Accounting. 1. Accounting. Student Number. Class & Cour

VerifiedAdded on 2022/10/19

|17

|4072

|2

AI Summary

My australian company is Pro Medicus Ltd (PME) and my South African Company is Mediclinic International PLC

I need this assignment in one week so that i can show my tutor as my draft, and can change if needed.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Accounting 1

Accounting

Student Number

Class & Course Code

Trimester Number

Professor

University

The City & State

Date

Accounting

Student Number

Class & Course Code

Trimester Number

Professor

University

The City & State

Date

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting 2

Executive Summary

The conceptual framework provides the company with the basis of developing accounting

standards. Before the adoption of the conceptual framework, there was no sufficient definition of

key financial elements in the balance sheet, income statement, and cash flow statements. Each of

the statements has its financial elements which are clearly defined and recognised in the

conceptual framework. The framework also outlines the qualitative characteristics of financial

reports. The reports should be relevant as well as the show as portrays the report as a faithful

representation of the company. According to 2018 annual report published by the Pro Medicus

Ltd, the company adhered to the requirement of the conceptual framework, and the Australian

corporation Act 2001. Companies are slowly turning their attention to CSR initiatives as a means

of creating value. The IIRC and the GRI have pushed for the adoption of integrated financial

reporting and sustainable financial reporting, respectively. Pro Medicus Ltd is yet to adopt either

sustainable reporting or integrate reporting within the current accounting practice globally. On

the other hand, Mediclinic International PLC engages with its stakeholders to organizational

value. Considering that CSR has become an essential part of business operations, it’s time to

adopt either sustainable reporting or integrated reporting.

Executive Summary

The conceptual framework provides the company with the basis of developing accounting

standards. Before the adoption of the conceptual framework, there was no sufficient definition of

key financial elements in the balance sheet, income statement, and cash flow statements. Each of

the statements has its financial elements which are clearly defined and recognised in the

conceptual framework. The framework also outlines the qualitative characteristics of financial

reports. The reports should be relevant as well as the show as portrays the report as a faithful

representation of the company. According to 2018 annual report published by the Pro Medicus

Ltd, the company adhered to the requirement of the conceptual framework, and the Australian

corporation Act 2001. Companies are slowly turning their attention to CSR initiatives as a means

of creating value. The IIRC and the GRI have pushed for the adoption of integrated financial

reporting and sustainable financial reporting, respectively. Pro Medicus Ltd is yet to adopt either

sustainable reporting or integrate reporting within the current accounting practice globally. On

the other hand, Mediclinic International PLC engages with its stakeholders to organizational

value. Considering that CSR has become an essential part of business operations, it’s time to

adopt either sustainable reporting or integrated reporting.

Accounting 3

Introduction

The conceptual framework provides the company with the basis of developing accounting

standards. A conceptual framework for financial reporting helps the companies to recognise and

measure their assets, liabilities, equity, incomes, and expenses. The essence of using the

conceptual framework is to ensure that financial reports are relevant and portrays a faithful

representation of a company’s financial position. Likewise, organisations such as The

International Integrated Reporting Council (IIRC) and the Global Reporting Initiative (GRI) of

integrated financial reporting and sustainable financial reporting, respectively. Companies are

slowly turning their attention to CSR initiatives as a means of creating value.

This paper examines the application of the conceptual framework, sustainable reporting, and

integrated reporting in current accounting practices. The paper is divided into two parts — part A

analysis of the application of the conceptual framework for financial reporting. Likewise, part B

evaluates the need to adopt either sustainable reporting or integrated reporting.

PART A: Conceptual framework

a) History and development of the Conceptual Framework for Financial Reporting

The International Accounting Standards Board (IASB) released its first conceptual framework in

1989. However, this version was criticised for lacking clarity and objectivity. The International

Financial Reporting Standards (IFRS) was tasked with the responsibility of providing an

improved version of the conceptual framework for financial reporting.

The process of collecting recommendations and views to develop conceptual framework began in

the 1940s in the UK. The process of reviewing the collected information began in 1991, which

show the release of the conceptual framework in 2010. In Australia, AASB developed the SACs

Introduction

The conceptual framework provides the company with the basis of developing accounting

standards. A conceptual framework for financial reporting helps the companies to recognise and

measure their assets, liabilities, equity, incomes, and expenses. The essence of using the

conceptual framework is to ensure that financial reports are relevant and portrays a faithful

representation of a company’s financial position. Likewise, organisations such as The

International Integrated Reporting Council (IIRC) and the Global Reporting Initiative (GRI) of

integrated financial reporting and sustainable financial reporting, respectively. Companies are

slowly turning their attention to CSR initiatives as a means of creating value.

This paper examines the application of the conceptual framework, sustainable reporting, and

integrated reporting in current accounting practices. The paper is divided into two parts — part A

analysis of the application of the conceptual framework for financial reporting. Likewise, part B

evaluates the need to adopt either sustainable reporting or integrated reporting.

PART A: Conceptual framework

a) History and development of the Conceptual Framework for Financial Reporting

The International Accounting Standards Board (IASB) released its first conceptual framework in

1989. However, this version was criticised for lacking clarity and objectivity. The International

Financial Reporting Standards (IFRS) was tasked with the responsibility of providing an

improved version of the conceptual framework for financial reporting.

The process of collecting recommendations and views to develop conceptual framework began in

the 1940s in the UK. The process of reviewing the collected information began in 1991, which

show the release of the conceptual framework in 2010. In Australia, AASB developed the SACs

Accounting 4

1 to 4 which are used to prepare financial reports in the 1990s. AASB adopted the IASB’s

conceptual framework in 2005. However, SAC 1 (reporting entity) and SAC 2 (objectives) were

retained.

In 2004, both IASB and FASB agreed to work together and revise the 1989 conceptual frame. As

a result, the 2010 revived conceptual framework was adopted (Delloite, 2018). The 2010 version

was more improved compared to the 1989 version. IASB embarked on the process of improving

its framework once more. The latest version of the conceptual framework was approved and

released on 29 March 2018. The updated version introduced comprehensive changes that had

been excluded by the two previous versions (IASB, 2018). Today. Over 200 nations have

adopted the IASB’s conceptual framework globally.

b) Concerns raised by the Australian accounting professions regarding the Conceptual

Framework

The Australian Accounting Standards Board (AASB) supports the IASB’s conceptual framework

for financial reporting. However, both the AASB and the Australian accounting professions are

concerned with the objectivity of the 2018 conceptual framework. AASB believes that the

concept cannot be relied on by standard creators at its current state. First, the board believes that

the IASB’s conceptual framework need several revisions to conform to the Australian accounting

standards and principles. Likewise, the Australian Accounting professions believe that the

conceptual framework is incomplete, unclear, and does not address all the current accounting

issues facing Australian firms (Delloite, 2018).

