Accounting Report: Conceptual Framework, Sustainability and Reporting

VerifiedAdded on 2023/03/31

|18

|4007

|307

Report

AI Summary

This report provides an in-depth analysis of the conceptual framework for financial reporting, examining its development in the USA, UK, Australia, and globally under the International Accounting Standards Board (IASB). The report investigates the Australian accounting profession's concerns regarding the application of the IASB/IFRS conceptual framework. It further explores sustainability and integrated reporting practices, discussing sustainability reporting guidelines and the integrated reporting framework. The report includes a comparison of Australian and South African companies' corporate social responsibility (CSR) reports, specifically focusing on PEET Limited and Echo Polska Properties. It also touches on the benefits, limitations, and applicability of integrated reporting and sustainability reporting theories, components of integrated reports, and how these are shown in the context of the companies mentioned.

RUNNING HEAD: ACCOUNTING 1

UNIVERSITY NAME

STUDENT NAME

STUDENT ID

COURSE

DATE

UNIVERSITY NAME

STUDENT NAME

STUDENT ID

COURSE

DATE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 2

EXECUTIVE SUMMARY

The purpose of this report is to shed light on how the conceptual framework was developed, its

fundamental principles and its applications globally. The report further outlines the process in

which the conceptual framework of accounting attempts to reduce the differences in the

accounting sector but harmonising different accounting methods and setting up the accounting

standards that must be meet by those in the sector. IFRS is the body mandated to supervise this

harmonisation process. Sustainability and integrated reporting of Australian and south African

companies is also discussed. The report discusses various components of an integrated report and

the applicability of such reports in the wider context of institutional reporting.

EXECUTIVE SUMMARY

The purpose of this report is to shed light on how the conceptual framework was developed, its

fundamental principles and its applications globally. The report further outlines the process in

which the conceptual framework of accounting attempts to reduce the differences in the

accounting sector but harmonising different accounting methods and setting up the accounting

standards that must be meet by those in the sector. IFRS is the body mandated to supervise this

harmonisation process. Sustainability and integrated reporting of Australian and south African

companies is also discussed. The report discusses various components of an integrated report and

the applicability of such reports in the wider context of institutional reporting.

ACCOUNTING 3

Table of Contents

INTRODUCTION...........................................................................................................................................4

CONCEPTUAL FRAMEWORK................................................................................................................4

ACCOUNTING PROFESION CONCERN................................................................................................5

BENEFITS AND LIMITATIONS OF CONCEPTUAL FRAMEWORK...................................................6

benefits....................................................................................................................................................6

Limitations..............................................................................................................................................7

REVENUE RECOGNITION AND MEASUREMENT BASIS..................................................................7

QUALITATIVE CHARACTERISTICS.....................................................................................................8

SUSTAINABILITY AND INTEGRATED REPORTING..........................................................................8

SUSTAINABILITY REPORTING GUIDELINES.....................................................................................9

INTEGRATED REPORT............................................................................................................................9

Integrated framework..............................................................................................................................9

Purpose of integrated report...................................................................................................................10

DIFFERENCES BETWEEN SUSTAINABILITY REPORTING GUIDELINES AND

INTERNATIONAL INTEGRATED REPORTING COUNCIL...............................................................10

HOW HOLISTIC IS SUSTAINABILITY REPORTING AND INTEGRATED REPORTING?.............10

STRENGHTS AND LIMITATIONS........................................................................................................11

APPLICABILITY OF INTEGRATED REPORTING AND SUSTAINABILTY REPORTING

THEORIES................................................................................................................................................12

integrated reporting theories..................................................................................................................12

sustainability reporting theories.............................................................................................................12

LIMITATION OF THESE THEORIES....................................................................................................12

COMPONENTS OF AN INTEGRATED REPORT.................................................................................12

HOW IT IS SHOWN IN ECHO POLSKA PROPERTIES.......................................................................13

COMPARISON OF AUSTRALIAN COMPANY AND SOUTH AFRICAN COMPANY CSR

REPORTS.................................................................................................................................................14

CONCLUSION.........................................................................................................................................16

REFERENCES..........................................................................................................................................16

Table of Contents

INTRODUCTION...........................................................................................................................................4

CONCEPTUAL FRAMEWORK................................................................................................................4

ACCOUNTING PROFESION CONCERN................................................................................................5

BENEFITS AND LIMITATIONS OF CONCEPTUAL FRAMEWORK...................................................6

benefits....................................................................................................................................................6

Limitations..............................................................................................................................................7

REVENUE RECOGNITION AND MEASUREMENT BASIS..................................................................7

QUALITATIVE CHARACTERISTICS.....................................................................................................8

SUSTAINABILITY AND INTEGRATED REPORTING..........................................................................8

SUSTAINABILITY REPORTING GUIDELINES.....................................................................................9

INTEGRATED REPORT............................................................................................................................9

Integrated framework..............................................................................................................................9

Purpose of integrated report...................................................................................................................10

DIFFERENCES BETWEEN SUSTAINABILITY REPORTING GUIDELINES AND

INTERNATIONAL INTEGRATED REPORTING COUNCIL...............................................................10

HOW HOLISTIC IS SUSTAINABILITY REPORTING AND INTEGRATED REPORTING?.............10

STRENGHTS AND LIMITATIONS........................................................................................................11

APPLICABILITY OF INTEGRATED REPORTING AND SUSTAINABILTY REPORTING

THEORIES................................................................................................................................................12

integrated reporting theories..................................................................................................................12

sustainability reporting theories.............................................................................................................12

LIMITATION OF THESE THEORIES....................................................................................................12

COMPONENTS OF AN INTEGRATED REPORT.................................................................................12

HOW IT IS SHOWN IN ECHO POLSKA PROPERTIES.......................................................................13

COMPARISON OF AUSTRALIAN COMPANY AND SOUTH AFRICAN COMPANY CSR

REPORTS.................................................................................................................................................14

CONCLUSION.........................................................................................................................................16

REFERENCES..........................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING 4

INTRODUCTION.

