Accounting and Finance for Managers: Financial Performance

VerifiedAdded on 2023/04/05

|18

|3073

|363

Report

AI Summary

This report provides a detailed analysis of the financial health and performance of Tesco, Sainsbury, and Morrison's Plc, three major UK-based retail companies. The analysis is conducted using various financial ratios, including profitability, efficiency, and liquidity ratios, covering the period from 2010 to 2014. The report examines gross profit margin, operating profit margin, and net profit margin to assess profitability. It also evaluates management effectiveness using return on assets and return on equity. Efficiency ratios, such as inventory turnover, asset turnover, and receivable turnover, are analyzed to understand how effectively the companies manage their assets. Liquidity ratios, including current and quick ratios, are used to assess the companies' ability to meet short-term obligations. The report includes a memo to the managing director of Morrison's Plc regarding the company's financial performance and provides recommendations for improvement. Finally, it outlines the limitations of financial ratios and discusses the importance of considering non-financial factors in decision-making.

Accounting and Finance for Managers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

SECTION A.....................................................................................................................................3

a. Analyzing financial health and performance of Tesco, Sainsbury and Morrison’s Plc...........3

b. Writing a memo to managing director regarding the performance of firm along with the

recommendations.......................................................................................................................10

c. Outlining the limitations of financial ratios...........................................................................11

SECTION B...................................................................................................................................12

a. Using net present value technique to assess whether three year contract is profitable or not

...................................................................................................................................................12

b. Explaining approach of taxation in appraisal........................................................................14

c. Discussing the techniques that can be used for the evaluation of project..............................14

d. Stating the other factors that need to consider while taking final decision...........................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

SECTION A.....................................................................................................................................3

a. Analyzing financial health and performance of Tesco, Sainsbury and Morrison’s Plc...........3

b. Writing a memo to managing director regarding the performance of firm along with the

recommendations.......................................................................................................................10

c. Outlining the limitations of financial ratios...........................................................................11

SECTION B...................................................................................................................................12

a. Using net present value technique to assess whether three year contract is profitable or not

...................................................................................................................................................12

b. Explaining approach of taxation in appraisal........................................................................14

c. Discussing the techniques that can be used for the evaluation of project..............................14

d. Stating the other factors that need to consider while taking final decision...........................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION

Accounting and finance management are vital for the organizational growth and success.

In the business organization, manager places high level emphasis on maintaining accounting

records and information which in turn helps preparing suitable statements. Hence, by making

analysis of financial statements through the means of ratio analysis both internal and external

stakeholders can take suitable decision. This report is based on three major retail or supermarket

stores such as Tesco, Sainsbury’s and Morrison Plc. All these retail stores are listed on the

recognized stock exchange of UK and known for delivering high quality products. The present

report will light on the extent to which financial condition of company is sound over others. It

will develop understanding regarding the investment appraisal techniques and its significance in

the decision making aspect.

SECTION A

a. Analyzing financial health and performance of Tesco, Sainsbury and Morrison’s Plc

Profitability analysis

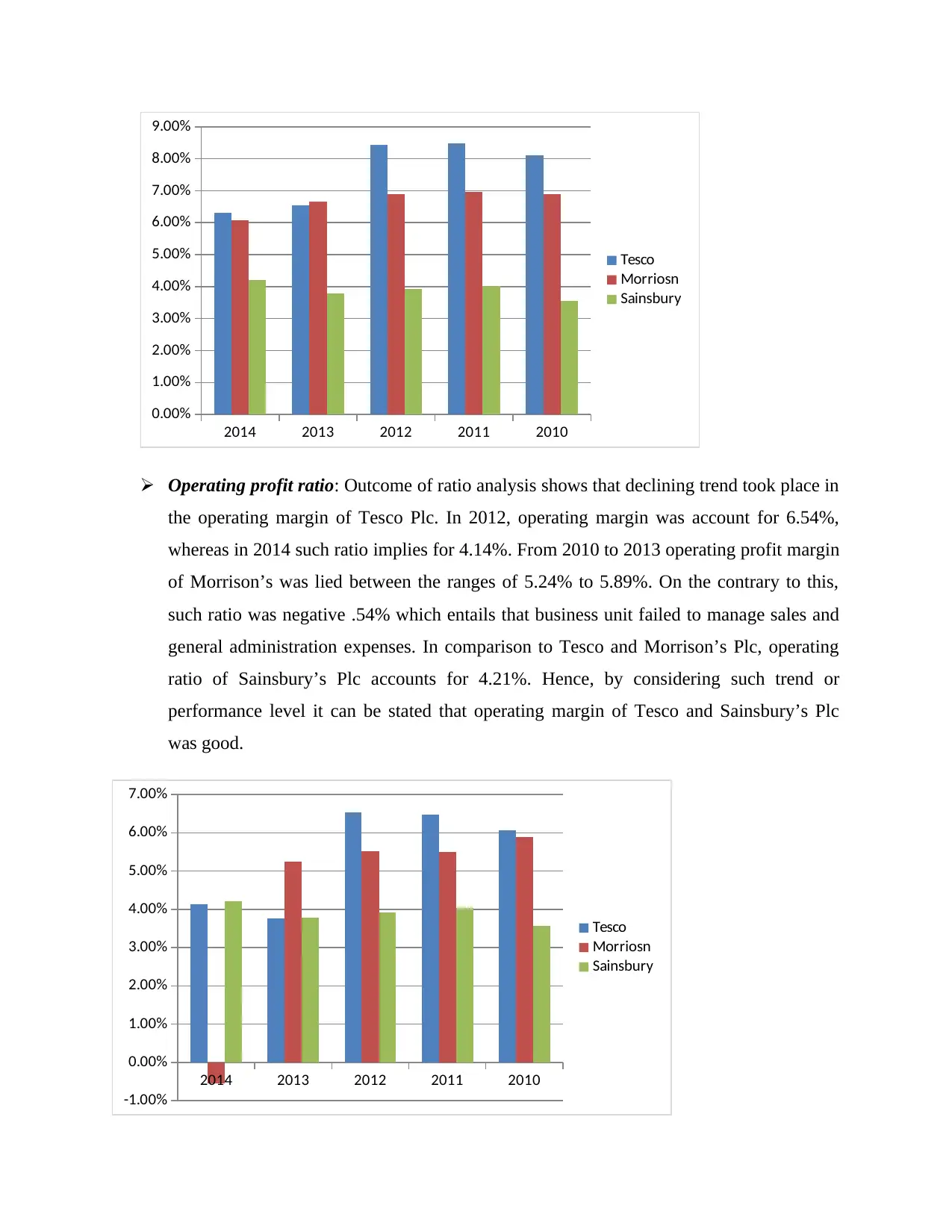

Gross margin ratio: It has been assessed from ratio analysis that GP margin of Tesco

decreased over the years and accounts for 6.31% respectively. Besides this, from 2010 to

2014 GP ratio Morrison fluctuated due to decline in sales revenue and high direct

expenses. In 2014, gross profit ratio of Morrison’s Plc was 6.07%. In comparison to this,

Sainsbury’s GP margin was 5.79% in 2014. Due to the existence of high competition

business units failed to generate more sales and profit. Hence, by considering such

aspects, it can be stated that GP margin of all such business units were not good.