There is a general view of the conceptual framework for financial reporting has failed to

adequately address the current accounting/ financial reporting issues in the Australian and global

1 to 4 which are used to prepare financial reports in the 1990s. AASB adopted the IASB’s

conceptual framework in 2005. However, SAC 1 (reporting entity) and SAC 2 (objectives) were

retained.

In 2004, both IASB and FASB agreed to work together and revise the 1989 conceptual frame. As

a result, the 2010 revived conceptual framework was adopted (Delloite, 2018). The 2010 version

was more improved compared to the 1989 version. IASB embarked on the process of improving

its framework once more. The latest version of the conceptual framework was approved and

released on 29 March 2018. The updated version introduced comprehensive changes that had

been excluded by the two previous versions (IASB, 2018). Today. Over 200 nations have

adopted the IASB’s conceptual framework globally.

b) Concerns raised by the Australian accounting professions regarding the Conceptual

Framework

The Australian Accounting Standards Board (AASB) supports the IASB’s conceptual framework

for financial reporting. However, both the AASB and the Australian accounting professions are

concerned with the objectivity of the 2018 conceptual framework. AASB believes that the

concept cannot be relied on by standard creators at its current state. First, the board believes that

the IASB’s conceptual framework need several revisions to conform to the Australian accounting

standards and principles. Likewise, the Australian Accounting professions believe that the

conceptual framework is incomplete, unclear, and does not address all the current accounting

issues facing Australian firms (Delloite, 2018).

There is a general view of the conceptual framework for financial reporting has failed to

adequately address the current accounting/ financial reporting issues in the Australian and global

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting 5

markets. For instance, there is no clear definition between the other comprehensive income (OCI)

and the profit and loss statements. Such a confusion might hinder recording to income and

expenses in either of the two statements. AASB proposes that IASB should provide a clear

distinction to help users to easily differentiate the financial items that appear in either of them.

Accounting professions are also concerned about the application of the bundle of rights. The

conceptual framework state that assets can be split for accounting purpose. However, professions

are concerned with the extent of splitting assets and the impact of such action on the recognition

and derecognition of assets. Lastly, New control based approach states that assets should be

derecognised when a company loses control of it. However, professions are concerned with what

to do when a company has retained partial right on an asset (IASB, 2018).

c) Concerns raised by the concerns of the academic about the quality of the Conceptual

Framework

Numerous academic researches and literature reviews support the 2018 version of the conceptual

framework for financial reporting. However, a few criticisms have been reported by

academicians. A review that the raised issues are substantial and should be addressed by the

IASB (Ravitch, 2016, p. 112). First, academicians claim that the process of developing the

conceptual framework in affected by political interference. Different players would present views

that support their application without carrying about other stakeholders. Contributors are more

interested in self-interest over social interest (PKF International Ltd, 2016, p. 733).

Second, the conceptual framework for financial reporting has failed to address weight accounting

issues. When heated arguments between members arise on the application of the framework, the

objectivity tends to be lost. Third, the conceptual framework has failed to address the non-

markets. For instance, there is no clear definition between the other comprehensive income (OCI)

and the profit and loss statements. Such a confusion might hinder recording to income and

expenses in either of the two statements. AASB proposes that IASB should provide a clear

distinction to help users to easily differentiate the financial items that appear in either of them.

Accounting professions are also concerned about the application of the bundle of rights. The

conceptual framework state that assets can be split for accounting purpose. However, professions

are concerned with the extent of splitting assets and the impact of such action on the recognition

and derecognition of assets. Lastly, New control based approach states that assets should be

derecognised when a company loses control of it. However, professions are concerned with what

to do when a company has retained partial right on an asset (IASB, 2018).

c) Concerns raised by the concerns of the academic about the quality of the Conceptual

Framework

Numerous academic researches and literature reviews support the 2018 version of the conceptual

framework for financial reporting. However, a few criticisms have been reported by

academicians. A review that the raised issues are substantial and should be addressed by the

IASB (Ravitch, 2016, p. 112). First, academicians claim that the process of developing the

conceptual framework in affected by political interference. Different players would present views

that support their application without carrying about other stakeholders. Contributors are more

interested in self-interest over social interest (PKF International Ltd, 2016, p. 733).

Second, the conceptual framework for financial reporting has failed to address weight accounting

issues. When heated arguments between members arise on the application of the framework, the

objectivity tends to be lost. Third, the conceptual framework has failed to address the non-

Accounting 6

performance aspect of business entities (Macve, 2015, p. 79). Fourth, the process of complying

with the conceptual framework is costly for small businesses. Fifth, the framework is considered

ambiguous because it is open to interpretation. Lastly, principles under the conceptual framework

are vague; they describe accounting practices without providing remedies to current accounting

issues (Hussey & Ong, 2017, p. 201).

d) How Pro Medicus Ltd (ASX: PME) apply a conceptual framework to prepare its annual

reports

AASB states that the conceptual framework for financial reporting should guide the public listed

companies in Australia. This section reviews the application of the framework by the Pro

Medicus Ltd to prepare its 2018 financial statements.

(i) Financial components used by Pro Medicus to prepare its financial statement

The conceptual framework for financial reporting states that an annual report must contain

several financial statements to be considered relevant and a faithful representation of an

organisation. The recognised financial statements under the conceptual frame and the AASB’s

SAC 3 are;

a) The balance sheet which comprises of financial elements such as asset, liabilities, and

capital,

b) The income statement which comprises of income and expense financial elements,

c) The cash flow statement is made up of operating, investment, and capital activities of a

business.

d) Other comprehensive income (OCI) statement, which comprises of the changes in the

income and expense financial elements (Pro Medicus Ltd, 2019, p. 45).

performance aspect of business entities (Macve, 2015, p. 79). Fourth, the process of complying

with the conceptual framework is costly for small businesses. Fifth, the framework is considered

ambiguous because it is open to interpretation. Lastly, principles under the conceptual framework

are vague; they describe accounting practices without providing remedies to current accounting

issues (Hussey & Ong, 2017, p. 201).

d) How Pro Medicus Ltd (ASX: PME) apply a conceptual framework to prepare its annual

reports

AASB states that the conceptual framework for financial reporting should guide the public listed

companies in Australia. This section reviews the application of the framework by the Pro

Medicus Ltd to prepare its 2018 financial statements.

