Accounting Report: Financial and Management Accounting for Business

VerifiedAdded on 2023/01/12

|20

|3591

|64

Report

AI Summary

This report delves into the core concepts of financial and management accounting, exploring their aims, purposes, and applications within a business context. It identifies the diverse users of accounting information, detailing their specific needs and the types of data they require for decision-making. The report also examines the role and significance of international accounting standards boards and the standard advisory council in shaping global accounting practices. Furthermore, it includes the analysis of two accounting problems involving different organizations, providing practical examples to illustrate key accounting principles. The report covers the journal entries, ledger accounts, and trial balance for the first problem to showcase the accounting process.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................3

TASK 1.......................................................................................................................................................3

Aims and Purpose of financial and management accounting to business................................................3

Various users of accounting information and what information they require..........................................4

Role of international accounting board and the standard advisory council..............................................5

TASK 2.......................................................................................................................................................6

Problem 1................................................................................................................................................6

Problem 2..............................................................................................................................................12

CONCLUSION.........................................................................................................................................14

REFERENCES..........................................................................................................................................15

INTRODUCTION.......................................................................................................................................3

TASK 1.......................................................................................................................................................3

Aims and Purpose of financial and management accounting to business................................................3

Various users of accounting information and what information they require..........................................4

Role of international accounting board and the standard advisory council..............................................5

TASK 2.......................................................................................................................................................6

Problem 1................................................................................................................................................6

Problem 2..............................................................................................................................................12

CONCLUSION.........................................................................................................................................14

REFERENCES..........................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Accounting could be characterized as the practice of documenting all business activities

in correct records in order to assess specific expenditure and profits. Financial planning is the

method of controlling and sustaining the company output by implementing various comments.

These are declaration of exchange, accounting of P&L, balance sheet and cash flow. This could

be decided with both the aid of all of them whether the business is doing well, or not (Davison,

2015). Each of these may also be used to assess competitiveness, liquidity etc. If a company

cannot stimulate then this will lead to the loss of confidence from shareholders and other

participants. This report based on the department store. In this report discuss about the aims and

purpose of management and financial accounting and identify various users of particular

accounting information. Along with analysis the requirement of these information and role of

international accounting standards boards and the standard advisory council. Additionally, in this

report analysis two problems of different organisation of Jack Uzi and woody train.

TASK 1

Aims and Purpose of financial and management accounting to business

Financial accounting: It relates to reporting for money transfers by categorizing,

reviewing, illustrating and reporting financial activities such as acquisitions, revenues, accounts

receivable and accruals and eventually planning financial accounts including income statement,

balance sheet and cash flow. Financial accounting's key goal is to present true and equitable

description of the firm's personal finances. Firstly firm will start with a double-entry method and

debit & credit, and then slowly recognize newspaper and account, trial account, and four

financial statements, to know its essence.

Purpose: Financial Accounting is intended to provide the details necessary for sound

economic judgment-making. The main purpose of financial accounting is to produce financial

statements and provide information to external parties such as shareholders, lenders and tax

office with details regarding the current results of a business.

Accounting could be characterized as the practice of documenting all business activities

in correct records in order to assess specific expenditure and profits. Financial planning is the

method of controlling and sustaining the company output by implementing various comments.

These are declaration of exchange, accounting of P&L, balance sheet and cash flow. This could

be decided with both the aid of all of them whether the business is doing well, or not (Davison,

2015). Each of these may also be used to assess competitiveness, liquidity etc. If a company

cannot stimulate then this will lead to the loss of confidence from shareholders and other

participants. This report based on the department store. In this report discuss about the aims and

purpose of management and financial accounting and identify various users of particular

accounting information. Along with analysis the requirement of these information and role of

international accounting standards boards and the standard advisory council. Additionally, in this

report analysis two problems of different organisation of Jack Uzi and woody train.

TASK 1

Aims and Purpose of financial and management accounting to business

Financial accounting: It relates to reporting for money transfers by categorizing,

reviewing, illustrating and reporting financial activities such as acquisitions, revenues, accounts

receivable and accruals and eventually planning financial accounts including income statement,

balance sheet and cash flow. Financial accounting's key goal is to present true and equitable

description of the firm's personal finances. Firstly firm will start with a double-entry method and

debit & credit, and then slowly recognize newspaper and account, trial account, and four

financial statements, to know its essence.