Accounting and finance management are vital for the organizational growth and success.

In the business organization, manager places high level emphasis on maintaining accounting

records and information which in turn helps preparing suitable statements. Hence, by making

analysis of financial statements through the means of ratio analysis both internal and external

stakeholders can take suitable decision. This report is based on three major retail or supermarket

stores such as Tesco, Sainsbury’s and Morrison Plc. All these retail stores are listed on the

recognized stock exchange of UK and known for delivering high quality products. The present

report will light on the extent to which financial condition of company is sound over others. It

will develop understanding regarding the investment appraisal techniques and its significance in

the decision making aspect.

SECTION A

a. Analyzing financial health and performance of Tesco, Sainsbury and Morrison’s Plc

Profitability analysis

Gross margin ratio: It has been assessed from ratio analysis that GP margin of Tesco

decreased over the years and accounts for 6.31% respectively. Besides this, from 2010 to

2014 GP ratio Morrison fluctuated due to decline in sales revenue and high direct

expenses. In 2014, gross profit ratio of Morrison’s Plc was 6.07%. In comparison to this,

Sainsbury’s GP margin was 5.79% in 2014. Due to the existence of high competition

business units failed to generate more sales and profit. Hence, by considering such

aspects, it can be stated that GP margin of all such business units were not good.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2014 2013 2012 2011 2010

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

Tesco

Morriosn

Sainsbury

Operating profit ratio: Outcome of ratio analysis shows that declining trend took place in

the operating margin of Tesco Plc. In 2012, operating margin was account for 6.54%,

whereas in 2014 such ratio implies for 4.14%. From 2010 to 2013 operating profit margin

of Morrison’s was lied between the ranges of 5.24% to 5.89%. On the contrary to this,

such ratio was negative .54% which entails that business unit failed to manage sales and

general administration expenses. In comparison to Tesco and Morrison’s Plc, operating

ratio of Sainsbury’s Plc accounts for 4.21%. Hence, by considering such trend or

performance level it can be stated that operating margin of Tesco and Sainsbury’s Plc

was good.

2014 2013 2012 2011 2010

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

Tesco

Morriosn

Sainsbury

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

Tesco

Morriosn

Sainsbury

Operating profit ratio: Outcome of ratio analysis shows that declining trend took place in

the operating margin of Tesco Plc. In 2012, operating margin was account for 6.54%,

whereas in 2014 such ratio implies for 4.14%. From 2010 to 2013 operating profit margin

of Morrison’s was lied between the ranges of 5.24% to 5.89%. On the contrary to this,

such ratio was negative .54% which entails that business unit failed to manage sales and

general administration expenses. In comparison to Tesco and Morrison’s Plc, operating

ratio of Sainsbury’s Plc accounts for 4.21%. Hence, by considering such trend or

performance level it can be stated that operating margin of Tesco and Sainsbury’s Plc

was good.