(i) Financial components used by Pro Medicus to prepare its financial statement

The conceptual framework for financial reporting states that an annual report must contain

several financial statements to be considered relevant and a faithful representation of an

organisation. The recognised financial statements under the conceptual frame and the AASB’s

SAC 3 are;

a) The balance sheet which comprises of financial elements such as asset, liabilities, and

capital,

b) The income statement which comprises of income and expense financial elements,

c) The cash flow statement is made up of operating, investment, and capital activities of a

business.

d) Other comprehensive income (OCI) statement, which comprises of the changes in the

income and expense financial elements (Pro Medicus Ltd, 2019, p. 45).

Accounting 7

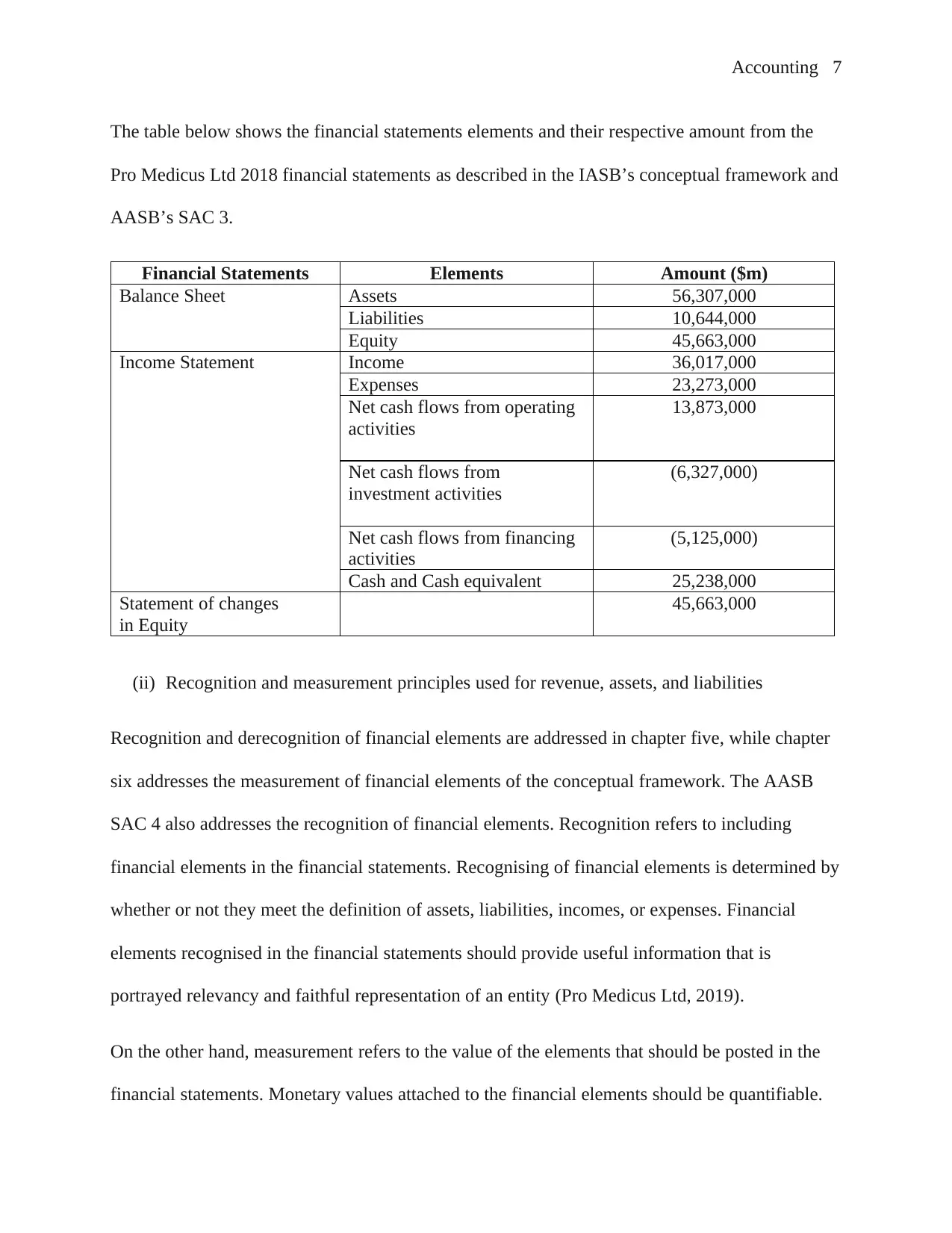

The table below shows the financial statements elements and their respective amount from the

Pro Medicus Ltd 2018 financial statements as described in the IASB’s conceptual framework and

AASB’s SAC 3.

Financial Statements Elements Amount ($m)

Balance Sheet Assets 56,307,000

Liabilities 10,644,000

Equity 45,663,000

Income Statement Income 36,017,000

Expenses 23,273,000

Net cash flows from operating

activities

13,873,000

Net cash flows from

investment activities

(6,327,000)

Net cash flows from financing

activities

(5,125,000)

Cash and Cash equivalent 25,238,000

Statement of changes

in Equity

45,663,000

(ii) Recognition and measurement principles used for revenue, assets, and liabilities

Recognition and derecognition of financial elements are addressed in chapter five, while chapter

six addresses the measurement of financial elements of the conceptual framework. The AASB

SAC 4 also addresses the recognition of financial elements. Recognition refers to including

financial elements in the financial statements. Recognising of financial elements is determined by

whether or not they meet the definition of assets, liabilities, incomes, or expenses. Financial

elements recognised in the financial statements should provide useful information that is

portrayed relevancy and faithful representation of an entity (Pro Medicus Ltd, 2019).

On the other hand, measurement refers to the value of the elements that should be posted in the

financial statements. Monetary values attached to the financial elements should be quantifiable.

The table below shows the financial statements elements and their respective amount from the

Pro Medicus Ltd 2018 financial statements as described in the IASB’s conceptual framework and

AASB’s SAC 3.

