Accounting and Finance for Decision Making: RED OIL Co. Analysis

VerifiedAdded on 2022/10/14

|9

|1774

|430

Report

AI Summary

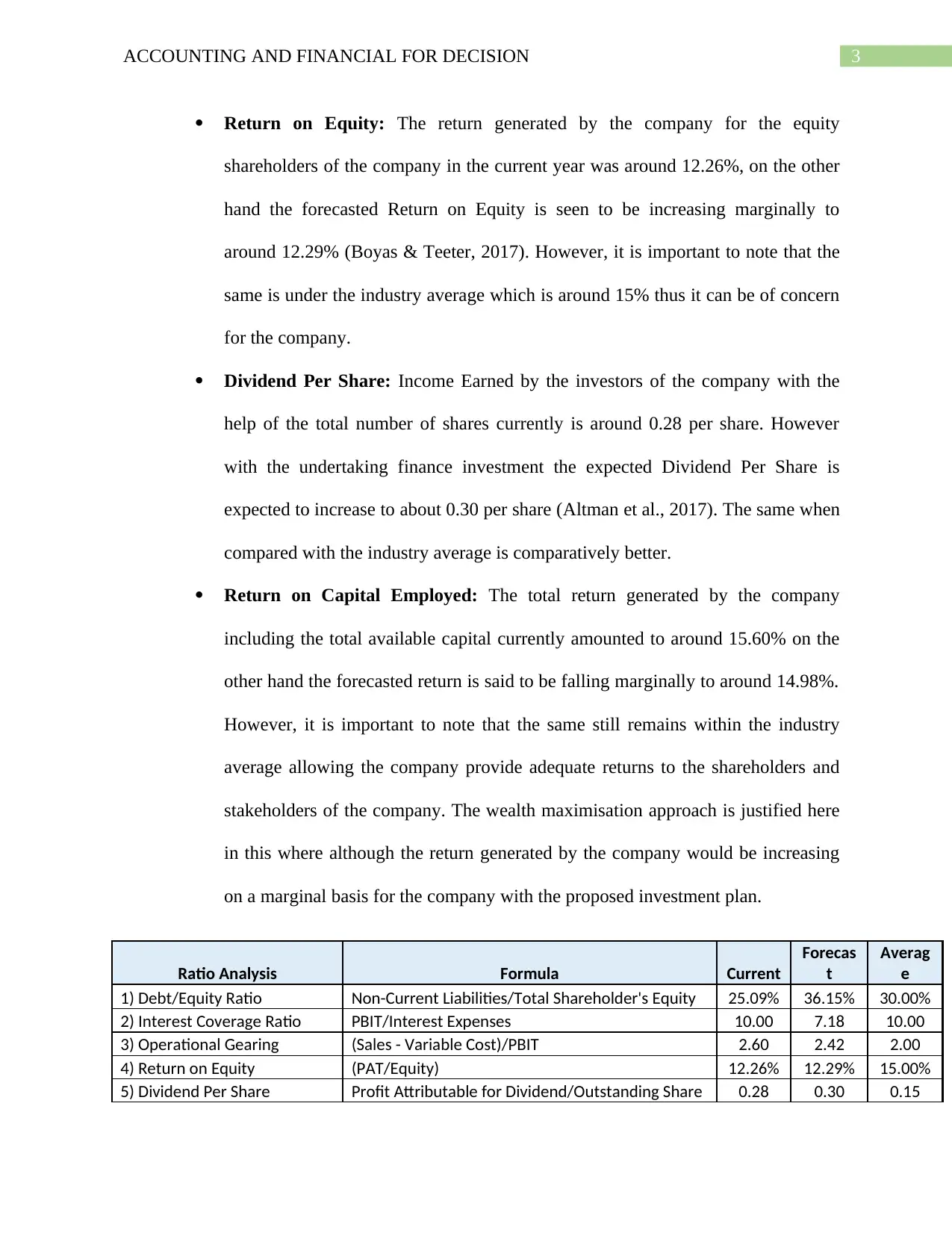

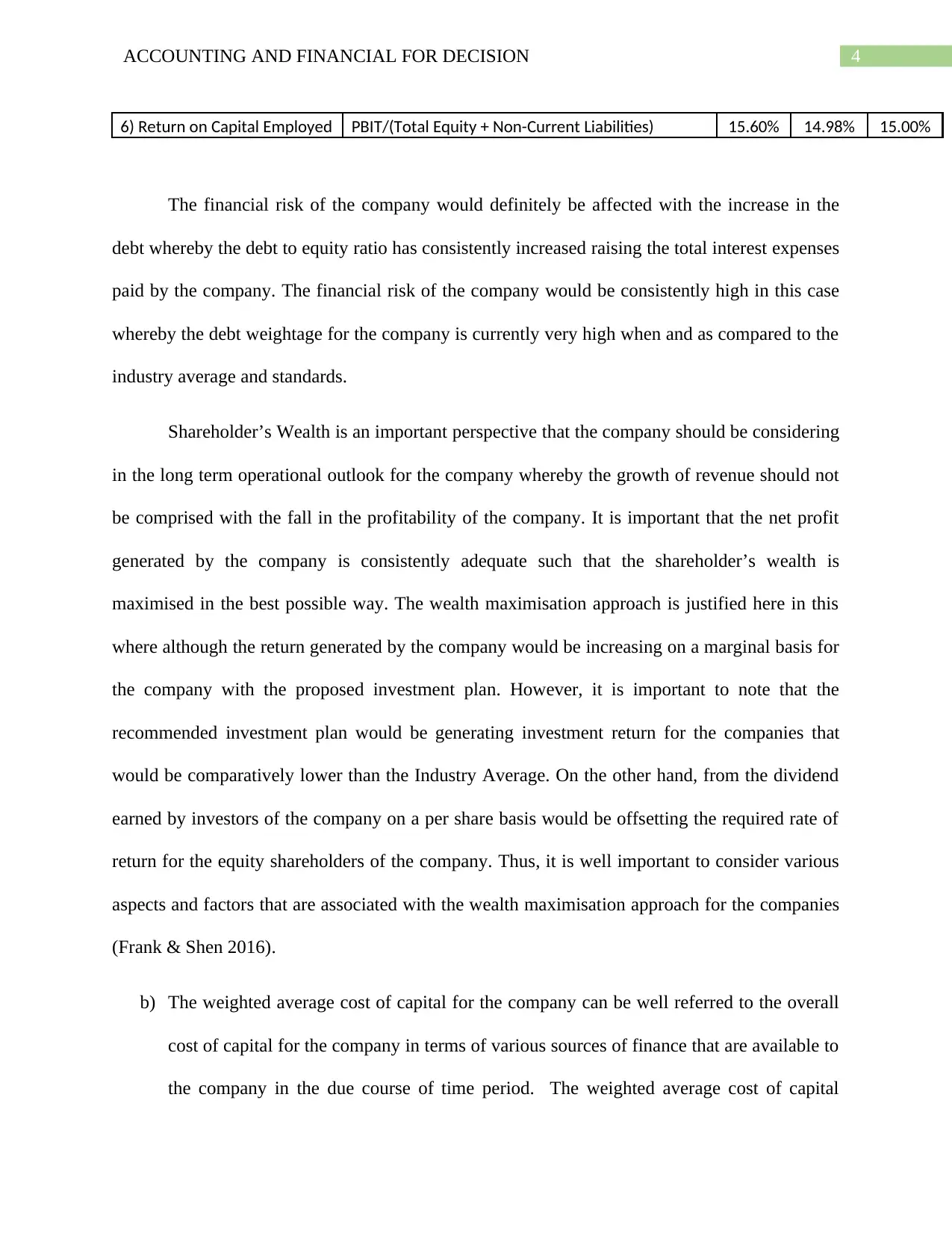

This report presents a financial analysis of RED OIL Co., focusing on the impact of a proposed $20 million financing on the company's expansion plans. The analysis utilizes key financial ratios, including debt-to-equity, interest coverage, operational gearing, return on equity, dividend per share, and return on capital employed, to assess the financial implications of the expansion. The report compares the company's current financial standing with projected figures, highlighting changes in financial risk and shareholder wealth. Furthermore, the report discusses the weighted average cost of capital (WACC) and its application in evaluating investment projects, emphasizing its role in assessing financial sustainability and making informed investment decisions. The analysis considers both the limitations and applications of WACC in different scenarios, such as projects with similar and varying risk profiles. The report concludes by emphasizing the importance of considering shareholder wealth maximization in the long-term operational outlook of the company.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.