Accounting Analysis Report: Konica Minolta Financial Statement Review

VerifiedAdded on 2022/08/26

|17

|3986

|26

Report

AI Summary

This report presents an accounting analysis of Konica Minolta's financial statements. The analysis begins with an introduction to the company, including its principal products and services, industry outlook, and key financial data such as stock price and dividend information. The core of the report focuses on the examination of the income statement, balance sheet, and cash flow statement, evaluating key financial figures and their trends. It delves into the company's accounting policies, particularly regarding revenue recognition. The report then proceeds to a financial analysis, including liquidity, profitability, and market indicator financial ratios, to assess the company's performance and financial health. The report also includes an analysis of financial risk and concludes with an overall assessment of Konica Minolta's financial position and future outlook, referencing the company's medium-term business plan and strategic goals.

Running head: ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

Accounting analysis statement of Konica Minolta

Name of the student

Name of the university

Student ID

Author note

Accounting analysis statement of Konica Minolta

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

Table of Contents

Introduction......................................................................................................................................2

Description of the company’s principal products or services..........................................................2

Industry outlook...............................................................................................................................4

Financial Statement.........................................................................................................................6

Income statement and its effects......................................................................................................7

Balance sheet...................................................................................................................................8

Cash flow statement.........................................................................................................................9

Accounting policies.........................................................................................................................9

Revenue.........................................................................................................................................10

Cash and cash equivalents.............................................................................................................11

Inventories.....................................................................................................................................11

Property, Plant and Equipment......................................................................................................11

Financial Analysis and ratios.........................................................................................................11

Financial Risk................................................................................................................................12

Market indicator financial ratios....................................................................................................13

Conclusion.....................................................................................................................................14

Reference.......................................................................................................................................14

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

Table of Contents

Introduction......................................................................................................................................2

Description of the company’s principal products or services..........................................................2

Industry outlook...............................................................................................................................4

Financial Statement.........................................................................................................................6

Income statement and its effects......................................................................................................7

Balance sheet...................................................................................................................................8

Cash flow statement.........................................................................................................................9

Accounting policies.........................................................................................................................9

Revenue.........................................................................................................................................10

Cash and cash equivalents.............................................................................................................11

Inventories.....................................................................................................................................11

Property, Plant and Equipment......................................................................................................11

Financial Analysis and ratios.........................................................................................................11

Financial Risk................................................................................................................................12

Market indicator financial ratios....................................................................................................13

Conclusion.....................................................................................................................................14

Reference.......................................................................................................................................14

2

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

Introduction

Company: Konica Minolta

Stock Code: 4902

Name of CEO: Shoei Yamana

Location of Headquarter Marunouchi, Chiyoda, Tokyo, Japan

Ending date of the last fiscal year: March 31, 2019

Description of the company’s principal products or services

The Products and services that the company can be divided into two segments that is

Healthcare Business and Industrial Business. Healthcare Business depicts product expansion,

manufacturing, sales and provisions of the diagnostic systems service. The measuring

instruments of manufacturing and sales, typical lenses for industrial and professional utilization

is came under Industrial Business. The have occupied many products and services segments like

Business solutions, Healthcare, Measuring instruments, industrial inkjet, optical products,

performance materials. These are the primary product segments of the company. Became a world

leader in the context of print industry, the company is recognized for inventive the technologies.

This business solution is also engaged to offer the office equipment, provide multi-function

printers, production printers.

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

Introduction

Company: Konica Minolta

Stock Code: 4902

Name of CEO: Shoei Yamana

Location of Headquarter Marunouchi, Chiyoda, Tokyo, Japan

Ending date of the last fiscal year: March 31, 2019

Description of the company’s principal products or services

The Products and services that the company can be divided into two segments that is

Healthcare Business and Industrial Business. Healthcare Business depicts product expansion,

manufacturing, sales and provisions of the diagnostic systems service. The measuring

instruments of manufacturing and sales, typical lenses for industrial and professional utilization

is came under Industrial Business. The have occupied many products and services segments like

Business solutions, Healthcare, Measuring instruments, industrial inkjet, optical products,

performance materials. These are the primary product segments of the company. Became a world

leader in the context of print industry, the company is recognized for inventive the technologies.

