Accounting and Finance - Assignment Sample

VerifiedAdded on 2021/05/30

|13

|1803

|19

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING AND FINANCE

ACCOUNTING AND FINANCE

Name of the Student:

Name of the University:

Author’s Note:

ACCOUNTING AND FINANCE

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

ACCOUNTING AND FINANCE

Executive Summary

The assignment is based on two separate tasks which focuses on two different companies which

are Saturn Pet care ltd which is engaged in manufacturing of pet products and ARB Ltd which is

engaged in manufacturing activities of road motors accessories. In the first task capital budgeting

technique will be applied so as to select from two different production site which are Bathurst

site and Wodonga site. In the second task the capital structure of ARB ltd is to be analysed and

also compared with a similar company belonging to same industry.

ACCOUNTING AND FINANCE

Executive Summary

The assignment is based on two separate tasks which focuses on two different companies which

are Saturn Pet care ltd which is engaged in manufacturing of pet products and ARB Ltd which is

engaged in manufacturing activities of road motors accessories. In the first task capital budgeting

technique will be applied so as to select from two different production site which are Bathurst

site and Wodonga site. In the second task the capital structure of ARB ltd is to be analysed and

also compared with a similar company belonging to same industry.

2

ACCOUNTING AND FINANCE

Table of Contents

Part A...............................................................................................................................................3

Capital Budgeting of Bathurst Site..............................................................................................3

Capital Budgeting of Wodonga Site............................................................................................4

Product Cannibalization...............................................................................................................5

Rectifying the Excessive Sales Recorded....................................................................................5

Inclusion of Original Cost of Old Factory Shed..........................................................................5

Part B...............................................................................................................................................6

Introduction..................................................................................................................................6

Capital Structure and Cost of Capital..........................................................................................6

Weighted Average Cost of Capital below...................................................................................6

Cost of Capital Under CAPM......................................................................................................7

Comparison between ARB ltd and Modine ltd............................................................................8

Financial Ratios of ARB Ltd.......................................................................................................8

Changes in capital structure.......................................................................................................10

Wealth Maximization................................................................................................................10

Recommendations......................................................................................................................11

Conclusion.....................................................................................................................................11

Reference.......................................................................................................................................12

ACCOUNTING AND FINANCE

Table of Contents

Part A...............................................................................................................................................3

Capital Budgeting of Bathurst Site..............................................................................................3

Capital Budgeting of Wodonga Site............................................................................................4

Product Cannibalization...............................................................................................................5

Rectifying the Excessive Sales Recorded....................................................................................5

Inclusion of Original Cost of Old Factory Shed..........................................................................5

Part B...............................................................................................................................................6

Introduction..................................................................................................................................6

Capital Structure and Cost of Capital..........................................................................................6

Weighted Average Cost of Capital below...................................................................................6

Cost of Capital Under CAPM......................................................................................................7

Comparison between ARB ltd and Modine ltd............................................................................8

Financial Ratios of ARB Ltd.......................................................................................................8

Changes in capital structure.......................................................................................................10

Wealth Maximization................................................................................................................10

Recommendations......................................................................................................................11

Conclusion.....................................................................................................................................11

Reference.......................................................................................................................................12

3

ACCOUNTING AND FINANCE

Part A

Capital Budgeting of Bathurst Site

Particulars 0 1 2 3 4 5 6 7 8 9 10

Initial Investment:

Construction on Manufacturing Unit -$275,00,000

Factory Building -$80,00,000

Infrastructure Grant $25,00,000

Total Initial Investment -$330,00,000

Operational Cash Flow:

Sales Growth Rate 10% 10% 10% 10% 10% 10% 10% 10% 10%

MAC 30% 30% 30% 30% 30% 30% 30% 30% 30% 30%

Annual Sales $300,00,000 $330,00,000 $363,00,000 $399,30,000 $439,23,000 $483,15,300 $531,46,830 $584,61,513 $643,07,664 $707,38,431

Conversion Cost -$210,00,000 -$231,00,000 -$254,10,000 -$279,51,000 -$307,46,100 -$338,20,710 -$372,02,781 -$409,23,059 -$450,15,365 -$495,16,902

Rebate on Municipal Rate $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000

Depreciation on Plant & Equipment -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000

Depreciation on Building -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000

Net Profit before Tax $64,30,000 $73,30,000 $83,20,000 $94,09,000 $106,06,900 $119,24,590 $133,74,049 $149,68,454 $167,22,299 $186,51,529

Less: Income Tax @ 30% -$19,29,000 -$21,99,000 -$24,96,000 -$28,22,700 -$31,82,070 -$35,77,377 -$40,12,215 -$44,90,536 -$50,16,690 -$55,95,459

Net Profit after Tax $45,01,000 $51,31,000 $58,24,000 $65,86,300 $74,24,830 $83,47,213 $93,61,834 $104,77,918 $117,05,610 $130,56,070

Add: Depreciation on Plant $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000

Add: Depreciation on Building $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000

After-Tax Cash Flows $75,71,000 $82,01,000 $88,94,000 $96,56,300 $104,94,830 $114,17,213 $124,31,834 $135,47,918 $147,75,610 $161,26,070

Net Cash Flow -$330,00,000 $75,71,000 $82,01,000 $88,94,000 $96,56,300 $104,94,830 $114,17,213 $124,31,834 $135,47,918 $147,75,610 $161,26,070

Cumulative Cash Flow -$330,00,000 -$254,29,000 -$172,28,000 -$83,34,000 $13,22,300 $118,17,130 $232,34,343 $356,66,177 $492,14,095 $639,89,705 $801,15,775

Discount Rate 22% 22% 22% 22% 22% 22% 22% 22% 22% 22% 22%

Discounted Cash Flow -$330,00,000 $62,05,738 $55,09,944 $48,97,987 $43,58,845 $38,83,079 $34,62,590 $30,90,412 $27,60,539 $24,67,783 $22,07,650