Conceptual framework is the coherent system of interrelated relationships that defines the roles

and the nature of the FASB.The evolution of the process in the US, UK, Australia and the globe

at large. The US is seen as the super economy in the globe and this was the first country to

develop a framework for recording and reporting financial information after which other

countries adopt the process.

CONCEPTUAL FRAMEWORK

It is defined as the consistent composing of objectives and ground laying notion that defines the

nature ,function and limitations of the FASB(Jackling, Raar, Wines & McDowall, 2010).The

development of the conceptual framework in the US is linked to two scholars Paton and

Littleton Monograph both of 1940.The framework was further expanded through a research

study done by Moonitz and Sprouse in the year 1962-1963.The two set up the basis for the

establishment of the Financial Accounting Standards Board.John B Canning in 1922 published a

book entitled Accounting Theory in which he identified the process of valuation of assets and the

concept of measurement that to him, it was based on the expected future and this today forms the

essential concepts that are applied in recording and reporting financial transactions. The earliest

body in the US to shed light on the way of financial transactions were recorded and reported was

Tentative Statement of Accounting Principles Affecting Corporate Reports that chiefly issued

directions to the newly established Securities and Exchange Commission. The report utilised the

use of historical cost accounting, concept of matching and revenue recognition concept in the

USA. In Australia the conceptual framework was set up by the Australian Accounting Research

Foundation in the yeas 1985-1995.The aim of the framework was to issue a combined

interrelated notion that highlights the nature ,need and an expanded content of the financial

reporting.IASC developed a framework use in the preparation and disclosure of financial

information by 1989.This directs the board the board in setting up the accounting standards that

could address accounting concerns that are mentioned clearly in an International Accounting

Standard/ Financial Reporting Standards .This framework;

Highlights financial statements objectives.

Elaborates qualitative characteristics making accounting information important.

INTRODUCTION.

Conceptual framework is the coherent system of interrelated relationships that defines the roles

and the nature of the FASB.The evolution of the process in the US, UK, Australia and the globe

at large. The US is seen as the super economy in the globe and this was the first country to

develop a framework for recording and reporting financial information after which other

countries adopt the process.

CONCEPTUAL FRAMEWORK

It is defined as the consistent composing of objectives and ground laying notion that defines the

nature ,function and limitations of the FASB(Jackling, Raar, Wines & McDowall, 2010).The

development of the conceptual framework in the US is linked to two scholars Paton and

Littleton Monograph both of 1940.The framework was further expanded through a research

study done by Moonitz and Sprouse in the year 1962-1963.The two set up the basis for the

establishment of the Financial Accounting Standards Board.John B Canning in 1922 published a

book entitled Accounting Theory in which he identified the process of valuation of assets and the

concept of measurement that to him, it was based on the expected future and this today forms the

essential concepts that are applied in recording and reporting financial transactions. The earliest

body in the US to shed light on the way of financial transactions were recorded and reported was

Tentative Statement of Accounting Principles Affecting Corporate Reports that chiefly issued

directions to the newly established Securities and Exchange Commission. The report utilised the

use of historical cost accounting, concept of matching and revenue recognition concept in the

USA. In Australia the conceptual framework was set up by the Australian Accounting Research

Foundation in the yeas 1985-1995.The aim of the framework was to issue a combined

interrelated notion that highlights the nature ,need and an expanded content of the financial

reporting.IASC developed a framework use in the preparation and disclosure of financial

information by 1989.This directs the board the board in setting up the accounting standards that

could address accounting concerns that are mentioned clearly in an International Accounting

Standard/ Financial Reporting Standards .This framework;

Highlights financial statements objectives.

Elaborates qualitative characteristics making accounting information important.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 5

ACCOUNTING PROFESSION CONCERN

Users of financial information are interested; to use them when making economic decisions

which encompasses decisions on whether to buy, evaluation of management and the involvement

of this in the national income statistics. Similarly, to assess the management stewardship only

attainable in a separate entity that is executed by an independent board of directors. Users of the

financial information includes; the shareholders who want to know whether their investments

will earn them dividends, the government is interested to make use of this in the national income

statistics to determine the living standards in the country, suppliers are interested in order to

know whether the company will meet its financial obligations when they supply goods and

services on credit .Employees need this to assess the security of their jobs and the management

for them to project the future outcomes in the business and to plan to face the consequences of

such. The IFRS regulating financial reporting standards comes with the following beneficial

effects;

lowers the differences in the preparation of financial statements.

safeguards investors interest in a listed company.

Advance the quality of accounting information produced.

IFRS aims at safeguarding interest of the public, promotion of top quality and globally

acceptable financial reporting standards and promotes sustainable application of the IFRS in

financial reporting.

BENEFITS AND LIMITATIONS OF CONCEPTUAL FRAMEWORK

The framework which is tasked with the duty of undertaking measures to ensure consistency is

uphold on the preparation of the financial statements. It further defines the scope of preparation

of financial statements.

benefits

Raises the interested party’s confidence and their thinking on financial reporting as the

variations in the accounting sector have been harmonized.

Establish a basis in which performance of accounting work is are tested in an objective

manner. This assists to put in place the standards from which financial statements

prepared adhere to.

ACCOUNTING PROFESSION CONCERN

Users of financial information are interested; to use them when making economic decisions

which encompasses decisions on whether to buy, evaluation of management and the involvement

of this in the national income statistics. Similarly, to assess the management stewardship only

attainable in a separate entity that is executed by an independent board of directors. Users of the

financial information includes; the shareholders who want to know whether their investments

will earn them dividends, the government is interested to make use of this in the national income

statistics to determine the living standards in the country, suppliers are interested in order to

know whether the company will meet its financial obligations when they supply goods and

services on credit .Employees need this to assess the security of their jobs and the management

for them to project the future outcomes in the business and to plan to face the consequences of

such. The IFRS regulating financial reporting standards comes with the following beneficial

effects;

lowers the differences in the preparation of financial statements.

safeguards investors interest in a listed company.

Advance the quality of accounting information produced.

IFRS aims at safeguarding interest of the public, promotion of top quality and globally

acceptable financial reporting standards and promotes sustainable application of the IFRS in

financial reporting.

