Sainsbury Plc: Financial Ratio Analysis and Performance Review

VerifiedAdded on 2020/12/29

|12

|3170

|190

Report

AI Summary

This report provides a comprehensive financial analysis of Sainsbury Plc, focusing on the years 2015, 2016, and 2017. The analysis includes the calculation and interpretation of various financial ratios, such as profitability, liquidity, efficiency, and market ratios. The report examines Sainsbury's performance in terms of return on capital employed, operating profit, gross profit margin, current ratio, quick ratio, settlement periods for trade receivables and payables, and inventory turnover. It also includes an overview of Sainsbury's background and business operations, along with an assessment of its financial stability and performance. Furthermore, the report offers recommendations for improvement and discusses the merits and demerits of using financial ratios for decision-making, catering to the expectations of potential investors. The analysis highlights trends and provides insights into Sainsbury's financial health over the specified period.

Accounting and Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION ..........................................................................................................................3

1. Justifying organisation's performance along with its background..........................................3

2. Defining and calculating financial ratios of Sainsbury Plc for the period of 2015, 2016 and

2017.............................................................................................................................................3

3. Analyzing performance of Sainsbury over the period and give recommendations for

improvement...............................................................................................................................4

4. Elaborating merits and demerits of financial ratios................................................................8

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION ..........................................................................................................................3

1. Justifying organisation's performance along with its background..........................................3

2. Defining and calculating financial ratios of Sainsbury Plc for the period of 2015, 2016 and

2017.............................................................................................................................................3

3. Analyzing performance of Sainsbury over the period and give recommendations for

improvement...............................................................................................................................4

4. Elaborating merits and demerits of financial ratios................................................................8

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial management is replicated as managing money in proper and efficient manner

in order to accomplishing the goals and objective of any specific organizations. It is directly

associated with the board committees or top management. Financial stratgey of any

organization or company is directly interlinked with this specific term but on its contrary

individual management strategy has relationship with personal finance or financial life

management. The present report is giving brief description about appropriate analysis of finance

by choosing organization which is listed on London Stock Exchange i.e. Sainsburry Plc. It has

been undertaken by considering profitability, liquidity, efficiency and market indicator. Further

it has elaborated about financial performance and stability of organization through non financial

information as well. In this report, recommendations has been provided in context of

management and potential investor whose expectation is about £2 million for investing in

particular organization. In the same series, various merits and demerits of financial ratios has

been elaborated and comparison of different ratios along with different decisions which are

relevant has been interpreted.

1. Justifying organisation's performance along with its background.

Sainsbury has gained second position with 16.9% share in context of supermarkets in

the United Kingdom. The organization was founded by the James Sainsbury with a shop in

duary lane in London. It became the largest seller of groceries in 1922. J Sainsbury plc is

directly involved in retailing grocery related products in the United Kingdom.

Financial report of Sainsbury of November 2017 in November 2107, Sainsbury hit by

sharp fall in quarterly sales growth. The retailer told that in the same store sales rose by 0.6% in

3 months to September compared with the same time in last year. This contrasted with the 2.3

% quarterly growth in July (Stent and et. al., 2017). Sainsbury’s, which has adopted pricing

strategy for purpose of promoting special offers to an approach of low prices every day. It had

also reported a decrease in pre-tax margin for the half-year till June. Earnings which were

measured on this basis resulted as £220m, as it is compared with £372m this year.

2. Defining and calculating financial ratios of Sainsbury Plc for the period of 2015, 2016 and

2017

Ratio analysis of Sainsbury for the period of 3 years is as follows:

Financial management is replicated as managing money in proper and efficient manner

in order to accomplishing the goals and objective of any specific organizations. It is directly

associated with the board committees or top management. Financial stratgey of any

organization or company is directly interlinked with this specific term but on its contrary

individual management strategy has relationship with personal finance or financial life

management. The present report is giving brief description about appropriate analysis of finance

by choosing organization which is listed on London Stock Exchange i.e. Sainsburry Plc. It has

been undertaken by considering profitability, liquidity, efficiency and market indicator. Further

it has elaborated about financial performance and stability of organization through non financial

information as well. In this report, recommendations has been provided in context of

management and potential investor whose expectation is about £2 million for investing in

particular organization. In the same series, various merits and demerits of financial ratios has

been elaborated and comparison of different ratios along with different decisions which are

relevant has been interpreted.