Payback Period (in years) 3.863

Net Present Value $58,44,567

Profitability Index 1.177

Years

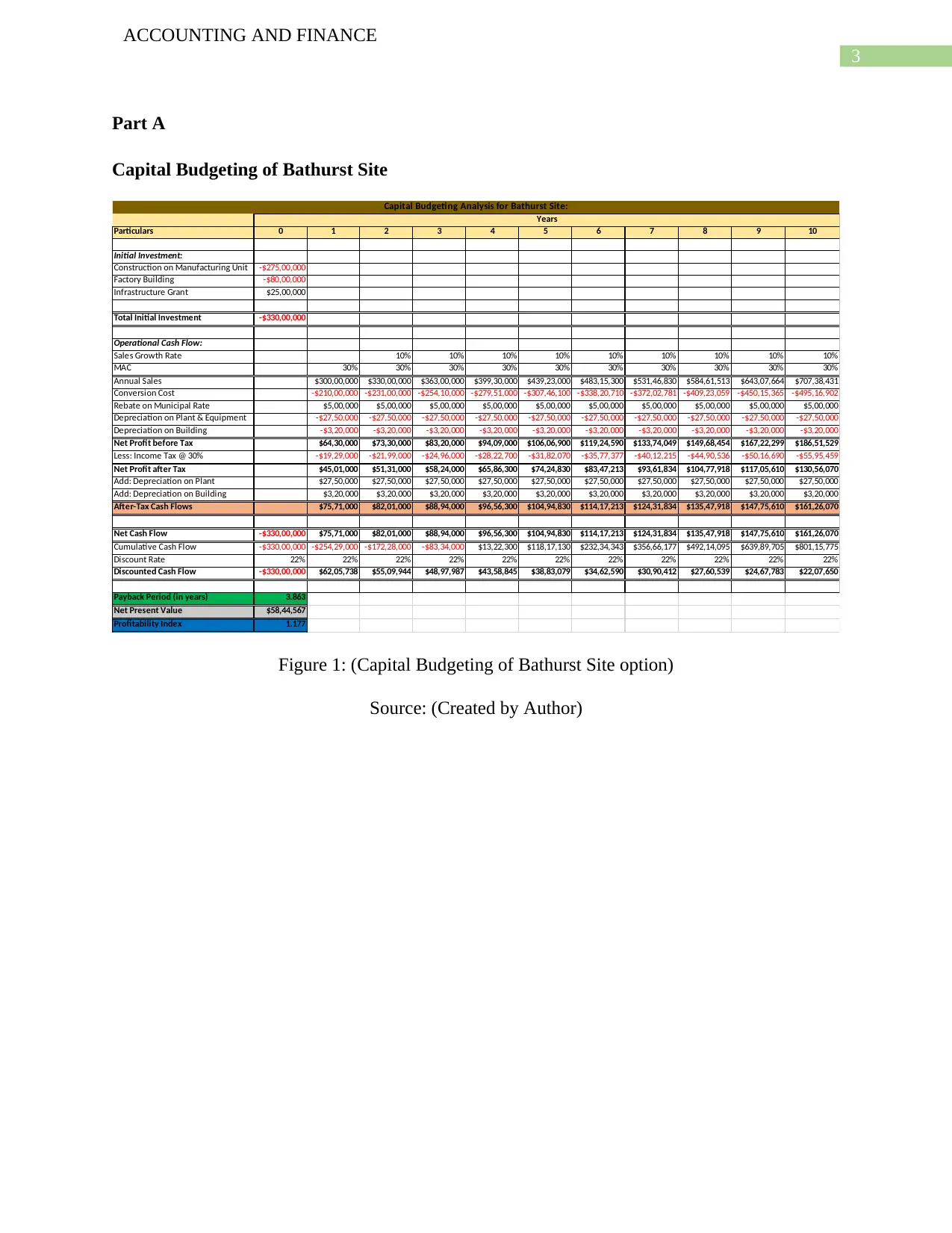

Capital Budgeting Analysis for Bathurst Site:

Figure 1: (Capital Budgeting of Bathurst Site option)

Source: (Created by Author)

ACCOUNTING AND FINANCE

Part A

Capital Budgeting of Bathurst Site

Particulars 0 1 2 3 4 5 6 7 8 9 10

Initial Investment:

Construction on Manufacturing Unit -$275,00,000

Factory Building -$80,00,000

Infrastructure Grant $25,00,000

Total Initial Investment -$330,00,000

Operational Cash Flow:

Sales Growth Rate 10% 10% 10% 10% 10% 10% 10% 10% 10%

MAC 30% 30% 30% 30% 30% 30% 30% 30% 30% 30%

Annual Sales $300,00,000 $330,00,000 $363,00,000 $399,30,000 $439,23,000 $483,15,300 $531,46,830 $584,61,513 $643,07,664 $707,38,431

Conversion Cost -$210,00,000 -$231,00,000 -$254,10,000 -$279,51,000 -$307,46,100 -$338,20,710 -$372,02,781 -$409,23,059 -$450,15,365 -$495,16,902

Rebate on Municipal Rate $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000 $5,00,000

Depreciation on Plant & Equipment -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000

Depreciation on Building -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000 -$3,20,000

Net Profit before Tax $64,30,000 $73,30,000 $83,20,000 $94,09,000 $106,06,900 $119,24,590 $133,74,049 $149,68,454 $167,22,299 $186,51,529

Less: Income Tax @ 30% -$19,29,000 -$21,99,000 -$24,96,000 -$28,22,700 -$31,82,070 -$35,77,377 -$40,12,215 -$44,90,536 -$50,16,690 -$55,95,459

Net Profit after Tax $45,01,000 $51,31,000 $58,24,000 $65,86,300 $74,24,830 $83,47,213 $93,61,834 $104,77,918 $117,05,610 $130,56,070

Add: Depreciation on Plant $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000

Add: Depreciation on Building $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000 $3,20,000

After-Tax Cash Flows $75,71,000 $82,01,000 $88,94,000 $96,56,300 $104,94,830 $114,17,213 $124,31,834 $135,47,918 $147,75,610 $161,26,070

Net Cash Flow -$330,00,000 $75,71,000 $82,01,000 $88,94,000 $96,56,300 $104,94,830 $114,17,213 $124,31,834 $135,47,918 $147,75,610 $161,26,070

Cumulative Cash Flow -$330,00,000 -$254,29,000 -$172,28,000 -$83,34,000 $13,22,300 $118,17,130 $232,34,343 $356,66,177 $492,14,095 $639,89,705 $801,15,775

Discount Rate 22% 22% 22% 22% 22% 22% 22% 22% 22% 22% 22%

Discounted Cash Flow -$330,00,000 $62,05,738 $55,09,944 $48,97,987 $43,58,845 $38,83,079 $34,62,590 $30,90,412 $27,60,539 $24,67,783 $22,07,650

Payback Period (in years) 3.863

Net Present Value $58,44,567

Profitability Index 1.177

Years

Capital Budgeting Analysis for Bathurst Site:

Figure 1: (Capital Budgeting of Bathurst Site option)

Source: (Created by Author)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

ACCOUNTING AND FINANCE

Capital Budgeting of Wodonga Site

Particulars 0 1 2 3 4 5 6 7 8 9 10

Initial Investment:

Construction on Manufacturing Unit -$275,00,000

Value of Wodonga Site

Total Initial Investment -$275,00,000

Operational Cash Flow:

Sales Growth Rate 10% 10% 10% 10% 10% 10% 10% 10% 10%

MAC 30% 30% 30% 30% 30% 30% 30% 30% 30% 30%

Annual Sales $300,00,000 $330,00,000 $363,00,000 $399,30,000 $439,23,000 $483,15,300 $531,46,830 $584,61,513 $643,07,664 $707,38,431

Conversion Cost -$210,00,000 -$231,00,000 -$254,10,000 -$279,51,000 -$307,46,100 -$338,20,710 -$372,02,781 -$409,23,059 -$450,15,365 -$495,16,902

Depreciation on Plant & Equipment -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000

Depreciation on Building $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

Net Profit before Tax $62,50,000 $71,50,000 $81,40,000 $92,29,000 $104,26,900 $117,44,590 $131,94,049 $147,88,454 $165,42,299 $184,71,529

Less: Income Tax @ 30% -$18,75,000 -$21,45,000 -$24,42,000 -$27,68,700 -$31,28,070 -$35,23,377 -$39,58,215 -$44,36,536 -$49,62,690 -$55,41,459

Net Profit after Tax $43,75,000 $50,05,000 $56,98,000 $64,60,300 $72,98,830 $82,21,213 $92,35,834 $103,51,918 $115,79,610 $129,30,070

Add: Depreciation on Plant $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000

Add: Depreciation on Building $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

After-Tax Cash Flows $71,25,000 $77,55,000 $84,48,000 $92,10,300 $100,48,830 $109,71,213 $119,85,834 $131,01,918 $143,29,610 $156,80,070

Net Cash Flow -$275,00,000 $71,25,000 $77,55,000 $84,48,000 $92,10,300 $100,48,830 $109,71,213 $119,85,834 $131,01,918 $143,29,610 $156,80,070

Cumulative Cash Flow -$275,00,000 -$203,75,000 -$126,20,000 -$41,72,000 $50,38,300 $150,87,130 $260,58,343 $380,44,177 $511,46,095 $654,75,705 $811,55,775

Discount Rate 22% 22% 22% 22% 22% 22% 22% 22% 22% 22% 22%

Discounted Cash Flow -$275,00,000 $58,40,164 $52,10,293 $46,52,372 $41,57,521 $37,18,060 $33,27,328 $29,79,542 $26,69,662 $23,93,293 $21,46,593

