Accounting and Financial Reporting 1 Assignment Solution 2018

VerifiedAdded on 2023/01/16

|12

|1773

|98

Homework Assignment

AI Summary

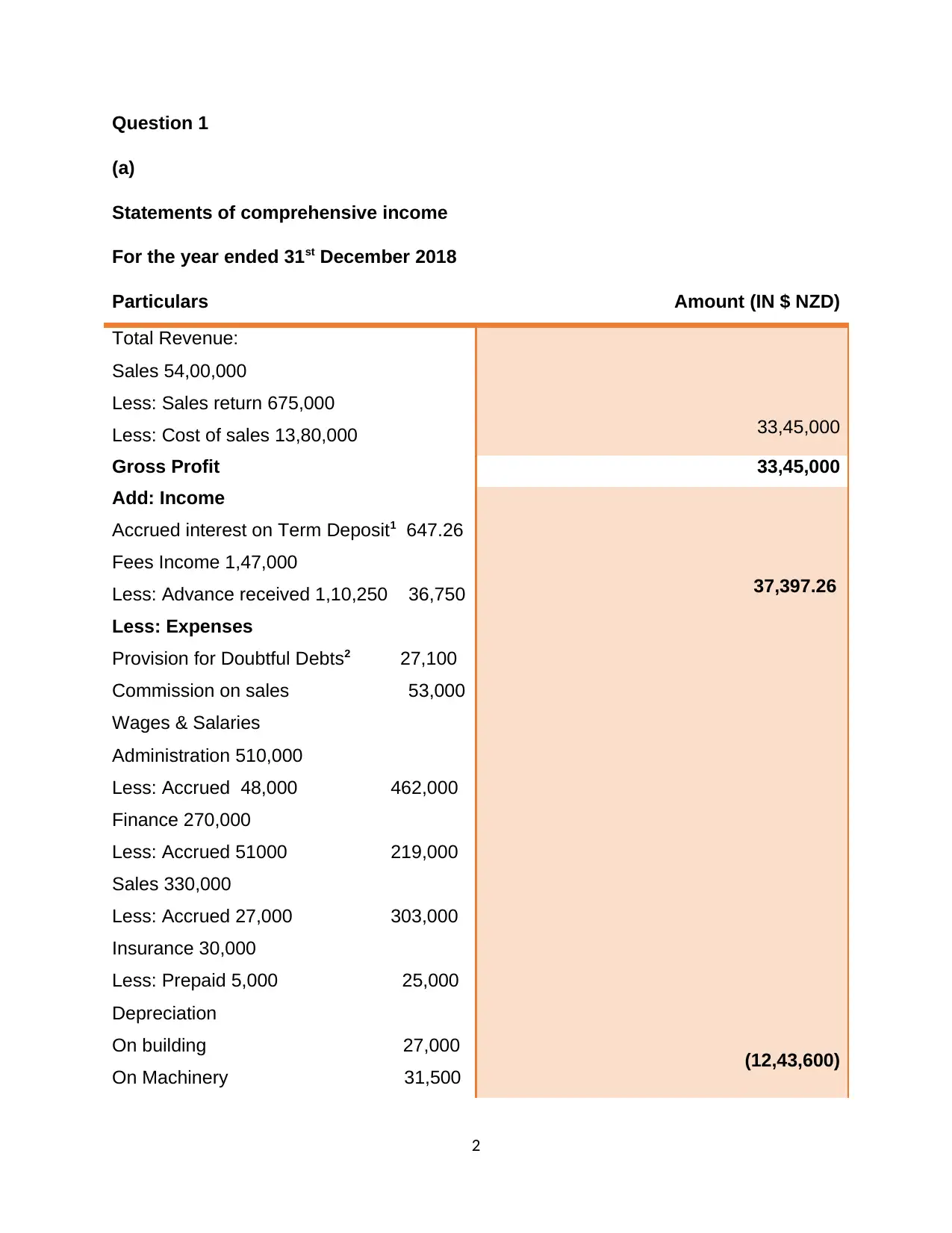

