Comprehensive Ratio Analysis of GlaxoSmithKline Plc (GSK) Finance

VerifiedAdded on 2023/04/20

|20

|1782

|184

Report

AI Summary

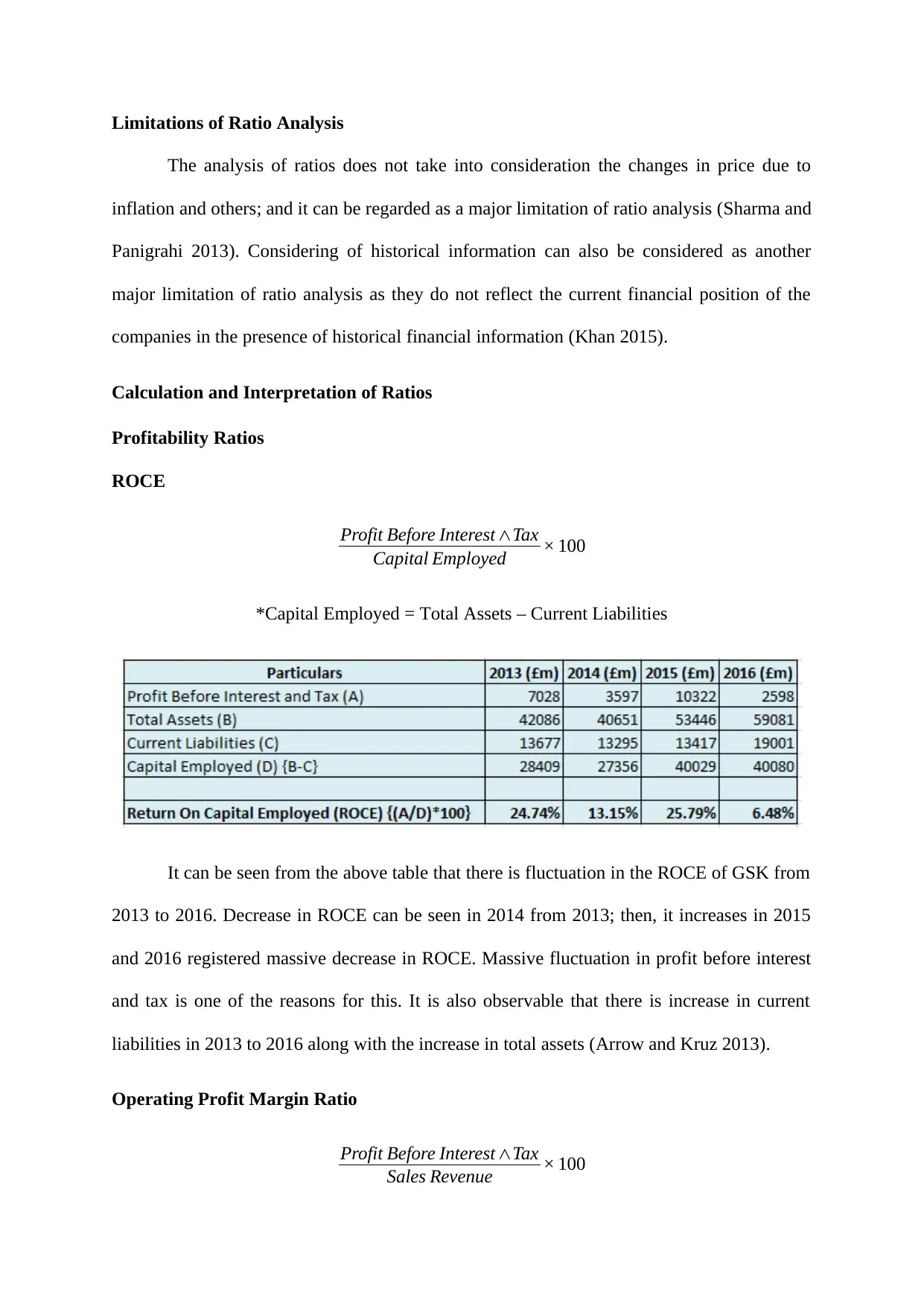

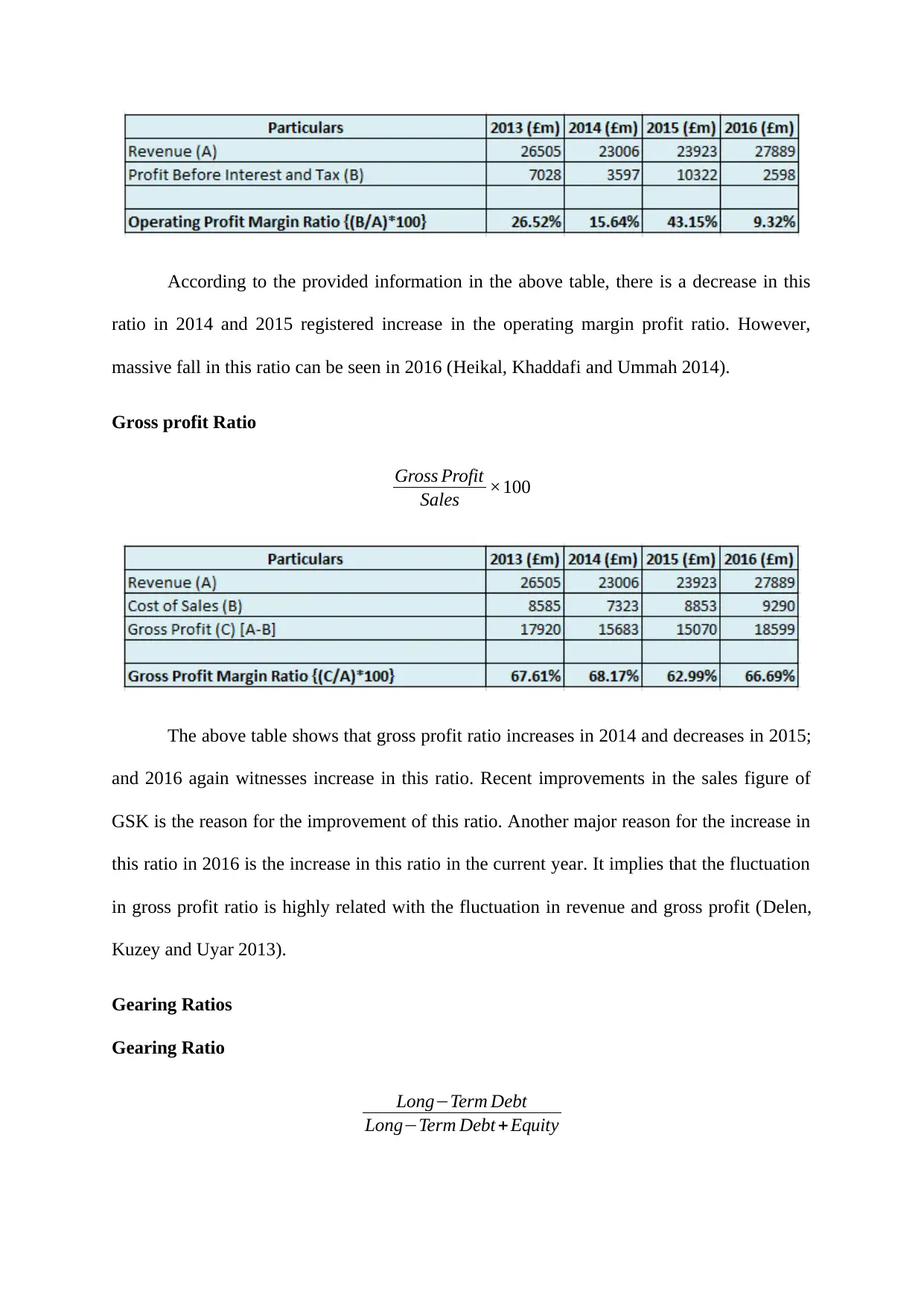