Financial Statements Elements Amount ($m)

Balance Sheet Assets 56,307,000

Liabilities 10,644,000

Equity 45,663,000

Income Statement Income 36,017,000

Expenses 23,273,000

Net cash flows from operating

activities

13,873,000

Net cash flows from

investment activities

(6,327,000)

Net cash flows from financing

activities

(5,125,000)

Cash and Cash equivalent 25,238,000

Statement of changes

in Equity

45,663,000

(ii) Recognition and measurement principles used for revenue, assets, and liabilities

Recognition and derecognition of financial elements are addressed in chapter five, while chapter

six addresses the measurement of financial elements of the conceptual framework. The AASB

SAC 4 also addresses the recognition of financial elements. Recognition refers to including

financial elements in the financial statements. Recognising of financial elements is determined by

whether or not they meet the definition of assets, liabilities, incomes, or expenses. Financial

elements recognised in the financial statements should provide useful information that is

portrayed relevancy and faithful representation of an entity (Pro Medicus Ltd, 2019).

On the other hand, measurement refers to the value of the elements that should be posted in the

financial statements. Monetary values attached to the financial elements should be quantifiable.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 8

The conceptual framework offers several basis for measuring financial elements. The recognised

measurement basis is historical cost, and current cost (fair value, present value, and net realisable

value) (Pro Medicus Ltd, 2019).

Pro Medicus Ltd used the following measurement basis in its 2018 financial statements.

The company recognises its income at fair value.

Expenses are recognised at their historical cost.

Cash and cash equivalent is recognised at fair value, which is their carrying amount.

Account receivable are initially recognised at fair value and subsequently at their

amortised cost.

Plant and equipment are recognised at historical cost less accumulated depreciation and

impairment value.

Inventory is recognised at the lower value between realisable value and historical cost.

Intangible assets are recognised at their fair value.

Account payable is recognised at the amortised cost.

Provisions are recognised at the present obligations

(iii) Qualitative characteristics of information exhibit in the report

Chapter two of the financial statement states that financial statements should have qualitative

characteristics such as faithful representation, relevance, and materiality. The characteristics are

further enhanced by attributes like comparability, understandability, timeliness, and verifiability.

Pro Medicus Ltd’s 2018 annual report was prepared by the Australian Corporation Act 2001. The

management also complied with the requirements of AASB and IASB. The accounting

judgments, assumptions, and estimates made by the management were based on historical

The conceptual framework offers several basis for measuring financial elements. The recognised

measurement basis is historical cost, and current cost (fair value, present value, and net realisable

value) (Pro Medicus Ltd, 2019).

Pro Medicus Ltd used the following measurement basis in its 2018 financial statements.

The company recognises its income at fair value.

Expenses are recognised at their historical cost.

Cash and cash equivalent is recognised at fair value, which is their carrying amount.

Account receivable are initially recognised at fair value and subsequently at their

amortised cost.

Plant and equipment are recognised at historical cost less accumulated depreciation and

impairment value.

Inventory is recognised at the lower value between realisable value and historical cost.

Intangible assets are recognised at their fair value.

Account payable is recognised at the amortised cost.

Provisions are recognised at the present obligations

(iii) Qualitative characteristics of information exhibit in the report

Chapter two of the financial statement states that financial statements should have qualitative

characteristics such as faithful representation, relevance, and materiality. The characteristics are

further enhanced by attributes like comparability, understandability, timeliness, and verifiability.

Pro Medicus Ltd’s 2018 annual report was prepared by the Australian Corporation Act 2001. The

management also complied with the requirements of AASB and IASB. The accounting

judgments, assumptions, and estimates made by the management were based on historical

Accounting 9

experience, market information, expert opinions, and other valuable factors. The Ernst & young

auditors were contracted to contract the 2018 financial report. The auditors believed that the

financial report was presented a true and fair value of the company and was complied with the

necessary accounting requirements. Therefore, the statements are relevant and present a faithful

representation of Pro Medicus Ltd financial position as of June 30, 2018 (Pro Medicus Ltd, 2019,

p. 18).

PART B: Integrated/sustainability reporting

a) Comparing Sustainability Reporting Guidelines and International Integrated Reporting

Framework

The International Integrated Reporting Council (IIRC) and the Global Reporting Initiative (GRI)

have a common goal which seeks the inclusion of non-financial performance indicators in the

annual reports. The two organizations believe that the paradigm should shift from conventional

financial reporting to a sustainable or integrated financial reporting. GRI and IIRC maintain that

firms use a significant amount of resources and time to promote environmental and social

wellbeing. The resources and time are invested in creating value by contributing positively to the

wellbeing of the stakeholders. However, failure to include such a noble investment in the annual

reporting does not profit faithful representation and relevance characteristics of the conceptual

framework (IIRC, 2019).

The GRI is promoting the adoption of a sustainable reporting over the financial performance

based reporting. Sustainable reporting comprises of both the financial and non-financial aspects

such as environmental and social. According to the GRI, sustainable financial reporting would

enhance efficient and effecting reporting of annual performances. Moreover, it would help in

experience, market information, expert opinions, and other valuable factors. The Ernst & young

auditors were contracted to contract the 2018 financial report. The auditors believed that the

financial report was presented a true and fair value of the company and was complied with the

necessary accounting requirements. Therefore, the statements are relevant and present a faithful

representation of Pro Medicus Ltd financial position as of June 30, 2018 (Pro Medicus Ltd, 2019,

p. 18).

PART B: Integrated/sustainability reporting

a) Comparing Sustainability Reporting Guidelines and International Integrated Reporting

Framework

The International Integrated Reporting Council (IIRC) and the Global Reporting Initiative (GRI)

have a common goal which seeks the inclusion of non-financial performance indicators in the

annual reports. The two organizations believe that the paradigm should shift from conventional

financial reporting to a sustainable or integrated financial reporting. GRI and IIRC maintain that

firms use a significant amount of resources and time to promote environmental and social

wellbeing. The resources and time are invested in creating value by contributing positively to the

wellbeing of the stakeholders. However, failure to include such a noble investment in the annual

reporting does not profit faithful representation and relevance characteristics of the conceptual

framework (IIRC, 2019).

The GRI is promoting the adoption of a sustainable reporting over the financial performance

based reporting. Sustainable reporting comprises of both the financial and non-financial aspects

such as environmental and social. According to the GRI, sustainable financial reporting would

enhance efficient and effecting reporting of annual performances. Moreover, it would help in

Accounting 10

producing reliable and relevant information that will help stakeholders to make informed

decisions. On the other hand, IIRC is pushing for the adoption of an integrated financial

reporting, which has a broader view as compared to the GRI’s sustainable reporting. The

integrated reporting promotes the inclusion of social and environmental elements of value

creation in addition to governance and the relationship between a company and its stakeholders

(Deloitte, 2018).

b) Examining the conventional accounting about the concepts of sustainability and

integrated reporting

Conventional accounting can also be referred to as the traditional accounting methods. Under the

conventional accounting method focuses more on the financial performance of an organization.

