Accounting Assignment: ST Energy Ltd - Financial Analysis

VerifiedAdded on 2022/11/18

|22

|2554

|91

Homework Assignment

AI Summary

This document presents a comprehensive solution to an accounting assignment, addressing various financial reporting and accounting principles. The assignment delves into fair value measurement, adhering to NZ IFRS 13, and analyzes different scenarios to determine fair value based on market conditions and participant usage. It covers the revaluation of assets using the gross method and examines the accounting treatment of damaged equipment, including journal entries. Furthermore, the solution explores intangible assets, specifically patents, and their amortization, alongside the accounting for research and development projects. The assignment also includes detailed calculations of taxable profit, tax payable, and deferred tax, with corresponding journal entries, as well as the classification of financial instruments. Finally, it provides calculations related to loan repayment schedules.

Running head: ACCOUNTING

Accounting

Name of the student

Name of the university

Student ID

Author note

Accounting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING

Table of Contents

Question 1........................................................................................................................................2

Fair Value Measurement..............................................................................................................2

Revaluation using gross method..................................................................................................3

Damaged Equipment....................................................................................................................4

Intangible Assets..........................................................................................................................7

Usage of patents in the manufacturing process............................................................................7

Research and development project..............................................................................................7

Question 2........................................................................................................................................9

Answer (a)....................................................................................................................................9

Answer (b)....................................................................................................................................9

Answer (c)..................................................................................................................................11

Answer (d)..................................................................................................................................12

Question 3......................................................................................................................................14

Answer (a)..................................................................................................................................14

Answer (b)..................................................................................................................................14

References..................................................................................................................................17

ACCOUNTING

Table of Contents

Question 1........................................................................................................................................2

Fair Value Measurement..............................................................................................................2

Revaluation using gross method..................................................................................................3

Damaged Equipment....................................................................................................................4

Intangible Assets..........................................................................................................................7

Usage of patents in the manufacturing process............................................................................7

Research and development project..............................................................................................7

Question 2........................................................................................................................................9

Answer (a)....................................................................................................................................9

Answer (b)....................................................................................................................................9

Answer (c)..................................................................................................................................11

Answer (d)..................................................................................................................................12

Question 3......................................................................................................................................14

Answer (a)..................................................................................................................................14

Answer (b)..................................................................................................................................14

References..................................................................................................................................17

2

ACCOUNTING

Question 1

Fair Value Measurement

1. Paragraph 16 of NZ IFRS 13 suggests a transaction always takes place primarily in the

principal market and only in the case of absence of a principal market, it takes place in the

most advantageous market. Paragraphs 25 and 26 of NZ IFRS 13 suggest that the fair

value amount shall not be adjusted for transaction costs. This is because transaction costs

are not a characteristic of the asset or the liability (Dvořáková, 2013). Transportation costs

are allowed as a deduction. A company cannot choose to measure a product in the value of

an advantageous market when there is a principal market. In scenario 1, the amount that is

to be considered as fair value is the price prevailing in the principal market, i.e. Market A.

Hence the fair value of the asset in the given scenario is $158440 ($160000-$1560). In

scenario 2, the price that is to be considered is the price prevailing in the most

advantageous market. Therefore, in scenario 2, the fair value of the asset is to be measured

at $236800 ($240000-$3200). Hence, it is considered the most advantageous market

(Xrb.govt.nz, 2019).

2. According to paragraph 27 of NZ IFRS 13, fair value measurement of a non-financial

asset considers a market participant’s ability to provide economic outflows by using the

asset in its best and highest possible manner (Barker & Schulte 2017). Otherwise, it

considers the amount that can be generated by selling it to a participant in another market

who would put the asset to its highest and best use. Hence, it is quite evident that we

should consider the market participant’s likely usage of the particular asset.

3. As per paragraph 61 of IFRS 13, an entity should use valuation techniques that are

appropriate for a circumstance and for which necessary data is available to measure the

fair value, which is maximising the amount of observable inputs and reducing the

unobservable inputs. The three most commonly used methods of valuation are the cost

approach, market approach and the income approach. In the given circumstances, a single

technique from any of the above mentioned three techniques cannot be used to measure

the fair value of the asset. A combination of techniques which best measures the fair value

of the asset according to the market conditions is to be used. Techniques like calibration

are to be used to determine the necessary adjustments to be made to the valuation

ACCOUNTING

Question 1

Fair Value Measurement

1. Paragraph 16 of NZ IFRS 13 suggests a transaction always takes place primarily in the

principal market and only in the case of absence of a principal market, it takes place in the

most advantageous market. Paragraphs 25 and 26 of NZ IFRS 13 suggest that the fair

value amount shall not be adjusted for transaction costs. This is because transaction costs

are not a characteristic of the asset or the liability (Dvořáková, 2013). Transportation costs

are allowed as a deduction. A company cannot choose to measure a product in the value of

an advantageous market when there is a principal market. In scenario 1, the amount that is

to be considered as fair value is the price prevailing in the principal market, i.e. Market A.

Hence the fair value of the asset in the given scenario is $158440 ($160000-$1560). In

scenario 2, the price that is to be considered is the price prevailing in the most

advantageous market. Therefore, in scenario 2, the fair value of the asset is to be measured

at $236800 ($240000-$3200). Hence, it is considered the most advantageous market

(Xrb.govt.nz, 2019).

2. According to paragraph 27 of NZ IFRS 13, fair value measurement of a non-financial

asset considers a market participant’s ability to provide economic outflows by using the

asset in its best and highest possible manner (Barker & Schulte 2017). Otherwise, it

considers the amount that can be generated by selling it to a participant in another market

who would put the asset to its highest and best use. Hence, it is quite evident that we

should consider the market participant’s likely usage of the particular asset.

