Accounting and Finance: Analyzing ABC Costing for UAE Trekker LLC

VerifiedAdded on 2023/01/12

|9

|2263

|23

Report

AI Summary

This report presents an analysis of the implementation of Activity-Based Costing (ABC) in the context of UAE Trekker LLC, a company producing hiking backpacks. The report begins with calculations of cost per unit under both full absorption costing and ABC, highlighting the differences and the reasons behind them. It explains how the switch from traditional absorption costing to ABC impacts cost allocation, emphasizing the use of multiple cost drivers in ABC. The report then discusses the implications of switching to ABC for cost management, emphasizing its accuracy and reliability in determining product costs, especially in technology-driven environments. The impact of ABC on product profitability and pricing is explored, along with steps and pitfalls to consider when introducing an ABC system. The analysis also provides insights into the benefits of ABC in enhancing profitability through accurate pricing and streamlined business processes. The report concludes by summarizing the advantages of ABC over traditional costing methods.

Accounting and Finance for

Decision Making

Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

a. Calculation...............................................................................................................................3

b. Explaining the reasons for changes in the cost per unit at the time when costing system get

changed from an absorption costing towards ABC.....................................................................5

c. Presenting implications relating to cost management for switching to ABC system..............5

d. Explaining an impact of switching from absorption to ABC on product & pricing

profitability..................................................................................................................................6

e. Describing steps and the pitfalls that needs to be avoided at the time of introducing ABC

system within the business...........................................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

a. Calculation...............................................................................................................................3

b. Explaining the reasons for changes in the cost per unit at the time when costing system get

changed from an absorption costing towards ABC.....................................................................5

c. Presenting implications relating to cost management for switching to ABC system..............5

d. Explaining an impact of switching from absorption to ABC on product & pricing

profitability..................................................................................................................................6

e. Describing steps and the pitfalls that needs to be avoided at the time of introducing ABC

system within the business...........................................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