This business solution is also engaged to offer the office equipment, provide multi-function

printers, production printers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

Main geographic area of activity

The company has presences in various geographic are like Asia/ Pacific, Americas and

Europe. In Asia, the presence in Japan, China, Hong Kong, India, Korea, Malaysia. In America it

is USA, Mexico, Canada and Brazil.

Name of the independent auditor: KPMG

One of the big four KPMG has audited the company’s account and report to all the

shareholders and Board of Directors of Konica Minolta. They have audited complementary

consolidated financial statements and its consolidated subsidiaries. It involves combined

financial statements as on 31 March 2019, combined report on profit and loss, combined

statements of revenue, collective report of changes of equity and collective statement of cash

flows for the year ended and prepared key auditors note (konicaminolta.com, 2020). After

analyzing the independent auditor’s report it can be noted that the combined financial statement

are presented legitimately, the combined financial position and its combined subsidiaries

presented their combined financial performance and cash flows for the year ended 31 march

2019 are being followed by International Financial Reporting Standards (Klychova et al, 2015).

Recent price of the company’s stock: 680 JPY.

Dividend per share:

March 2019 March 2018 March 2017 March 2016 March 2015

Dividend per

share (yen)

15.0 15.0 15.0 15.0 10.0

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

Main geographic area of activity

The company has presences in various geographic are like Asia/ Pacific, Americas and

Europe. In Asia, the presence in Japan, China, Hong Kong, India, Korea, Malaysia. In America it

is USA, Mexico, Canada and Brazil.

Name of the independent auditor: KPMG

One of the big four KPMG has audited the company’s account and report to all the

shareholders and Board of Directors of Konica Minolta. They have audited complementary

consolidated financial statements and its consolidated subsidiaries. It involves combined

financial statements as on 31 March 2019, combined report on profit and loss, combined

statements of revenue, collective report of changes of equity and collective statement of cash

flows for the year ended and prepared key auditors note (konicaminolta.com, 2020). After

analyzing the independent auditor’s report it can be noted that the combined financial statement

are presented legitimately, the combined financial position and its combined subsidiaries

presented their combined financial performance and cash flows for the year ended 31 march

2019 are being followed by International Financial Reporting Standards (Klychova et al, 2015).

Recent price of the company’s stock: 680 JPY.

Dividend per share:

March 2019 March 2018 March 2017 March 2016 March 2015

Dividend per

share (yen)

15.0 15.0 15.0 15.0 10.0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

As per the current fiscal year the board of director’s meeting which was held on 13 may 2019,

company has declared dividend per share 15 JPY (konicaminolta.com, 2020).

Industry outlook

Konica Minolta, a company comes under the electronic industry. So before going to brief

about the company analysis it is required to understand the industry positions and its outlook.

The global market of electronic components has been growing very vastly over the last few

years. Behind such growth of this electronic industry, the key components are expanding of the

internet of things (IoT) and introducing the automation across various industries. On the other

hand, improvement in computerized system and increasing progress for portable devices is

pulling up the growth of the electronic industry (Ogasavara, 2014). The study also scrutinize to

the most extent based on demand and supply that increasing price of the raw materials and the

shortage of supply in electronic components are the real factor of dwindling the growth on a

scale of global economy. It is anticipated to touch USD 332.20 billion by 2020, increasing at a

CAGR of 10.57% from 2016 to 2022. Global analysis and forecast of the industry from 2018 to

2023 are as follows:

To run the key analyzing factor that has certain affect for market growth.

Thorough analysis of the market organization along with the projection of various

sectors.

To forecast the revenues of their geographical area.

To deliver the country level investigation of the marketplace with respect to the recent

market size situation.

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

As per the current fiscal year the board of director’s meeting which was held on 13 may 2019,

company has declared dividend per share 15 JPY (konicaminolta.com, 2020).

Industry outlook

Konica Minolta, a company comes under the electronic industry. So before going to brief

about the company analysis it is required to understand the industry positions and its outlook.

The global market of electronic components has been growing very vastly over the last few

years. Behind such growth of this electronic industry, the key components are expanding of the

internet of things (IoT) and introducing the automation across various industries. On the other

hand, improvement in computerized system and increasing progress for portable devices is

pulling up the growth of the electronic industry (Ogasavara, 2014). The study also scrutinize to

the most extent based on demand and supply that increasing price of the raw materials and the

shortage of supply in electronic components are the real factor of dwindling the growth on a

scale of global economy. It is anticipated to touch USD 332.20 billion by 2020, increasing at a

CAGR of 10.57% from 2016 to 2022. Global analysis and forecast of the industry from 2018 to

2023 are as follows:

To run the key analyzing factor that has certain affect for market growth.