3. As per paragraph 61 of IFRS 13, an entity should use valuation techniques that are

appropriate for a circumstance and for which necessary data is available to measure the

fair value, which is maximising the amount of observable inputs and reducing the

unobservable inputs. The three most commonly used methods of valuation are the cost

approach, market approach and the income approach. In the given circumstances, a single

technique from any of the above mentioned three techniques cannot be used to measure

the fair value of the asset. A combination of techniques which best measures the fair value

of the asset according to the market conditions is to be used. Techniques like calibration

are to be used to determine the necessary adjustments to be made to the valuation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING

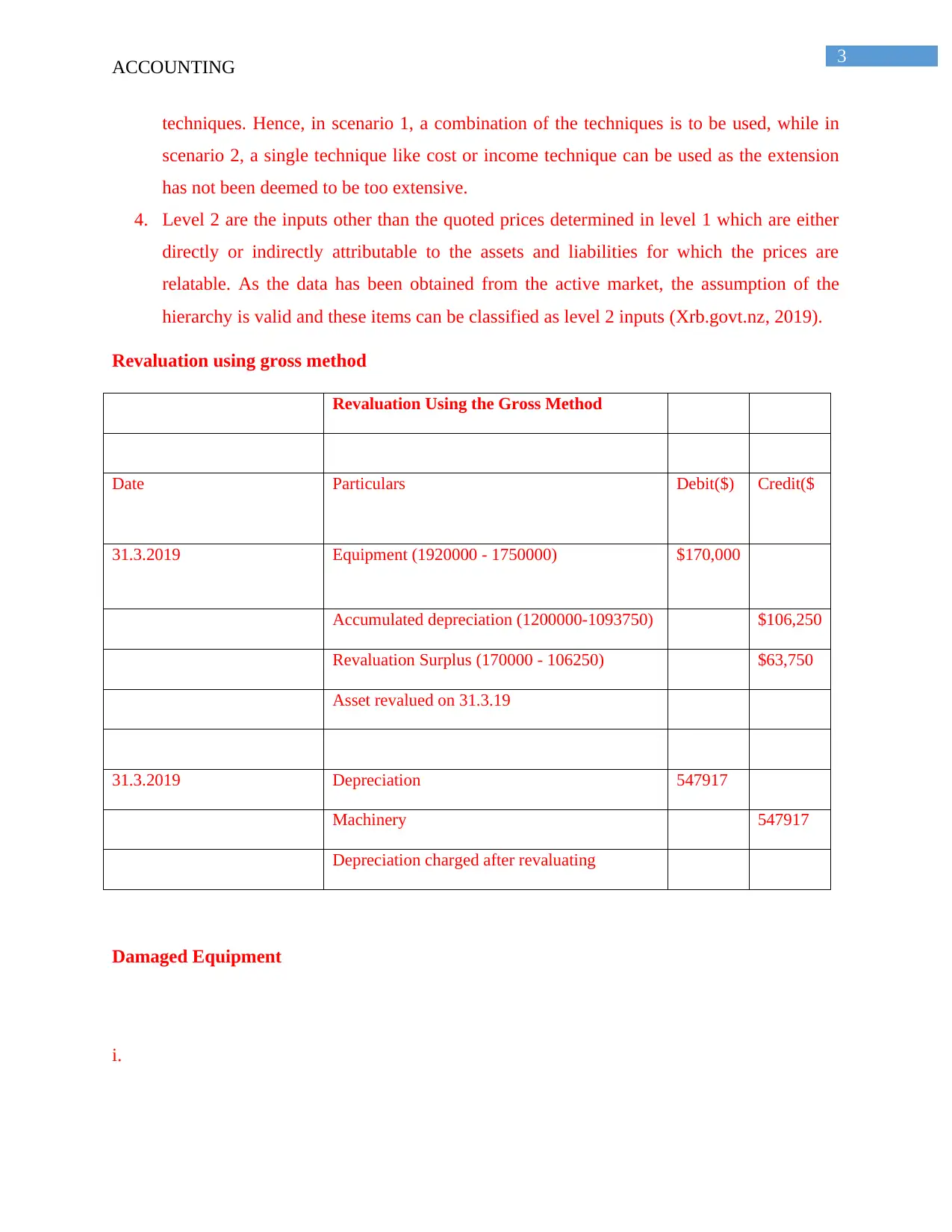

techniques. Hence, in scenario 1, a combination of the techniques is to be used, while in

scenario 2, a single technique like cost or income technique can be used as the extension

has not been deemed to be too extensive.

4. Level 2 are the inputs other than the quoted prices determined in level 1 which are either

directly or indirectly attributable to the assets and liabilities for which the prices are

relatable. As the data has been obtained from the active market, the assumption of the

hierarchy is valid and these items can be classified as level 2 inputs (Xrb.govt.nz, 2019).

Revaluation using gross method

Revaluation Using the Gross Method

Date Particulars Debit($) Credit($

31.3.2019 Equipment (1920000 - 1750000) $170,000

Accumulated depreciation (1200000-1093750) $106,250

Revaluation Surplus (170000 - 106250) $63,750

Asset revalued on 31.3.19

31.3.2019 Depreciation 547917

Machinery 547917

Depreciation charged after revaluating

Damaged Equipment

i.

ACCOUNTING

techniques. Hence, in scenario 1, a combination of the techniques is to be used, while in

scenario 2, a single technique like cost or income technique can be used as the extension

has not been deemed to be too extensive.

4. Level 2 are the inputs other than the quoted prices determined in level 1 which are either

directly or indirectly attributable to the assets and liabilities for which the prices are

relatable. As the data has been obtained from the active market, the assumption of the

hierarchy is valid and these items can be classified as level 2 inputs (Xrb.govt.nz, 2019).

