Preparation of Trial Balance and Adjusting Entries in Accounting

VerifiedAdded on 2023/03/23

|15

|1937

|75

AI Summary

This article explains the process of preparing a trial balance and the importance of balancing the general ledger. It also discusses the significance of adjusting entries in reflecting the true financial position of a company. The article provides examples of different types of adjusting entries and their impact on the final accounts. Overall, it provides a comprehensive understanding of trial balance and adjusting entries in accounting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCOUNTING 1

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING 2

Contents

Step 2:.........................................................................................................................................3

Step 3:.........................................................................................................................................3

Step 4:.........................................................................................................................................4

Step 5:.........................................................................................................................................5

Step 6:.........................................................................................................................................6

Step 7:.........................................................................................................................................7

Part 1:......................................................................................................................................7

Part 2:......................................................................................................................................8

Part 3:......................................................................................................................................9

Part 4:......................................................................................................................................9

References................................................................................................................................10

Contents

Step 2:.........................................................................................................................................3

Step 3:.........................................................................................................................................3

Step 4:.........................................................................................................................................4

Step 5:.........................................................................................................................................5

Step 6:.........................................................................................................................................6

Step 7:.........................................................................................................................................7

Part 1:......................................................................................................................................7

Part 2:......................................................................................................................................8

Part 3:......................................................................................................................................9

Part 4:......................................................................................................................................9

References................................................................................................................................10

ACCOUNTING 3

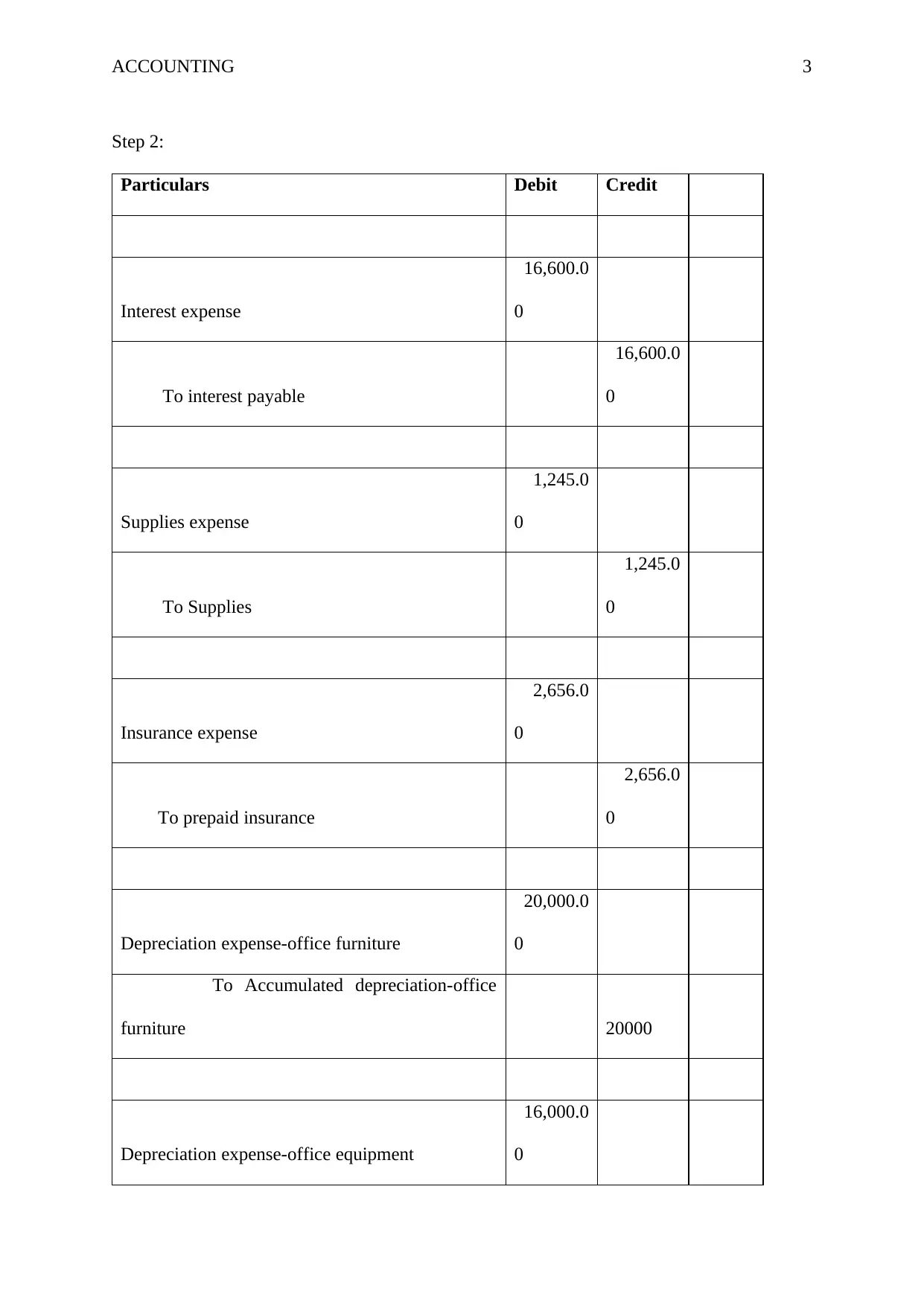

Step 2:

Particulars Debit Credit

Interest expense

16,600.0

0

To interest payable

16,600.0

0

Supplies expense

1,245.0

0

To Supplies

1,245.0

0

Insurance expense

2,656.0

0

To prepaid insurance

2,656.0

0

Depreciation expense-office furniture

20,000.0

0

To Accumulated depreciation-office

furniture 20000

Depreciation expense-office equipment

16,000.0

0

Step 2:

Particulars Debit Credit

Interest expense

16,600.0

0

To interest payable

16,600.0

0

Supplies expense

1,245.0

0

To Supplies

1,245.0

0

Insurance expense

2,656.0

0

To prepaid insurance

2,656.0

0

Depreciation expense-office furniture

20,000.0

0

To Accumulated depreciation-office

furniture 20000

Depreciation expense-office equipment

16,000.0

0

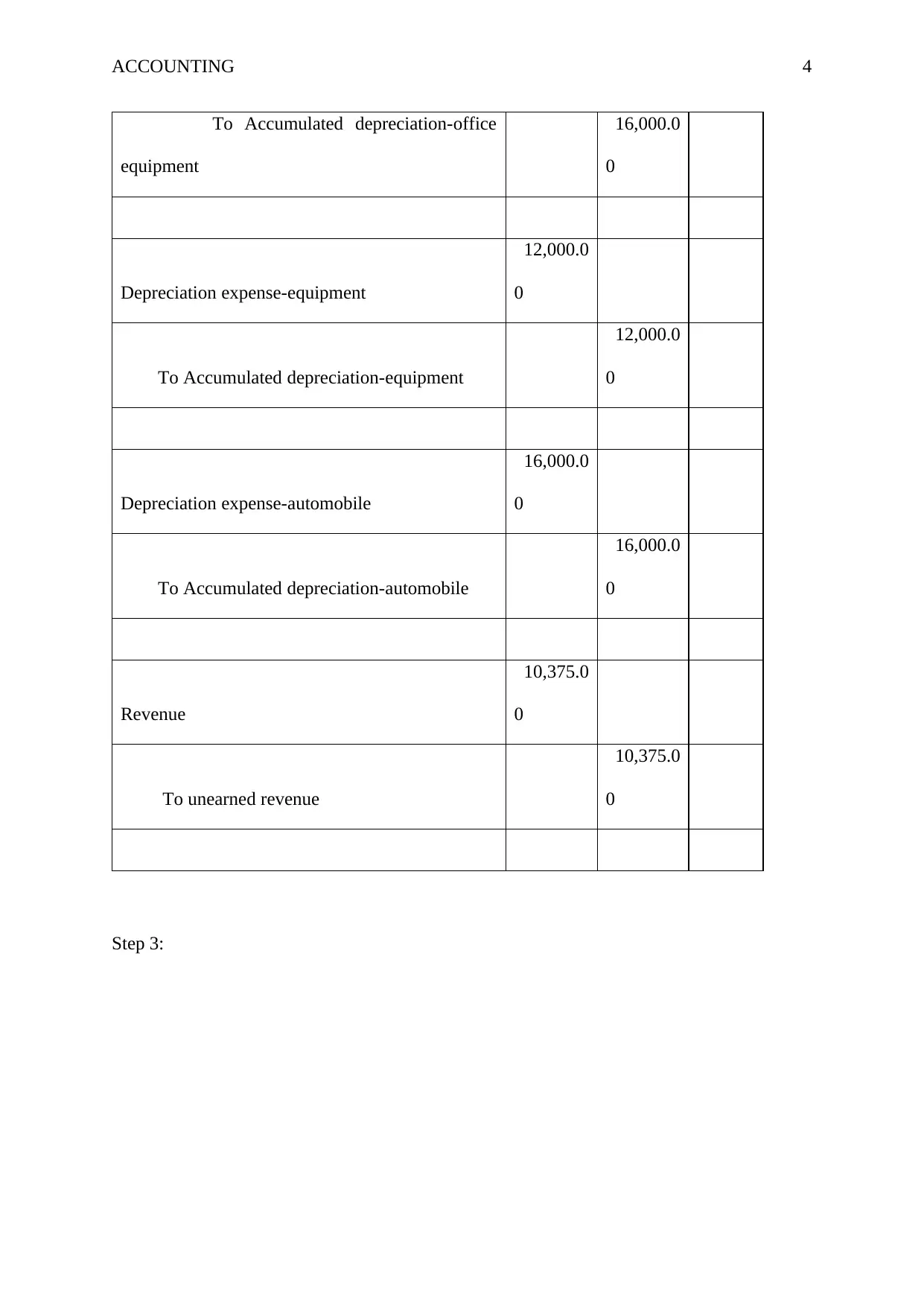

ACCOUNTING 4

To Accumulated depreciation-office

equipment

16,000.0

0

Depreciation expense-equipment

12,000.0

0

To Accumulated depreciation-equipment

12,000.0

0

Depreciation expense-automobile

16,000.0

0

To Accumulated depreciation-automobile

16,000.0

0

Revenue

10,375.0

0

To unearned revenue

10,375.0

0

Step 3:

To Accumulated depreciation-office

equipment

16,000.0

0

Depreciation expense-equipment

12,000.0

0

To Accumulated depreciation-equipment

12,000.0

0

Depreciation expense-automobile

16,000.0

0

To Accumulated depreciation-automobile

16,000.0

0

Revenue

10,375.0

0

To unearned revenue

10,375.0

0

Step 3:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING 5

Adjusted trial balance Income statement Balance Sheet

Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit

101 Cash at Bank 65,520.00 65,520.00 65,520.00

105 Accounts Receivable 21,840.00 21,840.00 21,840.00

115 Supplies 1,660.00 1,245.00 415.00 415.00

120 Prepaid Insurance 3,320.00 2,656.00 664.00 664.00

135 Office Furniture 41,500.00 41,500.00 41,500.00

137 Acc. Depreciation. - Furniture 20,000.00 20,000.00 20,000.00

140 Office Equipment 83,000.00 83,000.00 83,000.00

141 Acc. Depreciation - Equipment 16,000.00 16,000.00 16,000.00

145 Store Equipment 1,24,500.00 1,24,500.00 1,24,500.00

146 Acc. Depreciation - Equipment 12,000.00 12,000.00 12,000.00

170 Automobile 1,66,000.00 1,66,000.00 1,66,000.00

171 Acc. Depreciation - Automobile 16,000.00 16,000.00 16,000.00

201 Accounts Payable 43,680.00 43,680.00 43,680.00

201 Interest Payable 65,520.00 16,600.00 82,120.00 82,120.00

201 Unearned revenue 20,750.00 10,375.00 10,375.00 10,375.00

201 Loan Payable 8,300.00 8,300.00 8,300.00

201 Mortgage Payable 1,66,000.00 1,66,000.00 1,66,000.00

201 Paul's Capital 51,136.00 51,136.00 1,28,964.00

201 Paul's Drawings 166.00 166.00

201 Revenue 1,66,000.00 10,375.00 1,76,375.00 1,76,375.00

201 Advertising Expense 1,300.00 1,300.00 1,300.00

201 Automobile Expense 5,775.00 5,775.00 5,775.00

201 Depreciation Expense - Furniture 16,000.00 16,000.00 16,000.00

201 Depreciation Expense - Equipment 12,000.00 12,000.00 12,000.00

201 Depreciation Expense - Store Equipment 20,000.00 20,000.00 20,000.00

201 Depreciation Expense - Automobile 16,000.00 16,000.00 16,000.00

201 Insurance Expense 1,100.00 2,656.00 3,756.00 3,756.00

201 Maintenance Expense 4,550.00 4,550.00 4,550.00

201 Miscellaneous Expense 1,155.00 1,155.00 1,155.00

201 Rent Expense - -

201 Supplies Expense 1,245.00 1,245.00 1,245.00

201 Utilities Expense - -

201 Interest Expense 16,600.00 16,600.00 16,600.00

Total 5,21,386.00 5,21,386.00 94,876.00 94,876.00 6,01,986.00 6,01,986.00 98,381.00 1,76,375.00 5,03,439.00 5,03,439.00

Profit earned 77,994.00

1,76,375.00 1,76,375.00

Unadjusted trial balance Adjustment

Step 4:

Income statement

Revenue

1,76,375.0

0

Less: expenses:

Advertising Expense

1,300.

