NPV Forecast Analysis and Decision Making

VerifiedAdded on 2020/05/04

|11

|1037

|47

AI Summary

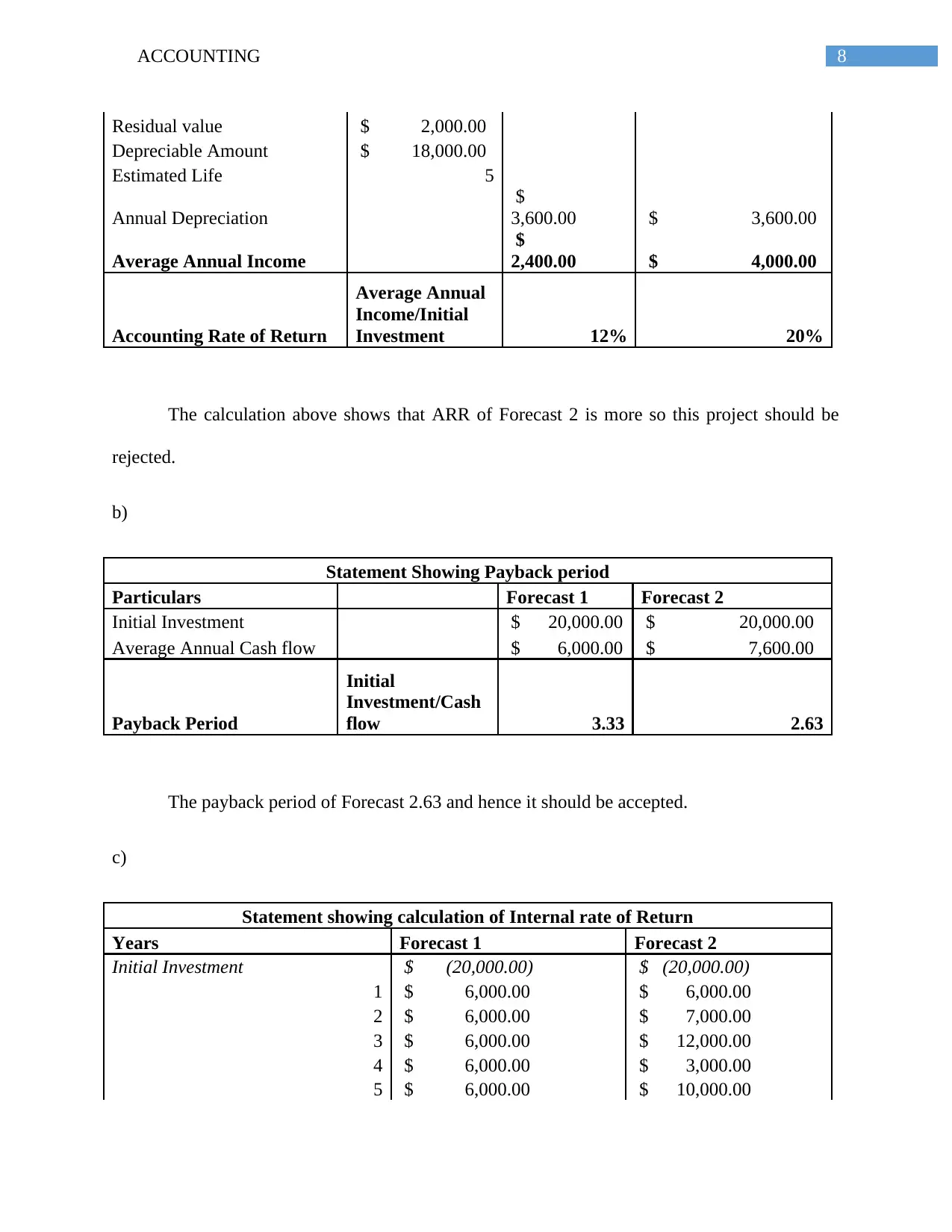

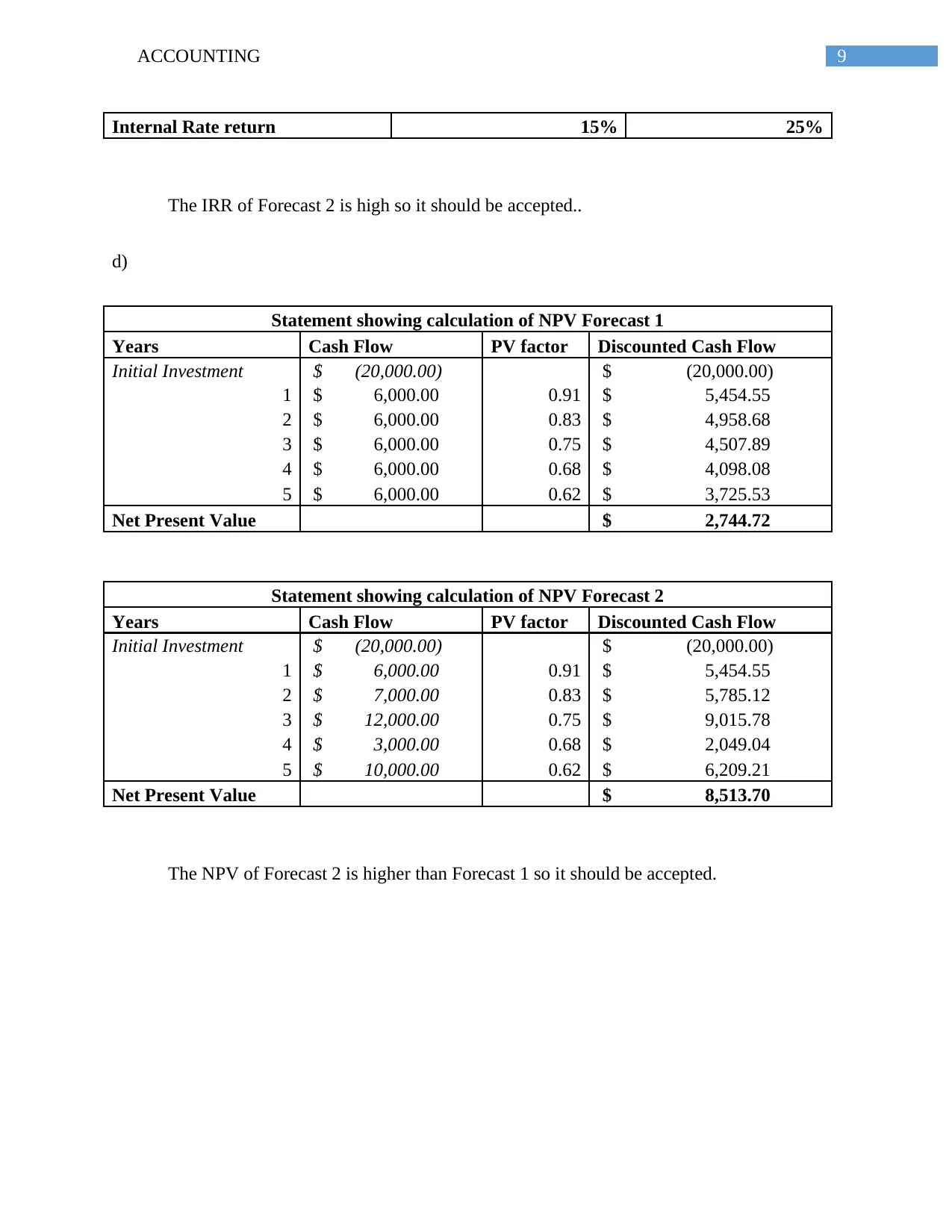

This assignment presents two financial forecasts (Forecast 1 and Forecast 2) with projected cash flows over five years. Students are tasked with calculating the Net Present Value (NPV) for each forecast using a discount rate and provided PV factors. The analysis should compare the NPVs of both forecasts and recommend the preferred forecast based on the results. The assignment emphasizes the practical application of NPV in making investment decisions.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.