Revaluation using gross method

Revaluation Using the Gross Method

Date Particulars Debit($) Credit($

31.3.2019 Equipment (1920000 - 1750000) $170,000

Accumulated depreciation (1200000-1093750) $106,250

Revaluation Surplus (170000 - 106250) $63,750

Asset revalued on 31.3.19

31.3.2019 Depreciation 547917

Machinery 547917

Depreciation charged after revaluating

Damaged Equipment

i.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING

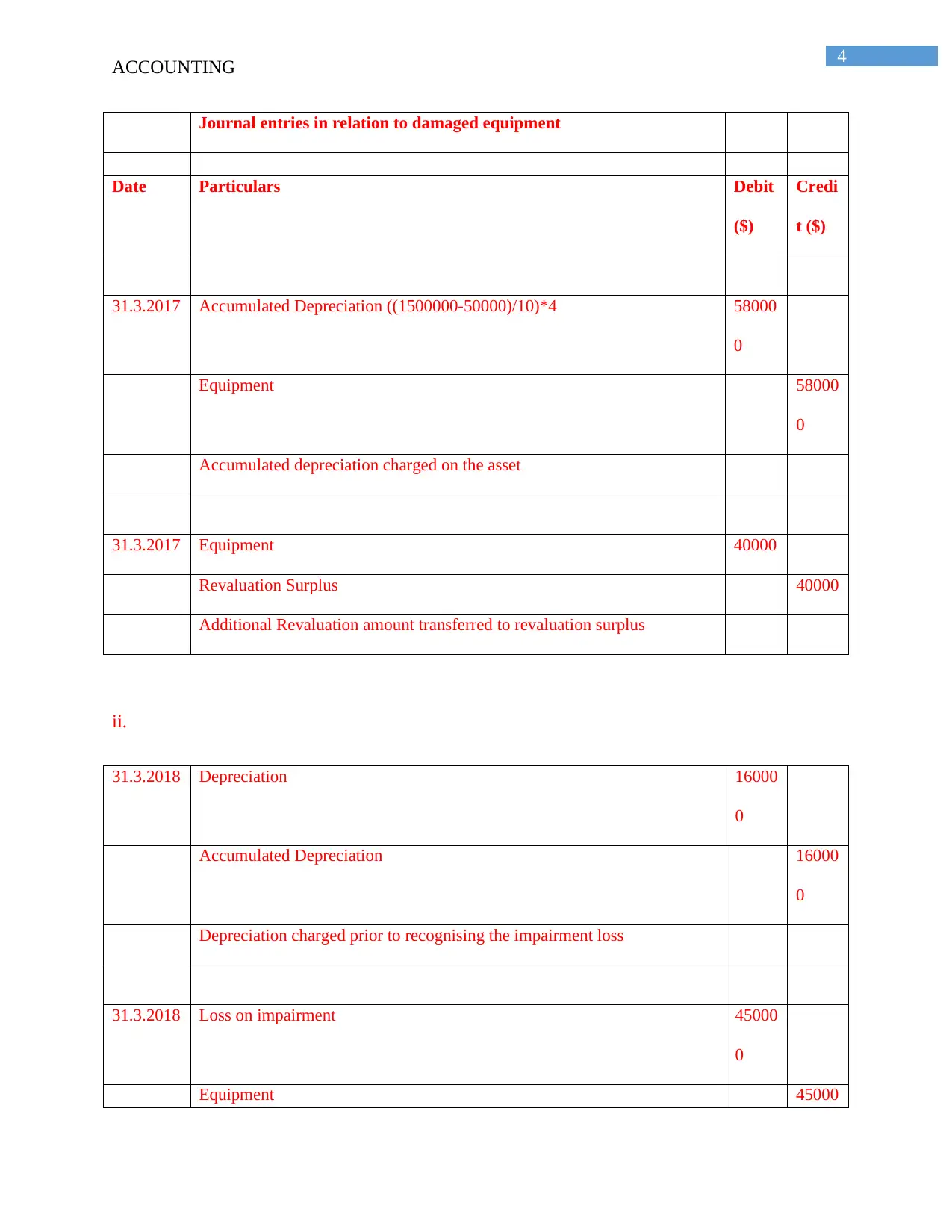

Journal entries in relation to damaged equipment

Date Particulars Debit

($)

Credi

t ($)

31.3.2017 Accumulated Depreciation ((1500000-50000)/10)*4 58000

0

Equipment 58000

0

Accumulated depreciation charged on the asset

31.3.2017 Equipment 40000

Revaluation Surplus 40000

Additional Revaluation amount transferred to revaluation surplus

ii.

31.3.2018 Depreciation 16000

0

Accumulated Depreciation 16000

0

Depreciation charged prior to recognising the impairment loss

31.3.2018 Loss on impairment 45000

0

Equipment 45000

ACCOUNTING

Journal entries in relation to damaged equipment

Date Particulars Debit

($)

Credi

t ($)

31.3.2017 Accumulated Depreciation ((1500000-50000)/10)*4 58000

0

Equipment 58000

0

Accumulated depreciation charged on the asset

31.3.2017 Equipment 40000

Revaluation Surplus 40000

Additional Revaluation amount transferred to revaluation surplus

ii.

