Accounting and Finance: Capital Budgeting and Structure Analysis

VerifiedAdded on 2021/05/30

|17

|3217

|25

Report

AI Summary

This report is divided into two parts. Part A focuses on Saturn Pet care's capital budgeting decisions for a new product, comparing Bathurst and Wodonga sites using NPV, payback period, and profitability index. The analysis favors the Wodonga site. It also discusses product cannibalization and marketing sales trends. Part B examines ARB Ltd's capital structure, comparing it to Modine Ltd, and analyzes its WACC and cost of equity using both a general method and CAPM. Financial ratios are computed to evaluate the performance of ARB Ltd. The report suggests recommendations to improve the company's capital structure, and also discusses the wealth maximization principle.

Running head: ACCOUNTING AND FINANCE

Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING AND FINANCE

Executive Summary

The assignment has two part which are Part A and Part B. The first part of the assignment deals

with the business of Saturn Pet care which is engaged in producing products for pets. As per the

plan of the business, the company wants to introduce a new product in the market for which the

management plans to apply capital budgeting techniques. Part A of the assignment focuses on

analysis of the options which are available for the selection of the production site which are

Bathurst site and Wodonga Site. Part B of the assignment deals with the analysis of the capital

structure of ARB ltd. The assignment will also be comparing the capital structure of ARB ltd

with another company belonging to the same industry. The assignment will also suggest

recommendations so as to improve the capital structure of the company.

ACCOUNTING AND FINANCE

Executive Summary

The assignment has two part which are Part A and Part B. The first part of the assignment deals

with the business of Saturn Pet care which is engaged in producing products for pets. As per the

plan of the business, the company wants to introduce a new product in the market for which the

management plans to apply capital budgeting techniques. Part A of the assignment focuses on

analysis of the options which are available for the selection of the production site which are

Bathurst site and Wodonga Site. Part B of the assignment deals with the analysis of the capital

structure of ARB ltd. The assignment will also be comparing the capital structure of ARB ltd

with another company belonging to the same industry. The assignment will also suggest

recommendations so as to improve the capital structure of the company.

2

ACCOUNTING AND FINANCE

Table of Contents

Part A...............................................................................................................................................3

Capital Budgeting of Bathurst Site..............................................................................................3

Product Cannibalization...............................................................................................................5

Marketing Sales Trend.................................................................................................................5

Original Cost of Factory Inclusion in NPV Analysis..................................................................6

Part B...............................................................................................................................................6

Introduction..................................................................................................................................6

Discussions..................................................................................................................................6

Capital Structure and Cost of Capital..........................................................................................6

Weighted Average Cost of Capital..............................................................................................7

Cost of Equity Under CAPM Approach......................................................................................8

Comparison between ARB Ltd and Modine Ltd.........................................................................9

Financial Ratio Analysis of ARB Ltd........................................................................................10

Change in Capital Structure.......................................................................................................12

Wealth Maximization Principle.................................................................................................13

Recommendations..........................................................................................................................13

Conclusion.....................................................................................................................................14

Reference.......................................................................................................................................15

ACCOUNTING AND FINANCE

Table of Contents

Part A...............................................................................................................................................3

Capital Budgeting of Bathurst Site..............................................................................................3

Product Cannibalization...............................................................................................................5

Marketing Sales Trend.................................................................................................................5

Original Cost of Factory Inclusion in NPV Analysis..................................................................6

Part B...............................................................................................................................................6

Introduction..................................................................................................................................6

Discussions..................................................................................................................................6

Capital Structure and Cost of Capital..........................................................................................6

Weighted Average Cost of Capital..............................................................................................7

Cost of Equity Under CAPM Approach......................................................................................8

Comparison between ARB Ltd and Modine Ltd.........................................................................9

Financial Ratio Analysis of ARB Ltd........................................................................................10

Change in Capital Structure.......................................................................................................12

Wealth Maximization Principle.................................................................................................13

Recommendations..........................................................................................................................13

Conclusion.....................................................................................................................................14

Reference.......................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING AND FINANCE

Part A

Capital Budgeting of Bathurst Site

Particulars 0 1 2 3 4 5 6 7 8 9 10

Initial Investment:

Construction on Manufacturing Unit -$275,00,000

Factory Building -$80,00,000

Infrastructure Grant $25,00,000

Total Initial Investment -$330,00,000

Operational Cash Flow:

Sales Growth Rate 10% 10% 10% 10% 10% 10% 10% 10% 10%

MAC 30% 30% 30% 30% 30% 30% 30% 30% 30% 30%

Annual Sales $300,00,000 $330,00,000 $363,00,000 $399,30,000 $439,23,000 $483,15,300 $531,46,830 $584,61,513 $643,07,664 $707,38,431

Conversion Cost -$210,00,000 -$231,00,000 -$254,10,000 -$279,51,000 -$307,46,100 -$338,20,710 -$372,02,781 -$409,23,059 -$450,15,365 -$495,16,902

Rebate on Municipal Rate $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000

Depreciation on Plant & Equipment -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000

Depreciation on Building -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000

Net Profit before Tax $64,30,000 $73,30,000 $83,20,000 $94,09,000 $106,06,900 $119,24,590 $133,74,049 $149,68,454 $167,22,299 $186,51,529

Less: Income Tax @ 30% -$19,29,000 -$21,99,000 -$24,96,000 -$28,22,700 -$31,82,070 -$35,77,377 -$40,12,215 -$44,90,536 -$50,16,690 -$55,95,459

Net Profit after Tax $45,01,000 $51,31,000 $58,24,000 $65,86,300 $74,24,830 $83,47,213 $93,61,834 $104,77,918 $117,05,610 $130,56,070

Add: Depreciation on Plant $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000

Add: Depreciation on Building $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000

After-Tax Cash Flows $75,71,000 $82,01,000 $88,94,000 $96,56,300 $104,94,830 $114,17,213 $124,31,834 $135,47,918 $147,75,610 $161,26,070

Net Cash Flow -$330,00,000 $75,71,000 $82,01,000 $88,94,000 $96,56,300 $104,94,830 $114,17,213 $124,31,834 $135,47,918 $147,75,610 $161,26,070

Cumulative Cash Flow -$330,00,000 -$254,29,000 -$172,28,000 -$83,34,000 $13,22,300 $118,17,130 $232,34,343 $356,66,177 $492,14,095 $639,89,705 $801,15,775

Discount Rate 22% 22% 22% 22% 22% 22% 22% 22% 22% 22% 22%

Discounted Cash Flow -$330,00,000 $62,05,738 $55,09,944 $48,97,987 $43,58,845 $38,83,079 $34,62,590 $30,90,412 $27,60,539 $24,67,783 $22,07,650