Payback Period (in years) 3.453

Net Present Value $95,94,827

Profitability Index 1.349

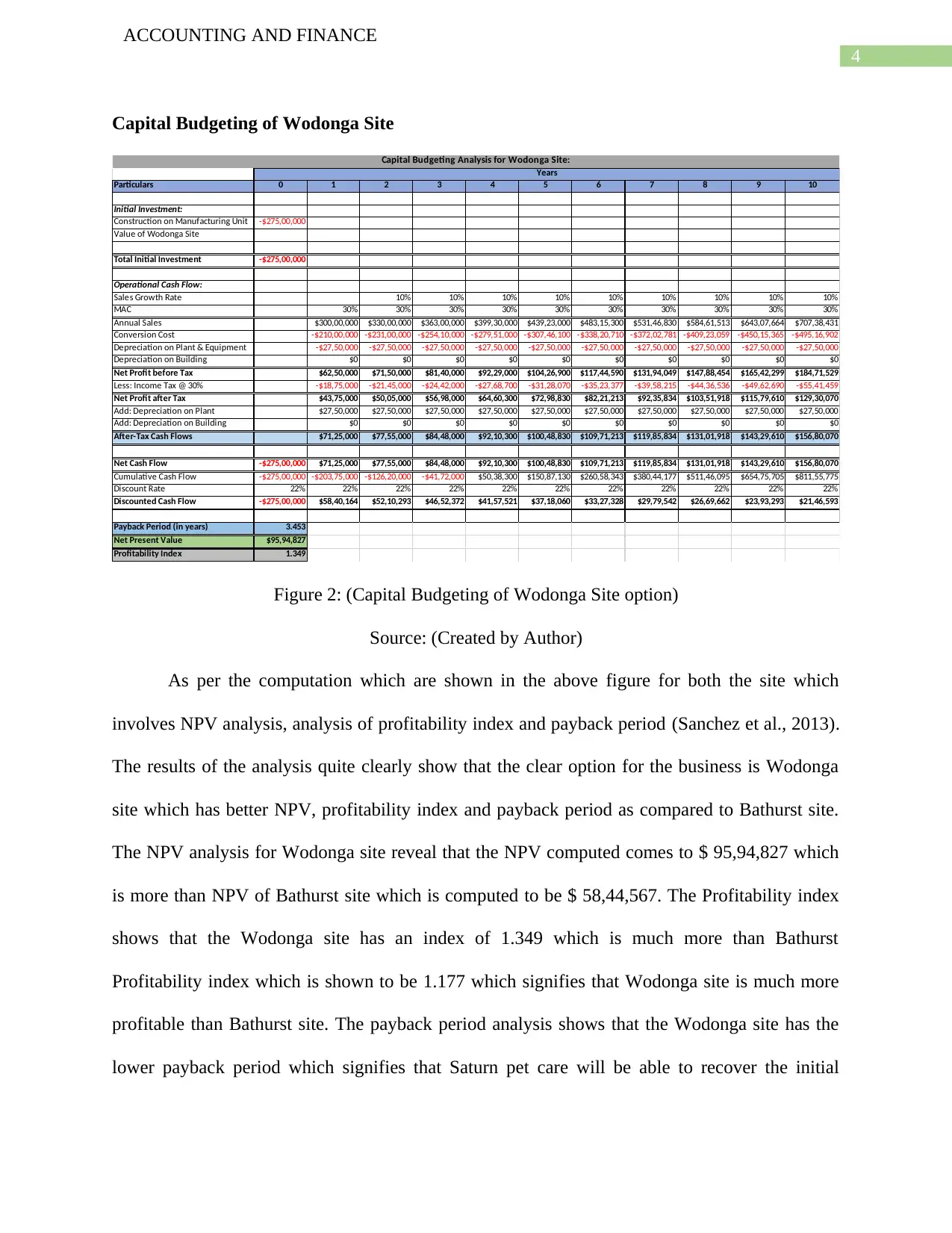

Capital Budgeting Analysis for Wodonga Site:

Years

Figure 2: (Capital Budgeting of Wodonga Site option)

Source: (Created by Author)

As per the computation which are shown in the above figure for both the site which

involves NPV analysis, analysis of profitability index and payback period (Sanchez et al., 2013).

The results of the analysis quite clearly show that the clear option for the business is Wodonga

site which has better NPV, profitability index and payback period as compared to Bathurst site.

The NPV analysis for Wodonga site reveal that the NPV computed comes to $ 95,94,827 which

is more than NPV of Bathurst site which is computed to be $ 58,44,567. The Profitability index

shows that the Wodonga site has an index of 1.349 which is much more than Bathurst

Profitability index which is shown to be 1.177 which signifies that Wodonga site is much more

profitable than Bathurst site. The payback period analysis shows that the Wodonga site has the

lower payback period which signifies that Saturn pet care will be able to recover the initial

ACCOUNTING AND FINANCE

Capital Budgeting of Wodonga Site

Particulars 0 1 2 3 4 5 6 7 8 9 10

Initial Investment:

Construction on Manufacturing Unit -$275,00,000

Value of Wodonga Site

Total Initial Investment -$275,00,000

Operational Cash Flow:

Sales Growth Rate 10% 10% 10% 10% 10% 10% 10% 10% 10%

MAC 30% 30% 30% 30% 30% 30% 30% 30% 30% 30%

Annual Sales $300,00,000 $330,00,000 $363,00,000 $399,30,000 $439,23,000 $483,15,300 $531,46,830 $584,61,513 $643,07,664 $707,38,431

Conversion Cost -$210,00,000 -$231,00,000 -$254,10,000 -$279,51,000 -$307,46,100 -$338,20,710 -$372,02,781 -$409,23,059 -$450,15,365 -$495,16,902

Depreciation on Plant & Equipment -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000 -$27,50,000

Depreciation on Building $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

Net Profit before Tax $62,50,000 $71,50,000 $81,40,000 $92,29,000 $104,26,900 $117,44,590 $131,94,049 $147,88,454 $165,42,299 $184,71,529

Less: Income Tax @ 30% -$18,75,000 -$21,45,000 -$24,42,000 -$27,68,700 -$31,28,070 -$35,23,377 -$39,58,215 -$44,36,536 -$49,62,690 -$55,41,459

Net Profit after Tax $43,75,000 $50,05,000 $56,98,000 $64,60,300 $72,98,830 $82,21,213 $92,35,834 $103,51,918 $115,79,610 $129,30,070

Add: Depreciation on Plant $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000 $27,50,000

Add: Depreciation on Building $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

After-Tax Cash Flows $71,25,000 $77,55,000 $84,48,000 $92,10,300 $100,48,830 $109,71,213 $119,85,834 $131,01,918 $143,29,610 $156,80,070

Net Cash Flow -$275,00,000 $71,25,000 $77,55,000 $84,48,000 $92,10,300 $100,48,830 $109,71,213 $119,85,834 $131,01,918 $143,29,610 $156,80,070

Cumulative Cash Flow -$275,00,000 -$203,75,000 -$126,20,000 -$41,72,000 $50,38,300 $150,87,130 $260,58,343 $380,44,177 $511,46,095 $654,75,705 $811,55,775

Discount Rate 22% 22% 22% 22% 22% 22% 22% 22% 22% 22% 22%

Discounted Cash Flow -$275,00,000 $58,40,164 $52,10,293 $46,52,372 $41,57,521 $37,18,060 $33,27,328 $29,79,542 $26,69,662 $23,93,293 $21,46,593

Payback Period (in years) 3.453

Net Present Value $95,94,827

Profitability Index 1.349

Capital Budgeting Analysis for Wodonga Site:

Years

Figure 2: (Capital Budgeting of Wodonga Site option)

Source: (Created by Author)

As per the computation which are shown in the above figure for both the site which

involves NPV analysis, analysis of profitability index and payback period (Sanchez et al., 2013).

The results of the analysis quite clearly show that the clear option for the business is Wodonga

site which has better NPV, profitability index and payback period as compared to Bathurst site.

The NPV analysis for Wodonga site reveal that the NPV computed comes to $ 95,94,827 which

is more than NPV of Bathurst site which is computed to be $ 58,44,567. The Profitability index

shows that the Wodonga site has an index of 1.349 which is much more than Bathurst

Profitability index which is shown to be 1.177 which signifies that Wodonga site is much more

profitable than Bathurst site. The payback period analysis shows that the Wodonga site has the

lower payback period which signifies that Saturn pet care will be able to recover the initial

5

ACCOUNTING AND FINANCE

investment which the company spend on the production project. Thus, it is clear that Wodonga

site is the clear option.

