Accounting and Finance - Assignment

VerifiedAdded on 2021/05/27

|14

|1824

|27

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING AND FINANCE

Accounting and Finance

Name of the Student

Name of the University

Author Note

Accounting and Finance

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING AND FINANCE

Executive summary:

The assignment is about two case studies that is divided into two sections Part A and part B.

Part A is about Saturn Pet Care that is seeking investment into two projects. Such projects are

evaluated by using the techniques of capital budgeting. Part B on other hand is about ARB

limited for which the financial performance is analyzed using tools of ratio and CAPM.

Table of Contents

Executive summary:...................................................................................................................1

Part A:........................................................................................................................................3

Executive summary:

The assignment is about two case studies that is divided into two sections Part A and part B.

Part A is about Saturn Pet Care that is seeking investment into two projects. Such projects are

evaluated by using the techniques of capital budgeting. Part B on other hand is about ARB

limited for which the financial performance is analyzed using tools of ratio and CAPM.

Table of Contents

Executive summary:...................................................................................................................1

Part A:........................................................................................................................................3

ACCOUNTING AND FINANCE

Analysis of capital budgeting for Bathurst project:...................................................................3

Analysis of capital budgeting for Wodonga project:.................................................................3

Importance of product cannibalization in capital budgeting decision:......................................3

Capital budgeting options for sales estimation:.........................................................................3

Evaluation of original value of vacant Wodonga factory :........................................................3

Part B:.........................................................................................................................................3

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................4

Categorizing the capital structure of ARB Corporation Limited:..............................................4

Computation of WACC:............................................................................................................4

Determining appropriate return using CAPM:...........................................................................4

Comparing the capital structure of ARM limited with similar firms of same industry:............4

Analyzing the financial performance of ARB limited using financial ratios:...........................4

Analyzing the change in capital structure for the last three years:............................................4

Evaluating the firm’s success in generating wealth to their shareholders:................................4

Recommendations for adopting alternative capital strcuture:....................................................4

Conclusion:................................................................................................................................4

References list:...........................................................................................................................6

Analysis of capital budgeting for Bathurst project:...................................................................3

Analysis of capital budgeting for Wodonga project:.................................................................3

Importance of product cannibalization in capital budgeting decision:......................................3

Capital budgeting options for sales estimation:.........................................................................3

Evaluation of original value of vacant Wodonga factory :........................................................3

Part B:.........................................................................................................................................3

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................4

Categorizing the capital structure of ARB Corporation Limited:..............................................4

Computation of WACC:............................................................................................................4

Determining appropriate return using CAPM:...........................................................................4

Comparing the capital structure of ARM limited with similar firms of same industry:............4

Analyzing the financial performance of ARB limited using financial ratios:...........................4

Analyzing the change in capital structure for the last three years:............................................4

Evaluating the firm’s success in generating wealth to their shareholders:................................4

Recommendations for adopting alternative capital strcuture:....................................................4

Conclusion:................................................................................................................................4

References list:...........................................................................................................................6

ACCOUNTING AND FINANCE

Part A:

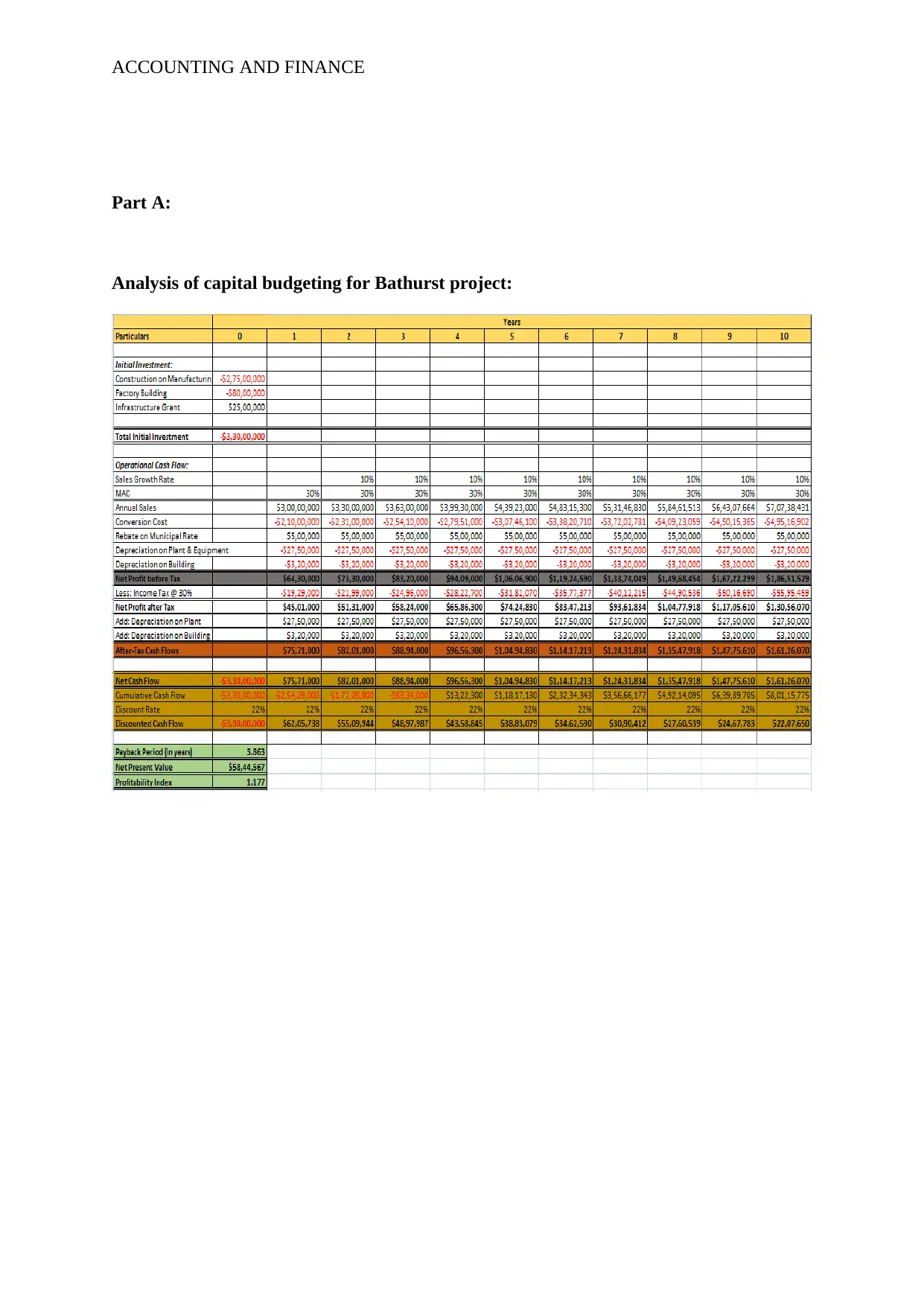

Analysis of capital budgeting for Bathurst project:

Part A:

Analysis of capital budgeting for Bathurst project:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING AND FINANCE

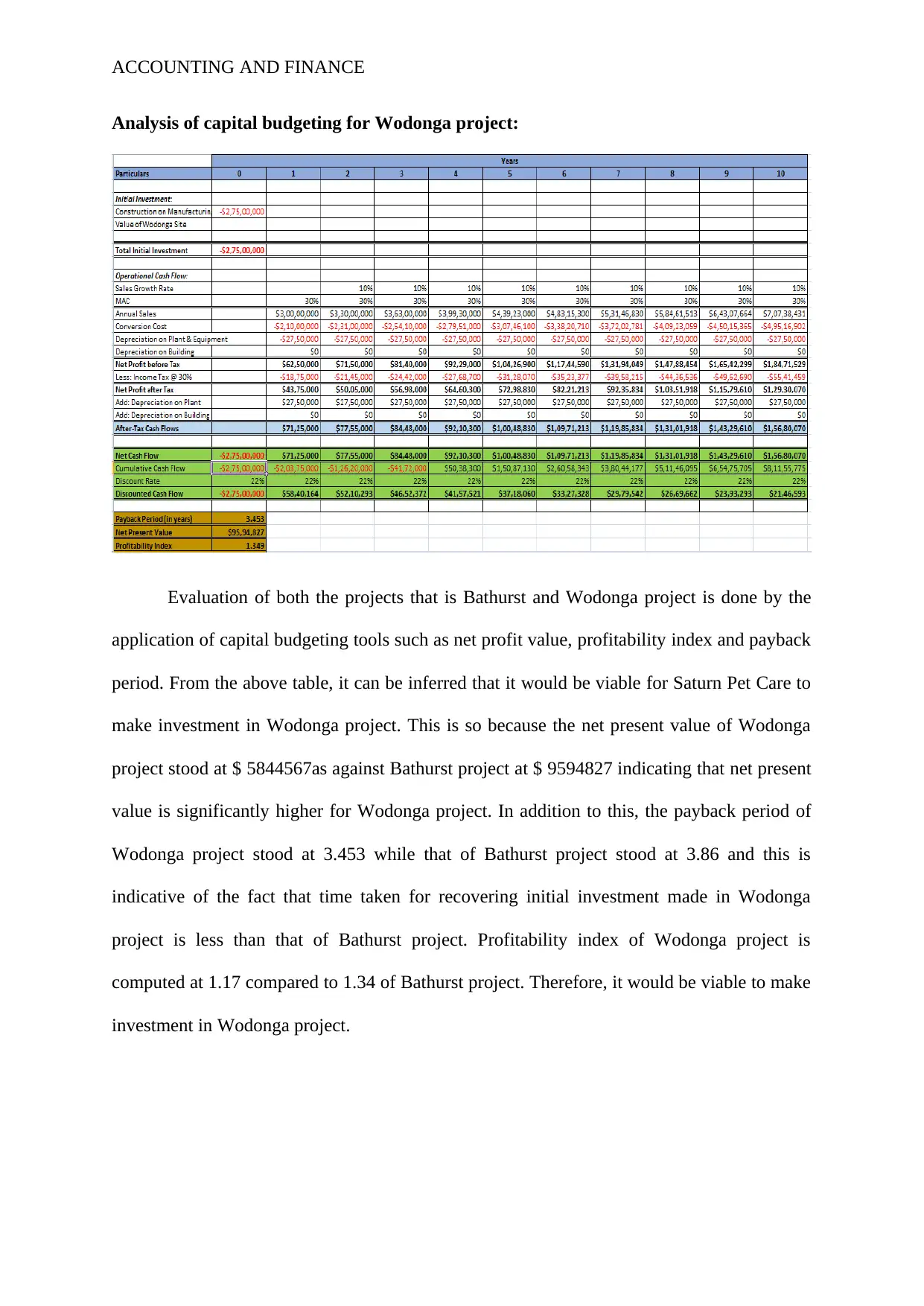

Analysis of capital budgeting for Wodonga project:

Evaluation of both the projects that is Bathurst and Wodonga project is done by the

application of capital budgeting tools such as net profit value, profitability index and payback

period. From the above table, it can be inferred that it would be viable for Saturn Pet Care to

make investment in Wodonga project. This is so because the net present value of Wodonga

project stood at $ 5844567as against Bathurst project at $ 9594827 indicating that net present

value is significantly higher for Wodonga project. In addition to this, the payback period of

Wodonga project stood at 3.453 while that of Bathurst project stood at 3.86 and this is

indicative of the fact that time taken for recovering initial investment made in Wodonga

project is less than that of Bathurst project. Profitability index of Wodonga project is

computed at 1.17 compared to 1.34 of Bathurst project. Therefore, it would be viable to make

investment in Wodonga project.

Analysis of capital budgeting for Wodonga project:

Evaluation of both the projects that is Bathurst and Wodonga project is done by the

application of capital budgeting tools such as net profit value, profitability index and payback

period. From the above table, it can be inferred that it would be viable for Saturn Pet Care to

make investment in Wodonga project. This is so because the net present value of Wodonga

project stood at $ 5844567as against Bathurst project at $ 9594827 indicating that net present

value is significantly higher for Wodonga project. In addition to this, the payback period of

Wodonga project stood at 3.453 while that of Bathurst project stood at 3.86 and this is

indicative of the fact that time taken for recovering initial investment made in Wodonga

project is less than that of Bathurst project. Profitability index of Wodonga project is

computed at 1.17 compared to 1.34 of Bathurst project. Therefore, it would be viable to make

investment in Wodonga project.

ACCOUNTING AND FINANCE

Importance of product cannibalization in capital budgeting decision:

Cannibalization of product is a strategy that is implemented by organization when

they intend to increase the sales of newly developed product by reducing the volume of sales,

sales revenue and share of market of the existing products. Under such strategy, there are

negative incremental effects of newly launched product as it reduces the sales of existing

product and any amount of loss generated from such product should be treated as cost. Saturn

Pet Care has adopted this particular strategy as a measure for promoting their new product

that will have the impact in terms of increasing sales revenue. Such affect will have

considerable impact on capital budgeting decision and accordingly investment decision (Chen

and Hong 2017).

