Comprehensive Financial Management Report: PARISS Plc and Subsidiaries

VerifiedAdded on 2020/05/28

|19

|3558

|41

Report

AI Summary

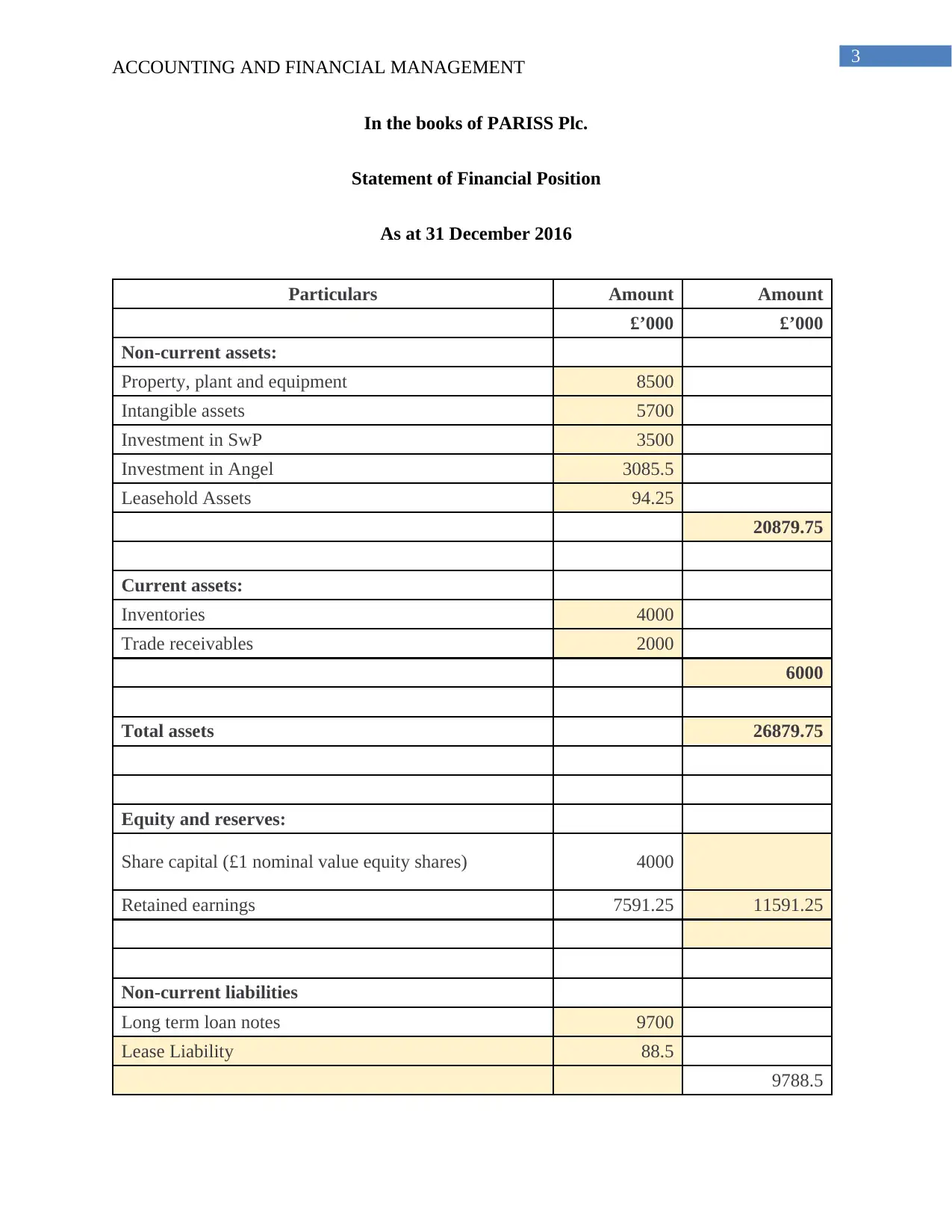

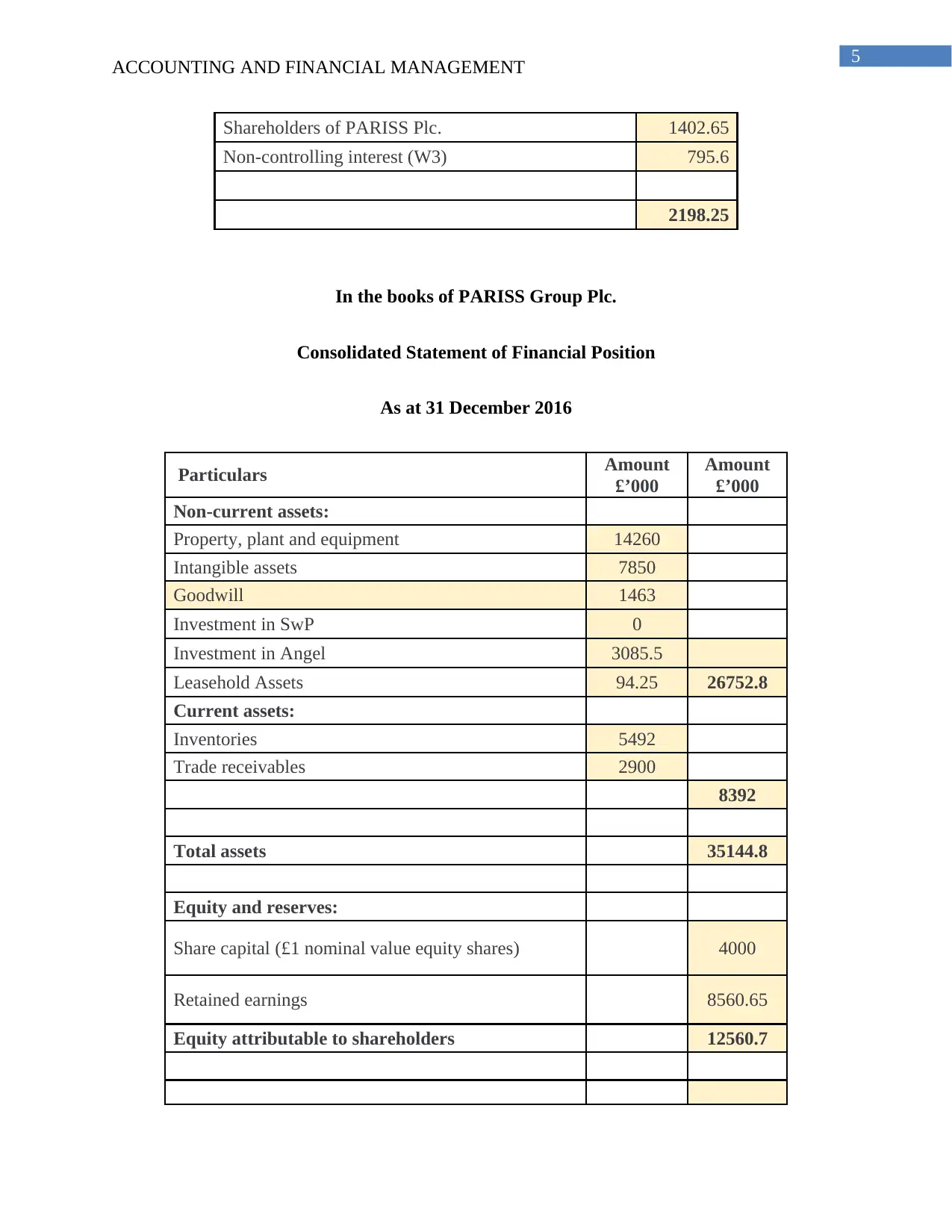

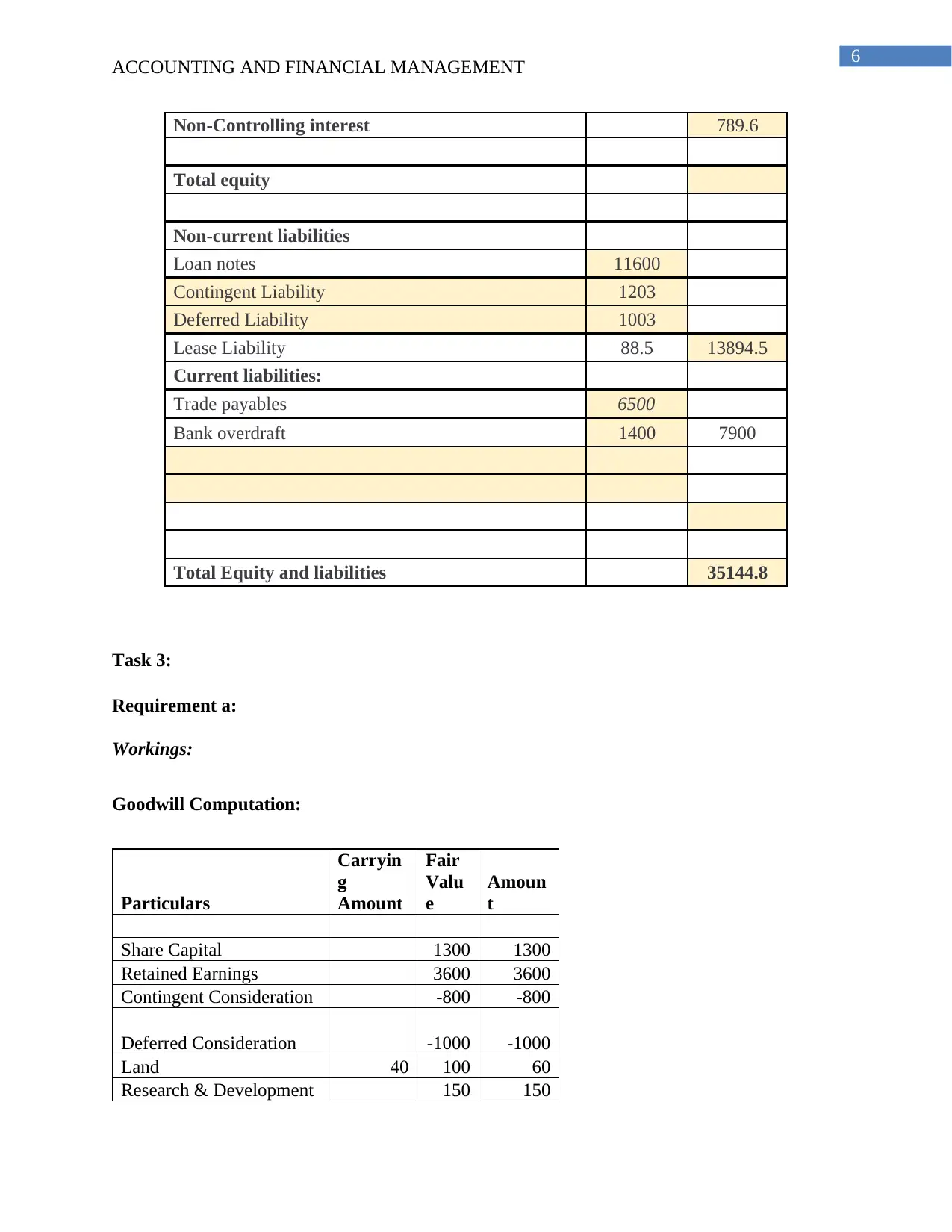