2014 2013 2012 2011 2010

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

Tesco

Morriosn

Sainsbury

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

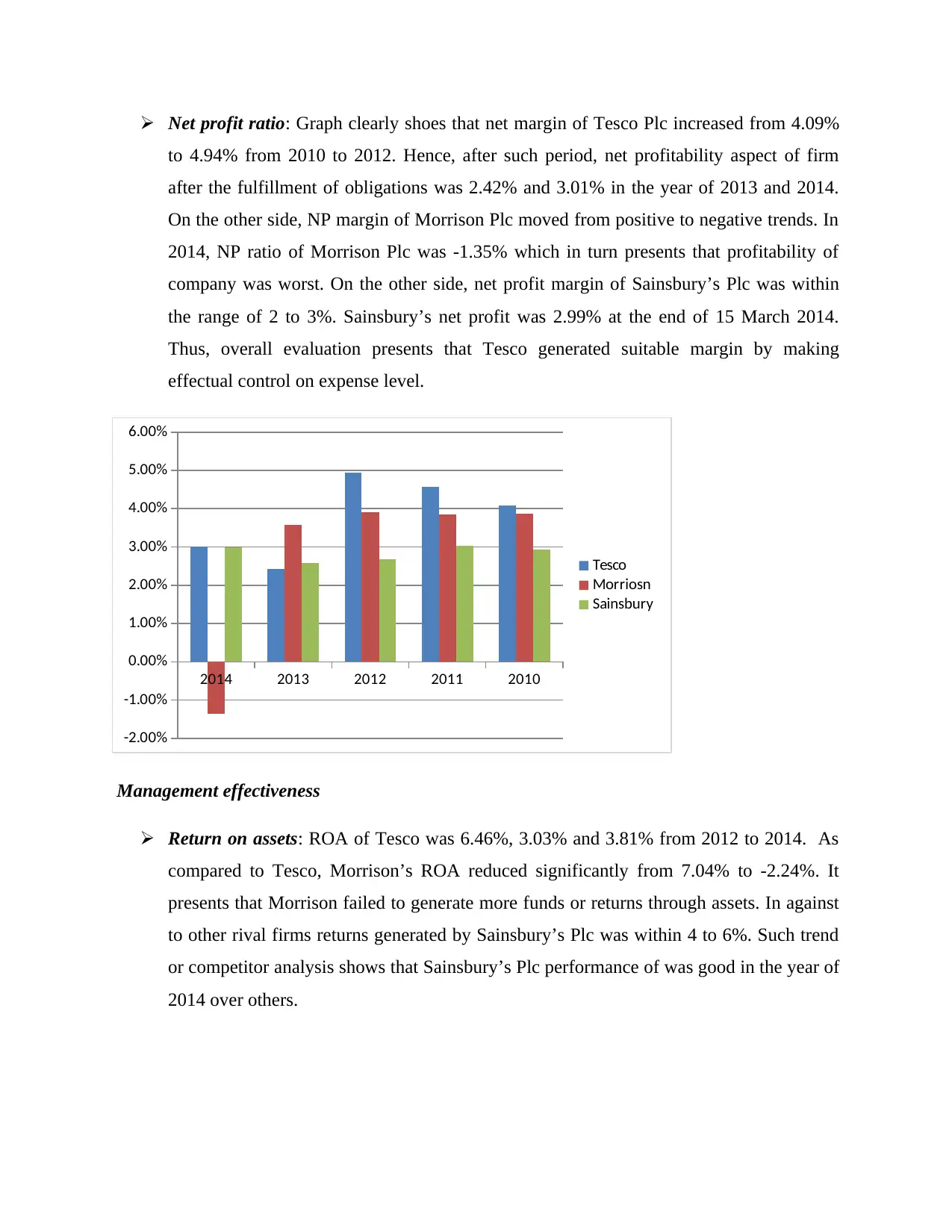

Net profit ratio: Graph clearly shoes that net margin of Tesco Plc increased from 4.09%

to 4.94% from 2010 to 2012. Hence, after such period, net profitability aspect of firm

after the fulfillment of obligations was 2.42% and 3.01% in the year of 2013 and 2014.

On the other side, NP margin of Morrison Plc moved from positive to negative trends. In

2014, NP ratio of Morrison Plc was -1.35% which in turn presents that profitability of

company was worst. On the other side, net profit margin of Sainsbury’s Plc was within

the range of 2 to 3%. Sainsbury’s net profit was 2.99% at the end of 15 March 2014.

Thus, overall evaluation presents that Tesco generated suitable margin by making

effectual control on expense level.

2014 2013 2012 2011 2010

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

Tesco

Morriosn

Sainsbury

Management effectiveness

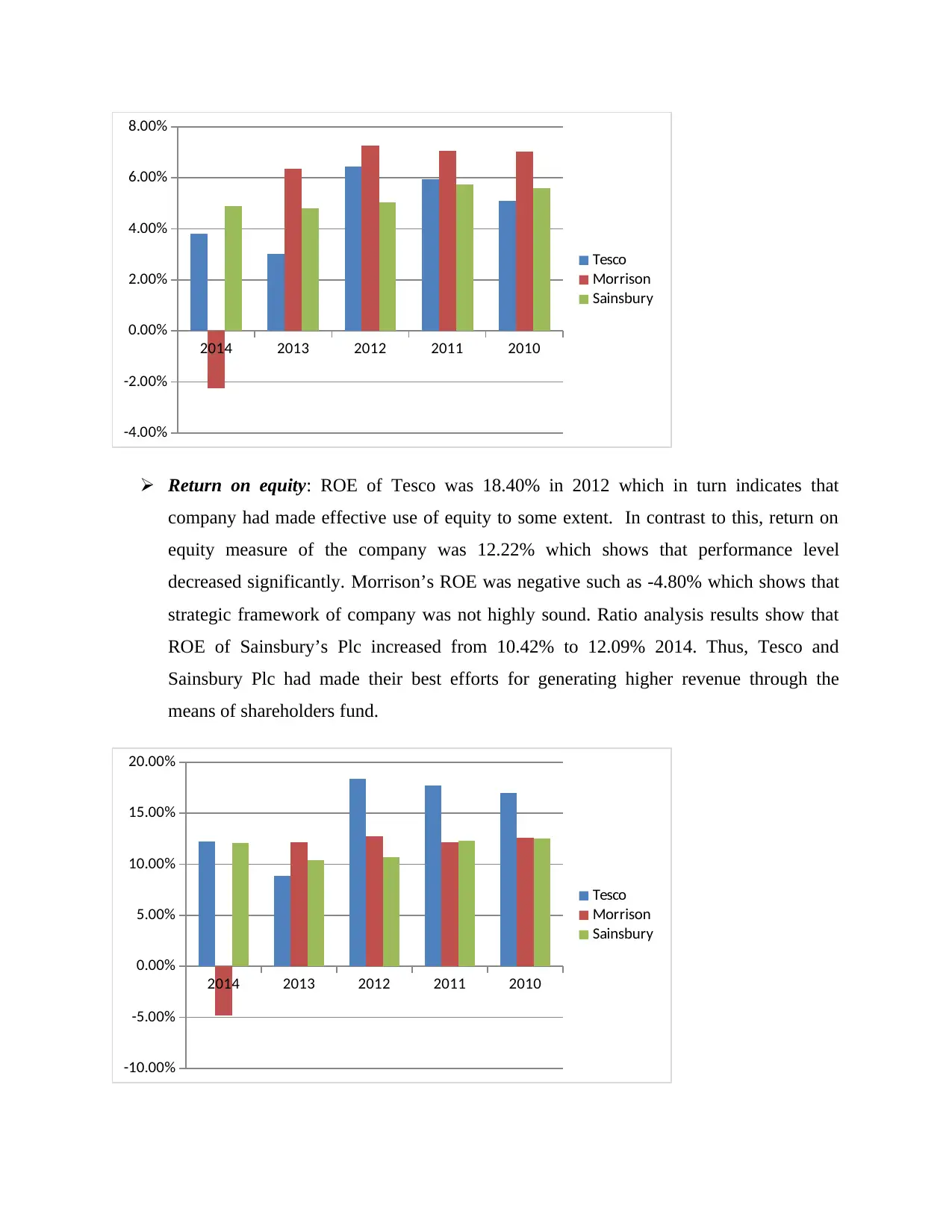

Return on assets: ROA of Tesco was 6.46%, 3.03% and 3.81% from 2012 to 2014. As

compared to Tesco, Morrison’s ROA reduced significantly from 7.04% to -2.24%. It

presents that Morrison failed to generate more funds or returns through assets. In against

to other rival firms returns generated by Sainsbury’s Plc was within 4 to 6%. Such trend

or competitor analysis shows that Sainsbury’s Plc performance of was good in the year of

2014 over others.

to 4.94% from 2010 to 2012. Hence, after such period, net profitability aspect of firm

after the fulfillment of obligations was 2.42% and 3.01% in the year of 2013 and 2014.