Capital budgeting options for sales estimation:

It is perceived by strategy finance director of Saturn Pet Care that the amount of

estimated sales is unreasonably high and any amount of such error would considerably

impact the decision relating to capital budgeting. The estimation of wrong budgeted sales

would have considerable impact on the process of budgeting and thereby on the decision of

making investment in project. Therefore, in order for minimizing the impact of such errors,

appropriate steps must be taken by Saturn Limited. Under such circumstances, it would be

suitable to employ the technique of net present value as using this value will help in

neutralizing the influence of wrong estimation in sales by generating an increased cash

outflow.

Evaluation of original value of vacant Wodonga factory:

Considering the original value of vacant Wodonga factory is the capital budgeting

analysis is another area of concern. It is opined by Natha that original factory cost should be

involved in the present value analysis. However, if the factory cost is considered then there

Importance of product cannibalization in capital budgeting decision:

Cannibalization of product is a strategy that is implemented by organization when

they intend to increase the sales of newly developed product by reducing the volume of sales,

sales revenue and share of market of the existing products. Under such strategy, there are

negative incremental effects of newly launched product as it reduces the sales of existing

product and any amount of loss generated from such product should be treated as cost. Saturn

Pet Care has adopted this particular strategy as a measure for promoting their new product

that will have the impact in terms of increasing sales revenue. Such affect will have

considerable impact on capital budgeting decision and accordingly investment decision (Chen

and Hong 2017).

Capital budgeting options for sales estimation:

It is perceived by strategy finance director of Saturn Pet Care that the amount of

estimated sales is unreasonably high and any amount of such error would considerably

impact the decision relating to capital budgeting. The estimation of wrong budgeted sales

would have considerable impact on the process of budgeting and thereby on the decision of

making investment in project. Therefore, in order for minimizing the impact of such errors,

appropriate steps must be taken by Saturn Limited. Under such circumstances, it would be

suitable to employ the technique of net present value as using this value will help in

neutralizing the influence of wrong estimation in sales by generating an increased cash

outflow.

Evaluation of original value of vacant Wodonga factory:

Considering the original value of vacant Wodonga factory is the capital budgeting

analysis is another area of concern. It is opined by Natha that original factory cost should be

involved in the present value analysis. However, if the factory cost is considered then there

ACCOUNTING AND FINANCE

would be change in net present value. There might be negative impact of such inclusion and

ultimately influencing the capital budgeting decision.

Part B:

Introduction:

The report is prepared for evaluation the financial performance of ARB limited by

analyzing their capital structure, financial ratios, and wealth of shareholders and cost of

capital. Change in structure of capital has been analyzed over the past three years by

comparing to the other firm operating in the same industry.

Discussion:

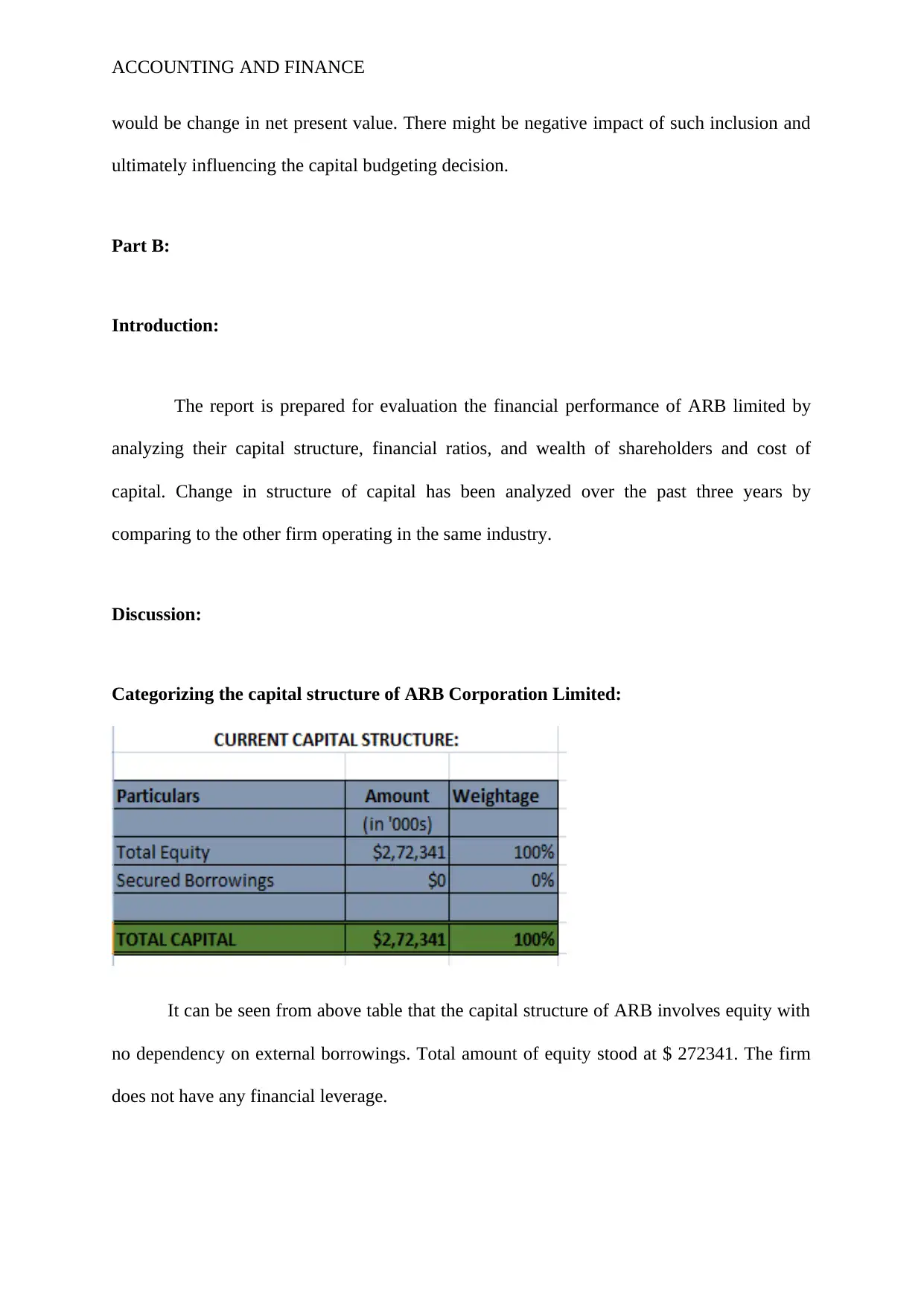

Categorizing the capital structure of ARB Corporation Limited:

It can be seen from above table that the capital structure of ARB involves equity with

no dependency on external borrowings. Total amount of equity stood at $ 272341. The firm

does not have any financial leverage.

would be change in net present value. There might be negative impact of such inclusion and

ultimately influencing the capital budgeting decision.

