Accounting: Income Statement, Balance Sheet, Break-even Analysis

Added on 2023-01-18

21 Pages3719 Words23 Views

Accounting

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

PART-A...........................................................................................................................................1

PART-B...........................................................................................................................................6

a. calculation of contribution in order to cover fixed cost..........................................................6

b. Computing break -even and MOS in respect of units as well as value in case each of the

wall clock sold at £40..................................................................................................................7

c. Valuing profit in case the company sells 54000 units at £40.................................................8

d. Calculation of the profit through revised sales and fixed cost................................................9

e. Determining and explaining break-even model with its assumptions...................................10

PART-C.........................................................................................................................................11

a. Assessing viability of project using investment appraisal tools and techniques..................11

b. Explaining and assessing benefits and the limitation of capital budgeting tools..................13

Identifying and explaining key benefits as well as drawbacks associated with budgeting

aspects.......................................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................1

PART-A...........................................................................................................................................1

PART-B...........................................................................................................................................6

a. calculation of contribution in order to cover fixed cost..........................................................6

b. Computing break -even and MOS in respect of units as well as value in case each of the

wall clock sold at £40..................................................................................................................7

c. Valuing profit in case the company sells 54000 units at £40.................................................8

d. Calculation of the profit through revised sales and fixed cost................................................9

e. Determining and explaining break-even model with its assumptions...................................10

PART-C.........................................................................................................................................11

a. Assessing viability of project using investment appraisal tools and techniques..................11

b. Explaining and assessing benefits and the limitation of capital budgeting tools..................13

Identifying and explaining key benefits as well as drawbacks associated with budgeting

aspects.......................................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION

Accounting refers to recording of the business transactions with storing, retrieving,

summarizing, sorting and communicating results in several reports for the users so that they

could assess the results and can make suitable decisions accordingly. The present study focuses

on preparation of the income statement and balance sheet of Terroy Plc which reflects its

financial performance and position in an overall industry. Furthermore, the study includes

computation of contribution per unit, break even assessment, profit evaluation and margin of

safety for Koklet Ltd in order to analyse that its operations are generating sufficient profits after

the payment fixed expenses and the variable cost. Moreover, the report highlights computation of

returns that the project will generate through application of various investment appraisal tools. It

also provides for a deeper insights towards different capital budgeting techniques with their

merits and demerits to the company.

PART-A

Income Statement

For the year ended 31 December 2018

Particulars Amount(

£)

Amount(

£)

Revenues:-

Sales(604800+154800) 759600

Other income 0

Total Revenues 759600

Expenses:-

COGS 291600

64800 356400

Depreciation 11000

1

Accounting refers to recording of the business transactions with storing, retrieving,

summarizing, sorting and communicating results in several reports for the users so that they

could assess the results and can make suitable decisions accordingly. The present study focuses

on preparation of the income statement and balance sheet of Terroy Plc which reflects its

financial performance and position in an overall industry. Furthermore, the study includes

computation of contribution per unit, break even assessment, profit evaluation and margin of

safety for Koklet Ltd in order to analyse that its operations are generating sufficient profits after

the payment fixed expenses and the variable cost. Moreover, the report highlights computation of

returns that the project will generate through application of various investment appraisal tools. It

also provides for a deeper insights towards different capital budgeting techniques with their

merits and demerits to the company.

PART-A

Income Statement

For the year ended 31 December 2018

Particulars Amount(

£)

Amount(

£)

Revenues:-

Sales(604800+154800) 759600

Other income 0

Total Revenues 759600

Expenses:-

COGS 291600

64800 356400

Depreciation 11000

1

Wages 140400

Add Outstanding wages at period end 2610 143010

Electricity Expenses 9270

Van running expenses 40320

Bad debts 1800

Rent paid 135000

Less:- prepaid rent at period end 27000 108000

Total Expenses:- 669800

Net profit before tax 89800

Less:- Tax paid 6930

Net profit after tax 82870

Balance sheet

Particulars Total Amount (£)