Purpose: Financial Accounting is intended to provide the details necessary for sound

economic judgment-making. The main purpose of financial accounting is to produce financial

statements and provide information to external parties such as shareholders, lenders and tax

office with details regarding the current results of a business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting: It is the method of defining, calculating, collecting,

evaluating, planning, interpreting, and transmitting financial information that administration uses

to prepare, analyze, and monitor an entity and to ensure the proper use and transparency of its

funds. Accounting management also involves writing financial statements for un-management

entities including stakeholders, lenders, enforcement officers and immigration authorities

(Merkl-Davies and Brennan, 2017).

Purpose: Accounting for management is essential to maintain the vitality of a company.

The overall purpose of this method of reporting is to help all facets of commercial activities in

choice-making procedures. Management accounting plays a variety of important objectives in

achieving that aim.

Use in business: Financial accounting is often used to record transactions in a company's

financial statements. Government businesses are expected to disclose the performance to the

government whereas private firms disclose to their holders. Financial information is generated in

each scenario and the effects are analyzed. That is the financial statement cycle.

Managerial accounting should be used for short- and long-term actions that concern a

business's safety. Management accounting allows executives make financial choices, aimed at

increasing the operating performance of the business, thereby helping to make lengthy-term

investment choices. Along with it also use by business for planning and control, record keeping

and decision making procedure (Burks, 2015).

Various users of accounting information and what information they require

The accounting information are utilized by the different users to make decision in regard

of business investments. External users are the shareholders, administrators, executives, business

staff, suppliers, stakeholders, administration, export markets, regulatory authorities, global

normalization departments, reporters and inner consumers. Internal users are that individual who

runs, manages and operates the daily activities of the inside area of an organization.

1. Owners and Stockholders.

2. Directors,

evaluating, planning, interpreting, and transmitting financial information that administration uses

to prepare, analyze, and monitor an entity and to ensure the proper use and transparency of its

funds. Accounting management also involves writing financial statements for un-management

entities including stakeholders, lenders, enforcement officers and immigration authorities

(Merkl-Davies and Brennan, 2017).

Purpose: Accounting for management is essential to maintain the vitality of a company.

The overall purpose of this method of reporting is to help all facets of commercial activities in

choice-making procedures. Management accounting plays a variety of important objectives in

achieving that aim.

Use in business: Financial accounting is often used to record transactions in a company's

financial statements. Government businesses are expected to disclose the performance to the

government whereas private firms disclose to their holders. Financial information is generated in

each scenario and the effects are analyzed. That is the financial statement cycle.

Managerial accounting should be used for short- and long-term actions that concern a

business's safety. Management accounting allows executives make financial choices, aimed at

increasing the operating performance of the business, thereby helping to make lengthy-term

investment choices. Along with it also use by business for planning and control, record keeping

and decision making procedure (Burks, 2015).

Various users of accounting information and what information they require

The accounting information are utilized by the different users to make decision in regard

of business investments. External users are the shareholders, administrators, executives, business

staff, suppliers, stakeholders, administration, export markets, regulatory authorities, global

normalization departments, reporters and inner consumers. Internal users are that individual who

runs, manages and operates the daily activities of the inside area of an organization.

1. Owners and Stockholders.

2. Directors,

3. Managers,

4. Officers.

5. Internal Departments.

6. Employees

7. Internal Auditor.

Management accounting defines tracks, assesses, and discusses the financial details that

administration uses to schedule, monitor, and assess the inner user activities of a organization.

External users are all those people who have a curiosity in an agency's account details and are

not member of the administrative phase of the organization. External consumers have a formal or

informal involvement in information pertaining to finance. Financial accounting is the

mechanism for preparing the company's financial statement that can be used by inner as well as

outside stakeholders. Those reports are essential to financial details external users (Boiral,

2016).. Examples of external users of accounting information are;

Creditors: Creditors or investors have used the financial documents to figure out the purchaser's

creditworthiness the debtor's mortgage, the amount of the claimant's current assets, verification

of revenue, economical situation, etc. until making loans to the business entity.

Investors: Investors are the suppliers of a business' money. An investor sees the financial

statements before spending to find out the prospects of the company in the future. For a

shareholder, financial data is essential for trying to make sure the expenditure is safe.

Government: To governmental federal agencies, financial statements is important because it

helps government to track the environment and the sector.