On the other side, NP margin of Morrison Plc moved from positive to negative trends. In

2014, NP ratio of Morrison Plc was -1.35% which in turn presents that profitability of

company was worst. On the other side, net profit margin of Sainsbury’s Plc was within

the range of 2 to 3%. Sainsbury’s net profit was 2.99% at the end of 15 March 2014.

Thus, overall evaluation presents that Tesco generated suitable margin by making

effectual control on expense level.

2014 2013 2012 2011 2010

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

Tesco

Morriosn

Sainsbury

Management effectiveness

Return on assets: ROA of Tesco was 6.46%, 3.03% and 3.81% from 2012 to 2014. As

compared to Tesco, Morrison’s ROA reduced significantly from 7.04% to -2.24%. It

presents that Morrison failed to generate more funds or returns through assets. In against

to other rival firms returns generated by Sainsbury’s Plc was within 4 to 6%. Such trend

or competitor analysis shows that Sainsbury’s Plc performance of was good in the year of

2014 over others.

2014 2013 2012 2011 2010

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

Tesco

Morrison

Sainsbury

Return on equity: ROE of Tesco was 18.40% in 2012 which in turn indicates that

company had made effective use of equity to some extent. In contrast to this, return on

equity measure of the company was 12.22% which shows that performance level

decreased significantly. Morrison’s ROE was negative such as -4.80% which shows that

strategic framework of company was not highly sound. Ratio analysis results show that

ROE of Sainsbury’s Plc increased from 10.42% to 12.09% 2014. Thus, Tesco and

Sainsbury Plc had made their best efforts for generating higher revenue through the

means of shareholders fund.

2014 2013 2012 2011 2010

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

Tesco

Morrison

Sainsbury

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

Tesco

Morrison

Sainsbury

Return on equity: ROE of Tesco was 18.40% in 2012 which in turn indicates that

company had made effective use of equity to some extent. In contrast to this, return on

equity measure of the company was 12.22% which shows that performance level

decreased significantly. Morrison’s ROE was negative such as -4.80% which shows that

strategic framework of company was not highly sound. Ratio analysis results show that

ROE of Sainsbury’s Plc increased from 10.42% to 12.09% 2014. Thus, Tesco and

Sainsbury Plc had made their best efforts for generating higher revenue through the

means of shareholders fund.

2014 2013 2012 2011 2010

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

Tesco

Morrison

Sainsbury

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Efficiency ratio analysis

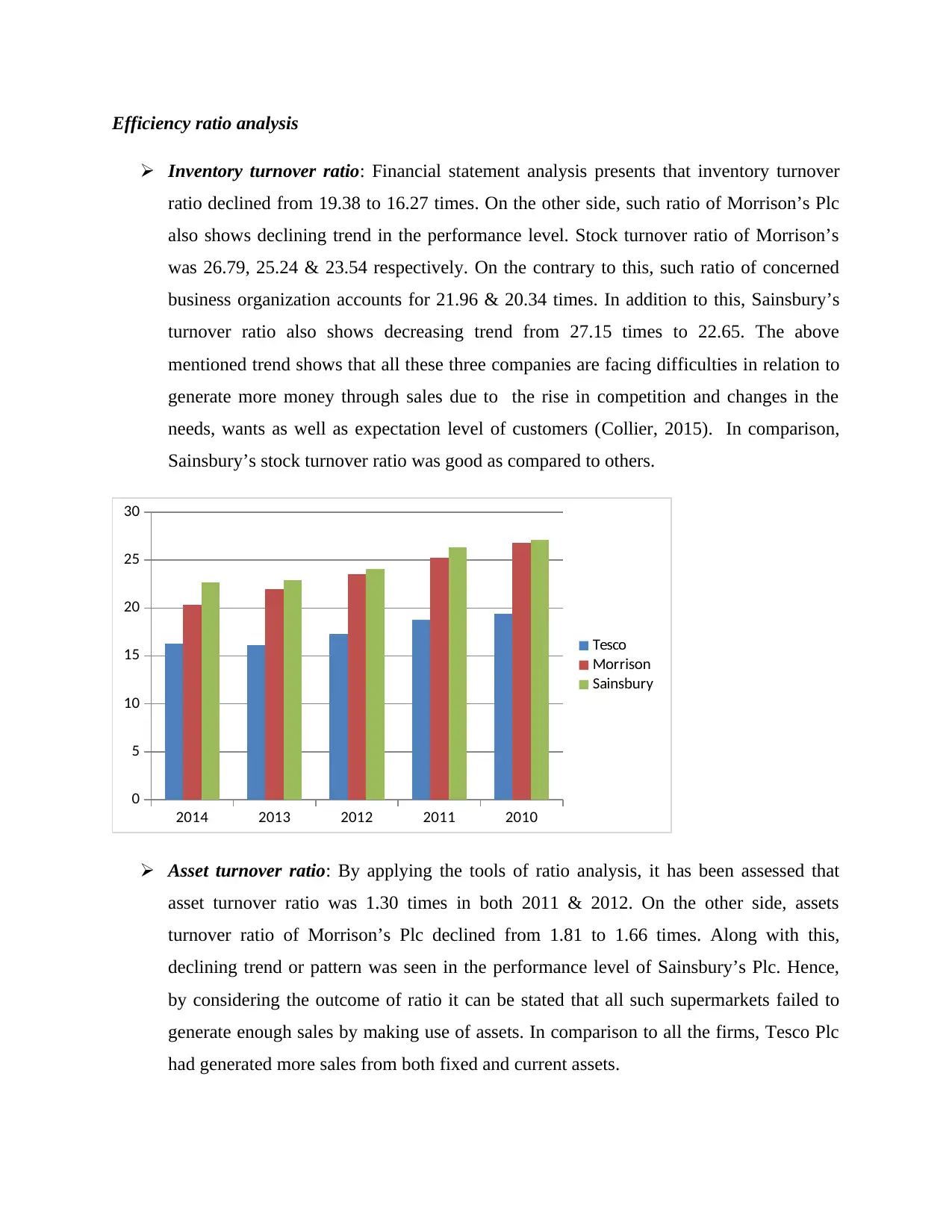

Inventory turnover ratio: Financial statement analysis presents that inventory turnover

ratio declined from 19.38 to 16.27 times. On the other side, such ratio of Morrison’s Plc

also shows declining trend in the performance level. Stock turnover ratio of Morrison’s

was 26.79, 25.24 & 23.54 respectively. On the contrary to this, such ratio of concerned

business organization accounts for 21.96 & 20.34 times. In addition to this, Sainsbury’s

turnover ratio also shows decreasing trend from 27.15 times to 22.65. The above

mentioned trend shows that all these three companies are facing difficulties in relation to

generate more money through sales due to the rise in competition and changes in the

needs, wants as well as expectation level of customers (Collier, 2015). In comparison,

Sainsbury’s stock turnover ratio was good as compared to others.