1. Justifying organisation's performance along with its background.

Sainsbury has gained second position with 16.9% share in context of supermarkets in

the United Kingdom. The organization was founded by the James Sainsbury with a shop in

duary lane in London. It became the largest seller of groceries in 1922. J Sainsbury plc is

directly involved in retailing grocery related products in the United Kingdom.

Financial report of Sainsbury of November 2017 in November 2107, Sainsbury hit by

sharp fall in quarterly sales growth. The retailer told that in the same store sales rose by 0.6% in

3 months to September compared with the same time in last year. This contrasted with the 2.3

% quarterly growth in July (Stent and et. al., 2017). Sainsbury’s, which has adopted pricing

strategy for purpose of promoting special offers to an approach of low prices every day. It had

also reported a decrease in pre-tax margin for the half-year till June. Earnings which were

measured on this basis resulted as £220m, as it is compared with £372m this year.

2. Defining and calculating financial ratios of Sainsbury Plc for the period of 2015, 2016 and

2017

Ratio analysis of Sainsbury for the period of 3 years is as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

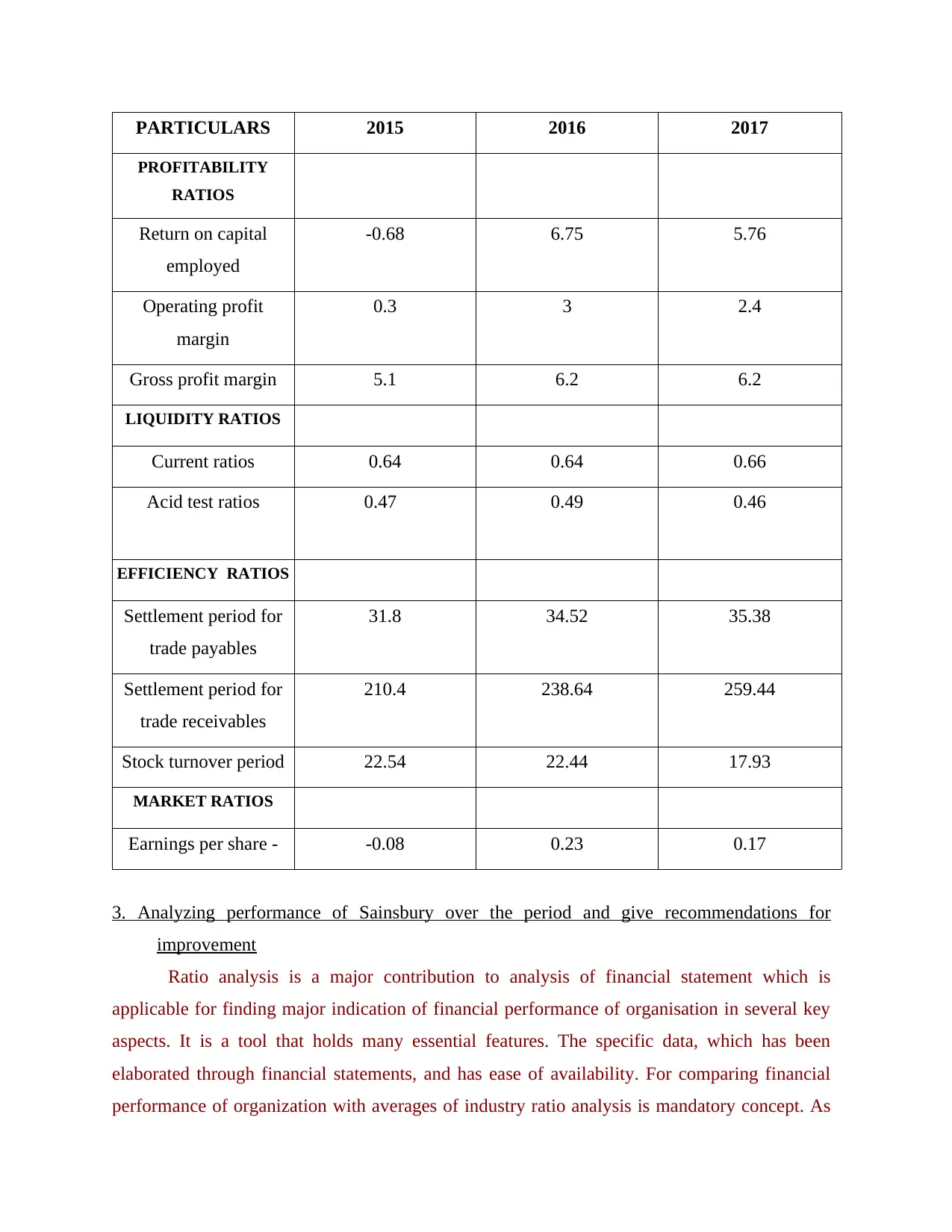

PARTICULARS 2015 2016 2017

PROFITABILITY

RATIOS

Return on capital

employed

-0.68 6.75 5.76

Operating profit

margin

0.3 3 2.4

Gross profit margin 5.1 6.2 6.2

LIQUIDITY RATIOS

Current ratios 0.64 0.64 0.66

Acid test ratios 0.47 0.49 0.46

EFFICIENCY RATIOS

Settlement period for

trade payables

31.8 34.52 35.38

Settlement period for

trade receivables

210.4 238.64 259.44

Stock turnover period 22.54 22.44 17.93

MARKET RATIOS

Earnings per share - -0.08 0.23 0.17

3. Analyzing performance of Sainsbury over the period and give recommendations for

improvement

Ratio analysis is a major contribution to analysis of financial statement which is

applicable for finding major indication of financial performance of organisation in several key

aspects. It is a tool that holds many essential features. The specific data, which has been

elaborated through financial statements, and has ease of availability. For comparing financial

performance of organization with averages of industry ratio analysis is mandatory concept. As

PROFITABILITY

RATIOS

Return on capital

employed

-0.68 6.75 5.76

Operating profit

margin

0.3 3 2.4

Gross profit margin 5.1 6.2 6.2

LIQUIDITY RATIOS

Current ratios 0.64 0.64 0.66

Acid test ratios 0.47 0.49 0.46