Thorough analysis of the market organization along with the projection of various

sectors.

To forecast the revenues of their geographical area.

To deliver the country level investigation of the marketplace with respect to the recent

market size situation.

5

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

To report strategic movement for the company, comprehensive analyzing the core

abilities and economic analysis for the market.

Some findings are noted below:

As per the concern of the product segment, the integrated circuit is important in the

market to generate the highest revenue growth of USD 87.22 billion.

Consumers electronics is projected a high market growth. It is expected to reach at the

highest CAGR of 11.95% and prospective to generate high market value of USD 144.7

billion.

The study also justified in geographically that the North America hold the largest market

share in globally in the context of electronic components followed by Asia-Pacific.

This paper very critically analyses the data reported on the annual report and provide a brief

about the transformation of the business and correlate with future plans. The company wants to

take a “Medium Term Business Plan” followed by “SHINKA 2019” evolution. Keeping the

vision of the Fiscal 2021 the company wants to establish an IoT business model in a much-

digitalized manner. When the company had, a business plan called as TRANSFORM 2016 they

have achieved a return on equity of 6.1 in the year 2016 but after introducing SHINKA 2019 the

company have gained also the same ROE in 2017 as compared to previous year but their

operating profit has got increased that is 53.8 billion. Apparently, it can be said that their

SHINKA program is moderately successful because in 2018, their operating profit is 62.4 billion

but the ROE is 7.7 and they have projected 60.00 billion operating profit along with 6.7 ROE in

2019. Now the company proceeds a Medium Term Targets by 2021 where it has been projected

100.00 billion or more operating profit along with 10.00 to 11.00 ROE will come into the

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

To report strategic movement for the company, comprehensive analyzing the core

abilities and economic analysis for the market.

Some findings are noted below:

As per the concern of the product segment, the integrated circuit is important in the

market to generate the highest revenue growth of USD 87.22 billion.

Consumers electronics is projected a high market growth. It is expected to reach at the

highest CAGR of 11.95% and prospective to generate high market value of USD 144.7

billion.

The study also justified in geographically that the North America hold the largest market

share in globally in the context of electronic components followed by Asia-Pacific.

This paper very critically analyses the data reported on the annual report and provide a brief

about the transformation of the business and correlate with future plans. The company wants to

take a “Medium Term Business Plan” followed by “SHINKA 2019” evolution. Keeping the

vision of the Fiscal 2021 the company wants to establish an IoT business model in a much-

digitalized manner. When the company had, a business plan called as TRANSFORM 2016 they

have achieved a return on equity of 6.1 in the year 2016 but after introducing SHINKA 2019 the

company have gained also the same ROE in 2017 as compared to previous year but their

operating profit has got increased that is 53.8 billion. Apparently, it can be said that their

SHINKA program is moderately successful because in 2018, their operating profit is 62.4 billion

but the ROE is 7.7 and they have projected 60.00 billion operating profit along with 6.7 ROE in

2019. Now the company proceeds a Medium Term Targets by 2021 where it has been projected

100.00 billion or more operating profit along with 10.00 to 11.00 ROE will come into the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

business. In shortly if the company achieve 100.00 billion operating profit then it will get 10.00

ROE and if the company achieve more than 100.00 billion then it will get 11.00 ROE

(konicaminolta.com, 2020) The company has aimed to achieve the higher profitability for the

transformation of the business portfolio. Under the Medium Term Business Plan, SHINKA 2019

has acknowledged the business areas like Core, Growth and New. It has been summarized that

the company is trying to increase the level of profitability and what cash will generate that will

reinvest into the Growth and New Businesses. By doing this the company will transform the

business portfolio.

The management also conveyed a message to the shareholders that they have a certain aim to

become a highly profitable company with some perception to the social issues of 10 years in the

future and building up a high value added business model it can get a sustainable growth. The

company will surely improve the profitability and transform the profit structure in the fiscal 2019

by expanding the earning power of the core business and enlarging the sales in the new and

growth business (Carayannis, Sindakis & Walter, 2015).