In other words, the success of an organisation is measured in its ability to use its financial

position to compete. Conventional accounting favoured the investors because it promoted wealth

maximisation. Organisations do not have to invest in society and the environment as a way of

creating value. Based on this position, conventional accounting cannot help in the successful

implementation of CSR initiatives (IIRC, 2019).

Today different accounting stakeholders acknowledge the importance of investing in CSR

initiatives as a way of creating value by companies. Investing in projects that promote social and

environmental wellbeing is on the rise. Likewise, companies are focussed on improving their

corporate image and brand reputation. Companies use part of their retained earnings to invest in

CSR projects. Stakeholders need to know why and how companies engage in CSR projects. The

CSR projects enhance the relationship between the company and stakeholders, which

subsequently increase sales volume and profitability. Companies need to embrace either

producing reliable and relevant information that will help stakeholders to make informed

decisions. On the other hand, IIRC is pushing for the adoption of an integrated financial

reporting, which has a broader view as compared to the GRI’s sustainable reporting. The

integrated reporting promotes the inclusion of social and environmental elements of value

creation in addition to governance and the relationship between a company and its stakeholders

(Deloitte, 2018).

b) Examining the conventional accounting about the concepts of sustainability and

integrated reporting

Conventional accounting can also be referred to as the traditional accounting methods. Under the

conventional accounting method focuses more on the financial performance of an organization.

In other words, the success of an organisation is measured in its ability to use its financial

position to compete. Conventional accounting favoured the investors because it promoted wealth

maximisation. Organisations do not have to invest in society and the environment as a way of

creating value. Based on this position, conventional accounting cannot help in the successful

implementation of CSR initiatives (IIRC, 2019).

Today different accounting stakeholders acknowledge the importance of investing in CSR

initiatives as a way of creating value by companies. Investing in projects that promote social and

environmental wellbeing is on the rise. Likewise, companies are focussed on improving their

corporate image and brand reputation. Companies use part of their retained earnings to invest in

CSR projects. Stakeholders need to know why and how companies engage in CSR projects. The

CSR projects enhance the relationship between the company and stakeholders, which

subsequently increase sales volume and profitability. Companies need to embrace either

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting 11

sustainable or integrated reporting, which includes both the financial and non-financial

performance in the annual reports (Deloitte, 2018).

c) Theoretical explanation of the sustainable and integrated reporting

Both the sustainable reporting and integrated reporting seek the inclusion of environmental and

social factors in financial reporting. The two reporting methods have gained momentum globally

because they promote the concept of the social contract. The adoption of the two reporting

methods can be explained using legitimacy theory, stakeholder theory, and institutional theory.

Legitimacy theory examines the relationship between community expectations and firms

disclosure. Firm use media reports to understand how the community perceives them as well as

the communities’ expectations from them. In return, the community should use annual reports to

address the issues raised by the community and win back its support (Deegan, 2013, p. 72).

Stakeholder theory states that the organisation should treat their stakeholders fairly. That is, the

decisions made by the management should benefit the organisation’s stakeholders. Organizations

have the responsibility to find an optimal balance for conflict of interest between the

stakeholders. Moreover, stakeholders have the right to information and accountability from the

management. The organization should take social and environmental actions and account for such

actions (Deegan, 2013, p. 73).

The institutional theory maintains that firms should engage in promoting the social and

environmental issues arising from their actions. Some of the stakeholders identified in theory are

the society, government, NGOs, and the industry. Organizations not only need to engage in CSR

activities but also account for them in the financial reports (Wolk, et al., 2017, p. 69).

sustainable or integrated reporting, which includes both the financial and non-financial

performance in the annual reports (Deloitte, 2018).

c) Theoretical explanation of the sustainable and integrated reporting

Both the sustainable reporting and integrated reporting seek the inclusion of environmental and

social factors in financial reporting. The two reporting methods have gained momentum globally

because they promote the concept of the social contract. The adoption of the two reporting

methods can be explained using legitimacy theory, stakeholder theory, and institutional theory.

Legitimacy theory examines the relationship between community expectations and firms

disclosure. Firm use media reports to understand how the community perceives them as well as

the communities’ expectations from them. In return, the community should use annual reports to

address the issues raised by the community and win back its support (Deegan, 2013, p. 72).

Stakeholder theory states that the organisation should treat their stakeholders fairly. That is, the

decisions made by the management should benefit the organisation’s stakeholders. Organizations

have the responsibility to find an optimal balance for conflict of interest between the

stakeholders. Moreover, stakeholders have the right to information and accountability from the

management. The organization should take social and environmental actions and account for such

actions (Deegan, 2013, p. 73).

The institutional theory maintains that firms should engage in promoting the social and

environmental issues arising from their actions. Some of the stakeholders identified in theory are

the society, government, NGOs, and the industry. Organizations not only need to engage in CSR

activities but also account for them in the financial reports (Wolk, et al., 2017, p. 69).