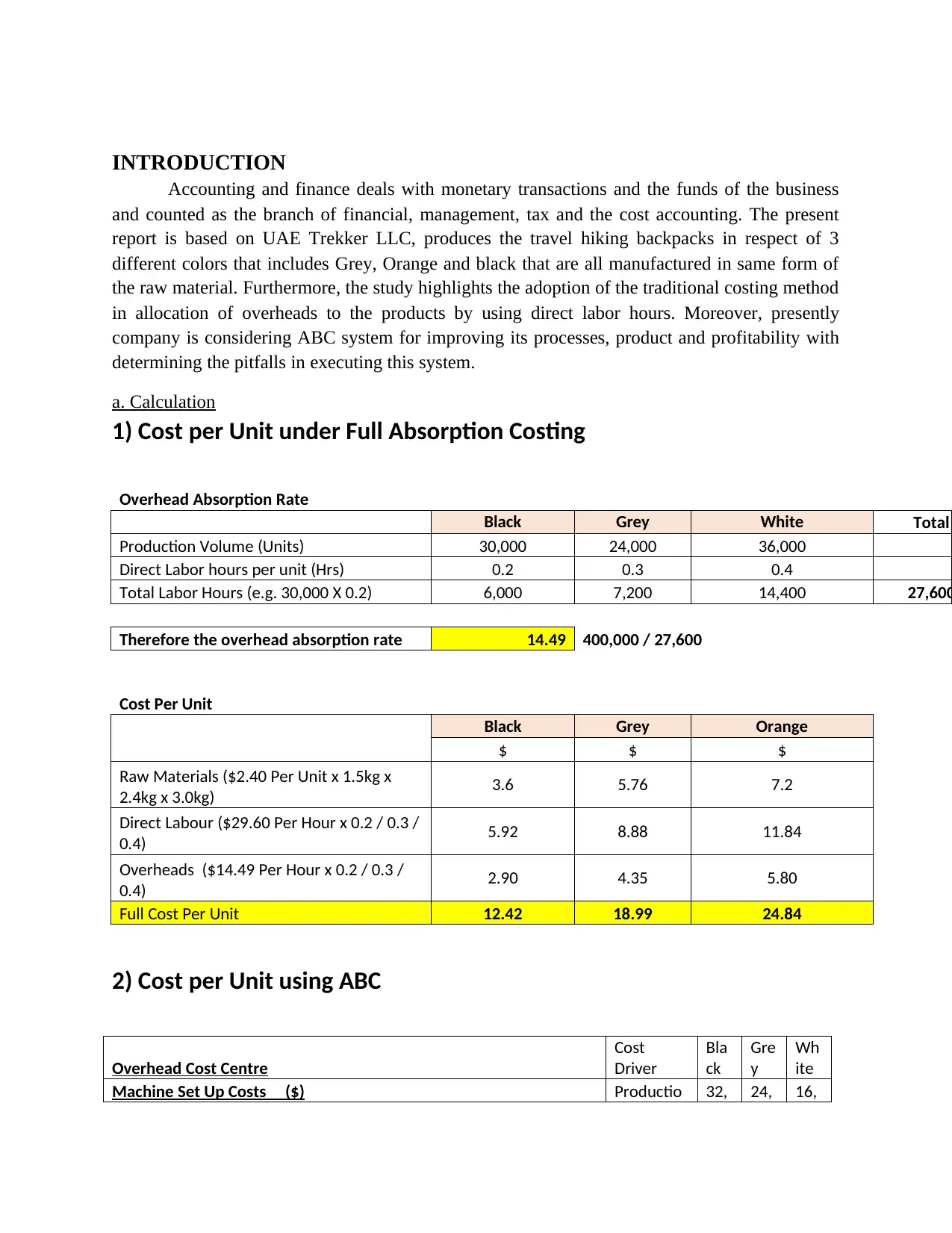

INTRODUCTION

Accounting and finance deals with monetary transactions and the funds of the business

and counted as the branch of financial, management, tax and the cost accounting. The present

report is based on UAE Trekker LLC, produces the travel hiking backpacks in respect of 3

different colors that includes Grey, Orange and black that are all manufactured in same form of

the raw material. Furthermore, the study highlights the adoption of the traditional costing method

in allocation of overheads to the products by using direct labor hours. Moreover, presently

company is considering ABC system for improving its processes, product and profitability with

determining the pitfalls in executing this system.

a. Calculation

1) Cost per Unit under Full Absorption Costing

Overhead Absorption Rate

Black Grey White Total

Production Volume (Units) 30,000 24,000 36,000

Direct Labor hours per unit (Hrs) 0.2 0.3 0.4

Total Labor Hours (e.g. 30,000 X 0.2) 6,000 7,200 14,400 27,600

Therefore the overhead absorption rate 14.49 400,000 / 27,600

Cost Per Unit

Black Grey Orange

$ $ $

Raw Materials ($2.40 Per Unit x 1.5kg x

2.4kg x 3.0kg) 3.6 5.76 7.2

Direct Labour ($29.60 Per Hour x 0.2 / 0.3 /

0.4) 5.92 8.88 11.84

Overheads ($14.49 Per Hour x 0.2 / 0.3 /

0.4) 2.90 4.35 5.80

Full Cost Per Unit 12.42 18.99 24.84

2) Cost per Unit using ABC

Overhead Cost Centre

Cost

Driver

Bla

ck

Gre

y

Wh

ite

Machine Set Up Costs ($) Productio 32, 24, 16,

Accounting and finance deals with monetary transactions and the funds of the business

and counted as the branch of financial, management, tax and the cost accounting. The present

report is based on UAE Trekker LLC, produces the travel hiking backpacks in respect of 3

different colors that includes Grey, Orange and black that are all manufactured in same form of

the raw material. Furthermore, the study highlights the adoption of the traditional costing method

in allocation of overheads to the products by using direct labor hours. Moreover, presently

company is considering ABC system for improving its processes, product and profitability with

determining the pitfalls in executing this system.