Financial Statement

As the organization follows all the circumstances that is postulated for a “Specified

Company under Designated International Accounting Standards” as regarded in Article 1-2 of

the “Ordinance on Terminology, Forms and Preparation methods of consolidated Financial

Statements”. The company has projected the financial statements following with the

“International Financial Reporting Standards” (IFRS) as reported in Article 93 under the equal

ordinance (Tsunogaya Hellmann & Scagnelli, 2015). The study examines the company’s

financial statements, which contains “income statement”, “balance sheet” and “cash flow”.

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

business. In shortly if the company achieve 100.00 billion operating profit then it will get 10.00

ROE and if the company achieve more than 100.00 billion then it will get 11.00 ROE

(konicaminolta.com, 2020) The company has aimed to achieve the higher profitability for the

transformation of the business portfolio. Under the Medium Term Business Plan, SHINKA 2019

has acknowledged the business areas like Core, Growth and New. It has been summarized that

the company is trying to increase the level of profitability and what cash will generate that will

reinvest into the Growth and New Businesses. By doing this the company will transform the

business portfolio.

The management also conveyed a message to the shareholders that they have a certain aim to

become a highly profitable company with some perception to the social issues of 10 years in the

future and building up a high value added business model it can get a sustainable growth. The

company will surely improve the profitability and transform the profit structure in the fiscal 2019

by expanding the earning power of the core business and enlarging the sales in the new and

growth business (Carayannis, Sindakis & Walter, 2015).

Financial Statement

As the organization follows all the circumstances that is postulated for a “Specified

Company under Designated International Accounting Standards” as regarded in Article 1-2 of

the “Ordinance on Terminology, Forms and Preparation methods of consolidated Financial

Statements”. The company has projected the financial statements following with the

“International Financial Reporting Standards” (IFRS) as reported in Article 93 under the equal

ordinance (Tsunogaya Hellmann & Scagnelli, 2015). The study examines the company’s

financial statements, which contains “income statement”, “balance sheet” and “cash flow”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