00

Automobile Expense

5,775.

00

Adjusted trial balance Income statement Balance Sheet

Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit

101 Cash at Bank 65,520.00 65,520.00 65,520.00

105 Accounts Receivable 21,840.00 21,840.00 21,840.00

115 Supplies 1,660.00 1,245.00 415.00 415.00

120 Prepaid Insurance 3,320.00 2,656.00 664.00 664.00

135 Office Furniture 41,500.00 41,500.00 41,500.00

137 Acc. Depreciation. - Furniture 20,000.00 20,000.00 20,000.00

140 Office Equipment 83,000.00 83,000.00 83,000.00

141 Acc. Depreciation - Equipment 16,000.00 16,000.00 16,000.00

145 Store Equipment 1,24,500.00 1,24,500.00 1,24,500.00

146 Acc. Depreciation - Equipment 12,000.00 12,000.00 12,000.00

170 Automobile 1,66,000.00 1,66,000.00 1,66,000.00

171 Acc. Depreciation - Automobile 16,000.00 16,000.00 16,000.00

201 Accounts Payable 43,680.00 43,680.00 43,680.00

201 Interest Payable 65,520.00 16,600.00 82,120.00 82,120.00

201 Unearned revenue 20,750.00 10,375.00 10,375.00 10,375.00

201 Loan Payable 8,300.00 8,300.00 8,300.00

201 Mortgage Payable 1,66,000.00 1,66,000.00 1,66,000.00

201 Paul's Capital 51,136.00 51,136.00 1,28,964.00

201 Paul's Drawings 166.00 166.00

201 Revenue 1,66,000.00 10,375.00 1,76,375.00 1,76,375.00

201 Advertising Expense 1,300.00 1,300.00 1,300.00

201 Automobile Expense 5,775.00 5,775.00 5,775.00

201 Depreciation Expense - Furniture 16,000.00 16,000.00 16,000.00

201 Depreciation Expense - Equipment 12,000.00 12,000.00 12,000.00

201 Depreciation Expense - Store Equipment 20,000.00 20,000.00 20,000.00

201 Depreciation Expense - Automobile 16,000.00 16,000.00 16,000.00

201 Insurance Expense 1,100.00 2,656.00 3,756.00 3,756.00

201 Maintenance Expense 4,550.00 4,550.00 4,550.00

201 Miscellaneous Expense 1,155.00 1,155.00 1,155.00

201 Rent Expense - -

201 Supplies Expense 1,245.00 1,245.00 1,245.00

201 Utilities Expense - -

201 Interest Expense 16,600.00 16,600.00 16,600.00

Total 5,21,386.00 5,21,386.00 94,876.00 94,876.00 6,01,986.00 6,01,986.00 98,381.00 1,76,375.00 5,03,439.00 5,03,439.00

Profit earned 77,994.00

1,76,375.00 1,76,375.00

Unadjusted trial balance Adjustment

Step 4:

Income statement

Revenue

1,76,375.0

0

Less: expenses:

Advertising Expense

1,300.

00

Automobile Expense

5,775.