31.3.2018 Depreciation 16000

0

Accumulated Depreciation 16000

0

Depreciation charged prior to recognising the impairment loss

31.3.2018 Loss on impairment 45000

0

Equipment 45000

5

ACCOUNTING

0

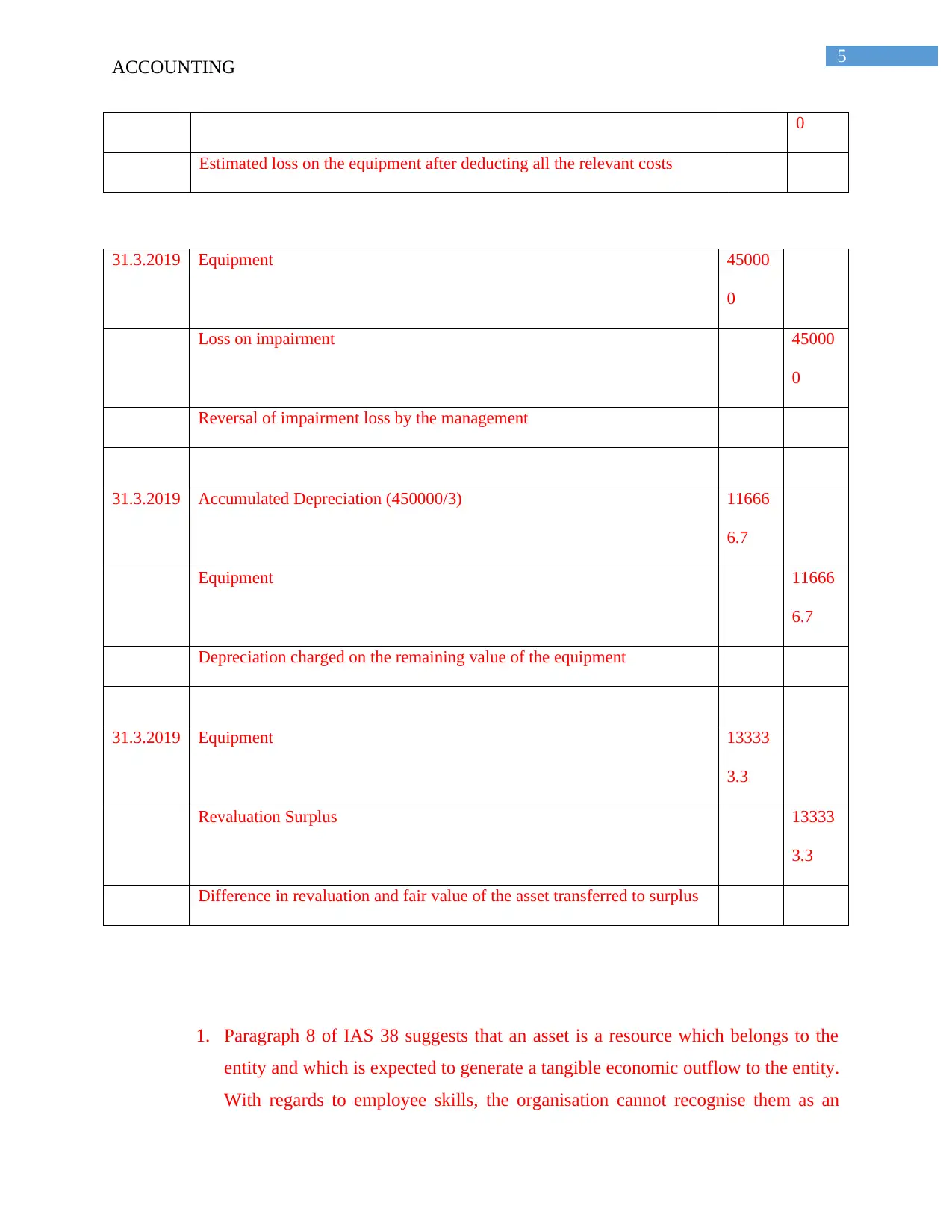

Estimated loss on the equipment after deducting all the relevant costs

31.3.2019 Equipment 45000

0

Loss on impairment 45000

0

Reversal of impairment loss by the management

31.3.2019 Accumulated Depreciation (450000/3) 11666

6.7

Equipment 11666

6.7

Depreciation charged on the remaining value of the equipment

31.3.2019 Equipment 13333

3.3

Revaluation Surplus 13333

3.3

Difference in revaluation and fair value of the asset transferred to surplus

1. Paragraph 8 of IAS 38 suggests that an asset is a resource which belongs to the

entity and which is expected to generate a tangible economic outflow to the entity.

With regards to employee skills, the organisation cannot recognise them as an

ACCOUNTING

0

Estimated loss on the equipment after deducting all the relevant costs

31.3.2019 Equipment 45000

0

Loss on impairment 45000

0

Reversal of impairment loss by the management

31.3.2019 Accumulated Depreciation (450000/3) 11666

6.7

Equipment 11666

6.7

Depreciation charged on the remaining value of the equipment

31.3.2019 Equipment 13333

3.3

Revaluation Surplus 13333

3.3

Difference in revaluation and fair value of the asset transferred to surplus

1. Paragraph 8 of IAS 38 suggests that an asset is a resource which belongs to the

entity and which is expected to generate a tangible economic outflow to the entity.

With regards to employee skills, the organisation cannot recognise them as an

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING

intangible asset due to its lack of control over the usage of the skills of the

employees and the economic benefits that can be obtained from them. Hence, as

per the paragraph 15 of IAS 38, the entity cannot recognise the skills as an

intangible asset unless it has a legal protection which allows it to use these skills

as an asset and measure the economic benefits obtained by it. This is the same

case with regards to customer loyalty, which cannot be recognised until it is

measurable or protected by a legal obligation.

2. Paragraph 75 of IAS 38 suggests that an intangible asset may be carried on a

revalued amount i.e. all amortisation expenses and losses deducted from the fair

value of an asset. This can be done only if the fair value of the intangible asset can

be arrived at by referring to an active and reliable market. Although it is very

uncommon for intangible assets, it is done in case of assets like tax licenses,

fishing licenses and quotas.

Usage of patents in the manufacturing process

As per paragraph 97 of IAS 38, the depreciable amount of an intangible asset with a

limited life shall be allocated on a systematic basis over the useful period of the life of the asset.

However, with regards to paragraph 104 of IAS 38, the amortisation period and the amortisation

method for each asset should be reviewed at the end of every financial year. In case of a change

in the useful life of the asset or an estimate of the economic assets that can be generated from an

asset, then the amortisation method should be changed to reflect a change in the estimates.

Hence, scenario 2 is correct and the company should change the amortisation method to reflect

the changes in the economic benefits that can be obtained from the patents.

Calculation of amortisation expense as on 31.3.2019

ACCOUNTING

intangible asset due to its lack of control over the usage of the skills of the

employees and the economic benefits that can be obtained from them. Hence, as

per the paragraph 15 of IAS 38, the entity cannot recognise the skills as an

intangible asset unless it has a legal protection which allows it to use these skills

as an asset and measure the economic benefits obtained by it. This is the same

case with regards to customer loyalty, which cannot be recognised until it is

measurable or protected by a legal obligation.

2. Paragraph 75 of IAS 38 suggests that an intangible asset may be carried on a

revalued amount i.e. all amortisation expenses and losses deducted from the fair

value of an asset. This can be done only if the fair value of the intangible asset can

be arrived at by referring to an active and reliable market. Although it is very

uncommon for intangible assets, it is done in case of assets like tax licenses,

fishing licenses and quotas.

Usage of patents in the manufacturing process

As per paragraph 97 of IAS 38, the depreciable amount of an intangible asset with a

limited life shall be allocated on a systematic basis over the useful period of the life of the asset.

However, with regards to paragraph 104 of IAS 38, the amortisation period and the amortisation

method for each asset should be reviewed at the end of every financial year. In case of a change

in the useful life of the asset or an estimate of the economic assets that can be generated from an

asset, then the amortisation method should be changed to reflect a change in the estimates.