Accounting 12

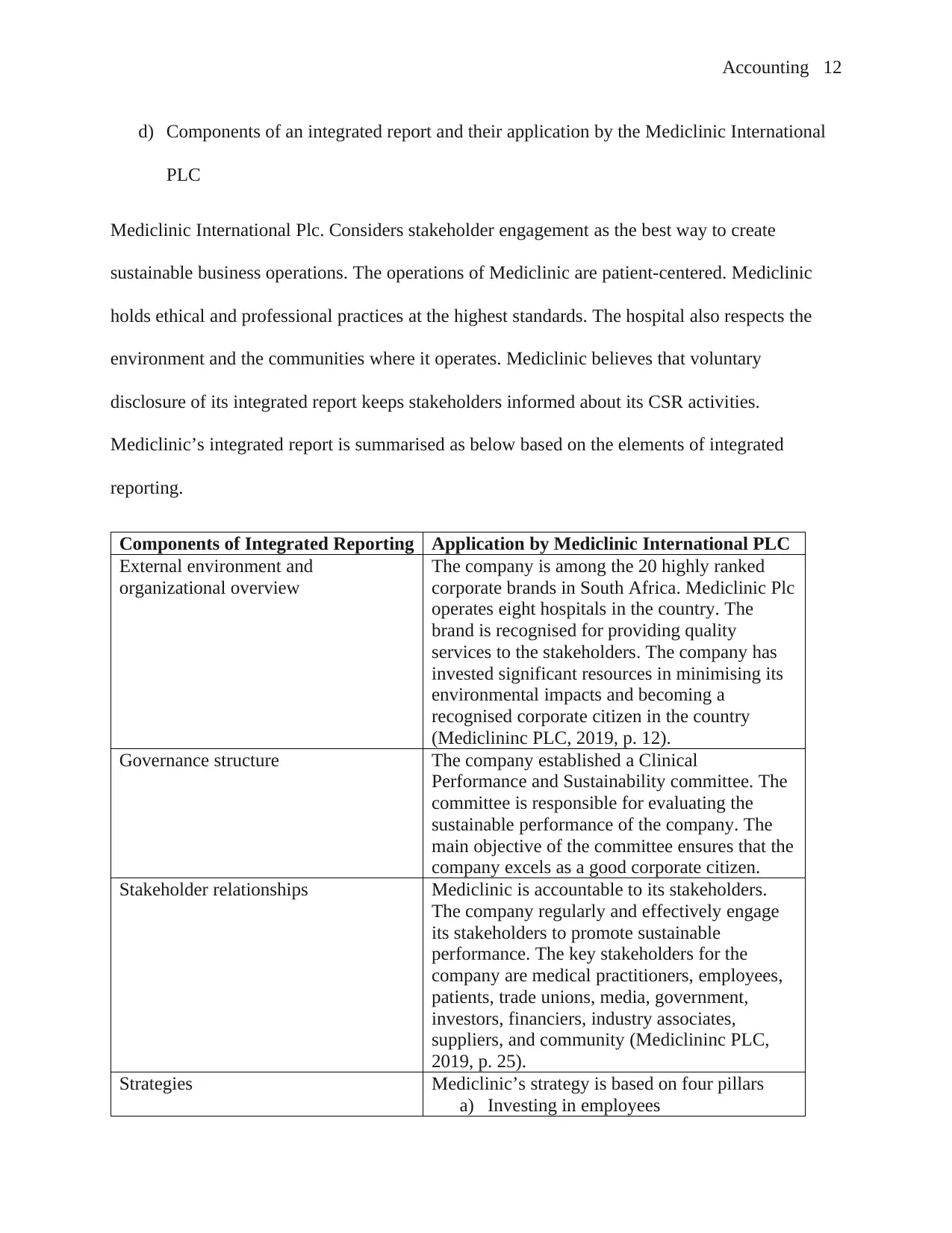

d) Components of an integrated report and their application by the Mediclinic International

PLC

Mediclinic International Plc. Considers stakeholder engagement as the best way to create

sustainable business operations. The operations of Mediclinic are patient-centered. Mediclinic

holds ethical and professional practices at the highest standards. The hospital also respects the

environment and the communities where it operates. Mediclinic believes that voluntary

disclosure of its integrated report keeps stakeholders informed about its CSR activities.

Mediclinic’s integrated report is summarised as below based on the elements of integrated

reporting.

Components of Integrated Reporting Application by Mediclinic International PLC

External environment and

organizational overview

The company is among the 20 highly ranked

corporate brands in South Africa. Mediclinic Plc

operates eight hospitals in the country. The

brand is recognised for providing quality

services to the stakeholders. The company has

invested significant resources in minimising its

environmental impacts and becoming a

recognised corporate citizen in the country

(Mediclininc PLC, 2019, p. 12).

Governance structure The company established a Clinical

Performance and Sustainability committee. The

committee is responsible for evaluating the

sustainable performance of the company. The

main objective of the committee ensures that the

company excels as a good corporate citizen.

Stakeholder relationships Mediclinic is accountable to its stakeholders.

The company regularly and effectively engage

its stakeholders to promote sustainable

performance. The key stakeholders for the

company are medical practitioners, employees,

patients, trade unions, media, government,

investors, financiers, industry associates,

suppliers, and community (Mediclininc PLC,

2019, p. 25).

Strategies Mediclinic’s strategy is based on four pillars

a) Investing in employees

d) Components of an integrated report and their application by the Mediclinic International

PLC

Mediclinic International Plc. Considers stakeholder engagement as the best way to create

sustainable business operations. The operations of Mediclinic are patient-centered. Mediclinic

holds ethical and professional practices at the highest standards. The hospital also respects the

environment and the communities where it operates. Mediclinic believes that voluntary

disclosure of its integrated report keeps stakeholders informed about its CSR activities.

Mediclinic’s integrated report is summarised as below based on the elements of integrated

reporting.

Components of Integrated Reporting Application by Mediclinic International PLC

External environment and

organizational overview

The company is among the 20 highly ranked

corporate brands in South Africa. Mediclinic Plc

operates eight hospitals in the country. The

brand is recognised for providing quality

services to the stakeholders. The company has

invested significant resources in minimising its

environmental impacts and becoming a

recognised corporate citizen in the country

(Mediclininc PLC, 2019, p. 12).

Governance structure The company established a Clinical

Performance and Sustainability committee. The

committee is responsible for evaluating the

sustainable performance of the company. The

main objective of the committee ensures that the

company excels as a good corporate citizen.

Stakeholder relationships Mediclinic is accountable to its stakeholders.

The company regularly and effectively engage

its stakeholders to promote sustainable

performance. The key stakeholders for the

company are medical practitioners, employees,

patients, trade unions, media, government,

investors, financiers, industry associates,

suppliers, and community (Mediclininc PLC,

2019, p. 25).