Product Cannibalization

This can be described as a technique which is used by businesses to promote or introduce

new products in the market by reducing the sales volume of another product (Lin & Okudan,

2013). In the case of Saturn pet care, it is expected the management will be applying this

technique in order to promote the new product of the business in the market.

Rectifying the Excessive Sales Recorded

The sales which is recorded and estimated by the marketing department of Saturn pet care

as per one of the directors of the business has been incorrectly estimated and the accurate one

might be a bit lower than what has been anticipated. Such an error in estimation can impact the

decision-making process of the business and therefore needs to be rectified. The management

can apply NPV method and increase the cost figures of the business so as to neutralize the erro in

estimation.

Inclusion of Original Cost of Old Factory Shed

It is also the opinion of the director that the existing factory site which is vacant which is

going to be used in the production process also must be included in the costs of initial investment

made by the business. This is an incorrect estimation as NPV analysis only recognizes current

investments which are undertaken for the project. Th initial investment must not include the such

costs in the initial investment of the business.

ACCOUNTING AND FINANCE

investment which the company spend on the production project. Thus, it is clear that Wodonga

site is the clear option.

Product Cannibalization

This can be described as a technique which is used by businesses to promote or introduce

new products in the market by reducing the sales volume of another product (Lin & Okudan,

2013). In the case of Saturn pet care, it is expected the management will be applying this

technique in order to promote the new product of the business in the market.

Rectifying the Excessive Sales Recorded

The sales which is recorded and estimated by the marketing department of Saturn pet care

as per one of the directors of the business has been incorrectly estimated and the accurate one

might be a bit lower than what has been anticipated. Such an error in estimation can impact the

decision-making process of the business and therefore needs to be rectified. The management

can apply NPV method and increase the cost figures of the business so as to neutralize the erro in

estimation.

Inclusion of Original Cost of Old Factory Shed

It is also the opinion of the director that the existing factory site which is vacant which is

going to be used in the production process also must be included in the costs of initial investment

made by the business. This is an incorrect estimation as NPV analysis only recognizes current

investments which are undertaken for the project. Th initial investment must not include the such

costs in the initial investment of the business.

6

ACCOUNTING AND FINANCE

Part B

Introduction

This part will be analyzing the capital structure which is used by the business for the

purpose of financing its operations. The later paragraph will also be containing an analysis which

will compare the capital structure of ARB ltd and another company belonging to same industry.

There will also be recommendations as to how the business can further develop.

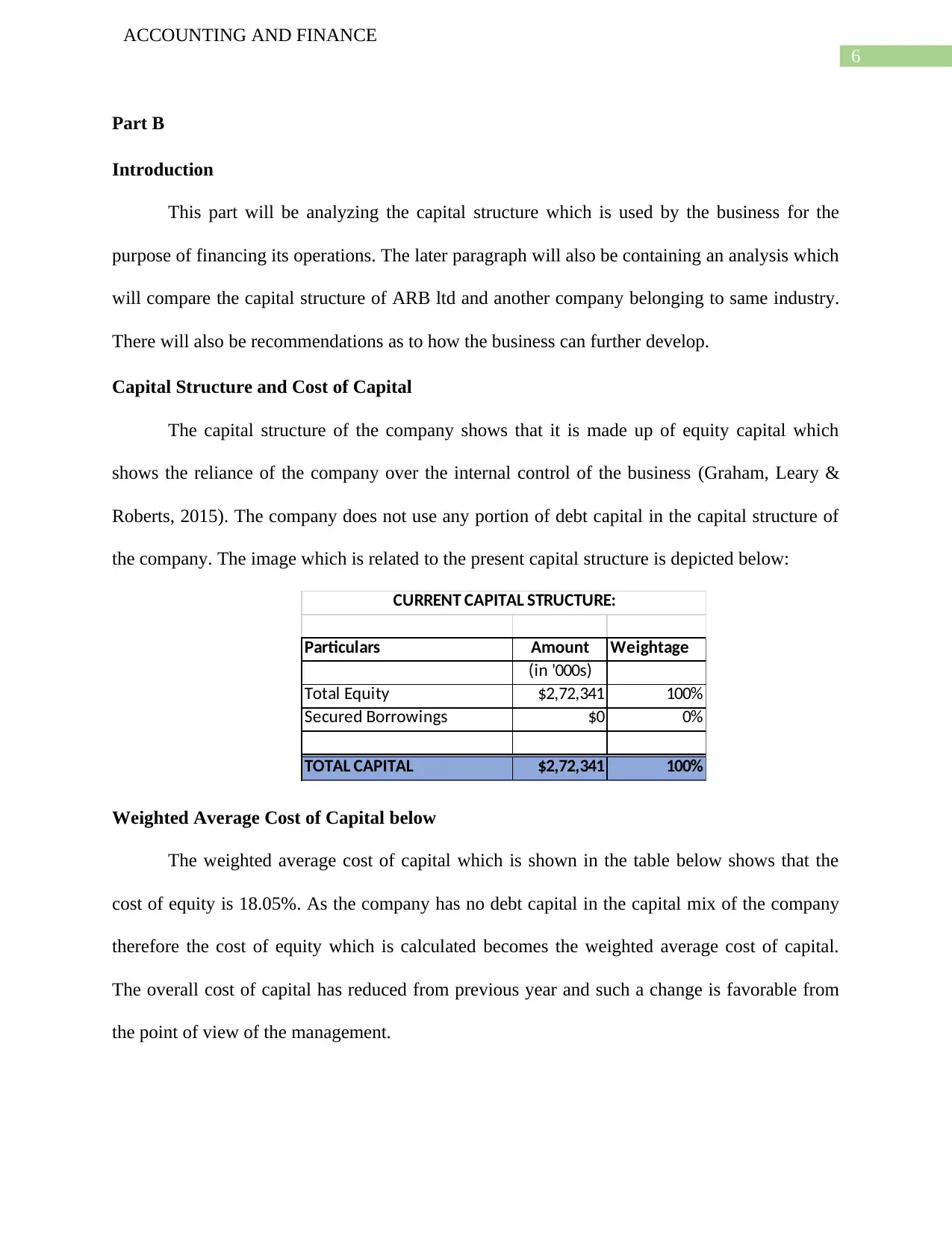

Capital Structure and Cost of Capital

The capital structure of the company shows that it is made up of equity capital which

shows the reliance of the company over the internal control of the business (Graham, Leary &

Roberts, 2015). The company does not use any portion of debt capital in the capital structure of

the company. The image which is related to the present capital structure is depicted below:

Particulars Amount Weightage

(in '000s)

Total Equity $2,72,341 100%

Secured Borrowings $0 0%

TOTAL CAPITAL $2,72,341 100%

CURRENT CAPITAL STRUCTURE:

Weighted Average Cost of Capital below

The weighted average cost of capital which is shown in the table below shows that the

cost of equity is 18.05%. As the company has no debt capital in the capital mix of the company

therefore the cost of equity which is calculated becomes the weighted average cost of capital.

The overall cost of capital has reduced from previous year and such a change is favorable from

the point of view of the management.

ACCOUNTING AND FINANCE

Part B

Introduction

This part will be analyzing the capital structure which is used by the business for the

purpose of financing its operations. The later paragraph will also be containing an analysis which

will compare the capital structure of ARB ltd and another company belonging to same industry.

There will also be recommendations as to how the business can further develop.

Capital Structure and Cost of Capital

The capital structure of the company shows that it is made up of equity capital which

shows the reliance of the company over the internal control of the business (Graham, Leary &

Roberts, 2015). The company does not use any portion of debt capital in the capital structure of

the company. The image which is related to the present capital structure is depicted below:

Particulars Amount Weightage

(in '000s)

Total Equity $2,72,341 100%

Secured Borrowings $0 0%

TOTAL CAPITAL $2,72,341 100%

CURRENT CAPITAL STRUCTURE:

Weighted Average Cost of Capital below

The weighted average cost of capital which is shown in the table below shows that the

cost of equity is 18.05%. As the company has no debt capital in the capital mix of the company

therefore the cost of equity which is calculated becomes the weighted average cost of capital.

