Accounting Information Systems Report: Purchases, Payroll, Cash

VerifiedAdded on 2022/10/19

|16

|3353

|372

Report

AI Summary

This report provides a comprehensive analysis of the accounting information systems (AIS) employed by Adam & Company, focusing on the purchases system, cash disbursement system, and payroll system. The report begins with an overview of the importance of AIS in modern businesses and its role in ensuring accuracy, efficiency, and profitability. It then details the step-by-step processes of each system, including the recognition of needs, quotations, purchase orders, delivery, inspection, payment, and recording of purchases. The report identifies weaknesses and risks associated with each system, such as limited separation of duties, lack of specialization, and manual data entry, which can lead to errors, fraud, and financial losses. The analysis highlights the importance of internal control systems in mitigating these risks and suggests improvements such as specialization of duties and the adoption of electronic data entry systems to improve accuracy and efficiency. The report emphasizes the need for qualified personnel and the implementation of robust internal control measures to ensure the long-term success of Adam & Company.

ACCOUNTING 1

Accounting Information Systems

Student’s name

Course

Instructor’s name

Institutional affiliation

City and state

Date

Accounting Information Systems

Student’s name

Course

Instructor’s name

Institutional affiliation

City and state

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 2

Table of Contents

Abstract.......................................................................................................................................................2

Introduction.................................................................................................................................................3

The purchases system flowchart..................................................................................................................3

Figure 1: Purchase process......................................................................................................................4

Weaknesses and risks involved with the purchases flowchart.....................................................................5

Cash disbursement flowchart system...........................................................................................................6

Figure 2: Sample flowchart of cash disbursement system.......................................................................7

The Risks and Weaknesses Faced by the Company using System of Cash Disbursement...........................7

Flowchart about the Payroll System............................................................................................................9

Figure 3: The System of the Payroll..........................................................................................................10

Weaknesses of Adam & Company Limited Payroll system......................................................................10

Summary Conclusion................................................................................................................................11

References.................................................................................................................................................12

Table of Contents

Abstract.......................................................................................................................................................2

Introduction.................................................................................................................................................3

The purchases system flowchart..................................................................................................................3

Figure 1: Purchase process......................................................................................................................4

Weaknesses and risks involved with the purchases flowchart.....................................................................5

Cash disbursement flowchart system...........................................................................................................6

Figure 2: Sample flowchart of cash disbursement system.......................................................................7

The Risks and Weaknesses Faced by the Company using System of Cash Disbursement...........................7

Flowchart about the Payroll System............................................................................................................9

Figure 3: The System of the Payroll..........................................................................................................10

Weaknesses of Adam & Company Limited Payroll system......................................................................10

Summary Conclusion................................................................................................................................11

References.................................................................................................................................................12

ACCOUNTING 3

Abstract

This paper explores the assessment of Accounting information system about the

management of internal control system. In this study, Adam and Company limited is taken as the

case study. The paper explains the system of the flowchart especially the purchase system,

payroll system and the cash disbursement system of the company. The study further assessed the

risks and weaknesses faced by each system in the company and the way it can resolve them. It is

evident that, most organizations have challenges that entail internal control systems arising from

poor management. This therefore leads to the failure of the company. In summary, several points

are concluded about the way how Adam & Company is to succeed in the current century in

which the applications about accounting information systems can be employed on a global basis.

This can be done to resolve different issues that may influence the business entity.

Abstract

This paper explores the assessment of Accounting information system about the

management of internal control system. In this study, Adam and Company limited is taken as the

case study. The paper explains the system of the flowchart especially the purchase system,

payroll system and the cash disbursement system of the company. The study further assessed the

risks and weaknesses faced by each system in the company and the way it can resolve them. It is

evident that, most organizations have challenges that entail internal control systems arising from

poor management. This therefore leads to the failure of the company. In summary, several points

are concluded about the way how Adam & Company is to succeed in the current century in

which the applications about accounting information systems can be employed on a global basis.