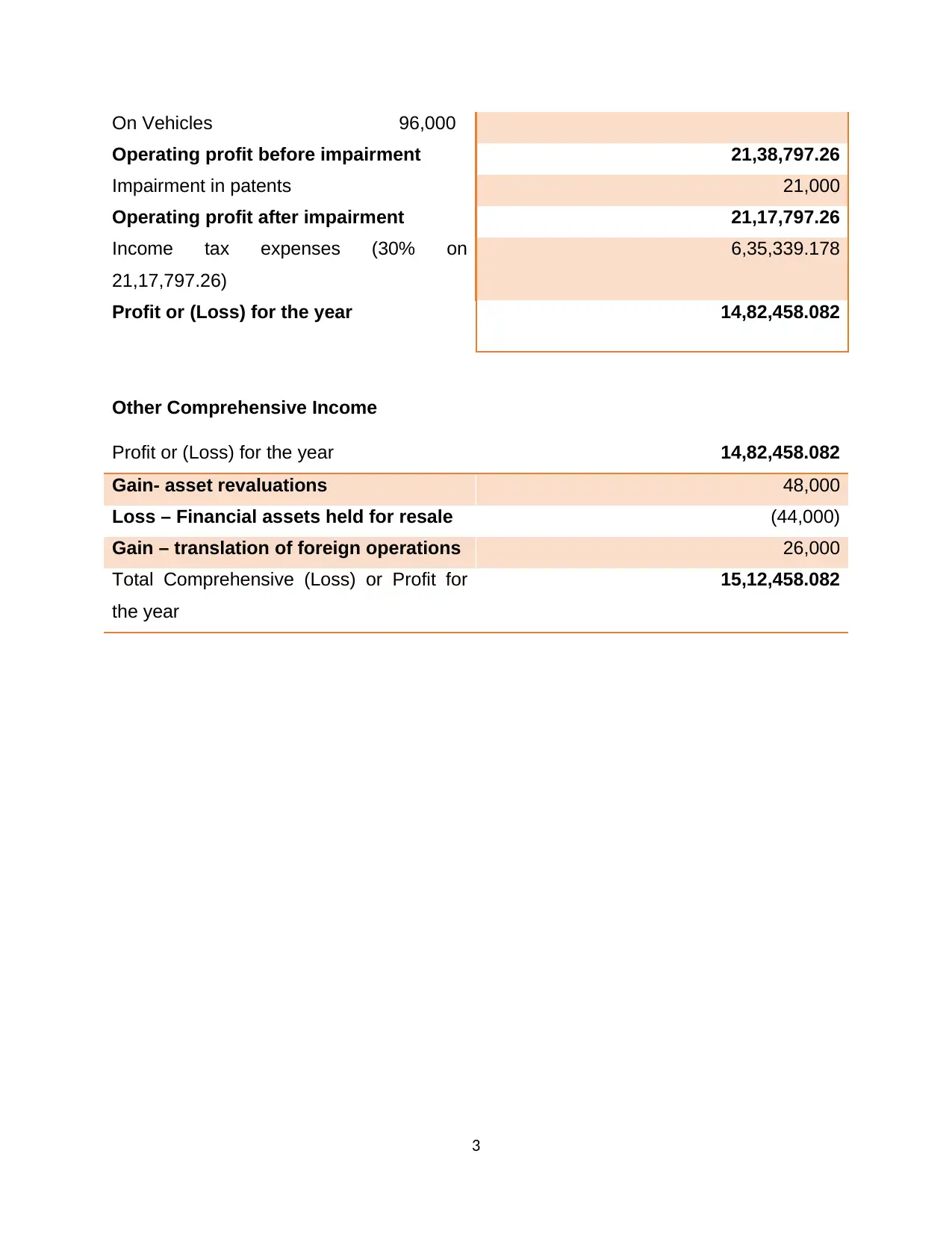

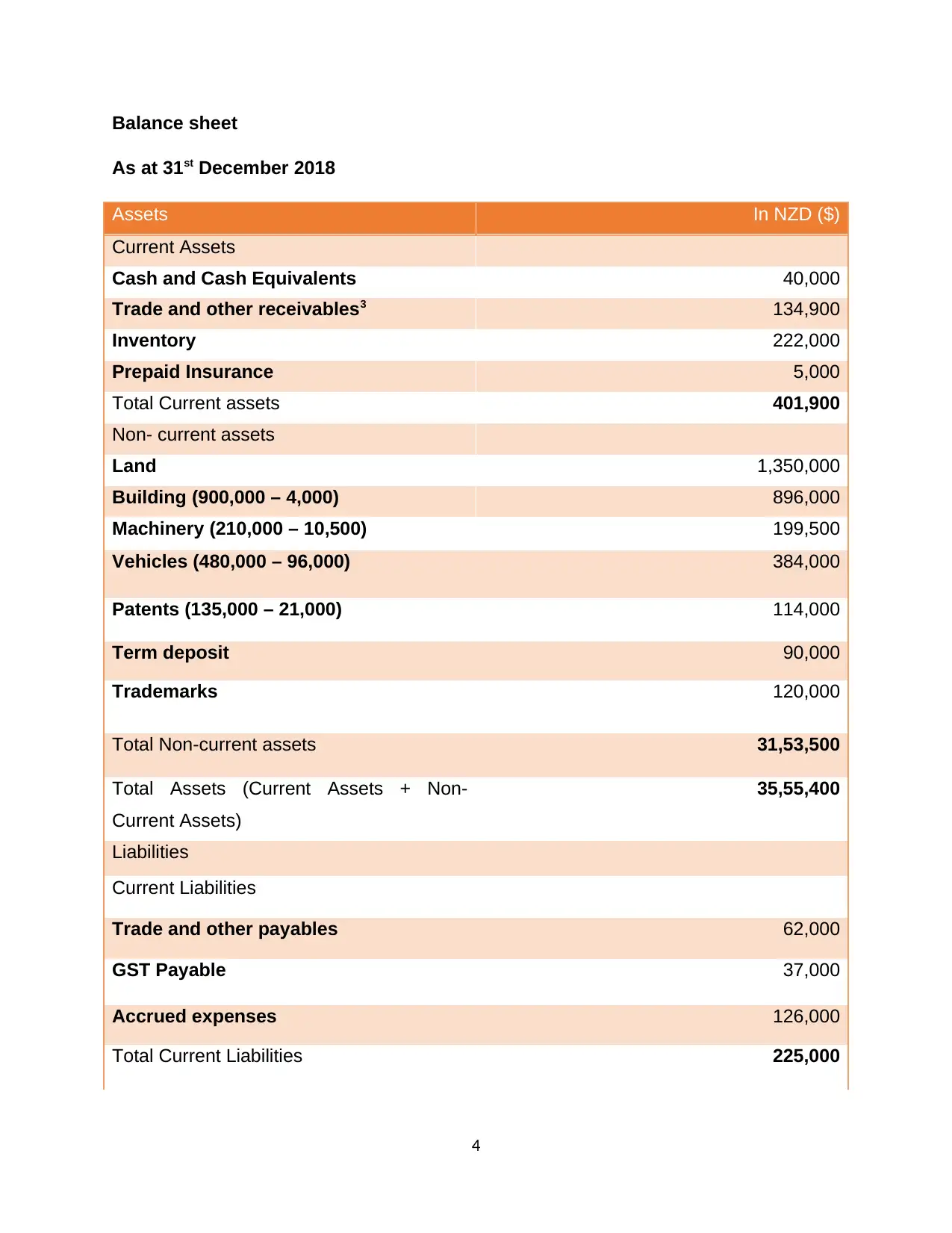

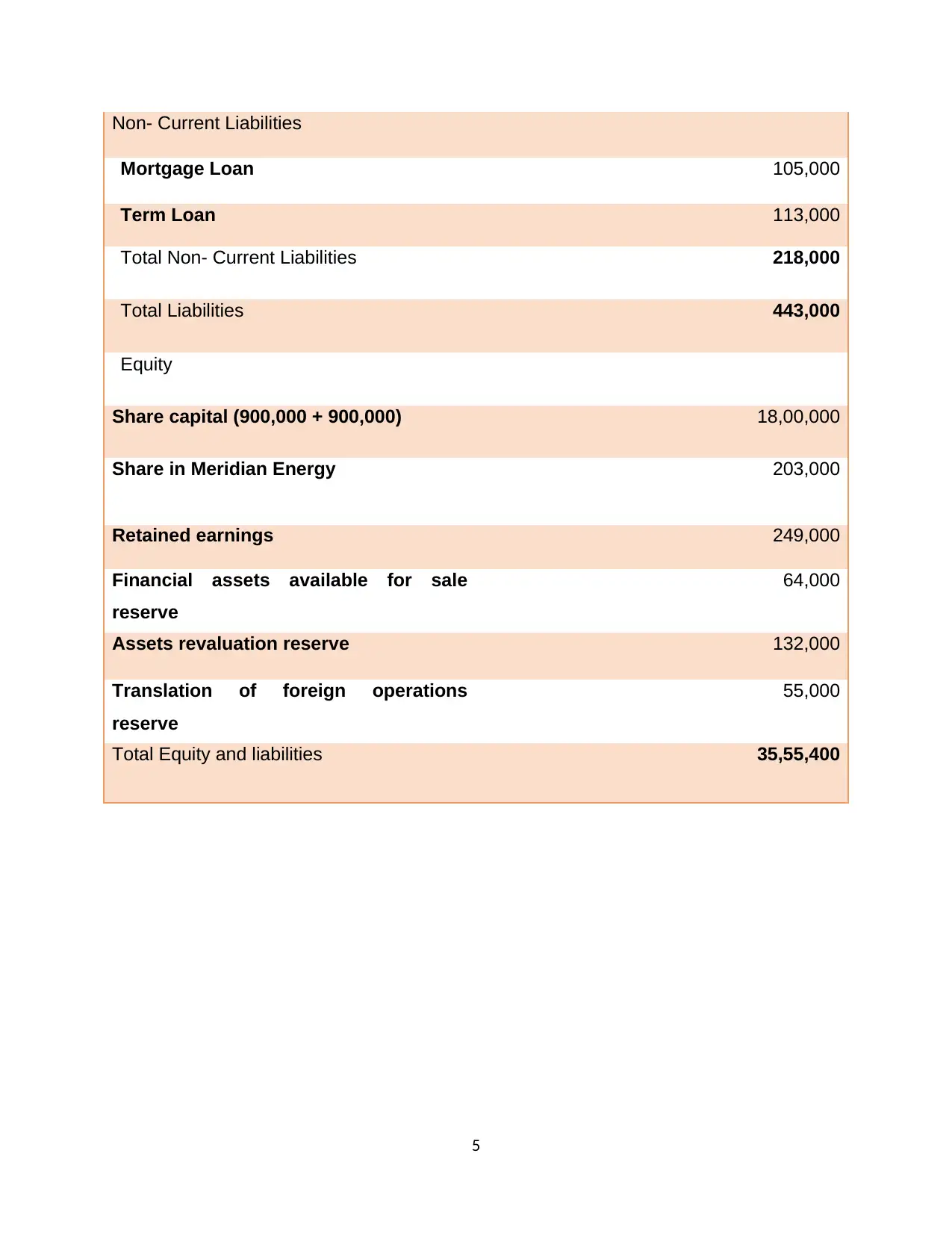

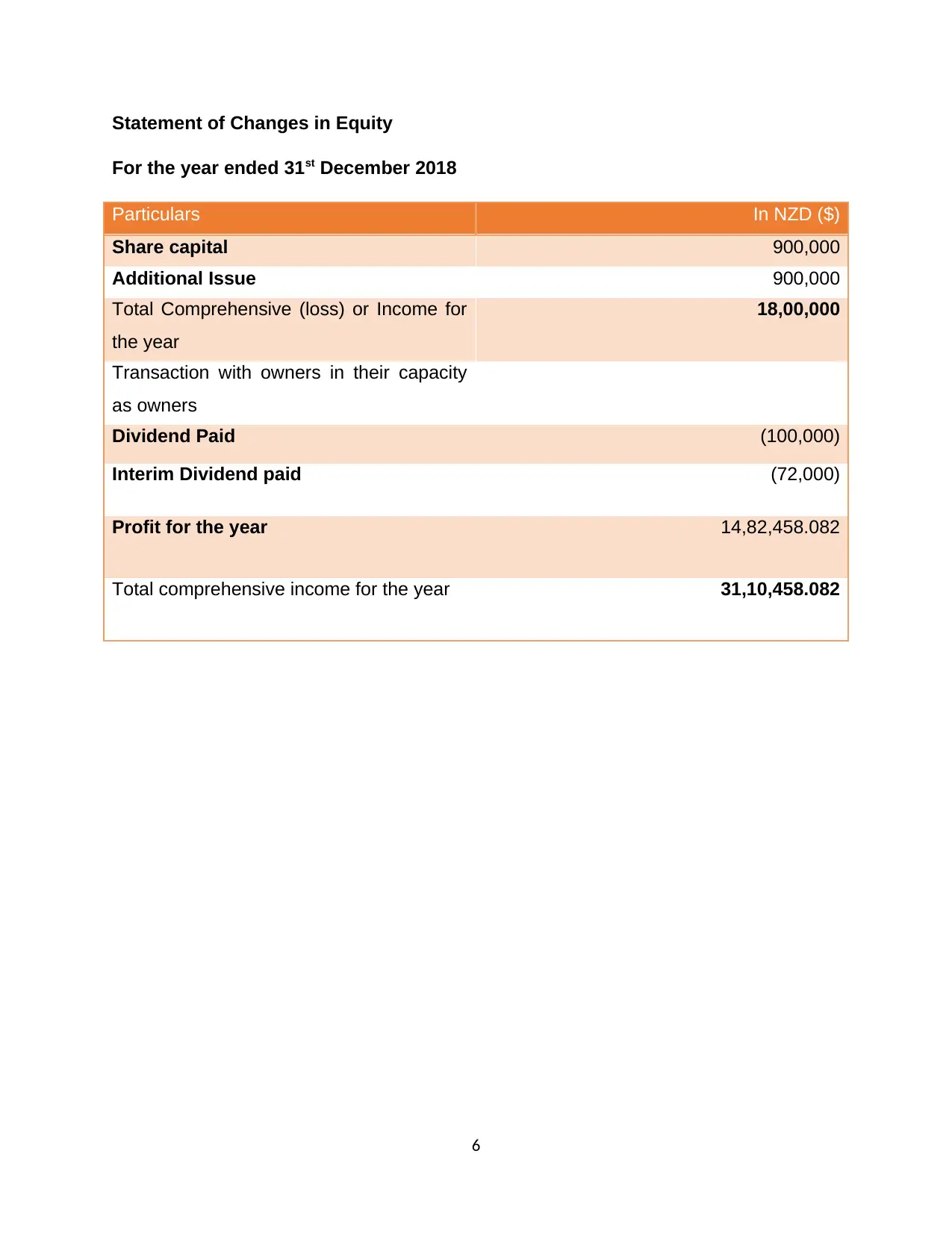

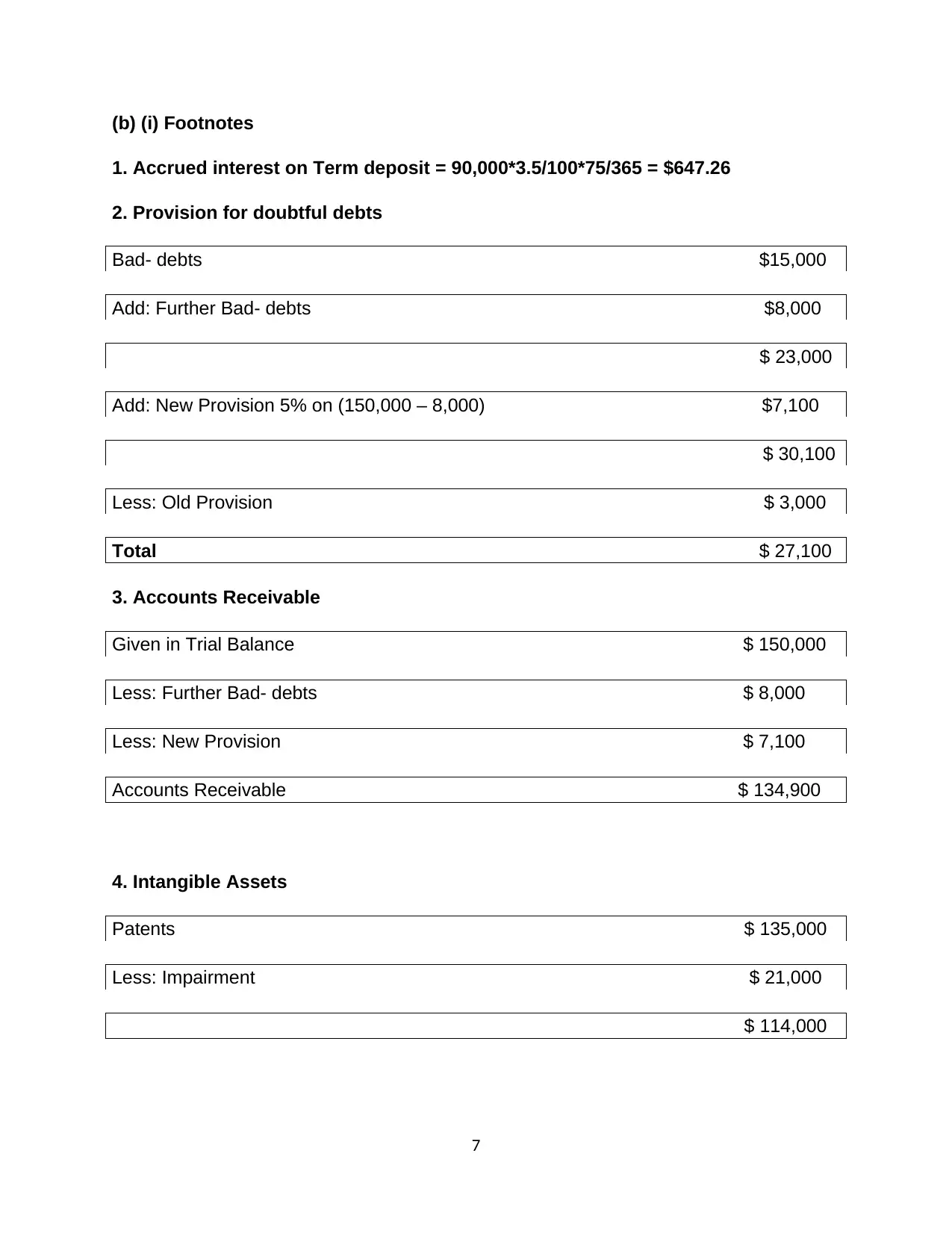