Payback Period (in years) 3.863

Net Present Value $58,44,567

Profitability Index 1.177

Years

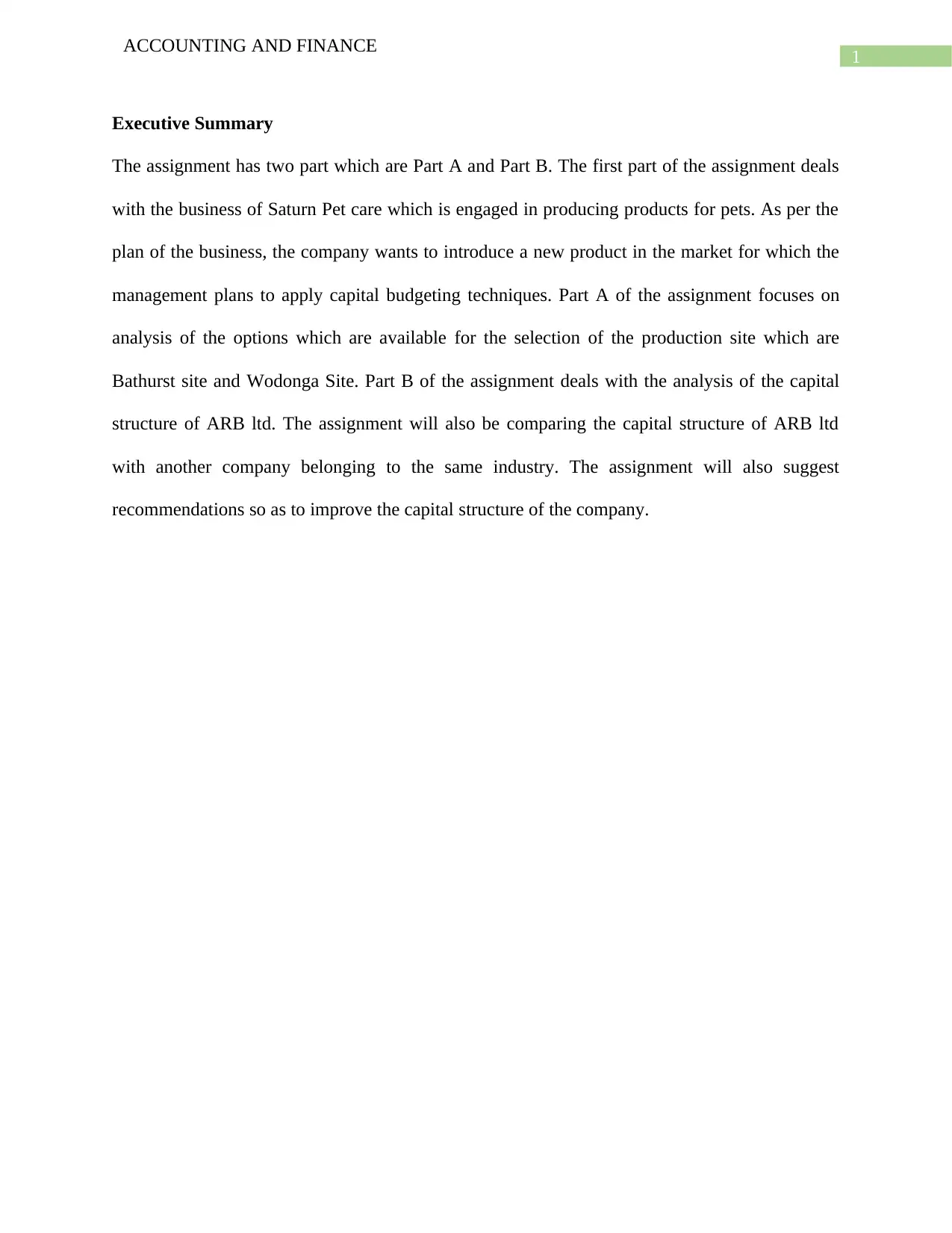

Capital Budgeting Analysis for Bathurst Site:

Figure 1: (Image Showing Capital Budgeting Techniques for Bathurst Site)

Source: (Created by Author)

ACCOUNTING AND FINANCE

Part A

Capital Budgeting of Bathurst Site

Particulars 0 1 2 3 4 5 6 7 8 9 10

Initial Investment:

Construction on Manufacturing Unit -$275,00,000

Factory Building -$80,00,000

Infrastructure Grant $25,00,000

Total Initial Investment -$330,00,000

Operational Cash Flow:

Sales Growth Rate 10% 10% 10% 10% 10% 10% 10% 10% 10%

MAC 30% 30% 30% 30% 30% 30% 30% 30% 30% 30%

Annual Sales $300,00,000 $330,00,000 $363,00,000 $399,30,000 $439,23,000 $483,15,300 $531,46,830 $584,61,513 $643,07,664 $707,38,431

Conversion Cost -$210,00,000 -$231,00,000 -$254,10,000 -$279,51,000 -$307,46,100 -$338,20,710 -$372,02,781 -$409,23,059 -$450,15,365 -$495,16,902

Rebate on Municipal Rate $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000

Depreciation on Plant & Equipment -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000

Depreciation on Building -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000

Net Profit before Tax $64,30,000 $73,30,000 $83,20,000 $94,09,000 $106,06,900 $119,24,590 $133,74,049 $149,68,454 $167,22,299 $186,51,529

Less: Income Tax @ 30% -$19,29,000 -$21,99,000 -$24,96,000 -$28,22,700 -$31,82,070 -$35,77,377 -$40,12,215 -$44,90,536 -$50,16,690 -$55,95,459

Net Profit after Tax $45,01,000 $51,31,000 $58,24,000 $65,86,300 $74,24,830 $83,47,213 $93,61,834 $104,77,918 $117,05,610 $130,56,070

Add: Depreciation on Plant $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000

Add: Depreciation on Building $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000

After-Tax Cash Flows $75,71,000 $82,01,000 $88,94,000 $96,56,300 $104,94,830 $114,17,213 $124,31,834 $135,47,918 $147,75,610 $161,26,070

Net Cash Flow -$330,00,000 $75,71,000 $82,01,000 $88,94,000 $96,56,300 $104,94,830 $114,17,213 $124,31,834 $135,47,918 $147,75,610 $161,26,070

Cumulative Cash Flow -$330,00,000 -$254,29,000 -$172,28,000 -$83,34,000 $13,22,300 $118,17,130 $232,34,343 $356,66,177 $492,14,095 $639,89,705 $801,15,775

Discount Rate 22% 22% 22% 22% 22% 22% 22% 22% 22% 22% 22%

Discounted Cash Flow -$330,00,000 $62,05,738 $55,09,944 $48,97,987 $43,58,845 $38,83,079 $34,62,590 $30,90,412 $27,60,539 $24,67,783 $22,07,650

Payback Period (in years) 3.863

Net Present Value $58,44,567

Profitability Index 1.177

Years

Capital Budgeting Analysis for Bathurst Site:

Figure 1: (Image Showing Capital Budgeting Techniques for Bathurst Site)

Source: (Created by Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING AND FINANCE

Particulars 0 1 2 3 4 5 6 7 8 9 10

Initial Investment:

Construction on Manufacturing Unit -$275,00,000

Value of Wodonga Site

Total Initial Investment -$275,00,000

Operational Cash Flow:

Sales Growth Rate 10% 10% 10% 10% 10% 10% 10% 10% 10%

MAC 30% 30% 30% 30% 30% 30% 30% 30% 30% 30%

Annual Sales $300,00,000 $330,00,000 $363,00,000 $399,30,000 $439,23,000 $483,15,300 $531,46,830 $584,61,513 $643,07,664 $707,38,431

Conversion Cost -$210,00,000 -$231,00,000 -$254,10,000 -$279,51,000 -$307,46,100 -$338,20,710 -$372,02,781 -$409,23,059 -$450,15,365 -$495,16,902

Depreciation on Plant & Equipment -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000

Depreciation on Building $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

Net Profit before Tax $62,50,000 $71,50,000 $81,40,000 $92,29,000 $104,26,900 $117,44,590 $131,94,049 $147,88,454 $165,42,299 $184,71,529

Less: Income Tax @ 30% -$18,75,000 -$21,45,000 -$24,42,000 -$27,68,700 -$31,28,070 -$35,23,377 -$39,58,215 -$44,36,536 -$49,62,690 -$55,41,459

Net Profit after Tax $43,75,000 $50,05,000 $56,98,000 $64,60,300 $72,98,830 $82,21,213 $92,35,834 $103,51,918 $115,79,610 $129,30,070

Add: Depreciation on Plant $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000

Add: Depreciation on Building $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

After-Tax Cash Flows $71,25,000 $77,55,000 $84,48,000 $92,10,300 $100,48,830 $109,71,213 $119,85,834 $131,01,918 $143,29,610 $156,80,070

Net Cash Flow -$275,00,000 $71,25,000 $77,55,000 $84,48,000 $92,10,300 $100,48,830 $109,71,213 $119,85,834 $131,01,918 $143,29,610 $156,80,070

Cumulative Cash Flow -$275,00,000 -$203,75,000 -$126,20,000 -$41,72,000 $50,38,300 $150,87,130 $260,58,343 $380,44,177 $511,46,095 $654,75,705 $811,55,775

Discount Rate 22% 22% 22% 22% 22% 22% 22% 22% 22% 22% 22%

Discounted Cash Flow -$275,00,000 $58,40,164 $52,10,293 $46,52,372 $41,57,521 $37,18,060 $33,27,328 $29,79,542 $26,69,662 $23,93,293 $21,46,593