00

ACCOUNTING 6

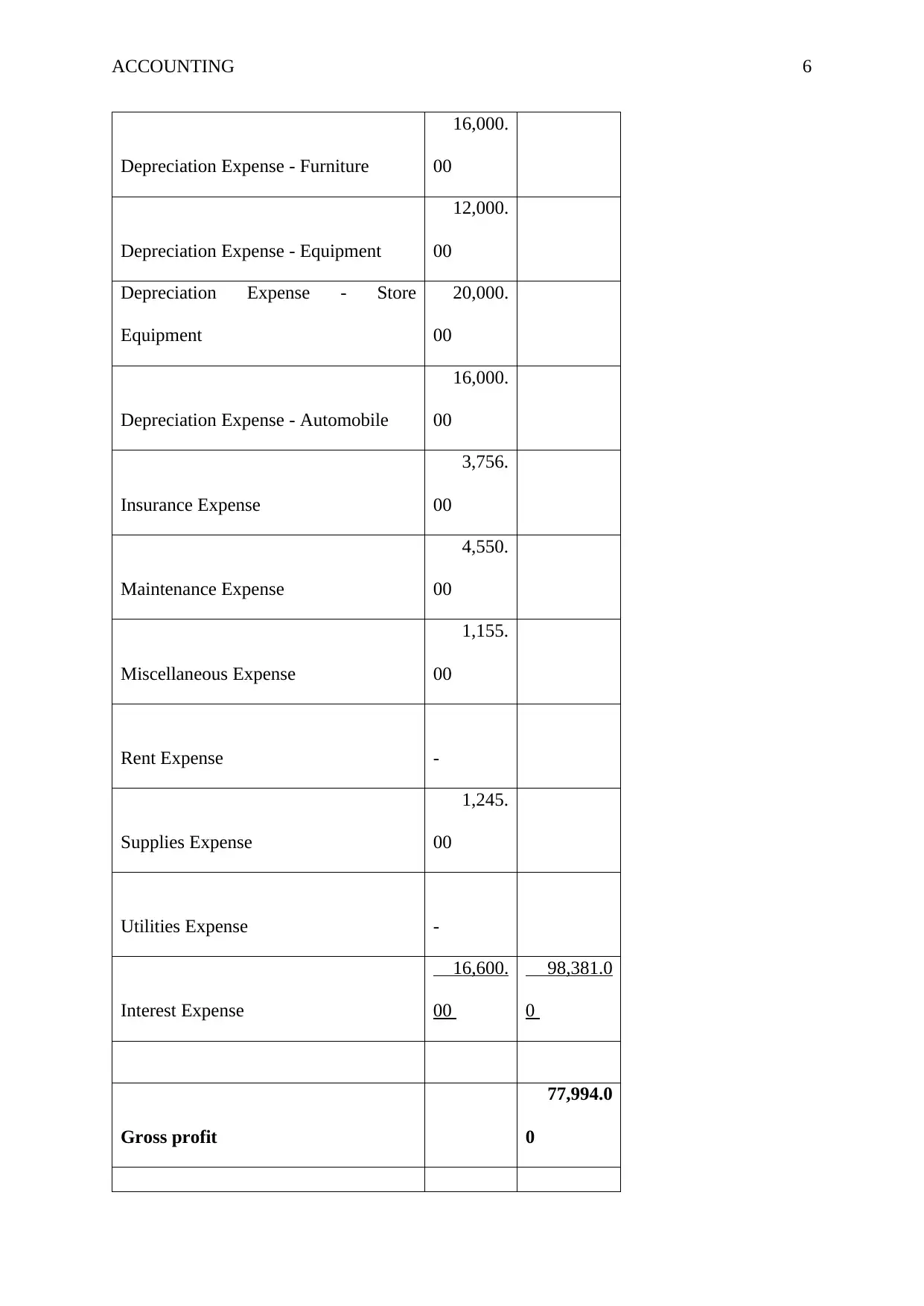

Depreciation Expense - Furniture

16,000.

00

Depreciation Expense - Equipment

12,000.

00

Depreciation Expense - Store

Equipment

20,000.

00

Depreciation Expense - Automobile

16,000.

00

Insurance Expense

3,756.

00

Maintenance Expense

4,550.

00

Miscellaneous Expense

1,155.

00

Rent Expense -

Supplies Expense

1,245.

00

Utilities Expense -

Interest Expense

16,600.

00

98,381.0

0

Gross profit

77,994.0

0

Depreciation Expense - Furniture

16,000.

00

Depreciation Expense - Equipment

12,000.

00

Depreciation Expense - Store

Equipment

20,000.

00

Depreciation Expense - Automobile

16,000.

00

Insurance Expense

3,756.

00

Maintenance Expense

4,550.

00

Miscellaneous Expense

1,155.

00

Rent Expense -

Supplies Expense

1,245.

00

Utilities Expense -

Interest Expense

16,600.

00

98,381.0

0

Gross profit

77,994.0

0

ACCOUNTING 7

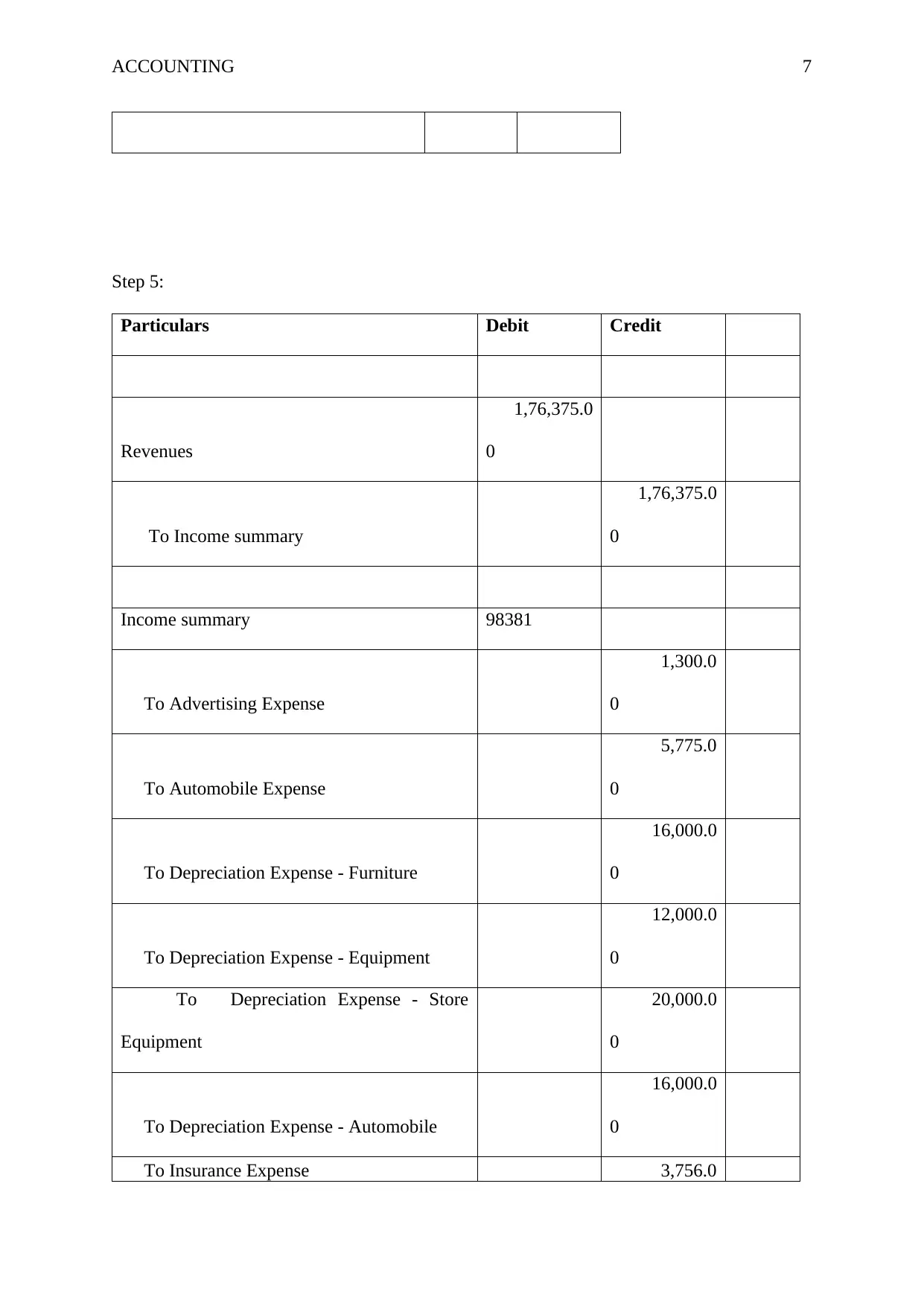

Step 5:

Particulars Debit Credit

Revenues

1,76,375.0

0

To Income summary

1,76,375.0

0

Income summary 98381

To Advertising Expense

1,300.0

0

To Automobile Expense

5,775.0

0

To Depreciation Expense - Furniture

16,000.0

0

To Depreciation Expense - Equipment

12,000.0

0

To Depreciation Expense - Store

Equipment

20,000.0

0

To Depreciation Expense - Automobile

16,000.0

0

To Insurance Expense 3,756.0

Step 5:

Particulars Debit Credit

Revenues

1,76,375.0

0

To Income summary

1,76,375.0

0

Income summary 98381

To Advertising Expense

1,300.0

0

To Automobile Expense

5,775.0

0

To Depreciation Expense - Furniture

16,000.0

0

To Depreciation Expense - Equipment

12,000.0

0

To Depreciation Expense - Store

Equipment

20,000.0

0

To Depreciation Expense - Automobile

16,000.0

0

To Insurance Expense 3,756.0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 8

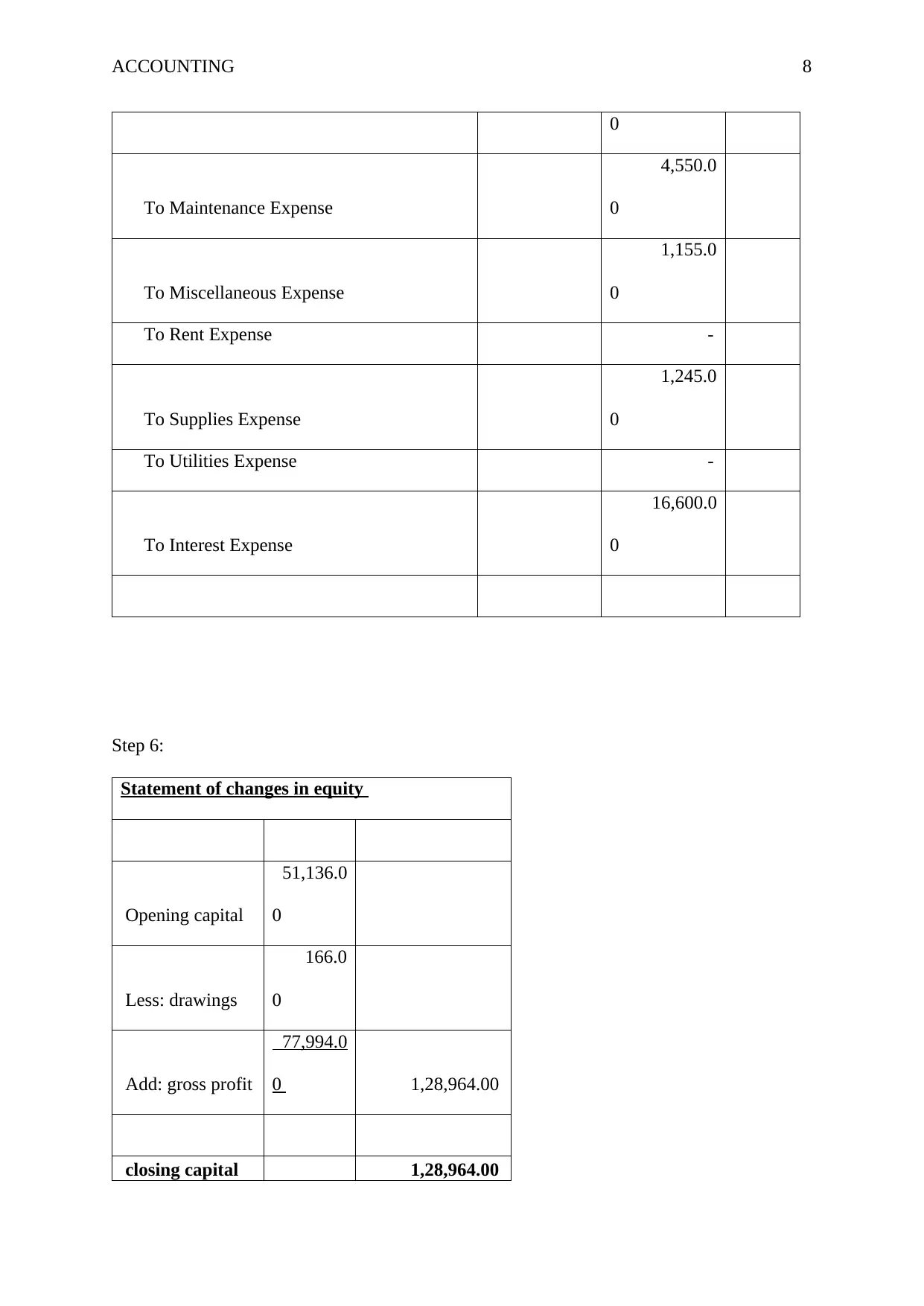

0

To Maintenance Expense

4,550.0

0

To Miscellaneous Expense

1,155.0

0

To Rent Expense -

To Supplies Expense

1,245.0

0

To Utilities Expense -

To Interest Expense

16,600.0

0

Step 6:

Statement of changes in equity

Opening capital

51,136.0

0

Less: drawings

166.0

0

Add: gross profit

77,994.0

0 1,28,964.00

closing capital 1,28,964.00

0

To Maintenance Expense

4,550.0

0

To Miscellaneous Expense

1,155.0

0

To Rent Expense -

To Supplies Expense

1,245.0

0

To Utilities Expense -

To Interest Expense

16,600.0

0

Step 6:

Statement of changes in equity

Opening capital

51,136.0

0

Less: drawings

166.0

0

Add: gross profit

77,994.0

0 1,28,964.00

closing capital 1,28,964.00

ACCOUNTING 9

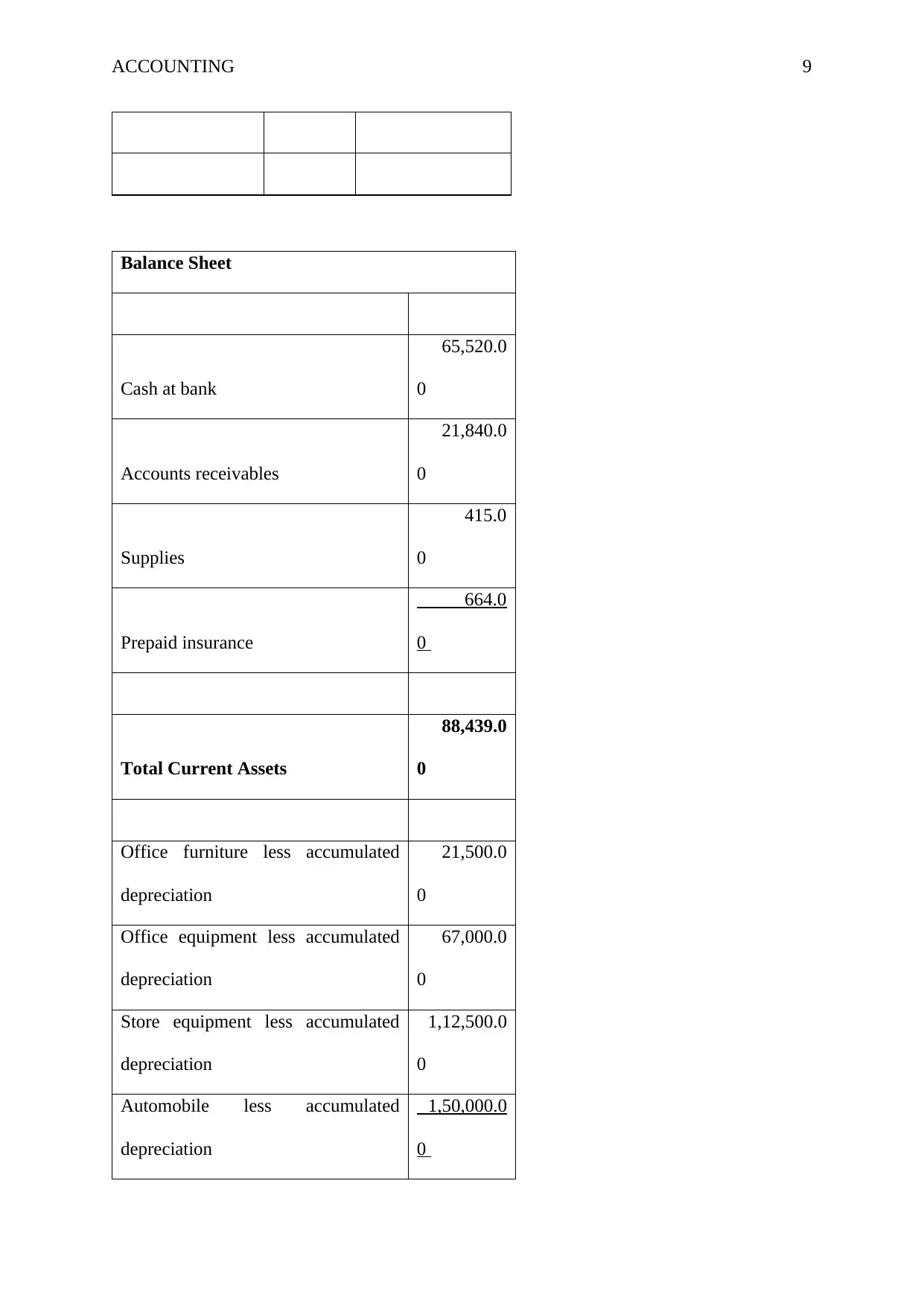

Balance Sheet

Cash at bank

65,520.0

0

Accounts receivables

21,840.0

0

Supplies

415.0

0

Prepaid insurance

664.0

0

Total Current Assets

88,439.0

0

Office furniture less accumulated

depreciation

21,500.0

0

Office equipment less accumulated

depreciation

67,000.0

0

Store equipment less accumulated

depreciation

1,12,500.0

0

Automobile less accumulated

depreciation

1,50,000.0

0

Balance Sheet

Cash at bank

65,520.0

0

Accounts receivables

21,840.0

0

Supplies

415.0

0

Prepaid insurance

664.0

0

Total Current Assets

88,439.0

0

Office furniture less accumulated

depreciation

21,500.0

0

Office equipment less accumulated

depreciation

67,000.0

0

Store equipment less accumulated

depreciation

1,12,500.0

0

Automobile less accumulated

depreciation

1,50,000.0

0

ACCOUNTING 10

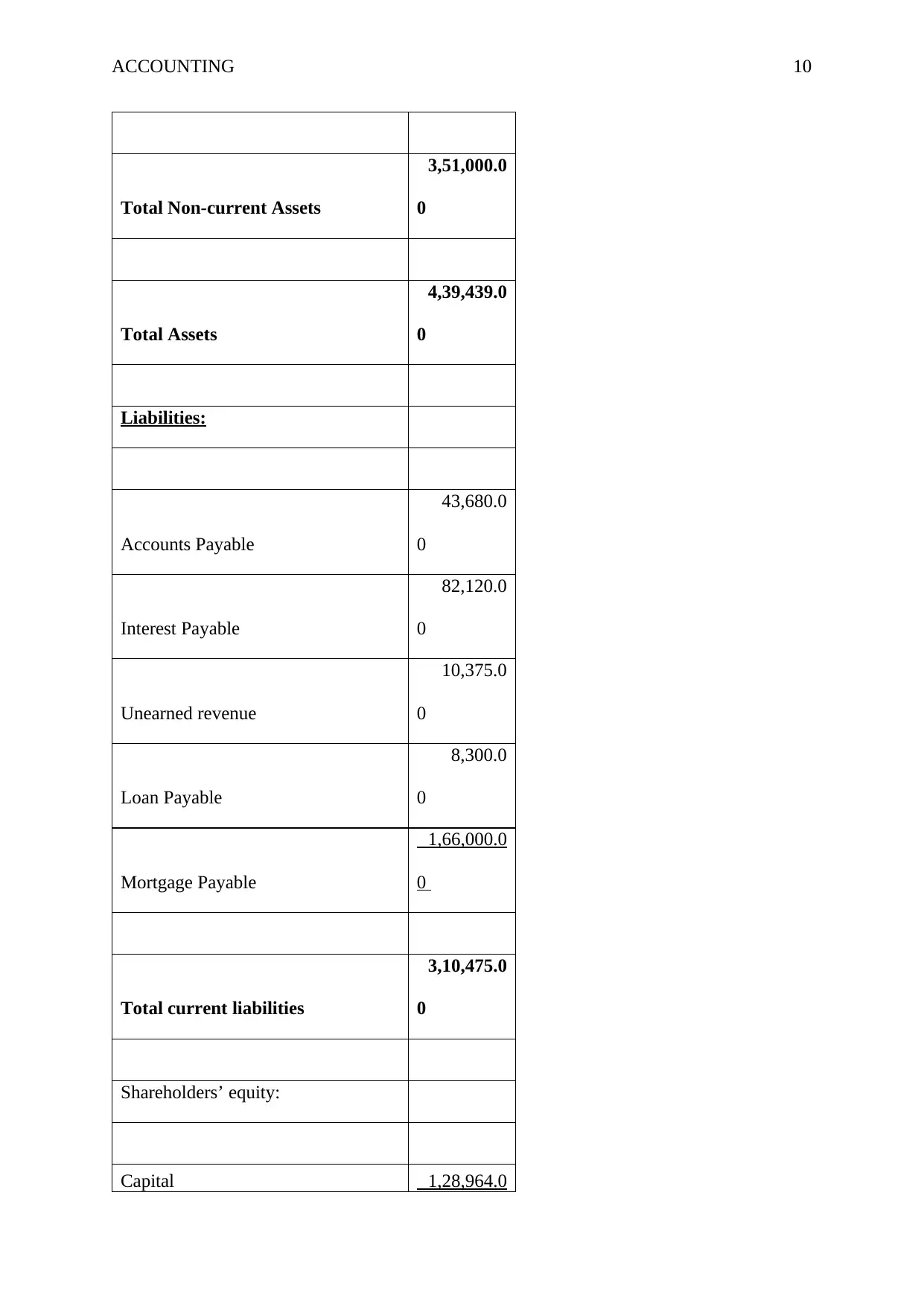

Total Non-current Assets

3,51,000.0

0

Total Assets

4,39,439.0

0

Liabilities:

Accounts Payable

43,680.0

0

Interest Payable

82,120.0

0

Unearned revenue

10,375.0

0

Loan Payable

8,300.0

0

Mortgage Payable

1,66,000.0

0

Total current liabilities

3,10,475.0

0

Shareholders’ equity:

Capital 1,28,964.0

Total Non-current Assets

3,51,000.0

0

Total Assets

4,39,439.0

0

Liabilities:

Accounts Payable

43,680.0

0

Interest Payable

82,120.0

0

Unearned revenue

10,375.0

0

Loan Payable

8,300.0

0

Mortgage Payable

1,66,000.0

0

Total current liabilities

3,10,475.0

0

Shareholders’ equity:

Capital 1,28,964.0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING 11

0

Total liabilities and shareholders’

equity

4,39,439.0

0

Step 7:

Part 1:

The main aim of the preparation of this statement is to ensure that all of the entries are

recorded successfully into the general ledger of the company. This is the list which lists

down the various balances in the balance sheet. The total amount of the dollar amounts

equal to the debit and credit in each one of the accounting entries and these amounts are

supposed to match. In case, the total amount of the debit is not equal to the credit

amount, then that merely means that the general ledger is not balanced and which also

means that there is an error. From the practical perspective, the packages of the

accounting software’s today, the users are not allowed to enter the entries that are not

balanced in GL. This means that the trial balance is not required by the companies that

use the computerised software’s for the purposes of preparing their financial statements.

In case, the business is recording the business transactions in manual manner, then the

trial balance prepared shall have no value. This is in light of the fact that financial

statements cannot be prepared using the trial balance which is not balanced. When the

financial records are maintained manually, then the trial balance is used for the purposes

0

Total liabilities and shareholders’

equity

4,39,439.0

0

Step 7:

Part 1:

The main aim of the preparation of this statement is to ensure that all of the entries are

recorded successfully into the general ledger of the company. This is the list which lists

down the various balances in the balance sheet. The total amount of the dollar amounts

equal to the debit and credit in each one of the accounting entries and these amounts are

supposed to match. In case, the total amount of the debit is not equal to the credit

amount, then that merely means that the general ledger is not balanced and which also

means that there is an error. From the practical perspective, the packages of the

accounting software’s today, the users are not allowed to enter the entries that are not

balanced in GL. This means that the trial balance is not required by the companies that