Part B:

Introduction:

The report is prepared for evaluation the financial performance of ARB limited by

analyzing their capital structure, financial ratios, and wealth of shareholders and cost of

capital. Change in structure of capital has been analyzed over the past three years by

comparing to the other firm operating in the same industry.

Discussion:

Categorizing the capital structure of ARB Corporation Limited:

It can be seen from above table that the capital structure of ARB involves equity with

no dependency on external borrowings. Total amount of equity stood at $ 272341. The firm

does not have any financial leverage.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE

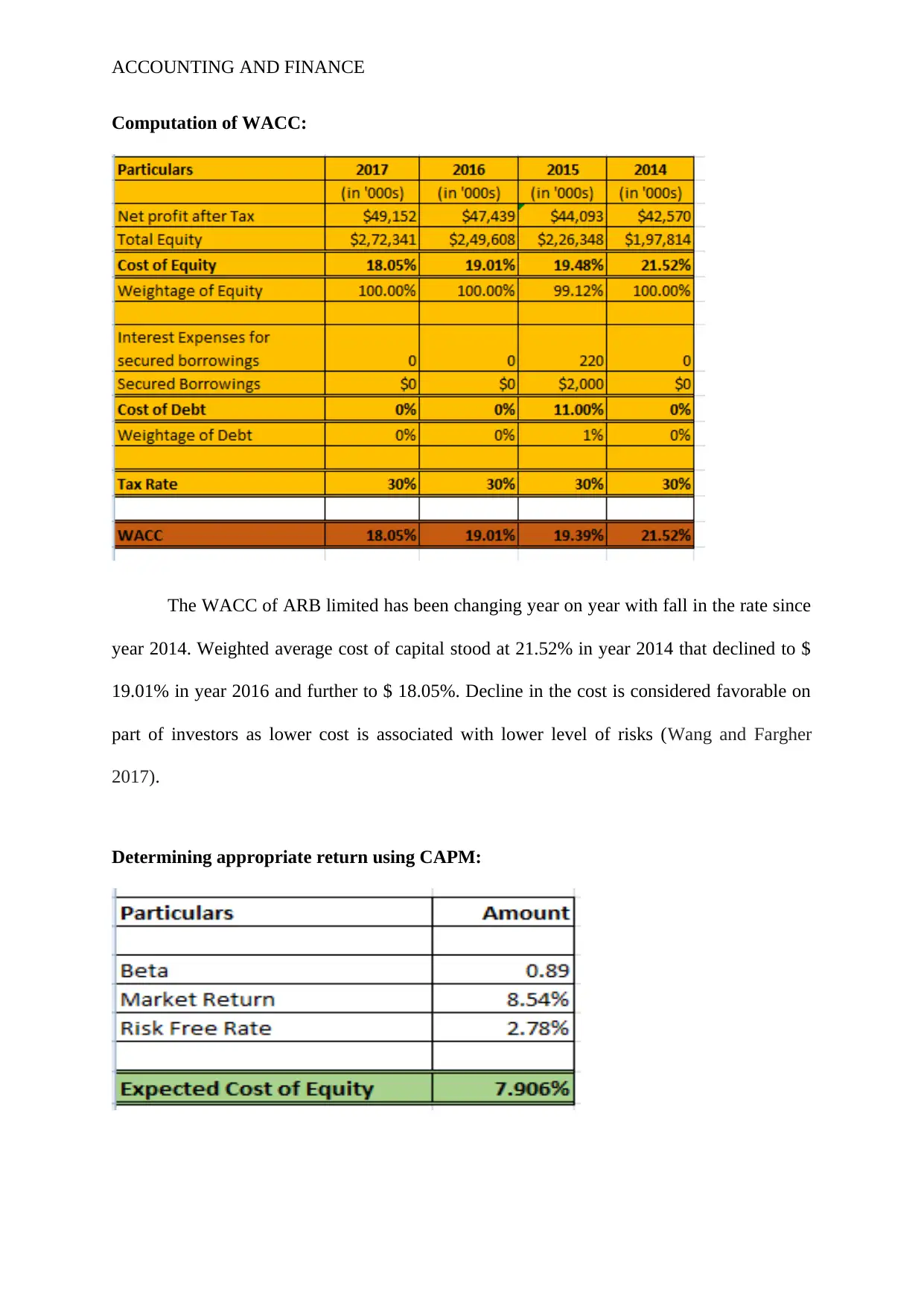

Computation of WACC:

The WACC of ARB limited has been changing year on year with fall in the rate since

year 2014. Weighted average cost of capital stood at 21.52% in year 2014 that declined to $

19.01% in year 2016 and further to $ 18.05%. Decline in the cost is considered favorable on

part of investors as lower cost is associated with lower level of risks (Wang and Fargher

2017).

Determining appropriate return using CAPM:

Computation of WACC:

The WACC of ARB limited has been changing year on year with fall in the rate since

year 2014. Weighted average cost of capital stood at 21.52% in year 2014 that declined to $

19.01% in year 2016 and further to $ 18.05%. Decline in the cost is considered favorable on

part of investors as lower cost is associated with lower level of risks (Wang and Fargher

2017).

Determining appropriate return using CAPM:

ACCOUNTING AND FINANCE

Value of equity cost is different when it is computed using general method and when

it is computed using CAPM. Cost of equity computed under the CAPM stood at 7.906% as

against 18.05% under the general method.

