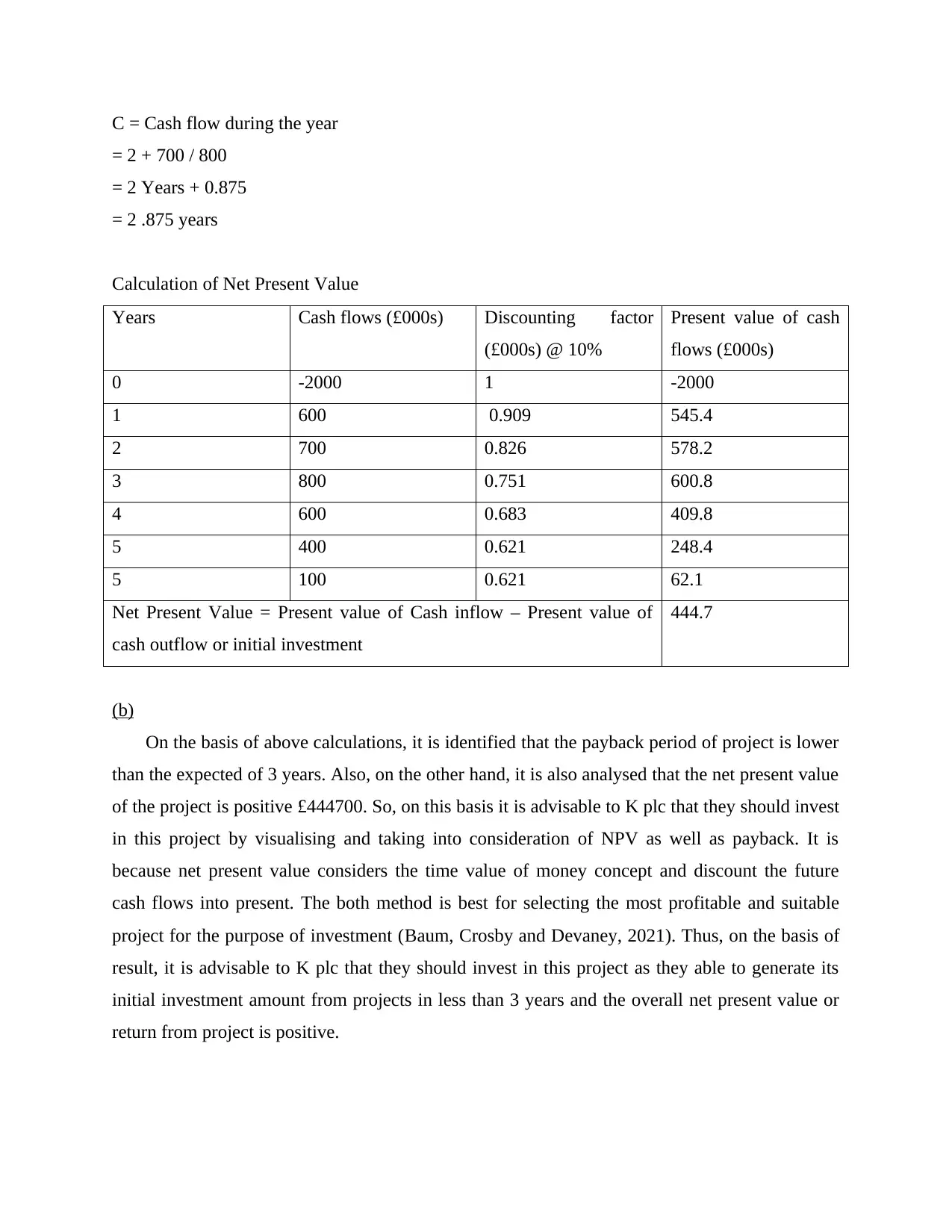

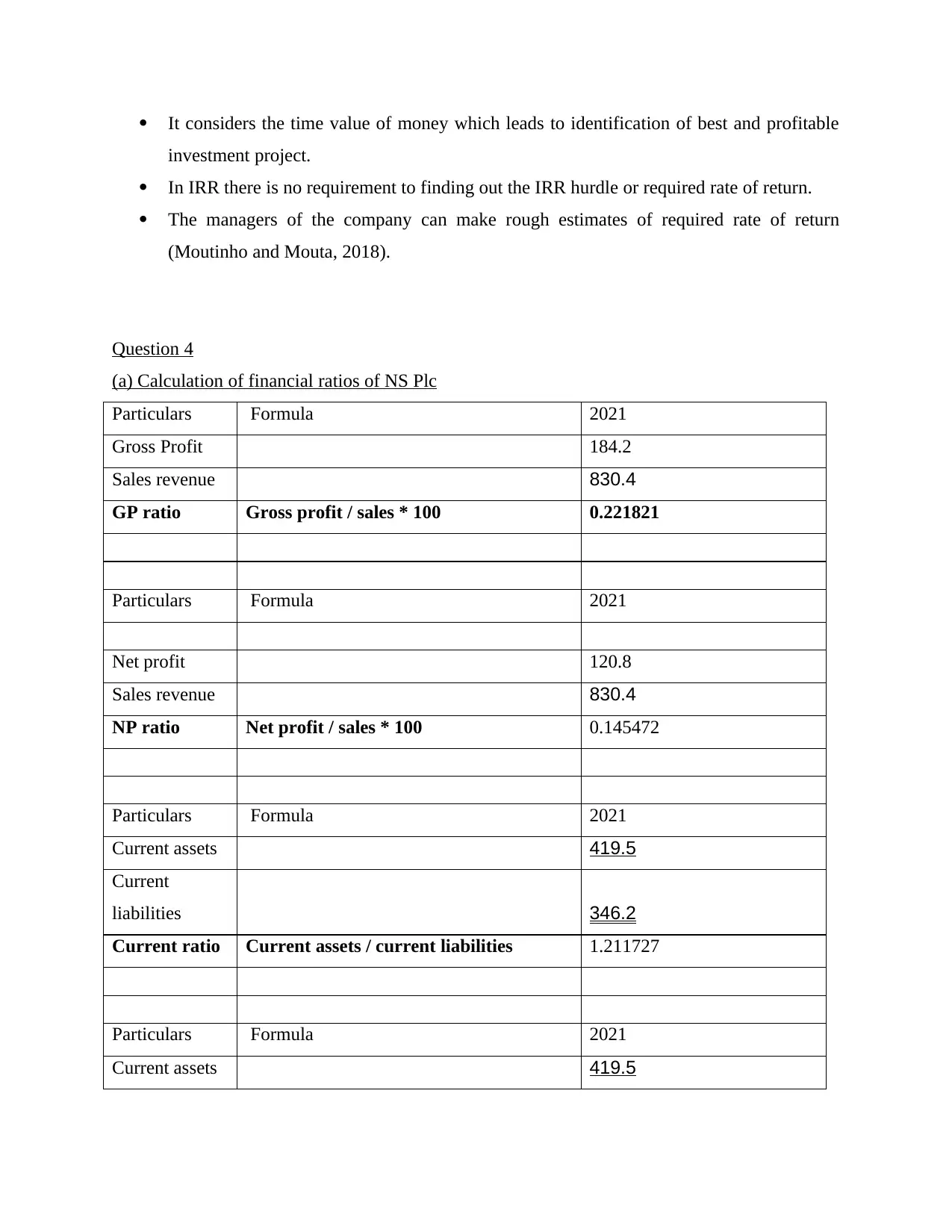

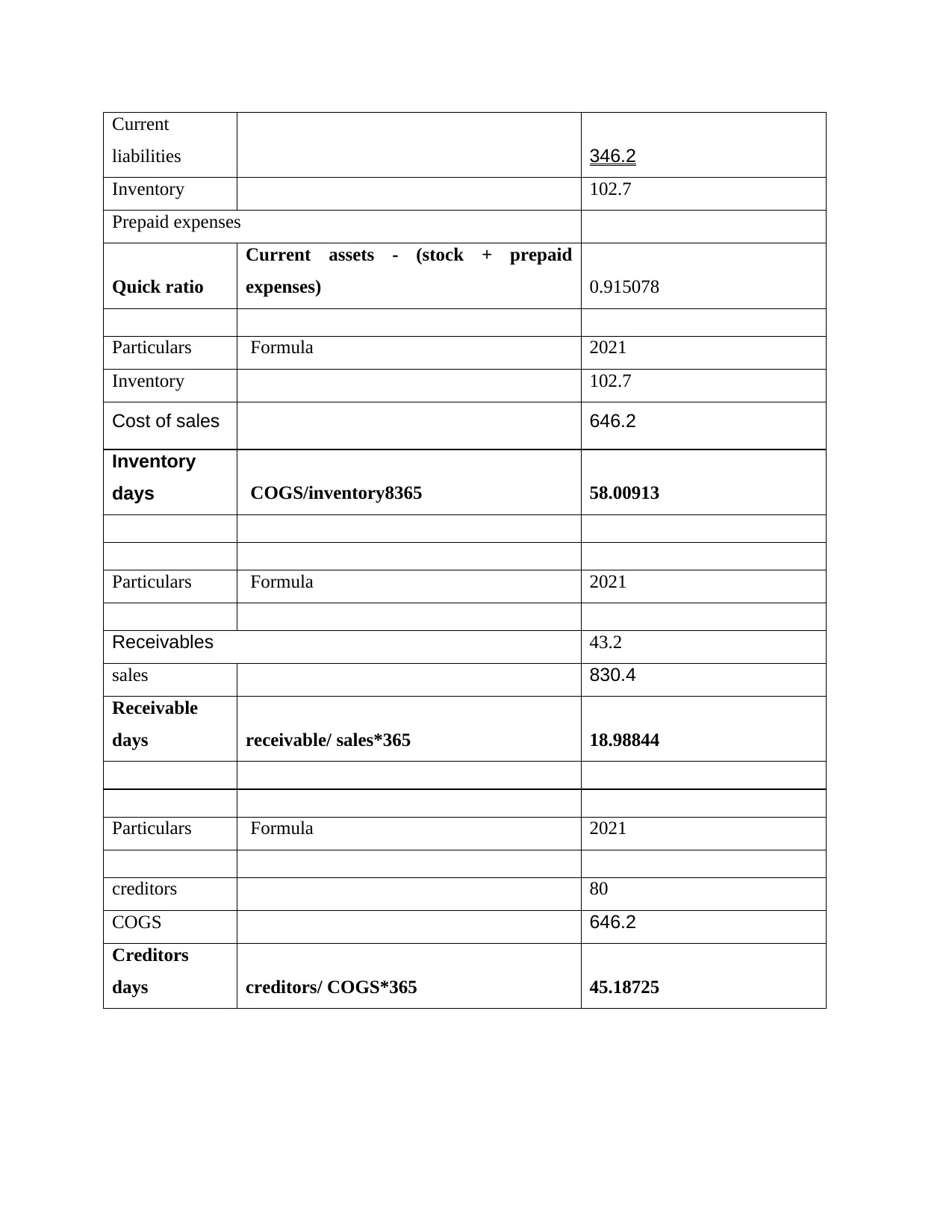

This accountancy homework assignment presents a comprehensive analysis of financial statements and investment decisions. Section A includes the preparation of an income statement and a statement of financial position. Section B focuses on investment appraisal techniques, specifically calculating payback period and net present value (NPV) to evaluate a project's feasibility. The assignment also explores non-financial factors influencing investment decisions and delves into the meaning and advantages of Internal Rate of Return (IRR). Furthermore, the homework includes the calculation and interpretation of various financial ratios, such as gross profit ratio, net profit ratio, current ratio, quick ratio, inventory days, receivable days, and creditor days, to assess the performance of NS Plc and compare it with MS Plc. The document incorporates working notes, calculations, and detailed comments to support the financial analysis and investment recommendations. References to relevant books and journals are also included.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.