Payback Period (in years) 3.453

Net Present Value $95,94,827

Profitability Index 1.349

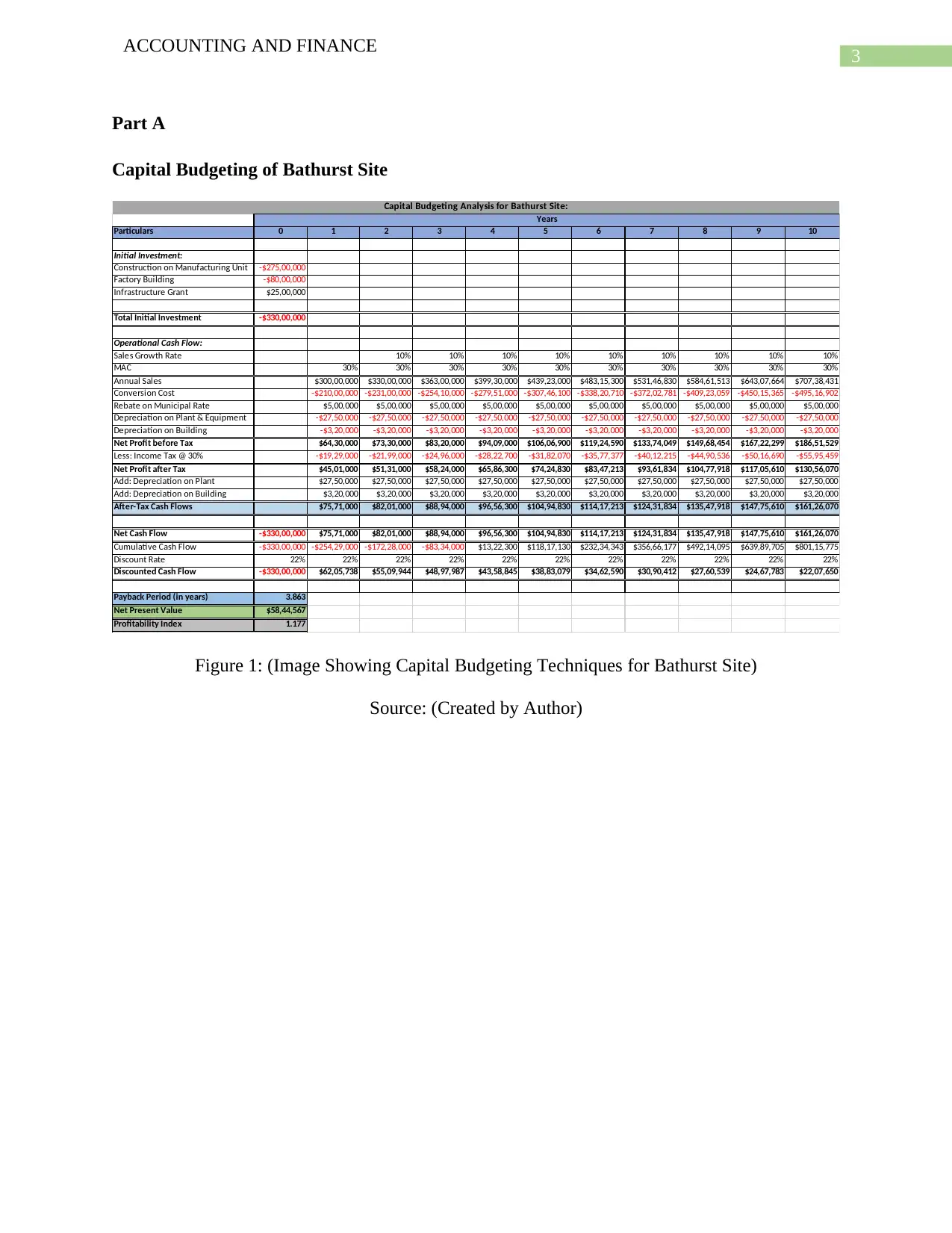

Capital Budgeting Analysis for Wodonga Site:

Years

Figure 2: (Image Showing Capital Budgeting Techniques for Wodonga Site)

Source: (Created by Author)

The first part of the assignment will be focusing on the business of Saturn Pet care which

is planning to launch a new product in the market. The business is planning to set a production

process for the new product for which the business has two possible production option which are

Bathurst site and Wodonga site. The first part will be applying capital budgeting techniques

which applies techniques like NPV analysis, Payback period and Profitability Index (Burns &

Walker, 2015).

From the analysis of the capital budgeting results of both the sites, it is clear that the best

option for the business to undertake the production of the new product is Wodonga site. The Net

Present Value (NPV) of Wodonga site is shown at $ 95,94,827 which is much more than the

NPV results of Bathurst site which is shown as $ 58,44,567. The results signify that the

profitability of Wodonga site is much more than Bathurst site. In addition to this, the expected

ACCOUNTING AND FINANCE

Particulars 0 1 2 3 4 5 6 7 8 9 10

Initial Investment:

Construction on Manufacturing Unit -$275,00,000

Value of Wodonga Site

Total Initial Investment -$275,00,000

Operational Cash Flow:

Sales Growth Rate 10% 10% 10% 10% 10% 10% 10% 10% 10%

MAC 30% 30% 30% 30% 30% 30% 30% 30% 30% 30%

Annual Sales $300,00,000 $330,00,000 $363,00,000 $399,30,000 $439,23,000 $483,15,300 $531,46,830 $584,61,513 $643,07,664 $707,38,431

Conversion Cost -$210,00,000 -$231,00,000 -$254,10,000 -$279,51,000 -$307,46,100 -$338,20,710 -$372,02,781 -$409,23,059 -$450,15,365 -$495,16,902

Depreciation on Plant & Equipment -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000

Depreciation on Building $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

Net Profit before Tax $62,50,000 $71,50,000 $81,40,000 $92,29,000 $104,26,900 $117,44,590 $131,94,049 $147,88,454 $165,42,299 $184,71,529

Less: Income Tax @ 30% -$18,75,000 -$21,45,000 -$24,42,000 -$27,68,700 -$31,28,070 -$35,23,377 -$39,58,215 -$44,36,536 -$49,62,690 -$55,41,459

Net Profit after Tax $43,75,000 $50,05,000 $56,98,000 $64,60,300 $72,98,830 $82,21,213 $92,35,834 $103,51,918 $115,79,610 $129,30,070

Add: Depreciation on Plant $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000

Add: Depreciation on Building $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

After-Tax Cash Flows $71,25,000 $77,55,000 $84,48,000 $92,10,300 $100,48,830 $109,71,213 $119,85,834 $131,01,918 $143,29,610 $156,80,070

Net Cash Flow -$275,00,000 $71,25,000 $77,55,000 $84,48,000 $92,10,300 $100,48,830 $109,71,213 $119,85,834 $131,01,918 $143,29,610 $156,80,070

Cumulative Cash Flow -$275,00,000 -$203,75,000 -$126,20,000 -$41,72,000 $50,38,300 $150,87,130 $260,58,343 $380,44,177 $511,46,095 $654,75,705 $811,55,775

Discount Rate 22% 22% 22% 22% 22% 22% 22% 22% 22% 22% 22%

Discounted Cash Flow -$275,00,000 $58,40,164 $52,10,293 $46,52,372 $41,57,521 $37,18,060 $33,27,328 $29,79,542 $26,69,662 $23,93,293 $21,46,593

Payback Period (in years) 3.453

Net Present Value $95,94,827

Profitability Index 1.349

Capital Budgeting Analysis for Wodonga Site:

Years

Figure 2: (Image Showing Capital Budgeting Techniques for Wodonga Site)

Source: (Created by Author)

The first part of the assignment will be focusing on the business of Saturn Pet care which

is planning to launch a new product in the market. The business is planning to set a production

process for the new product for which the business has two possible production option which are

Bathurst site and Wodonga site. The first part will be applying capital budgeting techniques

which applies techniques like NPV analysis, Payback period and Profitability Index (Burns &

Walker, 2015).

From the analysis of the capital budgeting results of both the sites, it is clear that the best

option for the business to undertake the production of the new product is Wodonga site. The Net

Present Value (NPV) of Wodonga site is shown at $ 95,94,827 which is much more than the

NPV results of Bathurst site which is shown as $ 58,44,567. The results signify that the

profitability of Wodonga site is much more than Bathurst site. In addition to this, the expected

5

ACCOUNTING AND FINANCE

cash inflow from Wodonga site is much more than the expected cash inflow from Bathurst site.

The profitability index of Wodonga site also proves that the profitability of the same is more than

the Bathurst site. The profitability index of Wodonga site is 1.349 and the profitability index of

Bathurst site is shown as 1.177. The payback period of Wodonga site is lesser than payback

period of Bathurst site. This suggests that Wodonga site is able to recover the initial investment

on the project much quicker than Bathurst site. Thus, from the discussion, it is clear that

Wodonga site is the clear choice for the Saturn Pet care.

Product Cannibalization

Product Cannibalization refers to the strategy which is adopted by companies in which a

sales price and sales volume of a product is reduced so as to facilitate a business to introduce a

new product in the market (Barroso & Giarratana, 2013). This strategy is followed by businesses

when the business is trying to promote a new product in the market. In the case of Saturn Pet

care, there is a possibility the management is following this strategy in order to promote the new

product in the market. The purpose of using Product Cannibalization is to establish a product in

the market for the purpose of sales maximization.