EFFICIENCY RATIOS

Settlement period for

trade payables

31.8 34.52 35.38

Settlement period for

trade receivables

210.4 238.64 259.44

Stock turnover period 22.54 22.44 17.93

MARKET RATIOS

Earnings per share - -0.08 0.23 0.17

3. Analyzing performance of Sainsbury over the period and give recommendations for

improvement

Ratio analysis is a major contribution to analysis of financial statement which is

applicable for finding major indication of financial performance of organisation in several key

aspects. It is a tool that holds many essential features. The specific data, which has been

elaborated through financial statements, and has ease of availability. For comparing financial

performance of organization with averages of industry ratio analysis is mandatory concept. As

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

it can be also applicable for trend analysis to extract areas where is presence of improvement in

performance over time. Dependency has been created by ratio analysis for accounting

information; as it ha limited effectiveness in context of distortion which arises in each financial

statements because of inflation. It is a first step in financial analysis to obtain the current

position of the business (Elliot and et. al., 2018).

These are very powerful tools to perform very quick analysis of statements. Basically

these are of four types liquidity ratio, activity ratios, profitability ratio and leverages ratio. Ratio

analysis is a powerful tool which helps to determine the company's current position with the

help of financial figures.

Profitability ratio analysis

Return on capital employed- It is termed as profitability indicator which is measuring

level of efficiency of Sainsbury which is capable of generating margin via its capital which is

employed and net operating profit has been directly compared with capital employed. In simple

words it can be indicated that how much quantity of margin of capital employed generates.

From 2015 to 2016 return on capital employed increase from -0.68% to 6.75 %. In 2015 return

on capital employed was in huge loss which is not beneficial for company's financial aspects.

Decline in 2015 shows that there was less sales in 2015 or it may happen due to increase in cost

or more debt. But from 2015 to 2016 the return on capital employed increases with 6.75 %

which provide a good financial stability to the Sainsbury limited. But later in 2017 it slightly

falls with .99 % and became 5.76 % due to decline in sales as comparison to 2016.

