Capital Budgeting Analysis Report: Accounting and Finance Module

VerifiedAdded on 2023/01/04

|11

|1377

|80

Report

AI Summary

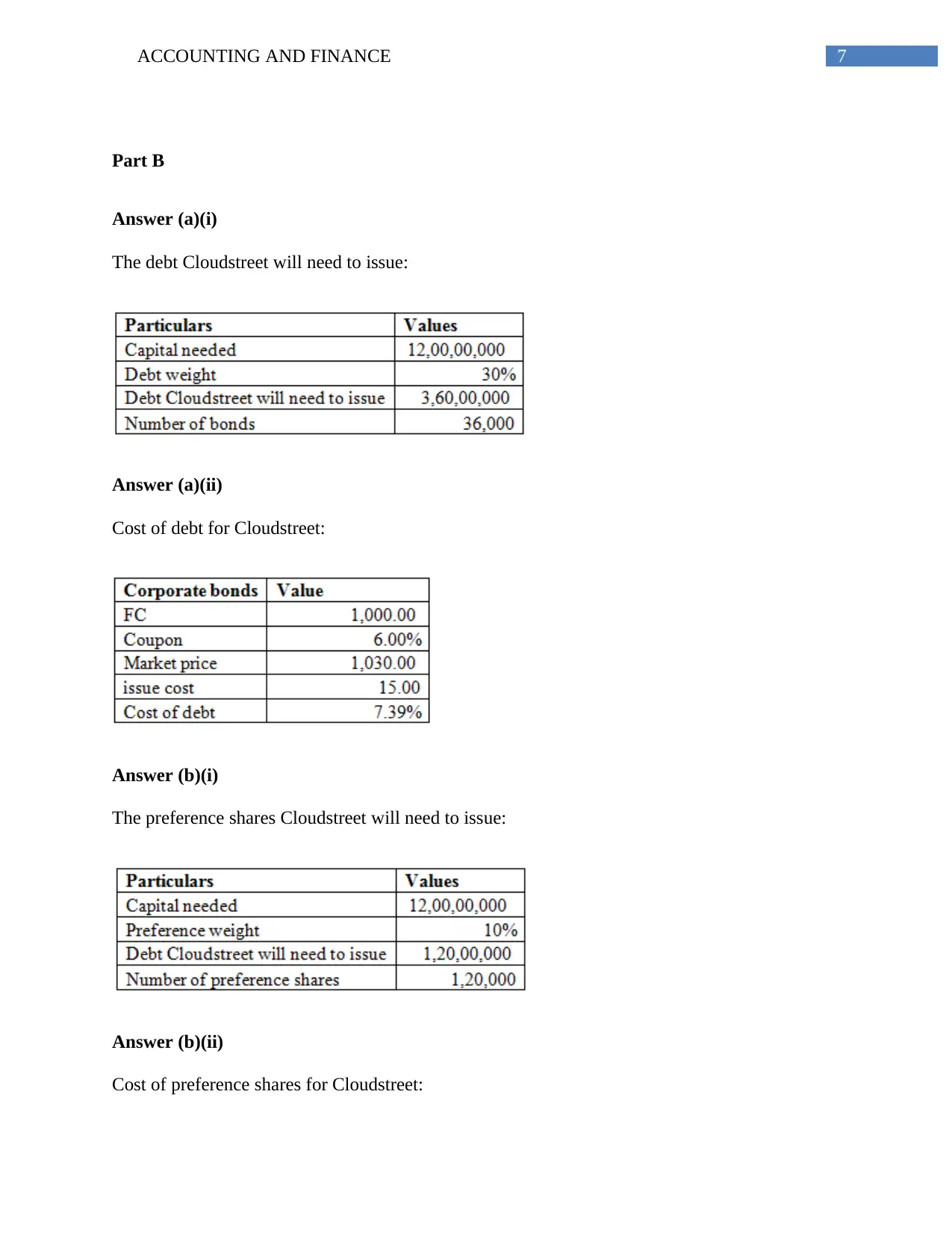

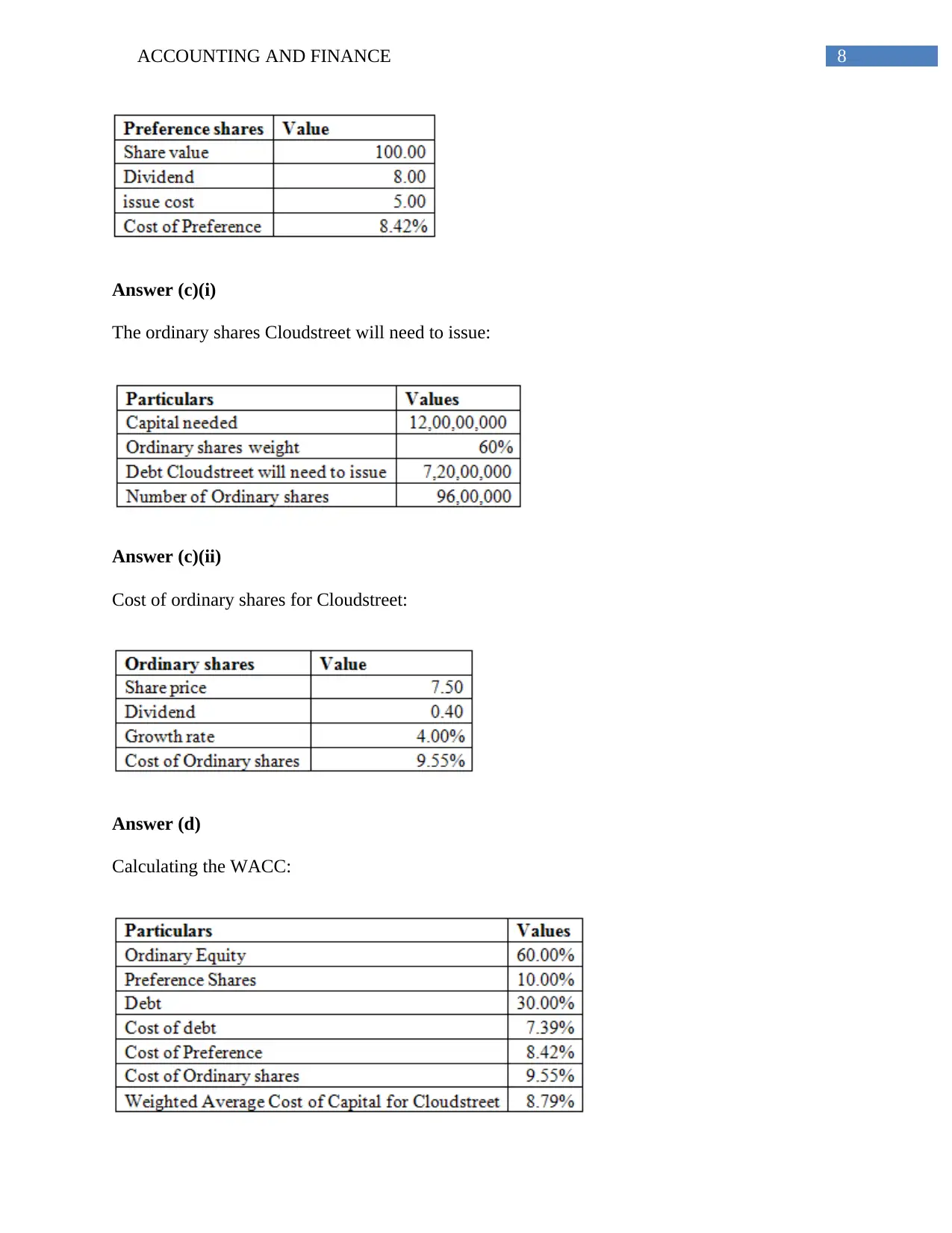

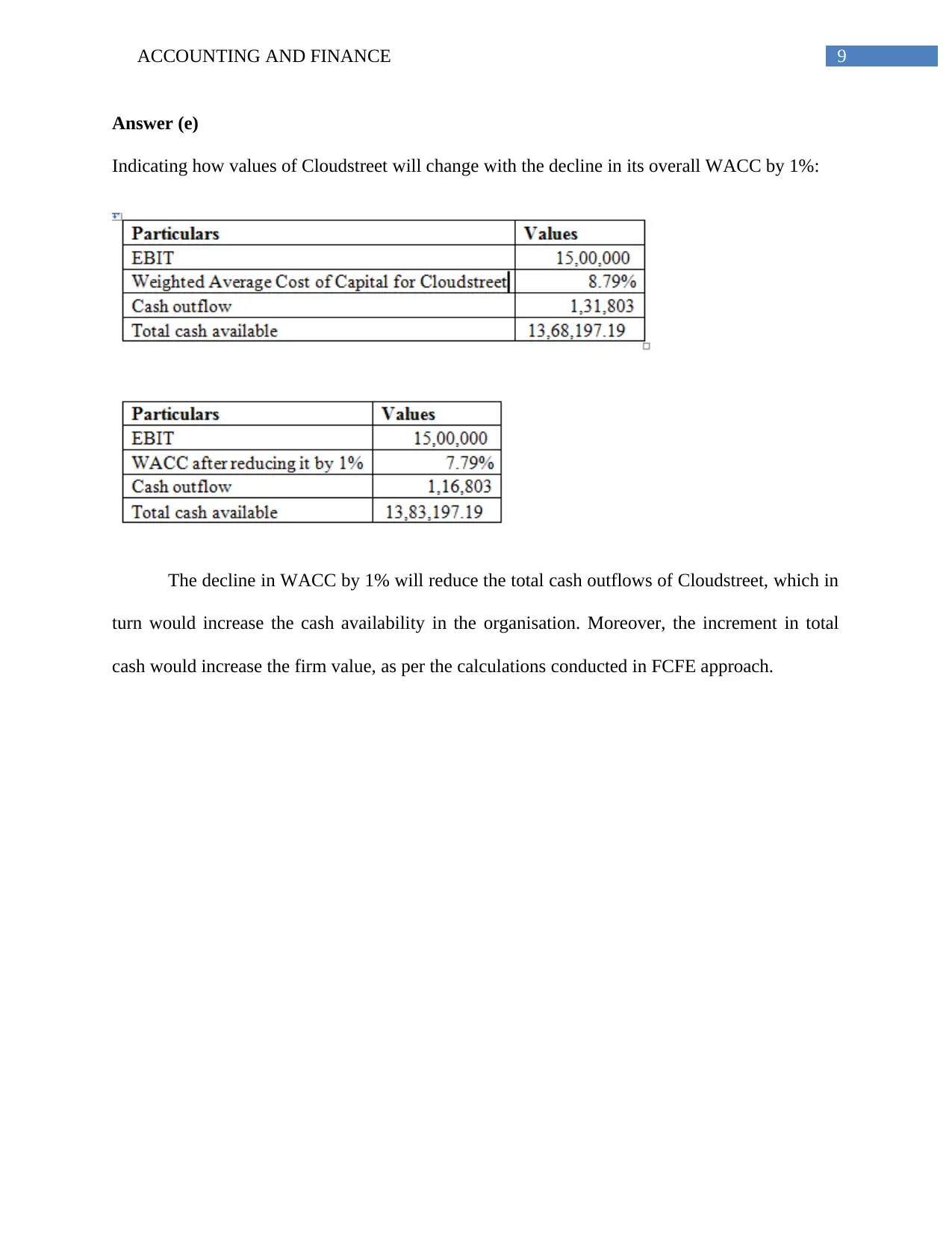

This report presents a comprehensive financial analysis of capital budgeting techniques and the Weighted Average Cost of Capital (WACC) for a hypothetical scenario involving Mars Australia and New Zealand. Part A focuses on evaluating a factory refurbishment and technology upgrade project using methods like Net Present Value (NPV), Internal Rate of Return (IRR), Profitability Index (PI), and payback period to determine project feasibility. The report concludes with a recommendation against the project based on the negative NPV and other unfavorable metrics. Part B shifts focus to WACC calculations, exploring the cost of debt, preference shares, and ordinary shares. It includes the calculation of WACC and assesses how changes in WACC impact firm value. The report provides detailed calculations and explanations, offering insights into financial decision-making and investment analysis.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.