Marketing Sales Trend

One of the directors of the company Nathan is of the opinion that the company is of the

opinion the sales which is estimated by the marketing department is in excess and therefore the

director is of the view that this might affect the capital budgeting analysis. The management

needs to rectify such an error in estimation as this will affect the planning process and also this is

unrealistic. The management can use NPV method in which the cash outflows can be increased

so as to neutralize the error in estimation of sales.

ACCOUNTING AND FINANCE

cash inflow from Wodonga site is much more than the expected cash inflow from Bathurst site.

The profitability index of Wodonga site also proves that the profitability of the same is more than

the Bathurst site. The profitability index of Wodonga site is 1.349 and the profitability index of

Bathurst site is shown as 1.177. The payback period of Wodonga site is lesser than payback

period of Bathurst site. This suggests that Wodonga site is able to recover the initial investment

on the project much quicker than Bathurst site. Thus, from the discussion, it is clear that

Wodonga site is the clear choice for the Saturn Pet care.

Product Cannibalization

Product Cannibalization refers to the strategy which is adopted by companies in which a

sales price and sales volume of a product is reduced so as to facilitate a business to introduce a

new product in the market (Barroso & Giarratana, 2013). This strategy is followed by businesses

when the business is trying to promote a new product in the market. In the case of Saturn Pet

care, there is a possibility the management is following this strategy in order to promote the new

product in the market. The purpose of using Product Cannibalization is to establish a product in

the market for the purpose of sales maximization.

Marketing Sales Trend

One of the directors of the company Nathan is of the opinion that the company is of the

opinion the sales which is estimated by the marketing department is in excess and therefore the

director is of the view that this might affect the capital budgeting analysis. The management

needs to rectify such an error in estimation as this will affect the planning process and also this is

unrealistic. The management can use NPV method in which the cash outflows can be increased

so as to neutralize the error in estimation of sales.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING AND FINANCE

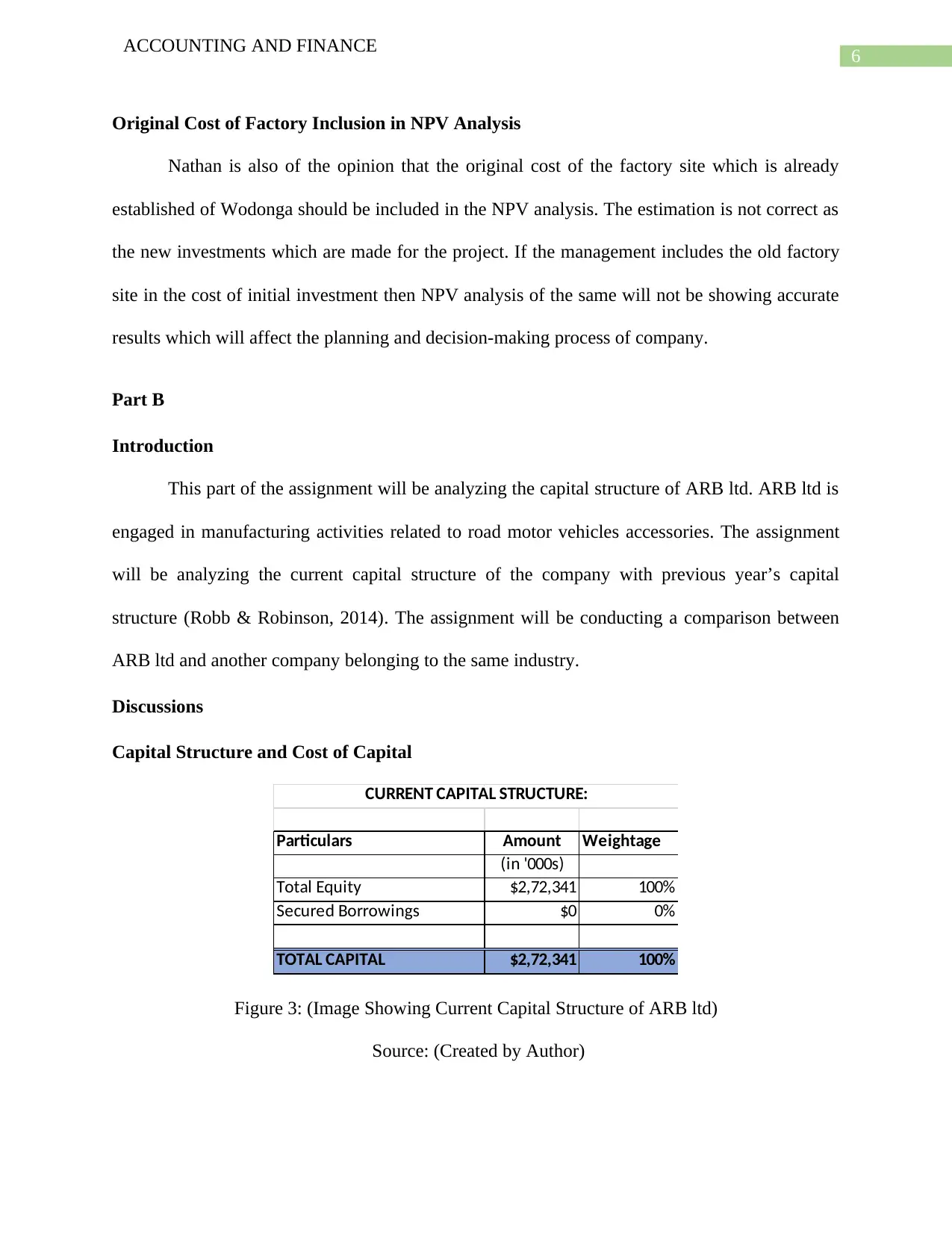

Original Cost of Factory Inclusion in NPV Analysis

Nathan is also of the opinion that the original cost of the factory site which is already

established of Wodonga should be included in the NPV analysis. The estimation is not correct as

the new investments which are made for the project. If the management includes the old factory

site in the cost of initial investment then NPV analysis of the same will not be showing accurate

results which will affect the planning and decision-making process of company.

Part B

Introduction

This part of the assignment will be analyzing the capital structure of ARB ltd. ARB ltd is

engaged in manufacturing activities related to road motor vehicles accessories. The assignment

will be analyzing the current capital structure of the company with previous year’s capital

structure (Robb & Robinson, 2014). The assignment will be conducting a comparison between

ARB ltd and another company belonging to the same industry.

Discussions

Capital Structure and Cost of Capital

Particulars Amount Weightage

(in '000s)

Total Equity $2,72,341 100%

Secured Borrowings $0 0%

TOTAL CAPITAL $2,72,341 100%

CURRENT CAPITAL STRUCTURE:

Figure 3: (Image Showing Current Capital Structure of ARB ltd)

Source: (Created by Author)

ACCOUNTING AND FINANCE

Original Cost of Factory Inclusion in NPV Analysis

Nathan is also of the opinion that the original cost of the factory site which is already

established of Wodonga should be included in the NPV analysis. The estimation is not correct as

the new investments which are made for the project. If the management includes the old factory

site in the cost of initial investment then NPV analysis of the same will not be showing accurate

results which will affect the planning and decision-making process of company.

Part B

Introduction

This part of the assignment will be analyzing the capital structure of ARB ltd. ARB ltd is

engaged in manufacturing activities related to road motor vehicles accessories. The assignment

will be analyzing the current capital structure of the company with previous year’s capital

structure (Robb & Robinson, 2014). The assignment will be conducting a comparison between

ARB ltd and another company belonging to the same industry.

Discussions

Capital Structure and Cost of Capital

Particulars Amount Weightage

(in '000s)

Total Equity $2,72,341 100%

Secured Borrowings $0 0%

TOTAL CAPITAL $2,72,341 100%

CURRENT CAPITAL STRUCTURE:

Figure 3: (Image Showing Current Capital Structure of ARB ltd)

Source: (Created by Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING AND FINANCE

The current capital structure which is used by ARB ltd comprises of only equity share

capital and there is no presence of debt capital in the capital mix of the company (Hasan et al.,

2014). This shows that the company is solely dependent on the equity-based capital and does not

rely on any leverage. The capital structure of the company is shown in figure 3 which is around $

2,72,341. The company finances all the operations of the business using this capital.

