Accounting and Finance for Executives– UUAC5300

Added on 2021-05-31

15 Pages3222 Words20 Views

1

Accounting and Finance for Executives – UUAC5300

Assignment - 2

Semester 1 - 2018

Accounting and Finance for Executives – UUAC5300

Assignment - 2

Semester 1 - 2018

2

Solution 1: Evaluation of financial statements and reporting findings

Answer 1.1:

A:

Following are implications of the ratio provided for the lending decision:

Current ratio: Current ratio reflects the ability of company to pay the short term

liabilities. In year 2016, the current ratio was 3.1 times whereas it was reduced to 2.1

times in year 2017. It indicates that short term solvency position of Borrower’s company

has been reduced in the current year as compared with previous year. The current ratio of

2.1 times in current year shows that company has enough assets to pay the current

liabilities as it arises.

Quick Ratio: Quick ratio is also an important indicator of liquidity position of the

company as it takes it into account only those assets those are capable of converting into

cash and cash equivalent very rapidly. Quick ratio of Borrowers Company has increased

in year 2017 as compared to previous year that shows improvement in quick assets and

company has now more assets to pay the short term liabilities.

Asset Turnover Ratio: This ratio indicates how frequently company uses total assets to

earn the revenue. This ratio has been decreased in year 2017 as compared to year 2016

that indicated company efficiency to use the assets to produce the revenue has been

decreased in current year (Damodaran, 2011).

Cash Debt Coverage: This ratio shows level of operating cash flows as against the debt

liabilities of the company. As this ratio is less than 1 it indicates that company has very

less cash flow to pay back the debt capital. Although, there has been rise in this ratio that

indicates increase in flow net cash flow from the operating activity.

Profit and Earning per share: Profit of company has been decreased in current year by

8% as compared with previous reflect the poor profitability position. The EPS of

Borrowers Company has also reduced from $3.30 to $2.50 that indicates poor position of

the company in the market in current year.

Although above ratios shows Company has stable liquidity position but poor profitability

position in the current year as compared to previous year made the financial position of the

Solution 1: Evaluation of financial statements and reporting findings

Answer 1.1:

A:

Following are implications of the ratio provided for the lending decision:

Current ratio: Current ratio reflects the ability of company to pay the short term

liabilities. In year 2016, the current ratio was 3.1 times whereas it was reduced to 2.1

times in year 2017. It indicates that short term solvency position of Borrower’s company

has been reduced in the current year as compared with previous year. The current ratio of

2.1 times in current year shows that company has enough assets to pay the current

liabilities as it arises.

Quick Ratio: Quick ratio is also an important indicator of liquidity position of the

company as it takes it into account only those assets those are capable of converting into

cash and cash equivalent very rapidly. Quick ratio of Borrowers Company has increased

in year 2017 as compared to previous year that shows improvement in quick assets and

company has now more assets to pay the short term liabilities.

Asset Turnover Ratio: This ratio indicates how frequently company uses total assets to

earn the revenue. This ratio has been decreased in year 2017 as compared to year 2016

that indicated company efficiency to use the assets to produce the revenue has been

decreased in current year (Damodaran, 2011).

Cash Debt Coverage: This ratio shows level of operating cash flows as against the debt

liabilities of the company. As this ratio is less than 1 it indicates that company has very

less cash flow to pay back the debt capital. Although, there has been rise in this ratio that

indicates increase in flow net cash flow from the operating activity.

Profit and Earning per share: Profit of company has been decreased in current year by

8% as compared with previous reflect the poor profitability position. The EPS of

Borrowers Company has also reduced from $3.30 to $2.50 that indicates poor position of

the company in the market in current year.

Although above ratios shows Company has stable liquidity position but poor profitability

position in the current year as compared to previous year made the financial position of the

3

company unfavorable. These ratios are not relevant for evaluating the debt worthiness of the

company.

B:

The three ratios that need to be calculated for analyzing the decision of the debt

worthiness are as follows:

Debt Equity Ratio: This ratio helps to know the level of debt against the shareholder

equity capital of the company. It will provide current level of debt and also shows

increase in debt level will change the capital structure to make it leveraged firm or not.

Interest Coverage Ratio: This ratio tells times the company can pay interest expenses on

the debt capital it is charge on the profitability of the company. This ratio will guide

whether company has enough profitability position to bear the increase in interest

expenses (Davies and Crawford, 2011).

Debt ratio: This ratio will provide information on level of debt capital used to finance

the total assets of the company.