This can be done to resolve different issues that may influence the business entity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING 4

Introduction

Recently in the globe, the demand rate is very efficient and effective each and every day

and this calls upon for better preparing, recording and analyzing the data concerning finance

(Darrough, et al, 2012). Because of this, Adam and company has come up with different steps

and measures all over the departments of the organization with an intention of meeting the needs

of its customers. Several organizations employ different control measures basing on the goals,

mission and targets for the company. Accounting Information systems thus play an important

role in this field by ensuring accuracy, efficiency and profitability within the organization

(Agbenyo et al, 2018). In this paper, an accounting information system is defined as a structure

or tool that is employed by any company, institute or organization applied to control the internal

performance so that every activity concerning finance is appropriately and accurately done to

minimize losses and errors (Nashwan, 2018). An internal control system has got a set of

principles and laws that an organization should follow to make sure there exists efficiency and

good performance of the business. These principles are used as guidelines to the operation of the

business so that the company can easily reach its set goals (Darrough, et al, 2012). The internal

control system is built up of five components and these are risk assessment, communication and

information systems, environmental controls and finally monitoring and control systems. The

accounting information system is also divided into three components and these include; the

purchases system, the system of payroll and the system of disbursement as they are discussed

below;

Introduction

Recently in the globe, the demand rate is very efficient and effective each and every day

and this calls upon for better preparing, recording and analyzing the data concerning finance

(Darrough, et al, 2012). Because of this, Adam and company has come up with different steps

and measures all over the departments of the organization with an intention of meeting the needs

of its customers. Several organizations employ different control measures basing on the goals,

mission and targets for the company. Accounting Information systems thus play an important

role in this field by ensuring accuracy, efficiency and profitability within the organization

(Agbenyo et al, 2018). In this paper, an accounting information system is defined as a structure

or tool that is employed by any company, institute or organization applied to control the internal

performance so that every activity concerning finance is appropriately and accurately done to

minimize losses and errors (Nashwan, 2018). An internal control system has got a set of

principles and laws that an organization should follow to make sure there exists efficiency and

good performance of the business. These principles are used as guidelines to the operation of the

business so that the company can easily reach its set goals (Darrough, et al, 2012). The internal

control system is built up of five components and these are risk assessment, communication and

information systems, environmental controls and finally monitoring and control systems. The

accounting information system is also divided into three components and these include; the

purchases system, the system of payroll and the system of disbursement as they are discussed