Operating profit- It is tracing profitability of organization along with its capacity after

repaying its variable costs of production like raw materials, wages etc. It is reflecting level of

efficiency of Sainsbury for cost controlling and expenses as well which are directly associated

with operations of business. From the year 2015 to 2016 the operating profit of the Sainsbury

increases from 0.3 % to 3 %, which was the good prospectus of the company in 2015 the

Sainsbury’s operating profit was very low due to high rise in operating expenses , in 2016 it

was increases but on 2017 the operating profit of the company falls from 3% to 2.4% due to

increase in expenses. To increase the operating profit of the organization Sainsbury should

focus on the profitable items . They have to follow those strategies which help to increase in its

sales revenue . Sainsbury should develop new product lines , increase productivity of your staff

,improve your customers services (Weygandt, Kimmel and Kieso, 2015).

performance over time. Dependency has been created by ratio analysis for accounting

information; as it ha limited effectiveness in context of distortion which arises in each financial

statements because of inflation. It is a first step in financial analysis to obtain the current

position of the business (Elliot and et. al., 2018).

These are very powerful tools to perform very quick analysis of statements. Basically

these are of four types liquidity ratio, activity ratios, profitability ratio and leverages ratio. Ratio

analysis is a powerful tool which helps to determine the company's current position with the

help of financial figures.

Profitability ratio analysis

Return on capital employed- It is termed as profitability indicator which is measuring

level of efficiency of Sainsbury which is capable of generating margin via its capital which is

employed and net operating profit has been directly compared with capital employed. In simple

words it can be indicated that how much quantity of margin of capital employed generates.

From 2015 to 2016 return on capital employed increase from -0.68% to 6.75 %. In 2015 return

on capital employed was in huge loss which is not beneficial for company's financial aspects.

Decline in 2015 shows that there was less sales in 2015 or it may happen due to increase in cost

or more debt. But from 2015 to 2016 the return on capital employed increases with 6.75 %

which provide a good financial stability to the Sainsbury limited. But later in 2017 it slightly

falls with .99 % and became 5.76 % due to decline in sales as comparison to 2016.

Operating profit- It is tracing profitability of organization along with its capacity after

repaying its variable costs of production like raw materials, wages etc. It is reflecting level of

efficiency of Sainsbury for cost controlling and expenses as well which are directly associated

with operations of business. From the year 2015 to 2016 the operating profit of the Sainsbury

increases from 0.3 % to 3 %, which was the good prospectus of the company in 2015 the

Sainsbury’s operating profit was very low due to high rise in operating expenses , in 2016 it

was increases but on 2017 the operating profit of the company falls from 3% to 2.4% due to

increase in expenses. To increase the operating profit of the organization Sainsbury should

focus on the profitable items . They have to follow those strategies which help to increase in its

sales revenue . Sainsbury should develop new product lines , increase productivity of your staff

,improve your customers services (Weygandt, Kimmel and Kieso, 2015).

Gross profit margin- It is also termed as ratio of gross margin which is depicted as

percentage of sales. It is replicating quantity of profit of organization repaying cost of goods

sold. If specific percentage is higher or growing than organization belong to efficient category.

From the year 2015 to the year 2016 the gross profit of the Sainsbury increases from 5.1% to

6.2% which was the sign of growth for the company. It happens due to decrease in cost of

goods sold. Further, the company was able to maintain its position in next year 2017 as well. By

observing the slight fall in 2017 shows that companies expenditure are increasing than the

company's income. To overcome from this Sainsbury need to restrict their expenditure and they

have to apply the budgetary control techniques in order to manage their inventory as well as

occurring expenditure.

Liquidity ratios

Current ratio- During the period of three years Sainsbury succeed in attaining the ideal

ratio in 2015 – 2016. Hence, from 2015 to 2017 Sainsbury has maintained its current assets in

appropriate manner but its exception is inventory and prepaid which could be easily converted

into cash. Therefore, current ratio of Sainsbury also inclined from 0.64 to 0.66 during the year.