The overall cost of capital has reduced from previous year and such a change is favorable from

the point of view of the management.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING AND FINANCE

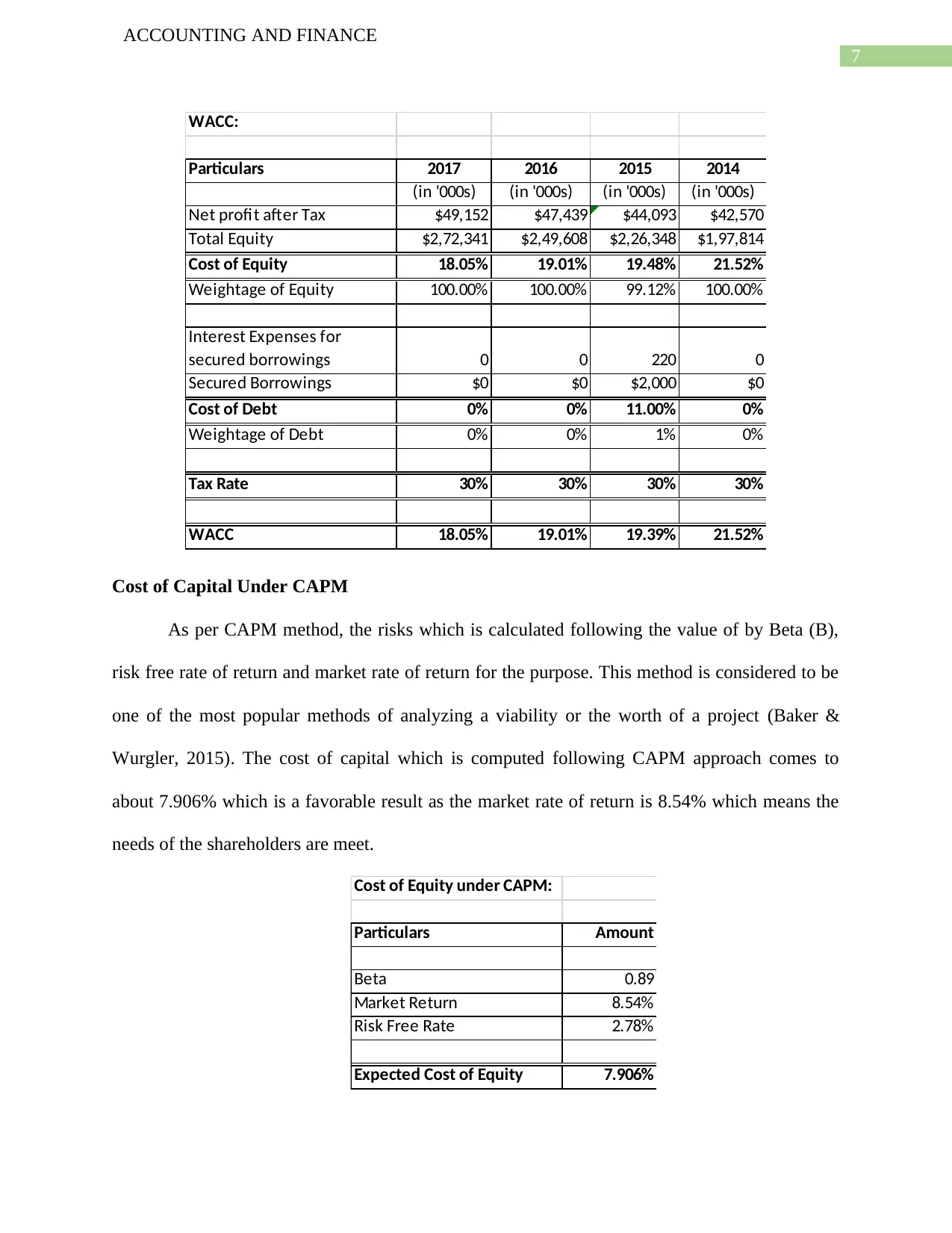

WACC:

Particulars 2017 2016 2015 2014

(in '000s) (in '000s) (in '000s) (in '000s)

Net profit after Tax $49,152 $47,439 $44,093 $42,570

Total Equity $2,72,341 $2,49,608 $2,26,348 $1,97,814

Cost of Equity 18.05% 19.01% 19.48% 21.52%

Weightage of Equity 100.00% 100.00% 99.12% 100.00%

Interest Expenses for

secured borrowings 0 0 220 0

Secured Borrowings $0 $0 $2,000 $0

Cost of Debt 0% 0% 11.00% 0%

Weightage of Debt 0% 0% 1% 0%

Tax Rate 30% 30% 30% 30%

WACC 18.05% 19.01% 19.39% 21.52%

Cost of Capital Under CAPM

As per CAPM method, the risks which is calculated following the value of by Beta (B),

risk free rate of return and market rate of return for the purpose. This method is considered to be

one of the most popular methods of analyzing a viability or the worth of a project (Baker &

Wurgler, 2015). The cost of capital which is computed following CAPM approach comes to

about 7.906% which is a favorable result as the market rate of return is 8.54% which means the

needs of the shareholders are meet.

Cost of Equity under CAPM:

Particulars Amount

Beta 0.89

Market Return 8.54%

Risk Free Rate 2.78%

Expected Cost of Equity 7.906%

ACCOUNTING AND FINANCE

WACC:

Particulars 2017 2016 2015 2014

(in '000s) (in '000s) (in '000s) (in '000s)

Net profit after Tax $49,152 $47,439 $44,093 $42,570

Total Equity $2,72,341 $2,49,608 $2,26,348 $1,97,814

Cost of Equity 18.05% 19.01% 19.48% 21.52%

Weightage of Equity 100.00% 100.00% 99.12% 100.00%

Interest Expenses for

secured borrowings 0 0 220 0

Secured Borrowings $0 $0 $2,000 $0

Cost of Debt 0% 0% 11.00% 0%

Weightage of Debt 0% 0% 1% 0%

Tax Rate 30% 30% 30% 30%

WACC 18.05% 19.01% 19.39% 21.52%

Cost of Capital Under CAPM

As per CAPM method, the risks which is calculated following the value of by Beta (B),

risk free rate of return and market rate of return for the purpose. This method is considered to be

one of the most popular methods of analyzing a viability or the worth of a project (Baker &

Wurgler, 2015). The cost of capital which is computed following CAPM approach comes to

about 7.906% which is a favorable result as the market rate of return is 8.54% which means the

needs of the shareholders are meet.

Cost of Equity under CAPM:

Particulars Amount

Beta 0.89

Market Return 8.54%

Risk Free Rate 2.78%

Expected Cost of Equity 7.906%

8

ACCOUNTING AND FINANCE

Comparison between ARB ltd and Modine ltd

For the purpose of conducting a comparative study, Modine ltd is selected which belongs

to the same industry as ARB ltd. The first observation which is made judging by the capital

structure of Modine ltd is that the company has a favorable capital structure and has employed

both equity and debt capital which are $ 421.20 million and 519.90 million respectively. ARB ltd

only has employed equity capital in the capital mix of the business.