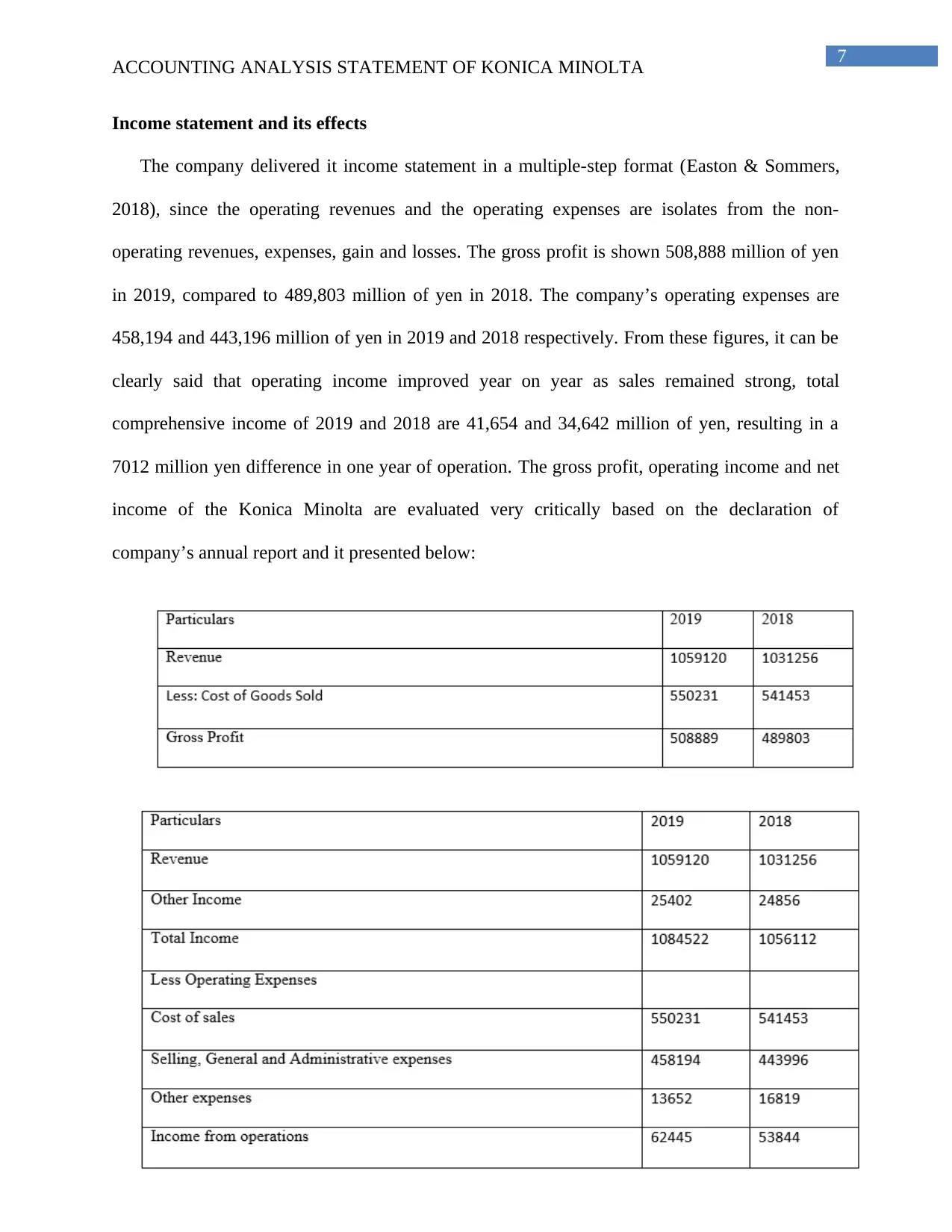

Income statement and its effects

The company delivered it income statement in a multiple-step format (Easton & Sommers,

2018), since the operating revenues and the operating expenses are isolates from the non-

operating revenues, expenses, gain and losses. The gross profit is shown 508,888 million of yen

in 2019, compared to 489,803 million of yen in 2018. The company’s operating expenses are

458,194 and 443,196 million of yen in 2019 and 2018 respectively. From these figures, it can be

clearly said that operating income improved year on year as sales remained strong, total

comprehensive income of 2019 and 2018 are 41,654 and 34,642 million of yen, resulting in a

7012 million yen difference in one year of operation. The gross profit, operating income and net

income of the Konica Minolta are evaluated very critically based on the declaration of

company’s annual report and it presented below:

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

Income statement and its effects

The company delivered it income statement in a multiple-step format (Easton & Sommers,

2018), since the operating revenues and the operating expenses are isolates from the non-

operating revenues, expenses, gain and losses. The gross profit is shown 508,888 million of yen

in 2019, compared to 489,803 million of yen in 2018. The company’s operating expenses are

458,194 and 443,196 million of yen in 2019 and 2018 respectively. From these figures, it can be

clearly said that operating income improved year on year as sales remained strong, total

comprehensive income of 2019 and 2018 are 41,654 and 34,642 million of yen, resulting in a

7012 million yen difference in one year of operation. The gross profit, operating income and net

income of the Konica Minolta are evaluated very critically based on the declaration of

company’s annual report and it presented below:

8

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

After critically evaluate the above calculation it can be suggested that Gross profit will

increase from the relevant previous year, Operating income also increase as compared to

previous year. Referring to the Net income, it also get increases from the previous year. In 2018,

last year gross profit is 489803 billion JPY and it has increased by 19086 billion. In case of

operating income, in 2018, it was 53844 and it was increased by 8601 whereas net income in last

year 32207 and it also increased by 9522 billion (konicaminolta.com, 2020).

