Finance Report: D1 and D2 Profitability and ROI Analysis

VerifiedAdded on 2023/01/10

|5

|408

|21

Report

AI Summary

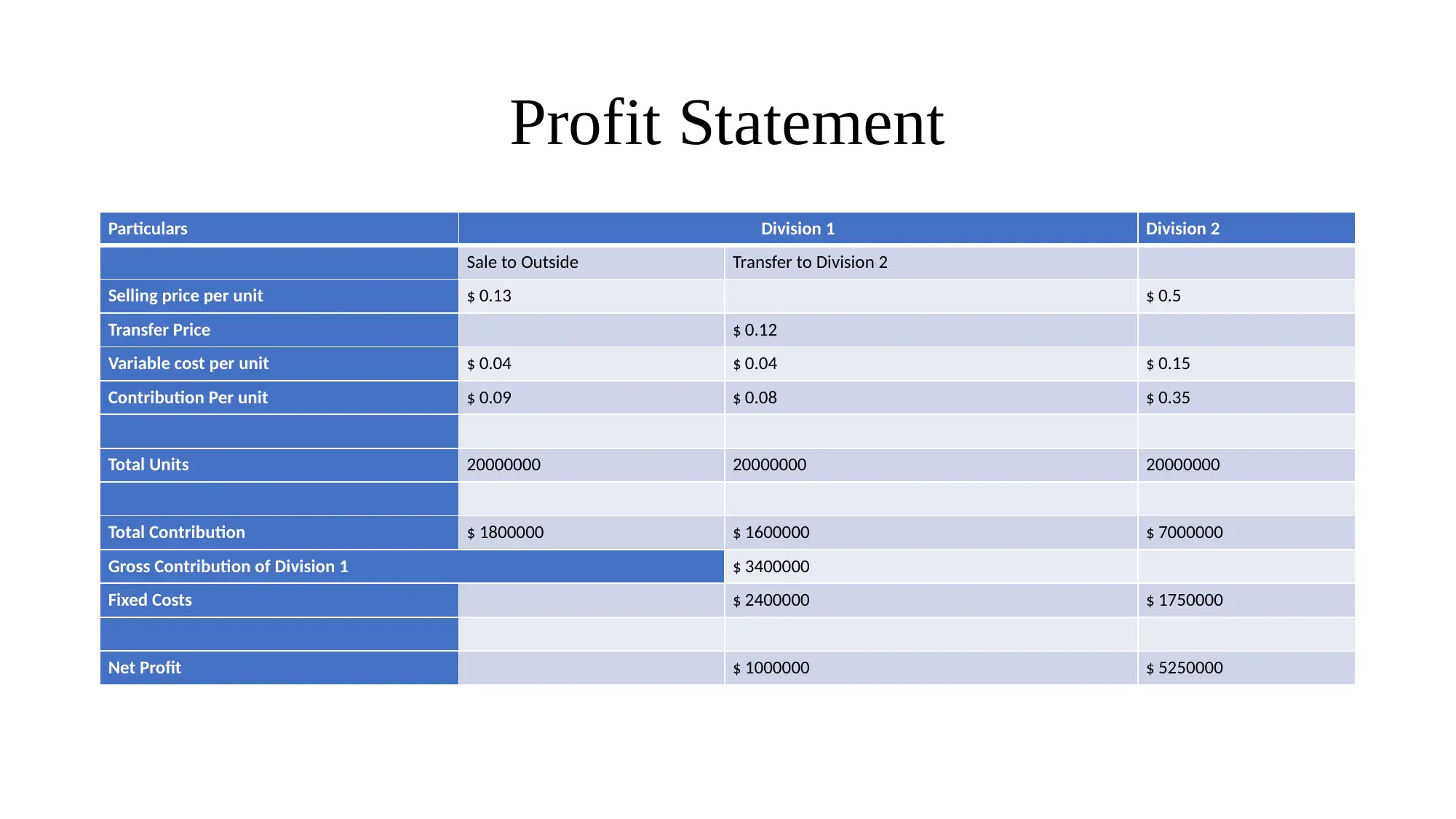

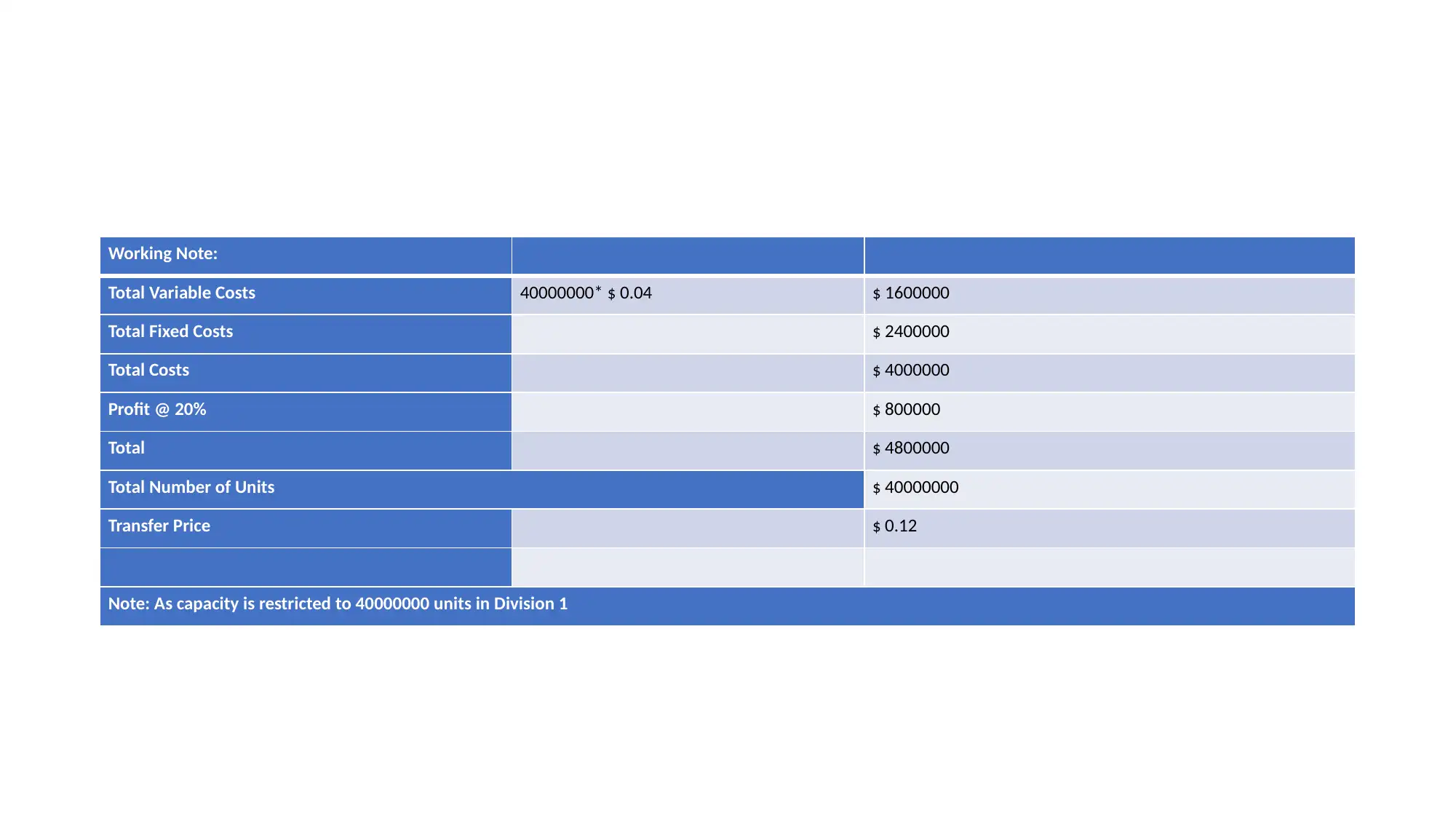

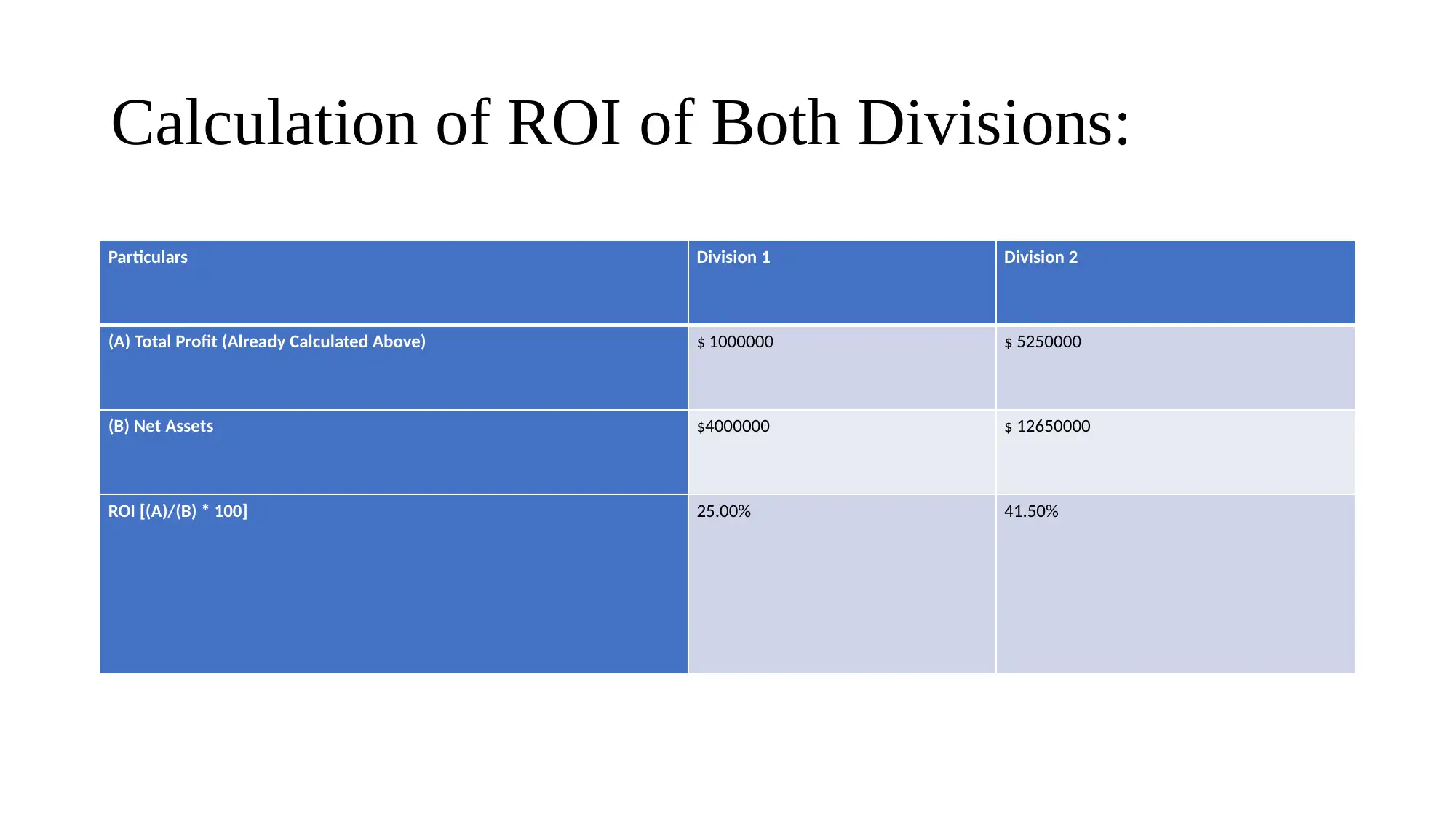

This report presents a detailed analysis of the profit statements for Divisions D1 and D2, focusing on their profitability and Return on Investment (ROI). The analysis includes calculations of contribution per unit, total contribution, and net profit for each division. It also examines the impact of transfer pricing on divisional performance, highlighting the potential conflicts that can arise when transfer prices are set below market value. The report provides a working note detailing the total variable costs, fixed costs, and profit calculations. Furthermore, it assesses the ROI of both divisions, comparing them against a market ROI benchmark. The commentary emphasizes the importance of considering capacity constraints, fairness in transfer pricing, and the potential for capacity expansion in the more profitable division. This analysis is based on the provided budget information, including selling prices, variable costs, fixed costs, and net assets for both divisions, and aims to offer insights for strategic decision-making. The document is a solution to an accounting and finance assignment, offering a comprehensive overview of the financial performance of the two divisions and is available on Desklib for students to use for study purposes.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.