Trading partners: Company requires to do trade, that is the reality. Partner investment companies

look at government details and plan to deal with the specific economy.

4. Officers.

5. Internal Departments.

6. Employees

7. Internal Auditor.

Management accounting defines tracks, assesses, and discusses the financial details that

administration uses to schedule, monitor, and assess the inner user activities of a organization.

External users are all those people who have a curiosity in an agency's account details and are

not member of the administrative phase of the organization. External consumers have a formal or

informal involvement in information pertaining to finance. Financial accounting is the

mechanism for preparing the company's financial statement that can be used by inner as well as

outside stakeholders. Those reports are essential to financial details external users (Boiral,

2016).. Examples of external users of accounting information are;

Creditors: Creditors or investors have used the financial documents to figure out the purchaser's

creditworthiness the debtor's mortgage, the amount of the claimant's current assets, verification

of revenue, economical situation, etc. until making loans to the business entity.

Investors: Investors are the suppliers of a business' money. An investor sees the financial

statements before spending to find out the prospects of the company in the future. For a

shareholder, financial data is essential for trying to make sure the expenditure is safe.

Government: To governmental federal agencies, financial statements is important because it

helps government to track the environment and the sector.

Trading partners: Company requires to do trade, that is the reality. Partner investment companies

look at government details and plan to deal with the specific economy.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