below;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 5

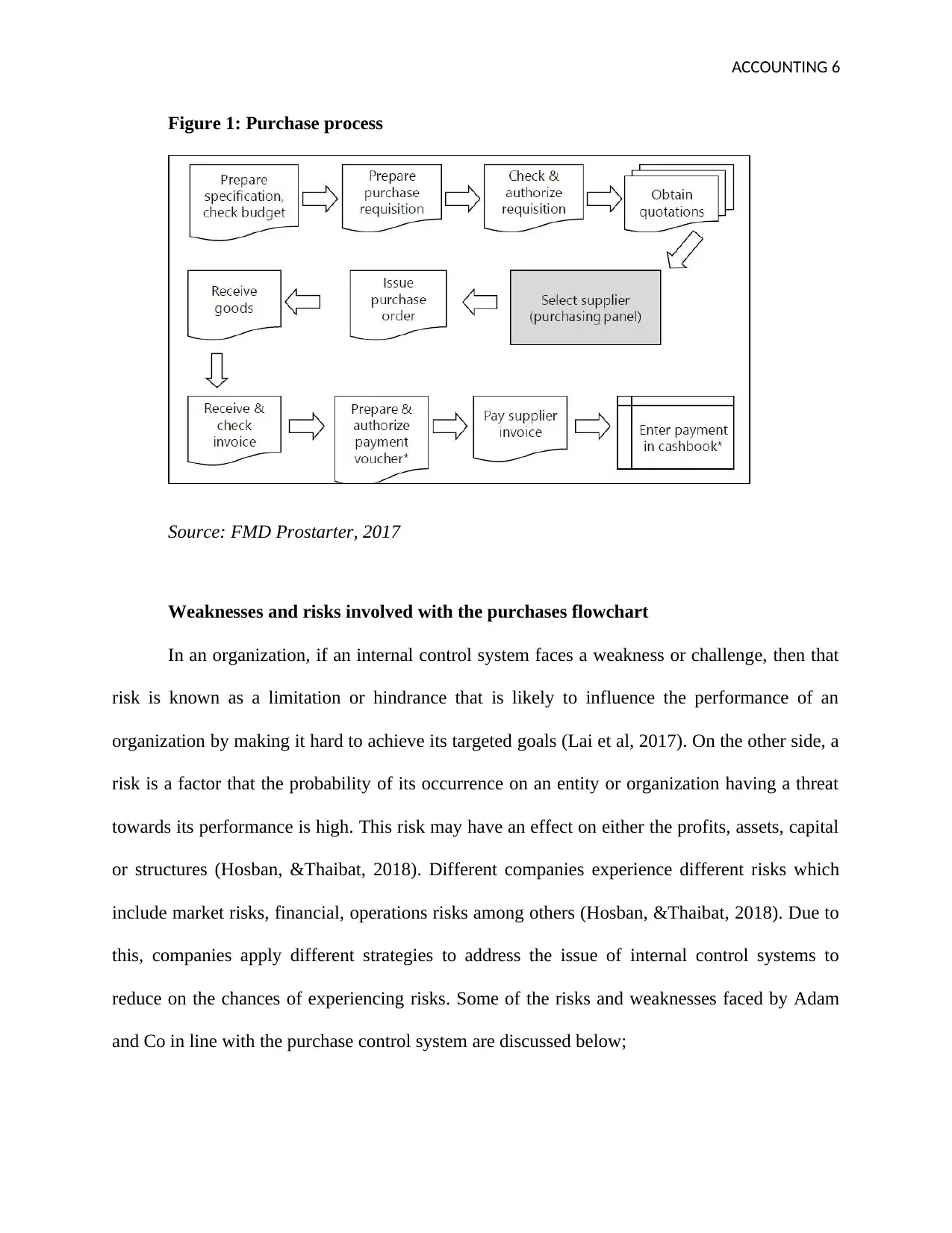

The purchases system flowchart

The purchases system flowchart refers to a combination of steps that any company

follows in the process of making purchases and procuring materials, inventories, stock and the

assets too that the business needs to continue operating. Furthermore, the purchases flowchart

system is a set of sequential events that are run by different people at different stages

(Monisola&Rekiat, 2016). The purchases system is composed of about nine steps or stages. The

very first stage of the system is composed of ‘the needs recognition’ well as the last stage is all

about ‘satisfaction of needs’. At a moment where the whole organization or part of the

organization requires to extend some financial information, then there is need to develop a

document known as the ‘recognition note’ that should be authorized by managers of the

organization (Agbenyo et al, 2018). Later, quotations are got and through the quotation, a

potential supplier is selected by issuing him a purchase order. After all this, delivery is made and

at this period, the goods are inspected thoroughly to ensure efficiency and high quality. In case

the goods are found out to be at the required and all stages completed, payment is approved and

made to the supplier. The last step of the process is now recording all the purchases made in the

‘book of accounts’ (Nashwan, 2018).

The figure below shows the purchase flow chart system that includes all the steps

followed throughout the process.

The purchases system flowchart

The purchases system flowchart refers to a combination of steps that any company

follows in the process of making purchases and procuring materials, inventories, stock and the

assets too that the business needs to continue operating. Furthermore, the purchases flowchart

system is a set of sequential events that are run by different people at different stages

(Monisola&Rekiat, 2016). The purchases system is composed of about nine steps or stages. The

very first stage of the system is composed of ‘the needs recognition’ well as the last stage is all

about ‘satisfaction of needs’. At a moment where the whole organization or part of the

organization requires to extend some financial information, then there is need to develop a

document known as the ‘recognition note’ that should be authorized by managers of the

organization (Agbenyo et al, 2018). Later, quotations are got and through the quotation, a

potential supplier is selected by issuing him a purchase order. After all this, delivery is made and

at this period, the goods are inspected thoroughly to ensure efficiency and high quality. In case

the goods are found out to be at the required and all stages completed, payment is approved and

made to the supplier. The last step of the process is now recording all the purchases made in the

‘book of accounts’ (Nashwan, 2018).

The figure below shows the purchase flow chart system that includes all the steps

followed throughout the process.

ACCOUNTING 6

Figure 1: Purchase process

Source: FMD Prostarter, 2017

Weaknesses and risks involved with the purchases flowchart

In an organization, if an internal control system faces a weakness or challenge, then that

risk is known as a limitation or hindrance that is likely to influence the performance of an

organization by making it hard to achieve its targeted goals (Lai et al, 2017). On the other side, a

risk is a factor that the probability of its occurrence on an entity or organization having a threat

towards its performance is high. This risk may have an effect on either the profits, assets, capital

or structures (Hosban, &Thaibat, 2018). Different companies experience different risks which

include market risks, financial, operations risks among others (Hosban, &Thaibat, 2018). Due to

this, companies apply different strategies to address the issue of internal control systems to

reduce on the chances of experiencing risks. Some of the risks and weaknesses faced by Adam

and Co in line with the purchase control system are discussed below;