BENEFITS AND LIMITATIONS OF CONCEPTUAL FRAMEWORK

The framework which is tasked with the duty of undertaking measures to ensure consistency is

uphold on the preparation of the financial statements. It further defines the scope of preparation

of financial statements.

benefits

Raises the interested party’s confidence and their thinking on financial reporting as the

variations in the accounting sector have been harmonized.

Establish a basis in which performance of accounting work is are tested in an objective

manner. This assists to put in place the standards from which financial statements

prepared adhere to.

ACCOUNTING 6

Promotes better relations between the accountants and the regulatory bodies This is made

possible as the accountants work should attain the minimum standards while the work of

the regulatory body is to make sure that the standards are achieved.

Improves the user’s reliability of the financial information as the users have a clear

validation that the financial statements have been prepared with due regard to the set and

has the minimum standards.

Limitations

Expensive to establish Conceptual framework is costly in terms of resources and time.

Developed countries only established this and will then imposes these policies on

developing countries which their financial and accounting standards are not in

commensuration with the set standards. The developing due to lack of resources adapts

the framework (Fidalgo,Sein & García, 2015).

Inflexibility of the framework, once the conceptual framework has been reached and set

up, it is difficult to be changed for it to incorporate new ideas that are deemed important

and not covered by the framework.

Disregard the interest of some parties; The framework only concerns matter that are

practical and relevant to specific parties. For instance, as largely as the framework is set

up by developed countries and imposed on developing countries whose standards are not

unison with those of developed countries (Weible & Schlager, 2014).

The framework can be challenge, in case of a conflict arising between the existing

standards and the one set out by the framework, the existing one overrides the framework

as the present is not much considered in accounting more than the past since accounting

is based on historical basis (Bes-Rastrollo et al. 2013).

REVENUE RECOGNITION AND MEASUREMENT BASIS

The core objective of financial statements is to provide information concerning the reporting

company relating to assets, liabilities, equity, income and expenses that are deemed to be crucial

by the interested to the entity's financial matters and applies this in determining the expected net

cash flow of the firm and determining the stewardship of the company economic resources. This

information in the balance sheet is shown by disclosing the assets, liabilities and equity values.

In the balance sheet of Peet limited company as at 30th June 2017, the total assets were 933,858

Promotes better relations between the accountants and the regulatory bodies This is made

possible as the accountants work should attain the minimum standards while the work of

the regulatory body is to make sure that the standards are achieved.

Improves the user’s reliability of the financial information as the users have a clear

validation that the financial statements have been prepared with due regard to the set and

has the minimum standards.

Limitations

Expensive to establish Conceptual framework is costly in terms of resources and time.

Developed countries only established this and will then imposes these policies on

developing countries which their financial and accounting standards are not in

commensuration with the set standards. The developing due to lack of resources adapts

the framework (Fidalgo,Sein & García, 2015).

Inflexibility of the framework, once the conceptual framework has been reached and set

up, it is difficult to be changed for it to incorporate new ideas that are deemed important

and not covered by the framework.

Disregard the interest of some parties; The framework only concerns matter that are

practical and relevant to specific parties. For instance, as largely as the framework is set

up by developed countries and imposed on developing countries whose standards are not

unison with those of developed countries (Weible & Schlager, 2014).

The framework can be challenge, in case of a conflict arising between the existing

standards and the one set out by the framework, the existing one overrides the framework

as the present is not much considered in accounting more than the past since accounting

is based on historical basis (Bes-Rastrollo et al. 2013).

REVENUE RECOGNITION AND MEASUREMENT BASIS

The core objective of financial statements is to provide information concerning the reporting

company relating to assets, liabilities, equity, income and expenses that are deemed to be crucial

by the interested to the entity's financial matters and applies this in determining the expected net

cash flow of the firm and determining the stewardship of the company economic resources. This

information in the balance sheet is shown by disclosing the assets, liabilities and equity values.

In the balance sheet of Peet limited company as at 30th June 2017, the total assets were 933,858

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING 7

Australian dollars’. The total liabilities amounted to 408,536 as at that date. The statement of

cash flow of the Peer Limited company shows that the net cash flow from operating activities

was 57,227, net cash flow from investing activities was 1488 and the cash flow from financing

activities amounted to 40745, all in Australian Dollars. The cash and cash equivalent increase is

14994 Australian Dollars. All this are as at 30th June 2017(Pg.39 Of the 2017 Annual Report). In

the statement of Equity of Peer Limited company as at 30th June 2017, the total balance is

disclosed at balance of 513,630 Australian Dollars (Pg.37 of the 2017 Annual Report). Peer

Limited company further discloses that interest is only recognisable when earned and computed

using an effective rate of interest. Dividends are recognized when the right to obtain payment has

been attained. Proceeds from the land sale is recognised after the sale has been serviced. When

the sales contract has been signed, the project management and selling fees are recognized. Other

trading activities are recognised only after the necessary services are executed (Pg.42 of the 2017

Annual Report). The Peer report also reveals that the total expenses as at 30th June 2017

amounted to 240,609 Australian Dollars The methods, assumptions and judgements used in

estimating the amount presented and the changes on them.

QUALITATIVE CHARACTERISTICS

Timeliness states that financial information should be available to users at suitable time for them

to make decisions. Peet Limited Company has its financial year ending at 30th June every

financial year and exhibits this by preparing its financial statements as at this date to enable the

users to make decisions on time (Choudhary, Merkley & Schipper, 2017).

Understandability the financial information should prepare simply and clearly. Peer limited

balance sheet statement, statement of Equity and the cash flow statements depicts this as they

have been prepared to suit the understanding interest of all the users.

SUSTAINABILITY AND INTEGRATED REPORTING.