a. Calculation

1) Cost per Unit under Full Absorption Costing

Overhead Absorption Rate

Black Grey White Total

Production Volume (Units) 30,000 24,000 36,000

Direct Labor hours per unit (Hrs) 0.2 0.3 0.4

Total Labor Hours (e.g. 30,000 X 0.2) 6,000 7,200 14,400 27,600

Therefore the overhead absorption rate 14.49 400,000 / 27,600

Cost Per Unit

Black Grey Orange

$ $ $

Raw Materials ($2.40 Per Unit x 1.5kg x

2.4kg x 3.0kg) 3.6 5.76 7.2

Direct Labour ($29.60 Per Hour x 0.2 / 0.3 /

0.4) 5.92 8.88 11.84

Overheads ($14.49 Per Hour x 0.2 / 0.3 /

0.4) 2.90 4.35 5.80

Full Cost Per Unit 12.42 18.99 24.84

2) Cost per Unit using ABC

Overhead Cost Centre

Cost

Driver

Bla

ck

Gre

y

Wh

ite

Machine Set Up Costs ($) Productio 32, 24, 16,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

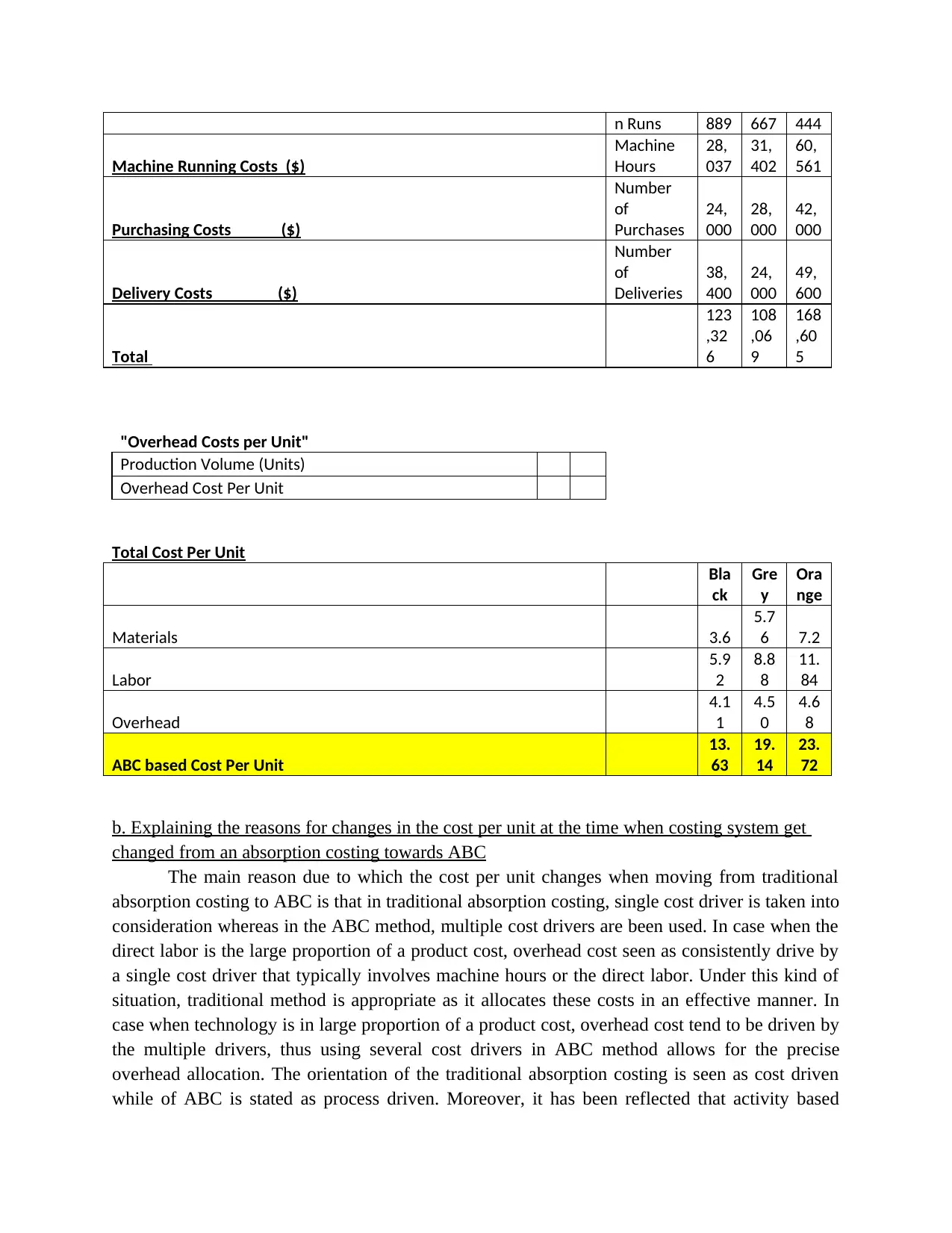

n Runs 889 667 444

Machine Running Costs ($)