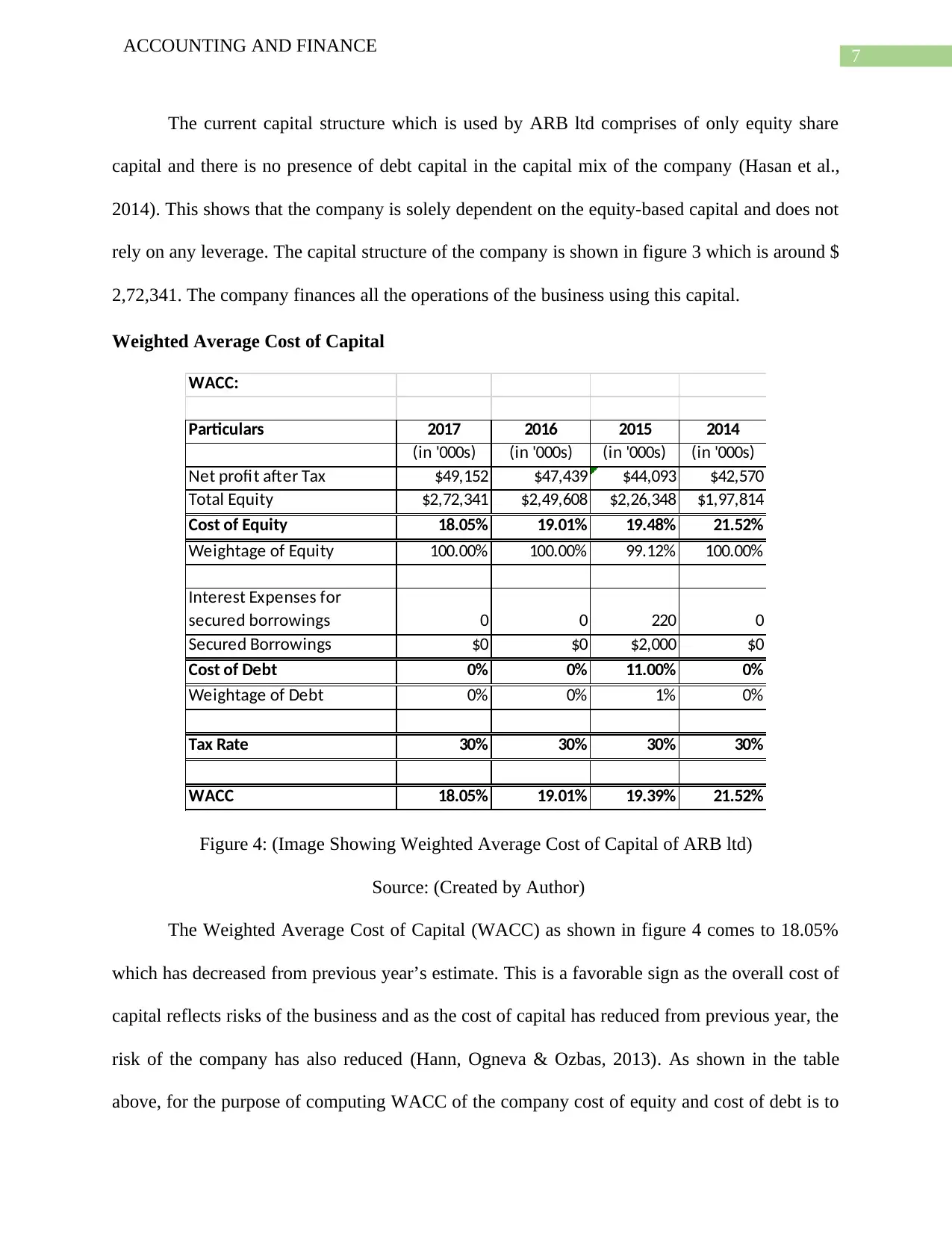

Weighted Average Cost of Capital

WACC:

Particulars 2017 2016 2015 2014

(in '000s) (in '000s) (in '000s) (in '000s)

Net profit after Tax $49,152 $47,439 $44,093 $42,570

Total Equity $2,72,341 $2,49,608 $2,26,348 $1,97,814

Cost of Equity 18.05% 19.01% 19.48% 21.52%

Weightage of Equity 100.00% 100.00% 99.12% 100.00%

Interest Expenses for

secured borrowings 0 0 220 0

Secured Borrowings $0 $0 $2,000 $0

Cost of Debt 0% 0% 11.00% 0%

Weightage of Debt 0% 0% 1% 0%

Tax Rate 30% 30% 30% 30%

WACC 18.05% 19.01% 19.39% 21.52%

Figure 4: (Image Showing Weighted Average Cost of Capital of ARB ltd)

Source: (Created by Author)

The Weighted Average Cost of Capital (WACC) as shown in figure 4 comes to 18.05%

which has decreased from previous year’s estimate. This is a favorable sign as the overall cost of

capital reflects risks of the business and as the cost of capital has reduced from previous year, the

risk of the company has also reduced (Hann, Ogneva & Ozbas, 2013). As shown in the table

above, for the purpose of computing WACC of the company cost of equity and cost of debt is to

ACCOUNTING AND FINANCE

The current capital structure which is used by ARB ltd comprises of only equity share

capital and there is no presence of debt capital in the capital mix of the company (Hasan et al.,

2014). This shows that the company is solely dependent on the equity-based capital and does not

rely on any leverage. The capital structure of the company is shown in figure 3 which is around $

2,72,341. The company finances all the operations of the business using this capital.

Weighted Average Cost of Capital

WACC:

Particulars 2017 2016 2015 2014

(in '000s) (in '000s) (in '000s) (in '000s)

Net profit after Tax $49,152 $47,439 $44,093 $42,570

Total Equity $2,72,341 $2,49,608 $2,26,348 $1,97,814

Cost of Equity 18.05% 19.01% 19.48% 21.52%

Weightage of Equity 100.00% 100.00% 99.12% 100.00%

Interest Expenses for

secured borrowings 0 0 220 0

Secured Borrowings $0 $0 $2,000 $0

Cost of Debt 0% 0% 11.00% 0%

Weightage of Debt 0% 0% 1% 0%

Tax Rate 30% 30% 30% 30%

WACC 18.05% 19.01% 19.39% 21.52%

Figure 4: (Image Showing Weighted Average Cost of Capital of ARB ltd)

Source: (Created by Author)

The Weighted Average Cost of Capital (WACC) as shown in figure 4 comes to 18.05%

which has decreased from previous year’s estimate. This is a favorable sign as the overall cost of

capital reflects risks of the business and as the cost of capital has reduced from previous year, the

risk of the company has also reduced (Hann, Ogneva & Ozbas, 2013). As shown in the table

above, for the purpose of computing WACC of the company cost of equity and cost of debt is to

8

ACCOUNTING AND FINANCE

be considered as well as the tax rate which is applicable on the company is also to be considered.

In this case as the company does not have any debt capital in the capital structure of the business

therefore the cost of debt will be zero (Cheynel, 2013). The cost of equity of ARB Ltd which is

computed following the general method comes to about 18.05%. as the equity capital forms

100% of the capital structure of ARB Ltd, hence the cost of equity will be the overall cost of

capital of the business which is 18.05%.