Sustainability report is a document prepared by various companies concerning their impacts on

various sectors of the community due to their day to day operations. This impacts could be

caused on the environment, society or on the general economy. This report also shows the

entity’s values and governance issues relating to how they intend to preserve the economy in

general. Sustainability report therefore aids the company to gauge, appreciate and convey their

key plans relating to how they intend to manage economic activities, environment, societal and

Australian dollars’. The total liabilities amounted to 408,536 as at that date. The statement of

cash flow of the Peer Limited company shows that the net cash flow from operating activities

was 57,227, net cash flow from investing activities was 1488 and the cash flow from financing

activities amounted to 40745, all in Australian Dollars. The cash and cash equivalent increase is

14994 Australian Dollars. All this are as at 30th June 2017(Pg.39 Of the 2017 Annual Report). In

the statement of Equity of Peer Limited company as at 30th June 2017, the total balance is

disclosed at balance of 513,630 Australian Dollars (Pg.37 of the 2017 Annual Report). Peer

Limited company further discloses that interest is only recognisable when earned and computed

using an effective rate of interest. Dividends are recognized when the right to obtain payment has

been attained. Proceeds from the land sale is recognised after the sale has been serviced. When

the sales contract has been signed, the project management and selling fees are recognized. Other

trading activities are recognised only after the necessary services are executed (Pg.42 of the 2017

Annual Report). The Peer report also reveals that the total expenses as at 30th June 2017

amounted to 240,609 Australian Dollars The methods, assumptions and judgements used in

estimating the amount presented and the changes on them.

QUALITATIVE CHARACTERISTICS

Timeliness states that financial information should be available to users at suitable time for them

to make decisions. Peet Limited Company has its financial year ending at 30th June every

financial year and exhibits this by preparing its financial statements as at this date to enable the

users to make decisions on time (Choudhary, Merkley & Schipper, 2017).

Understandability the financial information should prepare simply and clearly. Peer limited

balance sheet statement, statement of Equity and the cash flow statements depicts this as they

have been prepared to suit the understanding interest of all the users.

SUSTAINABILITY AND INTEGRATED REPORTING.

Sustainability report is a document prepared by various companies concerning their impacts on

various sectors of the community due to their day to day operations. This impacts could be

caused on the environment, society or on the general economy. This report also shows the

entity’s values and governance issues relating to how they intend to preserve the economy in

general. Sustainability report therefore aids the company to gauge, appreciate and convey their

key plans relating to how they intend to manage economic activities, environment, societal and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 8

governance issues. This will aid this organization in developing sound objectives and in efficient

management of this change. This report act as a tool to convey sustainable presentation and

effects whether they are good or bad. Sustainability reporting is sometimes considered as

corporate social responsibility (Dienes, Sassen & Fischer, 2016).

SUSTAINABILITY REPORTING GUIDELINES

identify its intended users and explain the way it has addressed the needs and interests of

those groups.

It should show how the entity has performed in its sustainable program

It should show how economic aspect, environment and societal aspect has been impacted

on

It must depict on completeness, that is, cover all performance of entity in terms of

economic, social and environmental.

Integrated reporting blends both financial aspect of the entity and the non-financial aspect

in terms of

entities performance.

INTEGRATED REPORT

It is a specific document that convey entity’s strategies, governance and achievement prospects

to the outside context leading to the creation of company’s value in the short, medium and long

term (Eccles & Krzus, 2010).

Integrated framework

the role of this is to set guides to be followed and items that must be included in the integrated

report and discuss various concepts that are used.

contains;

Relevant information to be included in the framework to be utilized in the assessment of

company’s ability to generate value

Show situation when such value is maintained or not.

Shows relationship of such value over time

governance issues. This will aid this organization in developing sound objectives and in efficient

management of this change. This report act as a tool to convey sustainable presentation and

effects whether they are good or bad. Sustainability reporting is sometimes considered as

corporate social responsibility (Dienes, Sassen & Fischer, 2016).

SUSTAINABILITY REPORTING GUIDELINES

identify its intended users and explain the way it has addressed the needs and interests of

those groups.

It should show how the entity has performed in its sustainable program

It should show how economic aspect, environment and societal aspect has been impacted

on

It must depict on completeness, that is, cover all performance of entity in terms of

economic, social and environmental.

Integrated reporting blends both financial aspect of the entity and the non-financial aspect

in terms of

entities performance.

INTEGRATED REPORT

It is a specific document that convey entity’s strategies, governance and achievement prospects

to the outside context leading to the creation of company’s value in the short, medium and long

term (Eccles & Krzus, 2010).

Integrated framework

the role of this is to set guides to be followed and items that must be included in the integrated

report and discuss various concepts that are used.

contains;

Relevant information to be included in the framework to be utilized in the assessment of

company’s ability to generate value

Show situation when such value is maintained or not.