Figure 1: Purchase process

Source: FMD Prostarter, 2017

Weaknesses and risks involved with the purchases flowchart

In an organization, if an internal control system faces a weakness or challenge, then that

risk is known as a limitation or hindrance that is likely to influence the performance of an

organization by making it hard to achieve its targeted goals (Lai et al, 2017). On the other side, a

risk is a factor that the probability of its occurrence on an entity or organization having a threat

towards its performance is high. This risk may have an effect on either the profits, assets, capital

or structures (Hosban, &Thaibat, 2018). Different companies experience different risks which

include market risks, financial, operations risks among others (Hosban, &Thaibat, 2018). Due to

this, companies apply different strategies to address the issue of internal control systems to

reduce on the chances of experiencing risks. Some of the risks and weaknesses faced by Adam

and Co in line with the purchase control system are discussed below;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING 7

According to the performance of the organization, the weakness of limited separation of

duties is observed. Many duties under the department of purchases are allocated to the purchases

clerk. This makes the clerk very tiresome and overworked. At the end of it, mistakes may appear.

Also, the clerk may purchase unwanted goods that make the calculations in the purchases

accounts imperfect and wrong. This affects the purchasing system and it leads to losses of the

company. Basing on the internal control systems within an environment, effectiveness and

efficiency in the activities on the organization are observed when there is specialization in the

company (Mahadeen, et al, 2017). This means that should have several workers who perform

tasks they are perfect within their area of specialization. However, Adam and Co do not follow

this statement since the purchases clerk performs a set of activities even where he lacks

experience. He is responsible for determining the number the amount of stock to be purchased

(Akwa-Sekyi& Gene, 2016). Nevertheless, all the duties that a clerk performs in this company

are meant to be entitled to professional personnel say the procurement officer who is meant to

purchase and procure whatever is required by the company (Prasetyaningsih et al, 2014). Only

this weakness exposes the company to threats and risks of making loses due to poor production,

purchase of unnecessary assets, spending more on buying few commodities and many more risks

related to purchasing systems (Mahadeen, et al, 2017).