2:1 is considered as ideal current ratio which signified that current assets are double than

current liability, then it is considered as satisfactory. For improving the current ratio there is

requirement by Sainsbury to focus on its different strategies which consist of current liabilities

and assets which cannot be known as one time activity. It has to be properly tracked throughout

the year. Current ratio can be improved by rolling of money in fast aspect through debtors

which will control current ratio. By increasing shareholder's fund current ratio could be

improved. When there is presence of financing current asset through equity instead of creditors,

as it will raise current liability and rest is considered as same (Francis and et. al., 2015).

Quick ratio- By analysing this quick ratio, it has been identified Sainsbury's quick ratio

is fluctuating within three years. While comparing it from past current ratio of 2 years which

got increment from 0.46 times to 0.49 in the ending of financial year in 2017- 2016. It reflects

capability of organization in context of fulfilling various obligation fluctuate or the year. The

quick ratio of Sainsbury was .47 .49 and .46 from the year 2015 to 2017. In contrast to this ,

quick ratio account for year 2015 and 2016 was calculated as .47 to .49 respectively with

specific objective for increasing customer base and market share. Sainsbury had set special

percentage of sales. It is replicating quantity of profit of organization repaying cost of goods

sold. If specific percentage is higher or growing than organization belong to efficient category.

From the year 2015 to the year 2016 the gross profit of the Sainsbury increases from 5.1% to

6.2% which was the sign of growth for the company. It happens due to decrease in cost of

goods sold. Further, the company was able to maintain its position in next year 2017 as well. By

observing the slight fall in 2017 shows that companies expenditure are increasing than the

company's income. To overcome from this Sainsbury need to restrict their expenditure and they

have to apply the budgetary control techniques in order to manage their inventory as well as

occurring expenditure.

Liquidity ratios

Current ratio- During the period of three years Sainsbury succeed in attaining the ideal

ratio in 2015 – 2016. Hence, from 2015 to 2017 Sainsbury has maintained its current assets in

appropriate manner but its exception is inventory and prepaid which could be easily converted

into cash. Therefore, current ratio of Sainsbury also inclined from 0.64 to 0.66 during the year.

2:1 is considered as ideal current ratio which signified that current assets are double than

current liability, then it is considered as satisfactory. For improving the current ratio there is

requirement by Sainsbury to focus on its different strategies which consist of current liabilities

and assets which cannot be known as one time activity. It has to be properly tracked throughout

the year. Current ratio can be improved by rolling of money in fast aspect through debtors

which will control current ratio. By increasing shareholder's fund current ratio could be

improved. When there is presence of financing current asset through equity instead of creditors,

as it will raise current liability and rest is considered as same (Francis and et. al., 2015).

Quick ratio- By analysing this quick ratio, it has been identified Sainsbury's quick ratio

is fluctuating within three years. While comparing it from past current ratio of 2 years which

got increment from 0.46 times to 0.49 in the ending of financial year in 2017- 2016. It reflects

capability of organization in context of fulfilling various obligation fluctuate or the year. The

quick ratio of Sainsbury was .47 .49 and .46 from the year 2015 to 2017. In contrast to this ,

quick ratio account for year 2015 and 2016 was calculated as .47 to .49 respectively with

specific objective for increasing customer base and market share. Sainsbury had set special

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

focus on various promotional aspects in strategies of discounting. It is the main reason that

company could not hold the more quick asset.

Efficiency ratios

Settlement period for trade receivables: It is also known as average collection period

and assumption has been taken for its calculations. It helps in comparing outstanding

receivables of a business in context of its aggregate of sales. During the year from 2015 to 2017

the settlement period for trade receivables increases from 210.4 to 259.44. Gradual rise in

debtor collection period may leads to the huge loss to the organization. If the collection from

debt is not received in certain point of time it will give a huge loss to the firm. Sainsbury's

debtor collection period increased during the year from 210.4 to 259.44. To reduce the

settlement period for trade receivable Sainsbury should negotiate payment terms with its

suppliers, or automate credit control , company has to bring some changes in its credit policy.