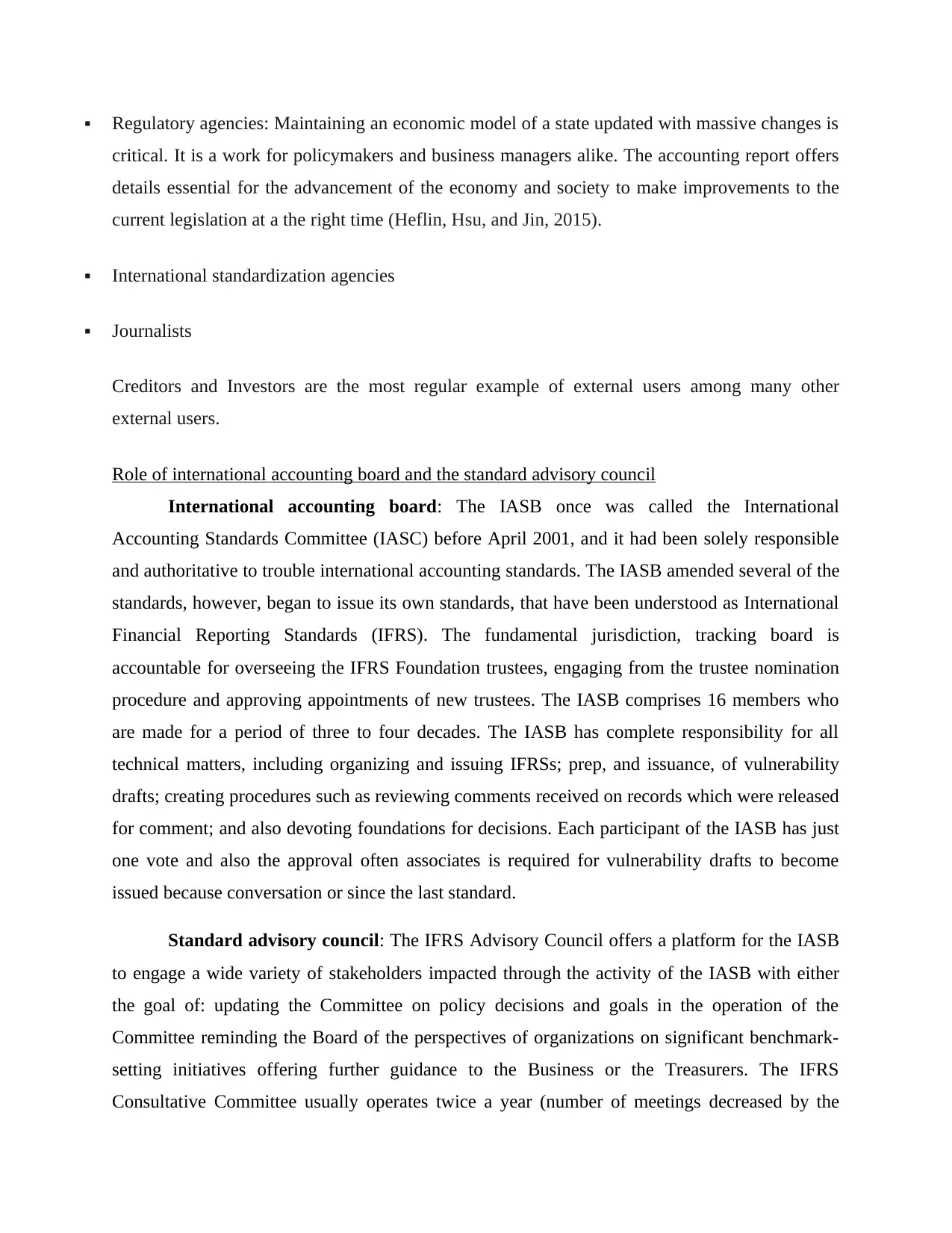

Regulatory agencies: Maintaining an economic model of a state updated with massive changes is

critical. It is a work for policymakers and business managers alike. The accounting report offers

details essential for the advancement of the economy and society to make improvements to the

current legislation at a the right time (Heflin, Hsu, and Jin, 2015).

International standardization agencies

Journalists

Creditors and Investors are the most regular example of external users among many other

external users.

Role of international accounting board and the standard advisory council

International accounting board: The IASB once was called the International

Accounting Standards Committee (IASC) before April 2001, and it had been solely responsible

and authoritative to trouble international accounting standards. The IASB amended several of the

standards, however, began to issue its own standards, that have been understood as International

Financial Reporting Standards (IFRS). The fundamental jurisdiction, tracking board is

accountable for overseeing the IFRS Foundation trustees, engaging from the trustee nomination

procedure and approving appointments of new trustees. The IASB comprises 16 members who

are made for a period of three to four decades. The IASB has complete responsibility for all

technical matters, including organizing and issuing IFRSs; prep, and issuance, of vulnerability

drafts; creating procedures such as reviewing comments received on records which were released

for comment; and also devoting foundations for decisions. Each participant of the IASB has just

one vote and also the approval often associates is required for vulnerability drafts to become

issued because conversation or since the last standard.

Standard advisory council: The IFRS Advisory Council offers a platform for the IASB

to engage a wide variety of stakeholders impacted through the activity of the IASB with either

the goal of: updating the Committee on policy decisions and goals in the operation of the

Committee reminding the Board of the perspectives of organizations on significant benchmark-

setting initiatives offering further guidance to the Business or the Treasurers. The IFRS

Consultative Committee usually operates twice a year (number of meetings decreased by the

critical. It is a work for policymakers and business managers alike. The accounting report offers

details essential for the advancement of the economy and society to make improvements to the

current legislation at a the right time (Heflin, Hsu, and Jin, 2015).

International standardization agencies

Journalists

Creditors and Investors are the most regular example of external users among many other

external users.

Role of international accounting board and the standard advisory council

International accounting board: The IASB once was called the International

Accounting Standards Committee (IASC) before April 2001, and it had been solely responsible

and authoritative to trouble international accounting standards. The IASB amended several of the

standards, however, began to issue its own standards, that have been understood as International

Financial Reporting Standards (IFRS). The fundamental jurisdiction, tracking board is

accountable for overseeing the IFRS Foundation trustees, engaging from the trustee nomination

procedure and approving appointments of new trustees. The IASB comprises 16 members who

are made for a period of three to four decades. The IASB has complete responsibility for all

technical matters, including organizing and issuing IFRSs; prep, and issuance, of vulnerability

drafts; creating procedures such as reviewing comments received on records which were released

for comment; and also devoting foundations for decisions. Each participant of the IASB has just

one vote and also the approval often associates is required for vulnerability drafts to become

issued because conversation or since the last standard.

Standard advisory council: The IFRS Advisory Council offers a platform for the IASB

to engage a wide variety of stakeholders impacted through the activity of the IASB with either

the goal of: updating the Committee on policy decisions and goals in the operation of the

Committee reminding the Board of the perspectives of organizations on significant benchmark-

setting initiatives offering further guidance to the Business or the Treasurers. The IFRS

Consultative Committee usually operates twice a year (number of meetings decreased by the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2015 examination of the Framework from three meetings to two). The IFRS consultative board

was referred to as the Standards Advisory Council.