Particulars Amount Weightage Amount Weightage

(in '000s) (in million)

Total Equity $2,72,341 100% $421.20 45%

Secured Borrowings:

Short Term Debt $73.4

Current Portion of Long

Term Debt $31.8

Long Term Debt $405.7

Total Secured Borrowings $0 0% $510.90 55%

TOTAL CAPITAL $2,72,341 100% $932 100%

ARB MODINE

COMPARISON with MODINE MANUFACTURING COMPANY

Financial Ratios of ARB Ltd

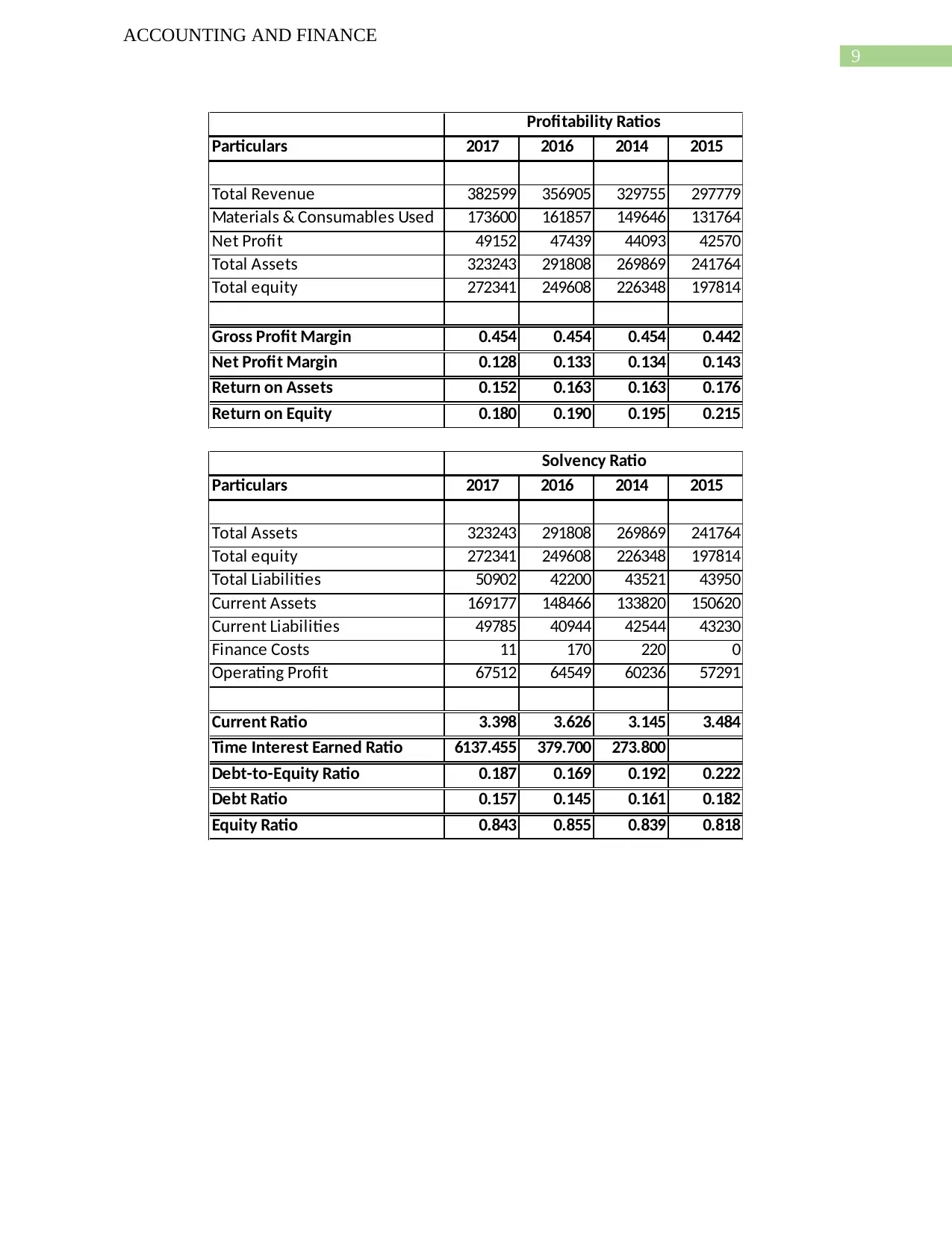

The current ratio which is covered in the liquidity ratio of the business shows that the

ratio has increased from previous year which suggest that the liquidity situations of the company

has improved. The debt equity ratio shows a slight increase in the ratio from the previous year’s

estimate (Fitó, Moya & Orgaz, 2013). The net profit margin of the company has reduced which

may be due to some issues which the company might be facing with the operational activities of

the business. The efficiency ratio of the business also shows favorable results especially

inventory turnover ratio.

ACCOUNTING AND FINANCE

Comparison between ARB ltd and Modine ltd

For the purpose of conducting a comparative study, Modine ltd is selected which belongs

to the same industry as ARB ltd. The first observation which is made judging by the capital

structure of Modine ltd is that the company has a favorable capital structure and has employed

both equity and debt capital which are $ 421.20 million and 519.90 million respectively. ARB ltd

only has employed equity capital in the capital mix of the business.

Particulars Amount Weightage Amount Weightage

(in '000s) (in million)

Total Equity $2,72,341 100% $421.20 45%

Secured Borrowings:

Short Term Debt $73.4

Current Portion of Long

Term Debt $31.8

Long Term Debt $405.7

Total Secured Borrowings $0 0% $510.90 55%

TOTAL CAPITAL $2,72,341 100% $932 100%

ARB MODINE

COMPARISON with MODINE MANUFACTURING COMPANY

Financial Ratios of ARB Ltd

The current ratio which is covered in the liquidity ratio of the business shows that the

ratio has increased from previous year which suggest that the liquidity situations of the company

has improved. The debt equity ratio shows a slight increase in the ratio from the previous year’s

estimate (Fitó, Moya & Orgaz, 2013). The net profit margin of the company has reduced which

may be due to some issues which the company might be facing with the operational activities of

the business. The efficiency ratio of the business also shows favorable results especially

inventory turnover ratio.