Shows relationship of such value over time

ACCOUNTING 9

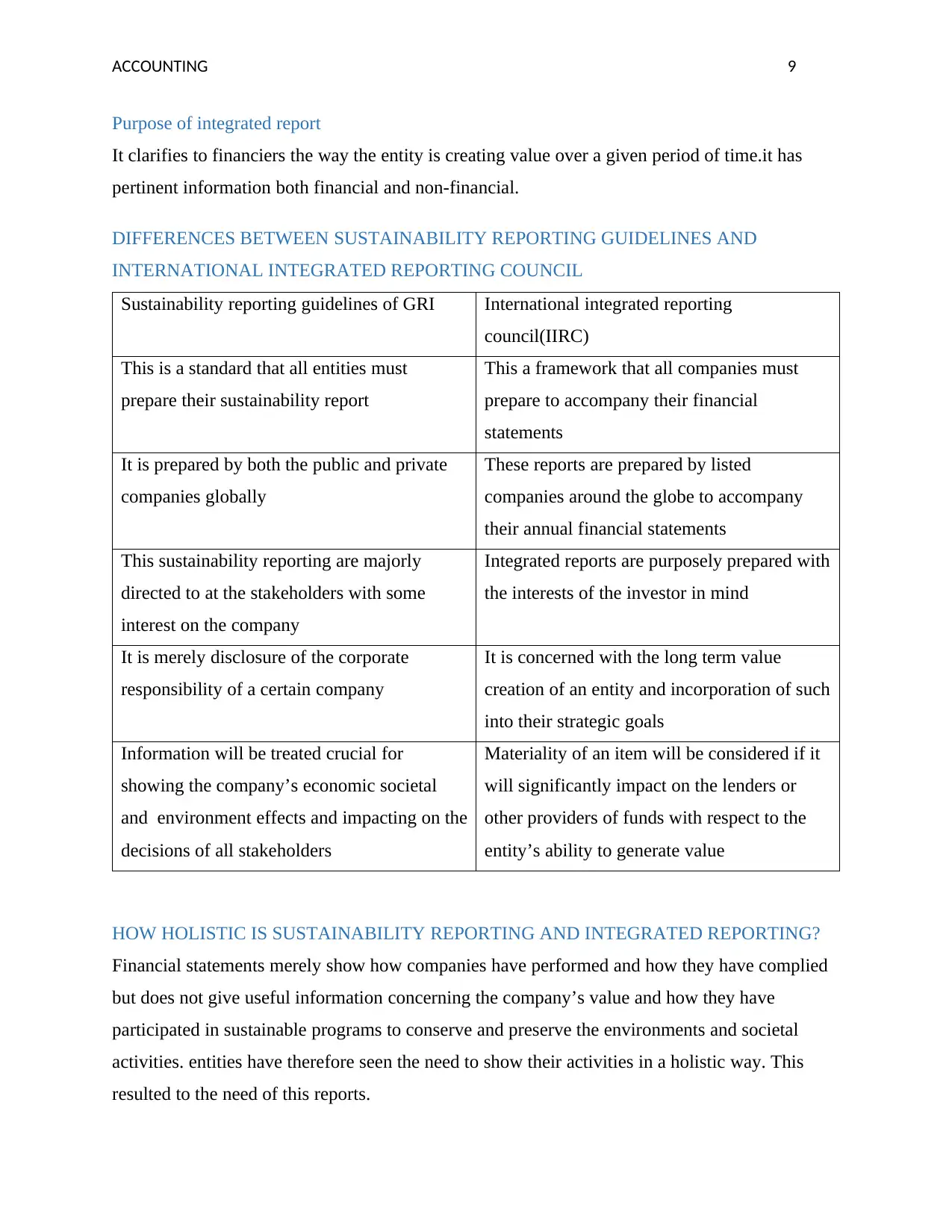

Purpose of integrated report

It clarifies to financiers the way the entity is creating value over a given period of time.it has

pertinent information both financial and non-financial.

DIFFERENCES BETWEEN SUSTAINABILITY REPORTING GUIDELINES AND

INTERNATIONAL INTEGRATED REPORTING COUNCIL

Sustainability reporting guidelines of GRI International integrated reporting

council(IIRC)

This is a standard that all entities must

prepare their sustainability report

This a framework that all companies must

prepare to accompany their financial

statements

It is prepared by both the public and private

companies globally

These reports are prepared by listed

companies around the globe to accompany

their annual financial statements

This sustainability reporting are majorly

directed to at the stakeholders with some

interest on the company

Integrated reports are purposely prepared with

the interests of the investor in mind

It is merely disclosure of the corporate

responsibility of a certain company

It is concerned with the long term value

creation of an entity and incorporation of such

into their strategic goals

Information will be treated crucial for

showing the company’s economic societal

and environment effects and impacting on the

decisions of all stakeholders

Materiality of an item will be considered if it

will significantly impact on the lenders or

other providers of funds with respect to the

entity’s ability to generate value

HOW HOLISTIC IS SUSTAINABILITY REPORTING AND INTEGRATED REPORTING?

Financial statements merely show how companies have performed and how they have complied

but does not give useful information concerning the company’s value and how they have

participated in sustainable programs to conserve and preserve the environments and societal

activities. entities have therefore seen the need to show their activities in a holistic way. This

resulted to the need of this reports.

Purpose of integrated report

It clarifies to financiers the way the entity is creating value over a given period of time.it has

pertinent information both financial and non-financial.

DIFFERENCES BETWEEN SUSTAINABILITY REPORTING GUIDELINES AND

INTERNATIONAL INTEGRATED REPORTING COUNCIL

Sustainability reporting guidelines of GRI International integrated reporting

council(IIRC)

This is a standard that all entities must

prepare their sustainability report

This a framework that all companies must

prepare to accompany their financial

statements

It is prepared by both the public and private

companies globally

These reports are prepared by listed

companies around the globe to accompany

their annual financial statements

This sustainability reporting are majorly

directed to at the stakeholders with some

interest on the company

Integrated reports are purposely prepared with

the interests of the investor in mind

It is merely disclosure of the corporate

responsibility of a certain company

It is concerned with the long term value

creation of an entity and incorporation of such

into their strategic goals

Information will be treated crucial for

showing the company’s economic societal

and environment effects and impacting on the

decisions of all stakeholders

Materiality of an item will be considered if it

will significantly impact on the lenders or

other providers of funds with respect to the

entity’s ability to generate value

HOW HOLISTIC IS SUSTAINABILITY REPORTING AND INTEGRATED REPORTING?

Financial statements merely show how companies have performed and how they have complied

but does not give useful information concerning the company’s value and how they have

participated in sustainable programs to conserve and preserve the environments and societal

activities. entities have therefore seen the need to show their activities in a holistic way. This

resulted to the need of this reports.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING 10

Integrated framework ensures presentation of various moves, discuss various capitals utilized

and show the view of the company in a long term basis

Sustainability guidelines show various elements that must be covered in reporting on the

corporate performance of an entity like materiality, completeness and others.

Integrated framework enables entities prepare its own document instead of using checklist

method. This will enable them adapt to changes thus reporting on their value more effectively.

According to the framework, entities will discuss various elements that drives their value and

include only information that is relevant to the user’s needs.