Settlement period for trade payable- in the same series, average time has been considers

for paying its creditors and business according to oweance. During the year 2015 to 2017 the

settle period for the trade payable increases from 31.8 to 35.38. rise in settlement period for the

trade receivable provide profit to the company. As company gets raw material on credit so it

increase the working capital of the company. Sainsbury should take the credit from those

suppliers who give more time for payback credit (Sheidu and Yusuf, 2015).

Inventory turnover ratio- It is a ratio which is depicting time taken for selling and

replacing inventory in specific period. Usually organization can set there days in period with

this specific formula. From the analysis of the ratio, it is concluded that from the year 2015 to

2017 the stock turnover ratio decreases from 22.54 to 17. 93 hence company was unable to sold

and replace the inventory more quickly. By evaluating this aspect it can be justified that

business unit was not capable for generating cash in quick aspect via sales in year 2017 and

2016 as well. This aspect will be influnencing in negative manner with relationship of

management of working capital of organization. Thus, Financial statements reflects that

turnover of inventory got decreased from 22.44 times to 17.93 times. So in the same series it

can be interpreted that there was not presence of appropriate management of specific business

unit in this specific duration of three years. Sainsbury was not able to transform cash in quick

aspect by inventory as trend is also declining along with ratio of turnover. It can be articulated

company could not hold the more quick asset.

Efficiency ratios

Settlement period for trade receivables: It is also known as average collection period

and assumption has been taken for its calculations. It helps in comparing outstanding

receivables of a business in context of its aggregate of sales. During the year from 2015 to 2017

the settlement period for trade receivables increases from 210.4 to 259.44. Gradual rise in

debtor collection period may leads to the huge loss to the organization. If the collection from

debt is not received in certain point of time it will give a huge loss to the firm. Sainsbury's

debtor collection period increased during the year from 210.4 to 259.44. To reduce the

settlement period for trade receivable Sainsbury should negotiate payment terms with its

suppliers, or automate credit control , company has to bring some changes in its credit policy.

Settlement period for trade payable- in the same series, average time has been considers

for paying its creditors and business according to oweance. During the year 2015 to 2017 the

settle period for the trade payable increases from 31.8 to 35.38. rise in settlement period for the

trade receivable provide profit to the company. As company gets raw material on credit so it

increase the working capital of the company. Sainsbury should take the credit from those

suppliers who give more time for payback credit (Sheidu and Yusuf, 2015).

Inventory turnover ratio- It is a ratio which is depicting time taken for selling and

replacing inventory in specific period. Usually organization can set there days in period with

this specific formula. From the analysis of the ratio, it is concluded that from the year 2015 to

2017 the stock turnover ratio decreases from 22.54 to 17. 93 hence company was unable to sold

and replace the inventory more quickly. By evaluating this aspect it can be justified that

business unit was not capable for generating cash in quick aspect via sales in year 2017 and

2016 as well. This aspect will be influnencing in negative manner with relationship of

management of working capital of organization. Thus, Financial statements reflects that

turnover of inventory got decreased from 22.44 times to 17.93 times. So in the same series it

can be interpreted that there was not presence of appropriate management of specific business

unit in this specific duration of three years. Sainsbury was not able to transform cash in quick

aspect by inventory as trend is also declining along with ratio of turnover. It can be articulated

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

from overall assessment that inventory could be converted into cash. Moreover, due to changes

takes place to the significant level.

Market ratio

Earnings per share- It is also termed as net income per share which is measuring

market prospect ratio along with specific amount on basis of net income of per share which is

earned and outstanding. Even profits of huge organization per share could be directly compared

to profit per share of small organization. As according to the analysis of ratios from the year

2015 to 2017 the ratios are in such a way from 0.08 to 0.07 which overall leads to the fall in

earning per share of the company. If any specific interest has been gained by investor in any

source of income then there is basic requirement of ratio of EPS as it estimates the amount of

dividend which is existing. It can be directly review history of specific organization and in

various cases alterations of dividend is termed as best indicator for future dividend of actual

size. If high ratio has been attained by organization but it does not pay dividend as it gives

preference to reinvesting cash in their specific business for accomplishing additional growth. If

there is huge growth in earning in stock of organization than it will directly tend to raise

remaining stocks. From the perspective of long term, prices of stock are parallel to growth of

EPS but there is presence of relationship in increment of EPS and prices of stock which is not

linear in short term.(Earning Per Share, 2018).

