Financial Performance Report: Britvic plc and Barr Group plc Analysis

VerifiedAdded on 2020/07/22

|17

|5120

|32

Report

AI Summary

This report presents a comprehensive financial analysis of Britvic plc and Barr Group plc, focusing on key performance indicators to aid investment decisions. It begins with an executive summary and an introduction outlining the report's objectives. Part A delves into the price-earnings ratio, its significance, and its application in valuing companies, including discussions on trailing and forward P/E ratios, and factors influencing P/E ratios such as previous performance, growth potential, risk, corporate governance, dividend pay-out, and economic cycles. The report then describes how to use P/E multiples to assess a company's value and provides a comparative analysis of Britvic plc and AG Barr plc within the beverages and non-alcoholic industry. It further explores various investment ratios, including price-to-book value, debt-equity ratio, operating profit margin, and earnings per share, emphasizing their importance in evaluating financial health and making informed investment decisions. Part B then examines the cash inflows and outflows, along with the calculation of the payback period, net present value, and internal rate of return for Grahams Inc, providing a practical application of financial analysis techniques. The report concludes with a summary of findings and references used.

Accounting and Financial

management

management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................1

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

PART B............................................................................................................................................6

Performance of two company's ..................................................................................................6

CASE B1: Grahams Inc:...........................................................................................................12

A. Cash inflows and outflows:..................................................................................................12

B. Calculate Payback period, Net present value and internal rate of return:............................12

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................14

EXECUTIVE SUMMARY.............................................................................................................1

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

PART B............................................................................................................................................6

Performance of two company's ..................................................................................................6

CASE B1: Grahams Inc:...........................................................................................................12

A. Cash inflows and outflows:..................................................................................................12

B. Calculate Payback period, Net present value and internal rate of return:............................12

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................14

EXECUTIVE SUMMARY

Analysis of the financial activities in a firm makes a perfect interpretation so that the

investors can take their decisions about the investment. This report is divided into two parts. One

part is mandatory and other part is totally related to the cash inflows and outflows and net

present value of the firm. This report likewise covers various financial ratios which are

calculated on the basis of the financial performance of the both Britvic plc and Barr group plc.

Their P/E ratio is also calculated under this.

INTRODUCTION

This report is totally based no the financial performance of the Britvic plc and Barr group

plc and their main aim is to make certain decisions so that they can come to final conclusion and

able to make decisions in an effective manner. Under this report, price earnings and other

investment ratios are used so that strategy director could build their own decisions in an effective

manner. In addition to this, they are also planning to merge or takeover with their competitors

after analysing their competitors’ performance.

PART A

Explanation of price earnings ratio: Price earnings ratio is used for valuing of stock price. This

is mostly applied for valuing stocks. This is complicated one for evaluating the stock price of a

company. This could be highly informative in few situations, while at the other times, this

interpret nothing. As an outcome, investors usually misinterpret this term and place more value

in it than is warranted (Ahmed and Duellman, 2013). Price to earnings ratio is applied to

interpret how expensive or cheap the stock of a share. This is a tool which can be used to forecast

an adequate value of the stock value. For calculating this,, the current stock prices of a

company’s share is adopted and divide it to its earning per share. However price to earning can

be calculated by way of under mentioned method:

Many of the time, P/E ratio is measured by using earning per share from the previous

four quarters. It is also recognised as the trailing P/E. although, such method for

calculating P/E, does not render the perfect reflection of the organisation growth

potential.

1

Analysis of the financial activities in a firm makes a perfect interpretation so that the

investors can take their decisions about the investment. This report is divided into two parts. One

part is mandatory and other part is totally related to the cash inflows and outflows and net

present value of the firm. This report likewise covers various financial ratios which are

calculated on the basis of the financial performance of the both Britvic plc and Barr group plc.

Their P/E ratio is also calculated under this.

INTRODUCTION

This report is totally based no the financial performance of the Britvic plc and Barr group

plc and their main aim is to make certain decisions so that they can come to final conclusion and

able to make decisions in an effective manner. Under this report, price earnings and other

investment ratios are used so that strategy director could build their own decisions in an effective

manner. In addition to this, they are also planning to merge or takeover with their competitors

after analysing their competitors’ performance.

PART A

Explanation of price earnings ratio: Price earnings ratio is used for valuing of stock price. This

is mostly applied for valuing stocks. This is complicated one for evaluating the stock price of a

company. This could be highly informative in few situations, while at the other times, this

interpret nothing. As an outcome, investors usually misinterpret this term and place more value

in it than is warranted (Ahmed and Duellman, 2013). Price to earnings ratio is applied to

interpret how expensive or cheap the stock of a share. This is a tool which can be used to forecast

an adequate value of the stock value. For calculating this,, the current stock prices of a

company’s share is adopted and divide it to its earning per share. However price to earning can

be calculated by way of under mentioned method:

Many of the time, P/E ratio is measured by using earning per share from the previous

four quarters. It is also recognised as the trailing P/E. although, such method for

calculating P/E, does not render the perfect reflection of the organisation growth

potential.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Price earnings ratio is also calculated by implementing EPS for the subsequent four

quarters. This is also recognised as the forward leading PE. This method demonstrates

effective growth potential.

Trailing P/E depends on the actual earnings and, henceforth this is more effective and adequate.

Irrespective of fixed return, share price of the company will fluctuate. As an outcome forward

P/E helps to investors for evaluating performance of a company.

IMPORTANCE OF P/E RATIO:

P/E ratio helps the company to evaluate the previous performance and also tells how to

growth in future with the help of their previous performance. Usually, it takes into the

account of following factors:

1. Previous Performance: If organizations have sound track record, then it would have

more price- earnings ratio as compared to those companies how have erratic performance

(Jacobs, 2012).

2. Potential Growth: It is crucial component incorporate in to the price-earnings ratio. In

an industry, those companies which are having higher P/E ratio reflect high growth

potential in the market.

3. Risk (Leverage): P/E ratio is more reliable on the capital structure of the company.

Leverage means debt taken on by the company. It effects on the earnings and share price

of the company in different ways, that’s includes the leveraging of earnings growth rate,

effects of tax on the company and have bankruptcy risk, and this could also impact the

financial performance of the company. Henceforth, lower leverage reflects the higher P/E

ratio of an organization.as an outcome, more capital intensive sector gets lower price-

earnings than low capital intensive sector.