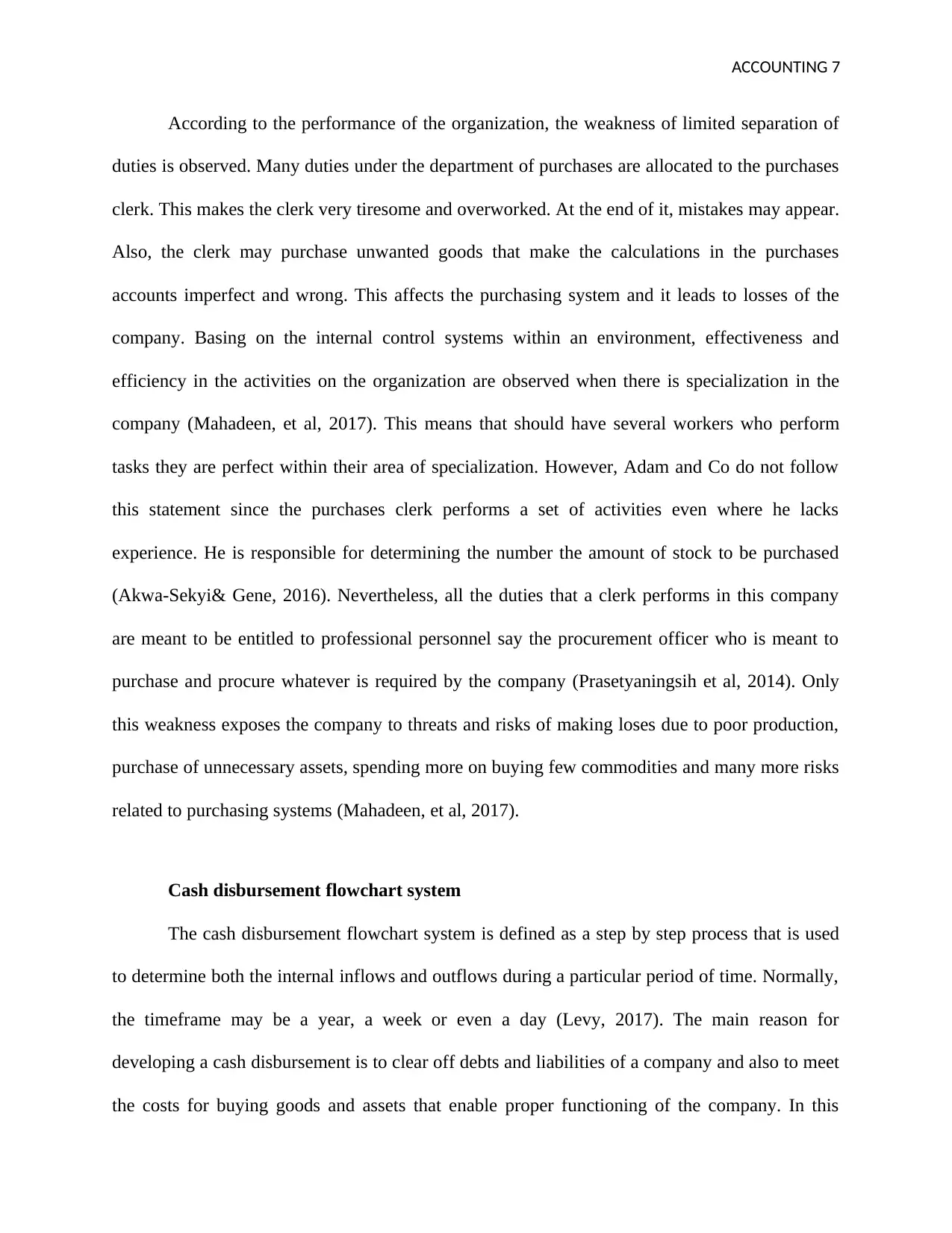

Cash disbursement flowchart system

The cash disbursement flowchart system is defined as a step by step process that is used

to determine both the internal inflows and outflows during a particular period of time. Normally,

the timeframe may be a year, a week or even a day (Levy, 2017). The main reason for

developing a cash disbursement is to clear off debts and liabilities of a company and also to meet

the costs for buying goods and assets that enable proper functioning of the company. In this

According to the performance of the organization, the weakness of limited separation of

duties is observed. Many duties under the department of purchases are allocated to the purchases

clerk. This makes the clerk very tiresome and overworked. At the end of it, mistakes may appear.

Also, the clerk may purchase unwanted goods that make the calculations in the purchases

accounts imperfect and wrong. This affects the purchasing system and it leads to losses of the

company. Basing on the internal control systems within an environment, effectiveness and

efficiency in the activities on the organization are observed when there is specialization in the

company (Mahadeen, et al, 2017). This means that should have several workers who perform

tasks they are perfect within their area of specialization. However, Adam and Co do not follow

this statement since the purchases clerk performs a set of activities even where he lacks

experience. He is responsible for determining the number the amount of stock to be purchased

(Akwa-Sekyi& Gene, 2016). Nevertheless, all the duties that a clerk performs in this company

are meant to be entitled to professional personnel say the procurement officer who is meant to

purchase and procure whatever is required by the company (Prasetyaningsih et al, 2014). Only

this weakness exposes the company to threats and risks of making loses due to poor production,

purchase of unnecessary assets, spending more on buying few commodities and many more risks

related to purchasing systems (Mahadeen, et al, 2017).

Cash disbursement flowchart system

The cash disbursement flowchart system is defined as a step by step process that is used

to determine both the internal inflows and outflows during a particular period of time. Normally,

the timeframe may be a year, a week or even a day (Levy, 2017). The main reason for

developing a cash disbursement is to clear off debts and liabilities of a company and also to meet

the costs for buying goods and assets that enable proper functioning of the company. In this

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 8

system, the payments are made by use of cheques in the bank or directly in cash

(Monisola&Rekiat, 2016).

The figure below represents the flowchart of cash disbursement system

Figure 2: Sample flowchart of cash disbursement system

Source: vishekbatra, 2019

The Risks and Weaknesses Faced by the Company using System of Cash

Disbursement

There are several risks and weaknesses faced by the company using cash disbursement

system. It is evident that organizations that have got revenue and cash maned by the individuals,

they are attributed to facing chances obtaining financial losses. With such a situation, there

should be the class of people who are to be entrusted with the organization’s finances (Bowers,

2017). In most case, practices that are unethical for example theft, funds misplacement, and

fraudulent are serious and common among amidst finance officers. This therefore leads to less

system, the payments are made by use of cheques in the bank or directly in cash

(Monisola&Rekiat, 2016).

The figure below represents the flowchart of cash disbursement system

Figure 2: Sample flowchart of cash disbursement system

Source: vishekbatra, 2019

The Risks and Weaknesses Faced by the Company using System of Cash

Disbursement

There are several risks and weaknesses faced by the company using cash disbursement

system. It is evident that organizations that have got revenue and cash maned by the individuals,

they are attributed to facing chances obtaining financial losses. With such a situation, there

should be the class of people who are to be entrusted with the organization’s finances (Bowers,

2017). In most case, practices that are unethical for example theft, funds misplacement, and

fraudulent are serious and common among amidst finance officers. This therefore leads to less