2014 2013 2012 2011 2010

0

5

10

15

20

25

30

Tesco

Morrison

Sainsbury

Asset turnover ratio: By applying the tools of ratio analysis, it has been assessed that

asset turnover ratio was 1.30 times in both 2011 & 2012. On the other side, assets

turnover ratio of Morrison’s Plc declined from 1.81 to 1.66 times. Along with this,

declining trend or pattern was seen in the performance level of Sainsbury’s Plc. Hence,

by considering the outcome of ratio it can be stated that all such supermarkets failed to

generate enough sales by making use of assets. In comparison to all the firms, Tesco Plc

had generated more sales from both fixed and current assets.

Inventory turnover ratio: Financial statement analysis presents that inventory turnover

ratio declined from 19.38 to 16.27 times. On the other side, such ratio of Morrison’s Plc

also shows declining trend in the performance level. Stock turnover ratio of Morrison’s

was 26.79, 25.24 & 23.54 respectively. On the contrary to this, such ratio of concerned

business organization accounts for 21.96 & 20.34 times. In addition to this, Sainsbury’s

turnover ratio also shows decreasing trend from 27.15 times to 22.65. The above

mentioned trend shows that all these three companies are facing difficulties in relation to

generate more money through sales due to the rise in competition and changes in the

needs, wants as well as expectation level of customers (Collier, 2015). In comparison,

Sainsbury’s stock turnover ratio was good as compared to others.

2014 2013 2012 2011 2010

0

5

10

15

20

25

30

Tesco

Morrison

Sainsbury

Asset turnover ratio: By applying the tools of ratio analysis, it has been assessed that

asset turnover ratio was 1.30 times in both 2011 & 2012. On the other side, assets

turnover ratio of Morrison’s Plc declined from 1.81 to 1.66 times. Along with this,

declining trend or pattern was seen in the performance level of Sainsbury’s Plc. Hence,

by considering the outcome of ratio it can be stated that all such supermarkets failed to

generate enough sales by making use of assets. In comparison to all the firms, Tesco Plc

had generated more sales from both fixed and current assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2014 2013 2012 2011 2010

0

0.5

1

1.5

2

2.5

Tesco

Morrison

Sainsbury

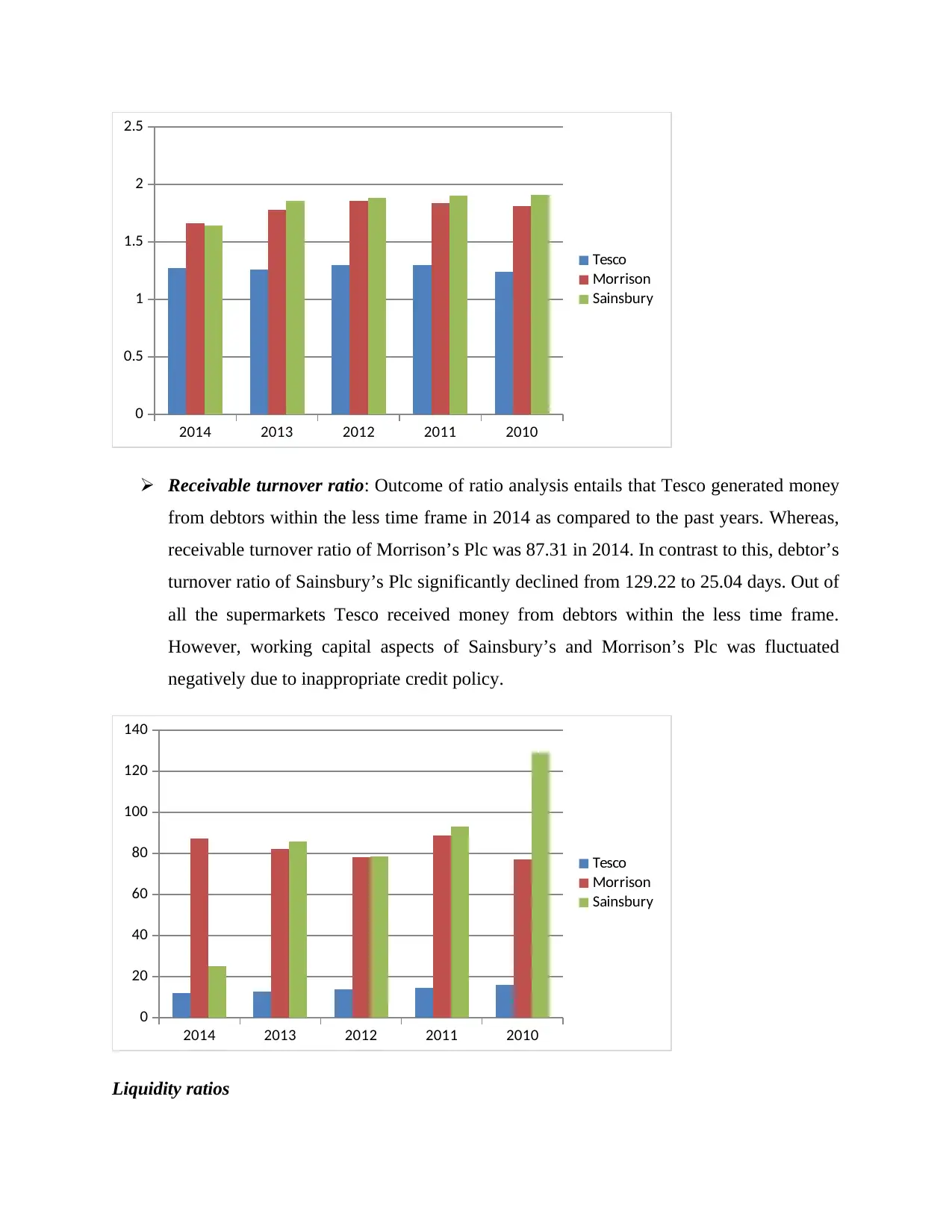

Receivable turnover ratio: Outcome of ratio analysis entails that Tesco generated money

from debtors within the less time frame in 2014 as compared to the past years. Whereas,

receivable turnover ratio of Morrison’s Plc was 87.31 in 2014. In contrast to this, debtor’s

turnover ratio of Sainsbury’s Plc significantly declined from 129.22 to 25.04 days. Out of

all the supermarkets Tesco received money from debtors within the less time frame.