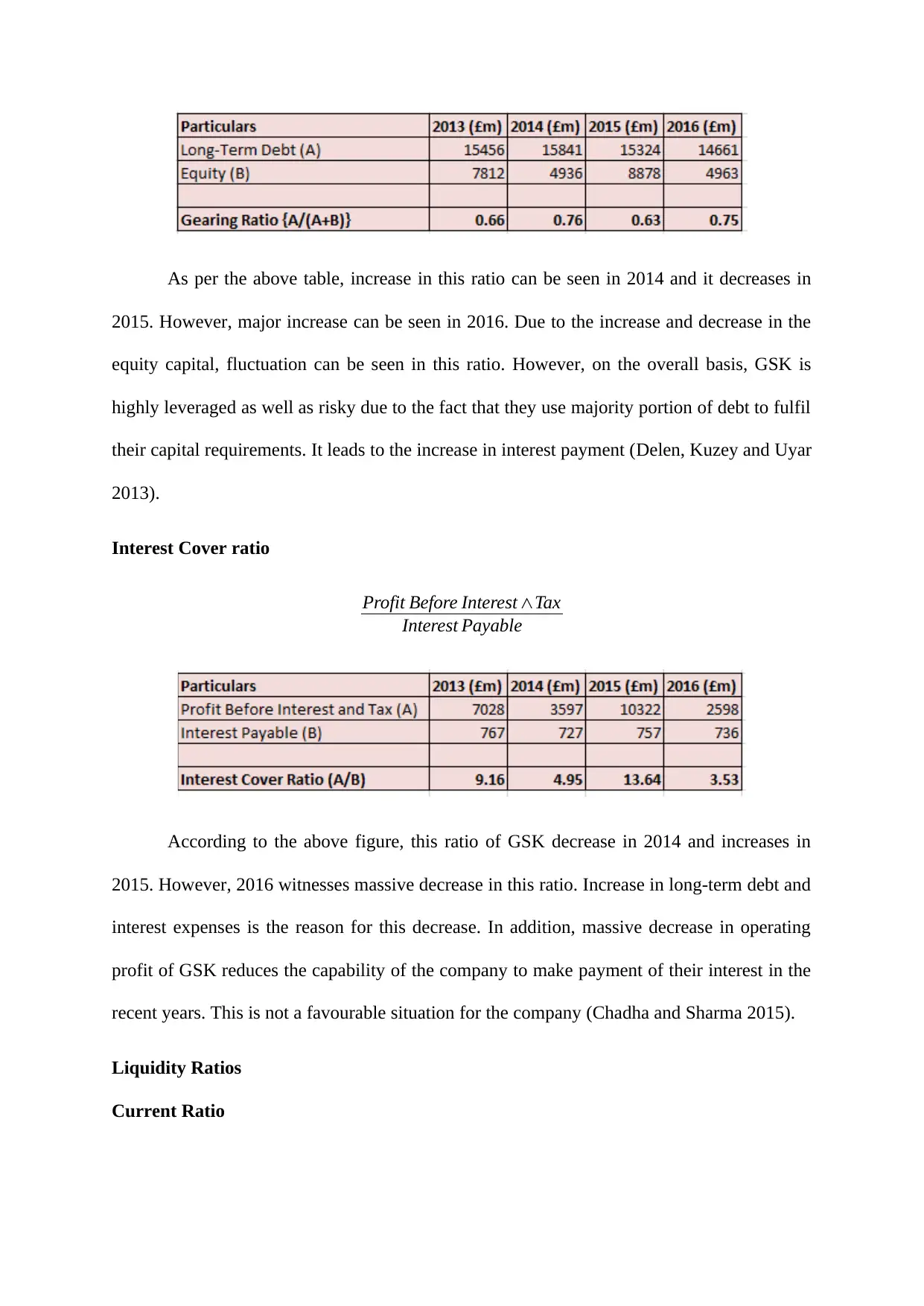

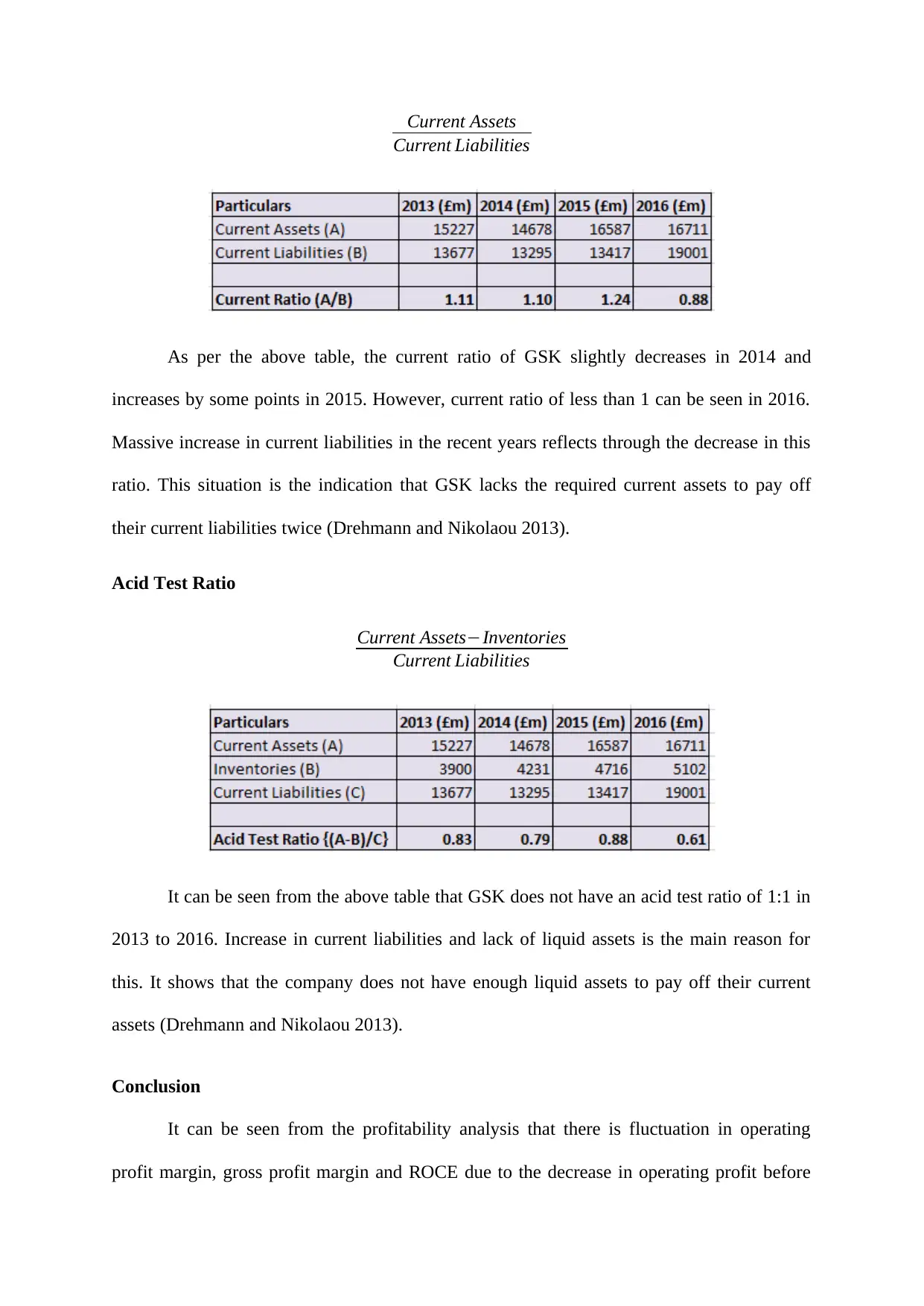

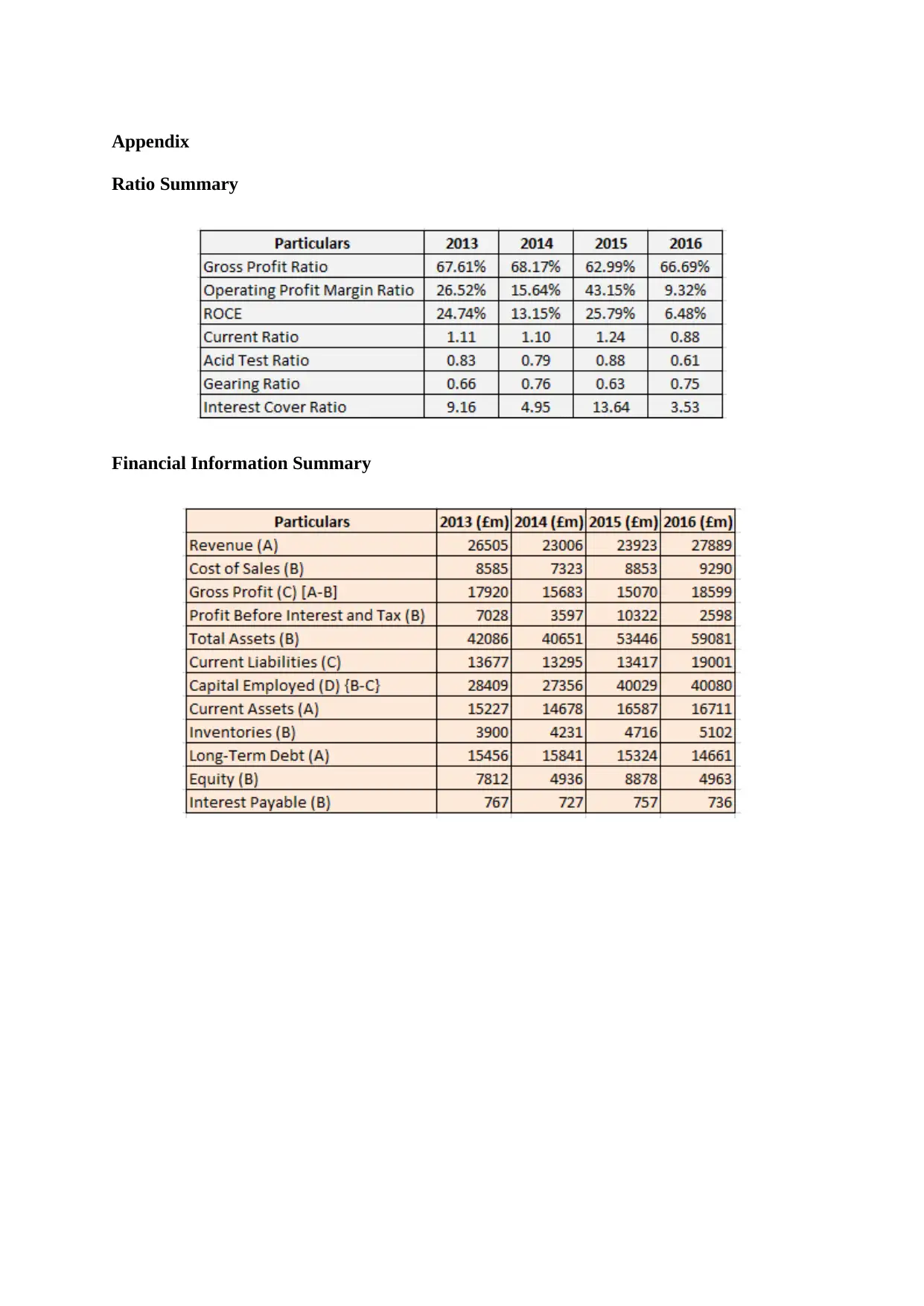

This report provides a financial analysis of GlaxoSmithKline Plc (GSK) using ratio analysis. It begins with a company introduction, followed by a literature review discussing the benefits and limitations of ratio analysis. The report then calculates and interprets key financial ratios, including profitability ratios (ROCE, operating profit margin, gross profit ratio), gearing ratios (gearing ratio, interest cover ratio), and liquidity ratios (current ratio, acid test ratio) for the years 2013-2016. The analysis reveals fluctuations in profitability, a reliance on debt financing, and potential liquidity issues for GSK. The report concludes with a summary of findings and includes references and an appendix with supporting financial information.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.