4. Corporate Governance: An organization which are having sound or effective corporate

governance policy they also have higher price-earnings ratio for instance, Infosys has

historically great corporate governance that’s why it have higher P/E than its peer group.

5. Dividend Pay-out: Usually, high and constant dividend paying organization have higher

P/E ratio as it demonstrate the basic strength of the organization and firm commitment to

reward its shareholder (Carraher and Van Auken, 2013).

2

quarters. This is also recognised as the forward leading PE. This method demonstrates

effective growth potential.

Trailing P/E depends on the actual earnings and, henceforth this is more effective and adequate.

Irrespective of fixed return, share price of the company will fluctuate. As an outcome forward

P/E helps to investors for evaluating performance of a company.

IMPORTANCE OF P/E RATIO:

P/E ratio helps the company to evaluate the previous performance and also tells how to

growth in future with the help of their previous performance. Usually, it takes into the

account of following factors:

1. Previous Performance: If organizations have sound track record, then it would have

more price- earnings ratio as compared to those companies how have erratic performance

(Jacobs, 2012).

2. Potential Growth: It is crucial component incorporate in to the price-earnings ratio. In

an industry, those companies which are having higher P/E ratio reflect high growth

potential in the market.

3. Risk (Leverage): P/E ratio is more reliable on the capital structure of the company.

Leverage means debt taken on by the company. It effects on the earnings and share price

of the company in different ways, that’s includes the leveraging of earnings growth rate,

effects of tax on the company and have bankruptcy risk, and this could also impact the

financial performance of the company. Henceforth, lower leverage reflects the higher P/E

ratio of an organization.as an outcome, more capital intensive sector gets lower price-

earnings than low capital intensive sector.

4. Corporate Governance: An organization which are having sound or effective corporate

governance policy they also have higher price-earnings ratio for instance, Infosys has

historically great corporate governance that’s why it have higher P/E than its peer group.

5. Dividend Pay-out: Usually, high and constant dividend paying organization have higher

P/E ratio as it demonstrate the basic strength of the organization and firm commitment to

reward its shareholder (Carraher and Van Auken, 2013).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6. Economic Cycle: This influences those industries which have lower P/E’s and this does

not affect defensive sector.

Implementing P/E multiple to value a company:

The initial step to analysis P/E ratio is like to search those companies which operate in a

similar field in which the company intend to exist. However, this is not an easy task to search a

perfect match, but by using certain parameters it can happen, these parameters like industry,

geography, goods and services, etc.

Once the comparable organization found by the financial analyst, the further step is to

arrange the corporate earnings throughout the peer group. Earnings reflect an accounting data

which comprises non-cash items and also covers non-recurring income, this could like-wise

adversely effected by the administration in a company. Henceforth there is a strong need to

monitor at the corporate earnings and arrange accordingly.

After arranging earnings, there is need to compare various fundamental factors

throughout the peer group then P/E ratio of these companies could achieve. After calculating P/E

ratio of one company then it would be easy to measure industry price-earnings ratio by taking

average of various companies within the industry.

Final step is to compare firm’s P/E with sector average:

If a firm have higher P/E to the industry average this reflects that industry is assuming

great return over future times. On the other hands, if a firm has low P/E ratio to the industry then

it doesn’t sound undervalued always (Henderson and et. al., 2015). Instead of that market

assumes that firm is headed for trouble in forth coming time.

If the company share price has downward and trading at lowest P/E, then there is need to

investigate the finding and make appropriate action by the management.

In an organization with higher P/E ratio would need to survive according to market

expectation, by way of enhancing its earnings. Henceforth, if any company’s share is trading in

market, then there is a need to analysis this kind of company’s performance.

3

not affect defensive sector.

Implementing P/E multiple to value a company:

The initial step to analysis P/E ratio is like to search those companies which operate in a

similar field in which the company intend to exist. However, this is not an easy task to search a

perfect match, but by using certain parameters it can happen, these parameters like industry,

geography, goods and services, etc.

Once the comparable organization found by the financial analyst, the further step is to

arrange the corporate earnings throughout the peer group. Earnings reflect an accounting data

which comprises non-cash items and also covers non-recurring income, this could like-wise

adversely effected by the administration in a company. Henceforth there is a strong need to

monitor at the corporate earnings and arrange accordingly.

After arranging earnings, there is need to compare various fundamental factors

throughout the peer group then P/E ratio of these companies could achieve. After calculating P/E

ratio of one company then it would be easy to measure industry price-earnings ratio by taking

average of various companies within the industry.

Final step is to compare firm’s P/E with sector average:

If a firm have higher P/E to the industry average this reflects that industry is assuming

great return over future times. On the other hands, if a firm has low P/E ratio to the industry then

it doesn’t sound undervalued always (Henderson and et. al., 2015). Instead of that market

assumes that firm is headed for trouble in forth coming time.

If the company share price has downward and trading at lowest P/E, then there is need to

investigate the finding and make appropriate action by the management.

In an organization with higher P/E ratio would need to survive according to market

expectation, by way of enhancing its earnings. Henceforth, if any company’s share is trading in

market, then there is a need to analysis this kind of company’s performance.

3

In the given case study, AG Barr plc. and Britvic plc. operate in beverages and non-

alcoholic industry and AG Barr plc. have 20.4 P/E ratios which is more than the Britvic plc. This

means that AG Barr plc. investors anticipates higher growth rate in nearer future. While on the

other hand Britvic plc. Have 17.8 P/E ratios which reflect the company is under performing to its

rival.

The difference between Britvic plc. and AG Barr plc. is 2.6. which is occurred due to

profit. Which reflects the negative sign for the Britvic group plc. however there is a strong need

to have detailed investigation about the financial performance of both of the companies and the

industry as well so that they can reach to the final outcome and make some merger and

acquisition strategy as well.

There are certain tools that can be used by the financial analysts before going to draw a

valid conclusion in an effective manner. For analysing the performance of the company, there is

a need to use various key investment ratio before going to invest in the intended company.

Various investment ratios are earning per share, dividend yield, debt to equity ratio and others.