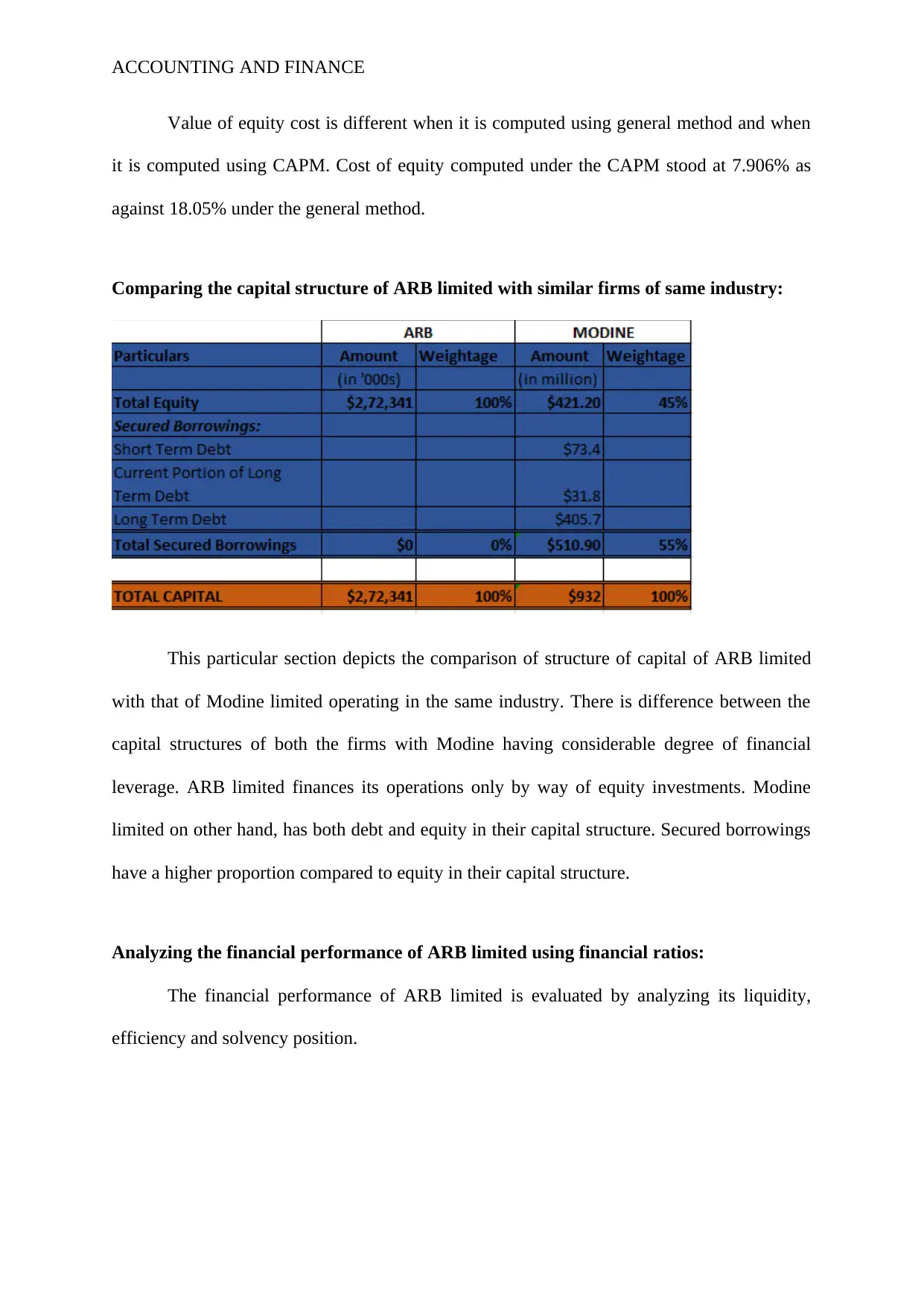

Comparing the capital structure of ARB limited with similar firms of same industry:

This particular section depicts the comparison of structure of capital of ARB limited

with that of Modine limited operating in the same industry. There is difference between the

capital structures of both the firms with Modine having considerable degree of financial

leverage. ARB limited finances its operations only by way of equity investments. Modine

limited on other hand, has both debt and equity in their capital structure. Secured borrowings

have a higher proportion compared to equity in their capital structure.

Analyzing the financial performance of ARB limited using financial ratios:

The financial performance of ARB limited is evaluated by analyzing its liquidity,

efficiency and solvency position.

Value of equity cost is different when it is computed using general method and when

it is computed using CAPM. Cost of equity computed under the CAPM stood at 7.906% as

against 18.05% under the general method.

Comparing the capital structure of ARB limited with similar firms of same industry:

This particular section depicts the comparison of structure of capital of ARB limited

with that of Modine limited operating in the same industry. There is difference between the

capital structures of both the firms with Modine having considerable degree of financial

leverage. ARB limited finances its operations only by way of equity investments. Modine

limited on other hand, has both debt and equity in their capital structure. Secured borrowings

have a higher proportion compared to equity in their capital structure.

Analyzing the financial performance of ARB limited using financial ratios:

The financial performance of ARB limited is evaluated by analyzing its liquidity,

efficiency and solvency position.