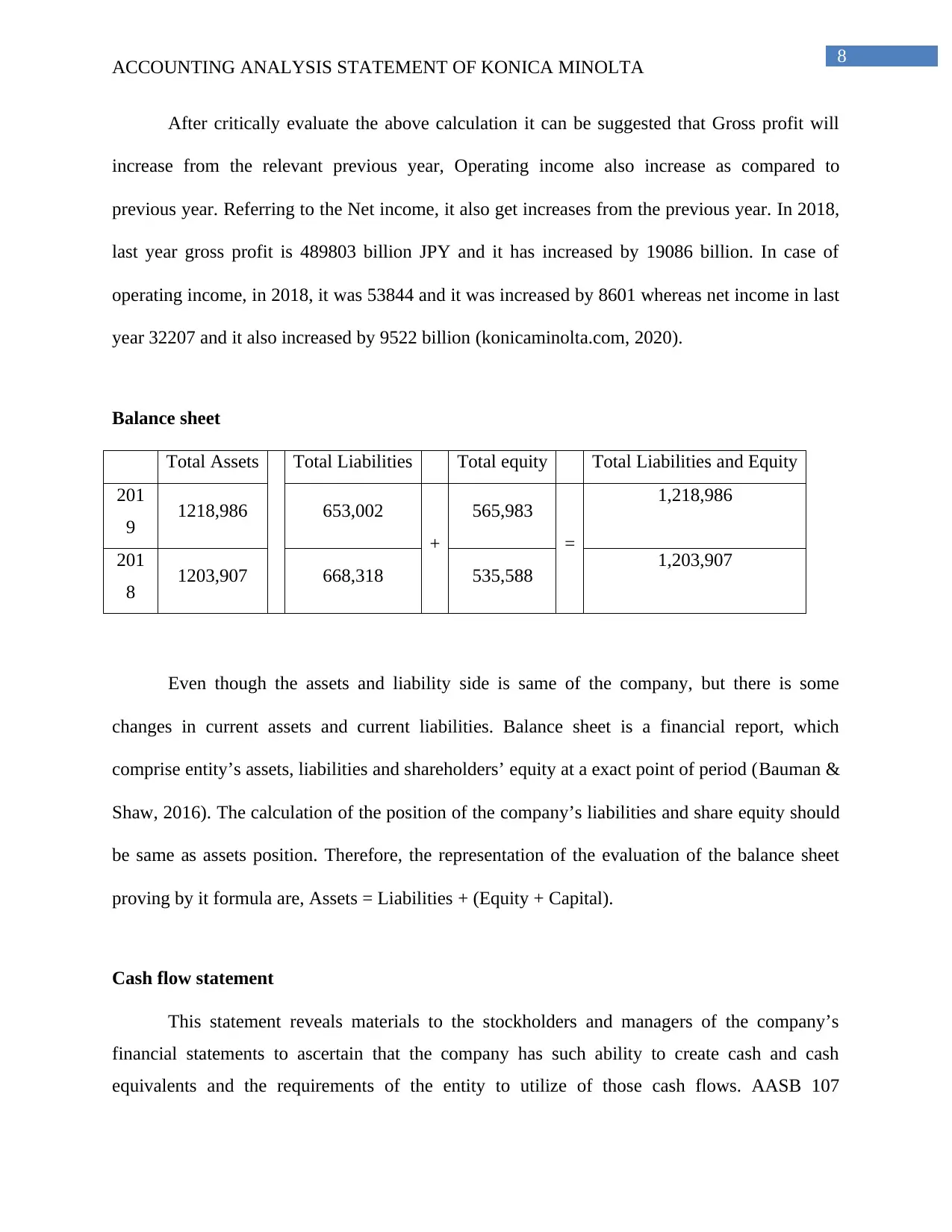

Balance sheet

Total Assets Total Liabilities Total equity Total Liabilities and Equity

201

9 1218,986 653,002

+

565,983

=

1,218,986

201

8 1203,907 668,318 535,588 1,203,907

Even though the assets and liability side is same of the company, but there is some

changes in current assets and current liabilities. Balance sheet is a financial report, which

comprise entity’s assets, liabilities and shareholders’ equity at a exact point of period (Bauman &

Shaw, 2016). The calculation of the position of the company’s liabilities and share equity should

be same as assets position. Therefore, the representation of the evaluation of the balance sheet

proving by it formula are, Assets = Liabilities + (Equity + Capital).

Cash flow statement

This statement reveals materials to the stockholders and managers of the company’s

financial statements to ascertain that the company has such ability to create cash and cash

equivalents and the requirements of the entity to utilize of those cash flows. AASB 107

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

After critically evaluate the above calculation it can be suggested that Gross profit will

increase from the relevant previous year, Operating income also increase as compared to

previous year. Referring to the Net income, it also get increases from the previous year. In 2018,

last year gross profit is 489803 billion JPY and it has increased by 19086 billion. In case of

operating income, in 2018, it was 53844 and it was increased by 8601 whereas net income in last

year 32207 and it also increased by 9522 billion (konicaminolta.com, 2020).

Balance sheet

Total Assets Total Liabilities Total equity Total Liabilities and Equity

201

9 1218,986 653,002

+

565,983

=

1,218,986

201

8 1203,907 668,318 535,588 1,203,907

Even though the assets and liability side is same of the company, but there is some

changes in current assets and current liabilities. Balance sheet is a financial report, which

comprise entity’s assets, liabilities and shareholders’ equity at a exact point of period (Bauman &

Shaw, 2016). The calculation of the position of the company’s liabilities and share equity should

be same as assets position. Therefore, the representation of the evaluation of the balance sheet

proving by it formula are, Assets = Liabilities + (Equity + Capital).