However, working capital aspects of Sainsbury’s and Morrison’s Plc was fluctuated

negatively due to inappropriate credit policy.

2014 2013 2012 2011 2010

0

20

40

60

80

100

120

140

Tesco

Morrison

Sainsbury

Liquidity ratios

0

0.5

1

1.5

2

2.5

Tesco

Morrison

Sainsbury

Receivable turnover ratio: Outcome of ratio analysis entails that Tesco generated money

from debtors within the less time frame in 2014 as compared to the past years. Whereas,

receivable turnover ratio of Morrison’s Plc was 87.31 in 2014. In contrast to this, debtor’s

turnover ratio of Sainsbury’s Plc significantly declined from 129.22 to 25.04 days. Out of

all the supermarkets Tesco received money from debtors within the less time frame.

However, working capital aspects of Sainsbury’s and Morrison’s Plc was fluctuated

negatively due to inappropriate credit policy.

2014 2013 2012 2011 2010

0

20

40

60

80

100

120

140

Tesco

Morrison

Sainsbury

Liquidity ratios

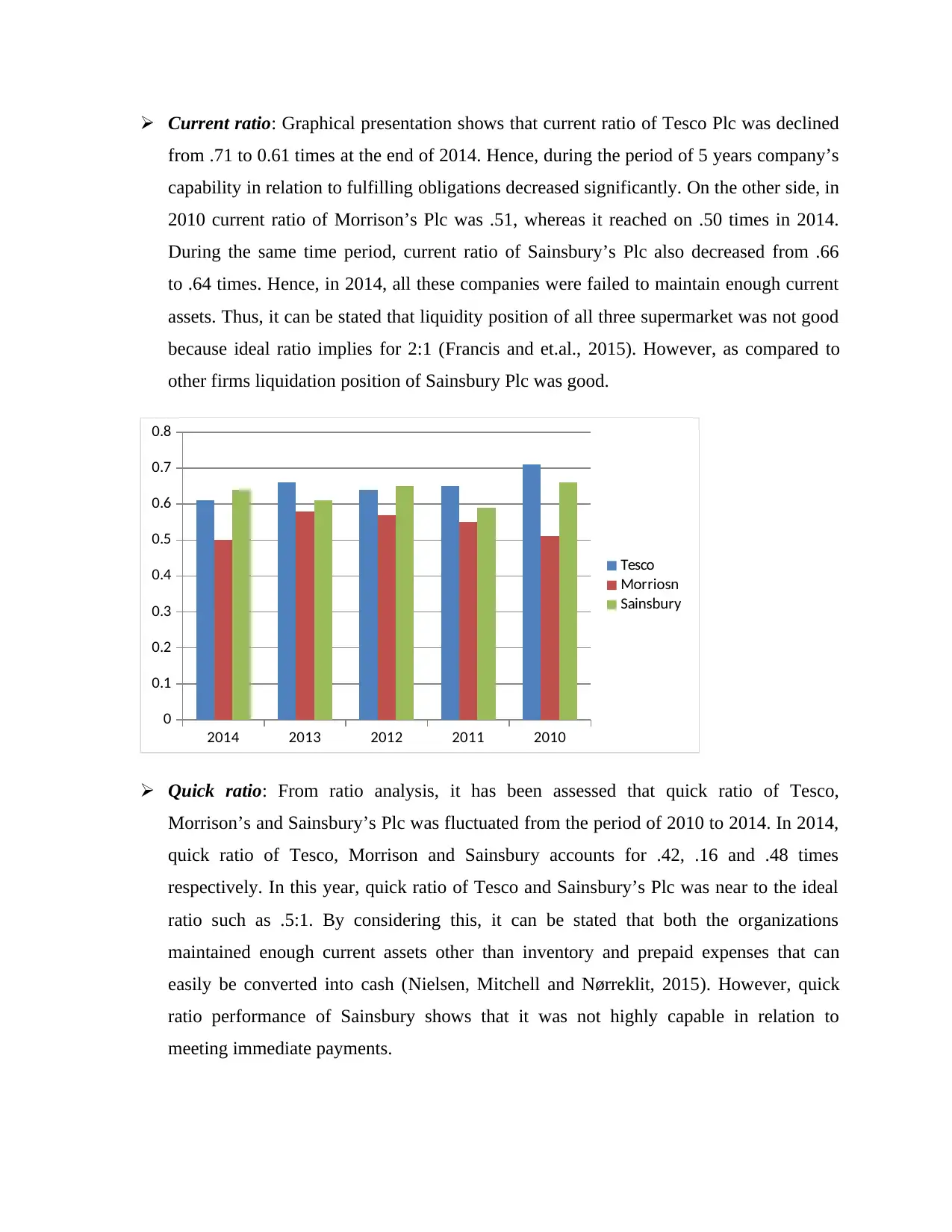

Current ratio: Graphical presentation shows that current ratio of Tesco Plc was declined

from .71 to 0.61 times at the end of 2014. Hence, during the period of 5 years company’s

capability in relation to fulfilling obligations decreased significantly. On the other side, in

2010 current ratio of Morrison’s Plc was .51, whereas it reached on .50 times in 2014.

During the same time period, current ratio of Sainsbury’s Plc also decreased from .66

to .64 times. Hence, in 2014, all these companies were failed to maintain enough current

assets. Thus, it can be stated that liquidity position of all three supermarket was not good

because ideal ratio implies for 2:1 (Francis and et.al., 2015). However, as compared to

other firms liquidation position of Sainsbury Plc was good.