However this is rightly said that the ratio analysis is the most important tool for

investment decisions. This is not only assist in measuring how the firm is performing but also

this is also makes convenient for the investors as well for comparing organisations in the similar

industry. Some of the ratios are mentioned hereunder:

Price to book value: This is the ratio which is used to compare a firm’s market price to

its book value. Company book value is the amount which would stay if the firm

liquidates its assets and repays all its liabilities. Price of book value shares of the

organisations with huge tangible assets on their balance sheets (Zadek, Evans and Pruzan,

2013). If a P/BV ratio is less than one which indicates that the stock is undervalued i.e.

value of the assets on the company’s books is more than the value the market is assigning

to the company. It shows that a company’s fundamental value and is very useful to give

value to those assets of the company which are usually liquid in form. For example,

banks and financial institutions.

Debt-Equity Ratio: This ratio indicates that how much a company is leveraged i.e., in a

business of a company how much debt is involved and also tells promoters’ capital

(equity) involvement in a business. In other words, it can be said that this ratio indicates

the relative proportion of entity’s equity and debt used to finance an entity’s assets. This

4

alcoholic industry and AG Barr plc. have 20.4 P/E ratios which is more than the Britvic plc. This

means that AG Barr plc. investors anticipates higher growth rate in nearer future. While on the

other hand Britvic plc. Have 17.8 P/E ratios which reflect the company is under performing to its

rival.

The difference between Britvic plc. and AG Barr plc. is 2.6. which is occurred due to

profit. Which reflects the negative sign for the Britvic group plc. however there is a strong need

to have detailed investigation about the financial performance of both of the companies and the

industry as well so that they can reach to the final outcome and make some merger and

acquisition strategy as well.

There are certain tools that can be used by the financial analysts before going to draw a

valid conclusion in an effective manner. For analysing the performance of the company, there is

a need to use various key investment ratio before going to invest in the intended company.

Various investment ratios are earning per share, dividend yield, debt to equity ratio and others.

However this is rightly said that the ratio analysis is the most important tool for

investment decisions. This is not only assist in measuring how the firm is performing but also

this is also makes convenient for the investors as well for comparing organisations in the similar

industry. Some of the ratios are mentioned hereunder:

Price to book value: This is the ratio which is used to compare a firm’s market price to

its book value. Company book value is the amount which would stay if the firm

liquidates its assets and repays all its liabilities. Price of book value shares of the

organisations with huge tangible assets on their balance sheets (Zadek, Evans and Pruzan,

2013). If a P/BV ratio is less than one which indicates that the stock is undervalued i.e.

value of the assets on the company’s books is more than the value the market is assigning

to the company. It shows that a company’s fundamental value and is very useful to give

value to those assets of the company which are usually liquid in form. For example,

banks and financial institutions.

Debt-Equity Ratio: This ratio indicates that how much a company is leveraged i.e., in a

business of a company how much debt is involved and also tells promoters’ capital

(equity) involvement in a business. In other words, it can be said that this ratio indicates

the relative proportion of entity’s equity and debt used to finance an entity’s assets. This

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ratio is the key financial ratio for the company and is also used to judge the standard of a

company’s financial positioning (Taipaleenmäki and Ikäheimo, 2013). It is also measure

of an organization ability to repay its liability. When measuring the health of a company,

it is important to pay attention to the debt-equity ratio. If the ratio is moving upward, the

company is being financed by creditors rather than from its own financial sources which

may be more dangerous. Lenders and investors usually prefer low debt-equity ratio

because their interests are better and well protected in the event of a business of the

company in a decline stage. Thus, a company which have high debt-equity ratios may not

be able to attract more and more investors and additional lending of capital from outside

from the investors.

Operating Profit Margin Ratio:This ratio shows that how much a profit a company

makes after paying for variable costs of manufacturing a product like wages, raw

materials, etc. It is also expressed as a proportionate of sales and then indicates the

efficiency of a company controlling costs and expenses associated with particular

business operations which is conducted by the company. Furthermore, it is the return

achieved from the standard operations and does not included one or unique time

transactions of an organization. This term is used to show operating profit margin ratios

this include the following:

Operating margin

Operating income margin

Return on sales

Operating profit margin

It is also used to measure a company’s pricing strategy regarding their product and

service which they are provided in the competitive market and operating efficiency.

While doing analysis of a company, one must see whether its Operating Profit Margin ratio has

been rising over a period of time (DRURY, 2013). The investors should also do comparison

Operating Profit Margin ratio of other companies in the same industry.

Earnings per Share: It is an important tool for financial measure, which shows the

profitability of a company. It is calculated by dividing the company’s net income after tax

with its total number of shares outstanding. It is a tool that investors who participates in

the market use suddenly to gauge the profitability of a company before buying its shares.

5

company’s financial positioning (Taipaleenmäki and Ikäheimo, 2013). It is also measure

of an organization ability to repay its liability. When measuring the health of a company,

it is important to pay attention to the debt-equity ratio. If the ratio is moving upward, the

company is being financed by creditors rather than from its own financial sources which

may be more dangerous. Lenders and investors usually prefer low debt-equity ratio

because their interests are better and well protected in the event of a business of the

company in a decline stage. Thus, a company which have high debt-equity ratios may not

be able to attract more and more investors and additional lending of capital from outside

from the investors.

Operating Profit Margin Ratio:This ratio shows that how much a profit a company

makes after paying for variable costs of manufacturing a product like wages, raw

materials, etc. It is also expressed as a proportionate of sales and then indicates the

efficiency of a company controlling costs and expenses associated with particular

business operations which is conducted by the company. Furthermore, it is the return

achieved from the standard operations and does not included one or unique time

transactions of an organization. This term is used to show operating profit margin ratios

this include the following:

Operating margin

Operating income margin

Return on sales

Operating profit margin

It is also used to measure a company’s pricing strategy regarding their product and

service which they are provided in the competitive market and operating efficiency.

While doing analysis of a company, one must see whether its Operating Profit Margin ratio has

been rising over a period of time (DRURY, 2013). The investors should also do comparison

Operating Profit Margin ratio of other companies in the same industry.

