MBA Finance Report: Bujang Lapok Berhad Credit Line Recommendation

VerifiedAdded on 2022/11/24

|6

|798

|147

Report

AI Summary

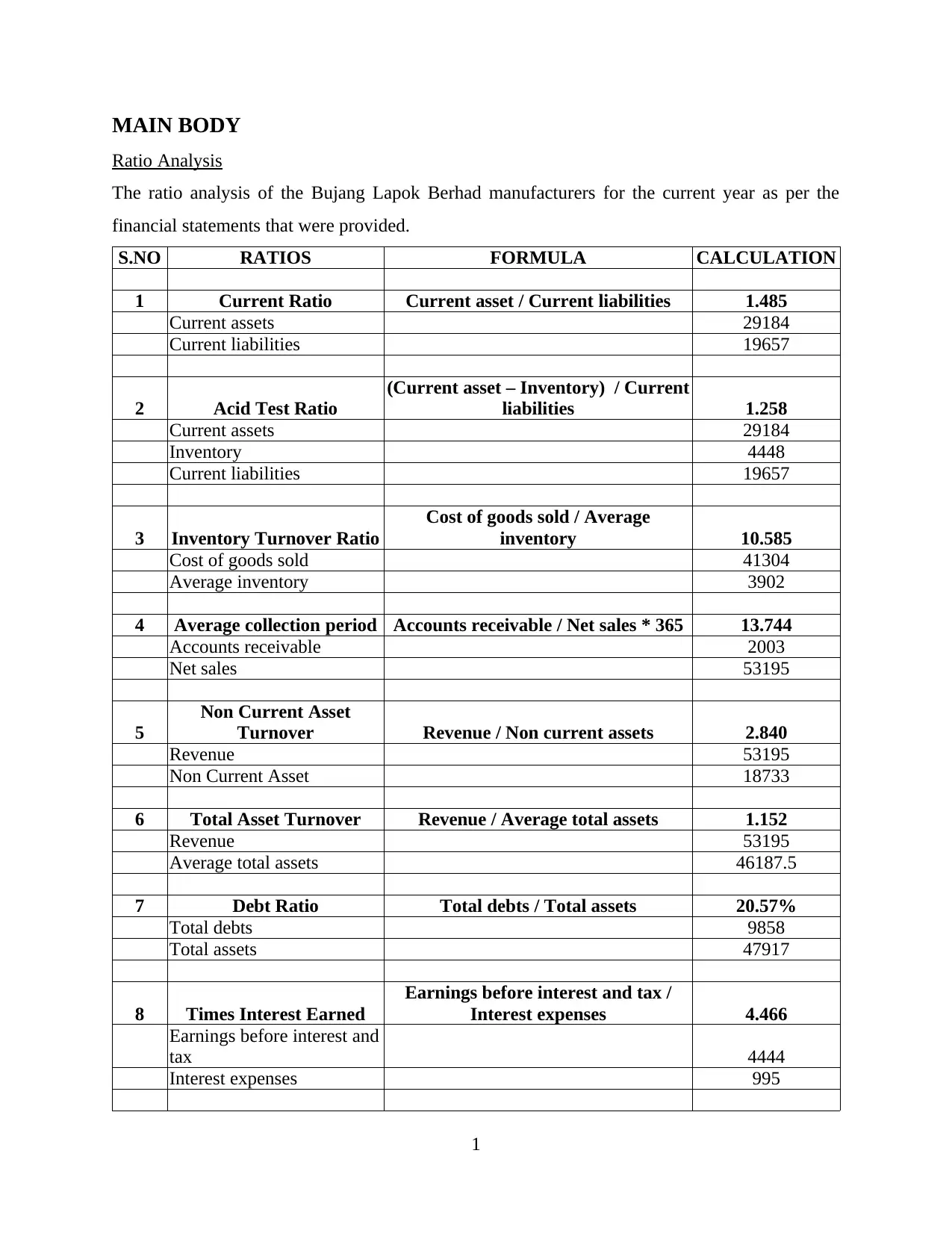

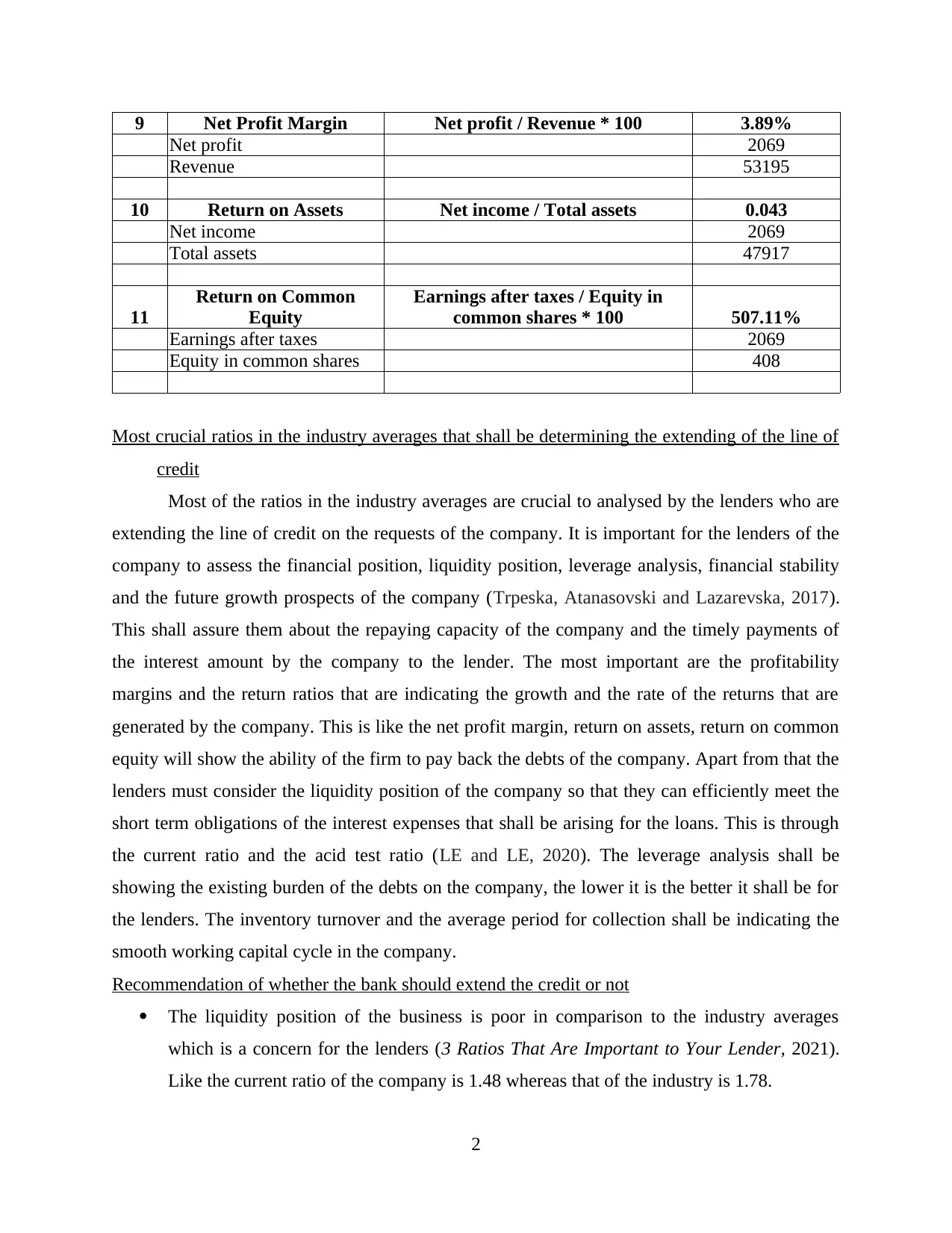

This report presents a financial analysis of Bujang Lapok Berhad, a sportswear manufacturer seeking a line of credit. It begins with a ratio analysis of the company's financial statements, calculating key metrics such as current ratio, acid test ratio, inventory turnover, and profitability ratios. The analysis compares these ratios to industry averages to assess the company's liquidity, profitability, and leverage. The report identifies the most crucial ratios for lenders, emphasizing profitability margins, return ratios, and the importance of liquidity and leverage analysis. The report then offers a recommendation on whether the bank should extend the credit, considering the company's performance against industry benchmarks. The conclusion is that the bank should consider the company's poor liquidity and profitability, which may influence the final decision. The report references several academic sources that support the analysis and recommendations.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.