Liabilities

Shareholder's Equity 216000

Equity share capital 82870

Reserves and surplus

Current Liabilities

Outstanding Wages 2610

Outstanding Electricity Expenses 2430

Trade Payables 111600

Bank Overdraft 132840

Total Liabilities 548350

Fixed Assets

Delivery Van 61000

2

Add Outstanding wages at period end 2610 143010

Electricity Expenses 9270

Van running expenses 40320

Bad debts 1800

Rent paid 135000

Less:- prepaid rent at period end 27000 108000

Total Expenses:- 669800

Net profit before tax 89800

Less:- Tax paid 6930

Net profit after tax 82870

Balance sheet

Particulars Total Amount (£)

Liabilities

Shareholder's Equity 216000

Equity share capital 82870

Reserves and surplus

Current Liabilities

Outstanding Wages 2610

Outstanding Electricity Expenses 2430

Trade Payables 111600

Bank Overdraft 132840

Total Liabilities 548350

Fixed Assets

Delivery Van 61000

2

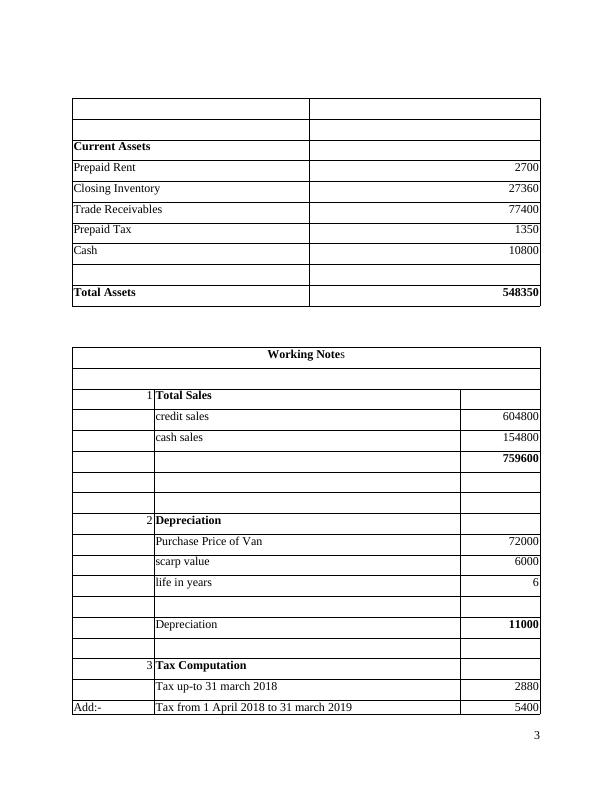

Current Assets

Prepaid Rent 2700

Closing Inventory 27360

Trade Receivables 77400

Prepaid Tax 1350

Cash 10800

Total Assets 548350

Working Notes

1 Total Sales

credit sales 604800

cash sales 154800

759600

2 Depreciation

Purchase Price of Van 72000

scarp value 6000

life in years 6

Depreciation 11000

3 Tax Computation

Tax up-to 31 march 2018 2880

Add:- Tax from 1 April 2018 to 31 march 2019 5400

3

Prepaid Rent 2700

Closing Inventory 27360

Trade Receivables 77400

Prepaid Tax 1350

Cash 10800

Total Assets 548350

Working Notes

1 Total Sales

credit sales 604800

cash sales 154800

759600

2 Depreciation

Purchase Price of Van 72000