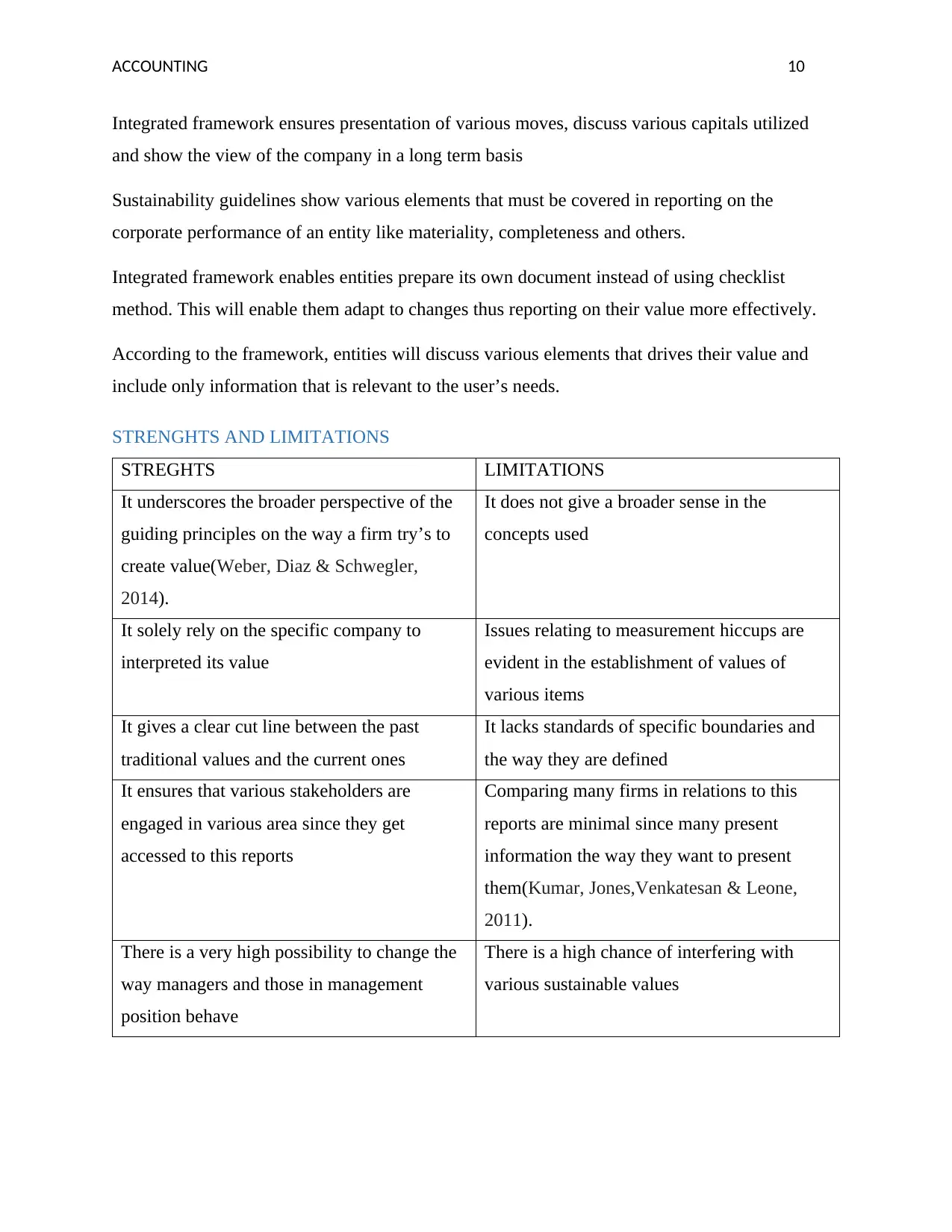

STRENGHTS AND LIMITATIONS

STREGHTS LIMITATIONS

It underscores the broader perspective of the

guiding principles on the way a firm try’s to

create value(Weber, Diaz & Schwegler,

2014).

It does not give a broader sense in the

concepts used

It solely rely on the specific company to

interpreted its value

Issues relating to measurement hiccups are

evident in the establishment of values of

various items

It gives a clear cut line between the past

traditional values and the current ones

It lacks standards of specific boundaries and

the way they are defined

It ensures that various stakeholders are

engaged in various area since they get

accessed to this reports

Comparing many firms in relations to this

reports are minimal since many present

information the way they want to present

them(Kumar, Jones,Venkatesan & Leone,

2011).

There is a very high possibility to change the

way managers and those in management

position behave

There is a high chance of interfering with

various sustainable values

Integrated framework ensures presentation of various moves, discuss various capitals utilized

and show the view of the company in a long term basis

Sustainability guidelines show various elements that must be covered in reporting on the

corporate performance of an entity like materiality, completeness and others.

Integrated framework enables entities prepare its own document instead of using checklist

method. This will enable them adapt to changes thus reporting on their value more effectively.

According to the framework, entities will discuss various elements that drives their value and

include only information that is relevant to the user’s needs.

STRENGHTS AND LIMITATIONS

STREGHTS LIMITATIONS

It underscores the broader perspective of the

guiding principles on the way a firm try’s to

create value(Weber, Diaz & Schwegler,

2014).

It does not give a broader sense in the

concepts used

It solely rely on the specific company to

interpreted its value

Issues relating to measurement hiccups are

evident in the establishment of values of

various items

It gives a clear cut line between the past

traditional values and the current ones

It lacks standards of specific boundaries and

the way they are defined

It ensures that various stakeholders are

engaged in various area since they get

accessed to this reports

Comparing many firms in relations to this

reports are minimal since many present

information the way they want to present

them(Kumar, Jones,Venkatesan & Leone,

2011).