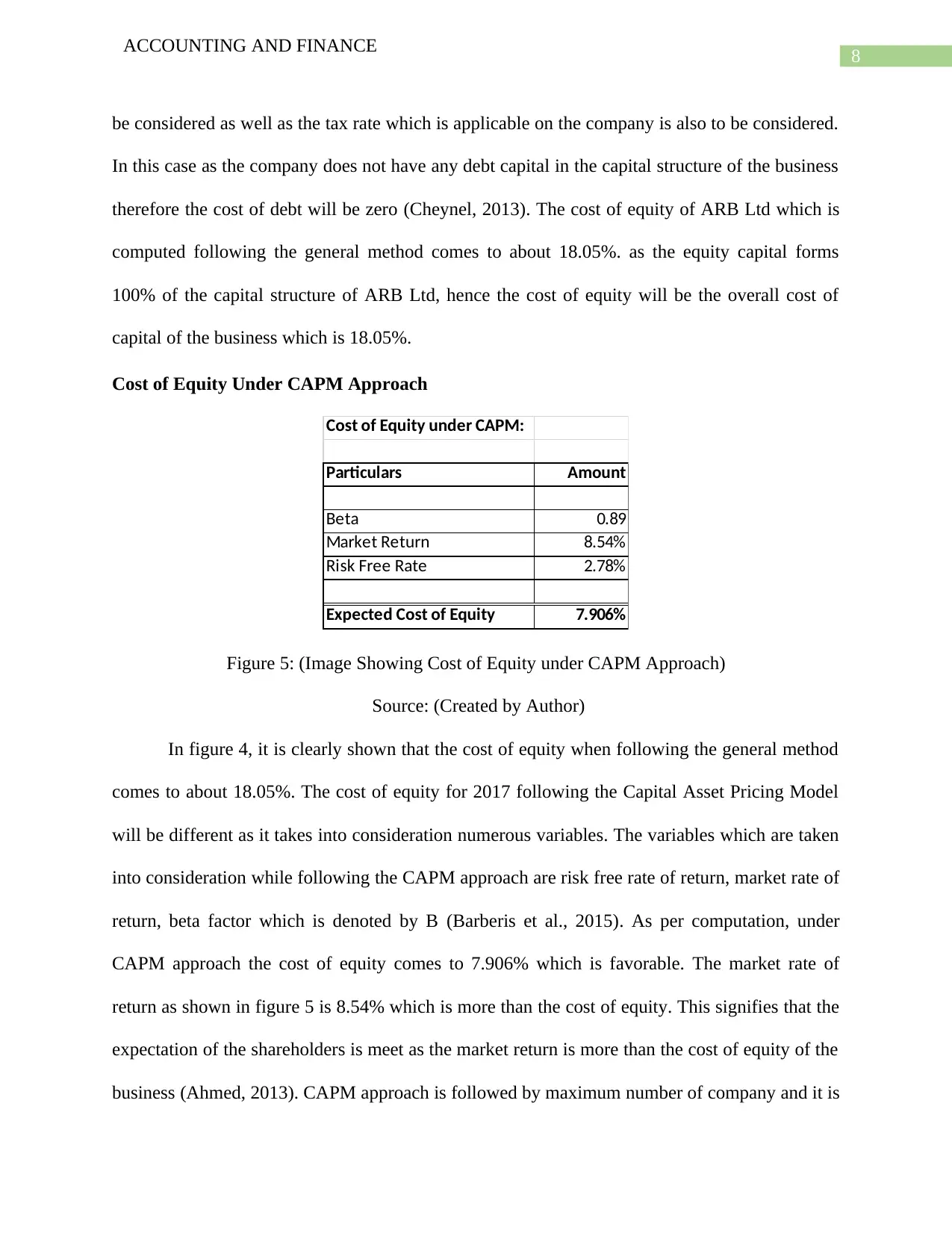

Cost of Equity Under CAPM Approach

Cost of Equity under CAPM:

Particulars Amount

Beta 0.89

Market Return 8.54%

Risk Free Rate 2.78%

Expected Cost of Equity 7.906%

Figure 5: (Image Showing Cost of Equity under CAPM Approach)

Source: (Created by Author)

In figure 4, it is clearly shown that the cost of equity when following the general method

comes to about 18.05%. The cost of equity for 2017 following the Capital Asset Pricing Model

will be different as it takes into consideration numerous variables. The variables which are taken

into consideration while following the CAPM approach are risk free rate of return, market rate of

return, beta factor which is denoted by B (Barberis et al., 2015). As per computation, under

CAPM approach the cost of equity comes to 7.906% which is favorable. The market rate of

return as shown in figure 5 is 8.54% which is more than the cost of equity. This signifies that the

expectation of the shareholders is meet as the market return is more than the cost of equity of the

business (Ahmed, 2013). CAPM approach is followed by maximum number of company and it is

ACCOUNTING AND FINANCE

be considered as well as the tax rate which is applicable on the company is also to be considered.

In this case as the company does not have any debt capital in the capital structure of the business

therefore the cost of debt will be zero (Cheynel, 2013). The cost of equity of ARB Ltd which is

computed following the general method comes to about 18.05%. as the equity capital forms

100% of the capital structure of ARB Ltd, hence the cost of equity will be the overall cost of

capital of the business which is 18.05%.

Cost of Equity Under CAPM Approach

Cost of Equity under CAPM:

Particulars Amount

Beta 0.89

Market Return 8.54%

Risk Free Rate 2.78%

Expected Cost of Equity 7.906%

Figure 5: (Image Showing Cost of Equity under CAPM Approach)

Source: (Created by Author)

In figure 4, it is clearly shown that the cost of equity when following the general method

comes to about 18.05%. The cost of equity for 2017 following the Capital Asset Pricing Model

will be different as it takes into consideration numerous variables. The variables which are taken

into consideration while following the CAPM approach are risk free rate of return, market rate of

return, beta factor which is denoted by B (Barberis et al., 2015). As per computation, under

CAPM approach the cost of equity comes to 7.906% which is favorable. The market rate of

return as shown in figure 5 is 8.54% which is more than the cost of equity. This signifies that the

expectation of the shareholders is meet as the market return is more than the cost of equity of the

business (Ahmed, 2013). CAPM approach is followed by maximum number of company and it is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING AND FINANCE

considered to be the most accurate method of computing cost of equity for a company (McKay &

Haque, 2016).

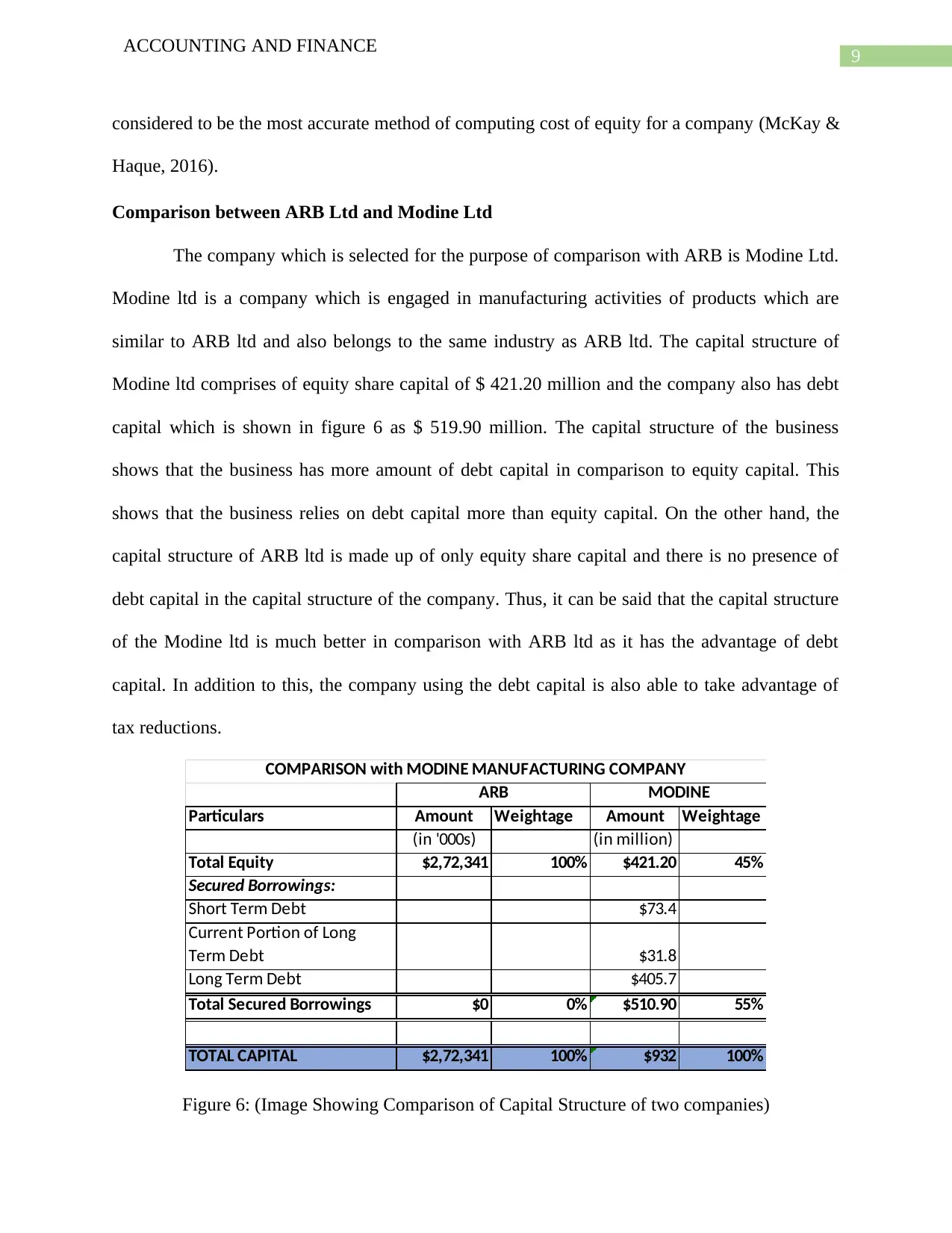

Comparison between ARB Ltd and Modine Ltd

The company which is selected for the purpose of comparison with ARB is Modine Ltd.