scarp value 6000

life in years 6

Depreciation 11000

3 Tax Computation

Tax up-to 31 march 2018 2880

Add:- Tax from 1 April 2018 to 31 march 2019 5400

3

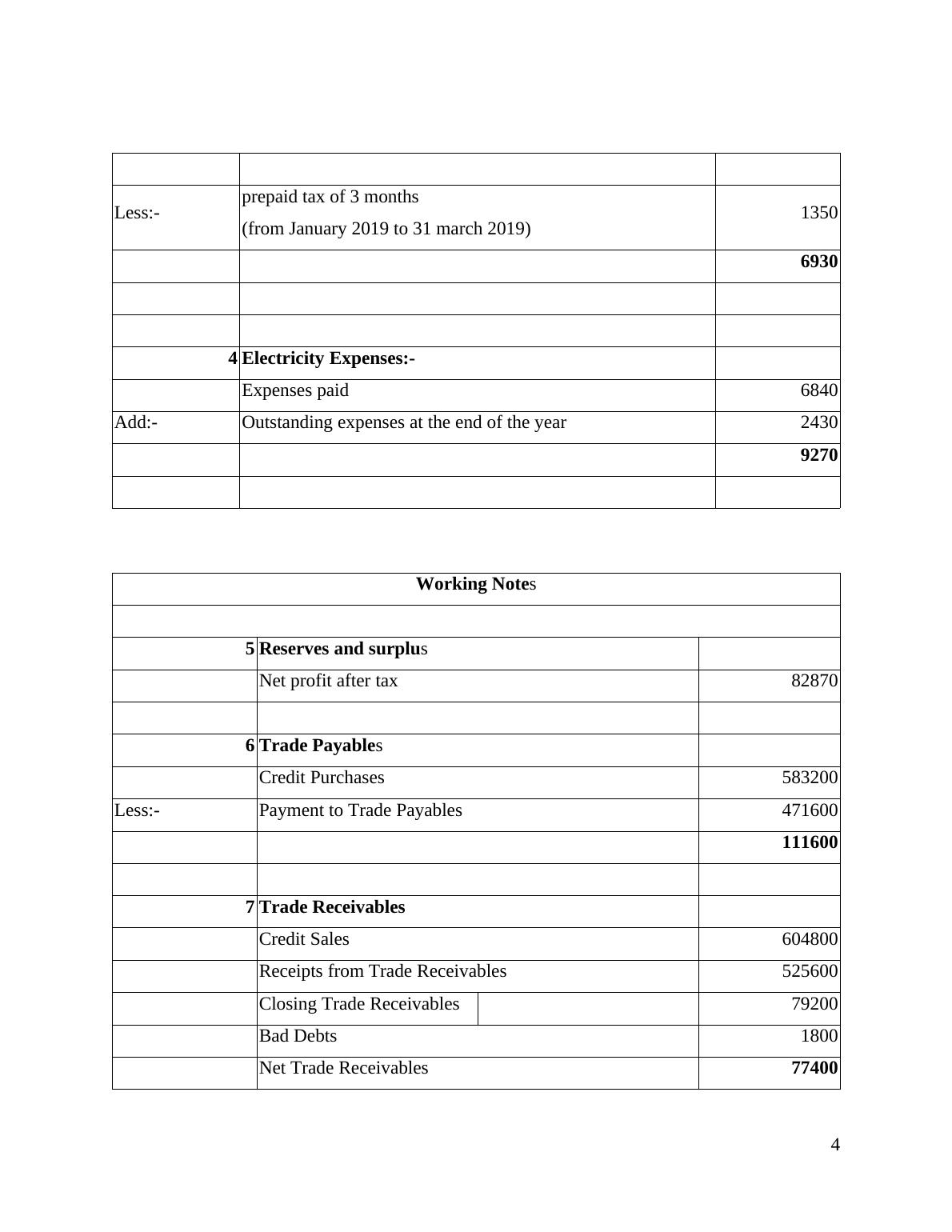

Less:- prepaid tax of 3 months

(from January 2019 to 31 march 2019) 1350

6930

4 Electricity Expenses:-

Expenses paid 6840

Add:- Outstanding expenses at the end of the year 2430

9270

Working Notes

5 Reserves and surplus

Net profit after tax 82870

6 Trade Payables

Credit Purchases 583200

Less:- Payment to Trade Payables 471600

111600

7 Trade Receivables

Credit Sales 604800

Receipts from Trade Receivables 525600

Closing Trade Receivables 79200

Bad Debts 1800

Net Trade Receivables 77400

4

(from January 2019 to 31 march 2019) 1350

6930

4 Electricity Expenses:-

Expenses paid 6840

Add:- Outstanding expenses at the end of the year 2430

9270

Working Notes

5 Reserves and surplus

Net profit after tax 82870

6 Trade Payables

Credit Purchases 583200

Less:- Payment to Trade Payables 471600

111600

7 Trade Receivables

Credit Sales 604800

Receipts from Trade Receivables 525600

Closing Trade Receivables 79200

Bad Debts 1800

Net Trade Receivables 77400

4

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Introduction to Accounting and Financelg...

|17

|3751

|35

Introduction to Accounting and Financelg...

|20

|3983

|67

Introduction to Accounting & Financelg...

|17

|5128

|72

Introduction to Accounting and Financelg...

|17

|3935

|59

Introduction to Accounting and Finance Assessmentlg...

|22

|3794

|58

Introduction to Accounting and Financelg...

|20

|2543

|73