Machine

Hours

28,

037

31,

402

60,

561

Purchasing Costs ($)

Number

of

Purchases

24,

000

28,

000

42,

000

Delivery Costs ($)

Number

of

Deliveries

38,

400

24,

000

49,

600

Total

123

,32

6

108

,06

9

168

,60

5

"Overhead Costs per Unit"

Production Volume (Units)

Overhead Cost Per Unit

Total Cost Per Unit

Bla

ck

Gre

y

Ora

nge

Materials 3.6

5.7

6 7.2

Labor

5.9

2

8.8

8

11.

84

Overhead

4.1

1

4.5

0

4.6

8

ABC based Cost Per Unit

13.

63

19.

14

23.

72

b. Explaining the reasons for changes in the cost per unit at the time when costing system get

changed from an absorption costing towards ABC

The main reason due to which the cost per unit changes when moving from traditional

absorption costing to ABC is that in traditional absorption costing, single cost driver is taken into

consideration whereas in the ABC method, multiple cost drivers are been used. In case when the

direct labor is the large proportion of a product cost, overhead cost seen as consistently drive by

a single cost driver that typically involves machine hours or the direct labor. Under this kind of

situation, traditional method is appropriate as it allocates these costs in an effective manner. In

case when technology is in large proportion of a product cost, overhead cost tend to be driven by

the multiple drivers, thus using several cost drivers in ABC method allows for the precise

overhead allocation. The orientation of the traditional absorption costing is seen as cost driven

while of ABC is stated as process driven. Moreover, it has been reflected that activity based

Machine Running Costs ($)

Machine

Hours

28,

037

31,

402

60,

561

Purchasing Costs ($)

Number

of

Purchases

24,

000

28,

000

42,

000

Delivery Costs ($)

Number

of

Deliveries

38,

400

24,

000

49,

600

Total

123

,32

6

108

,06

9

168

,60

5

"Overhead Costs per Unit"

Production Volume (Units)

Overhead Cost Per Unit

Total Cost Per Unit

Bla

ck

Gre

y

Ora

nge

Materials 3.6

5.7

6 7.2

Labor

5.9

2

8.8

8

11.

84

Overhead

4.1

1

4.5

0

4.6

8

ABC based Cost Per Unit

13.

63

19.

14

23.

72

b. Explaining the reasons for changes in the cost per unit at the time when costing system get

changed from an absorption costing towards ABC

The main reason due to which the cost per unit changes when moving from traditional

absorption costing to ABC is that in traditional absorption costing, single cost driver is taken into

consideration whereas in the ABC method, multiple cost drivers are been used. In case when the

direct labor is the large proportion of a product cost, overhead cost seen as consistently drive by

a single cost driver that typically involves machine hours or the direct labor. Under this kind of

situation, traditional method is appropriate as it allocates these costs in an effective manner. In

case when technology is in large proportion of a product cost, overhead cost tend to be driven by

the multiple drivers, thus using several cost drivers in ABC method allows for the precise

overhead allocation. The orientation of the traditional absorption costing is seen as cost driven

while of ABC is stated as process driven. Moreover, it has been reflected that activity based

costing is the more accurate technique as it assigns an overhead cost on the basis of activities that

drives for an overhead costs. By this it could be concluded that subsequent gross loss and the

cost for every sales unit provides for a more accurate picture or view than the entire cost and the

gross profit under a traditional absorption method.

c. Presenting implications relating to cost management for switching to ABC system