Modine ltd is a company which is engaged in manufacturing activities of products which are

similar to ARB ltd and also belongs to the same industry as ARB ltd. The capital structure of

Modine ltd comprises of equity share capital of $ 421.20 million and the company also has debt

capital which is shown in figure 6 as $ 519.90 million. The capital structure of the business

shows that the business has more amount of debt capital in comparison to equity capital. This

shows that the business relies on debt capital more than equity capital. On the other hand, the

capital structure of ARB ltd is made up of only equity share capital and there is no presence of

debt capital in the capital structure of the company. Thus, it can be said that the capital structure

of the Modine ltd is much better in comparison with ARB ltd as it has the advantage of debt

capital. In addition to this, the company using the debt capital is also able to take advantage of

tax reductions.

Particulars Amount Weightage Amount Weightage

(in '000s) (in million)

Total Equity $2,72,341 100% $421.20 45%

Secured Borrowings:

Short Term Debt $73.4

Current Portion of Long

Term Debt $31.8

Long Term Debt $405.7

Total Secured Borrowings $0 0% $510.90 55%

TOTAL CAPITAL $2,72,341 100% $932 100%

ARB MODINE

COMPARISON with MODINE MANUFACTURING COMPANY

Figure 6: (Image Showing Comparison of Capital Structure of two companies)

ACCOUNTING AND FINANCE

considered to be the most accurate method of computing cost of equity for a company (McKay &

Haque, 2016).

Comparison between ARB Ltd and Modine Ltd

The company which is selected for the purpose of comparison with ARB is Modine Ltd.

Modine ltd is a company which is engaged in manufacturing activities of products which are

similar to ARB ltd and also belongs to the same industry as ARB ltd. The capital structure of

Modine ltd comprises of equity share capital of $ 421.20 million and the company also has debt

capital which is shown in figure 6 as $ 519.90 million. The capital structure of the business

shows that the business has more amount of debt capital in comparison to equity capital. This

shows that the business relies on debt capital more than equity capital. On the other hand, the

capital structure of ARB ltd is made up of only equity share capital and there is no presence of

debt capital in the capital structure of the company. Thus, it can be said that the capital structure

of the Modine ltd is much better in comparison with ARB ltd as it has the advantage of debt

capital. In addition to this, the company using the debt capital is also able to take advantage of

tax reductions.

Particulars Amount Weightage Amount Weightage

(in '000s) (in million)

Total Equity $2,72,341 100% $421.20 45%

Secured Borrowings:

Short Term Debt $73.4

Current Portion of Long

Term Debt $31.8

Long Term Debt $405.7

Total Secured Borrowings $0 0% $510.90 55%

TOTAL CAPITAL $2,72,341 100% $932 100%

ARB MODINE

COMPARISON with MODINE MANUFACTURING COMPANY

Figure 6: (Image Showing Comparison of Capital Structure of two companies)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING AND FINANCE

Source: (Created by Author)

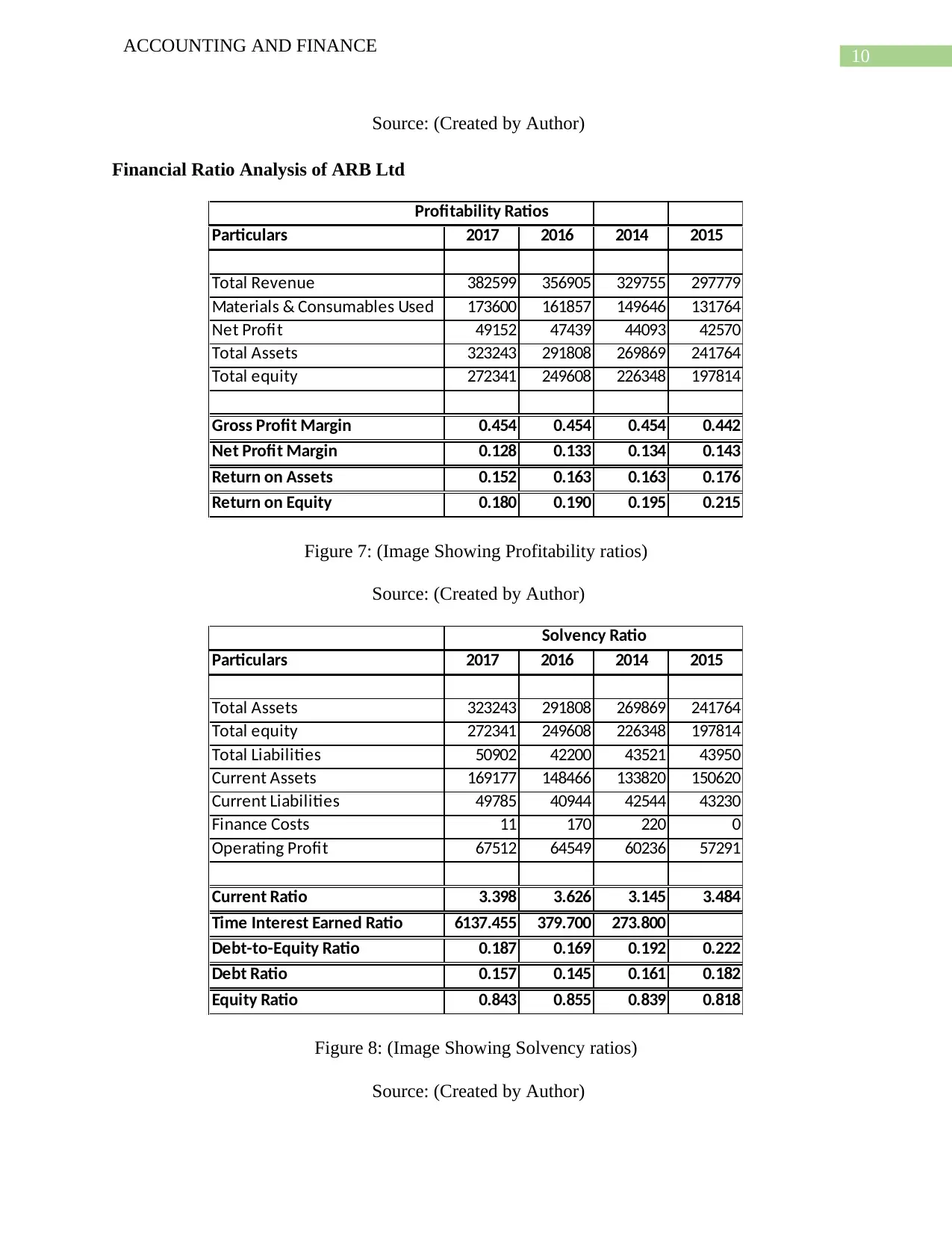

Financial Ratio Analysis of ARB Ltd

Profitability Ratios

Particulars 2017 2016 2014 2015

Total Revenue 382599 356905 329755 297779

Materials & Consumables Used 173600 161857 149646 131764

Net Profit 49152 47439 44093 42570

Total Assets 323243 291808 269869 241764

Total equity 272341 249608 226348 197814

Gross Profit Margin 0.454 0.454 0.454 0.442

Net Profit Margin 0.128 0.133 0.134 0.143

Return on Assets 0.152 0.163 0.163 0.176

Return on Equity 0.180 0.190 0.195 0.215

Figure 7: (Image Showing Profitability ratios)

Source: (Created by Author)

Particulars 2017 2016 2014 2015

Total Assets 323243 291808 269869 241764

Total equity 272341 249608 226348 197814

Total Liabilities 50902 42200 43521 43950

Current Assets 169177 148466 133820 150620

Current Liabilities 49785 40944 42544 43230

Finance Costs 11 170 220 0

Operating Profit 67512 64549 60236 57291

Current Ratio 3.398 3.626 3.145 3.484

Time Interest Earned Ratio 6137.455 379.700 273.800

Debt-to-Equity Ratio 0.187 0.169 0.192 0.222

Debt Ratio 0.157 0.145 0.161 0.182

Equity Ratio 0.843 0.855 0.839 0.818

Solvency Ratio

Figure 8: (Image Showing Solvency ratios)

Source: (Created by Author)

ACCOUNTING AND FINANCE

Source: (Created by Author)