Recommendation

From the above ratio analysis of Sainsbury, the outcome Is that company has progressed

in year 2017. As earlier it is seen that in 2015 company's return on capital employed as well as

gross profit margin was very low but over the year it has increases rapidly. If we will talk about

the current ratio of the company they have also increased from 0.64 to 0.66. On the basis of

current records of the company it can be considered that company will further progress. Access

to meaningful information is a prerequisite for reasoned investment decision and the proper

allocation of the capital. By observing the whole scenario the investors should invest in the

Sainsbury which inturns proves fruitful for the business (Tayeh, Al-Jarrah and Tarhini, 2015).

4. Elaborating merits and demerits of financial ratios

Following are the merits and demerits of financial ratios-

Advantages

takes place to the significant level.

Market ratio

Earnings per share- It is also termed as net income per share which is measuring

market prospect ratio along with specific amount on basis of net income of per share which is

earned and outstanding. Even profits of huge organization per share could be directly compared

to profit per share of small organization. As according to the analysis of ratios from the year

2015 to 2017 the ratios are in such a way from 0.08 to 0.07 which overall leads to the fall in

earning per share of the company. If any specific interest has been gained by investor in any

source of income then there is basic requirement of ratio of EPS as it estimates the amount of

dividend which is existing. It can be directly review history of specific organization and in

various cases alterations of dividend is termed as best indicator for future dividend of actual

size. If high ratio has been attained by organization but it does not pay dividend as it gives

preference to reinvesting cash in their specific business for accomplishing additional growth. If

there is huge growth in earning in stock of organization than it will directly tend to raise

remaining stocks. From the perspective of long term, prices of stock are parallel to growth of

EPS but there is presence of relationship in increment of EPS and prices of stock which is not

linear in short term.(Earning Per Share, 2018).

Recommendation

From the above ratio analysis of Sainsbury, the outcome Is that company has progressed

in year 2017. As earlier it is seen that in 2015 company's return on capital employed as well as

gross profit margin was very low but over the year it has increases rapidly. If we will talk about

the current ratio of the company they have also increased from 0.64 to 0.66. On the basis of

current records of the company it can be considered that company will further progress. Access

to meaningful information is a prerequisite for reasoned investment decision and the proper

allocation of the capital. By observing the whole scenario the investors should invest in the

Sainsbury which inturns proves fruitful for the business (Tayeh, Al-Jarrah and Tarhini, 2015).

4. Elaborating merits and demerits of financial ratios

Following are the merits and demerits of financial ratios-

Advantages

Budgeting

Budgeting can be defined as measuring various future events on basis of previous

experiences. The identification of figures for budget, budgeting is termed as key aspect. For

instance, preparation of sales budget could be performed with specific analysis of sales of past.

Planning and forecasting

The move in cost, sales, profit and other facts can be interpreted by computing different

ratios of accounting figures which are applicable. The trend analysis which has been performed

is very essential for planning and predicting future activities related to business.

3- Communication-

Ratios are considered as very useful and effective mode of communication as it has

major role in communicating and tracing progress and position which has been maintained by

various concerns of parties or owners as well.

DEMERITS

Limitations of financial statements

Ratios are extracted from obtained information on basis of important financial

statements. On the contrary side, it also suffers from various demerits which might impact level

and quality of analysis of ratio.

Different accounting policies

The different policies of accounting could be termed as stock calculation, applicably

charges of deprecation etc. as it frames data of accounting which could be able for comparing

two organizations.

Window dressing

Window dressing can be interpreted as reflection of financial statements in such aspect

which provides better position to specific business as compared to reality.

CONCLUSION

From the above study it can be concluded that financing and accounting plays very

important role in context of each organization whether it is small or big. It has been interpreted

in above report that profitability indicator is very essential for surviving and sustaining in

business with specific growth. It has been articulated from above analysis that Sainsburry is

increasing its financial performance and stability from year to year with huge growth and

innovation. Further it can be concluded that investor can invest in this specific organisation for

Budgeting can be defined as measuring various future events on basis of previous

experiences. The identification of figures for budget, budgeting is termed as key aspect. For

instance, preparation of sales budget could be performed with specific analysis of sales of past.