Strategies Mediclinic’s strategy is based on four pillars

a) Investing in employees

Accounting 13

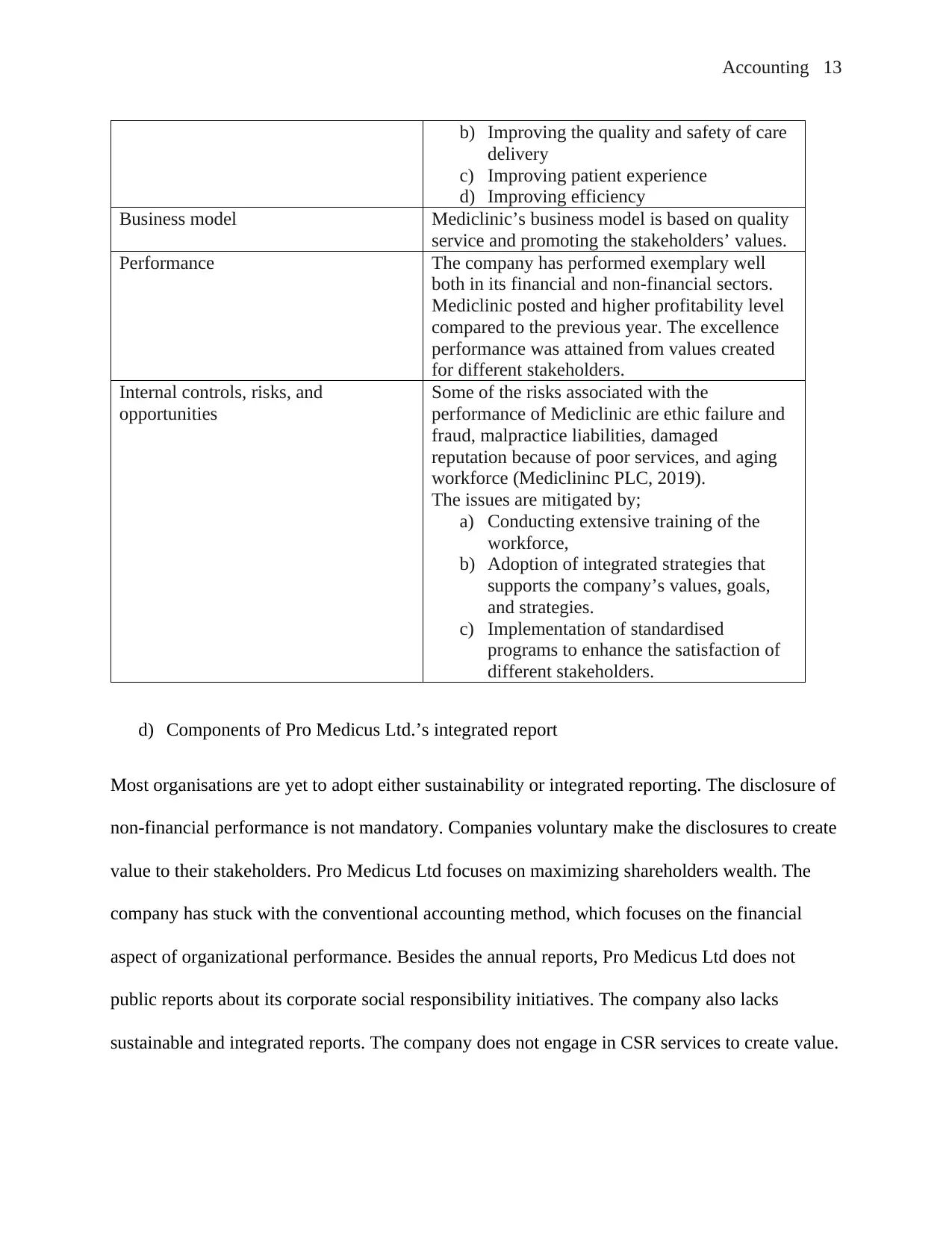

b) Improving the quality and safety of care

delivery

c) Improving patient experience

d) Improving efficiency

Business model Mediclinic’s business model is based on quality

service and promoting the stakeholders’ values.

Performance The company has performed exemplary well

both in its financial and non-financial sectors.

Mediclinic posted and higher profitability level

compared to the previous year. The excellence

performance was attained from values created

for different stakeholders.

Internal controls, risks, and

opportunities

Some of the risks associated with the

performance of Mediclinic are ethic failure and

fraud, malpractice liabilities, damaged

reputation because of poor services, and aging

workforce (Mediclininc PLC, 2019).

The issues are mitigated by;

a) Conducting extensive training of the

workforce,

b) Adoption of integrated strategies that

supports the company’s values, goals,

and strategies.

c) Implementation of standardised

programs to enhance the satisfaction of

different stakeholders.

d) Components of Pro Medicus Ltd.’s integrated report

Most organisations are yet to adopt either sustainability or integrated reporting. The disclosure of

non-financial performance is not mandatory. Companies voluntary make the disclosures to create

value to their stakeholders. Pro Medicus Ltd focuses on maximizing shareholders wealth. The

company has stuck with the conventional accounting method, which focuses on the financial

aspect of organizational performance. Besides the annual reports, Pro Medicus Ltd does not

public reports about its corporate social responsibility initiatives. The company also lacks

sustainable and integrated reports. The company does not engage in CSR services to create value.

b) Improving the quality and safety of care

delivery

c) Improving patient experience

d) Improving efficiency

Business model Mediclinic’s business model is based on quality

service and promoting the stakeholders’ values.

Performance The company has performed exemplary well

both in its financial and non-financial sectors.

Mediclinic posted and higher profitability level

compared to the previous year. The excellence

performance was attained from values created

for different stakeholders.

Internal controls, risks, and

opportunities

Some of the risks associated with the

performance of Mediclinic are ethic failure and

fraud, malpractice liabilities, damaged

reputation because of poor services, and aging

workforce (Mediclininc PLC, 2019).

The issues are mitigated by;

a) Conducting extensive training of the

workforce,

b) Adoption of integrated strategies that

supports the company’s values, goals,

and strategies.

c) Implementation of standardised

programs to enhance the satisfaction of

different stakeholders.

d) Components of Pro Medicus Ltd.’s integrated report

Most organisations are yet to adopt either sustainability or integrated reporting. The disclosure of

non-financial performance is not mandatory. Companies voluntary make the disclosures to create

value to their stakeholders. Pro Medicus Ltd focuses on maximizing shareholders wealth. The

company has stuck with the conventional accounting method, which focuses on the financial

aspect of organizational performance. Besides the annual reports, Pro Medicus Ltd does not

public reports about its corporate social responsibility initiatives. The company also lacks

sustainable and integrated reports. The company does not engage in CSR services to create value.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 14

Moreover, there is no evidence in the annual report that shows that Pro Medicus Ltd has reported

engaging in CSR activities.

A comparison between Pro Medicus Ltd and the Mediclinic International PLC shows that they

use two different accounting methods. Pro Medicus Ltd uses the conventional accounting

method. On the other hand, the Mediclinic International PLC has adopted the sustainability

reporting method where the financial and sustainable performance reports during a financial year

are released separately. Pro Medicus Ltd focuses its strategy on maximising the shareholders’

wealth without considering the impact of their business activities on the society and environment.

Unlike Pro Medicus Ltd., the Mediclinic International PLC publishes a report about its

engagement with the different stakeholders to create value.

Conclusion

The study is divided into two parts which addressed the conceptual framework concept and

sustainable and integrated reporting. A conceptual framework is provided to companies with the

basis of developing accounting standards. A conceptual framework for financial reporting helps

the companies to recognise and measure their assets, liabilities, equity, incomes, and expenses.