Earnings per Share: It is an important tool for financial measure, which shows the

profitability of a company. It is calculated by dividing the company’s net income after tax

with its total number of shares outstanding. It is a tool that investors who participates in

the market use suddenly to gauge the profitability of a company before buying its shares.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The higher the earnings per share of a company, the better are its profitability. While

calculating this ratio, it is advisable to use the weighted ratio, as the number of shares

outstanding can change over a period of time.

It is calculated in two ways:

1. Net income after tax/total number of outstanding shares.

2. Weighted earnings per share: net income after tax-total dividends/total number of

outstanding shares.

For investors who are primarily interested in steady source of income, the EPS ratio can

tell him that a company has increasing its existing dividend. This ratio is important and crucial

tools for investors, it should not be looked at in isolation. Earnings per share of a company

should always be considered in relation to other companies in order to make a more informed

and prudent investment decision.

Investors can use the dividend yield formula to help analyse their return on investment in stocks.

Dividend Yield Ratio: Dividend yield ratio is the financial ratio that measures the

quantum of dividend paid out to the shareholders relative to the market value per share. It

calculated by dividing per share and multiplying the result by 100. A company which

have higher dividend yield pays a substantial share of its profits in the form of dividends.

Dividend yield of a company is always compared with the average of the industry to

which the company belonged (Brigham and Houston, 2012).

Companies which distribute their profits as dividend to their shareholders, while retaining

the remaining portion to reinvest in the business. Dividends are paid out to the shareholders of a

company.

Companies with high dividend yield normally do not keep a substantial portion of profits

as retained earnings.