The Advisory Council is your appropriate judicial system into the International

Accounting Standards Board (Board) and also the Trustees of this IFRS Foundation. It is made

up of wide selection of agents, including organizations’ and individuals having an interest in

international economic coverage (Lowe, 2019). The attention of this Advisory Council would be

to give tactical support and information into this IFRS Foundation; also it matches in London at

least 2 times per year for a period of time of 2 weeks. The Standards Advisory Council (SAC)

could be your part- time frame which guides the Trustees and also the IASB in their work and

priorities. The Trustees of the IASC Foundation want to make a Chairman of this SAC, Who'd

devote a Minimum of One week a month into the SAC's job

TASK 2

Problem 1

Journal Entry

Date Particular Debit Credit

A Cash a/c 2000

Office supplies a/c 75

To accounts payable 75

To Jack's capital a/c 2000

(Being accounts payable to Bing

office supply)

B Computer Equipment a/c 500

To Lease a/c 500

(Being payment in advance for

lease for november)

was referred to as the Standards Advisory Council.

The Advisory Council is your appropriate judicial system into the International

Accounting Standards Board (Board) and also the Trustees of this IFRS Foundation. It is made

up of wide selection of agents, including organizations’ and individuals having an interest in

international economic coverage (Lowe, 2019). The attention of this Advisory Council would be

to give tactical support and information into this IFRS Foundation; also it matches in London at

least 2 times per year for a period of time of 2 weeks. The Standards Advisory Council (SAC)

could be your part- time frame which guides the Trustees and also the IASB in their work and

priorities. The Trustees of the IASC Foundation want to make a Chairman of this SAC, Who'd

devote a Minimum of One week a month into the SAC's job

TASK 2

Problem 1

Journal Entry

Date Particular Debit Credit

A Cash a/c 2000

Office supplies a/c 75

To accounts payable 75

To Jack's capital a/c 2000

(Being accounts payable to Bing

office supply)

B Computer Equipment a/c 500

To Lease a/c 500

(Being payment in advance for

lease for november)