Hence, scenario 2 is correct and the company should change the amortisation method to reflect

the changes in the economic benefits that can be obtained from the patents.

Calculation of amortisation expense as on 31.3.2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING

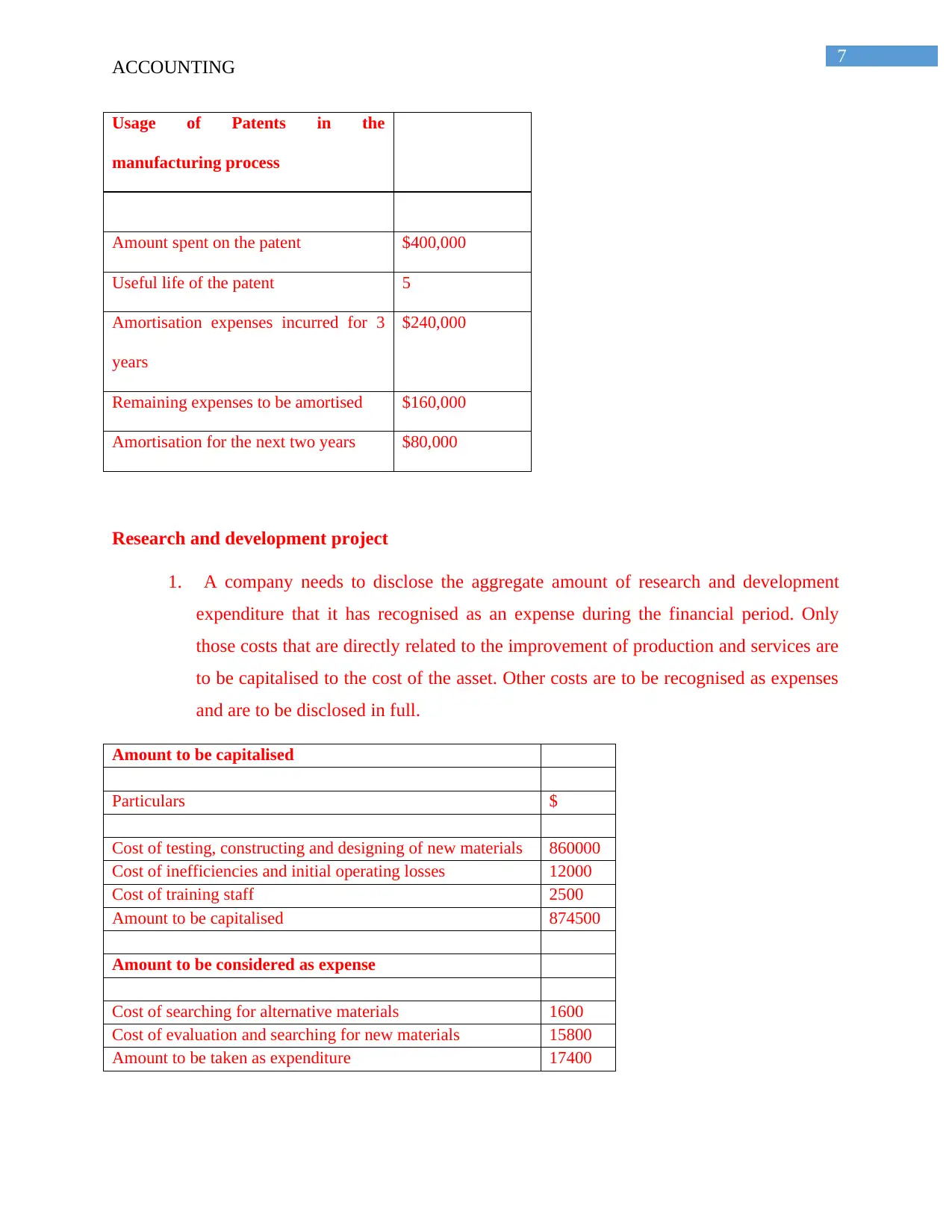

Usage of Patents in the

manufacturing process

Amount spent on the patent $400,000

Useful life of the patent 5

Amortisation expenses incurred for 3

years

$240,000

Remaining expenses to be amortised $160,000

Amortisation for the next two years $80,000

Research and development project

1. A company needs to disclose the aggregate amount of research and development

expenditure that it has recognised as an expense during the financial period. Only

those costs that are directly related to the improvement of production and services are

to be capitalised to the cost of the asset. Other costs are to be recognised as expenses

and are to be disclosed in full.

Amount to be capitalised

Particulars $

Cost of testing, constructing and designing of new materials 860000

Cost of inefficiencies and initial operating losses 12000

Cost of training staff 2500

Amount to be capitalised 874500

Amount to be considered as expense

Cost of searching for alternative materials 1600

Cost of evaluation and searching for new materials 15800

Amount to be taken as expenditure 17400

ACCOUNTING

Usage of Patents in the

manufacturing process

Amount spent on the patent $400,000

Useful life of the patent 5

Amortisation expenses incurred for 3

years

$240,000

Remaining expenses to be amortised $160,000

Amortisation for the next two years $80,000

Research and development project

1. A company needs to disclose the aggregate amount of research and development

expenditure that it has recognised as an expense during the financial period. Only

those costs that are directly related to the improvement of production and services are

to be capitalised to the cost of the asset. Other costs are to be recognised as expenses

and are to be disclosed in full.

Amount to be capitalised

Particulars $

Cost of testing, constructing and designing of new materials 860000

Cost of inefficiencies and initial operating losses 12000

Cost of training staff 2500

Amount to be capitalised 874500

Amount to be considered as expense

Cost of searching for alternative materials 1600

Cost of evaluation and searching for new materials 15800

Amount to be taken as expenditure 17400

8

ACCOUNTING

2. As per the above calculations, the amount that is to be capitalised is to be added to the

cost of the asset whereas other costs are to be shown as an expenditure and to be

disclosed fully in the books of accounts at the end of the year.