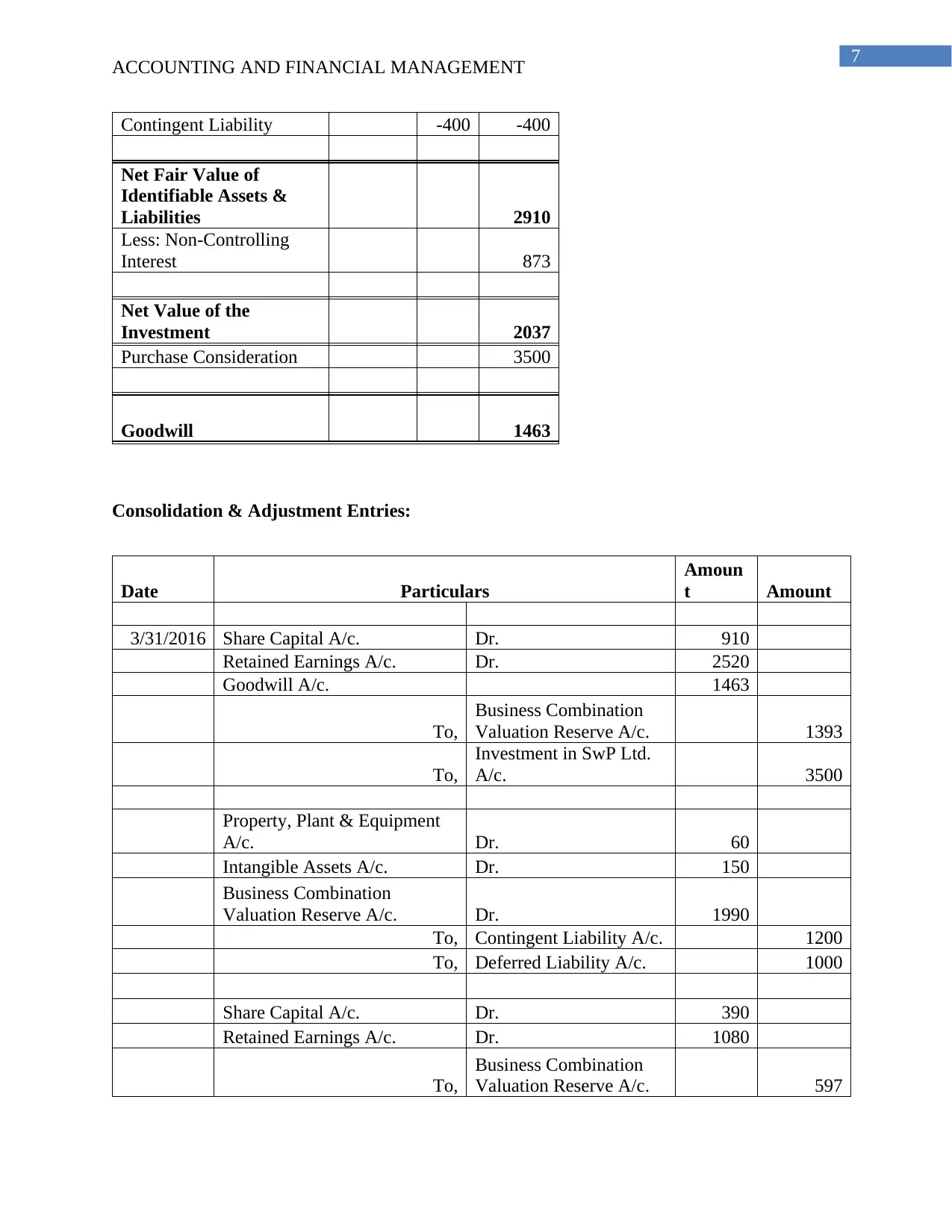

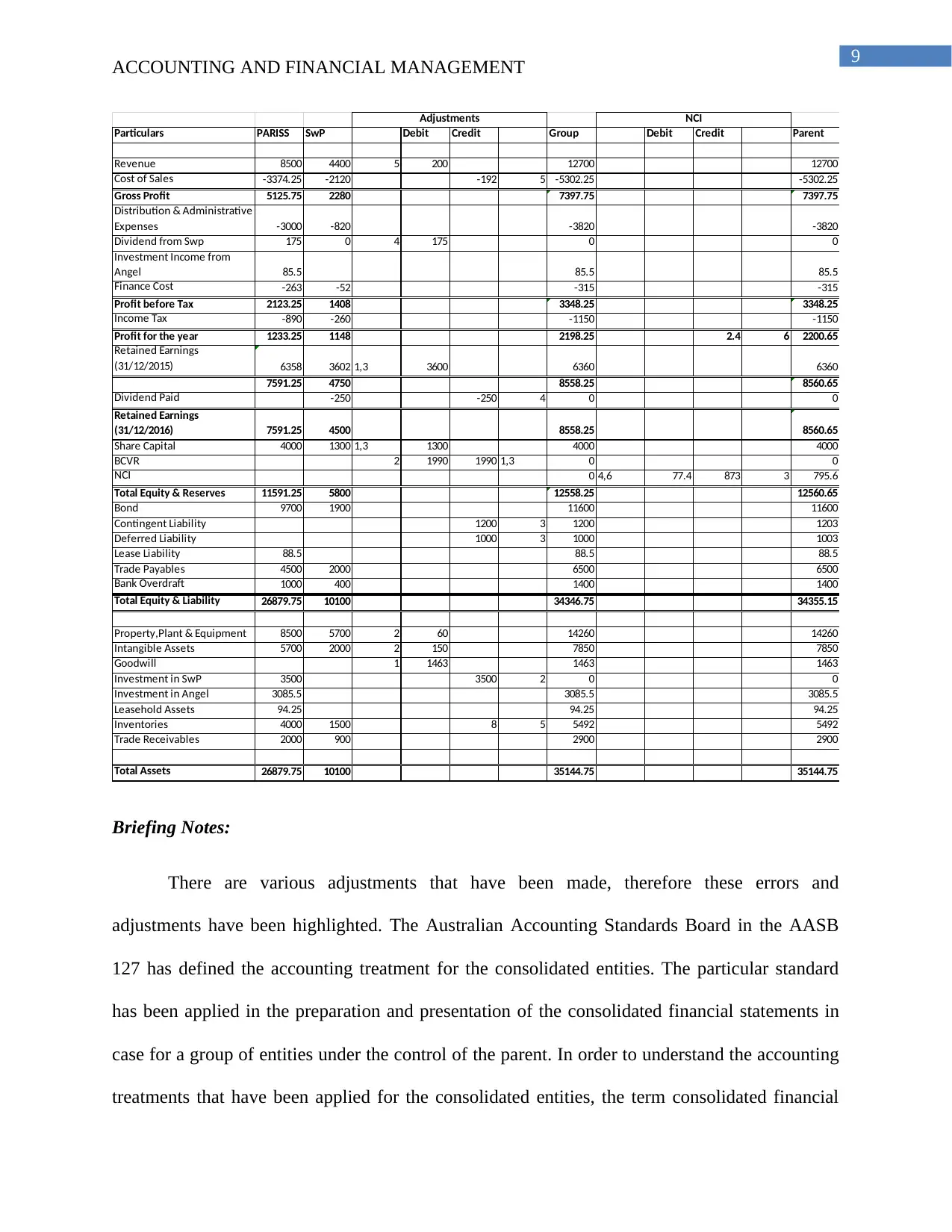

This report presents a comprehensive analysis of the financial statements of PARISS Plc, including the Statement of Profit or Loss and the Statement of Financial Position. The report covers the consolidation of subsidiaries, SwP and Angel, with detailed workings for goodwill computation and consolidation entries. It highlights adjustments made to correct errors in lease expenses and the application of accounting standards like AASB 127 and AASB 117. The report also evaluates the importance of human capital in financial reporting, noting that neither SwP nor Angel Plc has disclosed the value of human capital, and discusses the impact of employee performance on share value. The analysis emphasizes the importance of accurate financial statements for PARISS Plc's sustainability and competitive advantage, as well as the need to consider human capital in financial reporting for a complete picture of a company's value.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.