2014 2013 2012 2011 2010

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Tesco

Morriosn

Sainsbury

Quick ratio: From ratio analysis, it has been assessed that quick ratio of Tesco,

Morrison’s and Sainsbury’s Plc was fluctuated from the period of 2010 to 2014. In 2014,

quick ratio of Tesco, Morrison and Sainsbury accounts for .42, .16 and .48 times

respectively. In this year, quick ratio of Tesco and Sainsbury’s Plc was near to the ideal

ratio such as .5:1. By considering this, it can be stated that both the organizations

maintained enough current assets other than inventory and prepaid expenses that can

easily be converted into cash (Nielsen, Mitchell and Nørreklit, 2015). However, quick

ratio performance of Sainsbury shows that it was not highly capable in relation to

meeting immediate payments.

from .71 to 0.61 times at the end of 2014. Hence, during the period of 5 years company’s

capability in relation to fulfilling obligations decreased significantly. On the other side, in

2010 current ratio of Morrison’s Plc was .51, whereas it reached on .50 times in 2014.

During the same time period, current ratio of Sainsbury’s Plc also decreased from .66

to .64 times. Hence, in 2014, all these companies were failed to maintain enough current

assets. Thus, it can be stated that liquidity position of all three supermarket was not good

because ideal ratio implies for 2:1 (Francis and et.al., 2015). However, as compared to

other firms liquidation position of Sainsbury Plc was good.

2014 2013 2012 2011 2010

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Tesco

Morriosn

Sainsbury

Quick ratio: From ratio analysis, it has been assessed that quick ratio of Tesco,

Morrison’s and Sainsbury’s Plc was fluctuated from the period of 2010 to 2014. In 2014,

quick ratio of Tesco, Morrison and Sainsbury accounts for .42, .16 and .48 times

respectively. In this year, quick ratio of Tesco and Sainsbury’s Plc was near to the ideal

ratio such as .5:1. By considering this, it can be stated that both the organizations

maintained enough current assets other than inventory and prepaid expenses that can

easily be converted into cash (Nielsen, Mitchell and Nørreklit, 2015). However, quick

ratio performance of Sainsbury shows that it was not highly capable in relation to

meeting immediate payments.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2014 2013 2012 2011 2010

0

0.1

0.2

0.3

0.4

0.5

0.6

Tesco

Morriosn

Sainsbury

Non-financial ratios

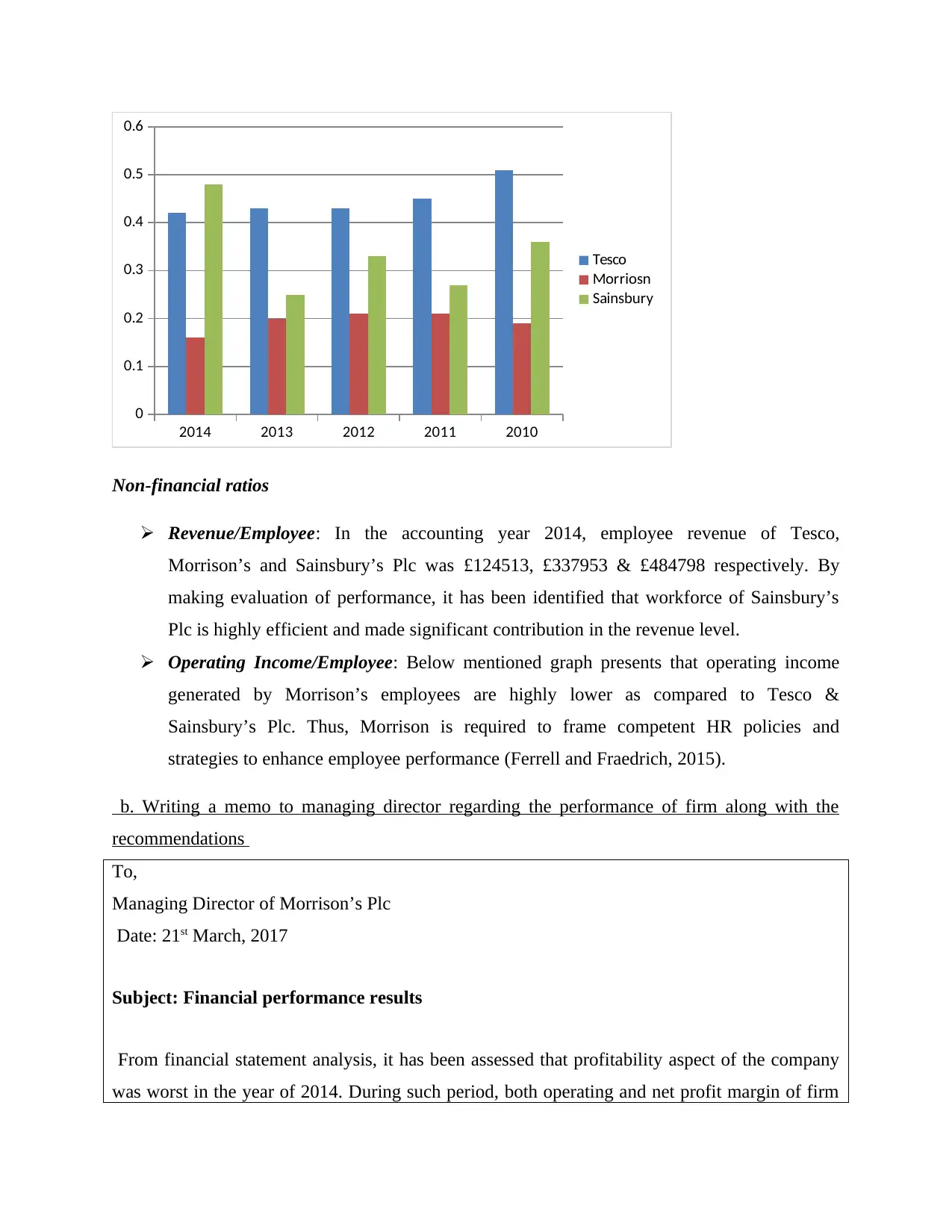

Revenue/Employee: In the accounting year 2014, employee revenue of Tesco,

Morrison’s and Sainsbury’s Plc was £124513, £337953 & £484798 respectively. By

making evaluation of performance, it has been identified that workforce of Sainsbury’s

Plc is highly efficient and made significant contribution in the revenue level.