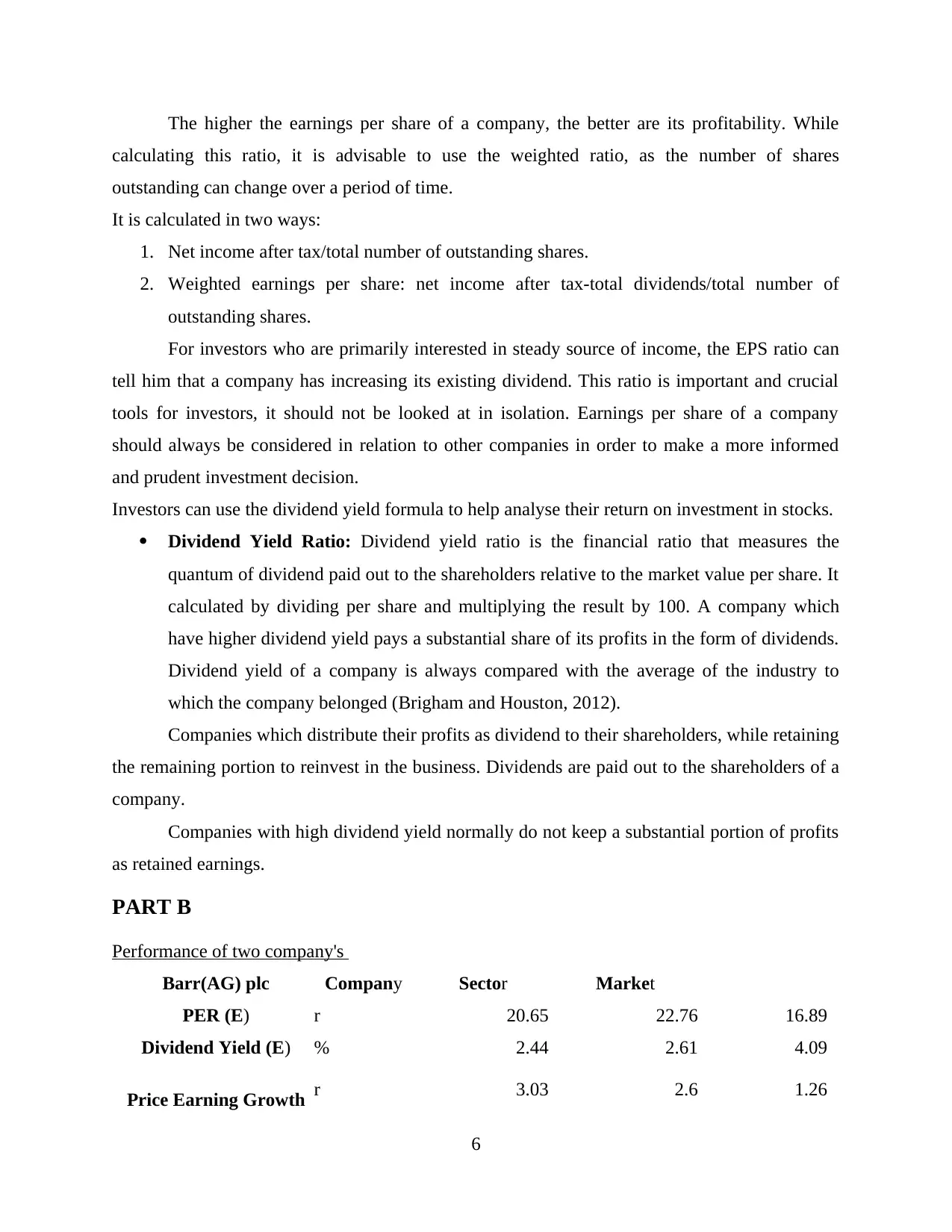

PART B

Performance of two company's

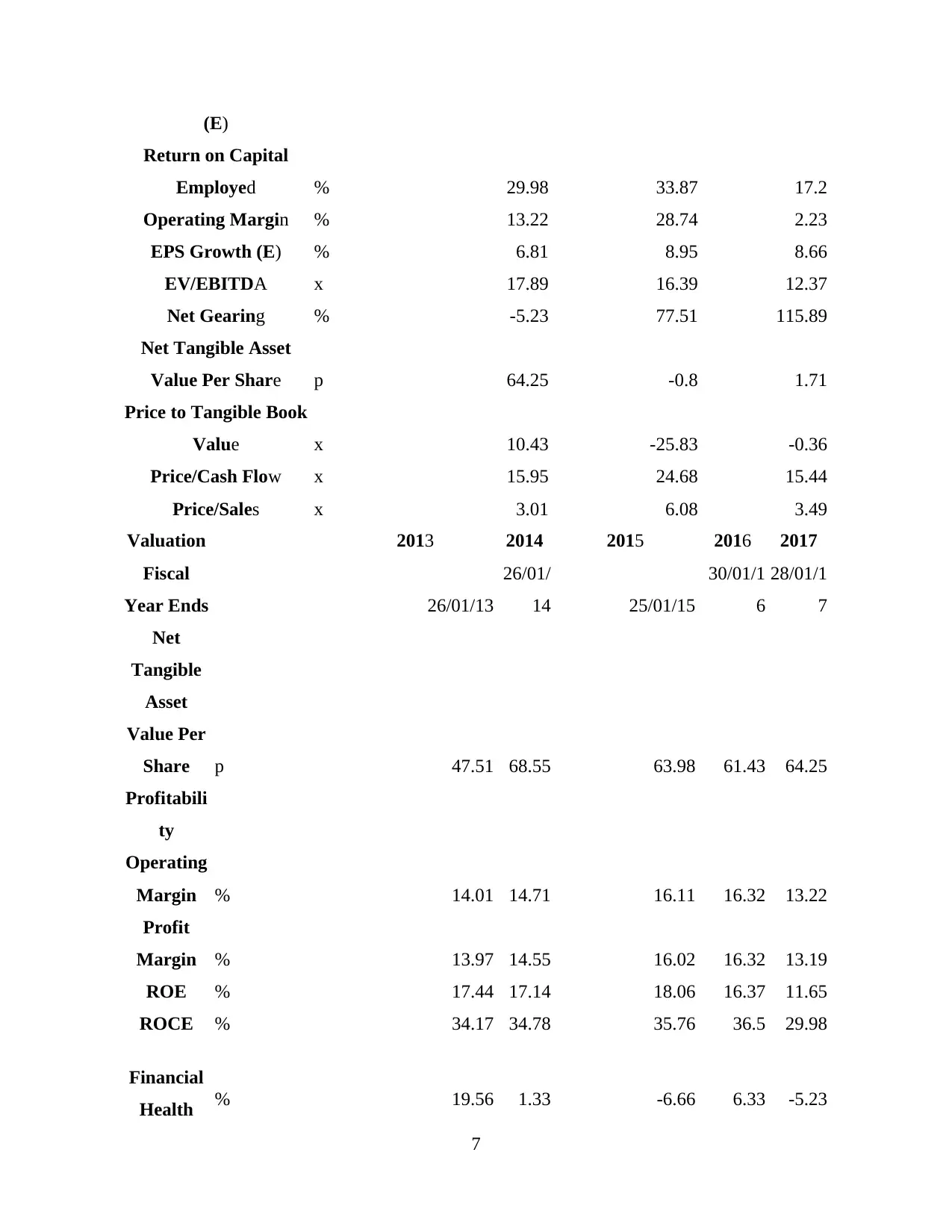

Barr(AG) plc Company Sector Market

PER (E) r 20.65 22.76 16.89

Dividend Yield (E) % 2.44 2.61 4.09

Price Earning Growth r 3.03 2.6 1.26

6

calculating this ratio, it is advisable to use the weighted ratio, as the number of shares

outstanding can change over a period of time.

It is calculated in two ways:

1. Net income after tax/total number of outstanding shares.

2. Weighted earnings per share: net income after tax-total dividends/total number of

outstanding shares.

For investors who are primarily interested in steady source of income, the EPS ratio can

tell him that a company has increasing its existing dividend. This ratio is important and crucial

tools for investors, it should not be looked at in isolation. Earnings per share of a company

should always be considered in relation to other companies in order to make a more informed

and prudent investment decision.

Investors can use the dividend yield formula to help analyse their return on investment in stocks.

Dividend Yield Ratio: Dividend yield ratio is the financial ratio that measures the

quantum of dividend paid out to the shareholders relative to the market value per share. It

calculated by dividing per share and multiplying the result by 100. A company which

have higher dividend yield pays a substantial share of its profits in the form of dividends.

Dividend yield of a company is always compared with the average of the industry to

which the company belonged (Brigham and Houston, 2012).

Companies which distribute their profits as dividend to their shareholders, while retaining

the remaining portion to reinvest in the business. Dividends are paid out to the shareholders of a

company.

Companies with high dividend yield normally do not keep a substantial portion of profits

as retained earnings.

PART B

Performance of two company's

Barr(AG) plc Company Sector Market

PER (E) r 20.65 22.76 16.89

Dividend Yield (E) % 2.44 2.61 4.09

Price Earning Growth r 3.03 2.6 1.26

6

(E)