use the computerised software’s for the purposes of preparing their financial statements.

In case, the business is recording the business transactions in manual manner, then the

trial balance prepared shall have no value. This is in light of the fact that financial

statements cannot be prepared using the trial balance which is not balanced. When the

financial records are maintained manually, then the trial balance is used for the purposes

ACCOUNTING 12

of creating the final accounts. This means that the account balances have to be

aggregated manually into the line items that are contained in the final accounts.

This statement is also used by the auditors. They require this trail balance since they

have to transfer the balances of each account from this report into the desired software of

auditing. Then they use the different audit procedures for the purposes of testing these

balances (Bragg, 2019).

For the purposes of understanding this trial balance, an understanding of the double entry

system which seeks to record the entry equal and on the opposite side of the general ledger.

The second concept used is that of journal in which all of the transactions have to be recorded

in the doubt entry book keeping system and also, the ledger which includes the summary of

all of the journals that are of similar nature.

All of the business transactions that have been entered into in the month will have to be

summarised at the end of the month and be classified into the various different categorised.

Once the worksheet is prepared, then the activities are divided into the productive and the

non-productive categories. All of the business transactions are recorded through a journal

entry, each item is summarised and then classified on the basis of the ledgers. Then these

items are classified in the trial balance.

A trial balance is the sheet which records all of these ledger balances that are categorised into

debit and credit. This is a typical trial balance that would have the name of the ledger and the

various balances. This is prepared as on a particular date which is usually a financial year or a

calendar year (Clear tax, 2019).

Part 2:

of creating the final accounts. This means that the account balances have to be

aggregated manually into the line items that are contained in the final accounts.

This statement is also used by the auditors. They require this trail balance since they

have to transfer the balances of each account from this report into the desired software of

auditing. Then they use the different audit procedures for the purposes of testing these

balances (Bragg, 2019).

For the purposes of understanding this trial balance, an understanding of the double entry

system which seeks to record the entry equal and on the opposite side of the general ledger.

The second concept used is that of journal in which all of the transactions have to be recorded

in the doubt entry book keeping system and also, the ledger which includes the summary of

all of the journals that are of similar nature.

All of the business transactions that have been entered into in the month will have to be

summarised at the end of the month and be classified into the various different categorised.

Once the worksheet is prepared, then the activities are divided into the productive and the

non-productive categories. All of the business transactions are recorded through a journal

entry, each item is summarised and then classified on the basis of the ledgers. Then these

items are classified in the trial balance.

A trial balance is the sheet which records all of these ledger balances that are categorised into

debit and credit. This is a typical trial balance that would have the name of the ledger and the

various balances. This is prepared as on a particular date which is usually a financial year or a

calendar year (Clear tax, 2019).