Financial Ratio Analysis of ARB Ltd

Profitability Ratios

Particulars 2017 2016 2014 2015

Total Revenue 382599 356905 329755 297779

Materials & Consumables Used 173600 161857 149646 131764

Net Profit 49152 47439 44093 42570

Total Assets 323243 291808 269869 241764

Total equity 272341 249608 226348 197814

Gross Profit Margin 0.454 0.454 0.454 0.442

Net Profit Margin 0.128 0.133 0.134 0.143

Return on Assets 0.152 0.163 0.163 0.176

Return on Equity 0.180 0.190 0.195 0.215

Figure 7: (Image Showing Profitability ratios)

Source: (Created by Author)

Particulars 2017 2016 2014 2015

Total Assets 323243 291808 269869 241764

Total equity 272341 249608 226348 197814

Total Liabilities 50902 42200 43521 43950

Current Assets 169177 148466 133820 150620

Current Liabilities 49785 40944 42544 43230

Finance Costs 11 170 220 0

Operating Profit 67512 64549 60236 57291

Current Ratio 3.398 3.626 3.145 3.484

Time Interest Earned Ratio 6137.455 379.700 273.800

Debt-to-Equity Ratio 0.187 0.169 0.192 0.222

Debt Ratio 0.157 0.145 0.161 0.182

Equity Ratio 0.843 0.855 0.839 0.818

Solvency Ratio

Figure 8: (Image Showing Solvency ratios)

Source: (Created by Author)

11

ACCOUNTING AND FINANCE

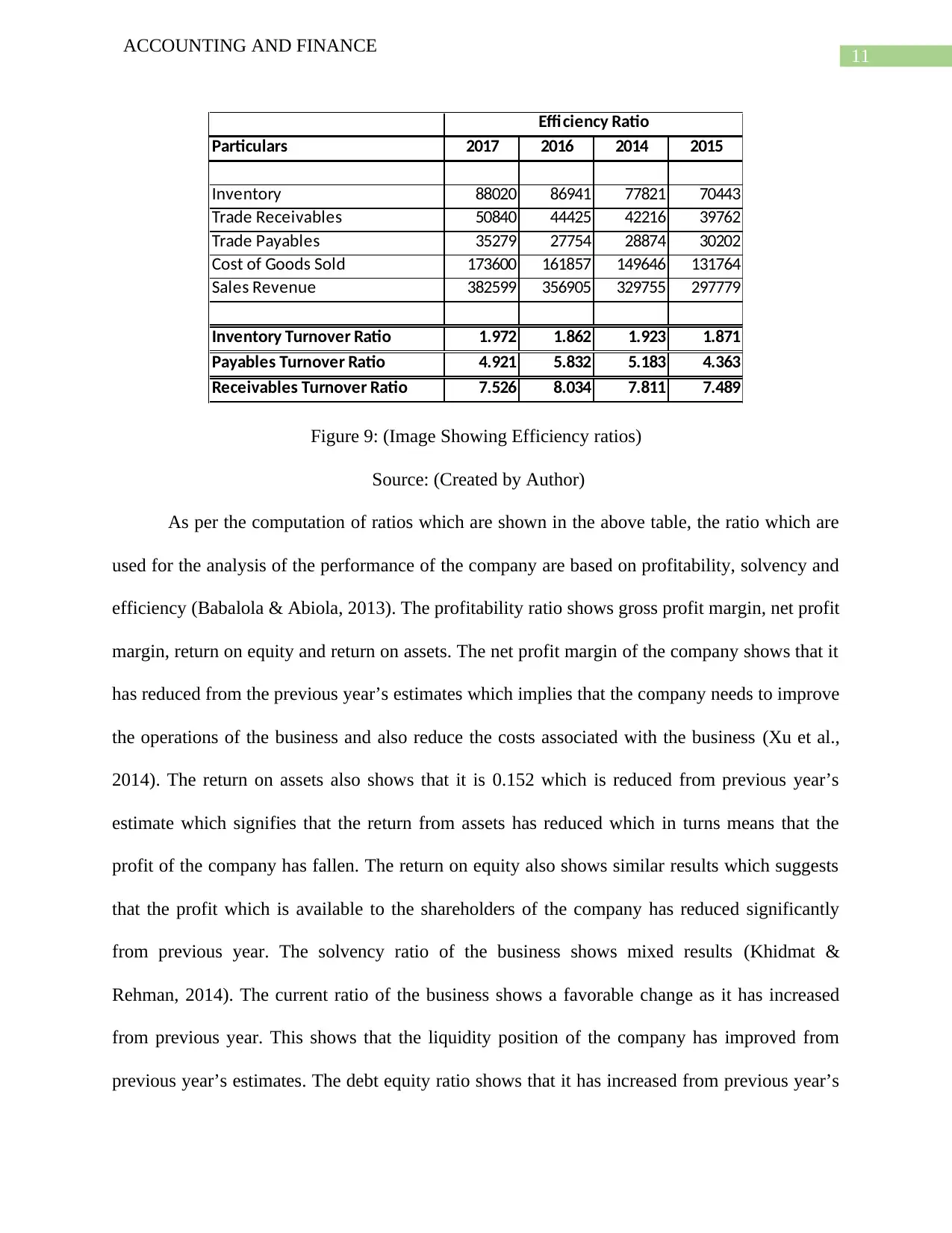

Particulars 2017 2016 2014 2015

Inventory 88020 86941 77821 70443

Trade Receivables 50840 44425 42216 39762

Trade Payables 35279 27754 28874 30202

Cost of Goods Sold 173600 161857 149646 131764

Sales Revenue 382599 356905 329755 297779

Inventory Turnover Ratio 1.972 1.862 1.923 1.871

Payables Turnover Ratio 4.921 5.832 5.183 4.363

Receivables Turnover Ratio 7.526 8.034 7.811 7.489

Efficiency Ratio

Figure 9: (Image Showing Efficiency ratios)

Source: (Created by Author)

As per the computation of ratios which are shown in the above table, the ratio which are

used for the analysis of the performance of the company are based on profitability, solvency and

efficiency (Babalola & Abiola, 2013). The profitability ratio shows gross profit margin, net profit

margin, return on equity and return on assets. The net profit margin of the company shows that it

has reduced from the previous year’s estimates which implies that the company needs to improve

the operations of the business and also reduce the costs associated with the business (Xu et al.,

2014). The return on assets also shows that it is 0.152 which is reduced from previous year’s

estimate which signifies that the return from assets has reduced which in turns means that the

profit of the company has fallen. The return on equity also shows similar results which suggests

that the profit which is available to the shareholders of the company has reduced significantly

from previous year. The solvency ratio of the business shows mixed results (Khidmat &

Rehman, 2014). The current ratio of the business shows a favorable change as it has increased

from previous year. This shows that the liquidity position of the company has improved from

previous year’s estimates. The debt equity ratio shows that it has increased from previous year’s

ACCOUNTING AND FINANCE

Particulars 2017 2016 2014 2015

Inventory 88020 86941 77821 70443

Trade Receivables 50840 44425 42216 39762

Trade Payables 35279 27754 28874 30202

Cost of Goods Sold 173600 161857 149646 131764

Sales Revenue 382599 356905 329755 297779

Inventory Turnover Ratio 1.972 1.862 1.923 1.871

Payables Turnover Ratio 4.921 5.832 5.183 4.363

Receivables Turnover Ratio 7.526 8.034 7.811 7.489

Efficiency Ratio

Figure 9: (Image Showing Efficiency ratios)

Source: (Created by Author)

As per the computation of ratios which are shown in the above table, the ratio which are

used for the analysis of the performance of the company are based on profitability, solvency and

efficiency (Babalola & Abiola, 2013). The profitability ratio shows gross profit margin, net profit

margin, return on equity and return on assets. The net profit margin of the company shows that it

has reduced from the previous year’s estimates which implies that the company needs to improve

the operations of the business and also reduce the costs associated with the business (Xu et al.,

2014). The return on assets also shows that it is 0.152 which is reduced from previous year’s

estimate which signifies that the return from assets has reduced which in turns means that the

profit of the company has fallen. The return on equity also shows similar results which suggests

that the profit which is available to the shareholders of the company has reduced significantly

from previous year. The solvency ratio of the business shows mixed results (Khidmat &

Rehman, 2014). The current ratio of the business shows a favorable change as it has increased

from previous year. This shows that the liquidity position of the company has improved from

previous year’s estimates. The debt equity ratio shows that it has increased from previous year’s

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.