Planning and forecasting

The move in cost, sales, profit and other facts can be interpreted by computing different

ratios of accounting figures which are applicable. The trend analysis which has been performed

is very essential for planning and predicting future activities related to business.

3- Communication-

Ratios are considered as very useful and effective mode of communication as it has

major role in communicating and tracing progress and position which has been maintained by

various concerns of parties or owners as well.

DEMERITS

Limitations of financial statements

Ratios are extracted from obtained information on basis of important financial

statements. On the contrary side, it also suffers from various demerits which might impact level

and quality of analysis of ratio.

Different accounting policies

The different policies of accounting could be termed as stock calculation, applicably

charges of deprecation etc. as it frames data of accounting which could be able for comparing

two organizations.

Window dressing

Window dressing can be interpreted as reflection of financial statements in such aspect

which provides better position to specific business as compared to reality.

CONCLUSION

From the above study it can be concluded that financing and accounting plays very

important role in context of each organization whether it is small or big. It has been interpreted

in above report that profitability indicator is very essential for surviving and sustaining in

business with specific growth. It has been articulated from above analysis that Sainsburry is

increasing its financial performance and stability from year to year with huge growth and

innovation. Further it can be concluded that investor can invest in this specific organisation for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

purpose of accomplishing growth and better decisions regarding investment by evaluating

various merits and demerits of specific financial ratios.

various merits and demerits of specific financial ratios.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Elliot, B. and et. al., 2018. Profitability and investment‐based factor pricing models. Accounting

& Finance. 58(2). pp.397-421.

Francis, B. and et. al., 2015. Gender differences in financial reporting decision making:

Evidence from accounting conservatism. Contemporary Accounting Research. 32(3).

pp.1285-1318.

Sheidu, A. D. and Yusuf, H., 2015. Bank consolidation and improvement of shareholder value:

An empirical evaluation of return on capital employed following bank mergers in

Nigeria. American International Journal of Contemporary Research. 5(5). pp.240-246.

Stent, W. and et. al., 2017. Insights into accounting choice from the adoption timing of I

nternational F inancial R eporting S tandards. Accounting & Finance. 57. pp.255-276.

Tayeh, M., Al-Jarrah, I. M. and Tarhini, A., 2015. Accounting vs. market-based measures of

firm performance related to information technology investments. International Review of

Social Sciences and Humanities, 9(1), pp.129-145.

Weygandt, J. J., Kimmel, P. D. and Kieso, D. E., 2015. Financial & managerial accounting.

John Wiley & Sons.

ONLINE

Earning Per Share. 2018. [Online]. Available through

:<https://corporatefinanceinstitute.com/resources/knowledge/finance/earnings-per-share-

eps-formula/>.

Books and Journals

Elliot, B. and et. al., 2018. Profitability and investment‐based factor pricing models. Accounting

& Finance. 58(2). pp.397-421.

Francis, B. and et. al., 2015. Gender differences in financial reporting decision making:

Evidence from accounting conservatism. Contemporary Accounting Research. 32(3).

pp.1285-1318.

Sheidu, A. D. and Yusuf, H., 2015. Bank consolidation and improvement of shareholder value:

An empirical evaluation of return on capital employed following bank mergers in

Nigeria. American International Journal of Contemporary Research. 5(5). pp.240-246.

Stent, W. and et. al., 2017. Insights into accounting choice from the adoption timing of I

nternational F inancial R eporting S tandards. Accounting & Finance. 57. pp.255-276.

Tayeh, M., Al-Jarrah, I. M. and Tarhini, A., 2015. Accounting vs. market-based measures of

firm performance related to information technology investments. International Review of

Social Sciences and Humanities, 9(1), pp.129-145.

Weygandt, J. J., Kimmel, P. D. and Kieso, D. E., 2015. Financial & managerial accounting.

John Wiley & Sons.

ONLINE

Earning Per Share. 2018. [Online]. Available through

:<https://corporatefinanceinstitute.com/resources/knowledge/finance/earnings-per-share-

eps-formula/>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12