Part 2:

ACCOUNTING 13

The main aim of preparing the adjusting entries is the fact of the updation of the accounts that

are in line with the accrual concept of accounting. There are some of the incomes and the

expenses that have not been recorded, or have been updated or have been taken up. Hence,

there is a requirement to update these in the financial statements.

In case, these adjusting entries are not prepared, then the assets, liabilities, incomes or the

expenses would not reflect the true values that would be reported in the final accounts.

Hence, these adjusting entries are of an utmost importance (Accounting verse, 2019).

There are certain types of the entries that are required to be adjusted during the period since

otherwise, the true financial facts of the company would not be indicated in the final

accounts. The examples include an accrued expense which is an expense which has been

incurred but not paid for etc. like these, there are some depreciation expense entries for which

the expense needs to be recorded as at the end of the period (Accounting coach, 2019).

Part 3:

This trial balance shows all of the debits and the credit in each account after all of the

balances have been adjusted in the final accounts. These are then posted into the respective

accounts. This is a mere internal document and is not the part of the final accounts

(Accounting coach, 2019).

Part 4:

These are the entries to adjust the financial facts contained in the final accounts. This is done

for the purposes of ensuring that the accrual basis of accounting is followed by the company.

For example, there could be a subscription of $1200 paid for 1 year, if the company prepares

the financial statements in the end of the 6 months, then this prepaid expense shall be credited

The main aim of preparing the adjusting entries is the fact of the updation of the accounts that

are in line with the accrual concept of accounting. There are some of the incomes and the

expenses that have not been recorded, or have been updated or have been taken up. Hence,

there is a requirement to update these in the financial statements.

In case, these adjusting entries are not prepared, then the assets, liabilities, incomes or the

expenses would not reflect the true values that would be reported in the final accounts.

Hence, these adjusting entries are of an utmost importance (Accounting verse, 2019).

There are certain types of the entries that are required to be adjusted during the period since

otherwise, the true financial facts of the company would not be indicated in the final

accounts. The examples include an accrued expense which is an expense which has been

incurred but not paid for etc. like these, there are some depreciation expense entries for which

the expense needs to be recorded as at the end of the period (Accounting coach, 2019).

Part 3:

This trial balance shows all of the debits and the credit in each account after all of the

balances have been adjusted in the final accounts. These are then posted into the respective

accounts. This is a mere internal document and is not the part of the final accounts

(Accounting coach, 2019).

Part 4:

These are the entries to adjust the financial facts contained in the final accounts. This is done

for the purposes of ensuring that the accrual basis of accounting is followed by the company.

For example, there could be a subscription of $1200 paid for 1 year, if the company prepares

the financial statements in the end of the 6 months, then this prepaid expense shall be credited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 14

with $600 and the balance of $600 would be recorded or be reported in the financial

statements.

The closing entries are the ones that are reported in the financial statements to close the

income and the expense accounts. These are reported in the statement of income. The net

effect of these entries must be 0. All the revenues and the expenses for the next year must

always start with 0 and then the transactions must be reported in them. Any amount of

difference in the amount of the net income and the net expenses shall be transferred to the

retained earnings account (Bayt, 2019).

References

AccountingCoach.com. (2019). What are adjusting entries? | AccountingCoach. [online]

Available at: https://www.accountingcoach.com/blog/appreciating-adjusting-entries

[Accessed 19 May 2019].

AccountingCoach.com. (2019). What is an adjusted trial balance? | AccountingCoach.

[online] Available at: https://www.accountingcoach.com/blog/what-is-an-adjusted-trial-

balance [Accessed 19 May 2019].

accountingverse.com. (2019). Types and Purpose of Adjusting Entries - AccountingVerse.

[online] Available at: https://www.accountingverse.com/accounting-basics/adjusting-entries-

introduction.html [Accessed 19 May 2019].

Bayt.com. (2019). What is the difference between adjusting entries and closing entries? -

Bayt.com Specialties. [online] Available at:

https://specialties.bayt.com/en/specialties/q/57214/what-is-the-difference-between-adjusting-

entries-and-closing-entries/ [Accessed 19 May 2019].

with $600 and the balance of $600 would be recorded or be reported in the financial

statements.

The closing entries are the ones that are reported in the financial statements to close the

income and the expense accounts. These are reported in the statement of income. The net

effect of these entries must be 0. All the revenues and the expenses for the next year must

always start with 0 and then the transactions must be reported in them. Any amount of

difference in the amount of the net income and the net expenses shall be transferred to the

retained earnings account (Bayt, 2019).

References

AccountingCoach.com. (2019). What are adjusting entries? | AccountingCoach. [online]

Available at: https://www.accountingcoach.com/blog/appreciating-adjusting-entries

[Accessed 19 May 2019].

AccountingCoach.com. (2019). What is an adjusted trial balance? | AccountingCoach.

[online] Available at: https://www.accountingcoach.com/blog/what-is-an-adjusted-trial-

balance [Accessed 19 May 2019].

accountingverse.com. (2019). Types and Purpose of Adjusting Entries - AccountingVerse.

[online] Available at: https://www.accountingverse.com/accounting-basics/adjusting-entries-

introduction.html [Accessed 19 May 2019].

Bayt.com. (2019). What is the difference between adjusting entries and closing entries? -

Bayt.com Specialties. [online] Available at:

https://specialties.bayt.com/en/specialties/q/57214/what-is-the-difference-between-adjusting-

entries-and-closing-entries/ [Accessed 19 May 2019].

ACCOUNTING 15

Bragg, S. and Bragg, S. (2019). The purpose of a trial balance. [online] AccountingTools.

Available at: https://www.accountingtools.com/articles/what-is-the-purpose-of-a-trial-

balance.html [Accessed 19 May 2019].

Cleartax.in. (2019). Trial Balance - Concept, Preparation, Advantages & Purpose. [online]

Available at: https://cleartax.in/s/trial-balance [Accessed 19 May 2019].

Bragg, S. and Bragg, S. (2019). The purpose of a trial balance. [online] AccountingTools.

Available at: https://www.accountingtools.com/articles/what-is-the-purpose-of-a-trial-

balance.html [Accessed 19 May 2019].

Cleartax.in. (2019). Trial Balance - Concept, Preparation, Advantages & Purpose. [online]

Available at: https://cleartax.in/s/trial-balance [Accessed 19 May 2019].

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.