9

ACCOUNTING AND FINANCE

Particulars 2017 2016 2014 2015

Total Revenue 382599 356905 329755 297779

Materials & Consumables Used 173600 161857 149646 131764

Net Profit 49152 47439 44093 42570

Total Assets 323243 291808 269869 241764

Total equity 272341 249608 226348 197814

Gross Profit Margin 0.454 0.454 0.454 0.442

Net Profit Margin 0.128 0.133 0.134 0.143

Return on Assets 0.152 0.163 0.163 0.176

Return on Equity 0.180 0.190 0.195 0.215

Profitability Ratios

Particulars 2017 2016 2014 2015

Total Assets 323243 291808 269869 241764

Total equity 272341 249608 226348 197814

Total Liabilities 50902 42200 43521 43950

Current Assets 169177 148466 133820 150620

Current Liabilities 49785 40944 42544 43230

Finance Costs 11 170 220 0

Operating Profit 67512 64549 60236 57291

Current Ratio 3.398 3.626 3.145 3.484

Time Interest Earned Ratio 6137.455 379.700 273.800

Debt-to-Equity Ratio 0.187 0.169 0.192 0.222

Debt Ratio 0.157 0.145 0.161 0.182

Equity Ratio 0.843 0.855 0.839 0.818

Solvency Ratio

ACCOUNTING AND FINANCE

Particulars 2017 2016 2014 2015

Total Revenue 382599 356905 329755 297779

Materials & Consumables Used 173600 161857 149646 131764

Net Profit 49152 47439 44093 42570

Total Assets 323243 291808 269869 241764

Total equity 272341 249608 226348 197814

Gross Profit Margin 0.454 0.454 0.454 0.442

Net Profit Margin 0.128 0.133 0.134 0.143

Return on Assets 0.152 0.163 0.163 0.176

Return on Equity 0.180 0.190 0.195 0.215

Profitability Ratios

Particulars 2017 2016 2014 2015

Total Assets 323243 291808 269869 241764

Total equity 272341 249608 226348 197814

Total Liabilities 50902 42200 43521 43950

Current Assets 169177 148466 133820 150620

Current Liabilities 49785 40944 42544 43230

Finance Costs 11 170 220 0

Operating Profit 67512 64549 60236 57291

Current Ratio 3.398 3.626 3.145 3.484

Time Interest Earned Ratio 6137.455 379.700 273.800

Debt-to-Equity Ratio 0.187 0.169 0.192 0.222

Debt Ratio 0.157 0.145 0.161 0.182

Equity Ratio 0.843 0.855 0.839 0.818

Solvency Ratio

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

ACCOUNTING AND FINANCE

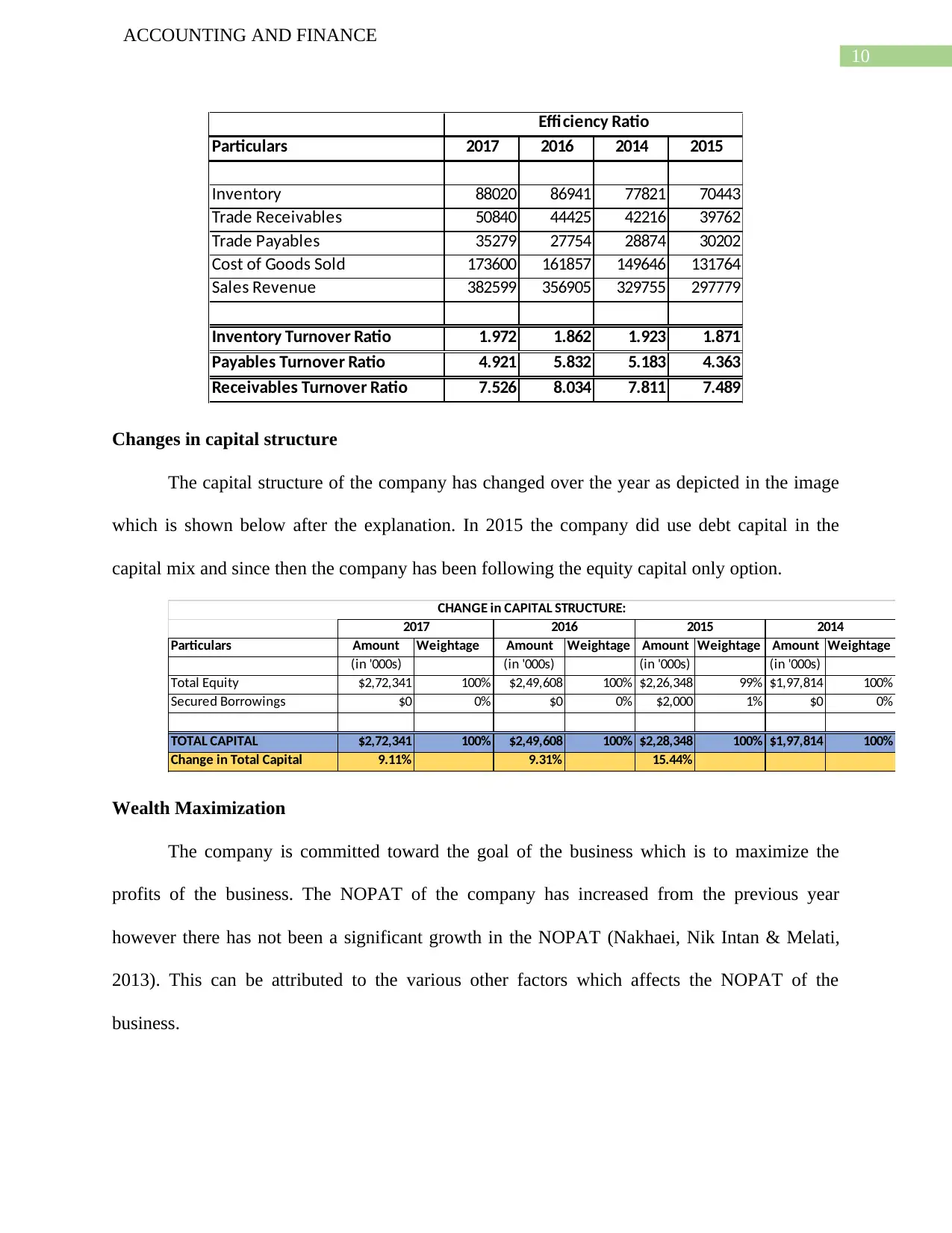

Particulars 2017 2016 2014 2015

Inventory 88020 86941 77821 70443

Trade Receivables 50840 44425 42216 39762

Trade Payables 35279 27754 28874 30202

Cost of Goods Sold 173600 161857 149646 131764

Sales Revenue 382599 356905 329755 297779

Inventory Turnover Ratio 1.972 1.862 1.923 1.871

Payables Turnover Ratio 4.921 5.832 5.183 4.363

Receivables Turnover Ratio 7.526 8.034 7.811 7.489

Efficiency Ratio

Changes in capital structure

The capital structure of the company has changed over the year as depicted in the image

which is shown below after the explanation. In 2015 the company did use debt capital in the

capital mix and since then the company has been following the equity capital only option.

Particulars Amount Weightage Amount Weightage Amount Weightage Amount Weightage

(in '000s) (in '000s) (in '000s) (in '000s)

Total Equity $2,72,341 100% $2,49,608 100% $2,26,348 99% $1,97,814 100%

Secured Borrowings $0 0% $0 0% $2,000 1% $0 0%

TOTAL CAPITAL $2,72,341 100% $2,49,608 100% $2,28,348 100% $1,97,814 100%

Change in Total Capital 9.11% 9.31% 15.44%

2015 2014

CHANGE in CAPITAL STRUCTURE:

2017 2016

Wealth Maximization

The company is committed toward the goal of the business which is to maximize the

profits of the business. The NOPAT of the company has increased from the previous year

however there has not been a significant growth in the NOPAT (Nakhaei, Nik Intan & Melati,

2013). This can be attributed to the various other factors which affects the NOPAT of the

business.

ACCOUNTING AND FINANCE

Particulars 2017 2016 2014 2015

Inventory 88020 86941 77821 70443

Trade Receivables 50840 44425 42216 39762

Trade Payables 35279 27754 28874 30202

Cost of Goods Sold 173600 161857 149646 131764

Sales Revenue 382599 356905 329755 297779

Inventory Turnover Ratio 1.972 1.862 1.923 1.871

Payables Turnover Ratio 4.921 5.832 5.183 4.363

Receivables Turnover Ratio 7.526 8.034 7.811 7.489

Efficiency Ratio

Changes in capital structure

The capital structure of the company has changed over the year as depicted in the image

which is shown below after the explanation. In 2015 the company did use debt capital in the

capital mix and since then the company has been following the equity capital only option.

Particulars Amount Weightage Amount Weightage Amount Weightage Amount Weightage

(in '000s) (in '000s) (in '000s) (in '000s)

Total Equity $2,72,341 100% $2,49,608 100% $2,26,348 99% $1,97,814 100%

Secured Borrowings $0 0% $0 0% $2,000 1% $0 0%

TOTAL CAPITAL $2,72,341 100% $2,49,608 100% $2,28,348 100% $1,97,814 100%

Change in Total Capital 9.11% 9.31% 15.44%

2015 2014

CHANGE in CAPITAL STRUCTURE:

2017 2016

Wealth Maximization

The company is committed toward the goal of the business which is to maximize the

profits of the business. The NOPAT of the company has increased from the previous year

however there has not been a significant growth in the NOPAT (Nakhaei, Nik Intan & Melati,

2013). This can be attributed to the various other factors which affects the NOPAT of the

business.