ACCOUNTING 9

trust of the company’s finances that is to say Adam & Company is not encourage to build

confidence in the single individual. This is because such incident may become the greatest risk to

the company (Levy, 2017). Furthermore, the internal control system at Adam & Company is not

good enough since the treasurers and clerks are mostly entitled the accounts of the company

which includes the ‘cash and purchase disbursement system’ (Salin, et al, 2018). In addition,

such situation is not supposed to e done in that way since other employees are likely to become

disgraced with the pressures arising from other employees (Akwa-Sekyi& Gene, 2016). Most

significant is that, the company’s income should be easily accessed by any member of the

company since there exists many chances of losing money through theft or embezzlement. The

system of the company does not give any provision of specific time to reconcile about several

accounts (International Accounting, Auditing and Ethics, 2015). Therefore, cash statements that

are manually designed continue putting the company’s control system into negative direction.

It is evident that, the cash disbursement system at Adam and Company is basically

manually done. Most important with this system is that, there are some benefits as well as

various risks or uncertainties that are embedded with cash disbursement system (Salin, et al,

2018). In this case, several financial statements and receipts are processed manually and stored

within the premises of the company. This therefore exposes the organization to the risks of

juxtaposing the information through ‘fore outbreaks’, manipulation of information and several

threats that are similar to the mentioned (Mitrefinch, 2019). In case when such information is

lost, threats of going into financial crisis are likely to be very high and thuis there causes some

staunch customers to lose confidence in the company (Crouthamel, 2013). Therefore, losing its

reputation in public especially the customers it serves

trust of the company’s finances that is to say Adam & Company is not encourage to build

confidence in the single individual. This is because such incident may become the greatest risk to

the company (Levy, 2017). Furthermore, the internal control system at Adam & Company is not

good enough since the treasurers and clerks are mostly entitled the accounts of the company

which includes the ‘cash and purchase disbursement system’ (Salin, et al, 2018). In addition,

such situation is not supposed to e done in that way since other employees are likely to become

disgraced with the pressures arising from other employees (Akwa-Sekyi& Gene, 2016). Most

significant is that, the company’s income should be easily accessed by any member of the

company since there exists many chances of losing money through theft or embezzlement. The

system of the company does not give any provision of specific time to reconcile about several

accounts (International Accounting, Auditing and Ethics, 2015). Therefore, cash statements that

are manually designed continue putting the company’s control system into negative direction.

It is evident that, the cash disbursement system at Adam and Company is basically

manually done. Most important with this system is that, there are some benefits as well as

various risks or uncertainties that are embedded with cash disbursement system (Salin, et al,

2018). In this case, several financial statements and receipts are processed manually and stored

within the premises of the company. This therefore exposes the organization to the risks of

juxtaposing the information through ‘fore outbreaks’, manipulation of information and several

threats that are similar to the mentioned (Mitrefinch, 2019). In case when such information is

lost, threats of going into financial crisis are likely to be very high and thuis there causes some

staunch customers to lose confidence in the company (Crouthamel, 2013). Therefore, losing its

reputation in public especially the customers it serves

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING 10

Furthermore, the risks that arise from obvious errors especially in times of entering

financial data are also confined at Adam & Company. This is because the company uses manual

methods of records, and this therefore leads to high chances of obtaining errors inform of

recording unnecessary figures due to the failure of catching up with the ethics of ‘double entry’

which are high (Bowers, 2017). In the daily life, it is evident that there is no one who is perfect

which means that errors and mistakes are commonly done. However, when using electronic

means of entering data, such mistakes or errors can be identified and corrected by using the term

that is commonly used and this term is “Garbage in Garbage Out” (International Accounting,

Auditing and Ethics, 2015).

Also, the Adam & Co lacks employs who are professionally fit to be working in

Auditing, finance and accounting firms instead it employs the clerks to be responsible for all

transactions and statements in the company. This situation indicates big challenge in the system

of internal control (Crouthamel, 2013). It is clear that, the experienced personnel should be

recruited in order to resolve such risks that the company face through restructuring all on-going

activities in the company. It is evident that, Adam & Co does not have a qualified personnel who

is to help in raising the activities such as analyzing, evaluation, interpretation and presentation of

the information for further policy making as well as the person who is to authorize all

transactions of the company (Mitrefinch, 2019). This therefore aids to the weakness of the

organization where it makes wrong transactions, the charges that are not correct especially of

purchases and wrong calculations drastically affect the survival of the company in operation in

long run.