ABC brings reliability and accuracy in the determination of cost by emphasizing on the cause&

effect relationship in the occurrence of the cost. It helps in recognizing the activity that causes

costs not the products and identifies the product that consumes more and more activities. In an

advanced manufacturing and the technology where the support functions the overheads presents

larger share of a total costs, the ABC technique facilitates a more true and realistic cost of

products. As in this case three products are included so ABC is counted as the best method

because it works well with diversity in the products produced and provide a correct and the

reliable data of the product cost (Altawati and et.al., 2018). Traditional system brings

anticipations and the errors in determination of the product cost because of using an arbitrary

apportionment and the absorption technique. ABC system facilitates better costing related

information and enables the management in gaining a better insights or an understanding of

company’s competitive strength and the weaknesses. Moreover, managers recognizes

requirement for the better costing method like ABC in case they are been experiencing an

increased lost of the sales because of erroneous pricing which led from an inaccurate data of the

costing. It provides not only the base for computing the accurate cost but also provides for a

mechanism in managing the cost. It is the systems that emphasize attention of the management

on underlying causes of the costs. This system assumes that the resource-consuming activity

causes the cost and that the product which incur cost by way of activities that they are needed for

manufacturing, designing, delivery, marketing and the servicing. Through gathering and

reporting on important activities within which an organization engages, there are chances for

understanding and managing the cost effectively.

Along with an ABC system, costs are been managed in long run through controlling activities

which drives them. On the other hand, aim of this system is to manage all the activities instead of

cost. By way of managing those forces which causes an activity that is cost drivers,

automatically cost would be managed effectively in long term. Thus, Application of ABC system

might be having a greatest potential in contributing to the cost management, control, budgeting

and an evaluation of the performance.

d. Explaining an impact of switching from absorption to ABC on product & pricing profitability

ABC system has a great impact on the companies that are having large areas, higher level of

expenses, having numerous products, customers, services, processes and the combination all

these factors. For example- Plants that are producing a custom and the standard products, low

volume products and mature or new products. Corporations that are accepting the large and the

small orders offers for a customized and the standard deliveries and satisfies all the customers

involving those with frequent changes in their demand before and after a delivery and a customer

drives for an overhead costs. By this it could be concluded that subsequent gross loss and the

cost for every sales unit provides for a more accurate picture or view than the entire cost and the

gross profit under a traditional absorption method.

c. Presenting implications relating to cost management for switching to ABC system

ABC brings reliability and accuracy in the determination of cost by emphasizing on the cause&

effect relationship in the occurrence of the cost. It helps in recognizing the activity that causes

costs not the products and identifies the product that consumes more and more activities. In an

advanced manufacturing and the technology where the support functions the overheads presents

larger share of a total costs, the ABC technique facilitates a more true and realistic cost of

products. As in this case three products are included so ABC is counted as the best method

because it works well with diversity in the products produced and provide a correct and the

reliable data of the product cost (Altawati and et.al., 2018). Traditional system brings

anticipations and the errors in determination of the product cost because of using an arbitrary

apportionment and the absorption technique. ABC system facilitates better costing related

information and enables the management in gaining a better insights or an understanding of

company’s competitive strength and the weaknesses. Moreover, managers recognizes

requirement for the better costing method like ABC in case they are been experiencing an

increased lost of the sales because of erroneous pricing which led from an inaccurate data of the

costing. It provides not only the base for computing the accurate cost but also provides for a

mechanism in managing the cost. It is the systems that emphasize attention of the management

on underlying causes of the costs. This system assumes that the resource-consuming activity

causes the cost and that the product which incur cost by way of activities that they are needed for

manufacturing, designing, delivery, marketing and the servicing. Through gathering and

reporting on important activities within which an organization engages, there are chances for

understanding and managing the cost effectively.

Along with an ABC system, costs are been managed in long run through controlling activities

which drives them. On the other hand, aim of this system is to manage all the activities instead of

cost. By way of managing those forces which causes an activity that is cost drivers,

automatically cost would be managed effectively in long term. Thus, Application of ABC system

might be having a greatest potential in contributing to the cost management, control, budgeting

and an evaluation of the performance.

d. Explaining an impact of switching from absorption to ABC on product & pricing profitability

ABC system has a great impact on the companies that are having large areas, higher level of

expenses, having numerous products, customers, services, processes and the combination all

these factors. For example- Plants that are producing a custom and the standard products, low

volume products and mature or new products. Corporations that are accepting the large and the

small orders offers for a customized and the standard deliveries and satisfies all the customers

involving those with frequent changes in their demand before and after a delivery and a customer