ACCOUNTING AND FINANCE

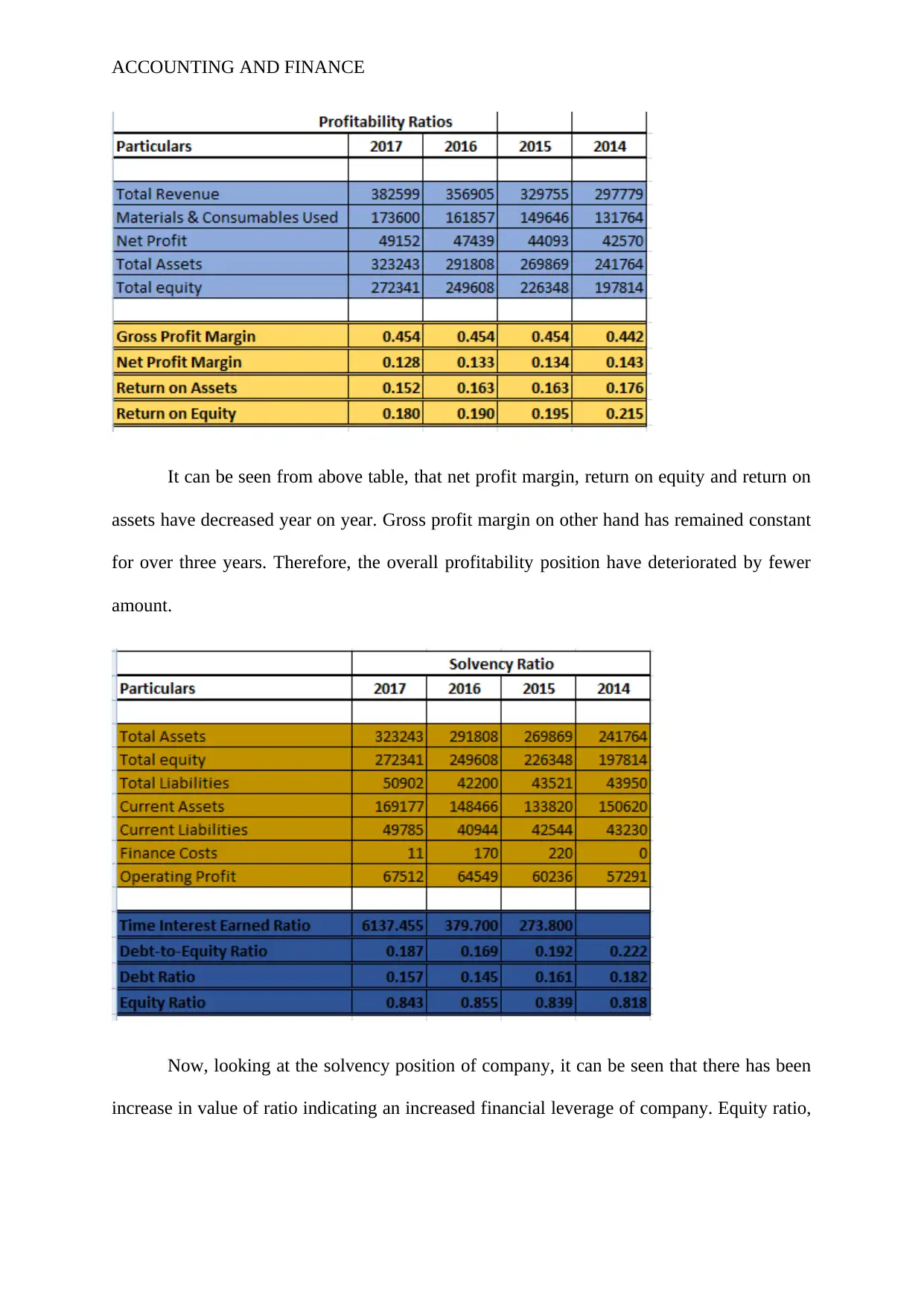

It can be seen from above table, that net profit margin, return on equity and return on

assets have decreased year on year. Gross profit margin on other hand has remained constant

for over three years. Therefore, the overall profitability position have deteriorated by fewer

amount.

Now, looking at the solvency position of company, it can be seen that there has been

increase in value of ratio indicating an increased financial leverage of company. Equity ratio,

It can be seen from above table, that net profit margin, return on equity and return on

assets have decreased year on year. Gross profit margin on other hand has remained constant

for over three years. Therefore, the overall profitability position have deteriorated by fewer

amount.

Now, looking at the solvency position of company, it can be seen that there has been

increase in value of ratio indicating an increased financial leverage of company. Equity ratio,

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING AND FINANCE

debt ratio, time interest earned ratio and debt to equity ratio have declined in earlier year and

have increased subsequently in later years (Elliot et al. 2016).

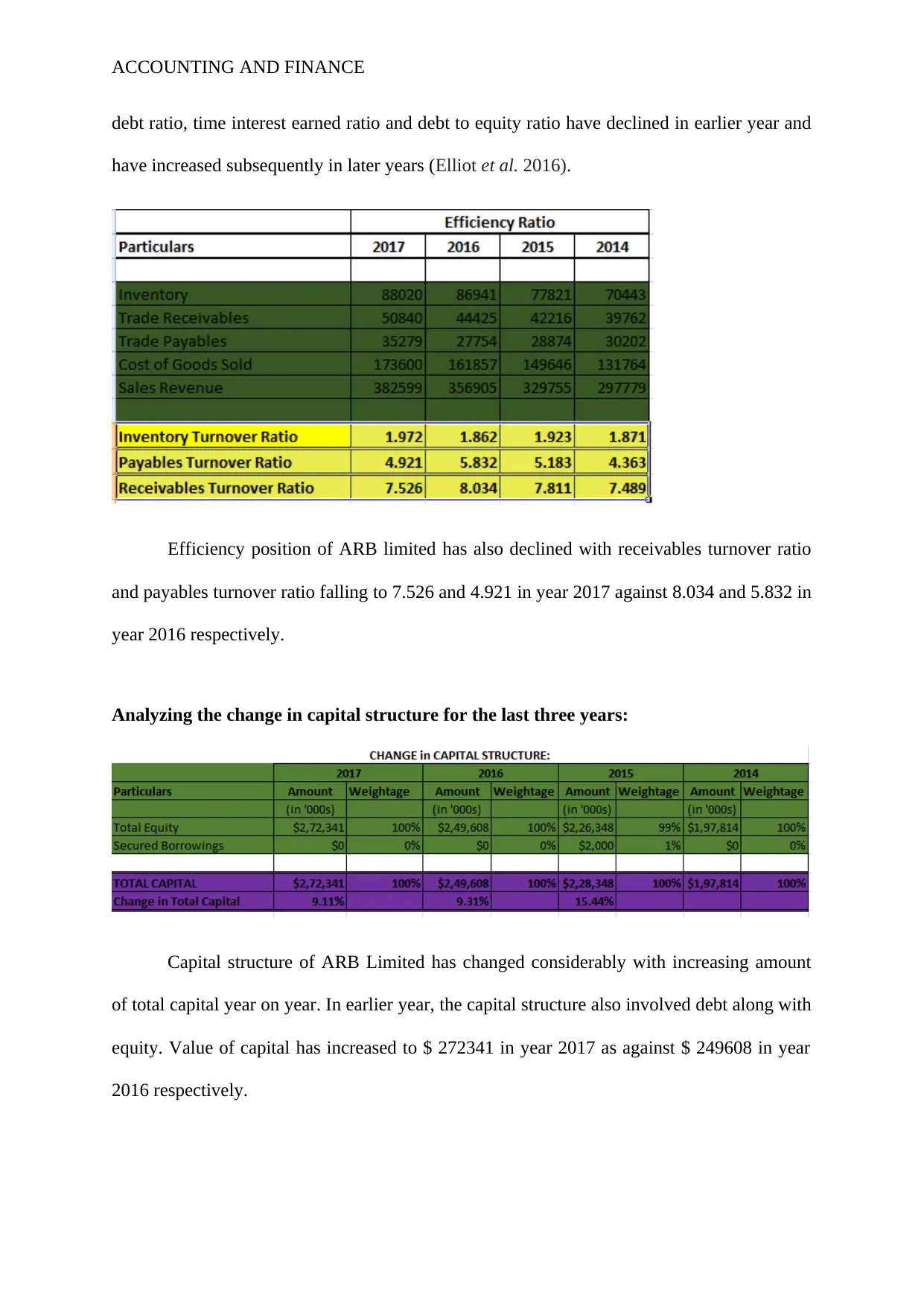

Efficiency position of ARB limited has also declined with receivables turnover ratio

and payables turnover ratio falling to 7.526 and 4.921 in year 2017 against 8.034 and 5.832 in

year 2016 respectively.