Furthermore, the risks that arise from obvious errors especially in times of entering

financial data are also confined at Adam & Company. This is because the company uses manual

methods of records, and this therefore leads to high chances of obtaining errors inform of

recording unnecessary figures due to the failure of catching up with the ethics of ‘double entry’

which are high (Bowers, 2017). In the daily life, it is evident that there is no one who is perfect

which means that errors and mistakes are commonly done. However, when using electronic

means of entering data, such mistakes or errors can be identified and corrected by using the term

that is commonly used and this term is “Garbage in Garbage Out” (International Accounting,

Auditing and Ethics, 2015).

Also, the Adam & Co lacks employs who are professionally fit to be working in

Auditing, finance and accounting firms instead it employs the clerks to be responsible for all

transactions and statements in the company. This situation indicates big challenge in the system

of internal control (Crouthamel, 2013). It is clear that, the experienced personnel should be

recruited in order to resolve such risks that the company face through restructuring all on-going

activities in the company. It is evident that, Adam & Co does not have a qualified personnel who

is to help in raising the activities such as analyzing, evaluation, interpretation and presentation of

the information for further policy making as well as the person who is to authorize all

transactions of the company (Mitrefinch, 2019). This therefore aids to the weakness of the

organization where it makes wrong transactions, the charges that are not correct especially of

purchases and wrong calculations drastically affect the survival of the company in operation in

long run.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 11

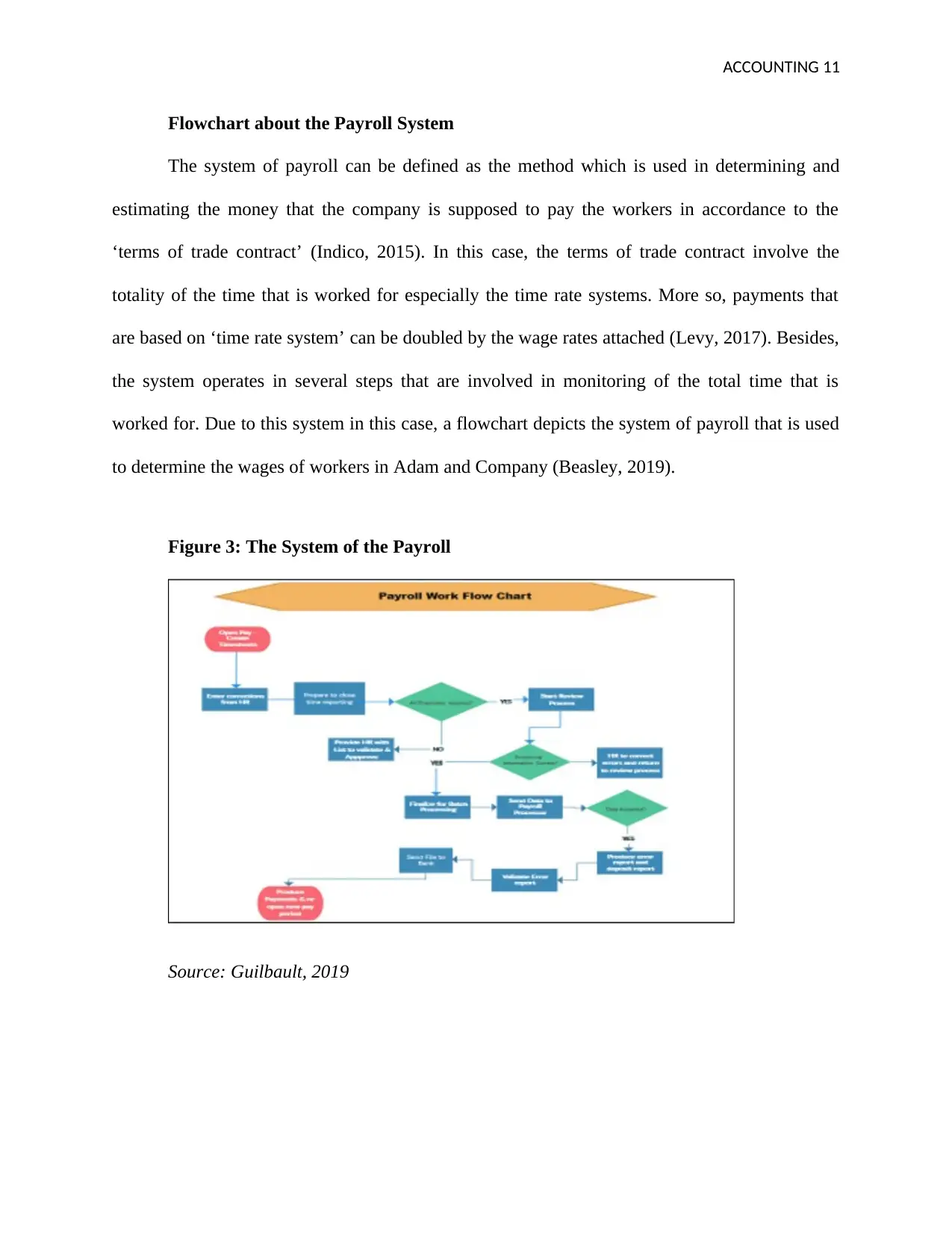

Flowchart about the Payroll System

The system of payroll can be defined as the method which is used in determining and