Return on Capital

Employed % 29.98 33.87 17.2

Operating Margin % 13.22 28.74 2.23

EPS Growth (E) % 6.81 8.95 8.66

EV/EBITDA x 17.89 16.39 12.37

Net Gearing % -5.23 77.51 115.89

Net Tangible Asset

Value Per Share p 64.25 -0.8 1.71

Price to Tangible Book

Value x 10.43 -25.83 -0.36

Price/Cash Flow x 15.95 24.68 15.44

Price/Sales x 3.01 6.08 3.49

Valuation 2013 2014 2015 2016 2017

Fiscal

Year Ends 26/01/13

26/01/

14 25/01/15

30/01/1

6

28/01/1

7

Net

Tangible

Asset

Value Per

Share p 47.51 68.55 63.98 61.43 64.25

Profitabili

ty

Operating

Margin % 14.01 14.71 16.11 16.32 13.22

Profit

Margin % 13.97 14.55 16.02 16.32 13.19

ROE % 17.44 17.14 18.06 16.37 11.65

ROCE % 34.17 34.78 35.76 36.5 29.98

Financial

Health % 19.56 1.33 -6.66 6.33 -5.23

7

Return on Capital

Employed % 29.98 33.87 17.2

Operating Margin % 13.22 28.74 2.23

EPS Growth (E) % 6.81 8.95 8.66

EV/EBITDA x 17.89 16.39 12.37

Net Gearing % -5.23 77.51 115.89

Net Tangible Asset

Value Per Share p 64.25 -0.8 1.71

Price to Tangible Book

Value x 10.43 -25.83 -0.36

Price/Cash Flow x 15.95 24.68 15.44

Price/Sales x 3.01 6.08 3.49

Valuation 2013 2014 2015 2016 2017

Fiscal

Year Ends 26/01/13

26/01/

14 25/01/15

30/01/1

6

28/01/1

7

Net

Tangible

Asset

Value Per

Share p 47.51 68.55 63.98 61.43 64.25

Profitabili

ty

Operating

Margin % 14.01 14.71 16.11 16.32 13.22

Profit

Margin % 13.97 14.55 16.02 16.32 13.19

ROE % 17.44 17.14 18.06 16.37 11.65

ROCE % 34.17 34.78 35.76 36.5 29.98