ACCOUNTING

2. As per the above calculations, the amount that is to be capitalised is to be added to the

cost of the asset whereas other costs are to be shown as an expenditure and to be

disclosed fully in the books of accounts at the end of the year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING

Question 2

Answer (a)

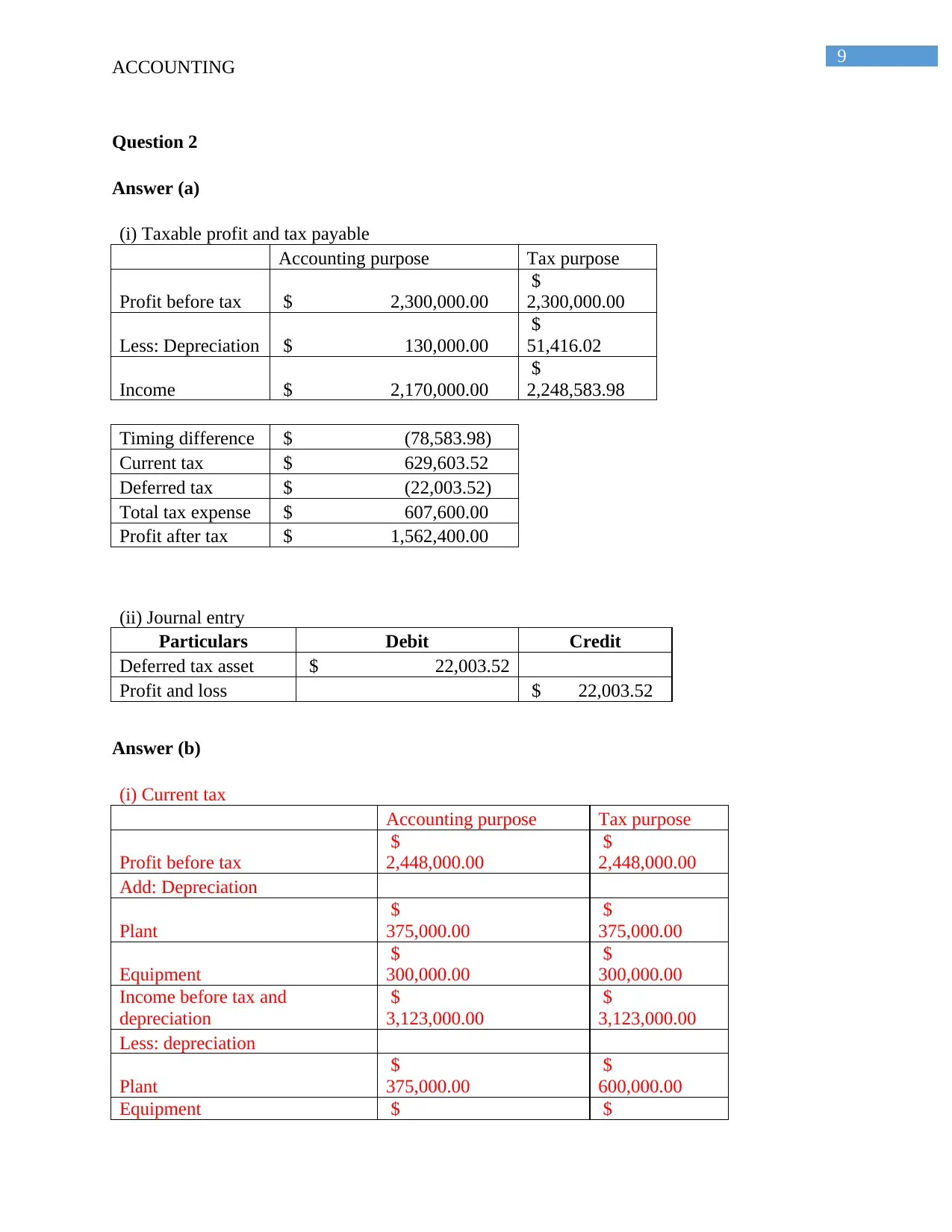

(i) Taxable profit and tax payable

Accounting purpose Tax purpose

Profit before tax $ 2,300,000.00

$

2,300,000.00

Less: Depreciation $ 130,000.00

$

51,416.02

Income $ 2,170,000.00

$

2,248,583.98

Timing difference $ (78,583.98)

Current tax $ 629,603.52

Deferred tax $ (22,003.52)

Total tax expense $ 607,600.00

Profit after tax $ 1,562,400.00

(ii) Journal entry

Particulars Debit Credit

Deferred tax asset $ 22,003.52

Profit and loss $ 22,003.52

Answer (b)

(i) Current tax

Accounting purpose Tax purpose

Profit before tax

$

2,448,000.00

$

2,448,000.00

Add: Depreciation

Plant

$

375,000.00

$

375,000.00

Equipment

$

300,000.00

$

300,000.00

Income before tax and

depreciation

$

3,123,000.00

$

3,123,000.00

Less: depreciation

Plant

$

375,000.00

$

600,000.00

Equipment $ $

ACCOUNTING

Question 2

Answer (a)

(i) Taxable profit and tax payable

Accounting purpose Tax purpose

Profit before tax $ 2,300,000.00

$

2,300,000.00

Less: Depreciation $ 130,000.00

$

51,416.02

Income $ 2,170,000.00

$

2,248,583.98

Timing difference $ (78,583.98)

Current tax $ 629,603.52

Deferred tax $ (22,003.52)

Total tax expense $ 607,600.00

Profit after tax $ 1,562,400.00

(ii) Journal entry

Particulars Debit Credit

Deferred tax asset $ 22,003.52

Profit and loss $ 22,003.52

Answer (b)