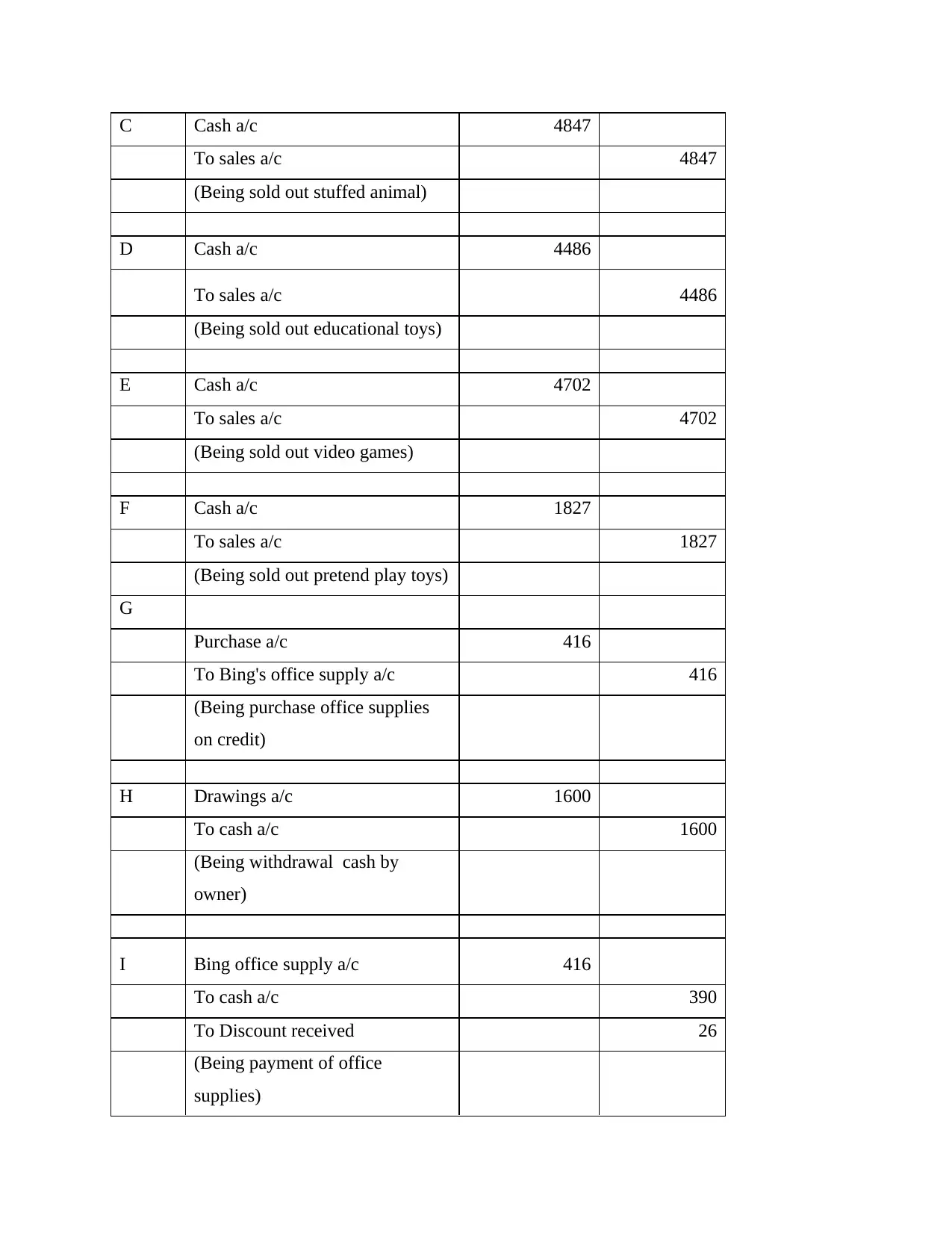

C Cash a/c 4847

To sales a/c 4847

(Being sold out stuffed animal)

D Cash a/c 4486

To sales a/c 4486

(Being sold out educational toys)

E Cash a/c 4702

To sales a/c 4702

(Being sold out video games)

F Cash a/c 1827

To sales a/c 1827

(Being sold out pretend play toys)

G

Purchase a/c 416

To Bing's office supply a/c 416

(Being purchase office supplies

on credit)

H Drawings a/c 1600

To cash a/c 1600

(Being withdrawal cash by

owner)

I Bing office supply a/c 416

To cash a/c 390

To Discount received 26

(Being payment of office

supplies)

To sales a/c 4847

(Being sold out stuffed animal)

D Cash a/c 4486

To sales a/c 4486

(Being sold out educational toys)

E Cash a/c 4702

To sales a/c 4702

(Being sold out video games)

F Cash a/c 1827

To sales a/c 1827

(Being sold out pretend play toys)

G

Purchase a/c 416

To Bing's office supply a/c 416

(Being purchase office supplies

on credit)

H Drawings a/c 1600

To cash a/c 1600

(Being withdrawal cash by

owner)