There is a very high possibility to change the

way managers and those in management

position behave

There is a high chance of interfering with

various sustainable values

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 11

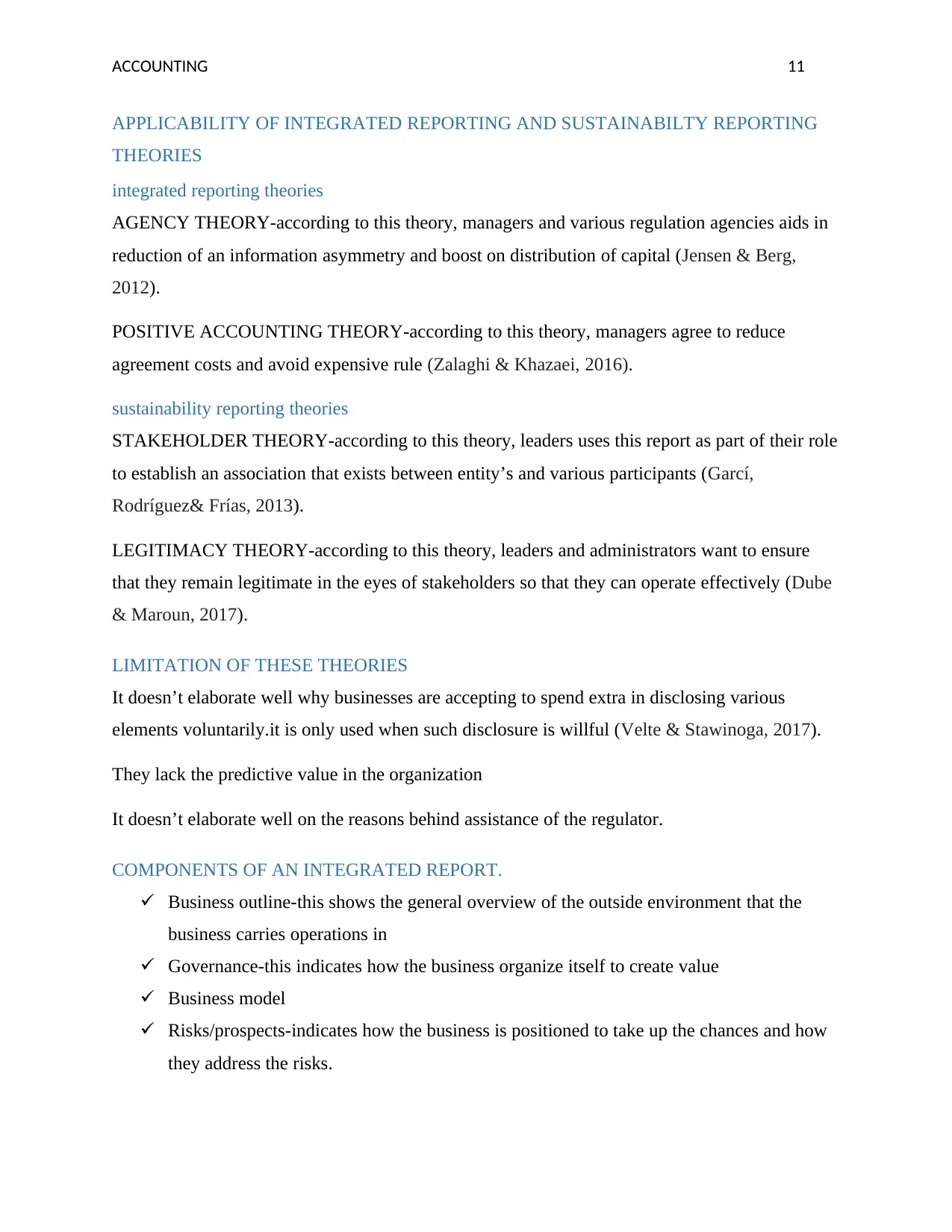

APPLICABILITY OF INTEGRATED REPORTING AND SUSTAINABILTY REPORTING

THEORIES

integrated reporting theories

AGENCY THEORY-according to this theory, managers and various regulation agencies aids in

reduction of an information asymmetry and boost on distribution of capital (Jensen & Berg,

2012).

POSITIVE ACCOUNTING THEORY-according to this theory, managers agree to reduce

agreement costs and avoid expensive rule (Zalaghi & Khazaei, 2016).

sustainability reporting theories

STAKEHOLDER THEORY-according to this theory, leaders uses this report as part of their role

to establish an association that exists between entity’s and various participants (Garcí,

Rodríguez& Frías, 2013).

LEGITIMACY THEORY-according to this theory, leaders and administrators want to ensure

that they remain legitimate in the eyes of stakeholders so that they can operate effectively (Dube

& Maroun, 2017).

LIMITATION OF THESE THEORIES

It doesn’t elaborate well why businesses are accepting to spend extra in disclosing various

elements voluntarily.it is only used when such disclosure is willful (Velte & Stawinoga, 2017).

They lack the predictive value in the organization

It doesn’t elaborate well on the reasons behind assistance of the regulator.

COMPONENTS OF AN INTEGRATED REPORT.

Business outline-this shows the general overview of the outside environment that the

business carries operations in

Governance-this indicates how the business organize itself to create value

Business model

Risks/prospects-indicates how the business is positioned to take up the chances and how

they address the risks.

APPLICABILITY OF INTEGRATED REPORTING AND SUSTAINABILTY REPORTING

THEORIES

integrated reporting theories

AGENCY THEORY-according to this theory, managers and various regulation agencies aids in

reduction of an information asymmetry and boost on distribution of capital (Jensen & Berg,

2012).

POSITIVE ACCOUNTING THEORY-according to this theory, managers agree to reduce

agreement costs and avoid expensive rule (Zalaghi & Khazaei, 2016).

sustainability reporting theories

STAKEHOLDER THEORY-according to this theory, leaders uses this report as part of their role

to establish an association that exists between entity’s and various participants (Garcí,

Rodríguez& Frías, 2013).

LEGITIMACY THEORY-according to this theory, leaders and administrators want to ensure

that they remain legitimate in the eyes of stakeholders so that they can operate effectively (Dube

& Maroun, 2017).

LIMITATION OF THESE THEORIES

It doesn’t elaborate well why businesses are accepting to spend extra in disclosing various

elements voluntarily.it is only used when such disclosure is willful (Velte & Stawinoga, 2017).

They lack the predictive value in the organization

It doesn’t elaborate well on the reasons behind assistance of the regulator.

COMPONENTS OF AN INTEGRATED REPORT.

Business outline-this shows the general overview of the outside environment that the

business carries operations in

Governance-this indicates how the business organize itself to create value

Business model

Risks/prospects-indicates how the business is positioned to take up the chances and how

they address the risks.