(i) Current tax

Accounting purpose Tax purpose

Profit before tax

$

2,448,000.00

$

2,448,000.00

Add: Depreciation

Plant

$

375,000.00

$

375,000.00

Equipment

$

300,000.00

$

300,000.00

Income before tax and

depreciation

$

3,123,000.00

$

3,123,000.00

Less: depreciation

Plant

$

375,000.00

$

600,000.00

Equipment $ $

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

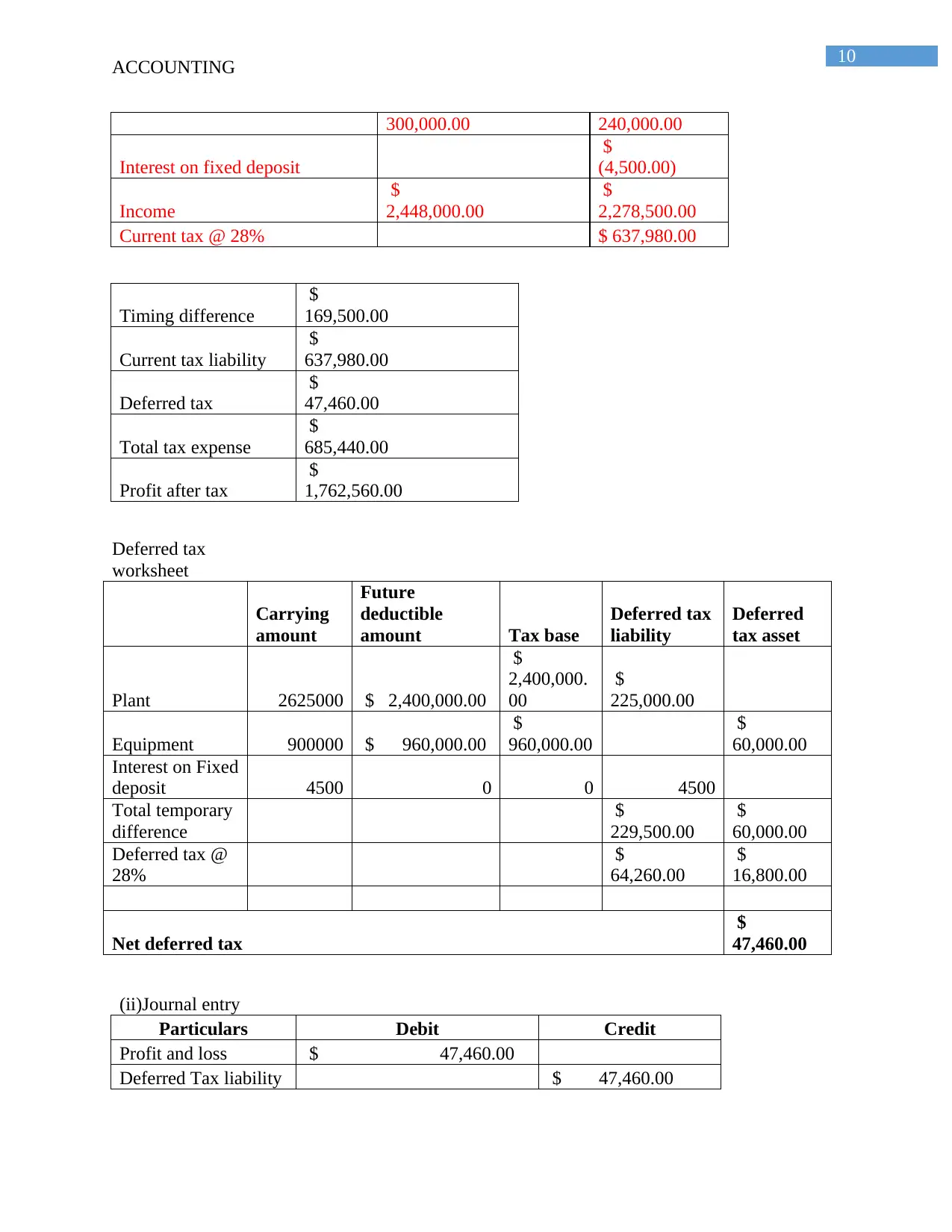

ACCOUNTING

300,000.00 240,000.00

Interest on fixed deposit

$

(4,500.00)

Income

$

2,448,000.00

$

2,278,500.00

Current tax @ 28% $ 637,980.00

Timing difference

$

169,500.00

Current tax liability

$

637,980.00

Deferred tax

$

47,460.00

Total tax expense

$

685,440.00

Profit after tax

$

1,762,560.00

Deferred tax

worksheet

Carrying

amount

Future

deductible

amount Tax base

Deferred tax

liability

Deferred

tax asset

Plant 2625000 $ 2,400,000.00

$

2,400,000.

00

$

225,000.00

Equipment 900000 $ 960,000.00

$

960,000.00

$

60,000.00

Interest on Fixed

deposit 4500 0 0 4500

Total temporary

difference

$

229,500.00

$

60,000.00

Deferred tax @

28%

$

64,260.00

$

16,800.00

Net deferred tax

$

47,460.00

(ii)Journal entry

Particulars Debit Credit

Profit and loss $ 47,460.00

Deferred Tax liability $ 47,460.00

ACCOUNTING

300,000.00 240,000.00

Interest on fixed deposit

$

(4,500.00)

Income

$

2,448,000.00

$

2,278,500.00

Current tax @ 28% $ 637,980.00

Timing difference

$

169,500.00

Current tax liability

$

637,980.00

Deferred tax

$

47,460.00

Total tax expense

$

685,440.00

Profit after tax

$

1,762,560.00

Deferred tax

worksheet

Carrying

amount

Future

deductible

amount Tax base

Deferred tax

liability

Deferred

tax asset

Plant 2625000 $ 2,400,000.00

$

2,400,000.