Financial

Health % 19.56 1.33 -6.66 6.33 -5.23

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

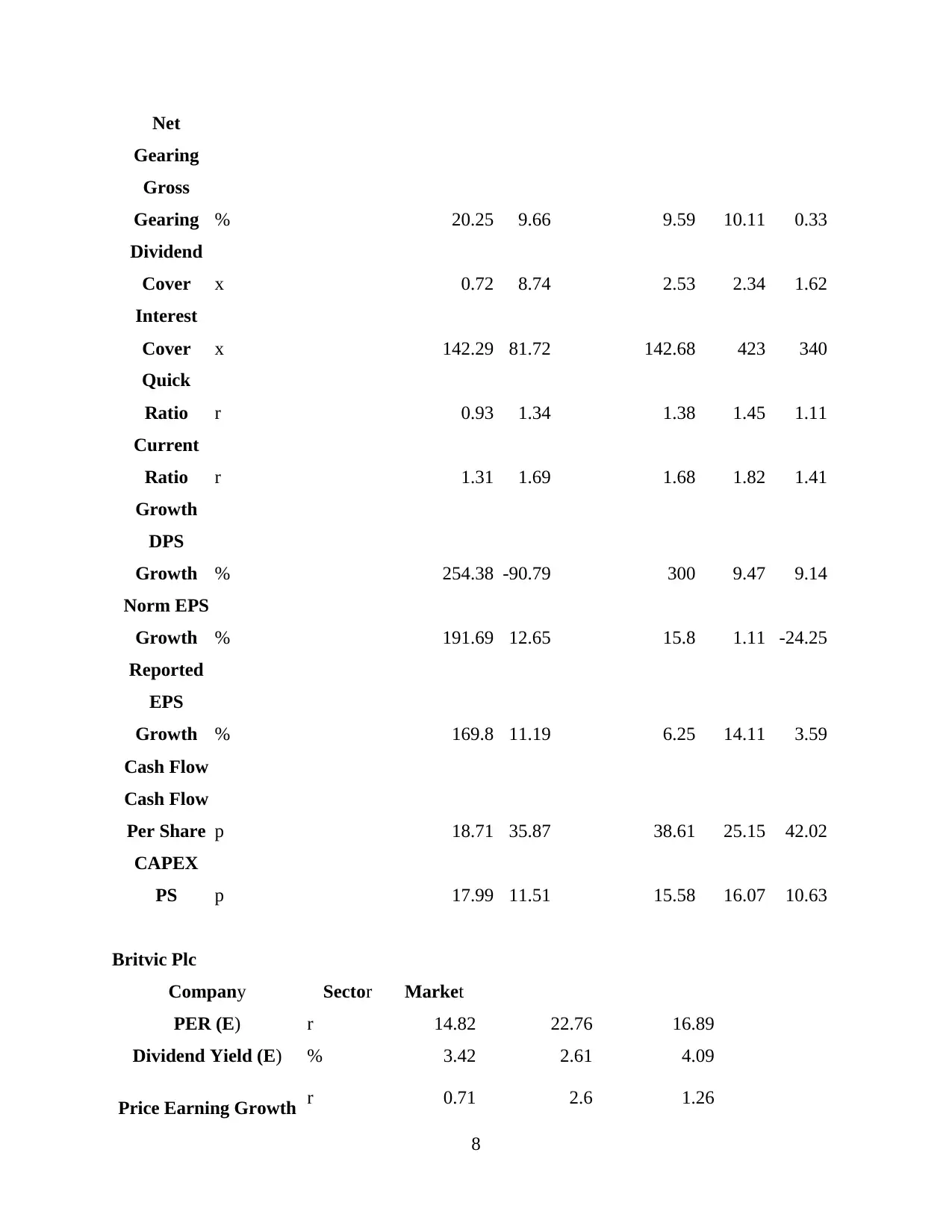

Net

Gearing

Gross

Gearing % 20.25 9.66 9.59 10.11 0.33

Dividend

Cover x 0.72 8.74 2.53 2.34 1.62

Interest

Cover x 142.29 81.72 142.68 423 340

Quick

Ratio r 0.93 1.34 1.38 1.45 1.11

Current

Ratio r 1.31 1.69 1.68 1.82 1.41

Growth

DPS

Growth % 254.38 -90.79 300 9.47 9.14

Norm EPS

Growth % 191.69 12.65 15.8 1.11 -24.25

Reported

EPS

Growth % 169.8 11.19 6.25 14.11 3.59

Cash Flow

Cash Flow

Per Share p 18.71 35.87 38.61 25.15 42.02

CAPEX

PS p 17.99 11.51 15.58 16.07 10.63

Britvic Plc

Company Sector Market

PER (E) r 14.82 22.76 16.89

Dividend Yield (E) % 3.42 2.61 4.09

Price Earning Growth r 0.71 2.6 1.26

8

Gearing

Gross

Gearing % 20.25 9.66 9.59 10.11 0.33

Dividend

Cover x 0.72 8.74 2.53 2.34 1.62

Interest

Cover x 142.29 81.72 142.68 423 340

Quick

Ratio r 0.93 1.34 1.38 1.45 1.11

Current

Ratio r 1.31 1.69 1.68 1.82 1.41

Growth

DPS

Growth % 254.38 -90.79 300 9.47 9.14

Norm EPS

Growth % 191.69 12.65 15.8 1.11 -24.25

Reported

EPS

Growth % 169.8 11.19 6.25 14.11 3.59

Cash Flow

Cash Flow

Per Share p 18.71 35.87 38.61 25.15 42.02

CAPEX

PS p 17.99 11.51 15.58 16.07 10.63

Britvic Plc

Company Sector Market

PER (E) r 14.82 22.76 16.89

Dividend Yield (E) % 3.42 2.61 4.09

Price Earning Growth r 0.71 2.6 1.26

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

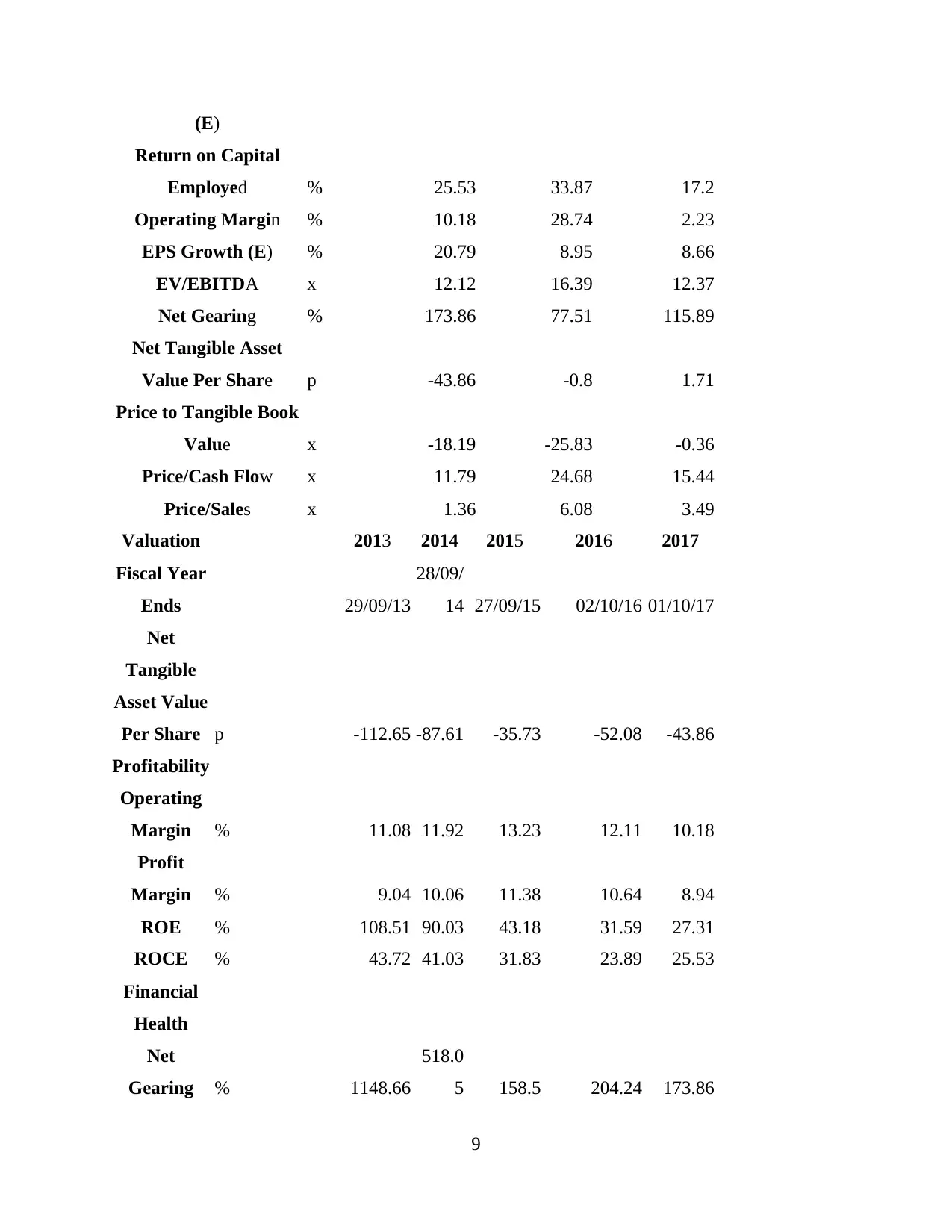

(E)