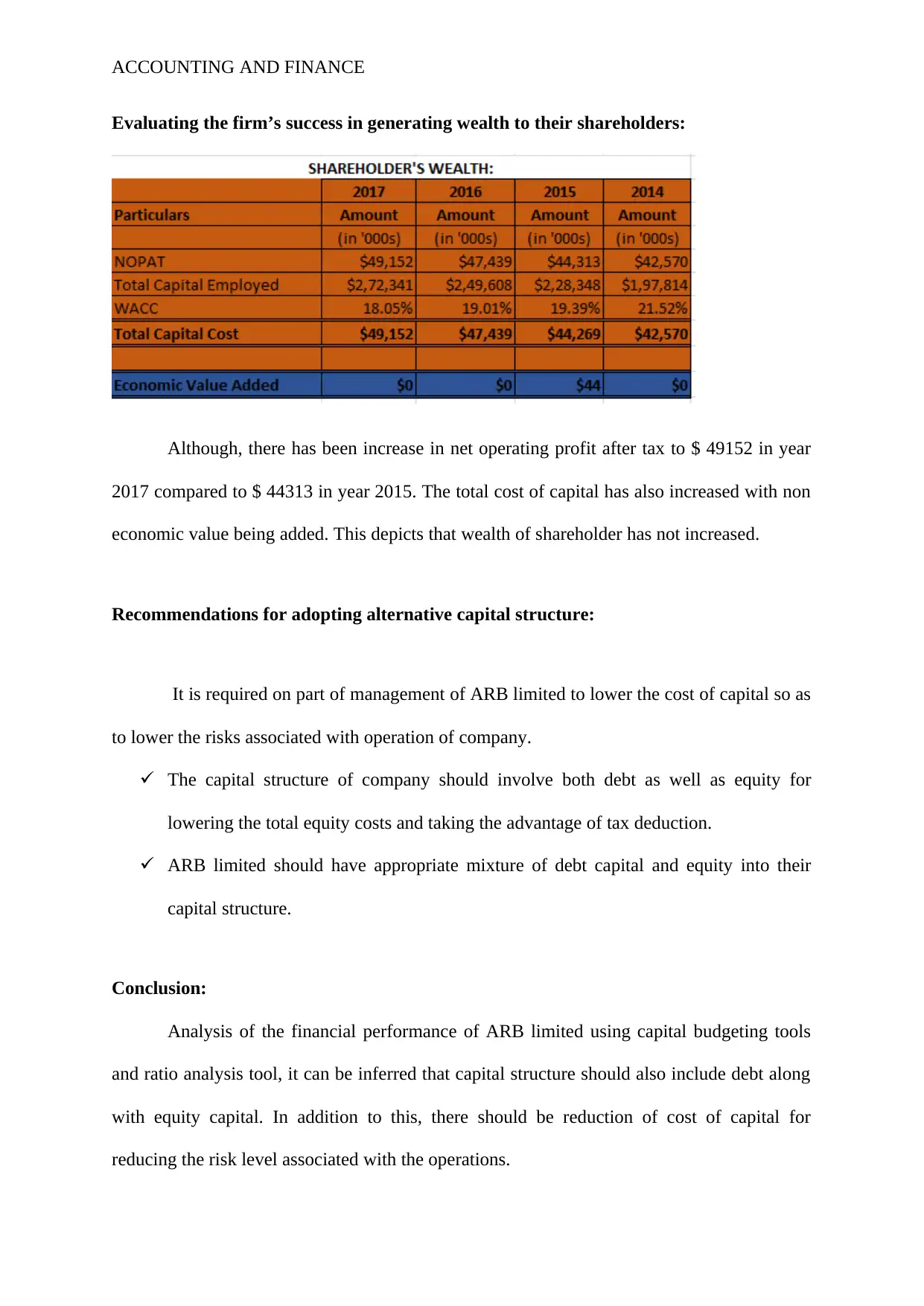

Analyzing the change in capital structure for the last three years:

Capital structure of ARB Limited has changed considerably with increasing amount

of total capital year on year. In earlier year, the capital structure also involved debt along with

equity. Value of capital has increased to $ 272341 in year 2017 as against $ 249608 in year

2016 respectively.

debt ratio, time interest earned ratio and debt to equity ratio have declined in earlier year and

have increased subsequently in later years (Elliot et al. 2016).

Efficiency position of ARB limited has also declined with receivables turnover ratio

and payables turnover ratio falling to 7.526 and 4.921 in year 2017 against 8.034 and 5.832 in

year 2016 respectively.

Analyzing the change in capital structure for the last three years:

Capital structure of ARB Limited has changed considerably with increasing amount

of total capital year on year. In earlier year, the capital structure also involved debt along with

equity. Value of capital has increased to $ 272341 in year 2017 as against $ 249608 in year

2016 respectively.