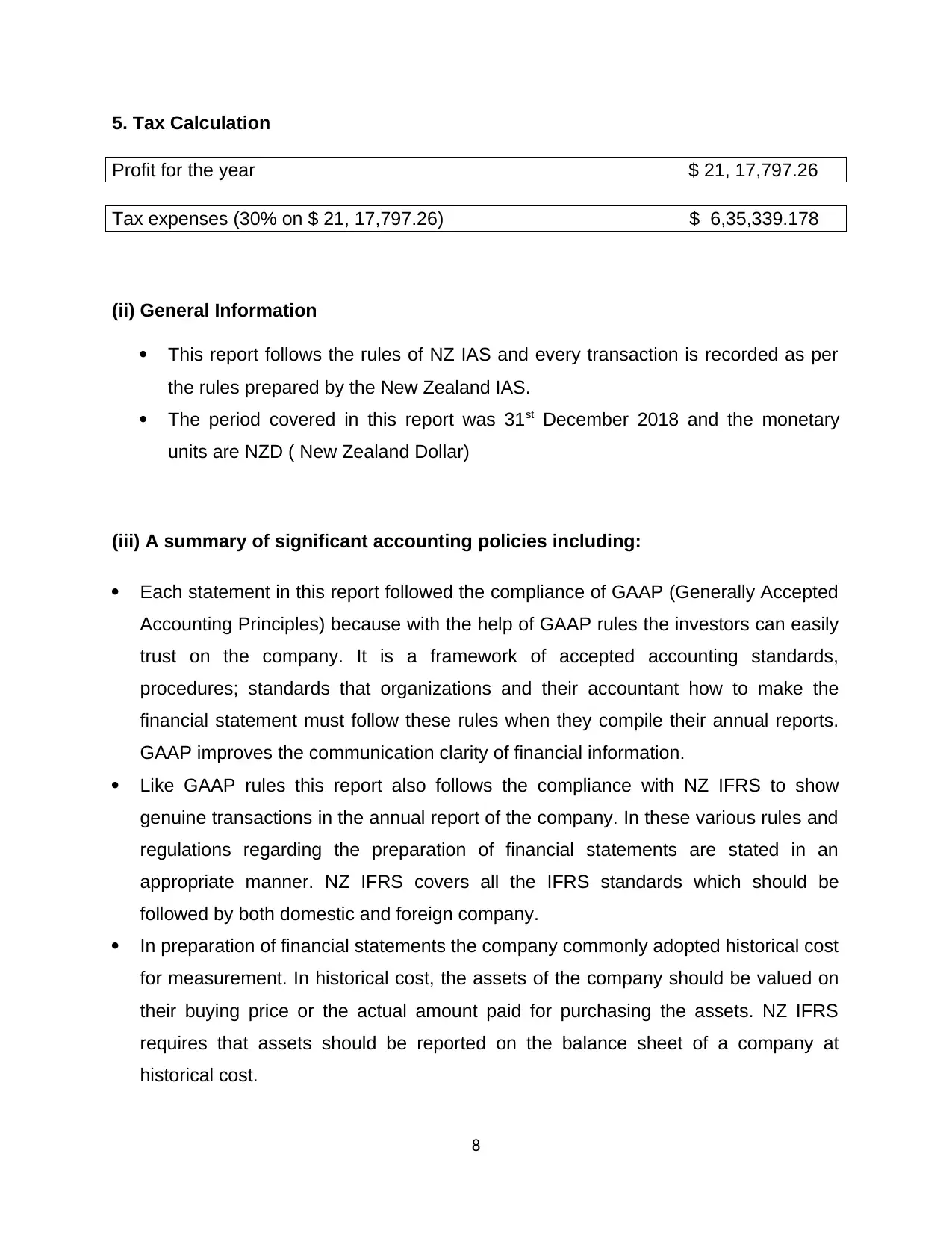

This document presents a comprehensive solution to an Accounting and Financial Reporting 1 assignment. The solution includes the preparation of a statement of comprehensive income and a balance sheet for the year ended 31st December 2018, incorporating various financial transactions and adjustments. It also involves the calculation of key financial metrics, such as gross profit, operating profit, and profit for the year. The assignment further addresses the application of IAS 10, differentiating between adjusting and non-adjusting events and their impact on financial statements. Additionally, it provides detailed footnotes explaining specific calculations and outlines significant accounting policies, including compliance with GAAP and NZ IFRS, inventory valuation methods, and property, plant, and equipment valuation and depreciation. The document concludes with a discussion of disclosures required by IAS 10.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.