Cash flow statement

This statement reveals materials to the stockholders and managers of the company’s

financial statements to ascertain that the company has such ability to create cash and cash

equivalents and the requirements of the entity to utilize of those cash flows. AASB 107

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

represents (Yu, 2016). Konica Minolta has generated cash flow from its operating activities

57,166 million yen in 2019, 65,367 million yen in 2018. Cash flow from investing activities

(41,480) yen and (133,737) yen in 2019 and 2018 respectively. Cash flow from financing

activities (40,246) and 126,638 yen in 2019 and 2018 respectively. From the cash flow

statement, it reveals that the company has generated cash through operating activities

moderately. The source of financing activities is short-term borrowings and bonds. In 2019, short

term loans payable 11,722 million yen. In shortly company’s cash and cash equivalents has

decreased. Cash position at the end of the year is 124,830 yen.

Accounting policies

The company has implemented IFRS 15, (Oncioiu & Tănase, 2016) which was effective

from the financial year ended March 31, 2019. The organization has applied the exemption from

the reflective application as per the transitional provisions. The entity has also applied IAS 18

Revenue to comparative information (Uyar, Kılıç & Gökçen, 2016).

There is no changes in substantial accounting strategies (Bui & De Villiers, 2017) as such

to the company’s combined financial statement. The combined financial statements of the group

has been prepared based depending on the financial statements of the company, its subsidiaries,

group’s associates and joint ventures which interpreted the accounting policies regularly.

Accounting policies that the company has applied to comparative information are as follows:

Revenue

Revenue from the sales of properties in the sequence of conventional commercial

activities is calculated at the true value of the contemplation, which was received, and

receivables, deduct returns, discounts and repayments. The organization has recognized its

revenue when the group moved the significant risks to the buyer and get plunders of the

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

represents (Yu, 2016). Konica Minolta has generated cash flow from its operating activities

57,166 million yen in 2019, 65,367 million yen in 2018. Cash flow from investing activities

(41,480) yen and (133,737) yen in 2019 and 2018 respectively. Cash flow from financing

activities (40,246) and 126,638 yen in 2019 and 2018 respectively. From the cash flow

statement, it reveals that the company has generated cash through operating activities

moderately. The source of financing activities is short-term borrowings and bonds. In 2019, short

term loans payable 11,722 million yen. In shortly company’s cash and cash equivalents has

decreased. Cash position at the end of the year is 124,830 yen.

Accounting policies

The company has implemented IFRS 15, (Oncioiu & Tănase, 2016) which was effective

from the financial year ended March 31, 2019. The organization has applied the exemption from

the reflective application as per the transitional provisions. The entity has also applied IAS 18

Revenue to comparative information (Uyar, Kılıç & Gökçen, 2016).

There is no changes in substantial accounting strategies (Bui & De Villiers, 2017) as such

to the company’s combined financial statement. The combined financial statements of the group

has been prepared based depending on the financial statements of the company, its subsidiaries,

group’s associates and joint ventures which interpreted the accounting policies regularly.

Accounting policies that the company has applied to comparative information are as follows:

Revenue

Revenue from the sales of properties in the sequence of conventional commercial

activities is calculated at the true value of the contemplation, which was received, and

receivables, deduct returns, discounts and repayments. The organization has recognized its

revenue when the group moved the significant risks to the buyer and get plunders of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

ownership of the goods. Revenue generated from the selling of goods is acknowledged when

regulator of the goods are being relocated to the customers and revenue is determined at an

amount, which was mentioned in the contract to the consumers less discounts, rebates, returns

and other similar items. Revenue from providing services is acknowledged when the service is

being completed and performance compulsions is being satisfied at a point in interval (Khamis,

2016).

The organizations has recognized the revenues based on the following steps:

Identify the agreements with the consumers

Identify the performance responsibilities in the agreement

Determination of the contract price

Allocate the contract price based on the performance responsibilities in the covenant

When a performance obligation is being satisfied, revenue would be accepted.