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

who very request for a special services could be substantially benefitted from the ABC costing

system (ȘUTEU and et.al., 2016). The main purpose of using activity based costing technique is

to increase profitability and an overall performance of the company. This objective is been

achieved by determining accurate amount of overhead cost and the cost drivers resulting to more

and more streamlined processes of the business. In case when all the direct and an indirect cost

are been allocated to product, manager starts with getting an idea of the business processes that

are performing well and which are not efficient. Thereafter, they could streamline such processes

through allocating more or additional resources towards the profitable activities and eliminates

the practices which are costly and irrelevant. As a result of an ABC processes, an organization

are efficient in managing its manufacturing performance and in improving quality of the service

and the product. Overall, the profitability increases as the result of more of an accurate pricing of

the product that could allow the company in offering a competitive pricing that helps in

maximizing the returns. Activity based costing technique is considered as more accurate

technique of the product or the service costing, resulting to the more accurate pricing related

decisions. It increases an understanding of the cost drivers and the overheads that makes costly

and the non-value adding activities more as visible, allowing managers in eliminating and

reducing it (Afonso, Wernke and Zanin, 2018). It enables effective challenge regarding operating

cost in order to find a better way of eliminating and allocating the overheads. It also assists in

improving the product and the customer profit assessment. It supports the method of

performance management like continuous improvement and the scorecards.

e. Describing steps and the pitfalls that needs to be avoided at the time of introducing ABC

system within the business

There are several pitfalls or the steps that needs to be considered while introducing or executing

ABC system that are as follows-

Company should not get caught up in so much attention into control and the detail. It could

obscure bigger picture or makes an entity lose sight of the strategic objectives in the quest for a

small savings.

It is an essential for the business in not getting fall into a trap of determining ABC costs that are

found as relevant for all types of the decisions. Not all the cost would disappear in case a product

is been discontinued. An example of being building occupancy costs (Sokolov and Elsukova,

2016). Common pitfalls in ABM involves in planning phase, various problems and the pitfalls

can be found as lack of top management commitment and buy-in, failure in gaining a complete

agreement on the execution objectives, planning inability of the team in articulating the reason

behind conducting the project, failure in creating a dedicated team within the project & lack of

understanding in relation to operational, financial and strategic information that an organization

expects.

Moreover, at time of assessing the activities, the most common pitfalls are seen such as no. of the

activities for which a detailed information need to be gathered seems as overwhelming, No any

system (ȘUTEU and et.al., 2016). The main purpose of using activity based costing technique is

to increase profitability and an overall performance of the company. This objective is been

achieved by determining accurate amount of overhead cost and the cost drivers resulting to more

and more streamlined processes of the business. In case when all the direct and an indirect cost

are been allocated to product, manager starts with getting an idea of the business processes that

are performing well and which are not efficient. Thereafter, they could streamline such processes

through allocating more or additional resources towards the profitable activities and eliminates

the practices which are costly and irrelevant. As a result of an ABC processes, an organization

are efficient in managing its manufacturing performance and in improving quality of the service

and the product. Overall, the profitability increases as the result of more of an accurate pricing of

the product that could allow the company in offering a competitive pricing that helps in

maximizing the returns. Activity based costing technique is considered as more accurate

technique of the product or the service costing, resulting to the more accurate pricing related

decisions. It increases an understanding of the cost drivers and the overheads that makes costly

and the non-value adding activities more as visible, allowing managers in eliminating and

reducing it (Afonso, Wernke and Zanin, 2018). It enables effective challenge regarding operating

cost in order to find a better way of eliminating and allocating the overheads. It also assists in

improving the product and the customer profit assessment. It supports the method of

performance management like continuous improvement and the scorecards.

e. Describing steps and the pitfalls that needs to be avoided at the time of introducing ABC

system within the business

There are several pitfalls or the steps that needs to be considered while introducing or executing

ABC system that are as follows-

Company should not get caught up in so much attention into control and the detail. It could

obscure bigger picture or makes an entity lose sight of the strategic objectives in the quest for a

small savings.

It is an essential for the business in not getting fall into a trap of determining ABC costs that are

found as relevant for all types of the decisions. Not all the cost would disappear in case a product

is been discontinued. An example of being building occupancy costs (Sokolov and Elsukova,

2016). Common pitfalls in ABM involves in planning phase, various problems and the pitfalls

can be found as lack of top management commitment and buy-in, failure in gaining a complete

agreement on the execution objectives, planning inability of the team in articulating the reason

behind conducting the project, failure in creating a dedicated team within the project & lack of

understanding in relation to operational, financial and strategic information that an organization

expects.