estimating the money that the company is supposed to pay the workers in accordance to the

‘terms of trade contract’ (Indico, 2015). In this case, the terms of trade contract involve the

totality of the time that is worked for especially the time rate systems. More so, payments that

are based on ‘time rate system’ can be doubled by the wage rates attached (Levy, 2017). Besides,

the system operates in several steps that are involved in monitoring of the total time that is

worked for. Due to this system in this case, a flowchart depicts the system of payroll that is used

to determine the wages of workers in Adam and Company (Beasley, 2019).

Figure 3: The System of the Payroll

Source: Guilbault, 2019

Flowchart about the Payroll System

The system of payroll can be defined as the method which is used in determining and

estimating the money that the company is supposed to pay the workers in accordance to the

‘terms of trade contract’ (Indico, 2015). In this case, the terms of trade contract involve the

totality of the time that is worked for especially the time rate systems. More so, payments that

are based on ‘time rate system’ can be doubled by the wage rates attached (Levy, 2017). Besides,

the system operates in several steps that are involved in monitoring of the total time that is

worked for. Due to this system in this case, a flowchart depicts the system of payroll that is used

to determine the wages of workers in Adam and Company (Beasley, 2019).

Figure 3: The System of the Payroll

Source: Guilbault, 2019

ACCOUNTING 12

Weaknesses of Adam & Company Limited Payroll system

It is clear that the procedures that are tradition in analyzing and evaluating the total time

worked by the employees can be the influence factor of increasing rate of inefficiency about the

past periods. This is due to the limitations that involve tradition systems more so the time cards

that have brought about the equipments that are sophisticated to get proper records (Nashwan,

2018). Furthermore, the payroll system at Adam & Company Limited is entailed with some risks

that are more significant. Moreover, time cards are traditionally operated with manual standards

which are attributed to manipulations (Beasley, 2019). In addition, there is emergence of huge

and basic potential of exposing several qualified personnel who can easily make financial reports

regularly in time (Indico, 2015).

Summary Conclusion

In summary, the system that is effective and efficient about the internal control is a basic

tool that various active companies should acquire. Most important is that, the level of profits

attained by the companies is taken as dependent factor on their effectiveness resulting from

utilization of resources. In the daily business situation, the trends of the market that have been

originated through the advancement of technology and ‘internal control system’ that are effective

and reliable in providing immediate changes of the state. In conclusion, Adam & Company

limited is advised to adopt the system of internal controls which may bring about positive trend

of the company. In addition to the internal control systems in the company, the manual methods

of ‘purchase charts’, ‘time cards’ that are applied in time recording should be acted upon in the

organization.

Weaknesses of Adam & Company Limited Payroll system

It is clear that the procedures that are tradition in analyzing and evaluating the total time

worked by the employees can be the influence factor of increasing rate of inefficiency about the

past periods. This is due to the limitations that involve tradition systems more so the time cards

that have brought about the equipments that are sophisticated to get proper records (Nashwan,

2018). Furthermore, the payroll system at Adam & Company Limited is entailed with some risks

that are more significant. Moreover, time cards are traditionally operated with manual standards

which are attributed to manipulations (Beasley, 2019). In addition, there is emergence of huge

and basic potential of exposing several qualified personnel who can easily make financial reports

regularly in time (Indico, 2015).

Summary Conclusion

In summary, the system that is effective and efficient about the internal control is a basic

tool that various active companies should acquire. Most important is that, the level of profits

attained by the companies is taken as dependent factor on their effectiveness resulting from

utilization of resources. In the daily business situation, the trends of the market that have been

originated through the advancement of technology and ‘internal control system’ that are effective

and reliable in providing immediate changes of the state. In conclusion, Adam & Company

limited is advised to adopt the system of internal controls which may bring about positive trend

of the company. In addition to the internal control systems in the company, the manual methods

of ‘purchase charts’, ‘time cards’ that are applied in time recording should be acted upon in the

organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.