00

$

225,000.00

Equipment 900000 $ 960,000.00

$

960,000.00

$

60,000.00

Interest on Fixed

deposit 4500 0 0 4500

Total temporary

difference

$

229,500.00

$

60,000.00

Deferred tax @

28%

$

64,260.00

$

16,800.00

Net deferred tax

$

47,460.00

(ii)Journal entry

Particulars Debit Credit

Profit and loss $ 47,460.00

Deferred Tax liability $ 47,460.00

11

ACCOUNTING

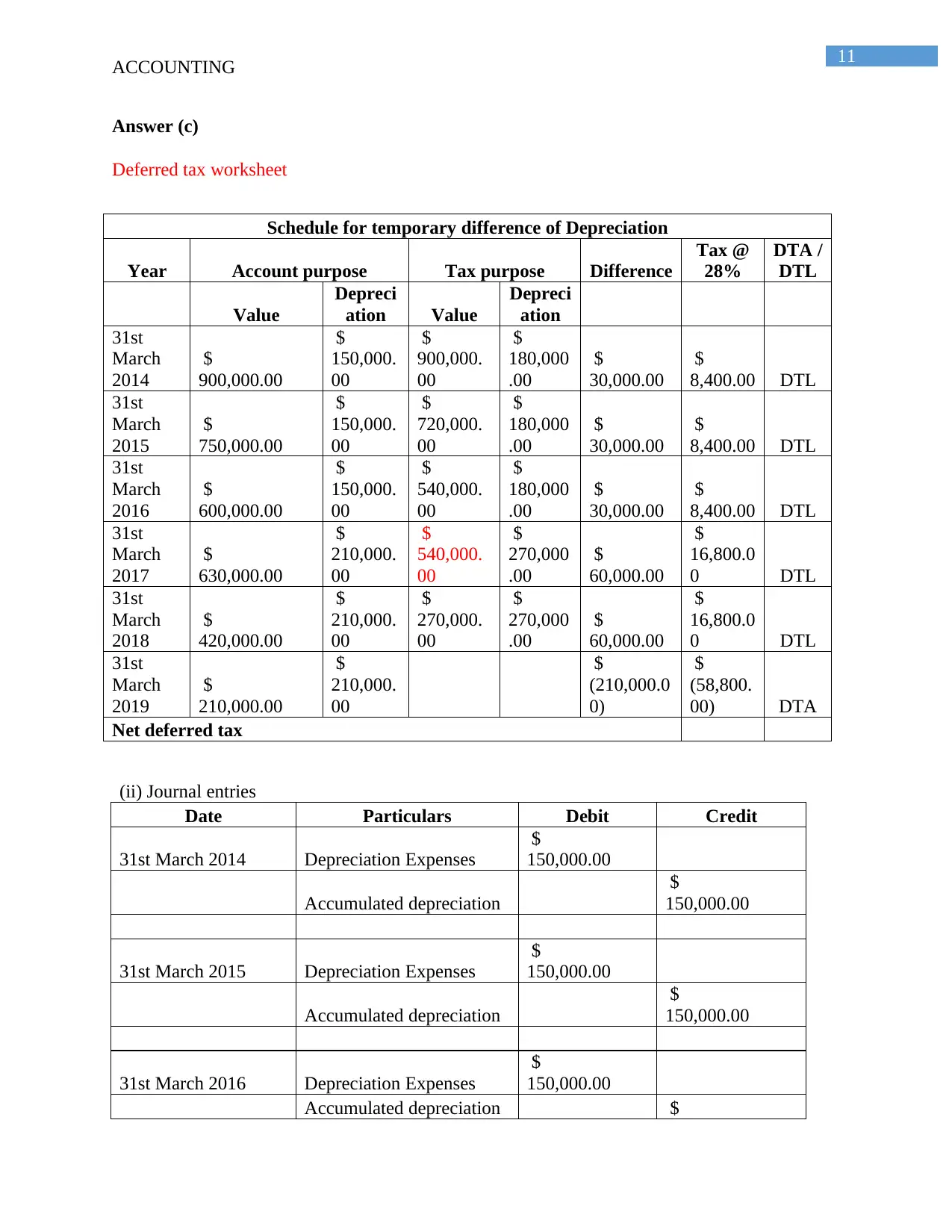

Answer (c)

Deferred tax worksheet

Schedule for temporary difference of Depreciation

Year Account purpose Tax purpose Difference

Tax @

28%

DTA /

DTL

Value

Depreci

ation Value

Depreci

ation

31st

March

2014

$

900,000.00

$

150,000.

00

$

900,000.

00

$

180,000

.00

$

30,000.00

$

8,400.00 DTL

31st

March

2015

$

750,000.00

$

150,000.

00

$

720,000.

00

$

180,000

.00

$

30,000.00

$

8,400.00 DTL

31st

March

2016

$

600,000.00

$

150,000.

00

$

540,000.

00

$

180,000

.00

$

30,000.00

$

8,400.00 DTL

31st

March

2017

$

630,000.00

$

210,000.

00

$

540,000.

00

$

270,000

.00

$

60,000.00

$

16,800.0

0 DTL

31st

March

2018

$

420,000.00

$

210,000.

00

$

270,000.

00

$

270,000

.00

$

60,000.00

$

16,800.0

0 DTL

31st

March

2019

$

210,000.00

$

210,000.

00

$

(210,000.0

0)

$

(58,800.

00) DTA

Net deferred tax

(ii) Journal entries

Date Particulars Debit Credit

31st March 2014 Depreciation Expenses

$

150,000.00

Accumulated depreciation

$

150,000.00

31st March 2015 Depreciation Expenses

$

150,000.00

Accumulated depreciation

$

150,000.00

31st March 2016 Depreciation Expenses

$

150,000.00

Accumulated depreciation $

ACCOUNTING

Answer (c)

Deferred tax worksheet

Schedule for temporary difference of Depreciation

Year Account purpose Tax purpose Difference

Tax @

28%

DTA /

DTL

Value

Depreci

ation Value

Depreci

ation

31st

March

2014

$

900,000.00

$

150,000.

00

$

900,000.

00

$

180,000

.00

$

30,000.00

$

8,400.00 DTL

31st

March

2015

$

750,000.00

$

150,000.

00

$

720,000.

00

$

180,000

.00

$

30,000.00

$

8,400.00 DTL

31st

March

2016

$

600,000.00

$

150,000.

00

$

540,000.

00

$

180,000

.00

$

30,000.00

$

8,400.00 DTL

31st

March

2017

$

630,000.00

$

210,000.

00

$

540,000.

00

$

270,000

.00

$

60,000.00

$

16,800.0

0 DTL

31st

March

2018

$

420,000.00

$

210,000.

00

$

270,000.

00

$

270,000

.00

$

60,000.00

$

16,800.0

0 DTL

31st

March

2019

$

210,000.00

$

210,000.

00

$

(210,000.0

0)

$

(58,800.

00) DTA

Net deferred tax

(ii) Journal entries

Date Particulars Debit Credit

31st March 2014 Depreciation Expenses

$

150,000.00

Accumulated depreciation

$

150,000.00

31st March 2015 Depreciation Expenses

$

150,000.00

Accumulated depreciation

$

150,000.00

31st March 2016 Depreciation Expenses

$

150,000.00

Accumulated depreciation $

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.