11

ACCOUNTING AND FINANCE

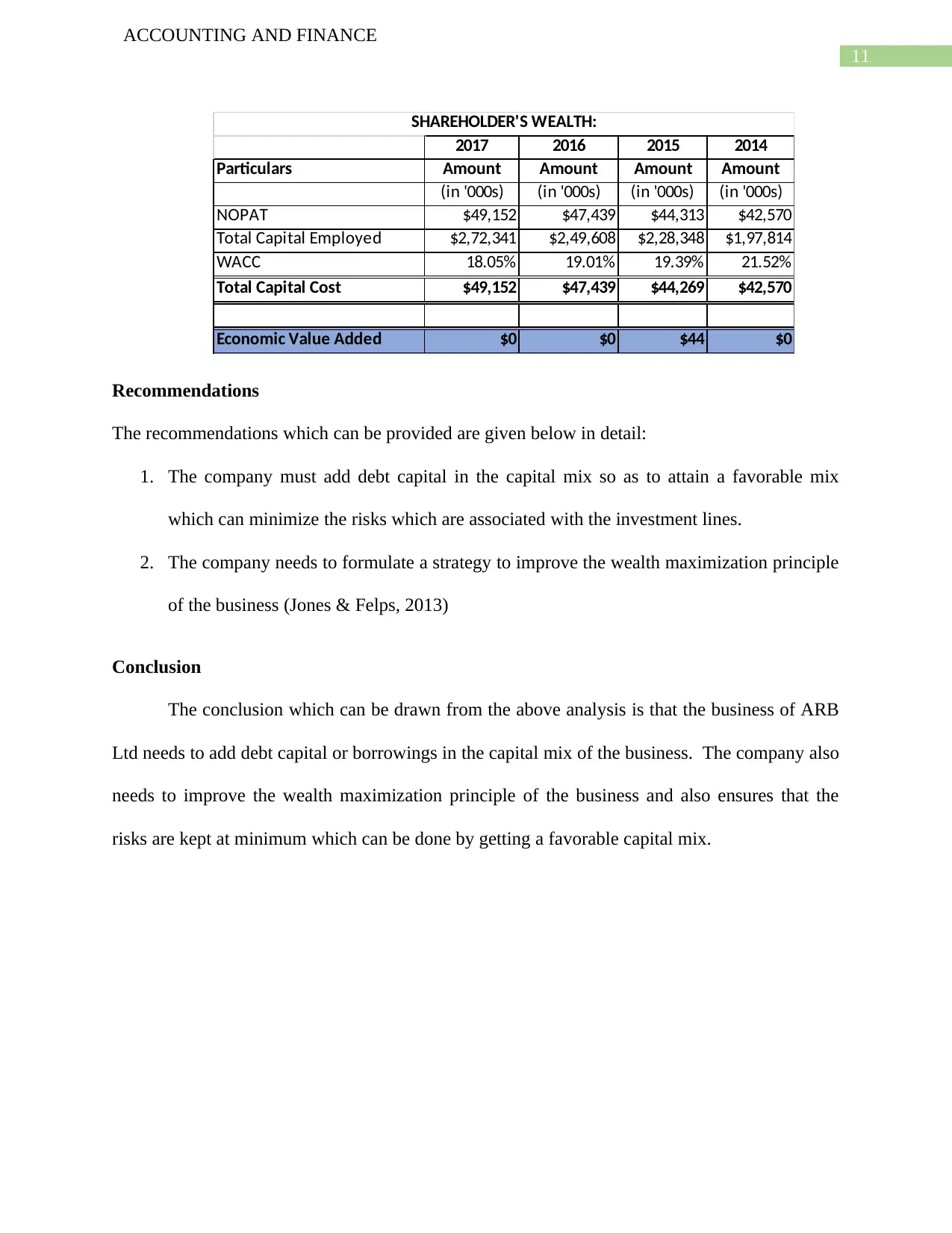

2017 2016 2015 2014

Particulars Amount Amount Amount Amount

(in '000s) (in '000s) (in '000s) (in '000s)

NOPAT $49,152 $47,439 $44,313 $42,570

Total Capital Employed $2,72,341 $2,49,608 $2,28,348 $1,97,814

WACC 18.05% 19.01% 19.39% 21.52%

Total Capital Cost $49,152 $47,439 $44,269 $42,570

Economic Value Added $0 $0 $44 $0

SHAREHOLDER'S WEALTH:

Recommendations

The recommendations which can be provided are given below in detail:

1. The company must add debt capital in the capital mix so as to attain a favorable mix

which can minimize the risks which are associated with the investment lines.

2. The company needs to formulate a strategy to improve the wealth maximization principle

of the business (Jones & Felps, 2013)

Conclusion

The conclusion which can be drawn from the above analysis is that the business of ARB

Ltd needs to add debt capital or borrowings in the capital mix of the business. The company also

needs to improve the wealth maximization principle of the business and also ensures that the

risks are kept at minimum which can be done by getting a favorable capital mix.

ACCOUNTING AND FINANCE

2017 2016 2015 2014

Particulars Amount Amount Amount Amount

(in '000s) (in '000s) (in '000s) (in '000s)

NOPAT $49,152 $47,439 $44,313 $42,570

Total Capital Employed $2,72,341 $2,49,608 $2,28,348 $1,97,814

WACC 18.05% 19.01% 19.39% 21.52%

Total Capital Cost $49,152 $47,439 $44,269 $42,570

Economic Value Added $0 $0 $44 $0

SHAREHOLDER'S WEALTH:

Recommendations

The recommendations which can be provided are given below in detail:

1. The company must add debt capital in the capital mix so as to attain a favorable mix

which can minimize the risks which are associated with the investment lines.

2. The company needs to formulate a strategy to improve the wealth maximization principle

of the business (Jones & Felps, 2013)

Conclusion

The conclusion which can be drawn from the above analysis is that the business of ARB

Ltd needs to add debt capital or borrowings in the capital mix of the business. The company also

needs to improve the wealth maximization principle of the business and also ensures that the

risks are kept at minimum which can be done by getting a favorable capital mix.

12

ACCOUNTING AND FINANCE

Reference

Baker, M., & Wurgler, J. (2015). Do strict capital requirements raise the cost of capital? Bank

regulation, capital structure, and the low-risk anomaly. American Economic Review, 105(5), 315-

20.

Fitó, M. À., Moya, S., & Orgaz, N. (2013). Considering the effects of operating lease capitalization

on key financial ratios. Spanish Journal of Finance and Accounting/Revista Española de

Financiación y Contabilidad, 42(159), 341-369.

Graham, J. R., Leary, M. T., & Roberts, M. R. (2015). A century of capital structure: The

leveraging of corporate America. Journal of Financial Economics, 118(3), 658-683.

Jones, T. M., & Felps, W. (2013). Shareholder wealth maximization and social welfare: A

utilitarian critique. Business Ethics Quarterly, 23(2), 207-238.

Lin, C. Y., & Okudan, G. E. (2013). Planning for multiple-generation product lines using dynamic

variable state models with data input from similar products. Expert systems with

applications, 40(6).

Nakhaei, H., Nik Intan, H., & Melati, A. (2013). Analyzing the relationship between economic

value added (EVA) and accounting variables with share market value in Tehran stock exchange

(TSE). Middle-East Journal of Scientific Research, 16(11), 1589-1598.

Sanchez, A., Sevilla-Güitrón, V., Magaña, G., & Gutierrez, L. (2013). Parametric analysis of total

costs and energy efficiency of 2G enzymatic ethanol production. Fuel, 113, 165-179.

ACCOUNTING AND FINANCE

Reference

Baker, M., & Wurgler, J. (2015). Do strict capital requirements raise the cost of capital? Bank

regulation, capital structure, and the low-risk anomaly. American Economic Review, 105(5), 315-

20.

Fitó, M. À., Moya, S., & Orgaz, N. (2013). Considering the effects of operating lease capitalization

on key financial ratios. Spanish Journal of Finance and Accounting/Revista Española de

Financiación y Contabilidad, 42(159), 341-369.

Graham, J. R., Leary, M. T., & Roberts, M. R. (2015). A century of capital structure: The

leveraging of corporate America. Journal of Financial Economics, 118(3), 658-683.

Jones, T. M., & Felps, W. (2013). Shareholder wealth maximization and social welfare: A

utilitarian critique. Business Ethics Quarterly, 23(2), 207-238.

Lin, C. Y., & Okudan, G. E. (2013). Planning for multiple-generation product lines using dynamic

variable state models with data input from similar products. Expert systems with

applications, 40(6).

Nakhaei, H., Nik Intan, H., & Melati, A. (2013). Analyzing the relationship between economic

value added (EVA) and accounting variables with share market value in Tehran stock exchange

(TSE). Middle-East Journal of Scientific Research, 16(11), 1589-1598.

Sanchez, A., Sevilla-Güitrón, V., Magaña, G., & Gutierrez, L. (2013). Parametric analysis of total

costs and energy efficiency of 2G enzymatic ethanol production. Fuel, 113, 165-179.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.