Return on Capital

Employed % 25.53 33.87 17.2

Operating Margin % 10.18 28.74 2.23

EPS Growth (E) % 20.79 8.95 8.66

EV/EBITDA x 12.12 16.39 12.37

Net Gearing % 173.86 77.51 115.89

Net Tangible Asset

Value Per Share p -43.86 -0.8 1.71

Price to Tangible Book

Value x -18.19 -25.83 -0.36

Price/Cash Flow x 11.79 24.68 15.44

Price/Sales x 1.36 6.08 3.49

Valuation 2013 2014 2015 2016 2017

Fiscal Year

Ends 29/09/13

28/09/

14 27/09/15 02/10/16 01/10/17

Net

Tangible

Asset Value

Per Share p -112.65 -87.61 -35.73 -52.08 -43.86

Profitability

Operating

Margin % 11.08 11.92 13.23 12.11 10.18

Profit

Margin % 9.04 10.06 11.38 10.64 8.94

ROE % 108.51 90.03 43.18 31.59 27.31

ROCE % 43.72 41.03 31.83 23.89 25.53

Financial

Health

Net

Gearing % 1148.66

518.0

5 158.5 204.24 173.86

9

Return on Capital

Employed % 25.53 33.87 17.2

Operating Margin % 10.18 28.74 2.23

EPS Growth (E) % 20.79 8.95 8.66

EV/EBITDA x 12.12 16.39 12.37

Net Gearing % 173.86 77.51 115.89

Net Tangible Asset

Value Per Share p -43.86 -0.8 1.71

Price to Tangible Book

Value x -18.19 -25.83 -0.36

Price/Cash Flow x 11.79 24.68 15.44

Price/Sales x 1.36 6.08 3.49

Valuation 2013 2014 2015 2016 2017

Fiscal Year

Ends 29/09/13

28/09/

14 27/09/15 02/10/16 01/10/17

Net

Tangible

Asset Value

Per Share p -112.65 -87.61 -35.73 -52.08 -43.86

Profitability

Operating

Margin % 11.08 11.92 13.23 12.11 10.18

Profit

Margin % 9.04 10.06 11.38 10.64 8.94

ROE % 108.51 90.03 43.18 31.59 27.31

ROCE % 43.72 41.03 31.83 23.89 25.53

Financial

Health

Net

Gearing % 1148.66

518.0

5 158.5 204.24 173.86

9

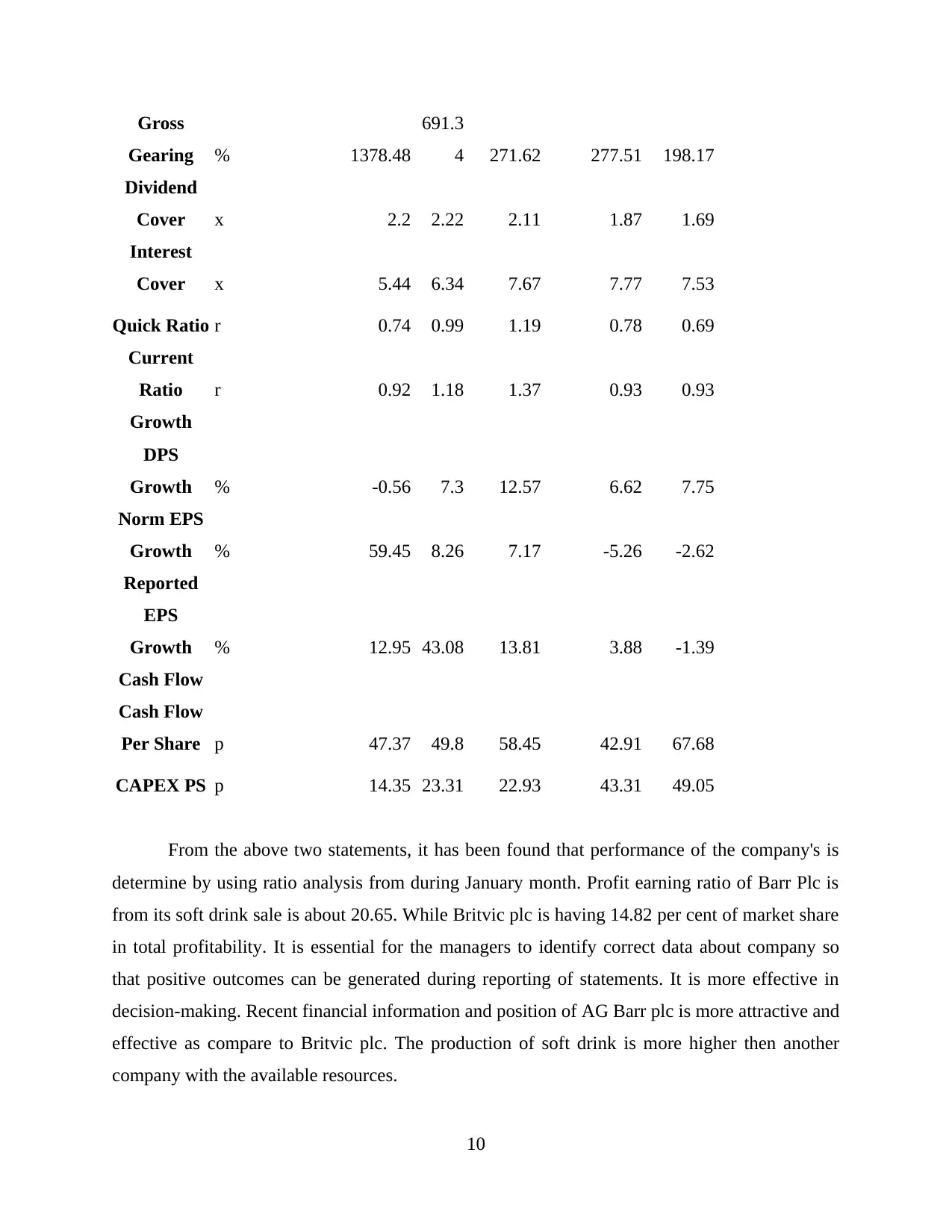

Gross

Gearing % 1378.48

691.3

4 271.62 277.51 198.17

Dividend

Cover x 2.2 2.22 2.11 1.87 1.69

Interest

Cover x 5.44 6.34 7.67 7.77 7.53

Quick Ratio r 0.74 0.99 1.19 0.78 0.69

Current

Ratio r 0.92 1.18 1.37 0.93 0.93

Growth

DPS

Growth % -0.56 7.3 12.57 6.62 7.75

Norm EPS

Growth % 59.45 8.26 7.17 -5.26 -2.62

Reported

EPS

Growth % 12.95 43.08 13.81 3.88 -1.39

Cash Flow

Cash Flow

Per Share p 47.37 49.8 58.45 42.91 67.68

CAPEX PS p 14.35 23.31 22.93 43.31 49.05

From the above two statements, it has been found that performance of the company's is

determine by using ratio analysis from during January month. Profit earning ratio of Barr Plc is

from its soft drink sale is about 20.65. While Britvic plc is having 14.82 per cent of market share

in total profitability. It is essential for the managers to identify correct data about company so

that positive outcomes can be generated during reporting of statements. It is more effective in

decision-making. Recent financial information and position of AG Barr plc is more attractive and

effective as compare to Britvic plc. The production of soft drink is more higher then another

company with the available resources.

10

Gearing % 1378.48

691.3

4 271.62 277.51 198.17

Dividend

Cover x 2.2 2.22 2.11 1.87 1.69

Interest

Cover x 5.44 6.34 7.67 7.77 7.53

Quick Ratio r 0.74 0.99 1.19 0.78 0.69

Current

Ratio r 0.92 1.18 1.37 0.93 0.93

Growth

DPS

Growth % -0.56 7.3 12.57 6.62 7.75

Norm EPS

Growth % 59.45 8.26 7.17 -5.26 -2.62

Reported

EPS

Growth % 12.95 43.08 13.81 3.88 -1.39

Cash Flow

Cash Flow

Per Share p 47.37 49.8 58.45 42.91 67.68

CAPEX PS p 14.35 23.31 22.93 43.31 49.05

From the above two statements, it has been found that performance of the company's is

determine by using ratio analysis from during January month. Profit earning ratio of Barr Plc is

from its soft drink sale is about 20.65. While Britvic plc is having 14.82 per cent of market share

in total profitability. It is essential for the managers to identify correct data about company so

that positive outcomes can be generated during reporting of statements. It is more effective in

decision-making. Recent financial information and position of AG Barr plc is more attractive and

effective as compare to Britvic plc. The production of soft drink is more higher then another

company with the available resources.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.