I Bing office supply a/c 416

To cash a/c 390

To Discount received 26

(Being payment of office

supplies)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

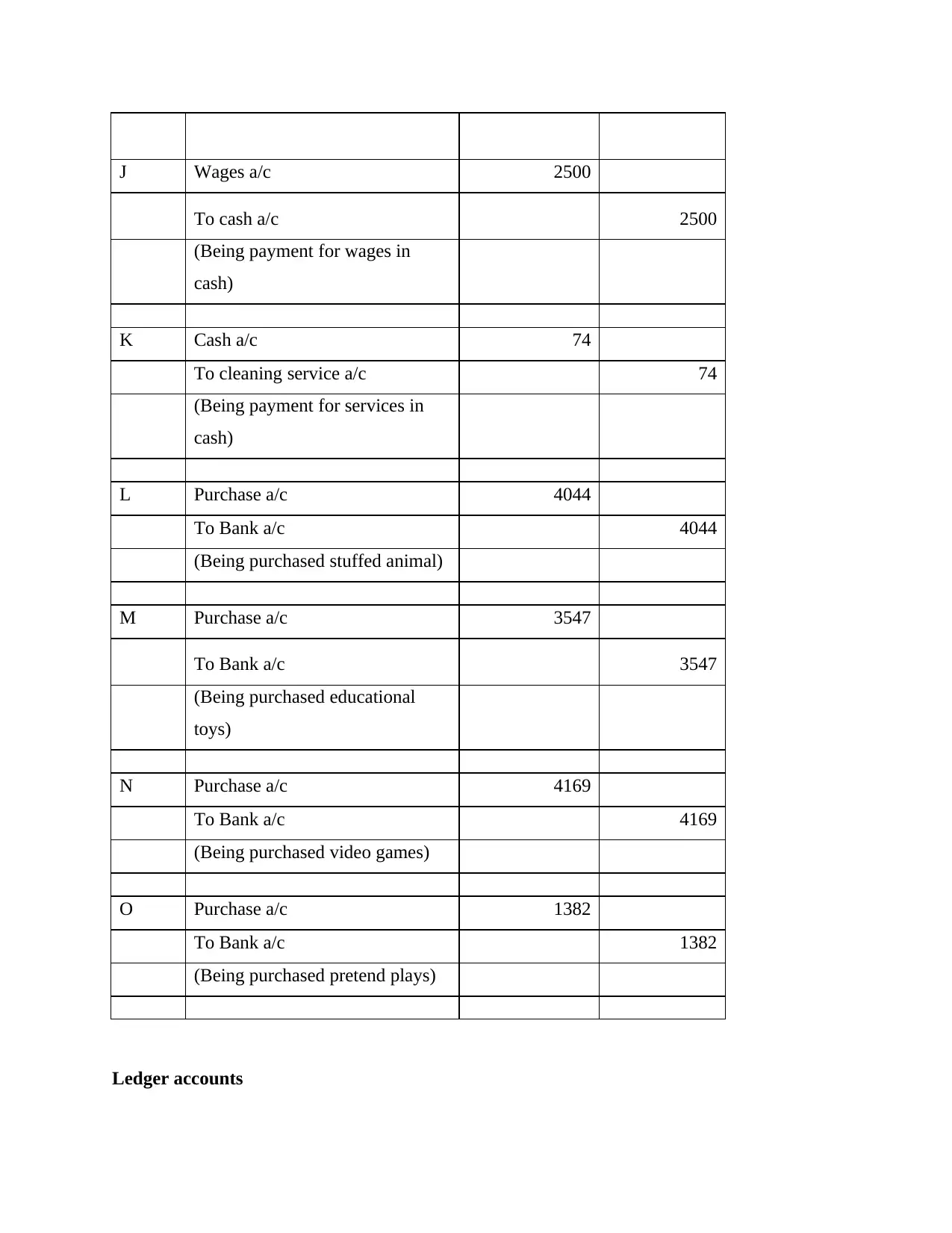

J Wages a/c 2500

To cash a/c 2500

(Being payment for wages in

cash)

K Cash a/c 74

To cleaning service a/c 74

(Being payment for services in

cash)

L Purchase a/c 4044

To Bank a/c 4044

(Being purchased stuffed animal)

M Purchase a/c 3547

To Bank a/c 3547

(Being purchased educational

toys)

N Purchase a/c 4169

To Bank a/c 4169

(Being purchased video games)

O Purchase a/c 1382

To Bank a/c 1382

(Being purchased pretend plays)

Ledger accounts

To cash a/c 2500

(Being payment for wages in

cash)

K Cash a/c 74

To cleaning service a/c 74

(Being payment for services in

cash)

L Purchase a/c 4044

To Bank a/c 4044

(Being purchased stuffed animal)

M Purchase a/c 3547

To Bank a/c 3547

(Being purchased educational

toys)

N Purchase a/c 4169

To Bank a/c 4169

(Being purchased video games)

O Purchase a/c 1382

To Bank a/c 1382

(Being purchased pretend plays)