ACCOUNTING 12

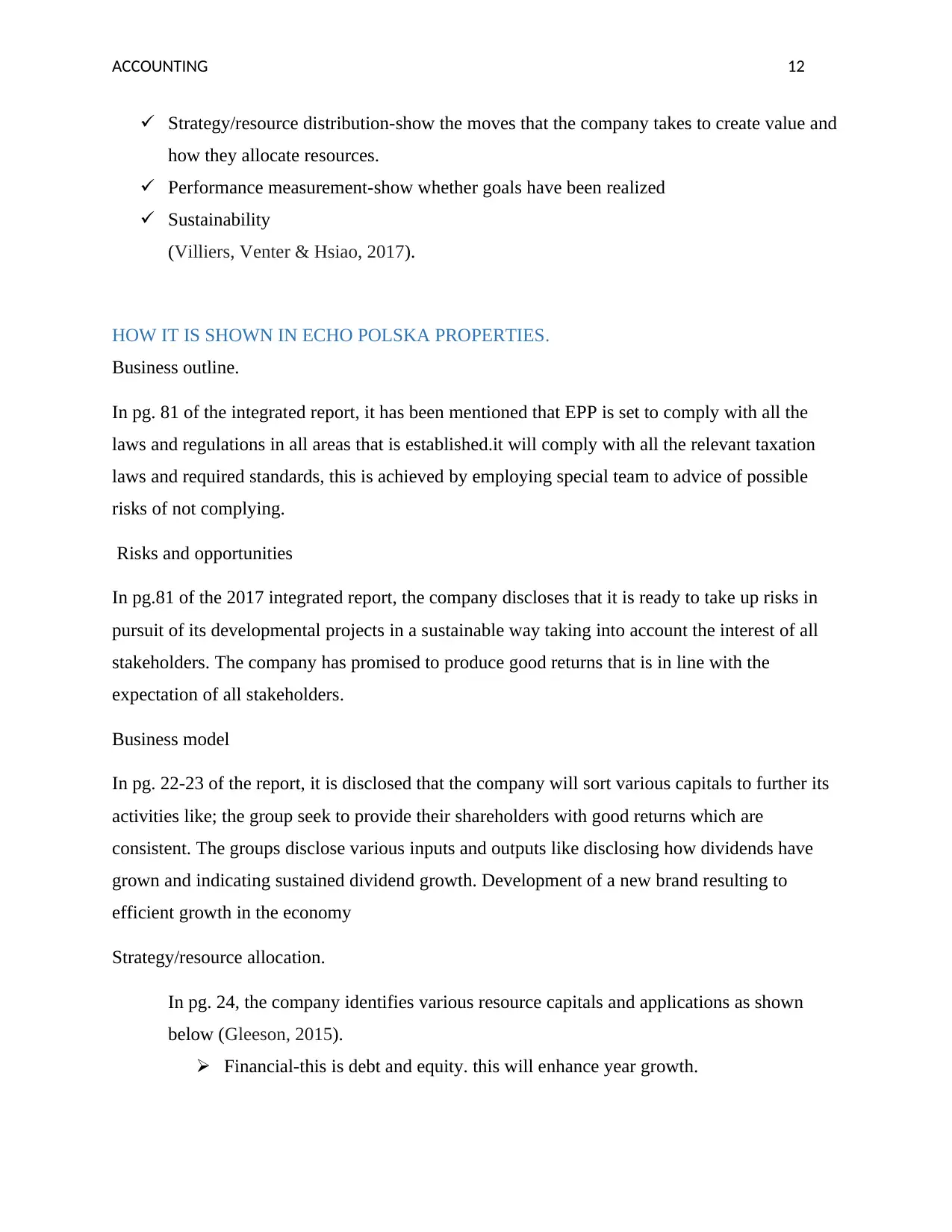

Strategy/resource distribution-show the moves that the company takes to create value and

how they allocate resources.

Performance measurement-show whether goals have been realized

Sustainability

(Villiers, Venter & Hsiao, 2017).

HOW IT IS SHOWN IN ECHO POLSKA PROPERTIES.

Business outline.

In pg. 81 of the integrated report, it has been mentioned that EPP is set to comply with all the

laws and regulations in all areas that is established.it will comply with all the relevant taxation

laws and required standards, this is achieved by employing special team to advice of possible

risks of not complying.

Risks and opportunities

In pg.81 of the 2017 integrated report, the company discloses that it is ready to take up risks in

pursuit of its developmental projects in a sustainable way taking into account the interest of all

stakeholders. The company has promised to produce good returns that is in line with the

expectation of all stakeholders.

Business model

In pg. 22-23 of the report, it is disclosed that the company will sort various capitals to further its

activities like; the group seek to provide their shareholders with good returns which are

consistent. The groups disclose various inputs and outputs like disclosing how dividends have

grown and indicating sustained dividend growth. Development of a new brand resulting to

efficient growth in the economy

Strategy/resource allocation.

In pg. 24, the company identifies various resource capitals and applications as shown

below (Gleeson, 2015).

Financial-this is debt and equity. this will enhance year growth.

Strategy/resource distribution-show the moves that the company takes to create value and

how they allocate resources.

Performance measurement-show whether goals have been realized

Sustainability

(Villiers, Venter & Hsiao, 2017).

HOW IT IS SHOWN IN ECHO POLSKA PROPERTIES.

Business outline.

In pg. 81 of the integrated report, it has been mentioned that EPP is set to comply with all the

laws and regulations in all areas that is established.it will comply with all the relevant taxation

laws and required standards, this is achieved by employing special team to advice of possible

risks of not complying.

Risks and opportunities

In pg.81 of the 2017 integrated report, the company discloses that it is ready to take up risks in

pursuit of its developmental projects in a sustainable way taking into account the interest of all

stakeholders. The company has promised to produce good returns that is in line with the

expectation of all stakeholders.

Business model

In pg. 22-23 of the report, it is disclosed that the company will sort various capitals to further its

activities like; the group seek to provide their shareholders with good returns which are

consistent. The groups disclose various inputs and outputs like disclosing how dividends have

grown and indicating sustained dividend growth. Development of a new brand resulting to

efficient growth in the economy

Strategy/resource allocation.

In pg. 24, the company identifies various resource capitals and applications as shown

below (Gleeson, 2015).

Financial-this is debt and equity. this will enhance year growth.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.