ACCOUNTING AND FINANCE

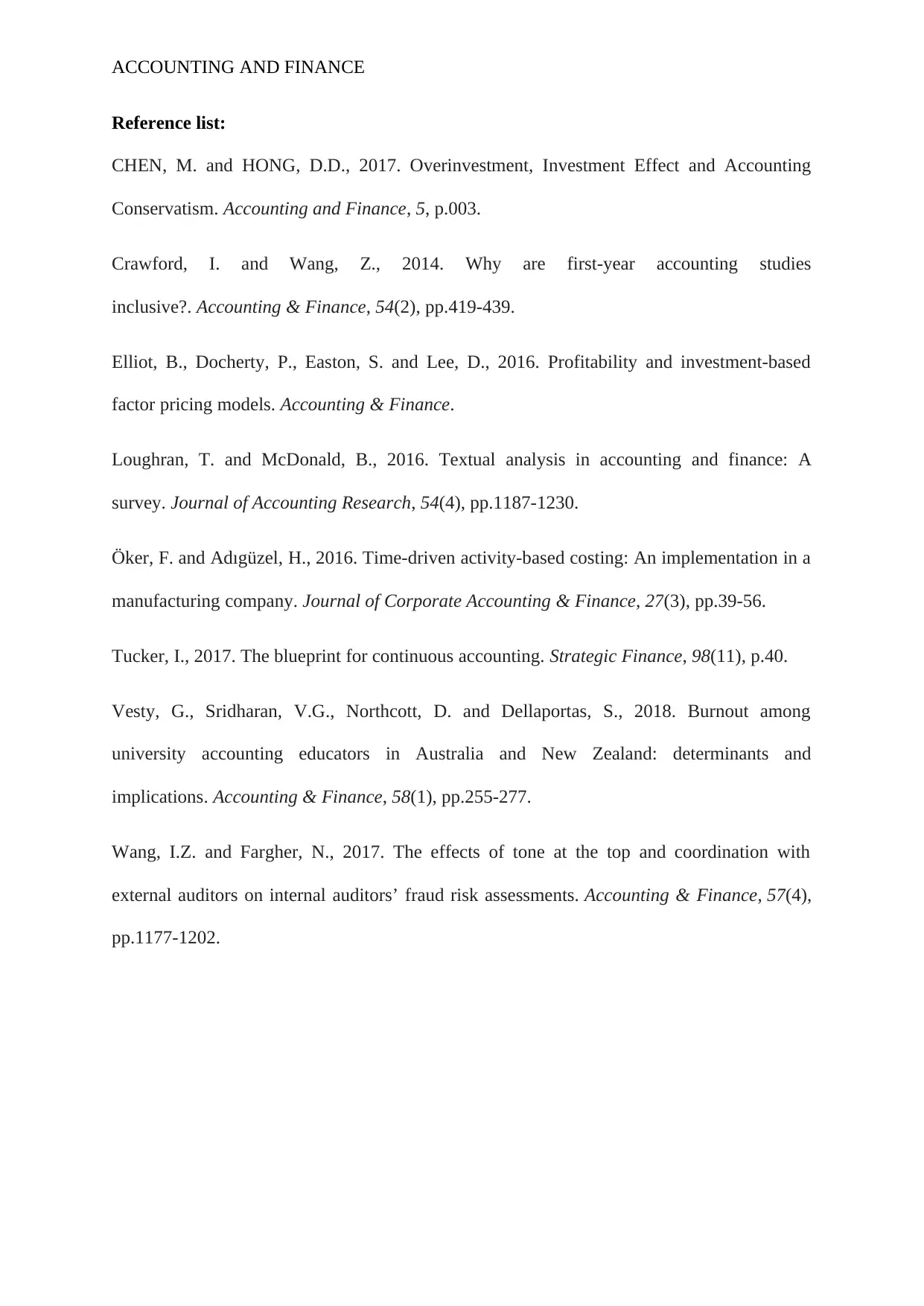

Evaluating the firm’s success in generating wealth to their shareholders:

Although, there has been increase in net operating profit after tax to $ 49152 in year

2017 compared to $ 44313 in year 2015. The total cost of capital has also increased with non

economic value being added. This depicts that wealth of shareholder has not increased.

Recommendations for adopting alternative capital structure:

It is required on part of management of ARB limited to lower the cost of capital so as

to lower the risks associated with operation of company.

The capital structure of company should involve both debt as well as equity for

lowering the total equity costs and taking the advantage of tax deduction.

ARB limited should have appropriate mixture of debt capital and equity into their

capital structure.

Conclusion:

Analysis of the financial performance of ARB limited using capital budgeting tools

and ratio analysis tool, it can be inferred that capital structure should also include debt along

with equity capital. In addition to this, there should be reduction of cost of capital for

reducing the risk level associated with the operations.

Evaluating the firm’s success in generating wealth to their shareholders:

Although, there has been increase in net operating profit after tax to $ 49152 in year

2017 compared to $ 44313 in year 2015. The total cost of capital has also increased with non

economic value being added. This depicts that wealth of shareholder has not increased.

Recommendations for adopting alternative capital structure:

It is required on part of management of ARB limited to lower the cost of capital so as

to lower the risks associated with operation of company.

The capital structure of company should involve both debt as well as equity for

lowering the total equity costs and taking the advantage of tax deduction.

ARB limited should have appropriate mixture of debt capital and equity into their

capital structure.

Conclusion:

Analysis of the financial performance of ARB limited using capital budgeting tools

and ratio analysis tool, it can be inferred that capital structure should also include debt along

with equity capital. In addition to this, there should be reduction of cost of capital for

reducing the risk level associated with the operations.

ACCOUNTING AND FINANCE

Reference list:

CHEN, M. and HONG, D.D., 2017. Overinvestment, Investment Effect and Accounting

Conservatism. Accounting and Finance, 5, p.003.

Crawford, I. and Wang, Z., 2014. Why are first‐year accounting studies

inclusive?. Accounting & Finance, 54(2), pp.419-439.

Elliot, B., Docherty, P., Easton, S. and Lee, D., 2016. Profitability and investment‐based

factor pricing models. Accounting & Finance.

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), pp.1187-1230.

Öker, F. and Adıgüzel, H., 2016. Time‐driven activity‐based costing: An implementation in a

manufacturing company. Journal of Corporate Accounting & Finance, 27(3), pp.39-56.

Tucker, I., 2017. The blueprint for continuous accounting. Strategic Finance, 98(11), p.40.

Vesty, G., Sridharan, V.G., Northcott, D. and Dellaportas, S., 2018. Burnout among

university accounting educators in Australia and New Zealand: determinants and

implications. Accounting & Finance, 58(1), pp.255-277.

Wang, I.Z. and Fargher, N., 2017. The effects of tone at the top and coordination with

external auditors on internal auditors’ fraud risk assessments. Accounting & Finance, 57(4),

pp.1177-1202.

Reference list:

CHEN, M. and HONG, D.D., 2017. Overinvestment, Investment Effect and Accounting

Conservatism. Accounting and Finance, 5, p.003.

Crawford, I. and Wang, Z., 2014. Why are first‐year accounting studies

inclusive?. Accounting & Finance, 54(2), pp.419-439.

Elliot, B., Docherty, P., Easton, S. and Lee, D., 2016. Profitability and investment‐based

factor pricing models. Accounting & Finance.

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), pp.1187-1230.

Öker, F. and Adıgüzel, H., 2016. Time‐driven activity‐based costing: An implementation in a

manufacturing company. Journal of Corporate Accounting & Finance, 27(3), pp.39-56.

Tucker, I., 2017. The blueprint for continuous accounting. Strategic Finance, 98(11), p.40.

Vesty, G., Sridharan, V.G., Northcott, D. and Dellaportas, S., 2018. Burnout among

university accounting educators in Australia and New Zealand: determinants and

implications. Accounting & Finance, 58(1), pp.255-277.

Wang, I.Z. and Fargher, N., 2017. The effects of tone at the top and coordination with

external auditors on internal auditors’ fraud risk assessments. Accounting & Finance, 57(4),

pp.1177-1202.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.