Ledger accounts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

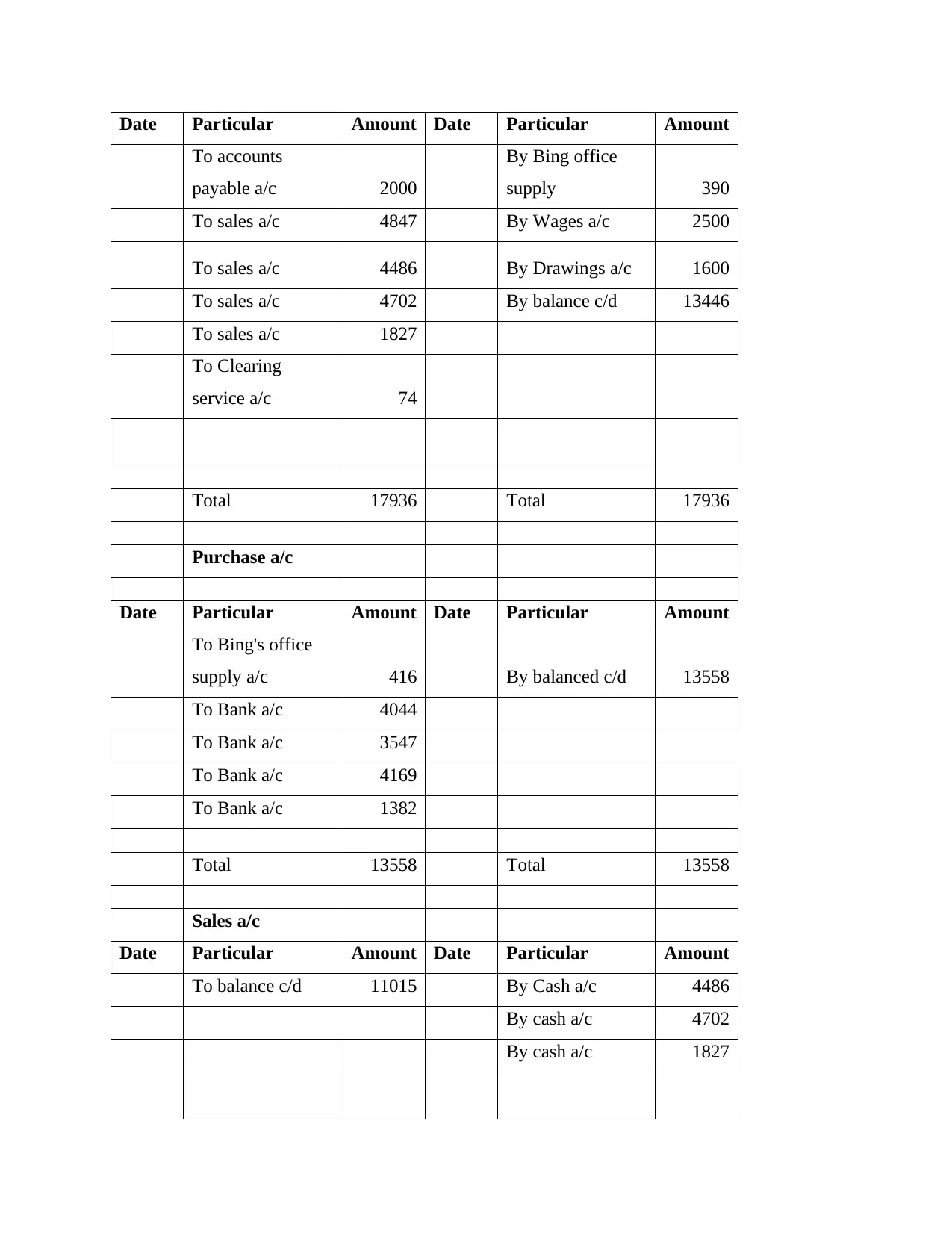

Cash a/c

Date Particular Amount Date Particular Amount

To accounts

payable a/c 2000

By Bing office

supply 390

To sales a/c 4847 By Wages a/c 2500

To sales a/c 4486 By Drawings a/c 1600

To sales a/c 4702 By balance c/d 13446

To sales a/c 1827

To Clearing

service a/c 74

Total 17936 Total 17936

Purchase a/c

Date Particular Amount Date Particular Amount

To Bing's office

supply a/c 416 By balanced c/d 13558

To Bank a/c 4044

To Bank a/c 3547

To Bank a/c 4169

To Bank a/c 1382

Total 13558 Total 13558

Sales a/c

Date Particular Amount Date Particular Amount

To balance c/d 11015 By Cash a/c 4486

By cash a/c 4702

By cash a/c 1827

To accounts

payable a/c 2000

By Bing office

supply 390

To sales a/c 4847 By Wages a/c 2500

To sales a/c 4486 By Drawings a/c 1600

To sales a/c 4702 By balance c/d 13446

To sales a/c 1827

To Clearing

service a/c 74

Total 17936 Total 17936

Purchase a/c

Date Particular Amount Date Particular Amount

To Bing's office

supply a/c 416 By balanced c/d 13558

To Bank a/c 4044

To Bank a/c 3547

To Bank a/c 4169

To Bank a/c 1382

Total 13558 Total 13558

Sales a/c

Date Particular Amount Date Particular Amount

To balance c/d 11015 By Cash a/c 4486

By cash a/c 4702

By cash a/c 1827

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.