Operating Income/Employee: Below mentioned graph presents that operating income

generated by Morrison’s employees are highly lower as compared to Tesco &

Sainsbury’s Plc. Thus, Morrison is required to frame competent HR policies and

strategies to enhance employee performance (Ferrell and Fraedrich, 2015).

b. Writing a memo to managing director regarding the performance of firm along with the

recommendations

To,

Managing Director of Morrison’s Plc

Date: 21st March, 2017

Subject: Financial performance results

From financial statement analysis, it has been assessed that profitability aspect of the company

was worst in the year of 2014. During such period, both operating and net profit margin of firm

0

0.1

0.2

0.3

0.4

0.5

0.6

Tesco

Morriosn

Sainsbury

Non-financial ratios

Revenue/Employee: In the accounting year 2014, employee revenue of Tesco,

Morrison’s and Sainsbury’s Plc was £124513, £337953 & £484798 respectively. By

making evaluation of performance, it has been identified that workforce of Sainsbury’s

Plc is highly efficient and made significant contribution in the revenue level.

Operating Income/Employee: Below mentioned graph presents that operating income

generated by Morrison’s employees are highly lower as compared to Tesco &

Sainsbury’s Plc. Thus, Morrison is required to frame competent HR policies and

strategies to enhance employee performance (Ferrell and Fraedrich, 2015).

b. Writing a memo to managing director regarding the performance of firm along with the

recommendations

To,

Managing Director of Morrison’s Plc

Date: 21st March, 2017

Subject: Financial performance results

From financial statement analysis, it has been assessed that profitability aspect of the company

was worst in the year of 2014. During such period, both operating and net profit margin of firm

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

was negative which in turn closely influence the future monetary aspects of firm. Further, it has

been identified that liquidity position of the company was not sound. Moreover, as compared to

ideal ratio business unit was maintained only 25% of current assets. This in turn entails that

company was not highly capable in relation to meeting its current liabilities during the period of

2014. Along with this, company was also failed to generate high return from assets such as

debtors, inventory etc. Thus, it is suggested to the firm to follow below mentioned aspects which

will help it in enhancing financial performance:

Business organization should focus on sales promotional activities and adverstisement campaign.

Hence, by providing suitable information to the large number of customer regarding the quality

and price of product sales revenue and thereby profitability can be maximized. Along with this,

Morrison Plc should undertake budgeting technique for making control on cost level.

In addition to this, Morrison should lay more emphasis on maintaining current assets such as

cash etc by reducing the level of expenses. It can be done by the firm through the means of

continuous monitoring. By this, firm can maintain high liquidity and thereby would become able

to meet obligations on time.

Further, by encouraging personnel to give their best efforts Morrison’s Plc can make optimum

utilization of assets and thereby would become able to generate high profit margin.

Hence, by following all such measurers Morrison Plc can make significant improvement in the

profitability and liquidity aspects. All these aspects will help company in gaining competitive

edge over others.

Sincerely

Financial analysts

c. Outlining the limitations of financial ratios

Limitations

Different rules and regulations: Accounting policies which are undertaken by different

organizations highly differ. Moreover, some organization considers UK GAAP, whereas

other considers IAS and IFRS for both recording and reporting (Reckers and Samuelson,

2016).

been identified that liquidity position of the company was not sound. Moreover, as compared to

ideal ratio business unit was maintained only 25% of current assets. This in turn entails that

company was not highly capable in relation to meeting its current liabilities during the period of

2014. Along with this, company was also failed to generate high return from assets such as

debtors, inventory etc. Thus, it is suggested to the firm to follow below mentioned aspects which

will help it in enhancing financial performance:

Business organization should focus on sales promotional activities and adverstisement campaign.

Hence, by providing suitable information to the large number of customer regarding the quality

and price of product sales revenue and thereby profitability can be maximized. Along with this,

Morrison Plc should undertake budgeting technique for making control on cost level.

In addition to this, Morrison should lay more emphasis on maintaining current assets such as

cash etc by reducing the level of expenses. It can be done by the firm through the means of

continuous monitoring. By this, firm can maintain high liquidity and thereby would become able

to meet obligations on time.

Further, by encouraging personnel to give their best efforts Morrison’s Plc can make optimum

utilization of assets and thereby would become able to generate high profit margin.

Hence, by following all such measurers Morrison Plc can make significant improvement in the

profitability and liquidity aspects. All these aspects will help company in gaining competitive

edge over others.

Sincerely

Financial analysts

c. Outlining the limitations of financial ratios

Limitations

Different rules and regulations: Accounting policies which are undertaken by different

organizations highly differ. Moreover, some organization considers UK GAAP, whereas

other considers IAS and IFRS for both recording and reporting (Reckers and Samuelson,

2016).

Inflation: Rate of inflation changes over the years or time frame which in turn closely

influences the financial health and performance (Anderson and et.al., 2015). Hence, rate

of inflation highly varied from one year to another. In this, it is not possible to evaluate

company’s performance over the years.

Historical evaluation: Financial statement analysis presents information regarding the

past performance. However, it does not reflect trend in relation to future performance and

aspects (Bebbington, Unerman and O'Dwyer, 2014). Hence, by considering this it can be

stated ratio analysis tool does not help in making suitable decision regarding investment.

SECTION B

a. Using net present value technique to assess whether three year contract is profitable or not

Calculation of cash inflow

Particulars Year 1 Year 2 year 3

Sales revenue / turnover 180000 216000 259200

Material 60000 63000 66150

Labor 40000 42000 44100

Depreciation 11250 11250 11250

total outflow 111250 116250 121500

EBIT 68750 99750 137700

Taxation 0

22687.

5

32917.

5

EAT 68750

77062.

5 104783

influences the financial health and performance (Anderson and et.al., 2015). Hence, rate

of inflation highly varied from one year to another. In this, it is not possible to evaluate

company’s performance over the years.

Historical evaluation: Financial statement analysis presents information regarding the

past performance. However, it does not reflect trend in relation to future performance and

aspects (Bebbington, Unerman and O'Dwyer, 2014). Hence, by considering this it can be

stated ratio analysis tool does not help in making suitable decision regarding investment.

SECTION B

a. Using net present value technique to assess whether three year contract is profitable or not

Calculation of cash inflow

Particulars Year 1 Year 2 year 3

Sales revenue / turnover 180000 216000 259200

Material 60000 63000 66150

Labor 40000 42000 44100

Depreciation 11250 11250 11250

total outflow 111250 116250 121500

EBIT 68750 99750 137700

Taxation 0

22687.

5

32917.

5

EAT 68750

77062.

5 104783

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.