Cash and cash equivalents

Cash and cash equivalents involves cash in hand and payments in bank that can be

withdrawn as per desirable, it refers the liquidity position of the company. It also indicates short-

term investments that are transformed into cash easily with some minute risk. It depends on the

changes in value. In 2019 cash and cash equivalents is 14660 billion, comparatively higher than

the previous year 2018 that was 11687 billion (Sankar, & Kumar, 2018).

Inventories

Following the IFRS, the inventory cost has included cost of purchases, cost of processing

and all other cost, which is related to the inventories. It is measured at net achievable value.

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

ownership of the goods. Revenue generated from the selling of goods is acknowledged when

regulator of the goods are being relocated to the customers and revenue is determined at an

amount, which was mentioned in the contract to the consumers less discounts, rebates, returns

and other similar items. Revenue from providing services is acknowledged when the service is

being completed and performance compulsions is being satisfied at a point in interval (Khamis,

2016).

The organizations has recognized the revenues based on the following steps:

Identify the agreements with the consumers

Identify the performance responsibilities in the agreement

Determination of the contract price

Allocate the contract price based on the performance responsibilities in the covenant

When a performance obligation is being satisfied, revenue would be accepted.

Cash and cash equivalents

Cash and cash equivalents involves cash in hand and payments in bank that can be

withdrawn as per desirable, it refers the liquidity position of the company. It also indicates short-

term investments that are transformed into cash easily with some minute risk. It depends on the

changes in value. In 2019 cash and cash equivalents is 14660 billion, comparatively higher than

the previous year 2018 that was 11687 billion (Sankar, & Kumar, 2018).

Inventories

Following the IFRS, the inventory cost has included cost of purchases, cost of processing

and all other cost, which is related to the inventories. It is measured at net achievable value.

11

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

Valuing the inventory the weighted average cost technique is adopted. If the net achievable value

is less than the actual price then the difference is to be accounted as write off and it will be

treated as expenses (Shin, Ennis & Spurlin, 2015).

Property, Plant and Equipment

This “property, plant and equipment” cost involves any cost directly proportionate to the

allocation that assets and dispose, subtraction, repair cost as well as cost of borrowing which is

acknowledged the capitalization of the company (Laing & Perrin, 2014).

Financial Analysis and ratios

Financial ratio analysis is a measureable method (Dalnial et al, 2014) of looking insight

into the company’s performance, liquidity, operational proficiency and productivity. It is a basic

part of the fundamental analysis.

Apparently, the company, Konica Minolta shows good performance in terms of profit in

the current fiscal year 2019. Profit is also increased from the previous year. From 32,207 to

41,729 yen.

Company’s current ratio has bit increased from the previous year. Current ratio is 2.14

and 2.13 in 2019 and 2018 respectively. It indicates a good liquidity position within the company

(Ulzanah & Murtaqi, 2015).

The working capital position of that company is higher in the current fiscal year. So the

liquidity is getting high from the previous year. 310,269 and 307,563 yen in 2019 and 2018

respectively. In other words, the company still managed to have enough current assets to meet

with its short-term liabilities (Mathuva, 2015).

ACCOUNTING ANALYSIS STATEMENT OF KONICA MINOLTA

Valuing the inventory the weighted average cost technique is adopted. If the net achievable value

is less than the actual price then the difference is to be accounted as write off and it will be

treated as expenses (Shin, Ennis & Spurlin, 2015).

Property, Plant and Equipment

This “property, plant and equipment” cost involves any cost directly proportionate to the

allocation that assets and dispose, subtraction, repair cost as well as cost of borrowing which is

acknowledged the capitalization of the company (Laing & Perrin, 2014).

Financial Analysis and ratios

Financial ratio analysis is a measureable method (Dalnial et al, 2014) of looking insight

into the company’s performance, liquidity, operational proficiency and productivity. It is a basic

part of the fundamental analysis.

Apparently, the company, Konica Minolta shows good performance in terms of profit in

the current fiscal year 2019. Profit is also increased from the previous year. From 32,207 to

41,729 yen.

Company’s current ratio has bit increased from the previous year. Current ratio is 2.14

and 2.13 in 2019 and 2018 respectively. It indicates a good liquidity position within the company

(Ulzanah & Murtaqi, 2015).

The working capital position of that company is higher in the current fiscal year. So the

liquidity is getting high from the previous year. 310,269 and 307,563 yen in 2019 and 2018

respectively. In other words, the company still managed to have enough current assets to meet

with its short-term liabilities (Mathuva, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.