Moreover, at time of assessing the activities, the most common pitfalls are seen such as no. of the

activities for which a detailed information need to be gathered seems as overwhelming, No any

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

significant activity appears, resources that are dedicated to project deemed as inadequate in

supporting analysis, inadequate attention towards training for building and forming an internal

expertise and lastly, failure in communicating to the employees about the purpose behind a

project and the questions results to negative feelings and defensive kind of behavior (Santana,

Afonso, Zanin and Wernke, 2017). Thus at each phase of its process, pitfalls does exist as like in

costing the products, activities and the services it includes inaccurate cost assignment to the

activities and the cost objects, activity and the resource drivers are resulting as too high, the

activity driver does not reflects a consumption rate and the pattern of its respective activities etc.

CONCLUSION

By summing up the above report, ABC costing technique is found as better as compared

to traditional method because it helps in increasing profitability by reducing cost and in taking

effective pricing decisions. Though it includes various pitfalls but there are measures which an

entity must take for avoiding such pitfalls at the time of allocating the cost and assessing

activities.

supporting analysis, inadequate attention towards training for building and forming an internal

expertise and lastly, failure in communicating to the employees about the purpose behind a

project and the questions results to negative feelings and defensive kind of behavior (Santana,

Afonso, Zanin and Wernke, 2017). Thus at each phase of its process, pitfalls does exist as like in

costing the products, activities and the services it includes inaccurate cost assignment to the

activities and the cost objects, activity and the resource drivers are resulting as too high, the

activity driver does not reflects a consumption rate and the pattern of its respective activities etc.

CONCLUSION

By summing up the above report, ABC costing technique is found as better as compared

to traditional method because it helps in increasing profitability by reducing cost and in taking

effective pricing decisions. Though it includes various pitfalls but there are measures which an

entity must take for avoiding such pitfalls at the time of allocating the cost and assessing

activities.

REFERENCES

Books and journal

Afonso, P. S. L. P., Wernke, R. and Zanin, A., 2018. Managing the cost of unused capacity: an

integrative and comparative analysis of the abc, tabc and uep methods. Revista del instituto

internacional de costos. 13. pp.150-163.

Altawati, N. O. M. T. and et.al., 2018. A Review of Traditional Cost System versus Activity

Based Costing Approaches. Advanced science letters. 24(6). pp.4688-4694.

Santana, A., Afonso, P. S. L. P., Zanin, A. and Wernke, R., 2017. Costing models for capacity

optimization in Industry 4.0: Trade-off between used capacity and operational

efficiency. Procedia Manufacturing. 13. pp.1183-1190.

Sokolov, A. Y. and Elsukova, T. V., 2016. Using ABC to enhance throughput accounting: an

integrated management approach. Academy of Strategic Management Journal. 15. pp.8-15.

ȘUTEU, M. D. and et.al., 2016. The impact of costing methods on profitability of enterprises

operating in the embroidery industry. Tekstil ve Konfeksiyon. 26(3). pp.239-243.

Books and journal

Afonso, P. S. L. P., Wernke, R. and Zanin, A., 2018. Managing the cost of unused capacity: an

integrative and comparative analysis of the abc, tabc and uep methods. Revista del instituto

internacional de costos. 13. pp.150-163.

Altawati, N. O. M. T. and et.al., 2018. A Review of Traditional Cost System versus Activity

Based Costing Approaches. Advanced science letters. 24(6). pp.4688-4694.

Santana, A., Afonso, P. S. L. P., Zanin, A. and Wernke, R., 2017. Costing models for capacity

optimization in Industry 4.0: Trade-off between used capacity and operational

efficiency. Procedia Manufacturing. 13. pp.1183-1190.

Sokolov, A. Y. and Elsukova, T. V., 2016. Using ABC to enhance throughput accounting: an

integrated management approach. Academy of Strategic Management Journal. 15. pp.8-15.

ȘUTEU, M. D. and et.al., 2016. The impact of costing methods on profitability of enterprises

operating in the embroidery industry. Tekstil ve Konfeksiyon. 26(3). pp.239-243.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.