The conceptual framework is to ensure that financial reports are relevant and portrays a faithful

representation of a company’s financial position.

Likewise, organisations such as The IIRC and the GRI have been pushing for the adoption of

integrated financial reporting and sustainable financial reporting, respectively. Companies are

slowly turning their attention to CSR initiatives as a means of creating value.

The study found out that Pro Medicus Ltd (ASX: PME) complied with the conceptual framework

for financial reporting to prepare its 2018 financial statements. However, the company is yet to

Moreover, there is no evidence in the annual report that shows that Pro Medicus Ltd has reported

engaging in CSR activities.

A comparison between Pro Medicus Ltd and the Mediclinic International PLC shows that they

use two different accounting methods. Pro Medicus Ltd uses the conventional accounting

method. On the other hand, the Mediclinic International PLC has adopted the sustainability

reporting method where the financial and sustainable performance reports during a financial year

are released separately. Pro Medicus Ltd focuses its strategy on maximising the shareholders’

wealth without considering the impact of their business activities on the society and environment.

Unlike Pro Medicus Ltd., the Mediclinic International PLC publishes a report about its

engagement with the different stakeholders to create value.

Conclusion

The study is divided into two parts which addressed the conceptual framework concept and

sustainable and integrated reporting. A conceptual framework is provided to companies with the

basis of developing accounting standards. A conceptual framework for financial reporting helps

the companies to recognise and measure their assets, liabilities, equity, incomes, and expenses.

The conceptual framework is to ensure that financial reports are relevant and portrays a faithful

representation of a company’s financial position.

Likewise, organisations such as The IIRC and the GRI have been pushing for the adoption of

integrated financial reporting and sustainable financial reporting, respectively. Companies are

slowly turning their attention to CSR initiatives as a means of creating value.

The study found out that Pro Medicus Ltd (ASX: PME) complied with the conceptual framework

for financial reporting to prepare its 2018 financial statements. However, the company is yet to

Accounting 15

adopt either sustainable reporting or integrate reporting within the current accounting practice

globally. On the other hand, the Mediclinic International PLC has incorporated both financial and

non-financial indicators of performance in its annual report. Mediclinic International PLC

engages with its stakeholders to organizational value. Considering that CSR has become an

important part of business operations, it’s time to adopt either sustainable reporting or integrated

reporting.

References List

Deegan, C., 2013. Financial accounting theory. 4th Edition ed. North Ryde, N.S.W: McGraw-

Hill Education.

Delloite, 2018. Conceptual Framework Phase A – Objective and qualitative characteristics, New

York: Delloite.

adopt either sustainable reporting or integrate reporting within the current accounting practice

globally. On the other hand, the Mediclinic International PLC has incorporated both financial and

non-financial indicators of performance in its annual report. Mediclinic International PLC

engages with its stakeholders to organizational value. Considering that CSR has become an

important part of business operations, it’s time to adopt either sustainable reporting or integrated

reporting.

References List

Deegan, C., 2013. Financial accounting theory. 4th Edition ed. North Ryde, N.S.W: McGraw-

Hill Education.

Delloite, 2018. Conceptual Framework Phase A – Objective and qualitative characteristics, New

York: Delloite.

Accounting 16

Deloitte, 2018. International Integrated Reporting Council (IIRC). [Online]

Available at: https://www.iasplus.com/en/resources/sustainability/iirc

[Accessed 25 May 2019].

Hussey, R. & Ong, A., 2017. Corporate Financial Reporting. London: Macmillan International

Higher Education.

IASB, 2018. Conceptual Framework for Financial Reporting 2018. [Online]

Available at: https://www.iasplus.com/en/standards/other/framework

[Accessed 25 May 2019].

Idowu, S. O. & Tudor, A. T., 2016. From CSR and Sustainability to integrated Reporting.

International Journal of Entrepreneurship and Innovation, 2(10).

IIRC, 2019. Global Reporting Initiative: GRI and the IIRC working together. [Online]

Available at: https://integratedreporting.org/profile/global-reporting-initiative/

[Accessed 25 May 2019].

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, or Threat?, New York: Routledge.

Mediclininc PLC, 2019. 2018 Sustainable Report, Johanesburg: Mediclininc PLC.

PKF International Ltd, 2016. Wiley IFRS 2016: Interpretation and Application of International

Financial Reporting Standards. Illustrated ed. Mew York: John Wiley & Sons.

Pro Medicus Ltd, 2019. 2018 Annual Report, Sydney: Pro Medicus Ltd.

Ravitch, S. M., 2016. Reason & Rigor: How Conceptual Frameworks Guide Research. London,

UK: SAGE Publications.

Deloitte, 2018. International Integrated Reporting Council (IIRC). [Online]

Available at: https://www.iasplus.com/en/resources/sustainability/iirc

[Accessed 25 May 2019].

Hussey, R. & Ong, A., 2017. Corporate Financial Reporting. London: Macmillan International

Higher Education.

IASB, 2018. Conceptual Framework for Financial Reporting 2018. [Online]

Available at: https://www.iasplus.com/en/standards/other/framework

[Accessed 25 May 2019].

Idowu, S. O. & Tudor, A. T., 2016. From CSR and Sustainability to integrated Reporting.

International Journal of Entrepreneurship and Innovation, 2(10).

IIRC, 2019. Global Reporting Initiative: GRI and the IIRC working together. [Online]

Available at: https://integratedreporting.org/profile/global-reporting-initiative/

[Accessed 25 May 2019].

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, or Threat?, New York: Routledge.

Mediclininc PLC, 2019. 2018 Sustainable Report, Johanesburg: Mediclininc PLC.

PKF International Ltd, 2016. Wiley IFRS 2016: Interpretation and Application of International

Financial Reporting Standards. Illustrated ed. Mew York: John Wiley & Sons.

Pro Medicus Ltd, 2019. 2018 Annual Report, Sydney: Pro Medicus Ltd.

Ravitch, S. M., 2016. Reason & Rigor: How Conceptual Frameworks Guide Research. London,

UK: SAGE Publications.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting 17

Wolk, H. I., Dodd , J. L. & Rozycki, J. J., 2017. Accounting Theory: Conceptual Issues in a

Political and Economic Environment. 1 ed. London: SAGE Publications.

Wolk, H. I., Dodd , J. L. & Rozycki, J. J., 2017. Accounting Theory: Conceptual Issues in a

Political and Economic Environment. 1 ed. London: SAGE Publications.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.