C:

There are some drawbacks associated with the use of financial ratio analysis that limits

the application of technique in investing and credit decisions. The most significant limitation

associated with the use of ratio analysis technique is that it is not suitable to be used on a stand-

alone basis and the results obtained need to be benchmarked against some specific criteria such

as industry norm, aggregate economy and past performance. Also, it is not regarded to be a

useful technique for carrying out comparison of the financial performance of the companies that

differ on the basis of size and also belongs to different industry groups. The ratio analysis

sometimes does not provide an actual depiction of the financial performance of a company as the

financial statements are subjected to distortion by the economic and seasonal factors. In addition

to this, the use of different accounting methods and policies can provide uneven comparison of

the companies that belong to even same sectors. Also, there may be some good and some weak

financial ratios which make it difficult for investors to predict the future growth potential of the

company (Tracy, 2012).

company unfavorable. These ratios are not relevant for evaluating the debt worthiness of the

company.

B:

The three ratios that need to be calculated for analyzing the decision of the debt

worthiness are as follows:

Debt Equity Ratio: This ratio helps to know the level of debt against the shareholder

equity capital of the company. It will provide current level of debt and also shows

increase in debt level will change the capital structure to make it leveraged firm or not.

Interest Coverage Ratio: This ratio tells times the company can pay interest expenses on

the debt capital it is charge on the profitability of the company. This ratio will guide

whether company has enough profitability position to bear the increase in interest

expenses (Davies and Crawford, 2011).

Debt ratio: This ratio will provide information on level of debt capital used to finance

the total assets of the company.

C:

There are some drawbacks associated with the use of financial ratio analysis that limits

the application of technique in investing and credit decisions. The most significant limitation

associated with the use of ratio analysis technique is that it is not suitable to be used on a stand-

alone basis and the results obtained need to be benchmarked against some specific criteria such

as industry norm, aggregate economy and past performance. Also, it is not regarded to be a

useful technique for carrying out comparison of the financial performance of the companies that

differ on the basis of size and also belongs to different industry groups. The ratio analysis

sometimes does not provide an actual depiction of the financial performance of a company as the

financial statements are subjected to distortion by the economic and seasonal factors. In addition

to this, the use of different accounting methods and policies can provide uneven comparison of

the companies that belong to even same sectors. Also, there may be some good and some weak

financial ratios which make it difficult for investors to predict the future growth potential of the

company (Tracy, 2012).

4

Answer 1.2:

A:

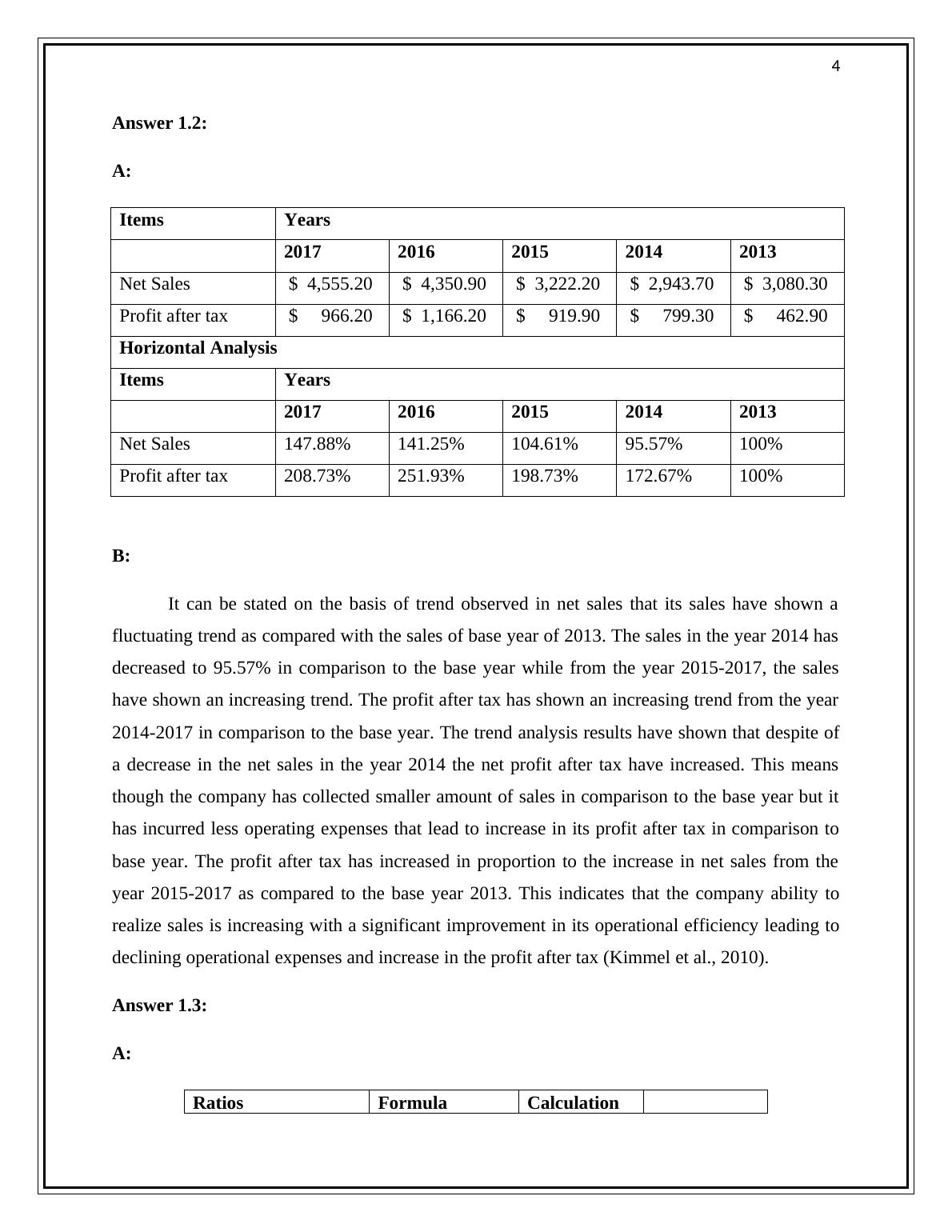

Items Years

2017 2016 2015 2014 2013

Net Sales $ 4,555.20 $ 4,350.90 $ 3,222.20 $ 2,943.70 $ 3,080.30

Profit after tax $ 966.20 $ 1,166.20 $ 919.90 $ 799.30 $ 462.90

Horizontal Analysis

Items Years

2017 2016 2015 2014 2013

Net Sales 147.88% 141.25% 104.61% 95.57% 100%

Profit after tax 208.73% 251.93% 198.73% 172.67% 100%

B:

It can be stated on the basis of trend observed in net sales that its sales have shown a

fluctuating trend as compared with the sales of base year of 2013. The sales in the year 2014 has

decreased to 95.57% in comparison to the base year while from the year 2015-2017, the sales

have shown an increasing trend. The profit after tax has shown an increasing trend from the year

2014-2017 in comparison to the base year. The trend analysis results have shown that despite of

a decrease in the net sales in the year 2014 the net profit after tax have increased. This means

though the company has collected smaller amount of sales in comparison to the base year but it

has incurred less operating expenses that lead to increase in its profit after tax in comparison to

base year. The profit after tax has increased in proportion to the increase in net sales from the

year 2015-2017 as compared to the base year 2013. This indicates that the company ability to

realize sales is increasing with a significant improvement in its operational efficiency leading to

declining operational expenses and increase in the profit after tax (Kimmel et al., 2010).

Answer 1.3:

A:

Ratios Formula Calculation

Answer 1.2:

A:

Items Years

2017 2016 2015 2014 2013

Net Sales $ 4,555.20 $ 4,350.90 $ 3,222.20 $ 2,943.70 $ 3,080.30

Profit after tax $ 966.20 $ 1,166.20 $ 919.90 $ 799.30 $ 462.90

Horizontal Analysis

Items Years

2017 2016 2015 2014 2013

Net Sales 147.88% 141.25% 104.61% 95.57% 100%

Profit after tax 208.73% 251.93% 198.73% 172.67% 100%

B:

It can be stated on the basis of trend observed in net sales that its sales have shown a

fluctuating trend as compared with the sales of base year of 2013. The sales in the year 2014 has

decreased to 95.57% in comparison to the base year while from the year 2015-2017, the sales

have shown an increasing trend. The profit after tax has shown an increasing trend from the year

2014-2017 in comparison to the base year. The trend analysis results have shown that despite of

a decrease in the net sales in the year 2014 the net profit after tax have increased. This means

though the company has collected smaller amount of sales in comparison to the base year but it

has incurred less operating expenses that lead to increase in its profit after tax in comparison to

base year. The profit after tax has increased in proportion to the increase in net sales from the

year 2015-2017 as compared to the base year 2013. This indicates that the company ability to

realize sales is increasing with a significant improvement in its operational efficiency leading to

declining operational expenses and increase in the profit after tax (Kimmel et al., 2010).

Answer 1.3:

A:

Ratios Formula Calculation

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Current Ratio for the Year 2007lg...

|12

|1460

|71

Accounting And Finance For Managers in UK Discussion 2022lg...

|5

|789

|26

Financial Analysis of Reliance Worldwide PDFlg...

|25

|4658

|95

Accounting for Managers in companieslg...

|5

|1619

|106

Answer 1: Financial Statements for Managing Companieslg...

|10

|3351

|210

HI6026 - Audit, Assurance | Questions & Answerslg...

|8

|2587

|48